Management Accounting Report: Financial Analysis of Tech UK Ltd

VerifiedAdded on 2020/07/22

|22

|5549

|89

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Tech UK Ltd, a company specializing in mobile phone chargers. It begins by differentiating between management and financial accounting, outlining their respective purposes and essential requirements, and then delves into various management accounting systems like cost accounting, performance management, and inventory management. The report explores different financial information and management accounting reports, including budgetary reports, account receivable reports, and costing reports. It emphasizes the significance of these reports in aiding effective business operations and decision-making, particularly in reducing financial issues. The report also covers the benefits of a management accounting system, including its role in cost control, performance evaluation, and strategic planning. Furthermore, the report includes an examination of costing methods, budgeting, and planning tools to address financial challenges within the company. Overall, the report serves as a valuable resource for understanding the role of management accounting in improving financial performance and operational efficiency within a business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 (A) Management accounting and essential requirements of its systems...............................1

P2) (B) Financial information.....................................................................................................4

M1) Benefits of management accounting system.......................................................................6

TASK 2............................................................................................................................................7

P3) Income statements using marginal and absorption costing methods....................................7

M2) Reconciliation of profits for financial reporting.................................................................8

TASK 3............................................................................................................................................9

P4) Budget planning and controlling tools..................................................................................9

M3) Planning tools and their usefulness for forecasting budget..............................................13

TASK 4..........................................................................................................................................14

P5) Management accounting reports reducing financial problems of Tech UK Ltd................14

M4) Significance of management accounting for reducing financial problems of Tech Ltd...15

D3) Importance of planning tools for accounting respond appropriately to solving out

financial issues..........................................................................................................................15

CONCLUSION .............................................................................................................................16

REFERENCE ................................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 (A) Management accounting and essential requirements of its systems...............................1

P2) (B) Financial information.....................................................................................................4

M1) Benefits of management accounting system.......................................................................6

TASK 2............................................................................................................................................7

P3) Income statements using marginal and absorption costing methods....................................7

M2) Reconciliation of profits for financial reporting.................................................................8

TASK 3............................................................................................................................................9

P4) Budget planning and controlling tools..................................................................................9

M3) Planning tools and their usefulness for forecasting budget..............................................13

TASK 4..........................................................................................................................................14

P5) Management accounting reports reducing financial problems of Tech UK Ltd................14

M4) Significance of management accounting for reducing financial problems of Tech Ltd...15

D3) Importance of planning tools for accounting respond appropriately to solving out

financial issues..........................................................................................................................15

CONCLUSION .............................................................................................................................16

REFERENCE ................................................................................................................................17

INDEX OF TABLES

Table 1: Comparison between management and financial accounting............................................2

Table 2: Income statement using marginal costing..........................................................................7

Table 3: Income statement using absorption costing.......................................................................8

Table 4: Reconciliation of profit......................................................................................................8

Table 1: Comparison between management and financial accounting............................................2

Table 2: Income statement using marginal costing..........................................................................7

Table 3: Income statement using absorption costing.......................................................................8

Table 4: Reconciliation of profit......................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ILLUSTRATION INDEX

Illustration 1: Stages for preparing budget.....................................................................................12

Illustration 1: Stages for preparing budget.....................................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is a multidisciplinary approach used for managing business

operations and increasing effectiveness of any organisation. It includes planning and decision-

making tools like costing, budgeting, investment appraisal for decision making regarding

business operations. This report is based to understand significance of management accounting

for reducing financial issue of Tech (UK) Ltd., it manufactures It provides special charger for

mobile phones and other gadgets for retail outlets in the country. However, being management

accountant of the entity, reports on financial position of organisation can be presented for

decision making and further operations. Including this, difference between financial and

management accounting system as well different costing systems can be described. Moreover,

management accounting reports and their usefulness in decision making process for the entity

will be introduced. Along with this, advantages and drawbacks on different kinds of budgets are

to understood. Similarly, management accounting systems for reducing financial problem of the

organisation is to be understood with the help of this assignment.

TASK 1

P1 (A) Management accounting and essential requirements of its systems

In the case scenario, it has been identified that, there is lack of fund in Tech (UK) Ltd for

its business operations. Therefore, its financial position and other business tools are identified by

which different ideas can be generated to reduce such deficiencies and improving services

(Chenhall and Moers, 2015). However, its systems' essential requirements can be described as

below with understanding comparison between financial and management accounting system:

11 Management accounting vs Financial accounting

Financial accounting deals with management of fund and decisions regarding financial

transactions of Tech Ltd. While, management accounting deals with entire business operations

including fund, inventory, performance of employees and so on. However, under financial

accounting system, decisions are made related to expenditures and revenue on business

operations by analysing financial statements like; profit and loss account, income statement,

balance sheet, cash flow and fund flow etc (Christ and Burritt, 2013). On the other hand, under

management accounting system, recording and reporting of entire business activities is done by

which appropriate decisions are made for upcoming years' so as to manage all business activities

1

Management accounting is a multidisciplinary approach used for managing business

operations and increasing effectiveness of any organisation. It includes planning and decision-

making tools like costing, budgeting, investment appraisal for decision making regarding

business operations. This report is based to understand significance of management accounting

for reducing financial issue of Tech (UK) Ltd., it manufactures It provides special charger for

mobile phones and other gadgets for retail outlets in the country. However, being management

accountant of the entity, reports on financial position of organisation can be presented for

decision making and further operations. Including this, difference between financial and

management accounting system as well different costing systems can be described. Moreover,

management accounting reports and their usefulness in decision making process for the entity

will be introduced. Along with this, advantages and drawbacks on different kinds of budgets are

to understood. Similarly, management accounting systems for reducing financial problem of the

organisation is to be understood with the help of this assignment.

TASK 1

P1 (A) Management accounting and essential requirements of its systems

In the case scenario, it has been identified that, there is lack of fund in Tech (UK) Ltd for

its business operations. Therefore, its financial position and other business tools are identified by

which different ideas can be generated to reduce such deficiencies and improving services

(Chenhall and Moers, 2015). However, its systems' essential requirements can be described as

below with understanding comparison between financial and management accounting system:

11 Management accounting vs Financial accounting

Financial accounting deals with management of fund and decisions regarding financial

transactions of Tech Ltd. While, management accounting deals with entire business operations

including fund, inventory, performance of employees and so on. However, under financial

accounting system, decisions are made related to expenditures and revenue on business

operations by analysing financial statements like; profit and loss account, income statement,

balance sheet, cash flow and fund flow etc (Christ and Burritt, 2013). On the other hand, under

management accounting system, recording and reporting of entire business activities is done by

which appropriate decisions are made for upcoming years' so as to manage all business activities

1

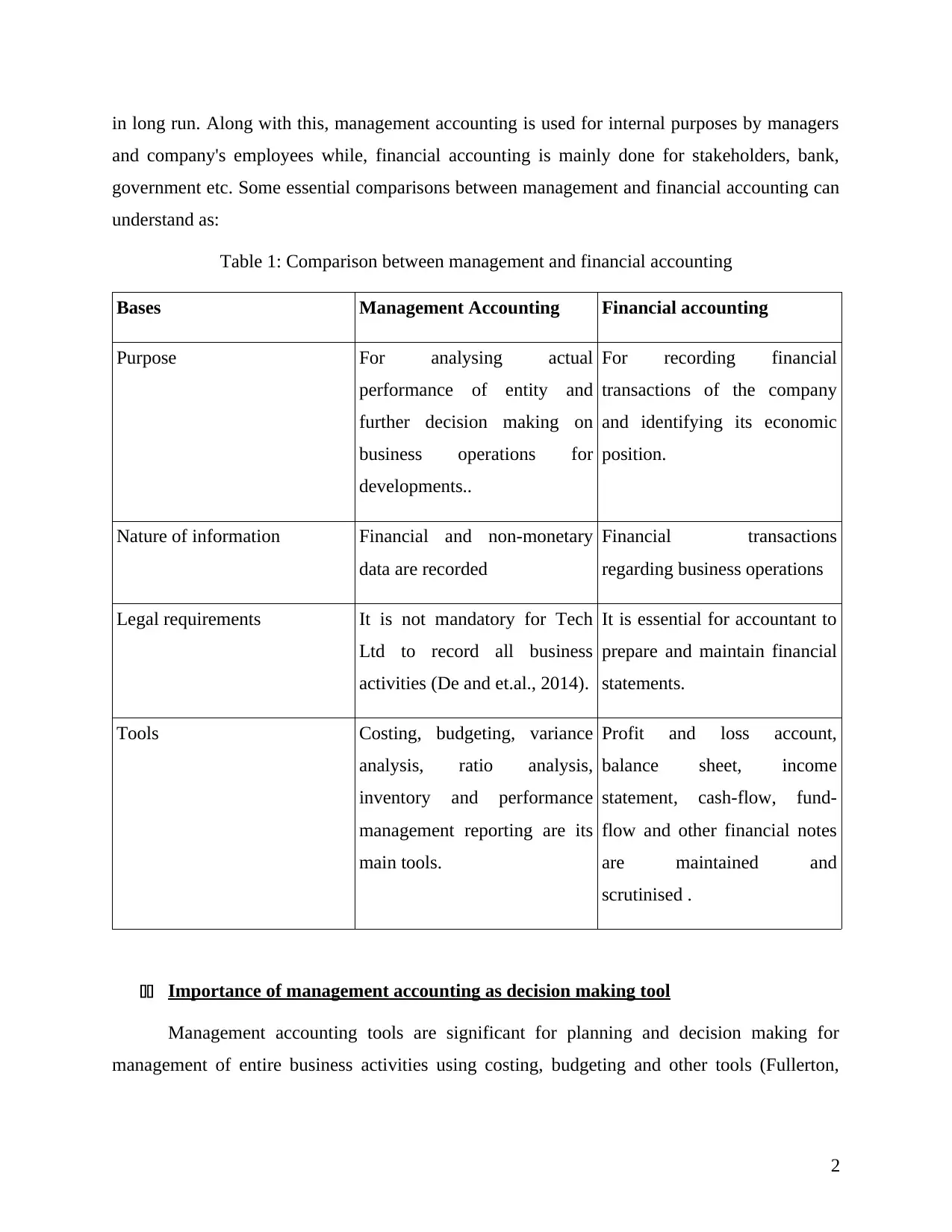

in long run. Along with this, management accounting is used for internal purposes by managers

and company's employees while, financial accounting is mainly done for stakeholders, bank,

government etc. Some essential comparisons between management and financial accounting can

understand as:

Table 1: Comparison between management and financial accounting

Bases Management Accounting Financial accounting

Purpose For analysing actual

performance of entity and

further decision making on

business operations for

developments..

For recording financial

transactions of the company

and identifying its economic

position.

Nature of information Financial and non-monetary

data are recorded

Financial transactions

regarding business operations

Legal requirements It is not mandatory for Tech

Ltd to record all business

activities (De and et.al., 2014).

It is essential for accountant to

prepare and maintain financial

statements.

Tools Costing, budgeting, variance

analysis, ratio analysis,

inventory and performance

management reporting are its

main tools.

Profit and loss account,

balance sheet, income

statement, cash-flow, fund-

flow and other financial notes

are maintained and

scrutinised .

11 Importance of management accounting as decision making tool

Management accounting tools are significant for planning and decision making for

management of entire business activities using costing, budgeting and other tools (Fullerton,

2

and company's employees while, financial accounting is mainly done for stakeholders, bank,

government etc. Some essential comparisons between management and financial accounting can

understand as:

Table 1: Comparison between management and financial accounting

Bases Management Accounting Financial accounting

Purpose For analysing actual

performance of entity and

further decision making on

business operations for

developments..

For recording financial

transactions of the company

and identifying its economic

position.

Nature of information Financial and non-monetary

data are recorded

Financial transactions

regarding business operations

Legal requirements It is not mandatory for Tech

Ltd to record all business

activities (De and et.al., 2014).

It is essential for accountant to

prepare and maintain financial

statements.

Tools Costing, budgeting, variance

analysis, ratio analysis,

inventory and performance

management reporting are its

main tools.

Profit and loss account,

balance sheet, income

statement, cash-flow, fund-

flow and other financial notes

are maintained and

scrutinised .

11 Importance of management accounting as decision making tool

Management accounting tools are significant for planning and decision making for

management of entire business activities using costing, budgeting and other tools (Fullerton,

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Kennedy and Widener, 2013). However, some essential management accounting systems and

their requirements can be understood as follows: Financial accounting system: It includes different components to identify economic

position of Tech Ltd and further decision making to reduce expenditures and increasing

sales revenue. However, accountant of the enterprise prepares and maintains financial

statements by which cost incurred on business operations is identified. Therefore,

different ideas are generated tom increase profitability of the organisation and effective

price determination for providing its services (Grabner and Moers, 2013). Cost accounting system: Under this management accounting system, cost incurred on

each financial transaction of Tech Ltd is recorded. In this process, price on

manufacturing, production and further marketing of services are determined for further

decisions. However, recording of costs incurred on purchasing materials, labour cost and

additional overhead is created by which further decisions are made for managed

production and distribution system (Heizer and Barry, 2013). Thus, cost accounting

system is beneficial for appropriate price determination and managing entire business

operations.

Performance management system: As management accounting is multidisciplinary

approach, it considers employees' performance and plans for increasing their working

efficiencies. It is linked with analysing employees' contribution in achieving effectiveness

of Tech Ltd and planning for organising training and development program is also

determined through this approach (Hope, 2016).

11 Cost accounting systems

Under cost accounting system, cost incurred on business operations is identified in terms

of actual, standard and normal costing. It is recognised that actual cost is determined cost

incurred on business operations actually for purchasing raw materials, labour cost and overhead.

However, standard costing shows price which should be appropriate for business operations

(Ibrahim and Yaya, 2016). Therefore, cost accounting system is linked with production and

distribution of goods and services as well.

11 Inventory management system

3

their requirements can be understood as follows: Financial accounting system: It includes different components to identify economic

position of Tech Ltd and further decision making to reduce expenditures and increasing

sales revenue. However, accountant of the enterprise prepares and maintains financial

statements by which cost incurred on business operations is identified. Therefore,

different ideas are generated tom increase profitability of the organisation and effective

price determination for providing its services (Grabner and Moers, 2013). Cost accounting system: Under this management accounting system, cost incurred on

each financial transaction of Tech Ltd is recorded. In this process, price on

manufacturing, production and further marketing of services are determined for further

decisions. However, recording of costs incurred on purchasing materials, labour cost and

additional overhead is created by which further decisions are made for managed

production and distribution system (Heizer and Barry, 2013). Thus, cost accounting

system is beneficial for appropriate price determination and managing entire business

operations.

Performance management system: As management accounting is multidisciplinary

approach, it considers employees' performance and plans for increasing their working

efficiencies. It is linked with analysing employees' contribution in achieving effectiveness

of Tech Ltd and planning for organising training and development program is also

determined through this approach (Hope, 2016).

11 Cost accounting systems

Under cost accounting system, cost incurred on business operations is identified in terms

of actual, standard and normal costing. It is recognised that actual cost is determined cost

incurred on business operations actually for purchasing raw materials, labour cost and overhead.

However, standard costing shows price which should be appropriate for business operations

(Ibrahim and Yaya, 2016). Therefore, cost accounting system is linked with production and

distribution of goods and services as well.

11 Inventory management system

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this management accounting system, planning for managing inventory for decision-making

regarding business operations. It is useful for reducing wastages and utilizing its inventories

adequately. In this process, decisions are also made regarding placing goods and maintaining

them efficiently. Therefore, variety of ideas are generated for managing resources affect

productivity and profitability of the enterprise. Moreover, decisions are made regarding

maintaining inventories for production and distribution of goods. It is also beneficial for

reducing wastage and allocating proper resources for the business activities (Ismail and King,

2014).

For inventory management, different software is used as; operations management,

logistics, supply chain management to manage products and services efficiently. In this process,

different ideas are generated for maintenance of production, sales and stock of the enterprise.

Therefore, inventory management system is beneficial for business operations of Tech Ltd

adequately (John, Etim and Ime, 2015).

11 Job costing system

Under this management accounting system, cost to be incurred on direct material, labour and

additional overheads are identified. In this process, planning to incurred for manufacturing

process and impacts on price determination. It includes decisions regarding purchasing raw

materials, labour and cost on additional overhead is estimated. Including this, it is linked with

price determination, production and distribution system of Tech Ltd and profitability as well

(Kaplan and Atkinson, 2015). Therefore, planning is created regarding business operations and

price determination to produce charger of mobile phone. Thus, job costing method is crucial for

business operations and appropriate decision.

P2) (B) Financial information

11 Management accounting reports

Accountant of Tech Ltd prepare and maintain records of financial transactions affect further

business operations and its profitability. However, different reports are prepared to analyse actual

performance of the enterprise and decision making regarding business activities (Novas, Alves

and Sousas, 2016). Reports are prepared as; budgeting, price optimization and different other

reports which are used for identifying actual business performance and further decision-making

4

regarding business operations. It is useful for reducing wastages and utilizing its inventories

adequately. In this process, decisions are also made regarding placing goods and maintaining

them efficiently. Therefore, variety of ideas are generated for managing resources affect

productivity and profitability of the enterprise. Moreover, decisions are made regarding

maintaining inventories for production and distribution of goods. It is also beneficial for

reducing wastage and allocating proper resources for the business activities (Ismail and King,

2014).

For inventory management, different software is used as; operations management,

logistics, supply chain management to manage products and services efficiently. In this process,

different ideas are generated for maintenance of production, sales and stock of the enterprise.

Therefore, inventory management system is beneficial for business operations of Tech Ltd

adequately (John, Etim and Ime, 2015).

11 Job costing system

Under this management accounting system, cost to be incurred on direct material, labour and

additional overheads are identified. In this process, planning to incurred for manufacturing

process and impacts on price determination. It includes decisions regarding purchasing raw

materials, labour and cost on additional overhead is estimated. Including this, it is linked with

price determination, production and distribution system of Tech Ltd and profitability as well

(Kaplan and Atkinson, 2015). Therefore, planning is created regarding business operations and

price determination to produce charger of mobile phone. Thus, job costing method is crucial for

business operations and appropriate decision.

P2) (B) Financial information

11 Management accounting reports

Accountant of Tech Ltd prepare and maintain records of financial transactions affect further

business operations and its profitability. However, different reports are prepared to analyse actual

performance of the enterprise and decision making regarding business activities (Novas, Alves

and Sousas, 2016). Reports are prepared as; budgeting, price optimization and different other

reports which are used for identifying actual business performance and further decision-making

4

regarding its operations for organisation's effectiveness. Some essential reports of management

accounting can describe as: Budgetary report: This report is essential to reduce wastage of resources and fund for

production and distribution of goods. In this process, different budgetary reports are

prepared including sales, purchase, cash and capital budgets. Therefore, monetary and

non-economic performance of Tech Ltd is identified on which decisions are made for

management of entire business operations. Including this, various ideas are generated for

reducing expenses and increasing sales revenue of the organisation. Moreover, it is

beneficial for proper management of production and distribution system as well In

addition to this, budget refers as a technique of planning procedure to be followed on for

business activities and effectiveness of the enterprise at higher level (Otto and et.al.,

2013). Therefore, for entire management of business' activities, preparing budget is

significant affect improvement in quality services and making decisions regarding

exchanging goods and implementing planning for further years. Thus, control over excess

of production and wastage of resources can be managed efficiently. Account receivable report: This management accounting report is beneficial for

managing cash flow of Tech Ltd and finding out issues occurred for its cash collection. In

this report, data and accounts are recorded related to cash in hand and proper balance of

production distribution of the enterprise. Moreover, various ideas are generated for

preparing credit policy and maintaining accounts. It impacts on financial position and

non-economic performance of the entity (Quattrone and Paolo, 2016). Therefore, old

debts and credit of the organisation are recognised.

Costing reports: This report is to record cost incurred for manufacturing, production and

further process of the business organisation. It includes costing for purchasing raw

materials, labour and additional overhead costs for business activities. It is linked with

production and distribution system impact for which decisions are made regarding

business operations. In addition to this, costing for business is identified affect

profitability and management of costs. Along with this, recording of cost on transactions

is created by which management of all activities is created (Tucker, 2016). Apart from

this, costing is of different kinds as; job order, process and other methods for which price

5

accounting can describe as: Budgetary report: This report is essential to reduce wastage of resources and fund for

production and distribution of goods. In this process, different budgetary reports are

prepared including sales, purchase, cash and capital budgets. Therefore, monetary and

non-economic performance of Tech Ltd is identified on which decisions are made for

management of entire business operations. Including this, various ideas are generated for

reducing expenses and increasing sales revenue of the organisation. Moreover, it is

beneficial for proper management of production and distribution system as well In

addition to this, budget refers as a technique of planning procedure to be followed on for

business activities and effectiveness of the enterprise at higher level (Otto and et.al.,

2013). Therefore, for entire management of business' activities, preparing budget is

significant affect improvement in quality services and making decisions regarding

exchanging goods and implementing planning for further years. Thus, control over excess

of production and wastage of resources can be managed efficiently. Account receivable report: This management accounting report is beneficial for

managing cash flow of Tech Ltd and finding out issues occurred for its cash collection. In

this report, data and accounts are recorded related to cash in hand and proper balance of

production distribution of the enterprise. Moreover, various ideas are generated for

preparing credit policy and maintaining accounts. It impacts on financial position and

non-economic performance of the entity (Quattrone and Paolo, 2016). Therefore, old

debts and credit of the organisation are recognised.

Costing reports: This report is to record cost incurred for manufacturing, production and

further process of the business organisation. It includes costing for purchasing raw

materials, labour and additional overhead costs for business activities. It is linked with

production and distribution system impact for which decisions are made regarding

business operations. In addition to this, costing for business is identified affect

profitability and management of costs. Along with this, recording of cost on transactions

is created by which management of all activities is created (Tucker, 2016). Apart from

this, costing is of different kinds as; job order, process and other methods for which price

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is determined on goods and services of the enterprise. Therefore, costing method is

essential for productivity and profitability of the organisation for which different ideas

are generated to create balance between its production and distribution system.

Significance of management accounting reports

Preparing and maintaining management accounting reports are needed for effective

business operations and increasing its efficiency. However, actual performance of Tech Ltd is

identified on which decisions are made . Including this, financial and non-economic position of

the enterprise is evaluated for which planning is created to optimum utilization of resources and

fund. It impacts on organisation's effectiveness and decision making to reduce issues and

increasing efficiencies (Chenhall and Moers, 2015).

Moreover, ideas are created to control over excess and reducing wastage of resources and

fund. Similarly, it impacts on production system affect business entity and its operations.

Including this, financial transactions on business operations are determined affect productivity

and profitability for which decisions are made regarding business operations. Along with this, it

is useful for managing entire business operations and increasing its quality services (Christ and

Burritt, 2013). However, by reporting performance of workers, their potential to contribute in

achieving organisation's effectiveness is recognised. Thus, ability and working efficiencies of the

workers are identified for segmenting work among them in the future time. Along with this, it is

useful term for managing all business operations and making decisions to reduce issues and

enhancing efficiencies on larger scale. Therefore, management accounting reports are essential

for further operations and increasing profit level of the enterprise.

M1) Benefits of management accounting system

As management accounting is multidisciplinary approach and works for managing entire

business operations of Tech Ltd. In this regard, variety of ideas are generated for appropriate

decision making regarding business operations and increasing profitability. Moreover, it is able

to create balance between production and distribution system as well demand and supply.

Therefore, management accounting is effective for management of business activities and

improving entity's effectiveness.

6

essential for productivity and profitability of the organisation for which different ideas

are generated to create balance between its production and distribution system.

Significance of management accounting reports

Preparing and maintaining management accounting reports are needed for effective

business operations and increasing its efficiency. However, actual performance of Tech Ltd is

identified on which decisions are made . Including this, financial and non-economic position of

the enterprise is evaluated for which planning is created to optimum utilization of resources and

fund. It impacts on organisation's effectiveness and decision making to reduce issues and

increasing efficiencies (Chenhall and Moers, 2015).

Moreover, ideas are created to control over excess and reducing wastage of resources and

fund. Similarly, it impacts on production system affect business entity and its operations.

Including this, financial transactions on business operations are determined affect productivity

and profitability for which decisions are made regarding business operations. Along with this, it

is useful for managing entire business operations and increasing its quality services (Christ and

Burritt, 2013). However, by reporting performance of workers, their potential to contribute in

achieving organisation's effectiveness is recognised. Thus, ability and working efficiencies of the

workers are identified for segmenting work among them in the future time. Along with this, it is

useful term for managing all business operations and making decisions to reduce issues and

enhancing efficiencies on larger scale. Therefore, management accounting reports are essential

for further operations and increasing profit level of the enterprise.

M1) Benefits of management accounting system

As management accounting is multidisciplinary approach and works for managing entire

business operations of Tech Ltd. In this regard, variety of ideas are generated for appropriate

decision making regarding business operations and increasing profitability. Moreover, it is able

to create balance between production and distribution system as well demand and supply.

Therefore, management accounting is effective for management of business activities and

improving entity's effectiveness.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

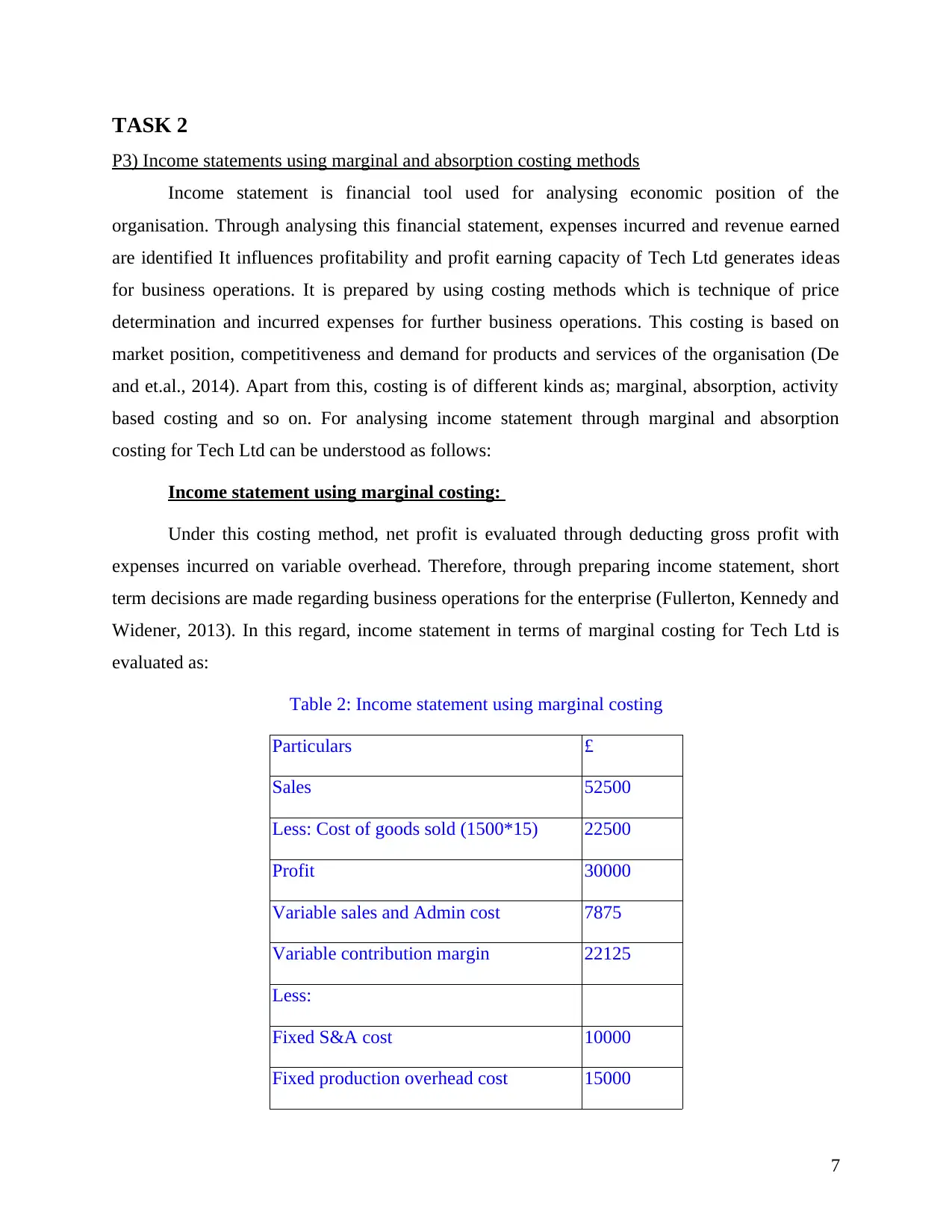

P3) Income statements using marginal and absorption costing methods

Income statement is financial tool used for analysing economic position of the

organisation. Through analysing this financial statement, expenses incurred and revenue earned

are identified It influences profitability and profit earning capacity of Tech Ltd generates ideas

for business operations. It is prepared by using costing methods which is technique of price

determination and incurred expenses for further business operations. This costing is based on

market position, competitiveness and demand for products and services of the organisation (De

and et.al., 2014). Apart from this, costing is of different kinds as; marginal, absorption, activity

based costing and so on. For analysing income statement through marginal and absorption

costing for Tech Ltd can be understood as follows:

Income statement using marginal costing:

Under this costing method, net profit is evaluated through deducting gross profit with

expenses incurred on variable overhead. Therefore, through preparing income statement, short

term decisions are made regarding business operations for the enterprise (Fullerton, Kennedy and

Widener, 2013). In this regard, income statement in terms of marginal costing for Tech Ltd is

evaluated as:

Table 2: Income statement using marginal costing

Particulars £

Sales 52500

Less: Cost of goods sold (1500*15) 22500

Profit 30000

Variable sales and Admin cost 7875

Variable contribution margin 22125

Less:

Fixed S&A cost 10000

Fixed production overhead cost 15000

7

P3) Income statements using marginal and absorption costing methods

Income statement is financial tool used for analysing economic position of the

organisation. Through analysing this financial statement, expenses incurred and revenue earned

are identified It influences profitability and profit earning capacity of Tech Ltd generates ideas

for business operations. It is prepared by using costing methods which is technique of price

determination and incurred expenses for further business operations. This costing is based on

market position, competitiveness and demand for products and services of the organisation (De

and et.al., 2014). Apart from this, costing is of different kinds as; marginal, absorption, activity

based costing and so on. For analysing income statement through marginal and absorption

costing for Tech Ltd can be understood as follows:

Income statement using marginal costing:

Under this costing method, net profit is evaluated through deducting gross profit with

expenses incurred on variable overhead. Therefore, through preparing income statement, short

term decisions are made regarding business operations for the enterprise (Fullerton, Kennedy and

Widener, 2013). In this regard, income statement in terms of marginal costing for Tech Ltd is

evaluated as:

Table 2: Income statement using marginal costing

Particulars £

Sales 52500

Less: Cost of goods sold (1500*15) 22500

Profit 30000

Variable sales and Admin cost 7875

Variable contribution margin 22125

Less:

Fixed S&A cost 10000

Fixed production overhead cost 15000

7

Net profit -2875

Interpretation: It is interpreted that Tech Ltd has incurred 22500 on direct material,

labour cost and variable production overhead on which sales revenue is gained as 52500.

Therefore, gross profit of the organisation is determined as 30000. It is quite effective and

indicates that entity can grow further. However, for evaluating net profit, this profit value is

deducted with cost incurred on variable overhead which is 25000. Therefore, net loss according

to marginal costing method is determined as (-) 2875.

Income statement using absorption costing:

Using this costing method, net income is evaluated by deducting gross profit with total

expenses incurred on fixed and variable overhead. Therefore, it is beneficial for decision making

for long time period operations (Grabner and Moers, 2013). In this regard, income statement

using absorption costing for Tech Ltd is mentioned below:

Table 3: Income statement using absorption costing

Particulars £

Fixed overhead absorbed 15000

Actual fixed production overhead 10000

Over absorbed 5000

Interpretation: it is recognised that for evaluating net profit under absorption costing,

gross profit is deducted with total cost incurred on fixed and variable overhead. However, it is

evaluated that organisation has achieved 15000 on expenditures on total overhead is 10000.

Therefore, net profit of Tech Ltd is determined as 5000 which indicates that entity can plan for

further growth in the future time.

M2) Reconciliation of profits for financial reporting

Table 4: Reconciliation of profit

8

Interpretation: It is interpreted that Tech Ltd has incurred 22500 on direct material,

labour cost and variable production overhead on which sales revenue is gained as 52500.

Therefore, gross profit of the organisation is determined as 30000. It is quite effective and

indicates that entity can grow further. However, for evaluating net profit, this profit value is

deducted with cost incurred on variable overhead which is 25000. Therefore, net loss according

to marginal costing method is determined as (-) 2875.

Income statement using absorption costing:

Using this costing method, net income is evaluated by deducting gross profit with total

expenses incurred on fixed and variable overhead. Therefore, it is beneficial for decision making

for long time period operations (Grabner and Moers, 2013). In this regard, income statement

using absorption costing for Tech Ltd is mentioned below:

Table 3: Income statement using absorption costing

Particulars £

Fixed overhead absorbed 15000

Actual fixed production overhead 10000

Over absorbed 5000

Interpretation: it is recognised that for evaluating net profit under absorption costing,

gross profit is deducted with total cost incurred on fixed and variable overhead. However, it is

evaluated that organisation has achieved 15000 on expenditures on total overhead is 10000.

Therefore, net profit of Tech Ltd is determined as 5000 which indicates that entity can plan for

further growth in the future time.

M2) Reconciliation of profits for financial reporting

Table 4: Reconciliation of profit

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.