Detailed Management Accounting Report: Zylla Company, UK Operations

VerifiedAdded on 2020/06/04

|17

|5266

|38

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Zylla Company, a UK-based business. It begins with an introduction to management accounting systems, outlining their essential requirements and different types, including cost accounting, inventory management, price optimization, and job costing systems. The report then delves into various types of management accounting reporting, such as budget reports, accounts receivable aging reports, job costs reports, inventory reports, income statement reports, and cash flow reports, highlighting their significance. The core of the report focuses on analyzing costs and profits using marginal and absorption costing techniques, providing detailed calculations and comparisons. Furthermore, it explores the advantages and disadvantages of different planning tools for budgetary control and discusses the application of management accounting systems in solving financial problems. The report concludes by summarizing the key findings and offering insights into improving Zylla Company's financial management practices, enhancing its operational efficiency, and supporting its strategic decision-making processes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and essential requirement of various management

accounting types.....................................................................................................................1

P2 Types of management accounting reporting.....................................................................3

TASK 2............................................................................................................................................5

P3 Analysation of cost and profit using costing techniques...................................................5

TASK 3............................................................................................................................................8

P4 Report on advantages and disadvantages of different types of planning tools for budgetary-

control.....................................................................................................................................8

P5 Uses of management accounting system in solving financial problems. .......................12

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and essential requirement of various management

accounting types.....................................................................................................................1

P2 Types of management accounting reporting.....................................................................3

TASK 2............................................................................................................................................5

P3 Analysation of cost and profit using costing techniques...................................................5

TASK 3............................................................................................................................................8

P4 Report on advantages and disadvantages of different types of planning tools for budgetary-

control.....................................................................................................................................8

P5 Uses of management accounting system in solving financial problems. .......................12

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMAPNY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

In this present world, Globalisation and liberalisation supports many organisations in

covering more areas of operations to made a positive impact on company's business. Sometimes

globalisation brings complexity into business. Regulations and provisions has to be followed by

companies (Banerjee, 2010). Management accounting system which is a procedure of gathering

financial data's and analysis of data's. It provides various informations and data's which provides

guidelines to different departments of a company (Bennett and James, 2017). In this process

allocation of companies funds is done. Zylla, a UK small-sized company which deals in

providing multiple products is taken for the purpose of preparing this report. The

In this assignment, focus on two areas which is minimising wastage and expansion of

business has been done. Reports presented in this assignment, will concentrate on various kind

of management accounting information systems. Reporting method is also being discussed in

reports, Difference between marginal costing and absorption costing will eliminate the

confusions between two. As both types of techniques uses different methods to calculate net

profit for the company.

TASK 1

P1 Management accounting system and essential requirement of various management accounting

types

Management accounting system: It can be defined as the process of preparing documents

which contains accounting and other important information which help management in making

an effective decision and plans. As there are large number of transactions happened on daily

basis which need to be recorded to find out the outcomes received in near future.

Therefore, the management should required to prepare accounting systems such as profit &

Loss a/c, Balance sheet, cash flow statements etc. which show the true and fair financial

position of company. There are several objectives of management accounting which are briefly

1

TO,

GENERAL MANAGER

ZYLLA COMAPNY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

In this present world, Globalisation and liberalisation supports many organisations in

covering more areas of operations to made a positive impact on company's business. Sometimes

globalisation brings complexity into business. Regulations and provisions has to be followed by

companies (Banerjee, 2010). Management accounting system which is a procedure of gathering

financial data's and analysis of data's. It provides various informations and data's which provides

guidelines to different departments of a company (Bennett and James, 2017). In this process

allocation of companies funds is done. Zylla, a UK small-sized company which deals in

providing multiple products is taken for the purpose of preparing this report. The

In this assignment, focus on two areas which is minimising wastage and expansion of

business has been done. Reports presented in this assignment, will concentrate on various kind

of management accounting information systems. Reporting method is also being discussed in

reports, Difference between marginal costing and absorption costing will eliminate the

confusions between two. As both types of techniques uses different methods to calculate net

profit for the company.

TASK 1

P1 Management accounting system and essential requirement of various management accounting

types

Management accounting system: It can be defined as the process of preparing documents

which contains accounting and other important information which help management in making

an effective decision and plans. As there are large number of transactions happened on daily

basis which need to be recorded to find out the outcomes received in near future.

Therefore, the management should required to prepare accounting systems such as profit &

Loss a/c, Balance sheet, cash flow statements etc. which show the true and fair financial

position of company. There are several objectives of management accounting which are briefly

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

described as below:

Allocation of resources to different departments while making an effective plans and

policies.

Analysis of transactions happened on daily basis in order to find out financial position of

company.

Numerical interpretation of various financial statements directs management to make an

effective plans and strategies for future business activities.

Types of management accounting systems:

Cost accounting system: Such system is more helpful in controlling and monitoring cost which

is incurred in execution of future business activities. Through such system, the cost accountant

can able to allocate cost to the activities of different departments after analysing the outcomes

received in near future. This will help in reducing wastage of money and increases the chances

of utilising cost in an optimum manner.

Inventory management system: Such system is useful in determining the inventory level

available with the company in order to meet customer's needs and requirements. The main

purpose of using such system is to control inventory cost through ordering whenever the

managers feels the shortage of raw materials. The management of Zylla should required to place

an order of inventory whenever they needed. It helps in reducing cost of inventory as keeping

unwanted stock should be ignored.

Price optimisation: Such system helps in setting up the cost of products which helps in

maximising the level of satisfaction of customers. It can be done after identifying and analysing

the perception and buying behaviour of customers towards the price company charged from

them for their products. The management of Zylla should required to identify that which

amount the customers should agreed to pay for their products and accordingly setting the prices

in order to influences their purchasing decision.

Job costing system: Such system is useful for allocation of cost to manufacture specific product

or group of products. The management need to first identify the expenses which will be incurred

in producing specific products such as direct materials, direct labour etc. And accordingly took

decision regarding allocation of cost with a motive of achieve better possible outcomes in near

future.

2

Allocation of resources to different departments while making an effective plans and

policies.

Analysis of transactions happened on daily basis in order to find out financial position of

company.

Numerical interpretation of various financial statements directs management to make an

effective plans and strategies for future business activities.

Types of management accounting systems:

Cost accounting system: Such system is more helpful in controlling and monitoring cost which

is incurred in execution of future business activities. Through such system, the cost accountant

can able to allocate cost to the activities of different departments after analysing the outcomes

received in near future. This will help in reducing wastage of money and increases the chances

of utilising cost in an optimum manner.

Inventory management system: Such system is useful in determining the inventory level

available with the company in order to meet customer's needs and requirements. The main

purpose of using such system is to control inventory cost through ordering whenever the

managers feels the shortage of raw materials. The management of Zylla should required to place

an order of inventory whenever they needed. It helps in reducing cost of inventory as keeping

unwanted stock should be ignored.

Price optimisation: Such system helps in setting up the cost of products which helps in

maximising the level of satisfaction of customers. It can be done after identifying and analysing

the perception and buying behaviour of customers towards the price company charged from

them for their products. The management of Zylla should required to identify that which

amount the customers should agreed to pay for their products and accordingly setting the prices

in order to influences their purchasing decision.

Job costing system: Such system is useful for allocation of cost to manufacture specific product

or group of products. The management need to first identify the expenses which will be incurred

in producing specific products such as direct materials, direct labour etc. And accordingly took

decision regarding allocation of cost with a motive of achieve better possible outcomes in near

future.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

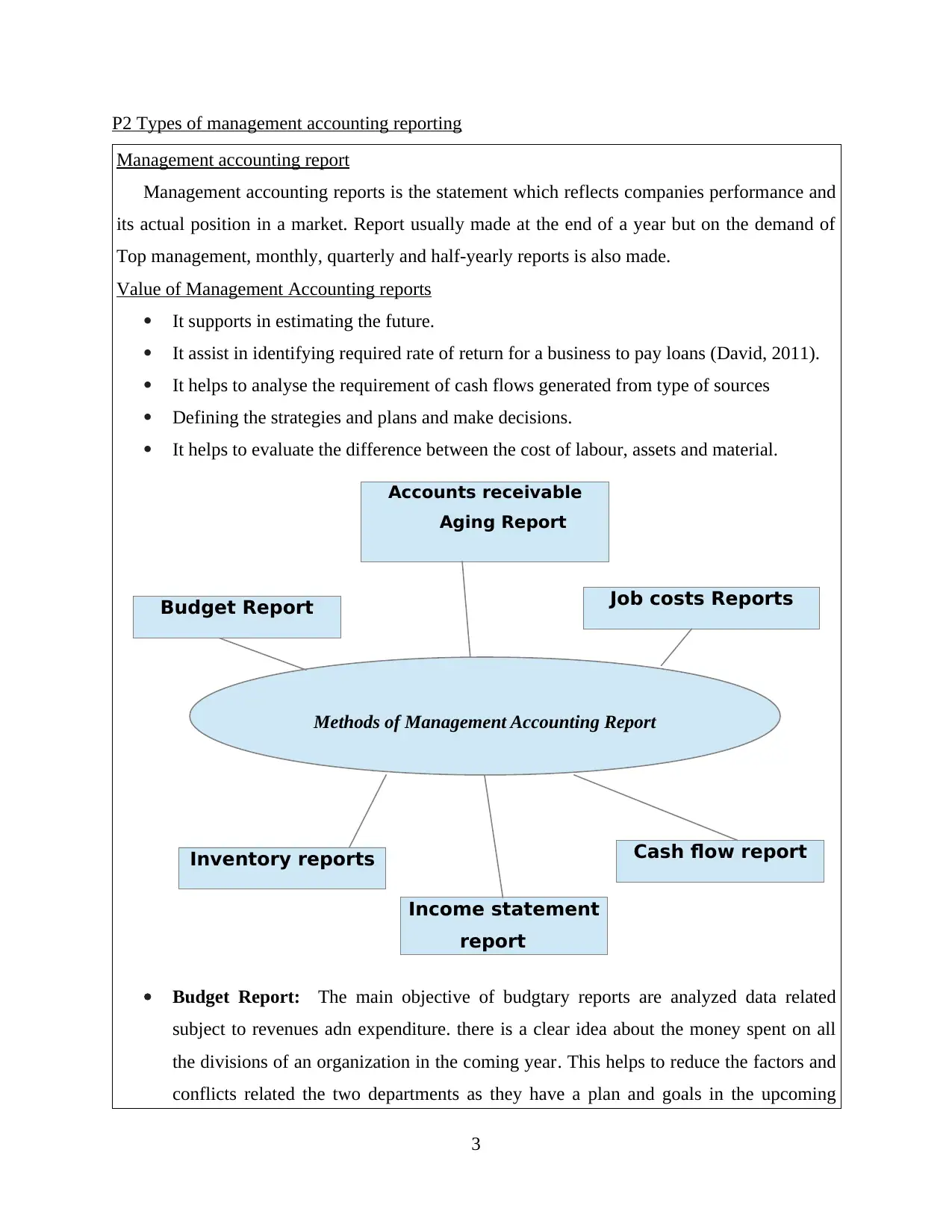

P2 Types of management accounting reporting

Management accounting report

Management accounting reports is the statement which reflects companies performance and

its actual position in a market. Report usually made at the end of a year but on the demand of

Top management, monthly, quarterly and half-yearly reports is also made.

Value of Management Accounting reports

It supports in estimating the future.

It assist in identifying required rate of return for a business to pay loans (David, 2011).

It helps to analyse the requirement of cash flows generated from type of sources

Defining the strategies and plans and make decisions.

It helps to evaluate the difference between the cost of labour, assets and material.

Budget Report: The main objective of budgtary reports are analyzed data related

subject to revenues adn expenditure. there is a clear idea about the money spent on all

the divisions of an organization in the coming year. This helps to reduce the factors and

conflicts related the two departments as they have a plan and goals in the upcoming

3

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

Management accounting report

Management accounting reports is the statement which reflects companies performance and

its actual position in a market. Report usually made at the end of a year but on the demand of

Top management, monthly, quarterly and half-yearly reports is also made.

Value of Management Accounting reports

It supports in estimating the future.

It assist in identifying required rate of return for a business to pay loans (David, 2011).

It helps to analyse the requirement of cash flows generated from type of sources

Defining the strategies and plans and make decisions.

It helps to evaluate the difference between the cost of labour, assets and material.

Budget Report: The main objective of budgtary reports are analyzed data related

subject to revenues adn expenditure. there is a clear idea about the money spent on all

the divisions of an organization in the coming year. This helps to reduce the factors and

conflicts related the two departments as they have a plan and goals in the upcoming

3

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

plan, which they have to achieve so that they are not confused with the strategy of other

companies operating in the same industry. This report could help Zylla in determination

of their actual position in a market.

Accounts Receivable Ageing Report: The quoted organisation is working in the retail

sector. This basically helps to determine the credit limits to potential customers. this

facility is also available to those who order massive orders (Fowzia, 2011). This report

helps find buyers who do not pay their debts on predetermined time. These reports are

used by organisation subject to support the organisational structure with in the

organisation. particularly at this level for their business, when they are working at lower

levels, report this on a weekly, monthly or quarterly basis. It depends on the size of the

enterprise and the complexity of the business.

Job Costs Reports: it is mainly associated with getting the information related to

multiple product units. the venture is using it in different departments of this

organization. In this method, they discover the cost of each job and increase the

profitability of organisation. It would help Zylla in determining those activities which

are not providing them the necessary amount of revenue. They can also concentrate on

problems which are becoming main hind rates in increasing the. Zylla can detect jobs

that do not give returns according to management expectations.

Inventory Reports: The main purpose of report to find the report the buisiness

problems. Zylla is a one of the small industry, they face the issue of overstalking, which

increase their overall cost of business. In the case of under-stocking, an organization can

lose some customers because they will buy essential items from other stores if they do

not get the desired product at the right time. These troubles can be resolved using

management accounting equipment such as economic order quantity, it provides the

right amount of goods in comparison to an enterprise so that they can live in their

warehouse so that they can reduce their carrying costs.

Income Statement Reports: This reporting techniques supports company in

determining overall net profits which is remaining at the end of a year after paying all its

expenses. This remaining balance is added to retained earnings account in balance sheet.

This reporting method would be useful for Zylla because company could know its

remaining balance in profit at the end of a year. For example, Company has recorded

4

companies operating in the same industry. This report could help Zylla in determination

of their actual position in a market.

Accounts Receivable Ageing Report: The quoted organisation is working in the retail

sector. This basically helps to determine the credit limits to potential customers. this

facility is also available to those who order massive orders (Fowzia, 2011). This report

helps find buyers who do not pay their debts on predetermined time. These reports are

used by organisation subject to support the organisational structure with in the

organisation. particularly at this level for their business, when they are working at lower

levels, report this on a weekly, monthly or quarterly basis. It depends on the size of the

enterprise and the complexity of the business.

Job Costs Reports: it is mainly associated with getting the information related to

multiple product units. the venture is using it in different departments of this

organization. In this method, they discover the cost of each job and increase the

profitability of organisation. It would help Zylla in determining those activities which

are not providing them the necessary amount of revenue. They can also concentrate on

problems which are becoming main hind rates in increasing the. Zylla can detect jobs

that do not give returns according to management expectations.

Inventory Reports: The main purpose of report to find the report the buisiness

problems. Zylla is a one of the small industry, they face the issue of overstalking, which

increase their overall cost of business. In the case of under-stocking, an organization can

lose some customers because they will buy essential items from other stores if they do

not get the desired product at the right time. These troubles can be resolved using

management accounting equipment such as economic order quantity, it provides the

right amount of goods in comparison to an enterprise so that they can live in their

warehouse so that they can reduce their carrying costs.

Income Statement Reports: This reporting techniques supports company in

determining overall net profits which is remaining at the end of a year after paying all its

expenses. This remaining balance is added to retained earnings account in balance sheet.

This reporting method would be useful for Zylla because company could know its

remaining balance in profit at the end of a year. For example, Company has recorded

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

£7500 net profit through calculation of income statements in marginal costing. After

paying all its variable expenses, firm has earned that much net earnings.

Cash flow report: This reporting method supports company in analysing availability of

cash with a business (Goetsch and Davis, 2014). It also helps company in evaluating

how much a business has a opportunity to earn cash in future. Zylla can applied this

method to find how much liquidity company has in its business. Like, company has

many accrual based analysis like budgeted sales and goods delivered to debtors. Hence,

in both cases, business doesn't received any cash. Therefore these type of real cash

analysis would help Zylla in identifying cash available with the business.

TASK 2

P3 Analysation of cost and profit using costing techniques

Cost management is an integral part of accounting. This helps the organization by

reducing their costs, which indirectly positively impacts the firm's profit. Following is

explanation of marginal and absorption costing:

Marginal Costing: This is an expense that a company has done on the production of an

additional item (Granlund, 2011). It can be divided into two parts, manufacturing and non-

construction costs. There are material, labour and upper main expenses which are considered in

this report. Apart from production, it also focuses on other expenditures like one of the main

points needed to consider the time of adoption of this form of time cost cost is that the closing

stock is treated in the same year. Break-even point is the main use of this method. Because

break-even point analysis is done to find optimum level of production that a company should do

to utilize maximum of its resources. This concept reveals that with increase in sales by a

company, it could earn a profit even if the profit margin is low.

Absorption Costing: In addition to direct material and labour, fixed manufacturing

overhead is also considered as the time to use this method (Lavia López and Hiebl, 2014).

Closing stock is included at the time of implementing this system, which is the main reason that

the company earns more income. Fixed overhead spent in this process is ignored if the goods are

not sold in the same year. It covers production process, manufacturing process and fixed

overheads. It mainly considers fixed and variable expenses together.

5

paying all its variable expenses, firm has earned that much net earnings.

Cash flow report: This reporting method supports company in analysing availability of

cash with a business (Goetsch and Davis, 2014). It also helps company in evaluating

how much a business has a opportunity to earn cash in future. Zylla can applied this

method to find how much liquidity company has in its business. Like, company has

many accrual based analysis like budgeted sales and goods delivered to debtors. Hence,

in both cases, business doesn't received any cash. Therefore these type of real cash

analysis would help Zylla in identifying cash available with the business.

TASK 2

P3 Analysation of cost and profit using costing techniques

Cost management is an integral part of accounting. This helps the organization by

reducing their costs, which indirectly positively impacts the firm's profit. Following is

explanation of marginal and absorption costing:

Marginal Costing: This is an expense that a company has done on the production of an

additional item (Granlund, 2011). It can be divided into two parts, manufacturing and non-

construction costs. There are material, labour and upper main expenses which are considered in

this report. Apart from production, it also focuses on other expenditures like one of the main

points needed to consider the time of adoption of this form of time cost cost is that the closing

stock is treated in the same year. Break-even point is the main use of this method. Because

break-even point analysis is done to find optimum level of production that a company should do

to utilize maximum of its resources. This concept reveals that with increase in sales by a

company, it could earn a profit even if the profit margin is low.

Absorption Costing: In addition to direct material and labour, fixed manufacturing

overhead is also considered as the time to use this method (Lavia López and Hiebl, 2014).

Closing stock is included at the time of implementing this system, which is the main reason that

the company earns more income. Fixed overhead spent in this process is ignored if the goods are

not sold in the same year. It covers production process, manufacturing process and fixed

overheads. It mainly considers fixed and variable expenses together.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

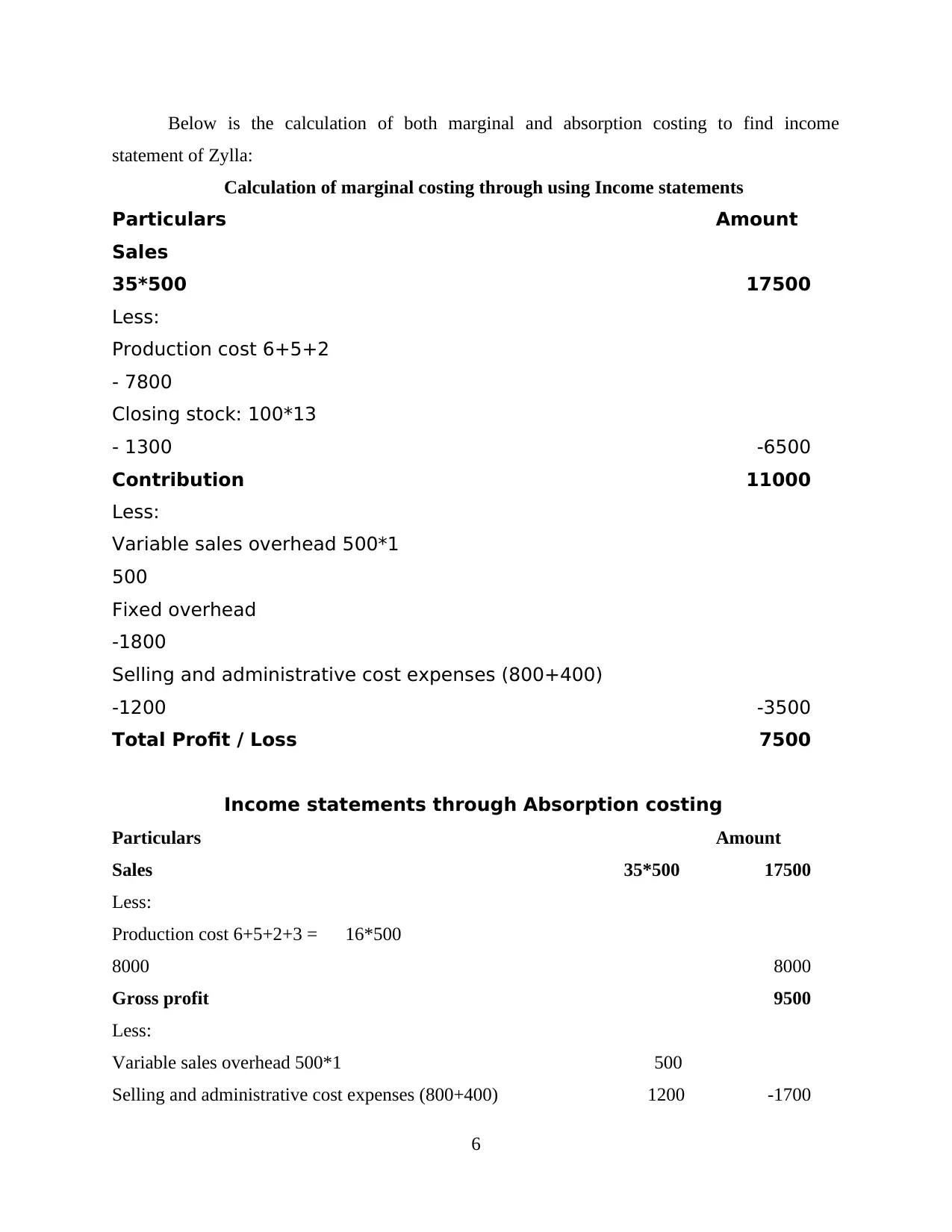

Below is the calculation of both marginal and absorption costing to find income

statement of Zylla:

Calculation of marginal costing through using Income statements

Particulars Amount

Sales

35*500 17500

Less:

Production cost 6+5+2

- 7800

Closing stock: 100*13

- 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1

500

Fixed overhead

-1800

Selling and administrative cost expenses (800+400)

-1200 -3500

Total Profit / Loss 7500

Income statements through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

6

statement of Zylla:

Calculation of marginal costing through using Income statements

Particulars Amount

Sales

35*500 17500

Less:

Production cost 6+5+2

- 7800

Closing stock: 100*13

- 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1

500

Fixed overhead

-1800

Selling and administrative cost expenses (800+400)

-1200 -3500

Total Profit / Loss 7500

Income statements through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

6

Total Profit / Loss 7800

Marginal costing considers mainly two types of costs that is variable and fixed costs on

the other hand absorption costing considers production and selling & distribution costs (Linoff

and Berry, 2011). there are significant difference are defined in terms of marginal costing and

absorption costing:

Basis for comparison Marginal Costing Absorption Costing

Meaning These techniques of marginal

costing is used for finding total

cost per unit of production for

the process of decision-making

is known as Marginal costing.

In this costing techniques,

costs are distributed among

various cost centres to analyse

total cost of productions

(Ward, 2012).

Cost Identification Expenses are arranged into

variable and settled in

negligible costing. To discover

commitment and net benefit

independently.

This basically helps to

determine variable cost

considered as cost of the

product.

Categorization Expenses Cost are analysed in respect of

bifurcating the structure and of

business in effective manner.

There are also some essential

elements considered for

analysing profitability and

administration cost,

profitability.

Lucrativeness Cost volume analysis is one of

the major technique which is

used in organisational context.

This is the main objective

related fixed cost and

affectivity of profitability.

Cost per Unit There's no effect of opening

and shutting stock on cost per

unit count of Negligible

costing.

It mainly affect the difference

of opening and closing stock

cost per unit calculation of

absorption cost.

High spot This mainly helps to analyse Both the net profit and gross

7

Marginal costing considers mainly two types of costs that is variable and fixed costs on

the other hand absorption costing considers production and selling & distribution costs (Linoff

and Berry, 2011). there are significant difference are defined in terms of marginal costing and

absorption costing:

Basis for comparison Marginal Costing Absorption Costing

Meaning These techniques of marginal

costing is used for finding total

cost per unit of production for

the process of decision-making

is known as Marginal costing.

In this costing techniques,

costs are distributed among

various cost centres to analyse

total cost of productions

(Ward, 2012).

Cost Identification Expenses are arranged into

variable and settled in

negligible costing. To discover

commitment and net benefit

independently.

This basically helps to

determine variable cost

considered as cost of the

product.

Categorization Expenses Cost are analysed in respect of

bifurcating the structure and of

business in effective manner.

There are also some essential

elements considered for

analysing profitability and

administration cost,

profitability.

Lucrativeness Cost volume analysis is one of

the major technique which is

used in organisational context.

This is the main objective

related fixed cost and

affectivity of profitability.

Cost per Unit There's no effect of opening

and shutting stock on cost per

unit count of Negligible

costing.

It mainly affect the difference

of opening and closing stock

cost per unit calculation of

absorption cost.

High spot This mainly helps to analyse Both the net profit and gross

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the contribution of this

techniques.

profit are analysed the net

profit from the cost of various

department centres.

Cost Collection Collection of data and outline

the endeavour of subject to

each product.

Cost of data are collected

through type of type of data.

Absorption costing includes various methods which supports proper absorption

techniques, these different methods are explained below:

Distribution of overheads: It involves charging overhead expense directly to production

department separately. Distribution of overheads contains allocation and apportionment

of overhead among various departments.

Renomination of service cost centre overheads:In production activities, there is no

direct involvement of service cost centres or various departments. Therefore, to calculate

proper absorption costs, fixed overhead charges could be distribute among production

departments because they supports operational process of a company. For example,

canteen provides food to labour, stores provides protective equipments and maintenance

contributes in proper working of a machine. It is necessary to include these costs also

because main event of a company which is production of goods is depended on these

supportive stores, canteen and maintenance departments.

Overhead absorptions: It is characterized as charging per unit cost of creation by

figuring based on add up to no. of units to be created. Overhead retention is a technique

in which overheads costs are incorporated into the aggregate cost of an item.

TASK 3

P4 Report on advantages and disadvantages of different types of planning tools for budgetary-

control

Budgetary-control

Zyla needs to ensure that it gives equal importance to each variety of budgetary tool so that

maximum returns can be achieved from same. It will increase the financial capacity of an

enterprise as when budget is prepared it ensures effective control over the various operations of

firm. Budgetary control plays an important role in providing sustainability to an organization.

8

techniques.

profit are analysed the net

profit from the cost of various

department centres.

Cost Collection Collection of data and outline

the endeavour of subject to

each product.

Cost of data are collected

through type of type of data.

Absorption costing includes various methods which supports proper absorption

techniques, these different methods are explained below:

Distribution of overheads: It involves charging overhead expense directly to production

department separately. Distribution of overheads contains allocation and apportionment

of overhead among various departments.

Renomination of service cost centre overheads:In production activities, there is no

direct involvement of service cost centres or various departments. Therefore, to calculate

proper absorption costs, fixed overhead charges could be distribute among production

departments because they supports operational process of a company. For example,

canteen provides food to labour, stores provides protective equipments and maintenance

contributes in proper working of a machine. It is necessary to include these costs also

because main event of a company which is production of goods is depended on these

supportive stores, canteen and maintenance departments.

Overhead absorptions: It is characterized as charging per unit cost of creation by

figuring based on add up to no. of units to be created. Overhead retention is a technique

in which overheads costs are incorporated into the aggregate cost of an item.

TASK 3

P4 Report on advantages and disadvantages of different types of planning tools for budgetary-

control

Budgetary-control

Zyla needs to ensure that it gives equal importance to each variety of budgetary tool so that

maximum returns can be achieved from same. It will increase the financial capacity of an

enterprise as when budget is prepared it ensures effective control over the various operations of

firm. Budgetary control plays an important role in providing sustainability to an organization.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget is done for a specific time period, usually a year. It helps the management to see the

company fully, which is necessary to remove various types of confusions present in a firm

(Renz, 2016). Most managers have planned because they understand that it supports the

company to move in one direction.

Process of Budgetary control:

Discuss with managers to make an effective plan: Under this step, the managers of Zyla meet

together and conduct meeting regarding the formulation of plans and policies. The officials of

Zyla this way plan their financial resources so that they can be allocated in an appropriate

manner.

Record the actual performance: After formulation, the management should concentrate on

recording the performance of employees so as to direct them to perform in right direction. This

way Zyla keeps monitoring over the different departments of an enterprise so that the officials

invole in same can be checked that weather they are performing well or not.

Comparison of actual with the standard: After recording, the management should carefully

analyse the performance of each employee through comparing their actual with standard.

Determine difference or other variance: Through comparing actual with expected

performance, the managers are able to find out the deviation if any, which restricts employees to

perform well.

Respond immediately: In this last step, the managers should require to implement corrective

measures in order to eliminate deviations and problems which brings motivation among

employees to perform well.

Planning tools which need to be used by Managers:

Forecasting tools: This is the tool which is used by manager to forecast the business trends and

occurrence that will happened in near future such as prices, demands, labour etc. For this, the

manager need to conduct research and identify the possibilities that will help in achieving

desired goals and objectives. Due to forecasting, the managers should able to direct and gudie

employees so that they are ready to face future challenges and meet future needs and demands

of customers.

Advantages:

It helps management to make an effective plans and policies in order to compete with

future challenges.

9

company fully, which is necessary to remove various types of confusions present in a firm

(Renz, 2016). Most managers have planned because they understand that it supports the

company to move in one direction.

Process of Budgetary control:

Discuss with managers to make an effective plan: Under this step, the managers of Zyla meet

together and conduct meeting regarding the formulation of plans and policies. The officials of

Zyla this way plan their financial resources so that they can be allocated in an appropriate

manner.

Record the actual performance: After formulation, the management should concentrate on

recording the performance of employees so as to direct them to perform in right direction. This

way Zyla keeps monitoring over the different departments of an enterprise so that the officials

invole in same can be checked that weather they are performing well or not.

Comparison of actual with the standard: After recording, the management should carefully

analyse the performance of each employee through comparing their actual with standard.

Determine difference or other variance: Through comparing actual with expected

performance, the managers are able to find out the deviation if any, which restricts employees to

perform well.

Respond immediately: In this last step, the managers should require to implement corrective

measures in order to eliminate deviations and problems which brings motivation among

employees to perform well.

Planning tools which need to be used by Managers:

Forecasting tools: This is the tool which is used by manager to forecast the business trends and

occurrence that will happened in near future such as prices, demands, labour etc. For this, the

manager need to conduct research and identify the possibilities that will help in achieving

desired goals and objectives. Due to forecasting, the managers should able to direct and gudie

employees so that they are ready to face future challenges and meet future needs and demands

of customers.

Advantages:

It helps management to make an effective plans and policies in order to compete with

future challenges.

9

The chances of getting profitable outcomes from future business activities will be more

as the employees are ready to face future business activities.

Disadvantage:

Sometimes the assumptions are not accurate due to which the chances of facing losses

by an organisation will be high. If the company have low skilled workers who are inefficient to face future challenges,

then it will be difficult for them to handle future challenges.

Contingency planning tools: This is the tool which is used with a motive of identifying

uncertainties which may affect the growth and success of an organisation. The management

here play an important role in implementing corrective measures in order to protect business

organisation from such uncertainties.

Advantages:

It helps in handling and managing risk through implementation of contingency plan and

policies with a motive of achieving desired target. It help company in achieving competitive advantages through grabbing future

opportunities which are competitive in nature.

Disadvantages:

The contingency plan has been made on the basis of data collected by management

through research. Therefore, the quality of data is poor then the contingency may less

effective.

Formulation of contingency plans takes more time and money which affects the

profitability of company as well.

10

Types planning tools of Budgetary

control

Non-Monetary

Budgets

Financial Budgets

Operating Budgets

Fixed and variable

budgets

as the employees are ready to face future business activities.

Disadvantage:

Sometimes the assumptions are not accurate due to which the chances of facing losses

by an organisation will be high. If the company have low skilled workers who are inefficient to face future challenges,

then it will be difficult for them to handle future challenges.

Contingency planning tools: This is the tool which is used with a motive of identifying

uncertainties which may affect the growth and success of an organisation. The management

here play an important role in implementing corrective measures in order to protect business

organisation from such uncertainties.

Advantages:

It helps in handling and managing risk through implementation of contingency plan and

policies with a motive of achieving desired target. It help company in achieving competitive advantages through grabbing future

opportunities which are competitive in nature.

Disadvantages:

The contingency plan has been made on the basis of data collected by management

through research. Therefore, the quality of data is poor then the contingency may less

effective.

Formulation of contingency plans takes more time and money which affects the

profitability of company as well.

10

Types planning tools of Budgetary

control

Non-Monetary

Budgets

Financial Budgets

Operating Budgets

Fixed and variable

budgets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.