Management Accounting Systems and Reporting: Unit 5 Report

VerifiedAdded on 2021/02/22

|17

|4997

|87

Report

AI Summary

This report analyzes management accounting systems and their application within Cobell Ltd, a fruit juice and soft drink company. It covers various management accounting systems like inventory management, cost accounting, price optimization, and job costing, detailing their advantages and essential requirements. The report also explores management accounting reporting, including performance reports, budget reports, accounts receivable reports, and inventory reports. Furthermore, it delves into the preparation of income statements using marginal and absorption costing methods, planning tools, and how companies adapt management systems to address financial issues. The report provides a comprehensive overview of management accounting principles and their practical application in a business context, offering insights into financial reporting, cost analysis, and decision-making processes, and planning to solve financial problems.

Unit 5 – Management

Accounting L-4

Accounting L-4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems..........................................................................................1

P2. Management accounting reporting........................................................................................3

M1. Advantages of management accounting systems. ...............................................................4

D1 Evaluation of accounting systems and management accounting reporting that are

integrated within organisational processes..................................................................................5

TASK 2............................................................................................................................................6

P3 Preparation of income statement by using marginal or absorption costing method...............6

M2.Application of wide range of management accounting techniques and production of

appropriate financial reporting documents..................................................................................7

D2. Financial reports which helps in interpreting business operational activities.......................8

TASK 3............................................................................................................................................8

P4. Planning tools........................................................................................................................8

M3. Use of planning tools..........................................................................................................10

TASK 4..........................................................................................................................................10

P5. Examining how companies adapt to management systems in the face of financial issues. 10

M4. Management accounting in response to solve financial issue that can lead to the

sustainable success.....................................................................................................................12

D3. Planning tools to resolve the financial problems................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting systems..........................................................................................1

P2. Management accounting reporting........................................................................................3

M1. Advantages of management accounting systems. ...............................................................4

D1 Evaluation of accounting systems and management accounting reporting that are

integrated within organisational processes..................................................................................5

TASK 2............................................................................................................................................6

P3 Preparation of income statement by using marginal or absorption costing method...............6

M2.Application of wide range of management accounting techniques and production of

appropriate financial reporting documents..................................................................................7

D2. Financial reports which helps in interpreting business operational activities.......................8

TASK 3............................................................................................................................................8

P4. Planning tools........................................................................................................................8

M3. Use of planning tools..........................................................................................................10

TASK 4..........................................................................................................................................10

P5. Examining how companies adapt to management systems in the face of financial issues. 10

M4. Management accounting in response to solve financial issue that can lead to the

sustainable success.....................................................................................................................12

D3. Planning tools to resolve the financial problems................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting includes various procedures that are associated with preparation

along with presentation of financial information in such manner that assist internal management

to plan for future, formulate policies and controlling business operations (Booth, 2018). The

function of such accounting is to assist managers while making decisions for the betterment of

company. It is not necessary for any organisation to adopt management accounting as its

requirements are dependent on organisational objectives. To understand management

accounting, the selected organisation is Cobell Ltd which is situated at Leigham Business Units,

United Kingdom. The company was incorporated in the year 1999 and is famous for fruit along

with vegetable juices, soft drinks and mineral water (Cobell Ltd. 2019). The company has

specialisation in production of JOJO fruit juice and provides essential information to managers to

facilitate decision making. The report discusses about management accounting systems with their

essential requirements, methods of reporting, usage of appropriate technique of cost analysis for

preparation of income statement by using absorption costs as well as marginal costs. It further

includes planning tools with advantages and disadvantages, usage of management accounting

systems in order to responding to financial problems to lead sustainable success.

TASK 1

P1. Management accounting systems.

Management accounting is a procedural activity which includes understanding,

identifying, recording, examining, measuring and communicating financial and non financial

information to key managers to take essential decisions pursuit towards organisational goals.

Such accounting is also concerned with internal factors as well as assists financial personnels

while preparing as well as presenting important financial statements. In addition, it is used by

managers of Cobell Ltd while preparing short term and long term decisions to carry forward

operations or activities without any hurdles.

Management accounting systems: The concept of management accounting system is a

future oriented method which encompasses several practices and has wide scope that reaches

towards various departments of business. Some of the management accounting systems used by

management of Cobell Ltd are as follows:

1

Management accounting includes various procedures that are associated with preparation

along with presentation of financial information in such manner that assist internal management

to plan for future, formulate policies and controlling business operations (Booth, 2018). The

function of such accounting is to assist managers while making decisions for the betterment of

company. It is not necessary for any organisation to adopt management accounting as its

requirements are dependent on organisational objectives. To understand management

accounting, the selected organisation is Cobell Ltd which is situated at Leigham Business Units,

United Kingdom. The company was incorporated in the year 1999 and is famous for fruit along

with vegetable juices, soft drinks and mineral water (Cobell Ltd. 2019). The company has

specialisation in production of JOJO fruit juice and provides essential information to managers to

facilitate decision making. The report discusses about management accounting systems with their

essential requirements, methods of reporting, usage of appropriate technique of cost analysis for

preparation of income statement by using absorption costs as well as marginal costs. It further

includes planning tools with advantages and disadvantages, usage of management accounting

systems in order to responding to financial problems to lead sustainable success.

TASK 1

P1. Management accounting systems.

Management accounting is a procedural activity which includes understanding,

identifying, recording, examining, measuring and communicating financial and non financial

information to key managers to take essential decisions pursuit towards organisational goals.

Such accounting is also concerned with internal factors as well as assists financial personnels

while preparing as well as presenting important financial statements. In addition, it is used by

managers of Cobell Ltd while preparing short term and long term decisions to carry forward

operations or activities without any hurdles.

Management accounting systems: The concept of management accounting system is a

future oriented method which encompasses several practices and has wide scope that reaches

towards various departments of business. Some of the management accounting systems used by

management of Cobell Ltd are as follows:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: Inventory refers to the stock level of goods that are

used at various stages to produce a final product and making it ready for sale. Such system is

associated with management as well as supervision of stocks of enterprises. A proper record is

maintained using such system which includes date and time of the quantity of inventory entered

into the organisation as well as its warehouses along with the departure of bulk quantities for

selling purposes which becomes easy to calculate and determine actual available stock as well as

stock required for further operations (Boyns, Edwards and Nikitin, 2013). In context to Cobell

Ltd, management uses such system to track the inventory at different organisational locations in

order to get accurate information related with existing inventory level that helps in taking

decisions for further required stock. Essential requirement of Inventory management system is to

keep detailed record of inventory level to eliminate problems associated with overstock or under

stock at various point of production.

Cost accounting system: The framework that assists in cost estimation of various

organisational products and analysing aspects related with profitability, inventory valuation as

well as cost control. It is very essential for production managers to estimate accurate costs that

are associated with products as effective estimation leads towards profitable operations. The

managers of Cobell Ltd uses such system to estimate closing material inventory value, finished

products inventory along with work in process inventory. The managers with the help of this

system maintain proper books of accounts by recording cost of raw materials that were utilised

while preparing final products of fruit drinks like quantity of sugar, fruits, glucose, liquid

substance, flavours and so on. Cost accounting system is essentially required at workplace in

order to estimate costs of different inventories of organisational products as to prepare final

statements.

Price optimizing system: A mathematical analysis in which variations of demand are

calculated at different pricing level is termed as price optimisation system. It is used by

operational managers to control prices of key resources (Bragg, 2012). Using such system,

management of Corell Ltd determines response of customers towards different prices of fruit

juices, vegetable juices and soft drinks. It helps in deciding pricing that the managers should

determine of various juices in such manner that results in maximising profits of the company. It

is essentially required to allocate prices of products in effective manner that results in meeting

operational as well as organizational objectives.

2

used at various stages to produce a final product and making it ready for sale. Such system is

associated with management as well as supervision of stocks of enterprises. A proper record is

maintained using such system which includes date and time of the quantity of inventory entered

into the organisation as well as its warehouses along with the departure of bulk quantities for

selling purposes which becomes easy to calculate and determine actual available stock as well as

stock required for further operations (Boyns, Edwards and Nikitin, 2013). In context to Cobell

Ltd, management uses such system to track the inventory at different organisational locations in

order to get accurate information related with existing inventory level that helps in taking

decisions for further required stock. Essential requirement of Inventory management system is to

keep detailed record of inventory level to eliminate problems associated with overstock or under

stock at various point of production.

Cost accounting system: The framework that assists in cost estimation of various

organisational products and analysing aspects related with profitability, inventory valuation as

well as cost control. It is very essential for production managers to estimate accurate costs that

are associated with products as effective estimation leads towards profitable operations. The

managers of Cobell Ltd uses such system to estimate closing material inventory value, finished

products inventory along with work in process inventory. The managers with the help of this

system maintain proper books of accounts by recording cost of raw materials that were utilised

while preparing final products of fruit drinks like quantity of sugar, fruits, glucose, liquid

substance, flavours and so on. Cost accounting system is essentially required at workplace in

order to estimate costs of different inventories of organisational products as to prepare final

statements.

Price optimizing system: A mathematical analysis in which variations of demand are

calculated at different pricing level is termed as price optimisation system. It is used by

operational managers to control prices of key resources (Bragg, 2012). Using such system,

management of Corell Ltd determines response of customers towards different prices of fruit

juices, vegetable juices and soft drinks. It helps in deciding pricing that the managers should

determine of various juices in such manner that results in maximising profits of the company. It

is essentially required to allocate prices of products in effective manner that results in meeting

operational as well as organizational objectives.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: The accumulation of material, overhead and labour costs for

particular product or job is termed as job costing system. Such system is adopted at workplace

when numerous products are produced that are different from each other as well as involves

significant costs in each item. It further elaborates manufacturing cost into sub parts such as

direct material, direct labour, overhead and hence forth with the purpose to determine actual

costs of the products. In regards to Cobell Ltd, a separate department is designed takes

responsibility to manage costs along with expenses of the associated products. Essential

requirement of such system is to determine product as well as job monetary values by covering

actual costs to provide profitable results.

Thus, effectively using all the above mentioned accounting systems helps management of

Cobell Ltd to keep proper records of activities or operations in systematic manner that took place

at workplace. All these helps in enhancing operational efficiency to increase profit amrgins of

the company.

P2. Management accounting reporting.

Management accounting reporting: In an organisation, various kinds of accounting

reports are prepared and all have significant importance while delivering information to top

management authorities (Catanachand Feldmann, 2010). Accounting reports are prepared with

intention to aid in planning, measuring performances as well as making effective decisions.

Such reports are prepared by all managers at workplace as they provide accurate as well as

reliable statistical or financial information. Departmental heads of Cobell Ltd prepares following

accounting reports:

Performance reports: With the purpose of reviewing and evaluate employees as well as

company performance as a whole performance reports are prepared. Such report provides

comparison of performances within actual performance and base lined performances in any

project. The differences that are calculated by comparing actual results and standard

performances are clearly analysed as well as presented in such reports. Using such reports,

managers of Cobell Ltd analyses efficiencies as well as deficiencies in performances of

employees and other activities and measures actual performances to take decisions for the

improvements.

Budget reports: The crucial report that helps in measuring financial performance of a

company in the accounting time period. The managers prepares them at organisational level and

3

particular product or job is termed as job costing system. Such system is adopted at workplace

when numerous products are produced that are different from each other as well as involves

significant costs in each item. It further elaborates manufacturing cost into sub parts such as

direct material, direct labour, overhead and hence forth with the purpose to determine actual

costs of the products. In regards to Cobell Ltd, a separate department is designed takes

responsibility to manage costs along with expenses of the associated products. Essential

requirement of such system is to determine product as well as job monetary values by covering

actual costs to provide profitable results.

Thus, effectively using all the above mentioned accounting systems helps management of

Cobell Ltd to keep proper records of activities or operations in systematic manner that took place

at workplace. All these helps in enhancing operational efficiency to increase profit amrgins of

the company.

P2. Management accounting reporting.

Management accounting reporting: In an organisation, various kinds of accounting

reports are prepared and all have significant importance while delivering information to top

management authorities (Catanachand Feldmann, 2010). Accounting reports are prepared with

intention to aid in planning, measuring performances as well as making effective decisions.

Such reports are prepared by all managers at workplace as they provide accurate as well as

reliable statistical or financial information. Departmental heads of Cobell Ltd prepares following

accounting reports:

Performance reports: With the purpose of reviewing and evaluate employees as well as

company performance as a whole performance reports are prepared. Such report provides

comparison of performances within actual performance and base lined performances in any

project. The differences that are calculated by comparing actual results and standard

performances are clearly analysed as well as presented in such reports. Using such reports,

managers of Cobell Ltd analyses efficiencies as well as deficiencies in performances of

employees and other activities and measures actual performances to take decisions for the

improvements.

Budget reports: The crucial report that helps in measuring financial performance of a

company in the accounting time period. The managers prepares them at organisational level and

3

departmental levels that helps in formulating overall budget for the business. The managers of

Cobell Ltd all the past performance of financial resource are analysed and future budgets are

formulated to attain accurate results (Chiwamit, Modell and Yang, 2014).

Account receivable reports: These are generally prepared by businesses which relies on

extending credits as well as helps in determining reimbursement for doubtful accounts. It

categorises accounts receivables of the entities according to the time outstanding length related

to an invoice. Furthermore, management of Cobell Ltd by using such report identifies financial

position of customers and prepares report through making different columns for the amount

received as well as amount not received from customers which helps in evaluating the name of

defaulters by quick glance.

Inventory as well as manufacturing reports: The organisations that are involved in the

procedures of manufacturing prepares this type of accounting report as to record all activities

based on inventory usage as well as manufacturing of products so that their relevant procedures

becomes effective and efficient. It involves detailed information such as overhead cost per unit,

inventory wastages and labour costs. The managers of Cobell Ltd compares their current records

with last year using the report in order to determine the necessity of improvements. By analysing

such report managers can formulate plans to make performances of inventory and resources

effectively.

Hence, all the mentioned accounting reports are used by Cobell Ltd managers to control

various costs as well as making improvements in the areas in which they are lacking behind that

will result in performing business functions in more efficient ways.

M1. Advantages of management accounting systems.

Accounting system Advantages

Inventory management system This system is beneficial to keep records of inventory and

manage it properly. Cobell Ltd can reduce wastage and

maximize production with the help of this system.

Moreover, by using this system company can place next

order to raw material that helps in continue a business for

long term (DRURY, 2013).

4

Cobell Ltd all the past performance of financial resource are analysed and future budgets are

formulated to attain accurate results (Chiwamit, Modell and Yang, 2014).

Account receivable reports: These are generally prepared by businesses which relies on

extending credits as well as helps in determining reimbursement for doubtful accounts. It

categorises accounts receivables of the entities according to the time outstanding length related

to an invoice. Furthermore, management of Cobell Ltd by using such report identifies financial

position of customers and prepares report through making different columns for the amount

received as well as amount not received from customers which helps in evaluating the name of

defaulters by quick glance.

Inventory as well as manufacturing reports: The organisations that are involved in the

procedures of manufacturing prepares this type of accounting report as to record all activities

based on inventory usage as well as manufacturing of products so that their relevant procedures

becomes effective and efficient. It involves detailed information such as overhead cost per unit,

inventory wastages and labour costs. The managers of Cobell Ltd compares their current records

with last year using the report in order to determine the necessity of improvements. By analysing

such report managers can formulate plans to make performances of inventory and resources

effectively.

Hence, all the mentioned accounting reports are used by Cobell Ltd managers to control

various costs as well as making improvements in the areas in which they are lacking behind that

will result in performing business functions in more efficient ways.

M1. Advantages of management accounting systems.

Accounting system Advantages

Inventory management system This system is beneficial to keep records of inventory and

manage it properly. Cobell Ltd can reduce wastage and

maximize production with the help of this system.

Moreover, by using this system company can place next

order to raw material that helps in continue a business for

long term (DRURY, 2013).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system This is beneficial for managing cost of organisation and

control excess production within Cobell Ltd. Manager can

estimate cost of all expenses and decide cost of all products

by including expenses.

Price optimisation system It is beneficial for deciding the price of products and

services. Cobell Ltd gain advantage by using this system

such as it set the price of manufacturing products that helps

to increase productivity and profitability. So organization

should use this system for setting reasonable prices of

products and gain profit margin.

Job order costing system This system give an advantage to Cobell Ltd as to assign

work among employees and manage work according in

order to achieve goals. The manager of Cobell Ltd divides

roles and responsibility of organisation and increase

productivity.

D1 Evaluation of accounting systems and management accounting reporting that are integrated

within organisational processes

Management report and accounting system are integrated with organisational processes

such as accounting system helps to analysis, classification and make business decision in order to

run a business. Accounting reports are prepared by management for the purpose of comparing

standard information with actual information that helps to take corrective action. In Cobell Ltd,

manager uses different account system such as price optimization, cost accounting, job order

costing and inventory management system that helps to prepare budget report, performance,

inventory management and account receivable report in order to perform business activities that

helps in organizational processes. If management of Cobell uses these system properly and

generate reports then can achieve goals and objective of business industry. As result high

productivity and profitability that are considers as organisational processes (Edwards, 2014).

5

control excess production within Cobell Ltd. Manager can

estimate cost of all expenses and decide cost of all products

by including expenses.

Price optimisation system It is beneficial for deciding the price of products and

services. Cobell Ltd gain advantage by using this system

such as it set the price of manufacturing products that helps

to increase productivity and profitability. So organization

should use this system for setting reasonable prices of

products and gain profit margin.

Job order costing system This system give an advantage to Cobell Ltd as to assign

work among employees and manage work according in

order to achieve goals. The manager of Cobell Ltd divides

roles and responsibility of organisation and increase

productivity.

D1 Evaluation of accounting systems and management accounting reporting that are integrated

within organisational processes

Management report and accounting system are integrated with organisational processes

such as accounting system helps to analysis, classification and make business decision in order to

run a business. Accounting reports are prepared by management for the purpose of comparing

standard information with actual information that helps to take corrective action. In Cobell Ltd,

manager uses different account system such as price optimization, cost accounting, job order

costing and inventory management system that helps to prepare budget report, performance,

inventory management and account receivable report in order to perform business activities that

helps in organizational processes. If management of Cobell uses these system properly and

generate reports then can achieve goals and objective of business industry. As result high

productivity and profitability that are considers as organisational processes (Edwards, 2014).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

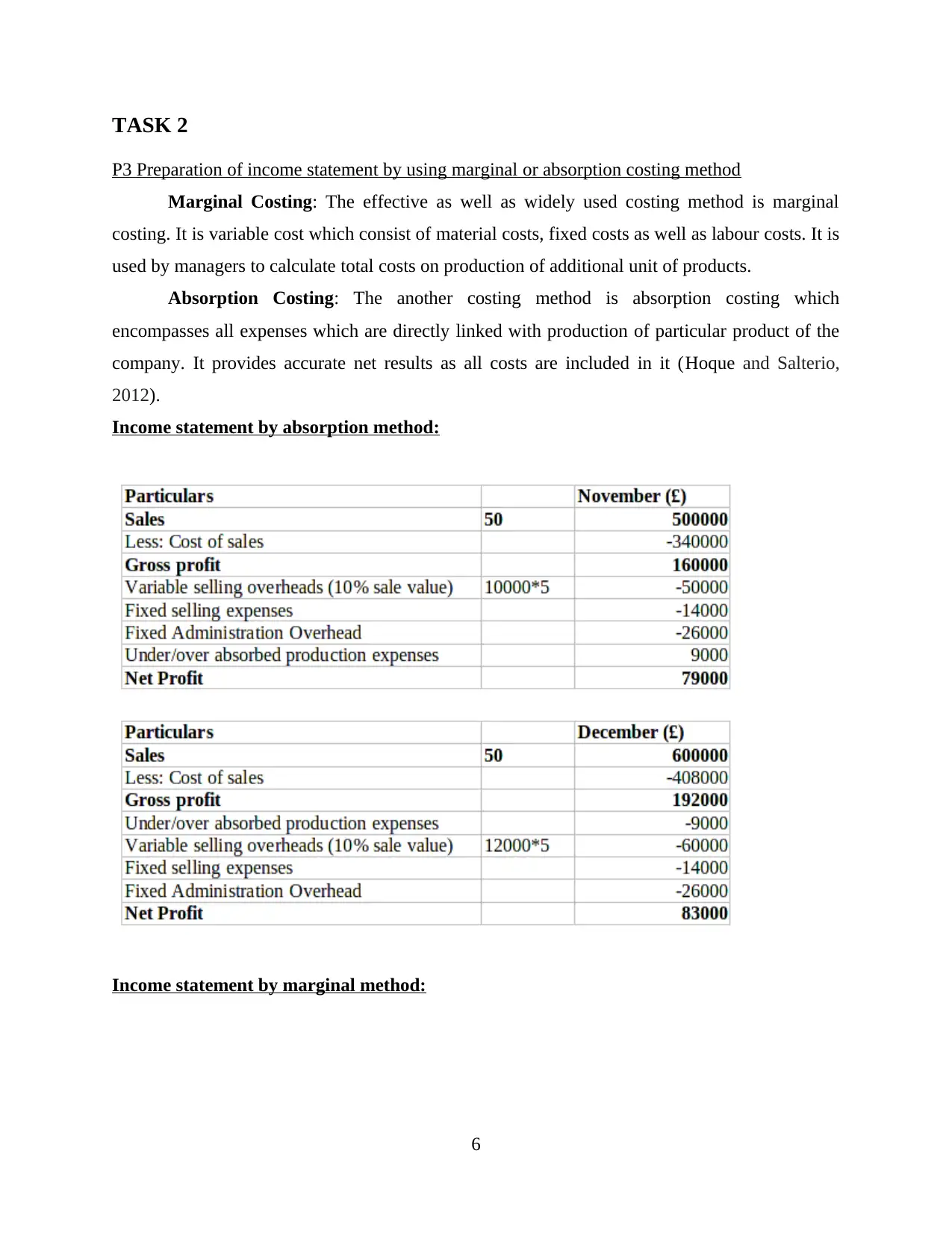

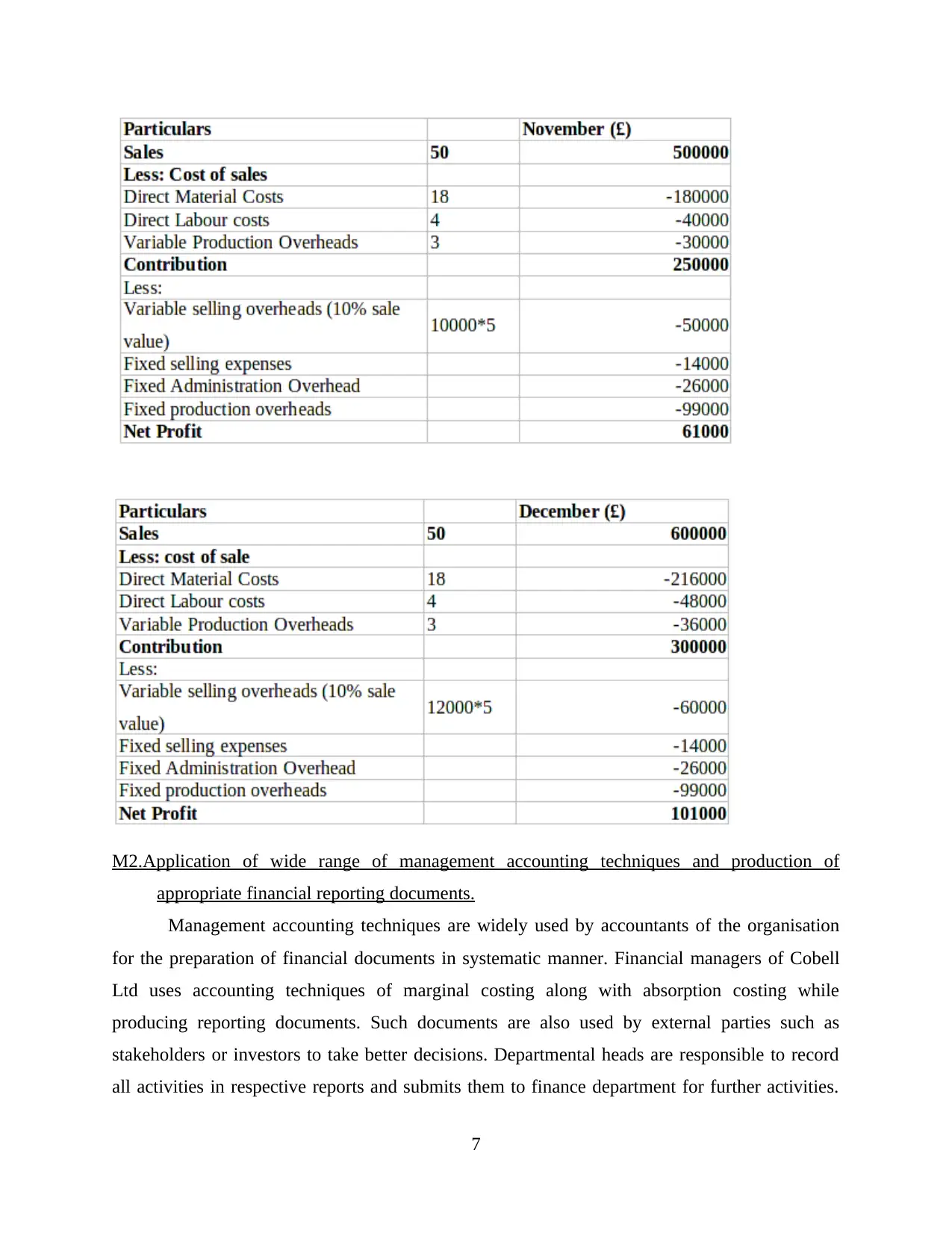

P3 Preparation of income statement by using marginal or absorption costing method

Marginal Costing: The effective as well as widely used costing method is marginal

costing. It is variable cost which consist of material costs, fixed costs as well as labour costs. It is

used by managers to calculate total costs on production of additional unit of products.

Absorption Costing: The another costing method is absorption costing which

encompasses all expenses which are directly linked with production of particular product of the

company. It provides accurate net results as all costs are included in it (Hoque and Salterio,

2012).

Income statement by absorption method:

Income statement by marginal method:

6

P3 Preparation of income statement by using marginal or absorption costing method

Marginal Costing: The effective as well as widely used costing method is marginal

costing. It is variable cost which consist of material costs, fixed costs as well as labour costs. It is

used by managers to calculate total costs on production of additional unit of products.

Absorption Costing: The another costing method is absorption costing which

encompasses all expenses which are directly linked with production of particular product of the

company. It provides accurate net results as all costs are included in it (Hoque and Salterio,

2012).

Income statement by absorption method:

Income statement by marginal method:

6

M2.Application of wide range of management accounting techniques and production of

appropriate financial reporting documents.

Management accounting techniques are widely used by accountants of the organisation

for the preparation of financial documents in systematic manner. Financial managers of Cobell

Ltd uses accounting techniques of marginal costing along with absorption costing while

producing reporting documents. Such documents are also used by external parties such as

stakeholders or investors to take better decisions. Departmental heads are responsible to record

all activities in respective reports and submits them to finance department for further activities.

7

appropriate financial reporting documents.

Management accounting techniques are widely used by accountants of the organisation

for the preparation of financial documents in systematic manner. Financial managers of Cobell

Ltd uses accounting techniques of marginal costing along with absorption costing while

producing reporting documents. Such documents are also used by external parties such as

stakeholders or investors to take better decisions. Departmental heads are responsible to record

all activities in respective reports and submits them to finance department for further activities.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial managers carefully analyses all information on such reports and further prepares

financial documents such as income statement, balance sheet, cash flow statements and so on in

order to analyse financial position of the organisation in competitive scenario (Kaplan and

Atkinson, 2015).

D2. Financial reports which helps in interpreting business operational activities

Financial reports are considered as important documents which stakeholders or investors

uses to analyse performance of the business in financial terms in an accounting year. They

analyses financial reports to make future investment decisions. From the above mentioned

income statements it is interpreted that Oshodi Plc is earning profits in the moth of November

and December. Through absorption costing technique, the ascertained net profit for the month of

November is 79000 £ and for December is 83000 £. At the same time, through marginal costing

technique, net profit for November is 61000 £ and December is 101000 £. The income

statements includes all transactions that helps in interpretation of all business operational

activities in effective manner.

TASK 3

P4. Planning tools.

Budget: It is the summary of all planned resources, revenues, costs and expenses for a

financial period in which income is also estimated far that particular period that reflects future

financial conditions, position along with objectives. It is basically defined for one year and

includes resource quantities, cash flows, volumes, revenues, liabilities, assets and many more.

The top management level of Cobell Ltd is responsible preparing budgets and communicates

them to all organisational members to follow them and perform operations accordingly.

Budgetary control: It encompasses the procedures to make comparisons between

estimated budgets as well as actual performances which helps in ascertaining the deviational

gaps and making strategies to deal with such gaps (Kotas, 2014). Such control helps the

managers of Cobell Ltd to prepare future budgets, devising comparisons along with controlling

costs of various operations. It aids towards providing assistances to enhance coordination

between different department such as production, human resource, sales and hence forth of the

organization. Some of the budgetary controls used by the company are the followings:

8

financial documents such as income statement, balance sheet, cash flow statements and so on in

order to analyse financial position of the organisation in competitive scenario (Kaplan and

Atkinson, 2015).

D2. Financial reports which helps in interpreting business operational activities

Financial reports are considered as important documents which stakeholders or investors

uses to analyse performance of the business in financial terms in an accounting year. They

analyses financial reports to make future investment decisions. From the above mentioned

income statements it is interpreted that Oshodi Plc is earning profits in the moth of November

and December. Through absorption costing technique, the ascertained net profit for the month of

November is 79000 £ and for December is 83000 £. At the same time, through marginal costing

technique, net profit for November is 61000 £ and December is 101000 £. The income

statements includes all transactions that helps in interpretation of all business operational

activities in effective manner.

TASK 3

P4. Planning tools.

Budget: It is the summary of all planned resources, revenues, costs and expenses for a

financial period in which income is also estimated far that particular period that reflects future

financial conditions, position along with objectives. It is basically defined for one year and

includes resource quantities, cash flows, volumes, revenues, liabilities, assets and many more.

The top management level of Cobell Ltd is responsible preparing budgets and communicates

them to all organisational members to follow them and perform operations accordingly.

Budgetary control: It encompasses the procedures to make comparisons between

estimated budgets as well as actual performances which helps in ascertaining the deviational

gaps and making strategies to deal with such gaps (Kotas, 2014). Such control helps the

managers of Cobell Ltd to prepare future budgets, devising comparisons along with controlling

costs of various operations. It aids towards providing assistances to enhance coordination

between different department such as production, human resource, sales and hence forth of the

organization. Some of the budgetary controls used by the company are the followings:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash budget: Such budget contains informations about cash inflows and outflows within

particular time period. The purpose behind such budget is to assess liquidity flow as well as

sufficient availability of required cash to handle operations without hurdles. Using such budget,

managers of Cobell Ltd makes projections related with organisational cash position in the

competitive market in future time period. The company performs operations mostly in cash terms

and records all receipts and payments of cash in cash budget.

Advantages: It provides benefits to Cobell Ltd in assessing requirements of cash in

coming time period. It also helps in avoiding expenditures in unnecessary raw materials, fees and

more as well as manages liquidity situations in effective manner.

Disadvantages: It creates situations of over usage of financial resources in several

situations and fails to provide accurate profitable results as it does not record credit transactions.

Operating budget: Such type of budget is based on incomes and expenses of particular

operation such as sales forecast, production forecast and many more. It is considered as short

term budget as capital outlays are not included in such budget. It is widely used in

manufacturing organisation in order to calculating actual income gained and expenses incurred

on production related activities. It helps Cobell Ltd managers to portray expected costs, incomes

as well as expenses by considering quarterly, half yearly or annual performance (Lind and

Thrane, 2010).

Advantages: Such budget helps managers of Cobell Limited to carefully manage current

expenses along with projecting future expenses. It benefits the company by building financial

reserves that are used to deal with temporary setbacks.

Disadvantages: Due to the uncertain future, such budget limits actual predictability and

fails to show real situations of the expense and incomes.

Master budget: The budget which includes detailed summary of budgets, accounts,

plans and statements that are required for business operation. It represents managements future

plans and the ways in which these will be accomplished by using different functional

components. Organisational managers of Cobell Ltd prepares such budget to get an idea of the

future objectives of company along with performing ways to accomplish them. It helps in

projecting cash flows as well as planing to attain potential financing.

9

particular time period. The purpose behind such budget is to assess liquidity flow as well as

sufficient availability of required cash to handle operations without hurdles. Using such budget,

managers of Cobell Ltd makes projections related with organisational cash position in the

competitive market in future time period. The company performs operations mostly in cash terms

and records all receipts and payments of cash in cash budget.

Advantages: It provides benefits to Cobell Ltd in assessing requirements of cash in

coming time period. It also helps in avoiding expenditures in unnecessary raw materials, fees and

more as well as manages liquidity situations in effective manner.

Disadvantages: It creates situations of over usage of financial resources in several

situations and fails to provide accurate profitable results as it does not record credit transactions.

Operating budget: Such type of budget is based on incomes and expenses of particular

operation such as sales forecast, production forecast and many more. It is considered as short

term budget as capital outlays are not included in such budget. It is widely used in

manufacturing organisation in order to calculating actual income gained and expenses incurred

on production related activities. It helps Cobell Ltd managers to portray expected costs, incomes

as well as expenses by considering quarterly, half yearly or annual performance (Lind and

Thrane, 2010).

Advantages: Such budget helps managers of Cobell Limited to carefully manage current

expenses along with projecting future expenses. It benefits the company by building financial

reserves that are used to deal with temporary setbacks.

Disadvantages: Due to the uncertain future, such budget limits actual predictability and

fails to show real situations of the expense and incomes.

Master budget: The budget which includes detailed summary of budgets, accounts,

plans and statements that are required for business operation. It represents managements future

plans and the ways in which these will be accomplished by using different functional

components. Organisational managers of Cobell Ltd prepares such budget to get an idea of the

future objectives of company along with performing ways to accomplish them. It helps in

projecting cash flows as well as planing to attain potential financing.

9

Advantages: Operating budget benefit the company by tracking entire business and

preparing financial responsibilities. It ensures managers that the organisation is performing

continuous operations in proper format.

Disadvantages: Operating budget is used by company to set daily activities and to

monitor such budget managers of the company required highly skilled accountant that adds

additional costs to the business (Maskell, Baggaley and Grasso, 2017).

M3. Use of planning tools.

Planning tools are used with the objective to asset in planning, preparation as well as

forecasting budgets. These plays crucial function in monitoring and controlling all operations

and activities. Some of the planning tools used by the management of Cobell Ltd are cash

budget, operating budget and master budget. All such budgets are effectively used while

estimating future expenses as well as incomes (Osborne and Ball, 2010). By effectively applying

them, organisational managers prepares as well as forecast budgets to accomplish business

objectives.

TASK 4

P5. Examining how companies adapt to management systems in the face of financial issues.

Financial problems: These are the issues related with monetary resources as well as

funds that are faced by all business whether small sized, medium sized or large sized to perform

day to day routines and operations. Such problems arises due to several factors such as external

forces, financial pressure, business cycle, changed customer preferences or internal factors. It is

the responsibility of financial manager of the company to resolve such problem. Following are

the financial problems that Cobell Ltd is facing:

Poor cash management: In order to carry out all operations, it is very essential to

manage available cash reserves of the company. Cobell Limited is not able to manage its

monetary resources in optimum manner due to no appropriate information of inventory,

increased competition and sudden changes in external environment. Thus, managers faces poor

cash management financial problem (Periasamy, 2010).

Late payments by clients: Various clients purchases products of the company on credit

terms and several times does not make payment on prescribed time which misbalances

10

preparing financial responsibilities. It ensures managers that the organisation is performing

continuous operations in proper format.

Disadvantages: Operating budget is used by company to set daily activities and to

monitor such budget managers of the company required highly skilled accountant that adds

additional costs to the business (Maskell, Baggaley and Grasso, 2017).

M3. Use of planning tools.

Planning tools are used with the objective to asset in planning, preparation as well as

forecasting budgets. These plays crucial function in monitoring and controlling all operations

and activities. Some of the planning tools used by the management of Cobell Ltd are cash

budget, operating budget and master budget. All such budgets are effectively used while

estimating future expenses as well as incomes (Osborne and Ball, 2010). By effectively applying

them, organisational managers prepares as well as forecast budgets to accomplish business

objectives.

TASK 4

P5. Examining how companies adapt to management systems in the face of financial issues.

Financial problems: These are the issues related with monetary resources as well as

funds that are faced by all business whether small sized, medium sized or large sized to perform

day to day routines and operations. Such problems arises due to several factors such as external

forces, financial pressure, business cycle, changed customer preferences or internal factors. It is

the responsibility of financial manager of the company to resolve such problem. Following are

the financial problems that Cobell Ltd is facing:

Poor cash management: In order to carry out all operations, it is very essential to

manage available cash reserves of the company. Cobell Limited is not able to manage its

monetary resources in optimum manner due to no appropriate information of inventory,

increased competition and sudden changes in external environment. Thus, managers faces poor

cash management financial problem (Periasamy, 2010).

Late payments by clients: Various clients purchases products of the company on credit

terms and several times does not make payment on prescribed time which misbalances

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.