University Assignment: Management Accounting Report - Unit 5 Analysis

VerifiedAdded on 2020/10/23

|21

|5420

|374

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within an organization, specifically focusing on Williams Performance Tenders. It begins by defining management accounting, outlining its essential requirements, and exploring various types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. The report then delves into different management accounting reports, such as budget reports, accounts receivable aging reports, cost managerial accounting reports, and performance reports, evaluating their benefits and integration within the organization. Furthermore, it examines absorption costing and marginal costing methods, producing income statements using each method and computing break-even analysis. The report also analyzes the application of management accounting techniques, including planning tools for budgetary control, and assesses how these techniques can address financial problems and contribute to the sustainable success of the organization. The report concludes by summarizing the key findings and emphasizing the significance of management accounting in effective decision-making and organizational growth.

UNIT 5 MA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Meaning of management accounting and essential requirements of different types of

management accounting systems...........................................................................................1

B. Explaining Different Management Accounting Reports...................................................3

C. Evaluating the benefits of management accounting systems ............................................5

D. Integration of management accounting system and reports are developed in organization ..6

TASK 2............................................................................................................................................6

A. 1 Explaining absorption costing and marginal costing methods.......................................6

A.2. Producing income statements by utilising costing methods...........................................7

B. Computation of Break-Even analysis................................................................................8

C. Applying the range of management accounting techniques and produce appropriate

financial reporting documents accurately for the scenarios given in the Task 2. ..................9

D. Producing financial reports that accurately apply and interpret data for business activities

shown in the scenarios .........................................................................................................11

TASK 3 .........................................................................................................................................11

A. Advantages and disadvantages of different types of planning tools for budgetary control 11

B. Showing application of the planning tools for preparing, forecasting and analysing budgets

..............................................................................................................................................13

C. Comparing how organization helps in adopting the management information system as

comparison with the financial problems...............................................................................14

D. Analysing how your management accounting techniques could respond to financial

problems and lead the organization to sustainable success..................................................15

E. Evaluating how planning tools could be used to solve financial problems and lead the

organization to sustainable success. ....................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Meaning of management accounting and essential requirements of different types of

management accounting systems...........................................................................................1

B. Explaining Different Management Accounting Reports...................................................3

C. Evaluating the benefits of management accounting systems ............................................5

D. Integration of management accounting system and reports are developed in organization ..6

TASK 2............................................................................................................................................6

A. 1 Explaining absorption costing and marginal costing methods.......................................6

A.2. Producing income statements by utilising costing methods...........................................7

B. Computation of Break-Even analysis................................................................................8

C. Applying the range of management accounting techniques and produce appropriate

financial reporting documents accurately for the scenarios given in the Task 2. ..................9

D. Producing financial reports that accurately apply and interpret data for business activities

shown in the scenarios .........................................................................................................11

TASK 3 .........................................................................................................................................11

A. Advantages and disadvantages of different types of planning tools for budgetary control 11

B. Showing application of the planning tools for preparing, forecasting and analysing budgets

..............................................................................................................................................13

C. Comparing how organization helps in adopting the management information system as

comparison with the financial problems...............................................................................14

D. Analysing how your management accounting techniques could respond to financial

problems and lead the organization to sustainable success..................................................15

E. Evaluating how planning tools could be used to solve financial problems and lead the

organization to sustainable success. ....................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management Accounting is defined as expertise of financial data and advice company to

use for a company and its business development. This assignment is about management

accounting and its significance for an organisation’s success. It will provide the meaning and

essential requirements of various types of management accounting techniques with their benefits.

The present report will study different accounting reports and their implementation in an

organization, i.e. Williams Performance Tenders which is the boat manufacturing company

which was founded in the year of 1979. It would be discussing about various advantage and

disadvantages of its planning tools in efficient manner.

Later, it will provide a profound analysis of marginal and absorption costing methods

with their income statements and interpretations for an insight about company’s overall growth.

The report will present significance of break-even analysis. This assignment will consist of

numerous advantages and disadvantages of planning tools with its applications. Along with this,

the overall impact on the decision-making process of a company.

TASK 1

A. Meaning of management accounting and essential requirements of different types of

management accounting systems

Management accounting includes preparation of managerial reports and accounts serving

to give accurate and precise financial and statistical data to the managers of organizations which

is required for decision-making. The major role played by it includes planning, organizing,

judgement creation, controlling in an organization (Ax and Greve, 2017).

Management accounting provides effective information from Williams Performance

Tenders so that manager can utilize this information and take better decisions to integrate it in

every level of an organization. It is provided only to management as internal decisions are taken

and thus, shortcomings can be eradicated with ease.

Such accounting is a useful tool for company because it serves decision making and leads

to an increased efficiency of functions of management. It also helps in fixing target and prices of

the products (Management Accounting: Meaning, Functions and Characteristics, 2017).

1

Management Accounting is defined as expertise of financial data and advice company to

use for a company and its business development. This assignment is about management

accounting and its significance for an organisation’s success. It will provide the meaning and

essential requirements of various types of management accounting techniques with their benefits.

The present report will study different accounting reports and their implementation in an

organization, i.e. Williams Performance Tenders which is the boat manufacturing company

which was founded in the year of 1979. It would be discussing about various advantage and

disadvantages of its planning tools in efficient manner.

Later, it will provide a profound analysis of marginal and absorption costing methods

with their income statements and interpretations for an insight about company’s overall growth.

The report will present significance of break-even analysis. This assignment will consist of

numerous advantages and disadvantages of planning tools with its applications. Along with this,

the overall impact on the decision-making process of a company.

TASK 1

A. Meaning of management accounting and essential requirements of different types of

management accounting systems

Management accounting includes preparation of managerial reports and accounts serving

to give accurate and precise financial and statistical data to the managers of organizations which

is required for decision-making. The major role played by it includes planning, organizing,

judgement creation, controlling in an organization (Ax and Greve, 2017).

Management accounting provides effective information from Williams Performance

Tenders so that manager can utilize this information and take better decisions to integrate it in

every level of an organization. It is provided only to management as internal decisions are taken

and thus, shortcomings can be eradicated with ease.

Such accounting is a useful tool for company because it serves decision making and leads

to an increased efficiency of functions of management. It also helps in fixing target and prices of

the products (Management Accounting: Meaning, Functions and Characteristics, 2017).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Requirements of different types of management accounting systems are explained below and

are used by William Performance Tenders:

Cost Accounting Systems

Inventory Management System

Job Costing System

Price Optimization System

The requirements of each system are listed below:

Cost accounting system

This is used to identify the cost of each product or service. In the process of production,

such accounting system aids to develop efficiency to minimize the cost. This helps in more

production. Therefore, it supports to initiate control over various types of costs such as direct,

indirect, fixed, variable and semi-variable quite successfully.

Inventory management system

This system has many benefits for William Performance Tenders. It reduces over

exploitation of resources to a certain level. Further, with the help of inventory management

system, no excess inventory is ordered that reduces amount of the expenses in operative means.

It is requisite so that business may be capable to attain maximum production and fulfilling

customers’ orders with ease.

Job costing system

It is also an impelling method to examine cost incurred on different manufacturing jobs.

It is fundamentally needed to evaluate costs so that it could be reduced for gaining production at

low cost. It assists Williams Performance Tenders to control costs and supports their

management for suitable distribution of jobs. This efficaciously assist to cut down costs and thus,

business is able to accomplish production timely. Hence, job costing accounting system has

plenty of benefits to company in achieving production and met demand of customers quite

effectually.

Price optimizing systems

It is a system that helps to identify the best possible price to be quoted for production. In

this system, it provides opportunities to concentrate on various goals. Firm takes into account

consideration of customers’ and quote less price for products and services (Cooper, Ezzamel and

1

are used by William Performance Tenders:

Cost Accounting Systems

Inventory Management System

Job Costing System

Price Optimization System

The requirements of each system are listed below:

Cost accounting system

This is used to identify the cost of each product or service. In the process of production,

such accounting system aids to develop efficiency to minimize the cost. This helps in more

production. Therefore, it supports to initiate control over various types of costs such as direct,

indirect, fixed, variable and semi-variable quite successfully.

Inventory management system

This system has many benefits for William Performance Tenders. It reduces over

exploitation of resources to a certain level. Further, with the help of inventory management

system, no excess inventory is ordered that reduces amount of the expenses in operative means.

It is requisite so that business may be capable to attain maximum production and fulfilling

customers’ orders with ease.

Job costing system

It is also an impelling method to examine cost incurred on different manufacturing jobs.

It is fundamentally needed to evaluate costs so that it could be reduced for gaining production at

low cost. It assists Williams Performance Tenders to control costs and supports their

management for suitable distribution of jobs. This efficaciously assist to cut down costs and thus,

business is able to accomplish production timely. Hence, job costing accounting system has

plenty of benefits to company in achieving production and met demand of customers quite

effectually.

Price optimizing systems

It is a system that helps to identify the best possible price to be quoted for production. In

this system, it provides opportunities to concentrate on various goals. Firm takes into account

consideration of customers’ and quote less price for products and services (Cooper, Ezzamel and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qu, 2017). Williams Performance Tenders uses this technique for setting the best prices of

goods.

B. Explanation of Different Management Accounting Reports

Management accounting is also known as managerial accounting. It focuses on internal

information of organization which is obtained from their financial accounting. These reports are

used for all the amendable regulations and measurable parameters for the overall growth and

development of Williams Performance Tenders. These reports are generated throughout the

accounting period to assist management in taking decisions.

Some essential reports of management accounting are listed below.

Budget reports

This report of management accounting is generated as a whole for small businesses

especially department wise. Budget reports are critical in measuring the performance of a

company. However, to understand the grand scheme for their business, each organization

implements an overall budget. It is prepared by keeping all the circumstances in mind which may

arise throughout the year. The establishment's budget lists several sources of earnings and

expenditures.

Account receivable aging reports

The Accounts Receivables Aging Reports are vital for this company which relies heavily

on extending credits. These reports are beneficial as they allow specifying the remaining

balances and also to identify defaulters in specific time period. In case of many defaulters, the

company may need a complete transformation of its credit policies (Accounts receivable aging

report. 2018). It is prepared to recover outstanding money from credit customers’ so that

operational tasks can be performed quickly by company. If funds remain outstanding for long

time, then it is required that strict credit policies should be implemented by which amount is

recovered within stipulated time. Thus, it helps company to prepare such report and thus, clarity

is observed for remaining amount to be recovered from debtors.

Cost managerial accounting reports

Cost of articles that are manufactured are computed by the management accounting. All

raw material costs, overhead, labour and any added costs are taken into consideration. This

2

goods.

B. Explanation of Different Management Accounting Reports

Management accounting is also known as managerial accounting. It focuses on internal

information of organization which is obtained from their financial accounting. These reports are

used for all the amendable regulations and measurable parameters for the overall growth and

development of Williams Performance Tenders. These reports are generated throughout the

accounting period to assist management in taking decisions.

Some essential reports of management accounting are listed below.

Budget reports

This report of management accounting is generated as a whole for small businesses

especially department wise. Budget reports are critical in measuring the performance of a

company. However, to understand the grand scheme for their business, each organization

implements an overall budget. It is prepared by keeping all the circumstances in mind which may

arise throughout the year. The establishment's budget lists several sources of earnings and

expenditures.

Account receivable aging reports

The Accounts Receivables Aging Reports are vital for this company which relies heavily

on extending credits. These reports are beneficial as they allow specifying the remaining

balances and also to identify defaulters in specific time period. In case of many defaulters, the

company may need a complete transformation of its credit policies (Accounts receivable aging

report. 2018). It is prepared to recover outstanding money from credit customers’ so that

operational tasks can be performed quickly by company. If funds remain outstanding for long

time, then it is required that strict credit policies should be implemented by which amount is

recovered within stipulated time. Thus, it helps company to prepare such report and thus, clarity

is observed for remaining amount to be recovered from debtors.

Cost managerial accounting reports

Cost of articles that are manufactured are computed by the management accounting. All

raw material costs, overhead, labour and any added costs are taken into consideration. This

2

report helps managers to classify the cost price of products and services with respect to its selling

price. The margins for the profits are identified with help of these reports.

Performance reports

This report is basically to review the performance of Williams Performance Tenders as

well as employees at the end of accounting year. In large organizations, departments

performance reports are also generated which measures and identifies the performance of each

department of the company (Performance report. 2018). To take the key strategic decisions

about the future of the organization, managers utilize such report. Performance-related

managerial accounting reports also offer an insight into the working of a company.

Other managerial reports

There are some more reports which are essential for business such as order information

reports, project reports, competitor’s analysis etc. (Eldenburg and et.al., 2016). They are either

created internally or outsourced through professionals.

These reports are required for an up-to-date and reliable manner so that decision-making

can be made by relying on such information. Moreover, any deviations are analysed in company

that could be effectively handled by taking corrective actions and as such, overall performance

can be judged in a better way. Management is able to take better decisions by assessing such

managerial reports to enhance performance of firm and increase financial standing by enriching

internal operations.

3

price. The margins for the profits are identified with help of these reports.

Performance reports

This report is basically to review the performance of Williams Performance Tenders as

well as employees at the end of accounting year. In large organizations, departments

performance reports are also generated which measures and identifies the performance of each

department of the company (Performance report. 2018). To take the key strategic decisions

about the future of the organization, managers utilize such report. Performance-related

managerial accounting reports also offer an insight into the working of a company.

Other managerial reports

There are some more reports which are essential for business such as order information

reports, project reports, competitor’s analysis etc. (Eldenburg and et.al., 2016). They are either

created internally or outsourced through professionals.

These reports are required for an up-to-date and reliable manner so that decision-making

can be made by relying on such information. Moreover, any deviations are analysed in company

that could be effectively handled by taking corrective actions and as such, overall performance

can be judged in a better way. Management is able to take better decisions by assessing such

managerial reports to enhance performance of firm and increase financial standing by enriching

internal operations.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

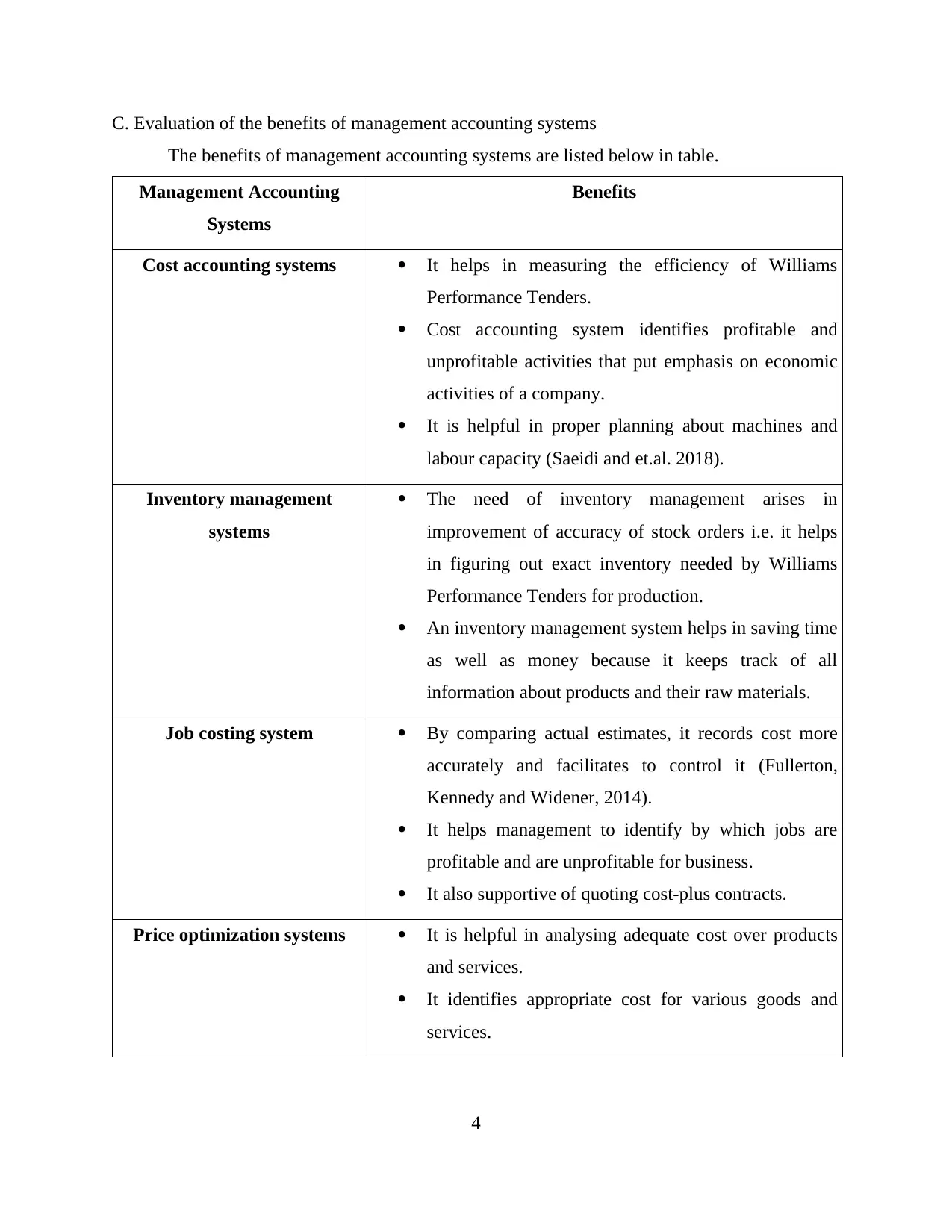

C. Evaluation of the benefits of management accounting systems

The benefits of management accounting systems are listed below in table.

Management Accounting

Systems

Benefits

Cost accounting systems It helps in measuring the efficiency of Williams

Performance Tenders.

Cost accounting system identifies profitable and

unprofitable activities that put emphasis on economic

activities of a company.

It is helpful in proper planning about machines and

labour capacity (Saeidi and et.al. 2018).

Inventory management

systems

The need of inventory management arises in

improvement of accuracy of stock orders i.e. it helps

in figuring out exact inventory needed by Williams

Performance Tenders for production.

An inventory management system helps in saving time

as well as money because it keeps track of all

information about products and their raw materials.

Job costing system By comparing actual estimates, it records cost more

accurately and facilitates to control it (Fullerton,

Kennedy and Widener, 2014).

It helps management to identify by which jobs are

profitable and are unprofitable for business.

It also supportive of quoting cost-plus contracts.

Price optimization systems It is helpful in analysing adequate cost over products

and services.

It identifies appropriate cost for various goods and

services.

4

The benefits of management accounting systems are listed below in table.

Management Accounting

Systems

Benefits

Cost accounting systems It helps in measuring the efficiency of Williams

Performance Tenders.

Cost accounting system identifies profitable and

unprofitable activities that put emphasis on economic

activities of a company.

It is helpful in proper planning about machines and

labour capacity (Saeidi and et.al. 2018).

Inventory management

systems

The need of inventory management arises in

improvement of accuracy of stock orders i.e. it helps

in figuring out exact inventory needed by Williams

Performance Tenders for production.

An inventory management system helps in saving time

as well as money because it keeps track of all

information about products and their raw materials.

Job costing system By comparing actual estimates, it records cost more

accurately and facilitates to control it (Fullerton,

Kennedy and Widener, 2014).

It helps management to identify by which jobs are

profitable and are unprofitable for business.

It also supportive of quoting cost-plus contracts.

Price optimization systems It is helpful in analysing adequate cost over products

and services.

It identifies appropriate cost for various goods and

services.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D. Integration of management accounting system and reports are developed in organization

There are various components in integrated management accounting systems that benefit

Williams Performance Tender for effective decision making. It assists in the reduction of

duplication of works, saves time and control unnecessary expenditures. Moreover, such

integration helps in providing data in time so that effective decisions can be done.

In recent times, computerized accounting is proved beneficial to firms which is time-

saving. Both systems provide a systematic data of organizations which is obtained from financial

accounting. The integration is required so that management may be able to effectively ascertain

reports and calculate decisions to enhance the overall performance with ease (Kihn and Ihantola,

2015).

TASK 2

A. 1 Explaining absorption costing and marginal costing methods.

Absorption costing

It is a method of accounting for valuing inventory. It adsorbs all cost which is used in

manufacturing of goods and services including fix and variable cost. It offers exact view of cost

that how much it relies in the production of goods and services. It is contrasted by direct costing

or variable costing. It is a technique which is used for recognizing cost and profits. Hence, it is

also known as a full costing technique. It determines all the practices under which fixed and

variable cost are converted into processes and operations. These techniques collect cost which

are associated with production and distribute them in an individual part. It accumulates the cost

of process of manufacturing.

Marginal costing

To find out the total cost of production, management uses marginal costing techniques for

decision-making (Fullerton, Kennedy and Widener, 2014). This technique differentiates both

fixed and variable cost. For managerial decision-making, it presents the data where fixed and

variable cost are shown individually. The marginal cost is the cost of one additional unit. While

valuing the finished goods and work in progress, variable cost is taken into consideration at the

time of valuation of stock. Behaviour of cost leads the concept of marginal accounting. It is also

known as variable costing because it takes only variable expenses into account at the time of

production.

5

There are various components in integrated management accounting systems that benefit

Williams Performance Tender for effective decision making. It assists in the reduction of

duplication of works, saves time and control unnecessary expenditures. Moreover, such

integration helps in providing data in time so that effective decisions can be done.

In recent times, computerized accounting is proved beneficial to firms which is time-

saving. Both systems provide a systematic data of organizations which is obtained from financial

accounting. The integration is required so that management may be able to effectively ascertain

reports and calculate decisions to enhance the overall performance with ease (Kihn and Ihantola,

2015).

TASK 2

A. 1 Explaining absorption costing and marginal costing methods.

Absorption costing

It is a method of accounting for valuing inventory. It adsorbs all cost which is used in

manufacturing of goods and services including fix and variable cost. It offers exact view of cost

that how much it relies in the production of goods and services. It is contrasted by direct costing

or variable costing. It is a technique which is used for recognizing cost and profits. Hence, it is

also known as a full costing technique. It determines all the practices under which fixed and

variable cost are converted into processes and operations. These techniques collect cost which

are associated with production and distribute them in an individual part. It accumulates the cost

of process of manufacturing.

Marginal costing

To find out the total cost of production, management uses marginal costing techniques for

decision-making (Fullerton, Kennedy and Widener, 2014). This technique differentiates both

fixed and variable cost. For managerial decision-making, it presents the data where fixed and

variable cost are shown individually. The marginal cost is the cost of one additional unit. While

valuing the finished goods and work in progress, variable cost is taken into consideration at the

time of valuation of stock. Behaviour of cost leads the concept of marginal accounting. It is also

known as variable costing because it takes only variable expenses into account at the time of

production.

5

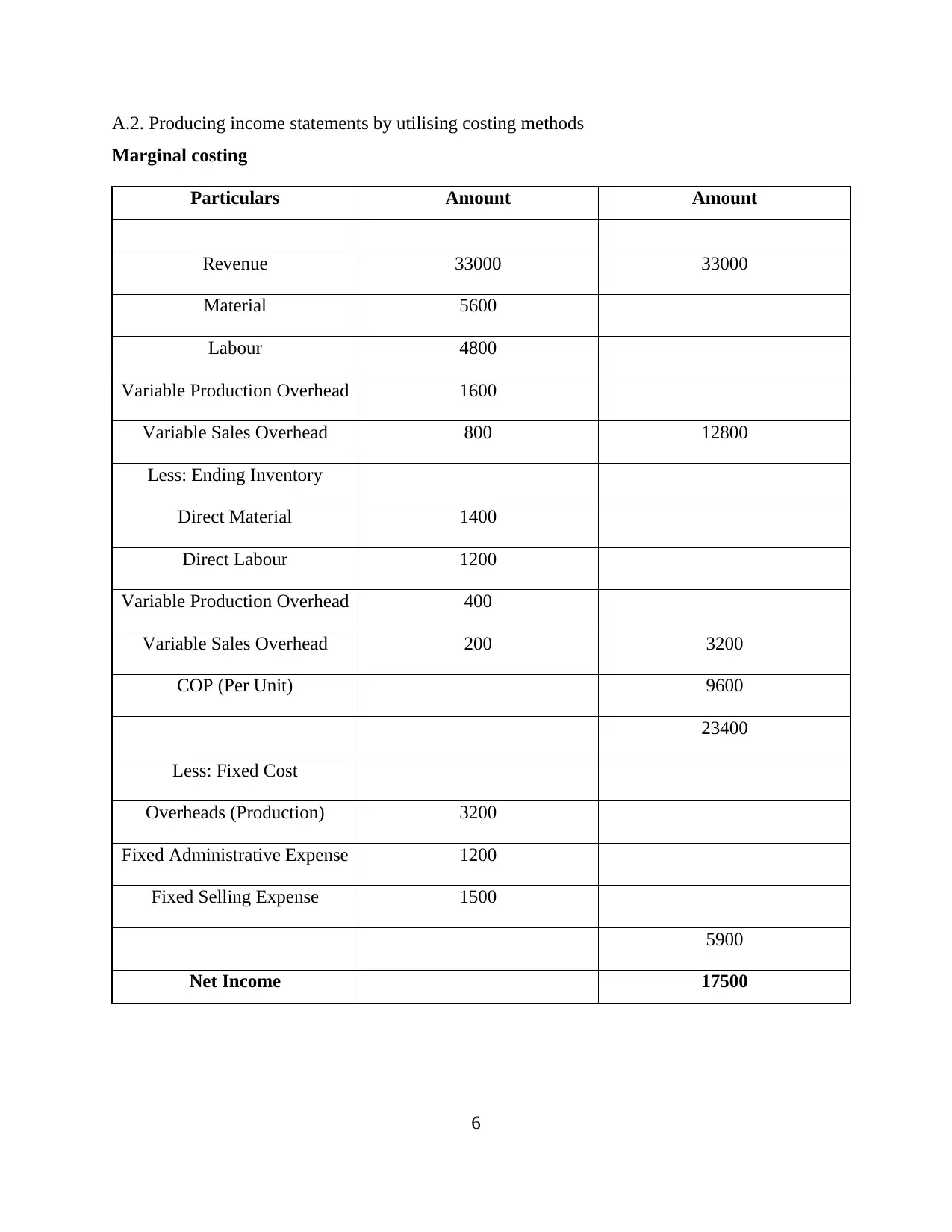

A.2. Producing income statements by utilising costing methods

Marginal costing

Particulars Amount Amount

Revenue 33000 33000

Material 5600

Labour 4800

Variable Production Overhead 1600

Variable Sales Overhead 800 12800

Less: Ending Inventory

Direct Material 1400

Direct Labour 1200

Variable Production Overhead 400

Variable Sales Overhead 200 3200

COP (Per Unit) 9600

23400

Less: Fixed Cost

Overheads (Production) 3200

Fixed Administrative Expense 1200

Fixed Selling Expense 1500

5900

Net Income 17500

6

Marginal costing

Particulars Amount Amount

Revenue 33000 33000

Material 5600

Labour 4800

Variable Production Overhead 1600

Variable Sales Overhead 800 12800

Less: Ending Inventory

Direct Material 1400

Direct Labour 1200

Variable Production Overhead 400

Variable Sales Overhead 200 3200

COP (Per Unit) 9600

23400

Less: Fixed Cost

Overheads (Production) 3200

Fixed Administrative Expense 1200

Fixed Selling Expense 1500

5900

Net Income 17500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

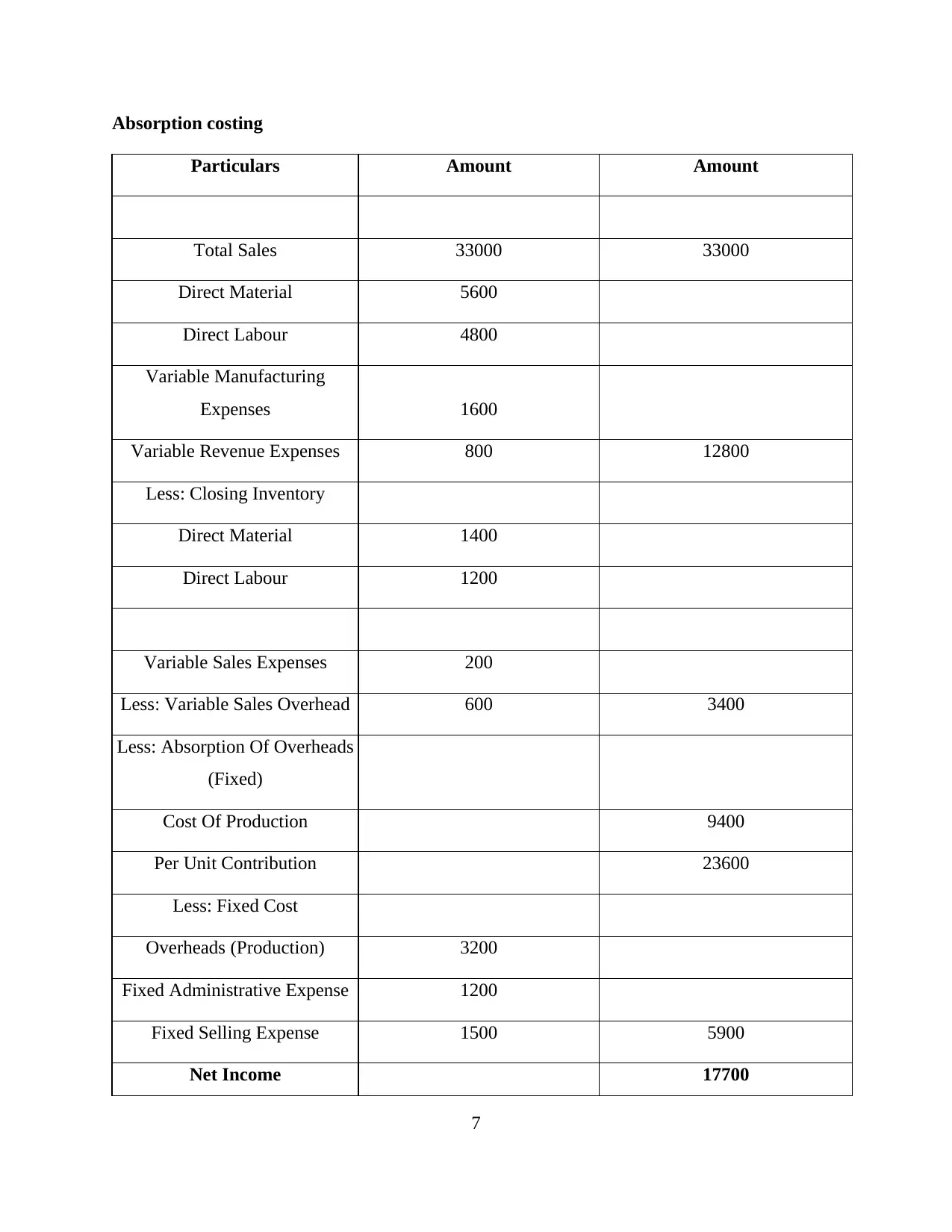

Absorption costing

Particulars Amount Amount

Total Sales 33000 33000

Direct Material 5600

Direct Labour 4800

Variable Manufacturing

Expenses 1600

Variable Revenue Expenses 800 12800

Less: Closing Inventory

Direct Material 1400

Direct Labour 1200

Variable Sales Expenses 200

Less: Variable Sales Overhead 600 3400

Less: Absorption Of Overheads

(Fixed)

Cost Of Production 9400

Per Unit Contribution 23600

Less: Fixed Cost

Overheads (Production) 3200

Fixed Administrative Expense 1200

Fixed Selling Expense 1500 5900

Net Income 17700

7

Particulars Amount Amount

Total Sales 33000 33000

Direct Material 5600

Direct Labour 4800

Variable Manufacturing

Expenses 1600

Variable Revenue Expenses 800 12800

Less: Closing Inventory

Direct Material 1400

Direct Labour 1200

Variable Sales Expenses 200

Less: Variable Sales Overhead 600 3400

Less: Absorption Of Overheads

(Fixed)

Cost Of Production 9400

Per Unit Contribution 23600

Less: Fixed Cost

Overheads (Production) 3200

Fixed Administrative Expense 1200

Fixed Selling Expense 1500 5900

Net Income 17700

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

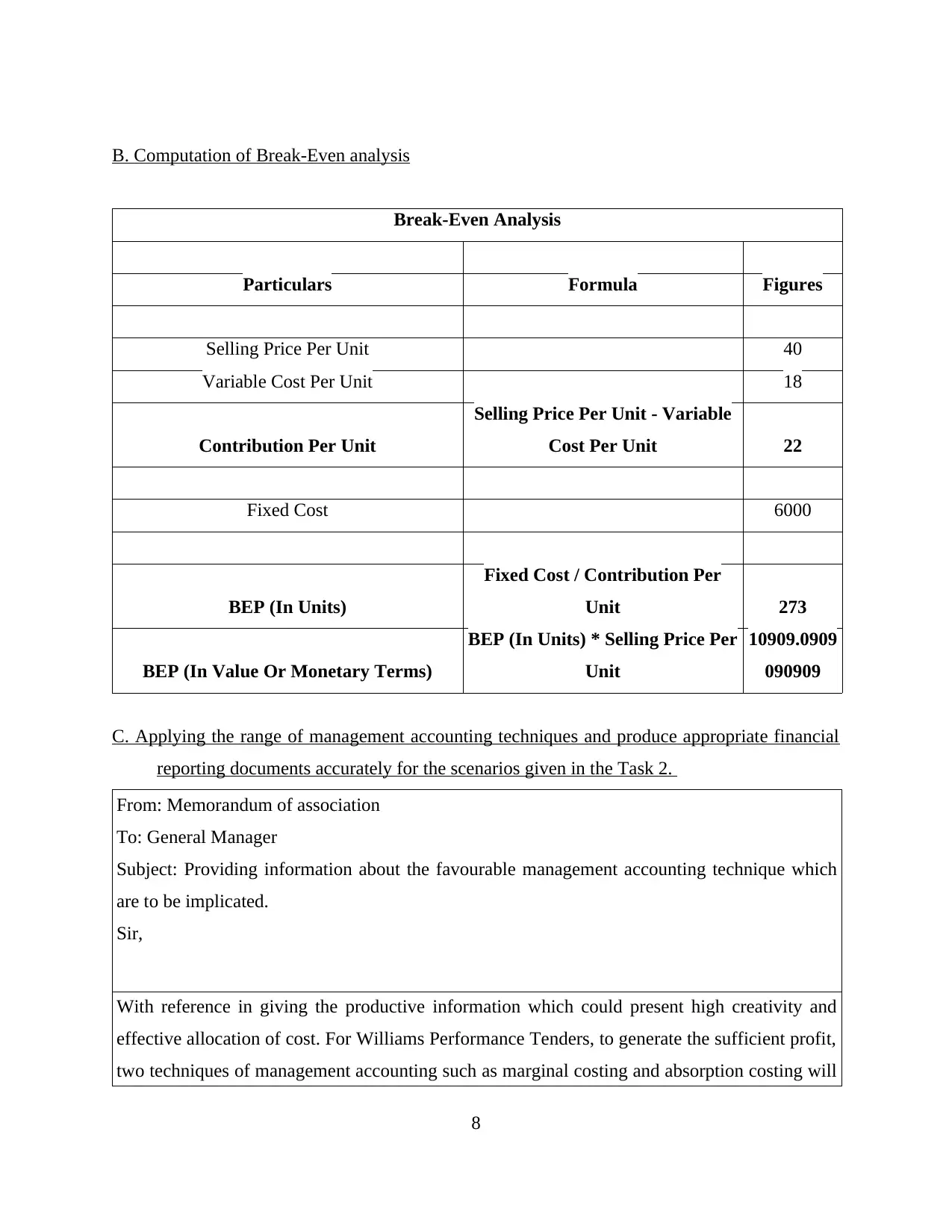

B. Computation of Break-Even analysis

Break-Even Analysis

Particulars Formula Figures

Selling Price Per Unit 40

Variable Cost Per Unit 18

Contribution Per Unit

Selling Price Per Unit - Variable

Cost Per Unit 22

Fixed Cost 6000

BEP (In Units)

Fixed Cost / Contribution Per

Unit 273

BEP (In Value Or Monetary Terms)

BEP (In Units) * Selling Price Per

Unit

10909.0909

090909

C. Applying the range of management accounting techniques and produce appropriate financial

reporting documents accurately for the scenarios given in the Task 2.

From: Memorandum of association

To: General Manager

Subject: Providing information about the favourable management accounting technique which

are to be implicated.

Sir,

With reference in giving the productive information which could present high creativity and

effective allocation of cost. For Williams Performance Tenders, to generate the sufficient profit,

two techniques of management accounting such as marginal costing and absorption costing will

8

Break-Even Analysis

Particulars Formula Figures

Selling Price Per Unit 40

Variable Cost Per Unit 18

Contribution Per Unit

Selling Price Per Unit - Variable

Cost Per Unit 22

Fixed Cost 6000

BEP (In Units)

Fixed Cost / Contribution Per

Unit 273

BEP (In Value Or Monetary Terms)

BEP (In Units) * Selling Price Per

Unit

10909.0909

090909

C. Applying the range of management accounting techniques and produce appropriate financial

reporting documents accurately for the scenarios given in the Task 2.

From: Memorandum of association

To: General Manager

Subject: Providing information about the favourable management accounting technique which

are to be implicated.

Sir,

With reference in giving the productive information which could present high creativity and

effective allocation of cost. For Williams Performance Tenders, to generate the sufficient profit,

two techniques of management accounting such as marginal costing and absorption costing will

8

help the system. Therefore, in this case the technique of absorption costing proves to be

beneficial because it consists of those all the cost incurred in the process on production.

Moreover, there are more methods which are proven to be beneficial for the Williams

Performance Tenders like

Cash Flow Statements with Historical Checking

Analysing Financial Accounts

Financial Accounting

Communicating Information

Review of Accounts

On comparing both the methods, it is seen that profit obtained from the marginal costing

technique is comparatively lower than other costing. It is highlighted that in absorption costing,

Williams Performance Tenders had a profit of $17700 than in marginal costing which was of

$17500. Hence, it can be concluded by saying that absorption costing will be more fruitful than

marginal. As it is a full costing method and shows the relevant profit for organization by

absorbing all costs. In marginal costing, it only takes fixed expenses into account to ascertain

the profits.

There are some reporting techniques which management should adopt like -

Cash Flows

Start-up Costing

Balance Sheet

Budget and Forecast Table

Thank you

9

beneficial because it consists of those all the cost incurred in the process on production.

Moreover, there are more methods which are proven to be beneficial for the Williams

Performance Tenders like

Cash Flow Statements with Historical Checking

Analysing Financial Accounts

Financial Accounting

Communicating Information

Review of Accounts

On comparing both the methods, it is seen that profit obtained from the marginal costing

technique is comparatively lower than other costing. It is highlighted that in absorption costing,

Williams Performance Tenders had a profit of $17700 than in marginal costing which was of

$17500. Hence, it can be concluded by saying that absorption costing will be more fruitful than

marginal. As it is a full costing method and shows the relevant profit for organization by

absorbing all costs. In marginal costing, it only takes fixed expenses into account to ascertain

the profits.

There are some reporting techniques which management should adopt like -

Cash Flows

Start-up Costing

Balance Sheet

Budget and Forecast Table

Thank you

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.