Detailed Management Accounting Report and Analysis for Bizdaq

VerifiedAdded on 2020/06/03

|18

|4935

|321

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their practical application, using Bizdaq as a case study. It explores essential requirements of different management accounting systems, including inventory management, price optimization, job costing, and cost accounting systems. The report details various methods used for management accounting reporting, such as budget reports, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, and income statement reports. It also delves into cost calculation techniques, specifically marginal and absorption costing, and formulates an income statement. Furthermore, the report examines the advantages and disadvantages of different planning tools used for budgetary control and discusses how organizations adapt management accounting systems to respond to financial problems. The report concludes with a synthesis of the findings and recommendations for Bizdaq.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P2 Various methods used for management accounting reporting ..............................................3

TASK 2............................................................................................................................................6

P3 Calculate of costs by using appropriate techniques of cost analysis for formulating an

income statement using marginal and absorption costs..............................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

P5 Ways through organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P2 Various methods used for management accounting reporting ..............................................3

TASK 2............................................................................................................................................6

P3 Calculate of costs by using appropriate techniques of cost analysis for formulating an

income statement using marginal and absorption costs..............................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

P5 Ways through organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management can be stated as a process in which there are certain guidelines which are

being utilised by the managers in order to monitor accounting of data so that decision-making

process can be much more effective. There are various steps and plans which are being involved

in the process of management accounting (Management accounting, 2017.). This process is

highly involved in gaining proficiency while creating reports regarding finance for supporting

the management. Company chosen for this report is Bizdaq which was established in the year

2015 and since then, they have been dealing in sales projects. Moreover, company’s turnover is

approx. £100,000 and it compiles of less than 50 staff members. There are certain things which

are being discussed in this report like understanding of management accounting systems and

implementation of management accounting techniques. Apart from that, there are various tools

which are being utilised planning techniques in management accounting so that aims and

objectives can be attained in effective manner of firm.

TASK 1

P1. Management accounting and essential requirements of different types of management

accounting systems

Management accounting system can be stated as a process in which motivation is being

provided to employees so that they can be involved in the decision making process. This kind of

process is highly essential and beneficial for the leaders as support is being provided to them

while planning and performance management system. While making financial reports, expertise

is being required in management accounting system.

Below shown is the diagram which explains various kinds of management accounting

systems:

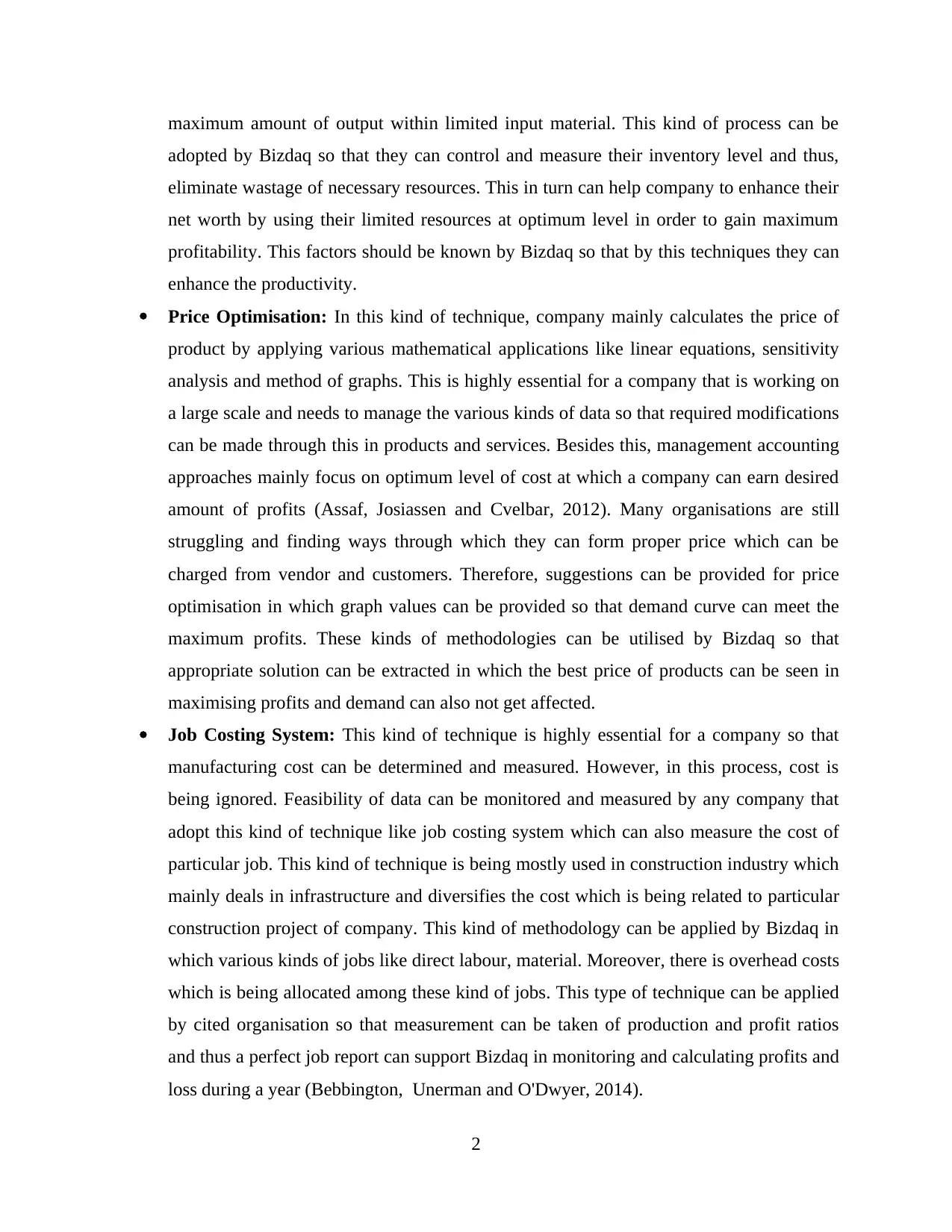

Inventory Management System: In this kind of management accounting system, the

main focus is on dealing with raw materials, methodologies and finished goods and thus,

they are being used in process of production by an organisation. There is high need of

managing the stock and therefore, various kinds of stock management software tools are

needed so that measurement can be taken of level of stock, number of orders as well as

sales and delivery of products (Armstrong and Taylor, 2014). This kind of software is

needed the manufacturing firms so that their process can be controlled for obtaining

1

Management can be stated as a process in which there are certain guidelines which are

being utilised by the managers in order to monitor accounting of data so that decision-making

process can be much more effective. There are various steps and plans which are being involved

in the process of management accounting (Management accounting, 2017.). This process is

highly involved in gaining proficiency while creating reports regarding finance for supporting

the management. Company chosen for this report is Bizdaq which was established in the year

2015 and since then, they have been dealing in sales projects. Moreover, company’s turnover is

approx. £100,000 and it compiles of less than 50 staff members. There are certain things which

are being discussed in this report like understanding of management accounting systems and

implementation of management accounting techniques. Apart from that, there are various tools

which are being utilised planning techniques in management accounting so that aims and

objectives can be attained in effective manner of firm.

TASK 1

P1. Management accounting and essential requirements of different types of management

accounting systems

Management accounting system can be stated as a process in which motivation is being

provided to employees so that they can be involved in the decision making process. This kind of

process is highly essential and beneficial for the leaders as support is being provided to them

while planning and performance management system. While making financial reports, expertise

is being required in management accounting system.

Below shown is the diagram which explains various kinds of management accounting

systems:

Inventory Management System: In this kind of management accounting system, the

main focus is on dealing with raw materials, methodologies and finished goods and thus,

they are being used in process of production by an organisation. There is high need of

managing the stock and therefore, various kinds of stock management software tools are

needed so that measurement can be taken of level of stock, number of orders as well as

sales and delivery of products (Armstrong and Taylor, 2014). This kind of software is

needed the manufacturing firms so that their process can be controlled for obtaining

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maximum amount of output within limited input material. This kind of process can be

adopted by Bizdaq so that they can control and measure their inventory level and thus,

eliminate wastage of necessary resources. This in turn can help company to enhance their

net worth by using their limited resources at optimum level in order to gain maximum

profitability. This factors should be known by Bizdaq so that by this techniques they can

enhance the productivity.

Price Optimisation: In this kind of technique, company mainly calculates the price of

product by applying various mathematical applications like linear equations, sensitivity

analysis and method of graphs. This is highly essential for a company that is working on

a large scale and needs to manage the various kinds of data so that required modifications

can be made through this in products and services. Besides this, management accounting

approaches mainly focus on optimum level of cost at which a company can earn desired

amount of profits (Assaf, Josiassen and Cvelbar, 2012). Many organisations are still

struggling and finding ways through which they can form proper price which can be

charged from vendor and customers. Therefore, suggestions can be provided for price

optimisation in which graph values can be provided so that demand curve can meet the

maximum profits. These kinds of methodologies can be utilised by Bizdaq so that

appropriate solution can be extracted in which the best price of products can be seen in

maximising profits and demand can also not get affected.

Job Costing System: This kind of technique is highly essential for a company so that

manufacturing cost can be determined and measured. However, in this process, cost is

being ignored. Feasibility of data can be monitored and measured by any company that

adopt this kind of technique like job costing system which can also measure the cost of

particular job. This kind of technique is being mostly used in construction industry which

mainly deals in infrastructure and diversifies the cost which is being related to particular

construction project of company. This kind of methodology can be applied by Bizdaq in

which various kinds of jobs like direct labour, material. Moreover, there is overhead costs

which is being allocated among these kind of jobs. This type of technique can be applied

by cited organisation so that measurement can be taken of production and profit ratios

and thus a perfect job report can support Bizdaq in monitoring and calculating profits and

loss during a year (Bebbington, Unerman and O'Dwyer, 2014).

2

adopted by Bizdaq so that they can control and measure their inventory level and thus,

eliminate wastage of necessary resources. This in turn can help company to enhance their

net worth by using their limited resources at optimum level in order to gain maximum

profitability. This factors should be known by Bizdaq so that by this techniques they can

enhance the productivity.

Price Optimisation: In this kind of technique, company mainly calculates the price of

product by applying various mathematical applications like linear equations, sensitivity

analysis and method of graphs. This is highly essential for a company that is working on

a large scale and needs to manage the various kinds of data so that required modifications

can be made through this in products and services. Besides this, management accounting

approaches mainly focus on optimum level of cost at which a company can earn desired

amount of profits (Assaf, Josiassen and Cvelbar, 2012). Many organisations are still

struggling and finding ways through which they can form proper price which can be

charged from vendor and customers. Therefore, suggestions can be provided for price

optimisation in which graph values can be provided so that demand curve can meet the

maximum profits. These kinds of methodologies can be utilised by Bizdaq so that

appropriate solution can be extracted in which the best price of products can be seen in

maximising profits and demand can also not get affected.

Job Costing System: This kind of technique is highly essential for a company so that

manufacturing cost can be determined and measured. However, in this process, cost is

being ignored. Feasibility of data can be monitored and measured by any company that

adopt this kind of technique like job costing system which can also measure the cost of

particular job. This kind of technique is being mostly used in construction industry which

mainly deals in infrastructure and diversifies the cost which is being related to particular

construction project of company. This kind of methodology can be applied by Bizdaq in

which various kinds of jobs like direct labour, material. Moreover, there is overhead costs

which is being allocated among these kind of jobs. This type of technique can be applied

by cited organisation so that measurement can be taken of production and profit ratios

and thus a perfect job report can support Bizdaq in monitoring and calculating profits and

loss during a year (Bebbington, Unerman and O'Dwyer, 2014).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost Accounting System: This type of technique can be stated as product cots system. It

is highly essential for a company because it determines and describes the structure of

finance by calculating various costs incurred. Support is being provided to company in

setting up of estimates cost budgets for the very next financial year. It provides guidance

to company in choosing the best method of accounting for calculating cost of product and

profits. This kind of methodology can be applied to Bizdaq in order to make smooth

running for the entire financial year. Company should refer marginal costing and

absorption costing methods for evaluating and analysing net earnings during year. For

example: in the given scenario, the budgeted cost of production expense, administration

and selling cost were determined by this type of approach.

P2 Various methods used for management accounting reporting

This kind of management accounting report helps the process of business to determine

functions and operations of business. There is difference between management accounting and

financial accounting as they prepare reports for the internal company along with external

stakeholders. This has to be produced in periodically basis so that current status and financial

performance of company can be measured and monitored. The main role of management

accounting is to provide support to managers by providing them financial and statistical status on

time so that day to day operations can be conducted in a smooth manner along with short term

decisions (Bellandi, 2012). The reports which are being generated by management accounting

are highly confidential and only obtained for internal use which are in opposition to financial

accounting statements which are being reported in public.

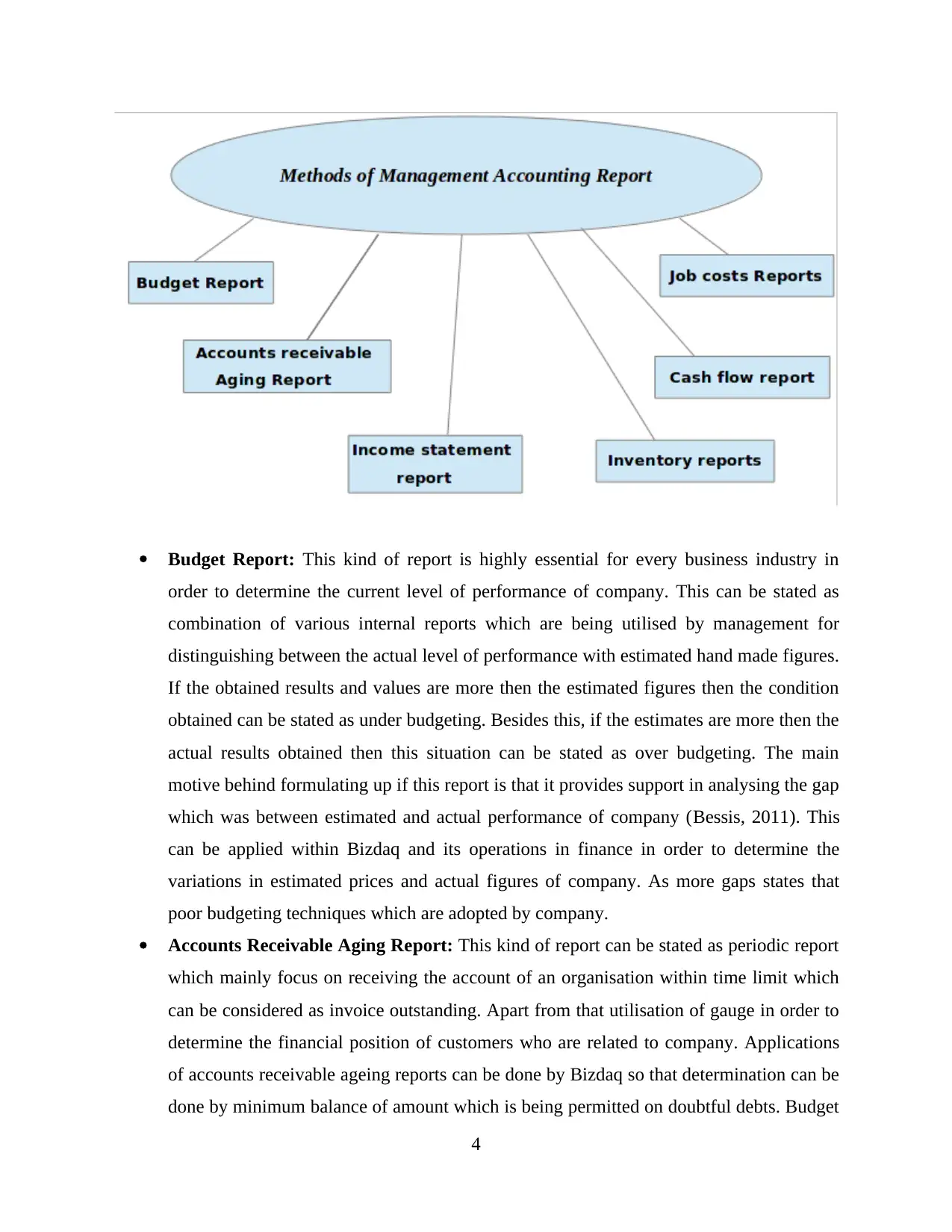

Below is the diagram which will explain different types of methods used in Management

Accounting Reports:

3

is highly essential for a company because it determines and describes the structure of

finance by calculating various costs incurred. Support is being provided to company in

setting up of estimates cost budgets for the very next financial year. It provides guidance

to company in choosing the best method of accounting for calculating cost of product and

profits. This kind of methodology can be applied to Bizdaq in order to make smooth

running for the entire financial year. Company should refer marginal costing and

absorption costing methods for evaluating and analysing net earnings during year. For

example: in the given scenario, the budgeted cost of production expense, administration

and selling cost were determined by this type of approach.

P2 Various methods used for management accounting reporting

This kind of management accounting report helps the process of business to determine

functions and operations of business. There is difference between management accounting and

financial accounting as they prepare reports for the internal company along with external

stakeholders. This has to be produced in periodically basis so that current status and financial

performance of company can be measured and monitored. The main role of management

accounting is to provide support to managers by providing them financial and statistical status on

time so that day to day operations can be conducted in a smooth manner along with short term

decisions (Bellandi, 2012). The reports which are being generated by management accounting

are highly confidential and only obtained for internal use which are in opposition to financial

accounting statements which are being reported in public.

Below is the diagram which will explain different types of methods used in Management

Accounting Reports:

3

Budget Report: This kind of report is highly essential for every business industry in

order to determine the current level of performance of company. This can be stated as

combination of various internal reports which are being utilised by management for

distinguishing between the actual level of performance with estimated hand made figures.

If the obtained results and values are more then the estimated figures then the condition

obtained can be stated as under budgeting. Besides this, if the estimates are more then the

actual results obtained then this situation can be stated as over budgeting. The main

motive behind formulating up if this report is that it provides support in analysing the gap

which was between estimated and actual performance of company (Bessis, 2011). This

can be applied within Bizdaq and its operations in finance in order to determine the

variations in estimated prices and actual figures of company. As more gaps states that

poor budgeting techniques which are adopted by company.

Accounts Receivable Aging Report: This kind of report can be stated as periodic report

which mainly focus on receiving the account of an organisation within time limit which

can be considered as invoice outstanding. Apart from that utilisation of gauge in order to

determine the financial position of customers who are related to company. Applications

of accounts receivable ageing reports can be done by Bizdaq so that determination can be

done by minimum balance of amount which is being permitted on doubtful debts. Budget

4

order to determine the current level of performance of company. This can be stated as

combination of various internal reports which are being utilised by management for

distinguishing between the actual level of performance with estimated hand made figures.

If the obtained results and values are more then the estimated figures then the condition

obtained can be stated as under budgeting. Besides this, if the estimates are more then the

actual results obtained then this situation can be stated as over budgeting. The main

motive behind formulating up if this report is that it provides support in analysing the gap

which was between estimated and actual performance of company (Bessis, 2011). This

can be applied within Bizdaq and its operations in finance in order to determine the

variations in estimated prices and actual figures of company. As more gaps states that

poor budgeting techniques which are adopted by company.

Accounts Receivable Aging Report: This kind of report can be stated as periodic report

which mainly focus on receiving the account of an organisation within time limit which

can be considered as invoice outstanding. Apart from that utilisation of gauge in order to

determine the financial position of customers who are related to company. Applications

of accounts receivable ageing reports can be done by Bizdaq so that determination can be

done by minimum balance of amount which is being permitted on doubtful debts. Budget

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

tools can be utilised by Bizdaq so that sales invoices can be sorted and thus better

position can be analysed (Bezhani, 2010).

Job costs Reports: It can be stated as process in which cost can be clarified which are

directly related to particular work of business process. This kind of process is mainly

used by constructing companies and they mostly allocate the cost of individual project of

construction project. This kind of technique can be applied by Bizdaq by creating various

kind of categories through which fund can be utilised and sorting can be done regrading

activities who utilise more funds. Best example can be stated as production, selling and

distribution cost of Bizdaq.

Inventory and manufacturing reports: This kind of management accounting mainly

consist of joining values of several stocks at three stages of productions and those are

manufacturing, whole-selling and retailing. It is highly needed by company as it consists

of sum of business sales at each three stages of production. This provide major benefits to

supervisors to maintain the management of stock, track the movement of products in

warehouse and list of several categories like items which are at hold and visible (Crippa

and et. al., 2010). This method should be applied by Bizdaq so resources can be

determined for integration of various kind of activities. Company can get support by this

report in counting cycle period and their deviation in data which is accessible on daily,

weekly and monthly purpose.

Income statement report: This kind of management accounting system mainly is

utilised by financial authorities to identify and calculate the profit which is being earned

during the financial year which is usually march end. This in turn helps out company to

determine the performance level by comparing with current and previous year income

statements. This method can be applied by Bizdaq in order to determine the profit along

with expense statements (Van Greuning, Scott and Terblanche, 2011). Company could

also know how much outstanding expenses, arrears and payments are due and

unidentified resources from which the left payment can be recovered in future time.

5

position can be analysed (Bezhani, 2010).

Job costs Reports: It can be stated as process in which cost can be clarified which are

directly related to particular work of business process. This kind of process is mainly

used by constructing companies and they mostly allocate the cost of individual project of

construction project. This kind of technique can be applied by Bizdaq by creating various

kind of categories through which fund can be utilised and sorting can be done regrading

activities who utilise more funds. Best example can be stated as production, selling and

distribution cost of Bizdaq.

Inventory and manufacturing reports: This kind of management accounting mainly

consist of joining values of several stocks at three stages of productions and those are

manufacturing, whole-selling and retailing. It is highly needed by company as it consists

of sum of business sales at each three stages of production. This provide major benefits to

supervisors to maintain the management of stock, track the movement of products in

warehouse and list of several categories like items which are at hold and visible (Crippa

and et. al., 2010). This method should be applied by Bizdaq so resources can be

determined for integration of various kind of activities. Company can get support by this

report in counting cycle period and their deviation in data which is accessible on daily,

weekly and monthly purpose.

Income statement report: This kind of management accounting system mainly is

utilised by financial authorities to identify and calculate the profit which is being earned

during the financial year which is usually march end. This in turn helps out company to

determine the performance level by comparing with current and previous year income

statements. This method can be applied by Bizdaq in order to determine the profit along

with expense statements (Van Greuning, Scott and Terblanche, 2011). Company could

also know how much outstanding expenses, arrears and payments are due and

unidentified resources from which the left payment can be recovered in future time.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P3 Calculate of costs by using appropriate techniques of cost analysis for

formulating an income statement using marginal and absorption costs

The main focus area of management accounting is on formulating

accurate reports and most essential element of the report is cost. Better

results can be obtained by using proper cost approach.

Marginal Costing: The main focus area is on incurring of extra

expenditure which company during extra generation of products and

services. The main focus of slim form of cost is on variable cost, if reduction

is done on variable expenditure then the price of certain goods can be

minimised which are present in stores. Thin turn can provide benefit to the

organisation and its managers like it can help them in making effective

decision-making process of cost related to products then the marginal cost

of product can be either increased or the same price can be continued for

process but if the commodity is low in nature, then the item will be less sold

among consumers (Kerzner, 2013). While calculating at final terms, fixed cost

is being considered in this situation which is in final stage.

Absorption Costing: This can be stated as traditional method in

which cost is being calculated. This kind of method can also be called full

costing method. The major benefit of utilising this kind of approach is that

shows the right path as it involves all the expenses which are incurred by

company. There are various kind of elements which are being included like

directly material, labour and upper (Laegreid and Christensen, 2013). There is no

kind of fluctuation in the fixed cost in this kind of method and certain price

is being allotted to every unit and if the cost is being added to final and total

amount in manufacturing then it all goes in marginal costs.

In order to calculate the absorption cost, conversion is being needed

in fixed overhead costs as per unit cost of production. Cost of standard

production is calculated through adding all per unit costs of production.

Below is the difference between Marginal costs and Absorption costs:

6

P3 Calculate of costs by using appropriate techniques of cost analysis for

formulating an income statement using marginal and absorption costs

The main focus area of management accounting is on formulating

accurate reports and most essential element of the report is cost. Better

results can be obtained by using proper cost approach.

Marginal Costing: The main focus area is on incurring of extra

expenditure which company during extra generation of products and

services. The main focus of slim form of cost is on variable cost, if reduction

is done on variable expenditure then the price of certain goods can be

minimised which are present in stores. Thin turn can provide benefit to the

organisation and its managers like it can help them in making effective

decision-making process of cost related to products then the marginal cost

of product can be either increased or the same price can be continued for

process but if the commodity is low in nature, then the item will be less sold

among consumers (Kerzner, 2013). While calculating at final terms, fixed cost

is being considered in this situation which is in final stage.

Absorption Costing: This can be stated as traditional method in

which cost is being calculated. This kind of method can also be called full

costing method. The major benefit of utilising this kind of approach is that

shows the right path as it involves all the expenses which are incurred by

company. There are various kind of elements which are being included like

directly material, labour and upper (Laegreid and Christensen, 2013). There is no

kind of fluctuation in the fixed cost in this kind of method and certain price

is being allotted to every unit and if the cost is being added to final and total

amount in manufacturing then it all goes in marginal costs.

In order to calculate the absorption cost, conversion is being needed

in fixed overhead costs as per unit cost of production. Cost of standard

production is calculated through adding all per unit costs of production.

Below is the difference between Marginal costs and Absorption costs:

6

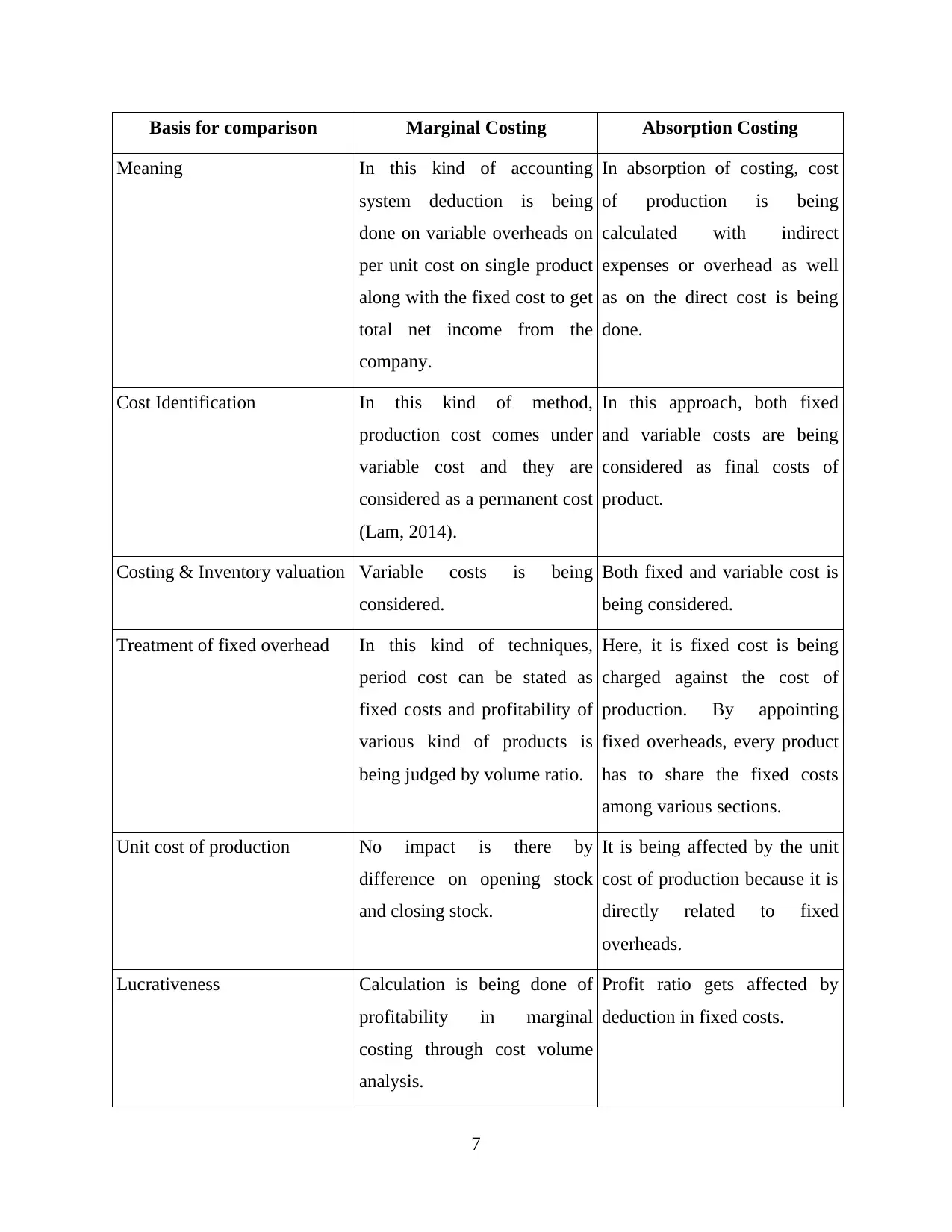

Basis for comparison Marginal Costing Absorption Costing

Meaning In this kind of accounting

system deduction is being

done on variable overheads on

per unit cost on single product

along with the fixed cost to get

total net income from the

company.

In absorption of costing, cost

of production is being

calculated with indirect

expenses or overhead as well

as on the direct cost is being

done.

Cost Identification In this kind of method,

production cost comes under

variable cost and they are

considered as a permanent cost

(Lam, 2014).

In this approach, both fixed

and variable costs are being

considered as final costs of

product.

Costing & Inventory valuation Variable costs is being

considered.

Both fixed and variable cost is

being considered.

Treatment of fixed overhead In this kind of techniques,

period cost can be stated as

fixed costs and profitability of

various kind of products is

being judged by volume ratio.

Here, it is fixed cost is being

charged against the cost of

production. By appointing

fixed overheads, every product

has to share the fixed costs

among various sections.

Unit cost of production No impact is there by

difference on opening stock

and closing stock.

It is being affected by the unit

cost of production because it is

directly related to fixed

overheads.

Lucrativeness Calculation is being done of

profitability in marginal

costing through cost volume

analysis.

Profit ratio gets affected by

deduction in fixed costs.

7

Meaning In this kind of accounting

system deduction is being

done on variable overheads on

per unit cost on single product

along with the fixed cost to get

total net income from the

company.

In absorption of costing, cost

of production is being

calculated with indirect

expenses or overhead as well

as on the direct cost is being

done.

Cost Identification In this kind of method,

production cost comes under

variable cost and they are

considered as a permanent cost

(Lam, 2014).

In this approach, both fixed

and variable costs are being

considered as final costs of

product.

Costing & Inventory valuation Variable costs is being

considered.

Both fixed and variable cost is

being considered.

Treatment of fixed overhead In this kind of techniques,

period cost can be stated as

fixed costs and profitability of

various kind of products is

being judged by volume ratio.

Here, it is fixed cost is being

charged against the cost of

production. By appointing

fixed overheads, every product

has to share the fixed costs

among various sections.

Unit cost of production No impact is there by

difference on opening stock

and closing stock.

It is being affected by the unit

cost of production because it is

directly related to fixed

overheads.

Lucrativeness Calculation is being done of

profitability in marginal

costing through cost volume

analysis.

Profit ratio gets affected by

deduction in fixed costs.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

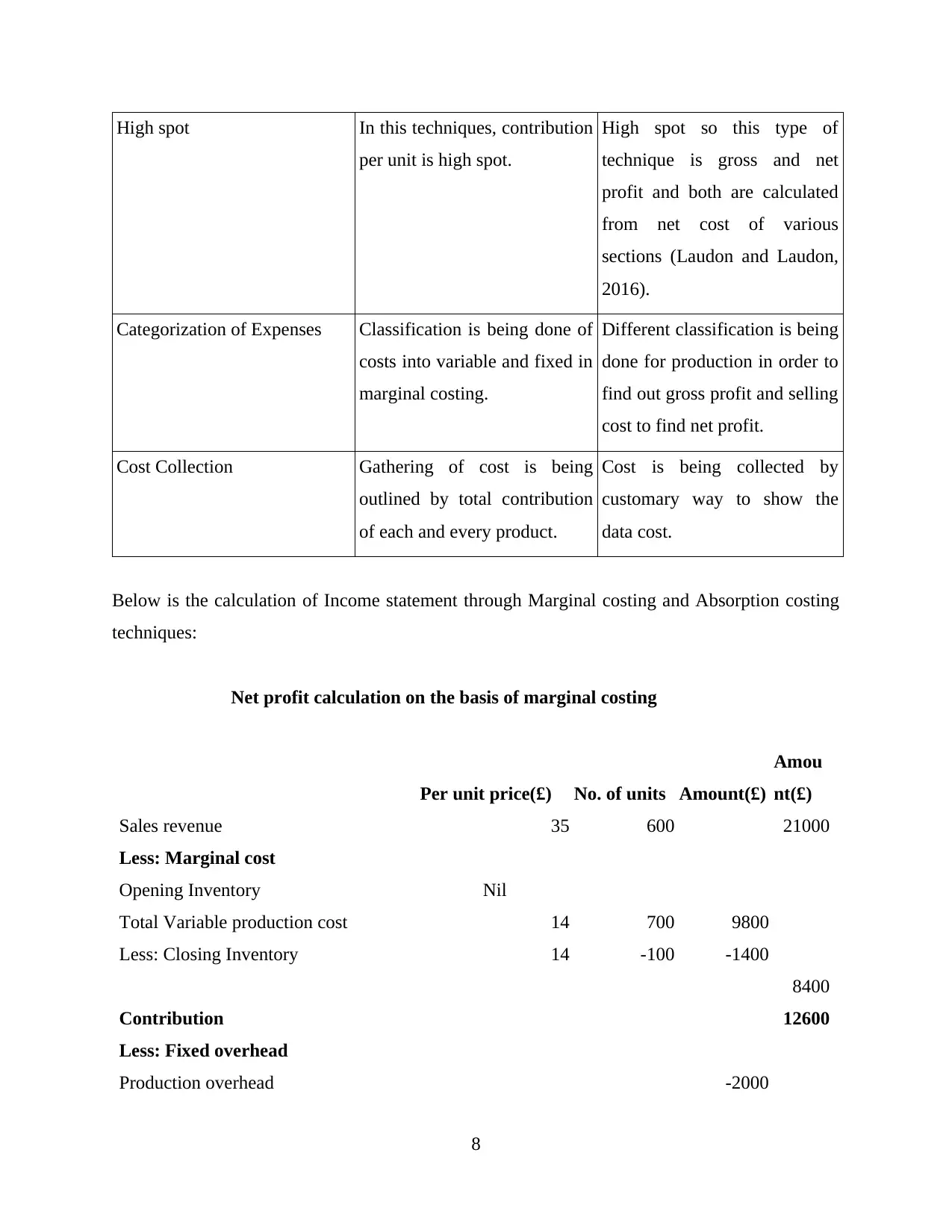

High spot In this techniques, contribution

per unit is high spot.

High spot so this type of

technique is gross and net

profit and both are calculated

from net cost of various

sections (Laudon and Laudon,

2016).

Categorization of Expenses Classification is being done of

costs into variable and fixed in

marginal costing.

Different classification is being

done for production in order to

find out gross profit and selling

cost to find net profit.

Cost Collection Gathering of cost is being

outlined by total contribution

of each and every product.

Cost is being collected by

customary way to show the

data cost.

Below is the calculation of Income statement through Marginal costing and Absorption costing

techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£)

Amou

nt(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

8

per unit is high spot.

High spot so this type of

technique is gross and net

profit and both are calculated

from net cost of various

sections (Laudon and Laudon,

2016).

Categorization of Expenses Classification is being done of

costs into variable and fixed in

marginal costing.

Different classification is being

done for production in order to

find out gross profit and selling

cost to find net profit.

Cost Collection Gathering of cost is being

outlined by total contribution

of each and every product.

Cost is being collected by

customary way to show the

data cost.

Below is the calculation of Income statement through Marginal costing and Absorption costing

techniques:

Net profit calculation on the basis of marginal costing

Per unit price(£) No. of units Amount(£)

Amou

nt(£)

Sales revenue 35 600 21000

Less: Marginal cost

Opening Inventory Nil

Total Variable production cost 14 700 9800

Less: Closing Inventory 14 -100 -1400

8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administration cost -700

Selling cost -600

-3300

Net Profit 9300

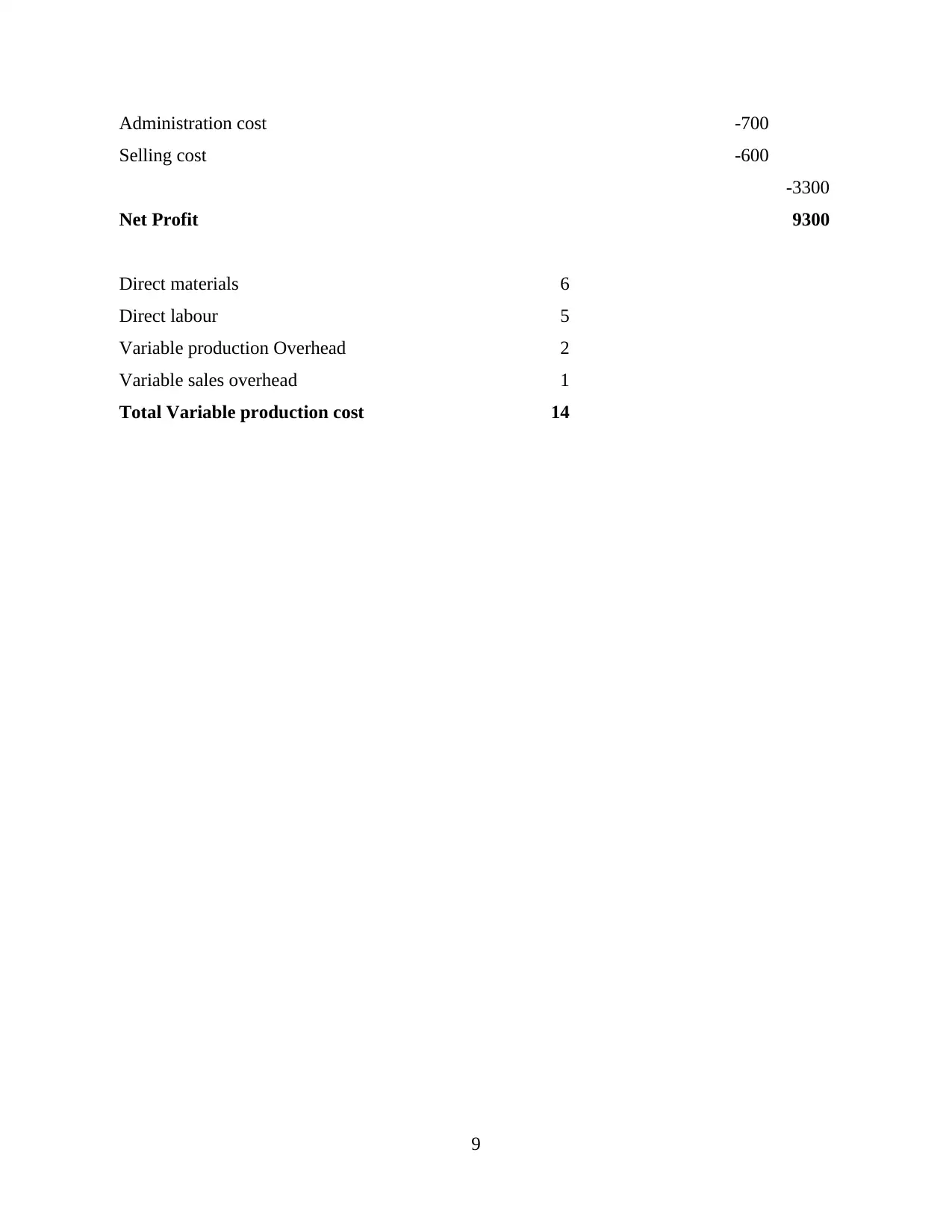

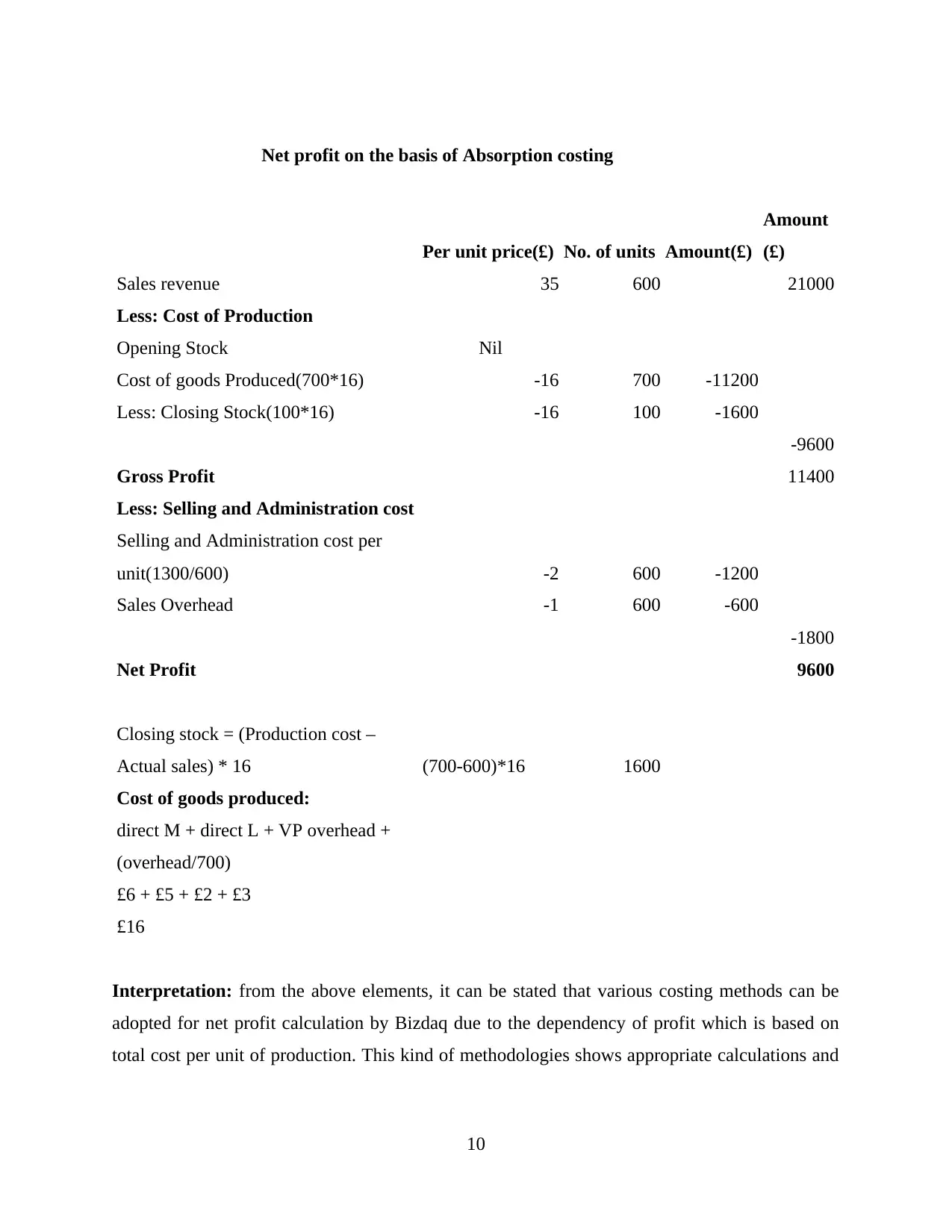

Direct materials 6

Direct labour 5

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

9

Selling cost -600

-3300

Net Profit 9300

Direct materials 6

Direct labour 5

Variable production Overhead 2

Variable sales overhead 1

Total Variable production cost 14

9

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£)

Amount

(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

£16

Interpretation: from the above elements, it can be stated that various costing methods can be

adopted for net profit calculation by Bizdaq due to the dependency of profit which is based on

total cost per unit of production. This kind of methodologies shows appropriate calculations and

10

Per unit price(£) No. of units Amount(£)

Amount

(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

Closing stock = (Production cost –

Actual sales) * 16 (700-600)*16 1600

Cost of goods produced:

direct M + direct L + VP overhead +

(overhead/700)

£6 + £5 + £2 + £3

£16

Interpretation: from the above elements, it can be stated that various costing methods can be

adopted for net profit calculation by Bizdaq due to the dependency of profit which is based on

total cost per unit of production. This kind of methodologies shows appropriate calculations and

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.