Rowlinson Knitwear: Analysis of Management Accounting Report

VerifiedAdded on 2020/10/22

|16

|5212

|359

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their practical application within Rowlinson Knitwear. It begins with an introduction to management accounting, its importance, and the essential requirements of a management accounting system, including different accounting systems like cost accounting and inventory management. The report then explores various management accounting reporting methods, such as performance reports and budget reports, along with their benefits. The core of the report delves into costing methods, comparing and contrasting absorption costing and marginal costing, and their implications for financial statements and decision-making. Furthermore, the report examines planning tools for budgetary control, evaluating their advantages and disadvantages, and analyzing their application in responding to financial issues. It concludes by discussing how management accounting systems can help resolve financial problems and lead organizations to sustainable success. The report utilizes real-world examples and case studies to illustrate the concepts and provide a practical understanding of management accounting in a business context.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 (LO1 & LO2).....................................................................................................................1

PART (A).........................................................................................................................................1

P1: Management accounting and essential requirement of management accounting system 1

P2: Explain different method of management accounting reporting......................................3

Benefits of management accounting system..........................................................................4

Evaluation of management accounting system and management accounting report integrated

with organizational process....................................................................................................5

PART (B).........................................................................................................................................5

P3: Appropriate technique of cost analysis to prepare an income statement.........................5

The difference between profits of marginal and absorption costing are as follows:..............6

TASK 2 (LO3 & LO4).....................................................................................................................8

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................8

Analysis of various planning tools and their application.....................................................10

Evaluation of Planning tools for Responding to financial issues.........................................10

P5: Response of management accounting systems towards resolving financial problems. .11

Management accounting leads organizations to achieve sustainable success......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1 (LO1 & LO2).....................................................................................................................1

PART (A).........................................................................................................................................1

P1: Management accounting and essential requirement of management accounting system 1

P2: Explain different method of management accounting reporting......................................3

Benefits of management accounting system..........................................................................4

Evaluation of management accounting system and management accounting report integrated

with organizational process....................................................................................................5

PART (B).........................................................................................................................................5

P3: Appropriate technique of cost analysis to prepare an income statement.........................5

The difference between profits of marginal and absorption costing are as follows:..............6

TASK 2 (LO3 & LO4).....................................................................................................................8

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................8

Analysis of various planning tools and their application.....................................................10

Evaluation of Planning tools for Responding to financial issues.........................................10

P5: Response of management accounting systems towards resolving financial problems. .11

Management accounting leads organizations to achieve sustainable success......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is the process of recording business transactions using different

accounting systems so as to facilitate management to formulate an effective plans and strategies

for the betterment of an organisation (Management accounting, 2018). It is useful almost for

every organisation to achieve competitive advantage in market as it help in analysing the actual

financial position of company which enable management to make changes in existing plans and

strategies so as to retail their strong position in market. Accounting manager is held responsible

to maintain books of accounts such as Profit and loss a/c, Balance sheet, Cash flow statement etc.

on annual basis. The present assignment report is based on Rowlinson Knitwear which is

engaged in manufacturing and selling school and corporate wear garments to the people of UK

and throughout the world. The report includes discussion on various accounting systems along

with their benefits, management reporting system, different costing methods, planning tools to

control budget and financial resolving tools such as KPI, Benchmarking etc.

TASK 1 (LO1 & LO2)

PART (A)

P1: Management accounting and essential requirement of management accounting system

According to the Institute of Management Accountants (IMA):- Management

accounting is termed as a profession which gets involved in decision making process,

formulation of planning, adoption of management styles and preparation of financial statements

with the help of which management can frame and implement organisation's strategy (Statements

on Management Accounting, 2018).

According to Chartered Institute of Management Accountants (CIMA):

Management accounting is defined as analysing of information to formulate business strategies

so as to drive business to achieve growth and success in competitive market (Belfo and Trigo,

2013).

According to Certified Management Accountants (CMA), Management accounting is

applicable on accounting manager's professional knowledge and skill in order to prepare

financial statements so that management of an organisation can assist organisation in achieve

growth and sustainability by making suitable plans and policies (Maher, Stickney and Weil,

2012).

1

Management accounting is the process of recording business transactions using different

accounting systems so as to facilitate management to formulate an effective plans and strategies

for the betterment of an organisation (Management accounting, 2018). It is useful almost for

every organisation to achieve competitive advantage in market as it help in analysing the actual

financial position of company which enable management to make changes in existing plans and

strategies so as to retail their strong position in market. Accounting manager is held responsible

to maintain books of accounts such as Profit and loss a/c, Balance sheet, Cash flow statement etc.

on annual basis. The present assignment report is based on Rowlinson Knitwear which is

engaged in manufacturing and selling school and corporate wear garments to the people of UK

and throughout the world. The report includes discussion on various accounting systems along

with their benefits, management reporting system, different costing methods, planning tools to

control budget and financial resolving tools such as KPI, Benchmarking etc.

TASK 1 (LO1 & LO2)

PART (A)

P1: Management accounting and essential requirement of management accounting system

According to the Institute of Management Accountants (IMA):- Management

accounting is termed as a profession which gets involved in decision making process,

formulation of planning, adoption of management styles and preparation of financial statements

with the help of which management can frame and implement organisation's strategy (Statements

on Management Accounting, 2018).

According to Chartered Institute of Management Accountants (CIMA):

Management accounting is defined as analysing of information to formulate business strategies

so as to drive business to achieve growth and success in competitive market (Belfo and Trigo,

2013).

According to Certified Management Accountants (CMA), Management accounting is

applicable on accounting manager's professional knowledge and skill in order to prepare

financial statements so that management of an organisation can assist organisation in achieve

growth and sustainability by making suitable plans and policies (Maher, Stickney and Weil,

2012).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting principles:

Influence: Communication facilitates insight that is influential. Management accounting

provide credible information about current position of company which can hugely influence the

decision-making process. For example, facing financial losses directs management to make

changes in their credit policies so as to avoid any bad-debts.

Relevance: It refers to accuracy of data which can decide the effectiveness of decisions

and plans formulated by the management of an organisation. For example, recording business

transactions in financial statement must be relevant and accurate so as to identify whether the

company operate business or successfully (Ax and Greve, 2017).

Value: In this, impact on value is analysed. Management accounting relates

organisation's strategy to its business model and requires a better understanding of environmental

factors. Analysing of information recorded under financial statement guides the management of

company to identify the errors which restrict them to achieve expected results.

Credibility: It means accounting professionals must be ethical, accountable and mindful

of the organisation's values, governance requirements and social responsibilities. For example, if

financial statements such as profit and loss a/c, Balance sheet etc. shows true and accurate

financial position of company then it help in gaining trust of shareholders which in turn

providing financial help to them (Bennett and James, 2017).

Different accounting systems:

Cost accounting system: It is a system which help in analysing cost of products which

includes fixed, variable cost etc. It facilitate management in identifying the actual cost incurred

in manufacturing process which enable them in setting up pricing policy for their targeted

customers after adding margin on it. Thus, using such system by Rowlinson Knitwear help them

in reducing cost of business operations by analysing amount invested properly (Crosson and

Needles, 2013) .

Price optimisation system: It refers to a system which determines the actual perception of

customers towards company's pricing policy which assist management to make decisions

whether to make changes in current pricing policy or not. Using such system by Rowlinson

Knitwear facilitate management to attract new and retain loyal customers by providing them

products and services at their preferred prices.

2

Influence: Communication facilitates insight that is influential. Management accounting

provide credible information about current position of company which can hugely influence the

decision-making process. For example, facing financial losses directs management to make

changes in their credit policies so as to avoid any bad-debts.

Relevance: It refers to accuracy of data which can decide the effectiveness of decisions

and plans formulated by the management of an organisation. For example, recording business

transactions in financial statement must be relevant and accurate so as to identify whether the

company operate business or successfully (Ax and Greve, 2017).

Value: In this, impact on value is analysed. Management accounting relates

organisation's strategy to its business model and requires a better understanding of environmental

factors. Analysing of information recorded under financial statement guides the management of

company to identify the errors which restrict them to achieve expected results.

Credibility: It means accounting professionals must be ethical, accountable and mindful

of the organisation's values, governance requirements and social responsibilities. For example, if

financial statements such as profit and loss a/c, Balance sheet etc. shows true and accurate

financial position of company then it help in gaining trust of shareholders which in turn

providing financial help to them (Bennett and James, 2017).

Different accounting systems:

Cost accounting system: It is a system which help in analysing cost of products which

includes fixed, variable cost etc. It facilitate management in identifying the actual cost incurred

in manufacturing process which enable them in setting up pricing policy for their targeted

customers after adding margin on it. Thus, using such system by Rowlinson Knitwear help them

in reducing cost of business operations by analysing amount invested properly (Crosson and

Needles, 2013) .

Price optimisation system: It refers to a system which determines the actual perception of

customers towards company's pricing policy which assist management to make decisions

whether to make changes in current pricing policy or not. Using such system by Rowlinson

Knitwear facilitate management to attract new and retain loyal customers by providing them

products and services at their preferred prices.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system: It is a system which determines the actual level of

inventory the company have at present to meet customer's needs and expectations. Thus, using

such system by Rowlinson Knitwear assist management to make decision whether current level

of inventory is sufficient or should order further inventory to meet client's orders. This help in

reducing cost of warehouses as the managers can easily order stock whenever they required by

using such system.

Job costing system: It is a system which determines the cost invested in producing

particular product or group of products. It can be used by Rowlinson Knitwear to facilitate

management in assigning cost to producing products which brings more profitable outcome in

return. For example, professional wear garments sell by company are more in demand as per

such system due to which the management should invest more in producing such demanded

product and lowering investment in manufacturing school wear products (Jamil and et. al., 2015).

P2: Explain different method of management accounting reporting

An organisation if maintaining their daily transactions in book of accounts such as profit

and loss a/c, Balance sheet etc. then it will help management in formulating an effective plans

and policies for the betterment of an organisation. For this, accounting manager is held

responsible to use different management accounting reporting on regular basis which must

provide accurate and reliable information to the management. Here are the some management

accounting reporting that can be used by Rowlinson Knitwear:

Performance reports: It is a report containing information related with the employees of

an organisation which enable management to review the overall performance of company.

Managers of Rowlinson Knitwear uses these performance reports to make strategic decisions for

their betterment. By analysing such report, employees are awarded for better performance and

providing training programs for low-performer. Increasing their contribution assist an

organisation to achieve growth and success in competitive market (Kokubu and Kitada, 2015)

Budget reports: It is a report which is very critical to measure company's performance

and prepared by almost every organisation irrespective of the size whether small, medium or

large. Every organisation such as Rowlinson Knitwear prepares an overall budget to execute

future business activities in more effective and efficient way. This will direct the employees to

utilise available resources without any wastage so that the financial position of company could be

3

inventory the company have at present to meet customer's needs and expectations. Thus, using

such system by Rowlinson Knitwear assist management to make decision whether current level

of inventory is sufficient or should order further inventory to meet client's orders. This help in

reducing cost of warehouses as the managers can easily order stock whenever they required by

using such system.

Job costing system: It is a system which determines the cost invested in producing

particular product or group of products. It can be used by Rowlinson Knitwear to facilitate

management in assigning cost to producing products which brings more profitable outcome in

return. For example, professional wear garments sell by company are more in demand as per

such system due to which the management should invest more in producing such demanded

product and lowering investment in manufacturing school wear products (Jamil and et. al., 2015).

P2: Explain different method of management accounting reporting

An organisation if maintaining their daily transactions in book of accounts such as profit

and loss a/c, Balance sheet etc. then it will help management in formulating an effective plans

and policies for the betterment of an organisation. For this, accounting manager is held

responsible to use different management accounting reporting on regular basis which must

provide accurate and reliable information to the management. Here are the some management

accounting reporting that can be used by Rowlinson Knitwear:

Performance reports: It is a report containing information related with the employees of

an organisation which enable management to review the overall performance of company.

Managers of Rowlinson Knitwear uses these performance reports to make strategic decisions for

their betterment. By analysing such report, employees are awarded for better performance and

providing training programs for low-performer. Increasing their contribution assist an

organisation to achieve growth and success in competitive market (Kokubu and Kitada, 2015)

Budget reports: It is a report which is very critical to measure company's performance

and prepared by almost every organisation irrespective of the size whether small, medium or

large. Every organisation such as Rowlinson Knitwear prepares an overall budget to execute

future business activities in more effective and efficient way. This will direct the employees to

utilise available resources without any wastage so that the financial position of company could be

3

maintained. Budget report is prepared by analysing previous year figures so that maximum

outcome can be gained by executing pre-determined activities in desired way.

Accounts receivable ageing report: It is a report which determines the list of debtors

whose payments to an organisation is unpaid. Preparing such report facilitate management of

Rowlinson Knitwear to identify the list of unpaid debtors which makes adverse impact on the

financial position. This will help managers to make some actions for recovery and also re-think

about their credit policies so as to overcome from any financial losses.

Cost managerial accounting report:

Managerial accounting computes the cost of articles which are manufactured including

raw material costs, overhead, labour, and any added costs. This costs are divided by the amounts

of products manufactured. This kind of report provides a overall summary of all information

related with the cost so that an effective pricing policy can be formulated which satisfy both the

needs and requirements of customers as well as expectations of an organisation (Lavia López and

Hiebl, 2014).

Benefits of management accounting system

Types of management

accounting system

Benefits of accounting system

Job costing system It assist company in identifying the cost incurred in

manufacturing particular product which enable management to

identify whether the invested cost has been recovered on not

after selling it to the final customers. This will make easy to

make decision whether to increase production of such product

or not.

Inventory management system It facilitate management of Rowlinson Knitwear to maintain

adequate level of inventory to meet customers requirements.

This will help in reducing storage cost and increase

profitability.

Cost accounting system It assist company in analysing the cost incurred in production

process which enable them to prepare an effective budget.

Through this, the business cost has been decreased and

4

outcome can be gained by executing pre-determined activities in desired way.

Accounts receivable ageing report: It is a report which determines the list of debtors

whose payments to an organisation is unpaid. Preparing such report facilitate management of

Rowlinson Knitwear to identify the list of unpaid debtors which makes adverse impact on the

financial position. This will help managers to make some actions for recovery and also re-think

about their credit policies so as to overcome from any financial losses.

Cost managerial accounting report:

Managerial accounting computes the cost of articles which are manufactured including

raw material costs, overhead, labour, and any added costs. This costs are divided by the amounts

of products manufactured. This kind of report provides a overall summary of all information

related with the cost so that an effective pricing policy can be formulated which satisfy both the

needs and requirements of customers as well as expectations of an organisation (Lavia López and

Hiebl, 2014).

Benefits of management accounting system

Types of management

accounting system

Benefits of accounting system

Job costing system It assist company in identifying the cost incurred in

manufacturing particular product which enable management to

identify whether the invested cost has been recovered on not

after selling it to the final customers. This will make easy to

make decision whether to increase production of such product

or not.

Inventory management system It facilitate management of Rowlinson Knitwear to maintain

adequate level of inventory to meet customers requirements.

This will help in reducing storage cost and increase

profitability.

Cost accounting system It assist company in analysing the cost incurred in production

process which enable them to prepare an effective budget.

Through this, the business cost has been decreased and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increase profits.

Price optimisation system It helps Rowlinson Knitwear to set an effective pricing policy

after identifying perception of customers and satisfaction level

towards their existing pricing policies.

Evaluation of management accounting system and management accounting report integrated with

organizational process

Rowlinson Knitwear uses both these system to maintain records on timely basis which

enable management to make suitable plans and strategic decisions. These two systems are

interrelated with each other in order to achieve organisational goals and objectives. For example,

using costing accounting system help in analysing the total cost incurred in execution of business

operations which further to be recorded in cost accounting report. This will help in preparing an

effective budget which in results reducing cost of operations and increases profitability.

PART (B)

P3: Appropriate technique of cost analysis to prepare an income statement

Absorption costing: It is a costing method which is used to calculate total costs incurred

in production process including fixed and variable costs. It is also known as full costing method

due to considering both fixed and variable cost while calculation of net profitability (Modell,

2014).

Marginal costing: It is method which is used to calculate net profitability in which

variable cost is considered as unit cost and fixed cost is considered as the period cost. Using such

method increases net profitability of company in their financial statement due to which it is most

preferable method adopted by small-medium organisation.

The difference between marginal and absorption costing are as follow:

Basis Marginal Costing Absorption Costing

Cost recognition In marginal costing fixed cost

is considered as period costs

whereas, variable cost is

In Absorption costing both

variable and fixed costs are

considered as product cost.

5

Price optimisation system It helps Rowlinson Knitwear to set an effective pricing policy

after identifying perception of customers and satisfaction level

towards their existing pricing policies.

Evaluation of management accounting system and management accounting report integrated with

organizational process

Rowlinson Knitwear uses both these system to maintain records on timely basis which

enable management to make suitable plans and strategic decisions. These two systems are

interrelated with each other in order to achieve organisational goals and objectives. For example,

using costing accounting system help in analysing the total cost incurred in execution of business

operations which further to be recorded in cost accounting report. This will help in preparing an

effective budget which in results reducing cost of operations and increases profitability.

PART (B)

P3: Appropriate technique of cost analysis to prepare an income statement

Absorption costing: It is a costing method which is used to calculate total costs incurred

in production process including fixed and variable costs. It is also known as full costing method

due to considering both fixed and variable cost while calculation of net profitability (Modell,

2014).

Marginal costing: It is method which is used to calculate net profitability in which

variable cost is considered as unit cost and fixed cost is considered as the period cost. Using such

method increases net profitability of company in their financial statement due to which it is most

preferable method adopted by small-medium organisation.

The difference between marginal and absorption costing are as follow:

Basis Marginal Costing Absorption Costing

Cost recognition In marginal costing fixed cost

is considered as period costs

whereas, variable cost is

In Absorption costing both

variable and fixed costs are

considered as product cost.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considered as product cost

Classification of overheads In marginal costing

classification of overheads is

done on the basis of fixed and

variable cost.

In absorption costing

calssification of overhead is

based on selling and

distribution, production and

administration.

Focus Marginal costing focus more

on contribution per unit.

Absorption costing highlights

more on Net profit per unit.

Use of marginal costing in an organization

Cost control: Margibal costing classify total cost into two parts which are fixed cost and

variable cost. Variable cost are managed by the lower level management while fixed cost is

managed by the top level mangement which help the businees to run smoothly in the long run.

Profit planning: Marginal costing helps the organization to figure out plan for coming

years in effectiner manner by maximization of profit. It helps to bring out correct effect of

change in variable cost and sales price.

The difference between profits of marginal and absorption costing are as follows:

The profit margins of marginal costing and adsorptional costing is different because

marginal costing includes only those costs to inventory which involve when each individual unit

is produces in the business. It more focus on the contribution of per unit. Whereas, absorption

costing includes all production cost to all units produced in a business. It focus more of net profit

per unit. This are the reason why there is difference in their profit margin in these costing

methods.

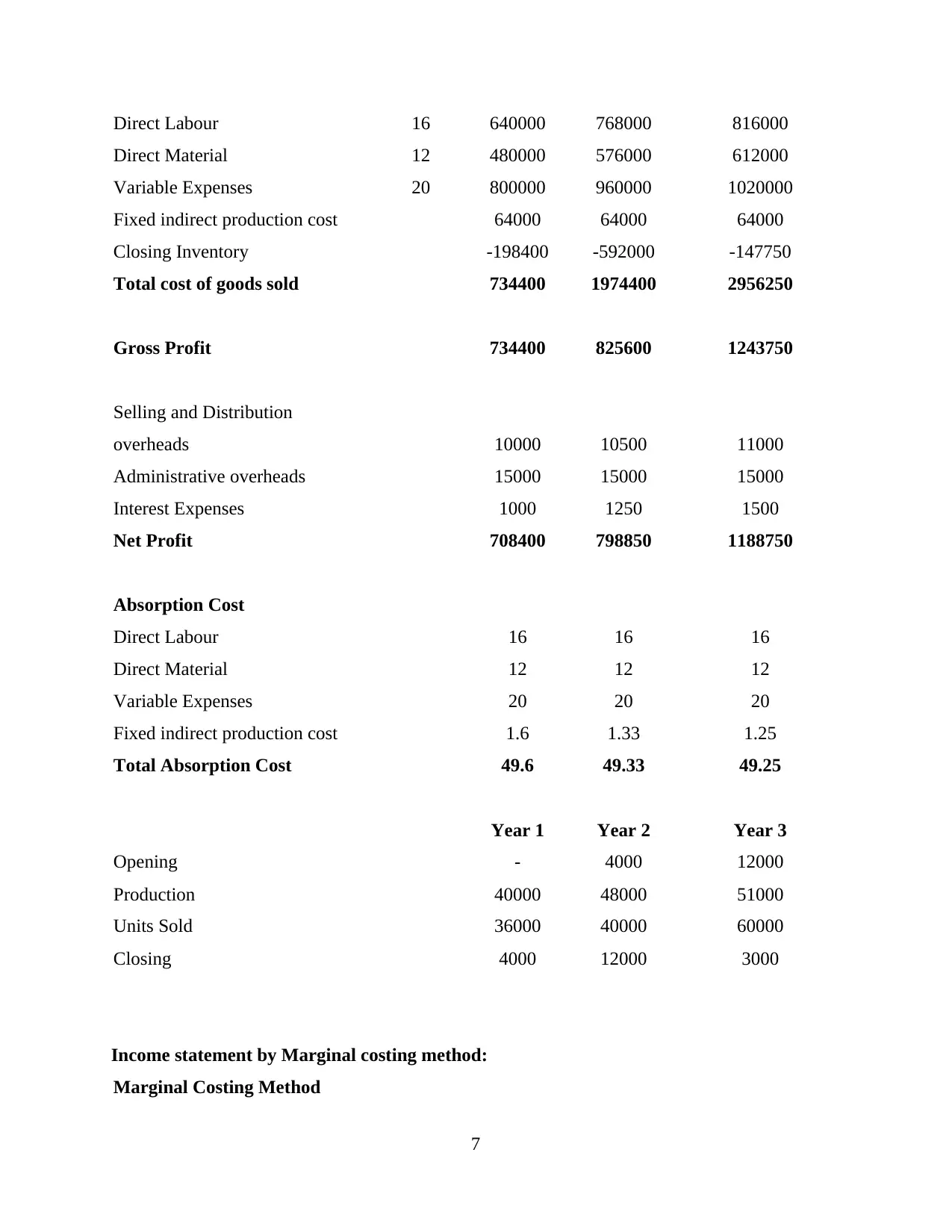

Income statement by absorption costing method:

Absorption Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Cost of Goods sold

Opening Inventory - 198400 592000

6

Classification of overheads In marginal costing

classification of overheads is

done on the basis of fixed and

variable cost.

In absorption costing

calssification of overhead is

based on selling and

distribution, production and

administration.

Focus Marginal costing focus more

on contribution per unit.

Absorption costing highlights

more on Net profit per unit.

Use of marginal costing in an organization

Cost control: Margibal costing classify total cost into two parts which are fixed cost and

variable cost. Variable cost are managed by the lower level management while fixed cost is

managed by the top level mangement which help the businees to run smoothly in the long run.

Profit planning: Marginal costing helps the organization to figure out plan for coming

years in effectiner manner by maximization of profit. It helps to bring out correct effect of

change in variable cost and sales price.

The difference between profits of marginal and absorption costing are as follows:

The profit margins of marginal costing and adsorptional costing is different because

marginal costing includes only those costs to inventory which involve when each individual unit

is produces in the business. It more focus on the contribution of per unit. Whereas, absorption

costing includes all production cost to all units produced in a business. It focus more of net profit

per unit. This are the reason why there is difference in their profit margin in these costing

methods.

Income statement by absorption costing method:

Absorption Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Cost of Goods sold

Opening Inventory - 198400 592000

6

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 960000 1020000

Fixed indirect production cost 64000 64000 64000

Closing Inventory -198400 -592000 -147750

Total cost of goods sold 734400 1974400 2956250

Gross Profit 734400 825600 1243750

Selling and Distribution

overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 708400 798850 1188750

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Fixed indirect production cost 1.6 1.33 1.25

Total Absorption Cost 49.6 49.33 49.25

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

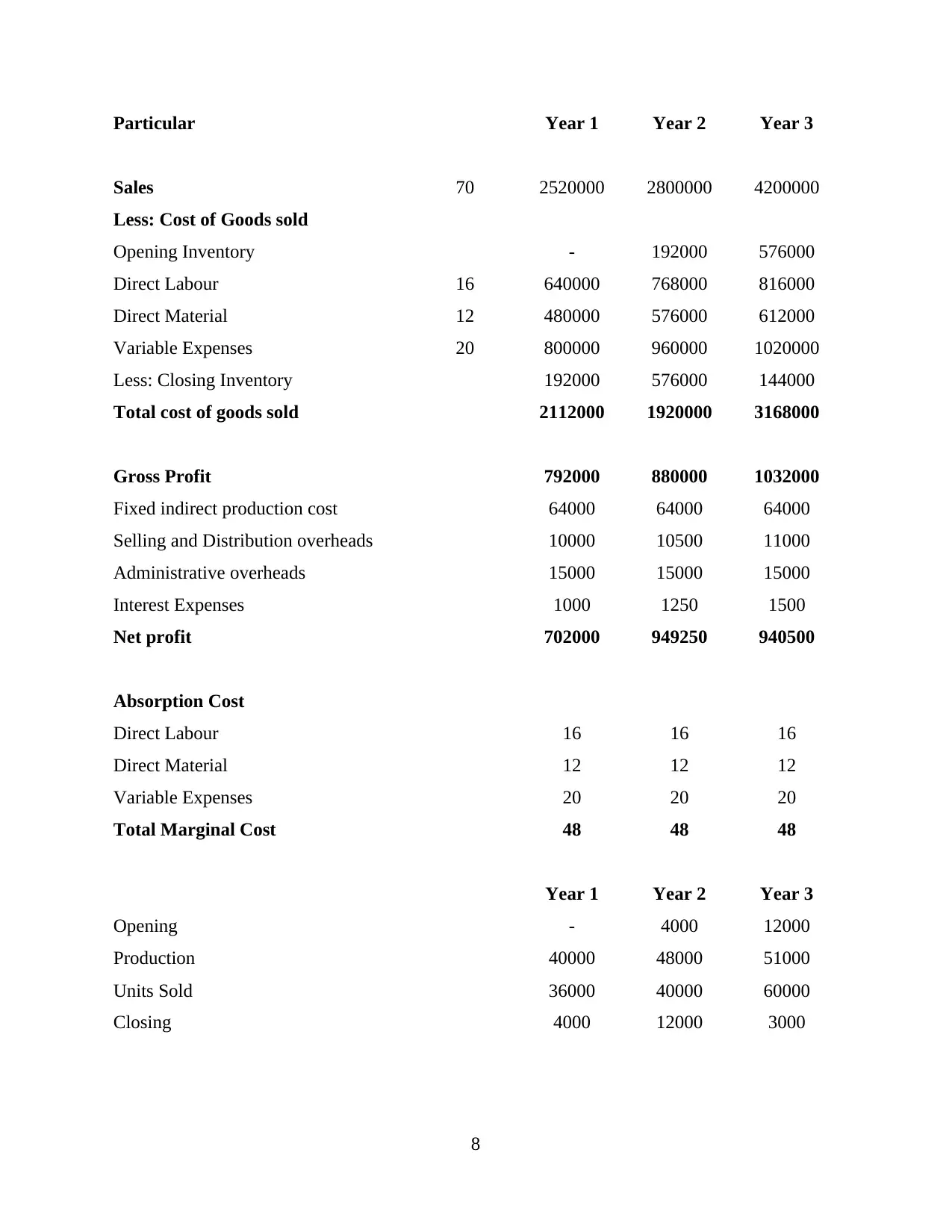

Income statement by Marginal costing method:

Marginal Costing Method

7

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 960000 1020000

Fixed indirect production cost 64000 64000 64000

Closing Inventory -198400 -592000 -147750

Total cost of goods sold 734400 1974400 2956250

Gross Profit 734400 825600 1243750

Selling and Distribution

overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 708400 798850 1188750

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Fixed indirect production cost 1.6 1.33 1.25

Total Absorption Cost 49.6 49.33 49.25

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

Income statement by Marginal costing method:

Marginal Costing Method

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Cost of Goods sold

Opening Inventory - 192000 576000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 960000 1020000

Less: Closing Inventory 192000 576000 144000

Total cost of goods sold 2112000 1920000 3168000

Gross Profit 792000 880000 1032000

Fixed indirect production cost 64000 64000 64000

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net profit 702000 949250 940500

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Total Marginal Cost 48 48 48

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

8

Sales 70 2520000 2800000 4200000

Less: Cost of Goods sold

Opening Inventory - 192000 576000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 960000 1020000

Less: Closing Inventory 192000 576000 144000

Total cost of goods sold 2112000 1920000 3168000

Gross Profit 792000 880000 1032000

Fixed indirect production cost 64000 64000 64000

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net profit 702000 949250 940500

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Total Marginal Cost 48 48 48

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

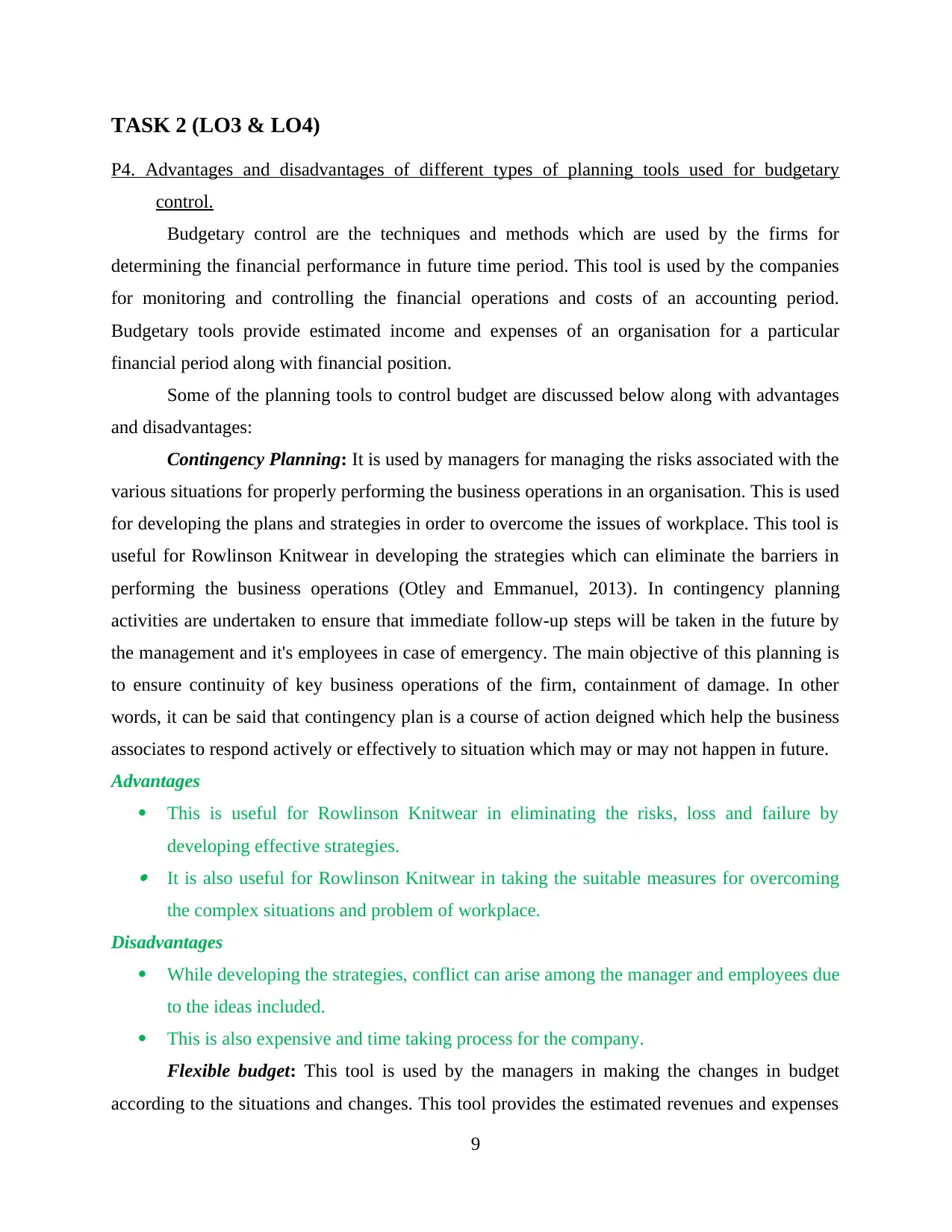

TASK 2 (LO3 & LO4)

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budgetary control are the techniques and methods which are used by the firms for

determining the financial performance in future time period. This tool is used by the companies

for monitoring and controlling the financial operations and costs of an accounting period.

Budgetary tools provide estimated income and expenses of an organisation for a particular

financial period along with financial position.

Some of the planning tools to control budget are discussed below along with advantages

and disadvantages:

Contingency Planning: It is used by managers for managing the risks associated with the

various situations for properly performing the business operations in an organisation. This is used

for developing the plans and strategies in order to overcome the issues of workplace. This tool is

useful for Rowlinson Knitwear in developing the strategies which can eliminate the barriers in

performing the business operations (Otley and Emmanuel, 2013). In contingency planning

activities are undertaken to ensure that immediate follow-up steps will be taken in the future by

the management and it's employees in case of emergency. The main objective of this planning is

to ensure continuity of key business operations of the firm, containment of damage. In other

words, it can be said that contingency plan is a course of action deigned which help the business

associates to respond actively or effectively to situation which may or may not happen in future.

Advantages

This is useful for Rowlinson Knitwear in eliminating the risks, loss and failure by

developing effective strategies. It is also useful for Rowlinson Knitwear in taking the suitable measures for overcoming

the complex situations and problem of workplace.

Disadvantages

While developing the strategies, conflict can arise among the manager and employees due

to the ideas included.

This is also expensive and time taking process for the company.

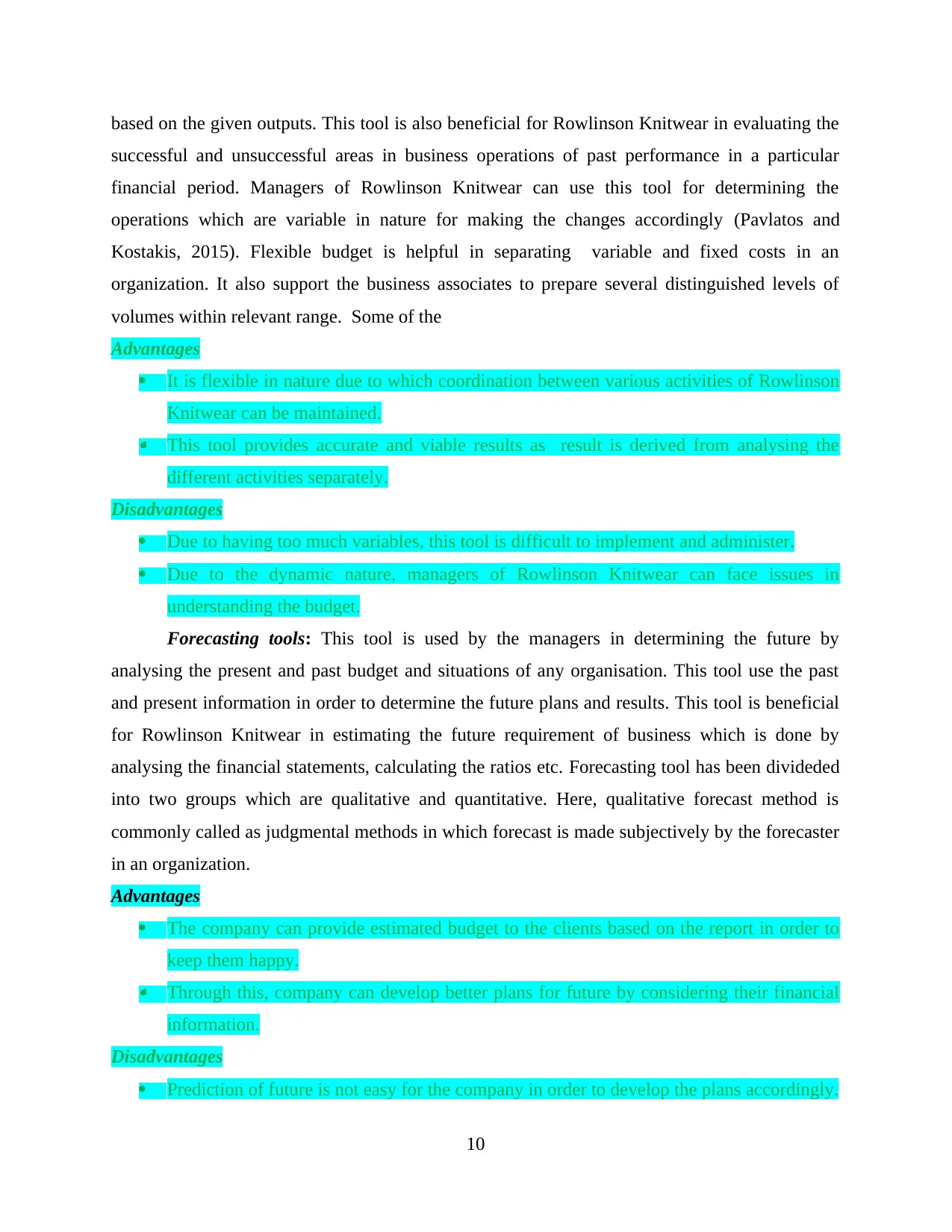

Flexible budget: This tool is used by the managers in making the changes in budget

according to the situations and changes. This tool provides the estimated revenues and expenses

9

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budgetary control are the techniques and methods which are used by the firms for

determining the financial performance in future time period. This tool is used by the companies

for monitoring and controlling the financial operations and costs of an accounting period.

Budgetary tools provide estimated income and expenses of an organisation for a particular

financial period along with financial position.

Some of the planning tools to control budget are discussed below along with advantages

and disadvantages:

Contingency Planning: It is used by managers for managing the risks associated with the

various situations for properly performing the business operations in an organisation. This is used

for developing the plans and strategies in order to overcome the issues of workplace. This tool is

useful for Rowlinson Knitwear in developing the strategies which can eliminate the barriers in

performing the business operations (Otley and Emmanuel, 2013). In contingency planning

activities are undertaken to ensure that immediate follow-up steps will be taken in the future by

the management and it's employees in case of emergency. The main objective of this planning is

to ensure continuity of key business operations of the firm, containment of damage. In other

words, it can be said that contingency plan is a course of action deigned which help the business

associates to respond actively or effectively to situation which may or may not happen in future.

Advantages

This is useful for Rowlinson Knitwear in eliminating the risks, loss and failure by

developing effective strategies. It is also useful for Rowlinson Knitwear in taking the suitable measures for overcoming

the complex situations and problem of workplace.

Disadvantages

While developing the strategies, conflict can arise among the manager and employees due

to the ideas included.

This is also expensive and time taking process for the company.

Flexible budget: This tool is used by the managers in making the changes in budget

according to the situations and changes. This tool provides the estimated revenues and expenses

9

based on the given outputs. This tool is also beneficial for Rowlinson Knitwear in evaluating the

successful and unsuccessful areas in business operations of past performance in a particular

financial period. Managers of Rowlinson Knitwear can use this tool for determining the

operations which are variable in nature for making the changes accordingly (Pavlatos and

Kostakis, 2015). Flexible budget is helpful in separating variable and fixed costs in an

organization. It also support the business associates to prepare several distinguished levels of

volumes within relevant range. Some of the

Advantages

It is flexible in nature due to which coordination between various activities of Rowlinson

Knitwear can be maintained. This tool provides accurate and viable results as result is derived from analysing the

different activities separately.

Disadvantages

Due to having too much variables, this tool is difficult to implement and administer.

Due to the dynamic nature, managers of Rowlinson Knitwear can face issues in

understanding the budget.

Forecasting tools: This tool is used by the managers in determining the future by

analysing the present and past budget and situations of any organisation. This tool use the past

and present information in order to determine the future plans and results. This tool is beneficial

for Rowlinson Knitwear in estimating the future requirement of business which is done by

analysing the financial statements, calculating the ratios etc. Forecasting tool has been divideded

into two groups which are qualitative and quantitative. Here, qualitative forecast method is

commonly called as judgmental methods in which forecast is made subjectively by the forecaster

in an organization.

Advantages

The company can provide estimated budget to the clients based on the report in order to

keep them happy. Through this, company can develop better plans for future by considering their financial

information.

Disadvantages

Prediction of future is not easy for the company in order to develop the plans accordingly.

10

successful and unsuccessful areas in business operations of past performance in a particular

financial period. Managers of Rowlinson Knitwear can use this tool for determining the

operations which are variable in nature for making the changes accordingly (Pavlatos and

Kostakis, 2015). Flexible budget is helpful in separating variable and fixed costs in an

organization. It also support the business associates to prepare several distinguished levels of

volumes within relevant range. Some of the

Advantages

It is flexible in nature due to which coordination between various activities of Rowlinson

Knitwear can be maintained. This tool provides accurate and viable results as result is derived from analysing the

different activities separately.

Disadvantages

Due to having too much variables, this tool is difficult to implement and administer.

Due to the dynamic nature, managers of Rowlinson Knitwear can face issues in

understanding the budget.

Forecasting tools: This tool is used by the managers in determining the future by

analysing the present and past budget and situations of any organisation. This tool use the past

and present information in order to determine the future plans and results. This tool is beneficial

for Rowlinson Knitwear in estimating the future requirement of business which is done by

analysing the financial statements, calculating the ratios etc. Forecasting tool has been divideded

into two groups which are qualitative and quantitative. Here, qualitative forecast method is

commonly called as judgmental methods in which forecast is made subjectively by the forecaster

in an organization.

Advantages

The company can provide estimated budget to the clients based on the report in order to

keep them happy. Through this, company can develop better plans for future by considering their financial

information.

Disadvantages

Prediction of future is not easy for the company in order to develop the plans accordingly.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.