Management Accounting Report: Tools, Methods, and Performance Analysis

VerifiedAdded on 2020/02/17

|14

|5439

|40

Report

AI Summary

This report provides an in-depth analysis of management accounting principles and their application within Nisa Ltd, a small retail business. The report begins by outlining the essential requirements of management accounting systems, including standard costing, cost accounting, job costing, inventory management, control accounting, and financial accounting. It then explores various management accounting methods, such as product costing, cost allocations, inventory costing, and planning tools for performance measurement. The report further delves into different costing methods, with a focus on marginal and absorption costing, and provides a critical evaluation of budgetary control systems. The content also covers the importance of management accounting systems for small businesses, emphasizing their role in forecasting, decision-making, and enhancing overall business efficiency. The report highlights the significance of financial statement analysis, planning tools, and strategic management in achieving business goals. Overall, the report aims to equip learners with a comprehensive understanding of management accounting tools and techniques for effective business operations and long-term sustainability.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Management accounting and its different systems' essential requirements..........................3

P2) Different management accounting methods..........................................................................5

TASK 2............................................................................................................................................6

P3) Various costing methods and differences between marginal and absorption costing...........6

TASK 3............................................................................................................................................6

P4) Critical evaluation on budgetary control systems.................................................................6

P5) Management accounting systems..........................................................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................7

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Management accounting and its different systems' essential requirements..........................3

P2) Different management accounting methods..........................................................................5

TASK 2............................................................................................................................................6

P3) Various costing methods and differences between marginal and absorption costing...........6

TASK 3............................................................................................................................................6

P4) Critical evaluation on budgetary control systems.................................................................6

P5) Management accounting systems..........................................................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................7

2

INTRODUCTION

Management accounting is multidisciplinary approach that is useful for expansion of

organization and increasing its efficiency. Therefore, management of entire business operations

that affects balance of production and distribution system of entity. The present report is based

on understanding different management accounting tools of Nisa Ltd. It is retail sector small

scale organization of UK that provides clothing, food and drink services of customers. Various

management accounting tools and systems can be described for forecasting and decision making

related to further implementation of firm. In this regard, several costing methods and their

described can be expressed for proper price determination. However, critical evaluation on

budgeting is to be considered through this assignment. Along with this, various aspects for

expansion of small size business and enhancing its quality services are to be defined by studying

this report. Hence, learners are able to understand applying different tools and techniques of

management accounting for overall business activities' effectiveness.

TASK 1

P1) Management accounting and its different systems' essential requirements

Management accounting is one of the crucial system for expansion of small business unit

and increasing efficiency for qualitative services. In accordance to this, overall business activities

get impacted as well remains able to creating positive environment of firm at large scale.

However, several tools and techniques are applied for enhancing efficiency of firm at firm. It is

useful for optimum utilization of resources and fund that impacts on productivity and

profitability of retail sector company (Anwar and et.al., 2016). Including this, management

accountant of firm recognizes business and employees' performance to build up relationship

among employees as well helpful for spreading wide scope of organization to gain their best

contribution for working in team. Therefore, business, marketing and competitive strategies of

organization can be enhanced at high level. In this regard, adequate utilization of resources can

be gained. Moreover, management accountant of company identifies all financial statements

including income statement, balance sheet, profit and loss account, cash flow and fund flow. On

the basis of these tools different ideas are created for implementing action plans that impacts on

company's effectiveness. It affects customer satisfaction and increasing in positive feelings of

3

Management accounting is multidisciplinary approach that is useful for expansion of

organization and increasing its efficiency. Therefore, management of entire business operations

that affects balance of production and distribution system of entity. The present report is based

on understanding different management accounting tools of Nisa Ltd. It is retail sector small

scale organization of UK that provides clothing, food and drink services of customers. Various

management accounting tools and systems can be described for forecasting and decision making

related to further implementation of firm. In this regard, several costing methods and their

described can be expressed for proper price determination. However, critical evaluation on

budgeting is to be considered through this assignment. Along with this, various aspects for

expansion of small size business and enhancing its quality services are to be defined by studying

this report. Hence, learners are able to understand applying different tools and techniques of

management accounting for overall business activities' effectiveness.

TASK 1

P1) Management accounting and its different systems' essential requirements

Management accounting is one of the crucial system for expansion of small business unit

and increasing efficiency for qualitative services. In accordance to this, overall business activities

get impacted as well remains able to creating positive environment of firm at large scale.

However, several tools and techniques are applied for enhancing efficiency of firm at firm. It is

useful for optimum utilization of resources and fund that impacts on productivity and

profitability of retail sector company (Anwar and et.al., 2016). Including this, management

accountant of firm recognizes business and employees' performance to build up relationship

among employees as well helpful for spreading wide scope of organization to gain their best

contribution for working in team. Therefore, business, marketing and competitive strategies of

organization can be enhanced at high level. In this regard, adequate utilization of resources can

be gained. Moreover, management accountant of company identifies all financial statements

including income statement, balance sheet, profit and loss account, cash flow and fund flow. On

the basis of these tools different ideas are created for implementing action plans that impacts on

company's effectiveness. It affects customer satisfaction and increasing in positive feelings of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consumers towards organization's effectiveness. Along with this, effective market value for

entity and products produced by company can be effective (Armitage and Webb, 2013). Thus,

high level of production and profit earning capacity of firm can be achieved efficiently. In this

process, management accounting is useful for applying different tools and techniques related to

enlargement of entity and increasing its market efficiency to sustain its good reputation for long

time period. Hence, management accounting is composition of different substances such as

costing, budgeting, income statements and business organization's operations that affects market

position of firm at large scale. It is interlinked with creating positive and developing atmosphere

of entity for various kinds of business operations (Berman, 2015). In accordance to this, varieties

of tools and techniques can be applied for enlargement of small scale enterprise also able to

enhance quality services of firm that impacts on organization's effectiveness. Therefore,

management accounting is useful for effectiveness of business entity and enhancing its efficiency

for long term sustainability of firm at high level.

Essential requirements of management accounting systems:- There are different

management accounting systems applied for expansion of small scale enterprise and increasing

its high position in market to face competition at large scale (Bucci, 2014). However, it increases

business and competitive strategies of firm for long time periodicity. Several management

accounting systems and their essentials can be described as below:-

Standard costing:- Under this process, management accounting of Nisa Ltd analyses

overall business operations and its performance that generates different ideas for further

implementation of small scale enterprise. In this process, forecasting and decision making

is presented to price determination (Burke, Corman and Story, 2016). Moreover, balance

between income and expenditure for business operations can be obtained. In addition to

this, estimation for incurring costs is determined that affects on production and

distribution system of firm. However, proper estimation and forecasting is applied for

expansion of small business unit. It is considered as a technique for following on

prepared action plan to increase efficiency of entity and presenting financial position of

firm for proper income statements.

4

entity and products produced by company can be effective (Armitage and Webb, 2013). Thus,

high level of production and profit earning capacity of firm can be achieved efficiently. In this

process, management accounting is useful for applying different tools and techniques related to

enlargement of entity and increasing its market efficiency to sustain its good reputation for long

time period. Hence, management accounting is composition of different substances such as

costing, budgeting, income statements and business organization's operations that affects market

position of firm at large scale. It is interlinked with creating positive and developing atmosphere

of entity for various kinds of business operations (Berman, 2015). In accordance to this, varieties

of tools and techniques can be applied for enlargement of small scale enterprise also able to

enhance quality services of firm that impacts on organization's effectiveness. Therefore,

management accounting is useful for effectiveness of business entity and enhancing its efficiency

for long term sustainability of firm at high level.

Essential requirements of management accounting systems:- There are different

management accounting systems applied for expansion of small scale enterprise and increasing

its high position in market to face competition at large scale (Bucci, 2014). However, it increases

business and competitive strategies of firm for long time periodicity. Several management

accounting systems and their essentials can be described as below:-

Standard costing:- Under this process, management accounting of Nisa Ltd analyses

overall business operations and its performance that generates different ideas for further

implementation of small scale enterprise. In this process, forecasting and decision making

is presented to price determination (Burke, Corman and Story, 2016). Moreover, balance

between income and expenditure for business operations can be obtained. In addition to

this, estimation for incurring costs is determined that affects on production and

distribution system of firm. However, proper estimation and forecasting is applied for

expansion of small business unit. It is considered as a technique for following on

prepared action plan to increase efficiency of entity and presenting financial position of

firm for proper income statements.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system: In this system, costing and price determination strategy is presented as

per which financial problem of small size enterprise can be overcome efficiently

Job Costing system: In this costing system assigning manufacturing costs to an individual

products, mainly job system is used only when the product manufactured are different from the

other ones.

Inventory management system: In this system, several tools and techniques are applied for

proper balance of production and distribution of goods.

inventory management is interlinked with several organizational functions related to expansion

of small size entity.

Control accounting:- It is one of the essential tool of management accounting for

controlling over excess of production and wastage of raw materials. Therefore, control

accounting is useful for creating balance of production and distribution of goods.

Similarly, it is beneficial for increasing in income as well able to adequate expenditure.

However, cost control is liable for handling overall business activities and further

expenses and incurring price on business operations (Kreibich and et.al., 2014).

Therefore, control accounting is helpful for effective balance of expenditures and revenue

to enhance profit earning capacity of small scale enterprise for proper management.

Control accounting is measure their control over the financial statements and do not

ensure compliance with laws and regulations but rather are designed to help a company .

It can aid to provide validity an accuracy of its own financial statement.

Financial accounting:- Through this approach, management accountant of Nisa Ltd

analyses financial accounting tools such as profit and loss account, balance sheet, income

statement and performance of organization. Therefore, on the basis of these components

several ideas are created for effective monetary performance as well increasing in

profitability can be achieved at high level (Lavia López and Hiebl, 2014). Apart from

this, financial statement analysis is useful to present organization's economic structure

that generates varieties of tools for increasing profit earning capacity of small scale

enterprise. It is a special branch of accounting that keeps track of a measure company

5

per which financial problem of small size enterprise can be overcome efficiently

Job Costing system: In this costing system assigning manufacturing costs to an individual

products, mainly job system is used only when the product manufactured are different from the

other ones.

Inventory management system: In this system, several tools and techniques are applied for

proper balance of production and distribution of goods.

inventory management is interlinked with several organizational functions related to expansion

of small size entity.

Control accounting:- It is one of the essential tool of management accounting for

controlling over excess of production and wastage of raw materials. Therefore, control

accounting is useful for creating balance of production and distribution of goods.

Similarly, it is beneficial for increasing in income as well able to adequate expenditure.

However, cost control is liable for handling overall business activities and further

expenses and incurring price on business operations (Kreibich and et.al., 2014).

Therefore, control accounting is helpful for effective balance of expenditures and revenue

to enhance profit earning capacity of small scale enterprise for proper management.

Control accounting is measure their control over the financial statements and do not

ensure compliance with laws and regulations but rather are designed to help a company .

It can aid to provide validity an accuracy of its own financial statement.

Financial accounting:- Through this approach, management accountant of Nisa Ltd

analyses financial accounting tools such as profit and loss account, balance sheet, income

statement and performance of organization. Therefore, on the basis of these components

several ideas are created for effective monetary performance as well increasing in

profitability can be achieved at high level (Lavia López and Hiebl, 2014). Apart from

this, financial statement analysis is useful to present organization's economic structure

that generates varieties of tools for increasing profit earning capacity of small scale

enterprise. It is a special branch of accounting that keeps track of a measure company

5

financial statement and some transaction. All of such transaction are recorded,

summarized and presented for a financial reports and financial statements.

P2) Different management accounting Reports

There are different management accounting methods applied for overall business

operations' management. However, it is beneficial for adequate supplement of goods and services

that impacts on productivity and profitability of firm at high level (Macinati and Anessi-Pessina,

2014). In this regard, actual business performance is obtained for enlargement of entity and

enhancing its quality services. Thus, best use of resources and fund can be achieved to enhance

good financial position of organization. In accordance to this, various management accounting

methods can be expressed as:- Product costing and cost allocations:- Project manager and management accountant of

Nisa Ltd determines price incurred on business operations. However, it is done through

different methods for example; marginal, absorption, demand based and market value

costing. It presents income-expenses balance of entity that affects on monetary position

of firm. In this process, cost is decided by manager for production and supplement of

goods. However, allocation of fund can be gained efficiently to create balance of gained

revenue and incurred expenditures (McLaughlin and et.al., 2014). Therefore, product

costing and its effectiveness can be obtained through management accounting process. It

is interconnected with organization's effectiveness and also affects economic

performance of business organization. In accordance to this, adequate pricing for cost

efficiency is applied for allocating fund as well profitability of firm can be enhanced.

However, product costing including price determination on the basis of job order and

processing for expansion of small business unit. In this process, different tools are

applied for setting price of products to be supplied in market to achieve effective

customer satisfaction. It impacts on long term sustainability of product that affects on

competitive strategies of organization. Determining cost of inventory:- Pricing for inventories is determined through this

management accounting tool. It is connected for effective costing and valuable for

systematic production and supplement of goods. Along with this, inventories are get

managed to keep goods safe (McNamee and et.al., 2015). In this process, management

6

summarized and presented for a financial reports and financial statements.

P2) Different management accounting Reports

There are different management accounting methods applied for overall business

operations' management. However, it is beneficial for adequate supplement of goods and services

that impacts on productivity and profitability of firm at high level (Macinati and Anessi-Pessina,

2014). In this regard, actual business performance is obtained for enlargement of entity and

enhancing its quality services. Thus, best use of resources and fund can be achieved to enhance

good financial position of organization. In accordance to this, various management accounting

methods can be expressed as:- Product costing and cost allocations:- Project manager and management accountant of

Nisa Ltd determines price incurred on business operations. However, it is done through

different methods for example; marginal, absorption, demand based and market value

costing. It presents income-expenses balance of entity that affects on monetary position

of firm. In this process, cost is decided by manager for production and supplement of

goods. However, allocation of fund can be gained efficiently to create balance of gained

revenue and incurred expenditures (McLaughlin and et.al., 2014). Therefore, product

costing and its effectiveness can be obtained through management accounting process. It

is interconnected with organization's effectiveness and also affects economic

performance of business organization. In accordance to this, adequate pricing for cost

efficiency is applied for allocating fund as well profitability of firm can be enhanced.

However, product costing including price determination on the basis of job order and

processing for expansion of small business unit. In this process, different tools are

applied for setting price of products to be supplied in market to achieve effective

customer satisfaction. It impacts on long term sustainability of product that affects on

competitive strategies of organization. Determining cost of inventory:- Pricing for inventories is determined through this

management accounting tool. It is connected for effective costing and valuable for

systematic production and supplement of goods. Along with this, inventories are get

managed to keep goods safe (McNamee and et.al., 2015). In this process, management

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accountant analyzes to store inventories at different places as warehouses, stores and

factories. On the basis of which, resource allocation is obtained and further production

and supplement of food and clothing is implemented. However, several ideas are

emerged for inventory management and controlling on its excess. Therefore, costs for

supplying goods and services are incurred on the basis of this productivity and

profitability of organization get impacted. In addition to this, inventory control

management is performed for systematic management of all resources and fund

allocation. Hence, management accounting methods are useful for management of all

inventories of Nisa Ltd that affects product quality and demand for goods. Including this,

management accounting component is liable to increase productivity and profitability that

is interrelated with market sustainability. Cost of inventory is to calculate the cost of

ending inventory using the retail inventory method such as, calculate the cost to retail

percentage. On the other hand calculate the cost of goods where available for sales. This

method is used by retailers that retailers that resell merchandise to estimate their ending

inventory blances.

Planning tools for performance measures for projects:- Management accountant of Nisa

Ltd prepares planning on the basis of recognizing business performance. Similarly, it is

valuable for implementing action plans measuring organizational structure. However,

effective project management is presented including recognizing performance and

increasing efficiency of firm at large scale (Moriarty and et.al., 2015). In this regard,

different goals and determinations are presented as per which varieties of ideas are

created for task accomplishment. It influences productivity and market position of entity

related to further business operations. In addition to this, planning tools including

forecasting and decision making process related to expansion of small scale enterprise

and enhancing quality services that is related to achieve customer satisfaction at

maximum level. Moreover, evaluation of business performance is obtained related to

operations and enlargement of entity thoroughly. In this process, various planning tools

are applied for overall management of Nisa Ltd activities (Nishizaki, Matoba and Nitta,

2014). Therefore, through this management accounting method, increasing in efficiency

for organization and quality services are presented that affects on market value of firm.

7

factories. On the basis of which, resource allocation is obtained and further production

and supplement of food and clothing is implemented. However, several ideas are

emerged for inventory management and controlling on its excess. Therefore, costs for

supplying goods and services are incurred on the basis of this productivity and

profitability of organization get impacted. In addition to this, inventory control

management is performed for systematic management of all resources and fund

allocation. Hence, management accounting methods are useful for management of all

inventories of Nisa Ltd that affects product quality and demand for goods. Including this,

management accounting component is liable to increase productivity and profitability that

is interrelated with market sustainability. Cost of inventory is to calculate the cost of

ending inventory using the retail inventory method such as, calculate the cost to retail

percentage. On the other hand calculate the cost of goods where available for sales. This

method is used by retailers that retailers that resell merchandise to estimate their ending

inventory blances.

Planning tools for performance measures for projects:- Management accountant of Nisa

Ltd prepares planning on the basis of recognizing business performance. Similarly, it is

valuable for implementing action plans measuring organizational structure. However,

effective project management is presented including recognizing performance and

increasing efficiency of firm at large scale (Moriarty and et.al., 2015). In this regard,

different goals and determinations are presented as per which varieties of ideas are

created for task accomplishment. It influences productivity and market position of entity

related to further business operations. In addition to this, planning tools including

forecasting and decision making process related to expansion of small scale enterprise

and enhancing quality services that is related to achieve customer satisfaction at

maximum level. Moreover, evaluation of business performance is obtained related to

operations and enlargement of entity thoroughly. In this process, various planning tools

are applied for overall management of Nisa Ltd activities (Nishizaki, Matoba and Nitta,

2014). Therefore, through this management accounting method, increasing in efficiency

for organization and quality services are presented that affects on market value of firm.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, as per this performance evaluation, different tools and techniques are applied

including costing and budgeting. On behalf of which, several ideas are generated that

affects business and competitive strategies at high level.

Therefore, above mentioned management accounting methods are useful for applying

different strategies to increase business and competitive strategies for effective customer

satisfaction and enhancing presenting actual business performance. Further, these are basic

elements which remains able to expand small scale enterprise as well efficiency of firm can be

increased at large scale. Including this, it is useful for effective business performance and proper

market value for long term sustainability (Sugimoto and et.al., 2015). Moreover, proper strategic

management related to reducing risks and creating positive environment of entity can be

obtained through coordination of employees in team work. Therefore, management accounting

methods are useful to present actual business performance and making decisions for further

operations.

TASK 2

P3) Various costing methods and differences between marginal and absorption costing

Costing is technique for price determination as well prepares income statement that

presents financial position of Nisa Ltd. It is useful approach for production and supplement of

goods and services (Tang, 2015). There are several costing methods applied for further business

operations. For example; marginal, absorption, demand based and competition related. In this

regard, marginal and absorption costing can be described in brief as follows:-

Marginal costing:- Through this costing method, income statement is prepared in simple

manner. In this process, gross profit margin is deducted with cost incurred on variable overheads.

However, it is useful for short term decision-making process that is also effective for getting

adjusted towards uncertain changes occur at workplace. In addition to this, as per this method,

various innovative ideas are created for effective price determination as well valuable for

financial development of small scale enterprise (Anwar and et.al., 2016). However, management

accountant of Nisa Ltd interprets following income statement for further business operations as:-

8

including costing and budgeting. On behalf of which, several ideas are generated that

affects business and competitive strategies at high level.

Therefore, above mentioned management accounting methods are useful for applying

different strategies to increase business and competitive strategies for effective customer

satisfaction and enhancing presenting actual business performance. Further, these are basic

elements which remains able to expand small scale enterprise as well efficiency of firm can be

increased at large scale. Including this, it is useful for effective business performance and proper

market value for long term sustainability (Sugimoto and et.al., 2015). Moreover, proper strategic

management related to reducing risks and creating positive environment of entity can be

obtained through coordination of employees in team work. Therefore, management accounting

methods are useful to present actual business performance and making decisions for further

operations.

TASK 2

P3) Various costing methods and differences between marginal and absorption costing

Costing is technique for price determination as well prepares income statement that

presents financial position of Nisa Ltd. It is useful approach for production and supplement of

goods and services (Tang, 2015). There are several costing methods applied for further business

operations. For example; marginal, absorption, demand based and competition related. In this

regard, marginal and absorption costing can be described in brief as follows:-

Marginal costing:- Through this costing method, income statement is prepared in simple

manner. In this process, gross profit margin is deducted with cost incurred on variable overheads.

However, it is useful for short term decision-making process that is also effective for getting

adjusted towards uncertain changes occur at workplace. In addition to this, as per this method,

various innovative ideas are created for effective price determination as well valuable for

financial development of small scale enterprise (Anwar and et.al., 2016). However, management

accountant of Nisa Ltd interprets following income statement for further business operations as:-

8

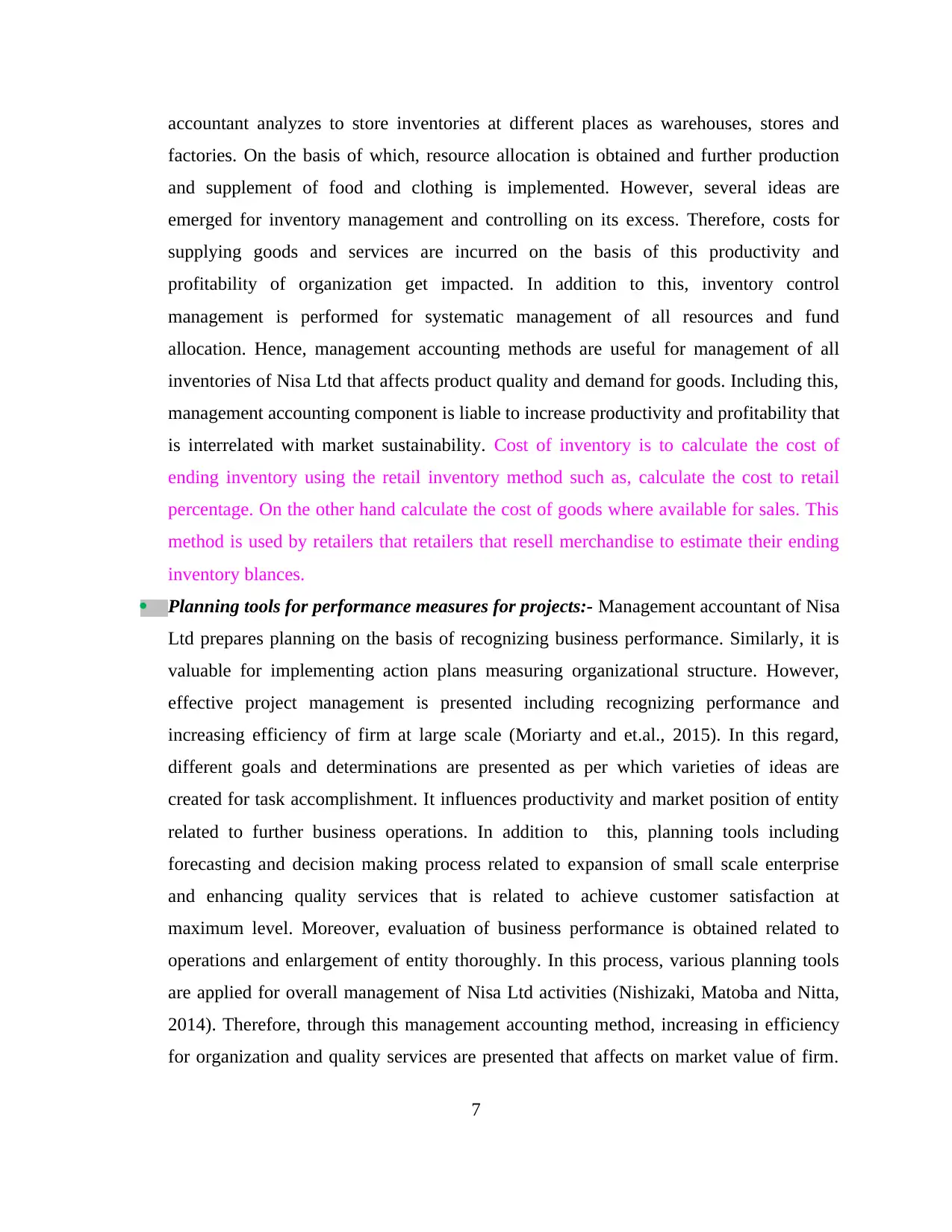

Interpretation:- It has been recognized that cost incurred for selling products is 6600 and

further gained revenue is 21000. Therefore, Nisa Ltd gains gross profit as 14400. On the basis of

this positive outcome, it can be foretasted that company can increase increase its profitability

effectively in future time. Afterwards, net profit margin is obtained by deducting gross profit to

expenses incurred for variable overheads. In accordance to this, it has evaluated that variable

expenditure is 1800 therefore, net profit for organization is 12600. In this process, it is identified

that organization has effective financial position as per several tools and techniques can be

applied for further implementation. Thus, marginal costing method is suitable for decision-

making process related to effectiveness of small scale enterprise.

Absorption costing:- This costing method is appropriate for long term decision-making

process. Under which, for determining net profit, gained gross profit is deducted with total cost

incurred on fixed and variable overheads (Berman, 2015). Therefore, profit margin is determined

in effective manner therefore systematic management of all goods and services can be gained

that affects on productivity and profitability of firm. However, absorption costing is beneficial

for expansion of small scale enterprise and increasing its efficiency can be achieved efficiently.

In this system, management accountant of organization evaluates following income statement as

per which long term, decision-making process is applied for further implementation:-

9

further gained revenue is 21000. Therefore, Nisa Ltd gains gross profit as 14400. On the basis of

this positive outcome, it can be foretasted that company can increase increase its profitability

effectively in future time. Afterwards, net profit margin is obtained by deducting gross profit to

expenses incurred for variable overheads. In accordance to this, it has evaluated that variable

expenditure is 1800 therefore, net profit for organization is 12600. In this process, it is identified

that organization has effective financial position as per several tools and techniques can be

applied for further implementation. Thus, marginal costing method is suitable for decision-

making process related to effectiveness of small scale enterprise.

Absorption costing:- This costing method is appropriate for long term decision-making

process. Under which, for determining net profit, gained gross profit is deducted with total cost

incurred on fixed and variable overheads (Berman, 2015). Therefore, profit margin is determined

in effective manner therefore systematic management of all goods and services can be gained

that affects on productivity and profitability of firm. However, absorption costing is beneficial

for expansion of small scale enterprise and increasing its efficiency can be achieved efficiently.

In this system, management accountant of organization evaluates following income statement as

per which long term, decision-making process is applied for further implementation:-

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

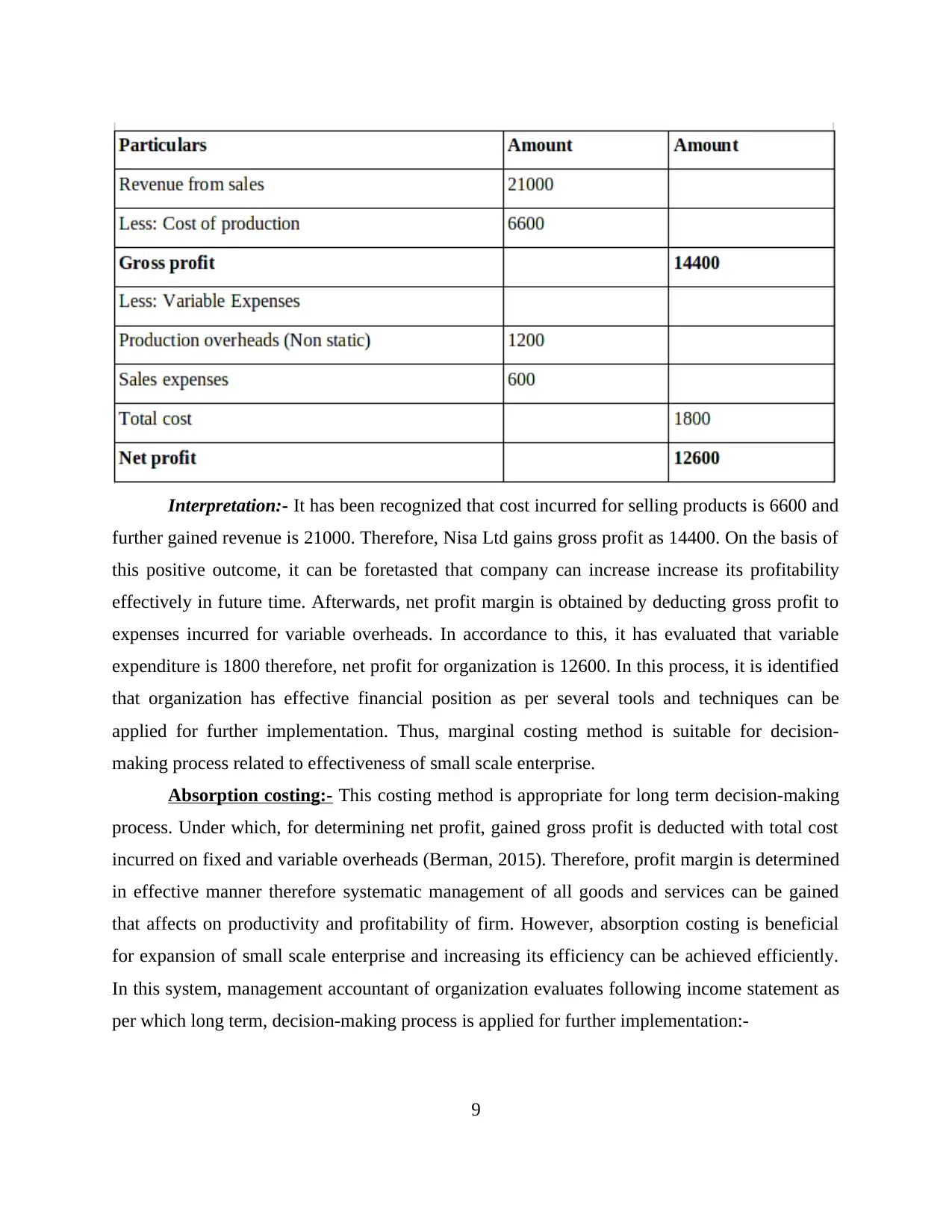

Interpretation:- As per above expressed absorption costing, it is determined for

calculating net profit through absorption costing, gross profit is deducted with total cost incurred

on expenses including variable and fixed. Therefore, gross profit is evaluated as 14400 and

further variable expense is incurred on business operations is 1800. Similarly, fixed expenditure

incurred on expenses is 3300. Therefore, total cost incurred on expenditure is 5100. Further, net

profit is determined by deducting gross profit to total expenditure. Thus, net profit is obtained as

9300. Hence, it can be foretasted that in future time organization can increase its profitability that

affects productivity and effective market position for long term sustainability. Therefore,

expansion of small scale enterprise can be achieved at high level. In this process, ideas can be

generated for long term sustainability of entity at to sustain attraction of customer towards goods

and services provided by small scale enterprise.

10

calculating net profit through absorption costing, gross profit is deducted with total cost incurred

on expenses including variable and fixed. Therefore, gross profit is evaluated as 14400 and

further variable expense is incurred on business operations is 1800. Similarly, fixed expenditure

incurred on expenses is 3300. Therefore, total cost incurred on expenditure is 5100. Further, net

profit is determined by deducting gross profit to total expenditure. Thus, net profit is obtained as

9300. Hence, it can be foretasted that in future time organization can increase its profitability that

affects productivity and effective market position for long term sustainability. Therefore,

expansion of small scale enterprise can be achieved at high level. In this process, ideas can be

generated for long term sustainability of entity at to sustain attraction of customer towards goods

and services provided by small scale enterprise.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

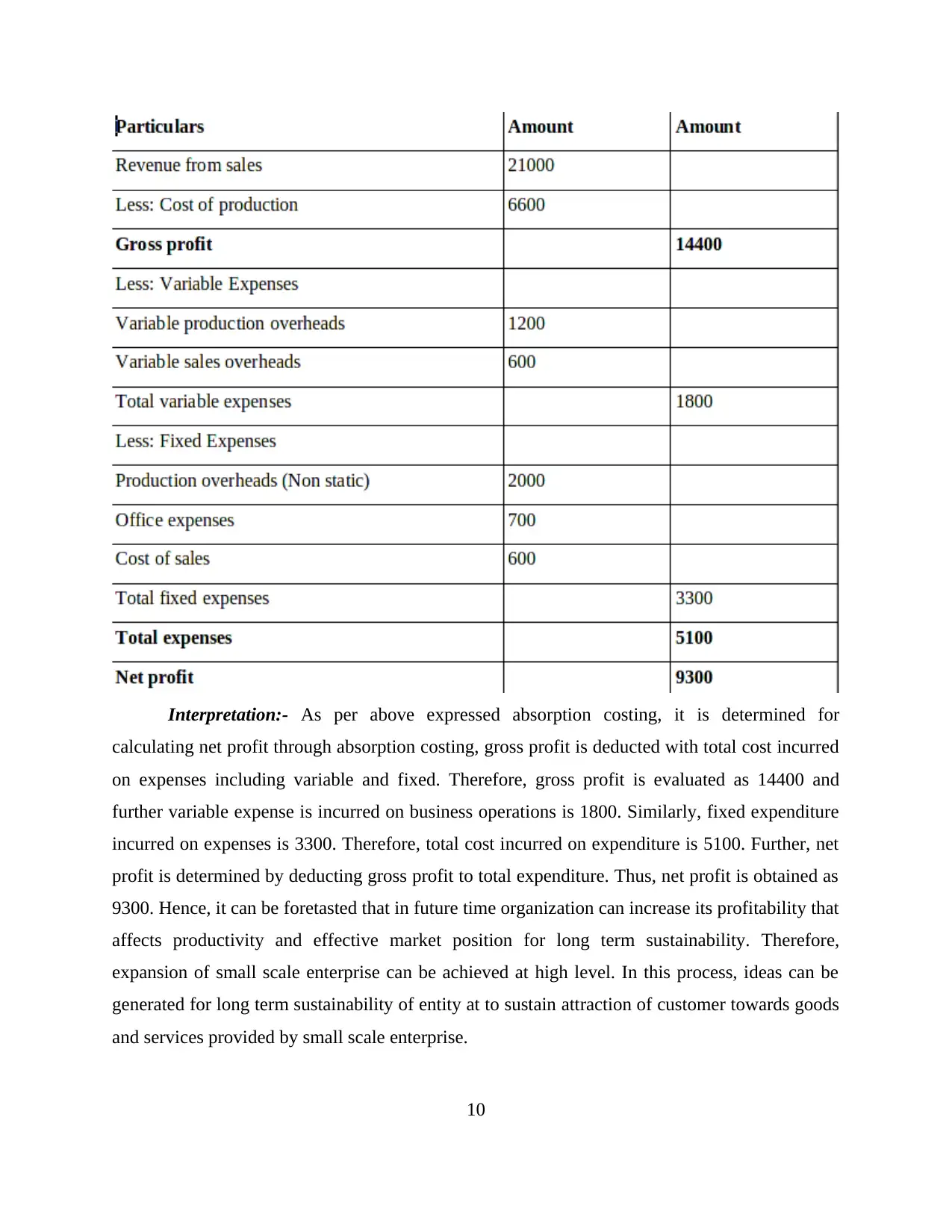

Comparison between marginal and absorption costing:- By comparing marginal to

absorption costing, the main variance between both costing methods is determined as profit

variance (Kreibich and et.al., 2014). In this regard, on the basis of this costing methods, income

statement is prepared that is useful for decision-making process to increase profit earning

capability of Nisa Ltd. Therefore, difference between marginal and absorption costing is

recognized through following tabular form comparison:-

Bases Marginal costing Absorption costing

Profit variance For determining net profit,

gross profit is deducted with

variable cost on expenditures

For evaluating net profit, gross

profit is deducted from total

cost incurred on total

expenditures including fixed

and variable.

Suitable time period for

decision-making process

Appropriate for short term

time

Able to take decisions for long

term decision-making process

Thus, main difference between marginal and absorption costing is profit variation for

preparing income statement. It is interrelated with decision making process as well different

ideas are generated for further business operations. In addition to this, various tools and

techniques are applied to present financial position of entity and decision-making for further

business operations. Therefore, marginal costing is suitable for short term decision-making as

well absorption costing is effective for long term sustainability of firm (Moriarty and et.al.,

2015). Including this, marginal costing is valuable to reduce problems occur at workplace while

absorption costing is appropriate for increasing competitive strategies of organization. However,

various techniques are applied for price determination as well economic structure of firm can be

prepared as per which further implementation can be gained efficiently. Including this, marginal

costing approach believes that only variable expenditures are valuable for determining net profit.

However, absorption costing is related to decision-making process for creating effectiveness of

firm and increasing efficiency of firm at high level. In this regard, it has been evaluated that

marginal costing is appropriate for short term decision-making while absorption costing is

related to long term decision-making process (Tang, 2015). In addition to this, costing is

effective for proper price determination as well able to increase profitability of small scale

enterprise effectively.

11

absorption costing, the main variance between both costing methods is determined as profit

variance (Kreibich and et.al., 2014). In this regard, on the basis of this costing methods, income

statement is prepared that is useful for decision-making process to increase profit earning

capability of Nisa Ltd. Therefore, difference between marginal and absorption costing is

recognized through following tabular form comparison:-

Bases Marginal costing Absorption costing

Profit variance For determining net profit,

gross profit is deducted with

variable cost on expenditures

For evaluating net profit, gross

profit is deducted from total

cost incurred on total

expenditures including fixed

and variable.

Suitable time period for

decision-making process

Appropriate for short term

time

Able to take decisions for long

term decision-making process

Thus, main difference between marginal and absorption costing is profit variation for

preparing income statement. It is interrelated with decision making process as well different

ideas are generated for further business operations. In addition to this, various tools and

techniques are applied to present financial position of entity and decision-making for further

business operations. Therefore, marginal costing is suitable for short term decision-making as

well absorption costing is effective for long term sustainability of firm (Moriarty and et.al.,

2015). Including this, marginal costing is valuable to reduce problems occur at workplace while

absorption costing is appropriate for increasing competitive strategies of organization. However,

various techniques are applied for price determination as well economic structure of firm can be

prepared as per which further implementation can be gained efficiently. Including this, marginal

costing approach believes that only variable expenditures are valuable for determining net profit.

However, absorption costing is related to decision-making process for creating effectiveness of

firm and increasing efficiency of firm at high level. In this regard, it has been evaluated that

marginal costing is appropriate for short term decision-making while absorption costing is

related to long term decision-making process (Tang, 2015). In addition to this, costing is

effective for proper price determination as well able to increase profitability of small scale

enterprise effectively.

11

TASK 3

P4) Critical evaluation on budgetary control systems

Budgeting is considered as a useful approach for forecasting and decision making for

operating business activities systematically. Therefore, management accountant of Nisa Ltd

analyzes entire business operations as per which several ideas are generated to be implemented

in future time. It is interrelated with effectiveness of firm and increasing its efficiency for proper

production and distribution of goods (Lavia and Hiebl, 2014). However, small scale organization

can develop its strategy for facing competition through attracting customers at high level. It

impacts on productivity and profit earning capability of firm. Therefore, best use of resources

and fund is obtained through this process. In accordance to this, budgetary control system is

useful for controlling over excess production and wastage of raw materials. Along with this,

budgeting is beneficial for planning procedure including decision making related to expansion of

small scale organization and enhancing service qualities of firm. Therefore, effectiveness of

organization can be gained at high level. It is helpful to create positive and peaceful atmosphere

of entity by encouraging employees for better work performance and contribute for working in

team. However, critical evaluation on budgeting and budgetary control system can be understood

as follows:-

Positive aspects of budgetary control system:- It is helpful to forecasts and making

decisions related to preparing planning for further business operations. Including this, effective

planning procedure is implemented for applying various techniques to expand Nisa Ltd and

enhancing service qualities of firm at high level (McNamee and et.al., 2015). In this regard,

characteristics of organization can be expressed briefly as below:-

Useful to present actual business performance including various operations of the

organization

Preparing strategies for increasing productivity and profitability of firm

Helpful for adequate utilization of resources and fund

Valuable for effectiveness of entity and increasing its efficiency at high level

Proper planning procedure and decision-making process for effective action planning

Increases strength to face competition as well impacts on competitive strategies

Key component for short term and long term decision-making

12

P4) Critical evaluation on budgetary control systems

Budgeting is considered as a useful approach for forecasting and decision making for

operating business activities systematically. Therefore, management accountant of Nisa Ltd

analyzes entire business operations as per which several ideas are generated to be implemented

in future time. It is interrelated with effectiveness of firm and increasing its efficiency for proper

production and distribution of goods (Lavia and Hiebl, 2014). However, small scale organization

can develop its strategy for facing competition through attracting customers at high level. It

impacts on productivity and profit earning capability of firm. Therefore, best use of resources

and fund is obtained through this process. In accordance to this, budgetary control system is

useful for controlling over excess production and wastage of raw materials. Along with this,

budgeting is beneficial for planning procedure including decision making related to expansion of

small scale organization and enhancing service qualities of firm. Therefore, effectiveness of

organization can be gained at high level. It is helpful to create positive and peaceful atmosphere

of entity by encouraging employees for better work performance and contribute for working in

team. However, critical evaluation on budgeting and budgetary control system can be understood

as follows:-

Positive aspects of budgetary control system:- It is helpful to forecasts and making

decisions related to preparing planning for further business operations. Including this, effective

planning procedure is implemented for applying various techniques to expand Nisa Ltd and

enhancing service qualities of firm at high level (McNamee and et.al., 2015). In this regard,

characteristics of organization can be expressed briefly as below:-

Useful to present actual business performance including various operations of the

organization

Preparing strategies for increasing productivity and profitability of firm

Helpful for adequate utilization of resources and fund

Valuable for effectiveness of entity and increasing its efficiency at high level

Proper planning procedure and decision-making process for effective action planning

Increases strength to face competition as well impacts on competitive strategies

Key component for short term and long term decision-making

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.