Management Accounting Systems and Reporting: Tuffen Mark Ltd Report

VerifiedAdded on 2020/10/05

|18

|5689

|132

Report

AI Summary

This report delves into the application of management accounting principles within Tuffen Mark Ltd, a UK-based ventilation system manufacturer. It begins with an introduction to management accounting, highlighting its importance in internal decision-making, and differentiates it from financial accounting. The report then explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. It also examines different management accounting reporting methods such as ratio analysis, budget reports, credit control reports, job cost reports, inventory reports, and project financial statements. Furthermore, the report outlines the benefits of these systems, such as cost control, efficient resource allocation, and improved decision-making. The report also includes calculations using absorption and marginal costing methods, and analyzes the advantages and disadvantages of planning tools used for budgetary control, emphasizing how management accounting can lead organizations to sustainable success in responding to financial problems. Finally, the report concludes by summarizing the key findings and emphasizes the importance of integrating management accounting systems into business processes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

P2 Different methods that can be used for management accounting reporting .....................3

M1 The benefits of management accounting systems and their application .........................4

D1 Management accounting systems and management reporting is integrated within Tuffen

Mark's processes.....................................................................................................................6

TASK 2............................................................................................................................................7

P3 Calculate the standard cost per ventilation system using absorption costing and marginal

costing method and prepare income statement.......................................................................7

M2 Apply a range of management accounting techniques and produce appropriate financial

reporting documents..............................................................................................................8

D2 Interpret data for a range of business activities................................................................9

TASK 3............................................................................................................................................9

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control ....................................................................................................................................9

M3 Use of different planning tools and their application for preparing and forecasting budgets

..............................................................................................................................................12

TASK 4..........................................................................................................................................12

P5 Compare how different organisations are adapting management accounting systems to

respond to financial problems..............................................................................................12

M4 Analyse how, in responding to financial problems, management accounting can lead these

organisations to sustainable success.....................................................................................13

D3 Planning tools for accounting respond appropriately to solving financial problems to an

organisation to sustainable success .....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems.................................................................................................................1

P2 Different methods that can be used for management accounting reporting .....................3

M1 The benefits of management accounting systems and their application .........................4

D1 Management accounting systems and management reporting is integrated within Tuffen

Mark's processes.....................................................................................................................6

TASK 2............................................................................................................................................7

P3 Calculate the standard cost per ventilation system using absorption costing and marginal

costing method and prepare income statement.......................................................................7

M2 Apply a range of management accounting techniques and produce appropriate financial

reporting documents..............................................................................................................8

D2 Interpret data for a range of business activities................................................................9

TASK 3............................................................................................................................................9

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control ....................................................................................................................................9

M3 Use of different planning tools and their application for preparing and forecasting budgets

..............................................................................................................................................12

TASK 4..........................................................................................................................................12

P5 Compare how different organisations are adapting management accounting systems to

respond to financial problems..............................................................................................12

M4 Analyse how, in responding to financial problems, management accounting can lead these

organisations to sustainable success.....................................................................................13

D3 Planning tools for accounting respond appropriately to solving financial problems to an

organisation to sustainable success .....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is a process that combine finance accounting and cost

accounting with the business skills and techniques. It is provided Financially and non-financially

information to the managers for taking appropriate decisions (Richardson, 2012). The collective

information is providing to managers, investors, creditors and other members to present

performance of the company. The given assignment is based on Tuffen mark Ltd which is a

small family company that designs, manufactures and sells a special air ventilation system in a

competitive UK market. The company has been operating for more than four years and doing

relatively well. In this report Management accounting systems and their requirements are

discussed. Also different methods of management accounting report, management techniques

and planning tools are studied. Assistant management accountant compare ways in which

organisation could use management accounting systems to respond to financial problems and

lead to sustainable success.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems

Management accounting – Management accounting which provide internal information

of the company to improves managers’ ability in decision making and planning process. The

provided information shows ability of company like company's external financing, liquidity,

ability to meet obligation and financial flexibility. The manager of Tuffen mark Ltd uses

information for short term decision making process and prepare strategies according to

performance of an organisation.

Financial accounting – Financial accounting is a specialized branch of accounting that

helps to track all financial transactions with in an organisation. The transactions are shows as

financial report, income statement and balance sheet (Cadez and Guilding, 2012).

Management accounting and financial accounting are part of accounting but both are different in

company perspective -

Basis Management accounting Financial accounting

Meaning Management accounting is process to Financial accounting classifies,

1

Management accounting is a process that combine finance accounting and cost

accounting with the business skills and techniques. It is provided Financially and non-financially

information to the managers for taking appropriate decisions (Richardson, 2012). The collective

information is providing to managers, investors, creditors and other members to present

performance of the company. The given assignment is based on Tuffen mark Ltd which is a

small family company that designs, manufactures and sells a special air ventilation system in a

competitive UK market. The company has been operating for more than four years and doing

relatively well. In this report Management accounting systems and their requirements are

discussed. Also different methods of management accounting report, management techniques

and planning tools are studied. Assistant management accountant compare ways in which

organisation could use management accounting systems to respond to financial problems and

lead to sustainable success.

TASK 1

P1 Management accounting and essential requirements of different types of management

accounting systems

Management accounting – Management accounting which provide internal information

of the company to improves managers’ ability in decision making and planning process. The

provided information shows ability of company like company's external financing, liquidity,

ability to meet obligation and financial flexibility. The manager of Tuffen mark Ltd uses

information for short term decision making process and prepare strategies according to

performance of an organisation.

Financial accounting – Financial accounting is a specialized branch of accounting that

helps to track all financial transactions with in an organisation. The transactions are shows as

financial report, income statement and balance sheet (Cadez and Guilding, 2012).

Management accounting and financial accounting are part of accounting but both are different in

company perspective -

Basis Management accounting Financial accounting

Meaning Management accounting is process to Financial accounting classifies,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

preparing accounts and reports to

make short term and day to day

decision.

analysis and summarises the

financial transaction of the

company.

Application It helps to management to take

meaningful steps and make effective

strategies (Cuganesan, Dunford and

Palmer, 2012).

It is prepared to present accurate and

fair information of financial

transactions.

Measuring grid Management accounting measure

quantitative and qualitative data.

Financial accounting only measures

quantitative data.

Dependence Management accounting depends on

financial accounting and cost

accounting.

It is not dependent on management

accounting.

Different types of management accounting systems -

Cost accounting system -

A cost accounting system is a framework which is used by manufactures to record

production activities using a perceptual inventory system. It is used to estimate the profitability

analysis, cost control and inventory valuation of their products in Tuffen mark Ltd. But cost

accounting system is not measuring accurate cost of products of the company.

Inventory management system -

An inventory management system is the combination of processes, technology and

procedures that helps to monitor and maintenance of stocked products of Tuffen mark Ltd. It is

very important system that determines ordering stock, storage of stock and controlling the

amount of goods. The system provides help to take decisions regarding to inventory like re-order

quantities, manage stock levels and quality of goods (ter Bogt and van Helden, 2012).

Job costing system -

A job costing system including the process of collect information about the costs which

are related to a specific production or service job in Tuffen mark Ltd. The collective information

is useful to determine the accuracy of company's estimating system. The information used by

manager to assign inventorial costs to manufactured goods.

2

make short term and day to day

decision.

analysis and summarises the

financial transaction of the

company.

Application It helps to management to take

meaningful steps and make effective

strategies (Cuganesan, Dunford and

Palmer, 2012).

It is prepared to present accurate and

fair information of financial

transactions.

Measuring grid Management accounting measure

quantitative and qualitative data.

Financial accounting only measures

quantitative data.

Dependence Management accounting depends on

financial accounting and cost

accounting.

It is not dependent on management

accounting.

Different types of management accounting systems -

Cost accounting system -

A cost accounting system is a framework which is used by manufactures to record

production activities using a perceptual inventory system. It is used to estimate the profitability

analysis, cost control and inventory valuation of their products in Tuffen mark Ltd. But cost

accounting system is not measuring accurate cost of products of the company.

Inventory management system -

An inventory management system is the combination of processes, technology and

procedures that helps to monitor and maintenance of stocked products of Tuffen mark Ltd. It is

very important system that determines ordering stock, storage of stock and controlling the

amount of goods. The system provides help to take decisions regarding to inventory like re-order

quantities, manage stock levels and quality of goods (ter Bogt and van Helden, 2012).

Job costing system -

A job costing system including the process of collect information about the costs which

are related to a specific production or service job in Tuffen mark Ltd. The collective information

is useful to determine the accuracy of company's estimating system. The information used by

manager to assign inventorial costs to manufactured goods.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Batch costing system -

It is similar to job costing system but for this method apply cost units of products system.

A batch consists of a specific number of goods and units. Batch cost is used to find out the cost

per unit and whether Tuffen mark Ltd want to get lower cost of stock. The company has to work

out economic batch quantity with the help of economic order quantity.

Price optimising system -

The price optimising system is a mathematical tool that helps to calculate demand of

products at different price stages and then combine the data with information on costs and

inventory levels to recommend prices that will improve profits (Merchant, 2012). The system

can be used of tailor pricing for different segments of customers and see respond of price

changes.

P2 Different methods that can be used for management accounting reporting

There are some important methods which are broadly used by Tuffen mark Ltd for the

determinate purpose of management accounting reporting. They are as following -

Ratio analysis: -

It is a quantitative analysis of information that can contained in a company's financial

statements. They are calculated on financial performance of the business access on how business

can perform various operating activities. For example, gross margin profit ratio of company will

inform management how much gross profit that mark Tuffen mark Ltd can earn to increase

percentage of sales value. If a company gross margin is 35%, then it means company can retain

$0.35 from each dollar the revenue will generate (Tappura and et. Al, 2015). This will help

management accounting to determine various ratios profits that can analyse risk and make

profits.

Budget report: -

Budget report is an internal report used by management to compare estimated budget

projections with actual performance. They are used for planning and decision making by

management of business. For example, the business budgeted $10,000 for expenses but actually

they spend $12,000, then management will be in position to investigate all variances. This will

help management accounting to make small business owners to analyse business performance

and managers can analyse the departmental performance and can control costs. Budgeted funds

may be given out as bonuses for meeting specific financial goals.

3

It is similar to job costing system but for this method apply cost units of products system.

A batch consists of a specific number of goods and units. Batch cost is used to find out the cost

per unit and whether Tuffen mark Ltd want to get lower cost of stock. The company has to work

out economic batch quantity with the help of economic order quantity.

Price optimising system -

The price optimising system is a mathematical tool that helps to calculate demand of

products at different price stages and then combine the data with information on costs and

inventory levels to recommend prices that will improve profits (Merchant, 2012). The system

can be used of tailor pricing for different segments of customers and see respond of price

changes.

P2 Different methods that can be used for management accounting reporting

There are some important methods which are broadly used by Tuffen mark Ltd for the

determinate purpose of management accounting reporting. They are as following -

Ratio analysis: -

It is a quantitative analysis of information that can contained in a company's financial

statements. They are calculated on financial performance of the business access on how business

can perform various operating activities. For example, gross margin profit ratio of company will

inform management how much gross profit that mark Tuffen mark Ltd can earn to increase

percentage of sales value. If a company gross margin is 35%, then it means company can retain

$0.35 from each dollar the revenue will generate (Tappura and et. Al, 2015). This will help

management accounting to determine various ratios profits that can analyse risk and make

profits.

Budget report: -

Budget report is an internal report used by management to compare estimated budget

projections with actual performance. They are used for planning and decision making by

management of business. For example, the business budgeted $10,000 for expenses but actually

they spend $12,000, then management will be in position to investigate all variances. This will

help management accounting to make small business owners to analyse business performance

and managers can analyse the departmental performance and can control costs. Budgeted funds

may be given out as bonuses for meeting specific financial goals.

3

Credit control report: -

It may explain how much credit was given to customers and in how much period. Report

can include strategies employed by business to accelerate sales of product or services through

extension of credit given to customers or clients. Business prefer to extend credit to good and

limits credit for weak position depending upon Tuffen mark Ltd financial position.

Job cost report: -

It is a report used to find out how much amount used to spend for completion of job. For

an accounting system to support job costing, it can follow many jobs to be assigned for

individuals. It may assess all costs involved in a construction job use or in a manufactured of

goods that are given to company. These costs are recorded in ledger accounts throughout life of

job before preparing of job cost or batch manufacturing statement (Li and et. Al, 2012).

Inventory and manufacturing report: -

The report used to find out how much inventory being used for manufactured department

to make budget production units. The report used to provide values of trade and business sales

and provide inventories to manufactures, retailers and wholesalers. For example, Tuffen mark

Ltd can used raw materials such as steel of make air ventilators, work in progress to make

components in manufacturing business, finished goods to assemble all parts and this can help

company to enhance business that can make future able profits to gain competency. It is the

biggest mark on inventory line item of balance sheet that can reflects directly or indirectly cost

item of company that can help managers to describe a level of stock that can mitigate risk of

stock outs or due to uncertainties in supply and demand (Kihn and Ihantola, 2015).

Project financial statements: -

This statement is used to prepare projected financial statements to make the long term

targets in business. It shows summary of income statements and balance sheet of mark tuffin that

can have expense considerations which include step costs to find revenue can have increased or

decline. This statement will indicate whether a business is going on a right direction or not, it is

making long term or short term goals. Hence the company would take right decisions and

financial results will be delivered in a good way. It helps a company to make risk easy so that

they can make financial results or make variables to take competitive advantage for mark tuffen

Ltd (Vosselman, 2014).

4

It may explain how much credit was given to customers and in how much period. Report

can include strategies employed by business to accelerate sales of product or services through

extension of credit given to customers or clients. Business prefer to extend credit to good and

limits credit for weak position depending upon Tuffen mark Ltd financial position.

Job cost report: -

It is a report used to find out how much amount used to spend for completion of job. For

an accounting system to support job costing, it can follow many jobs to be assigned for

individuals. It may assess all costs involved in a construction job use or in a manufactured of

goods that are given to company. These costs are recorded in ledger accounts throughout life of

job before preparing of job cost or batch manufacturing statement (Li and et. Al, 2012).

Inventory and manufacturing report: -

The report used to find out how much inventory being used for manufactured department

to make budget production units. The report used to provide values of trade and business sales

and provide inventories to manufactures, retailers and wholesalers. For example, Tuffen mark

Ltd can used raw materials such as steel of make air ventilators, work in progress to make

components in manufacturing business, finished goods to assemble all parts and this can help

company to enhance business that can make future able profits to gain competency. It is the

biggest mark on inventory line item of balance sheet that can reflects directly or indirectly cost

item of company that can help managers to describe a level of stock that can mitigate risk of

stock outs or due to uncertainties in supply and demand (Kihn and Ihantola, 2015).

Project financial statements: -

This statement is used to prepare projected financial statements to make the long term

targets in business. It shows summary of income statements and balance sheet of mark tuffin that

can have expense considerations which include step costs to find revenue can have increased or

decline. This statement will indicate whether a business is going on a right direction or not, it is

making long term or short term goals. Hence the company would take right decisions and

financial results will be delivered in a good way. It helps a company to make risk easy so that

they can make financial results or make variables to take competitive advantage for mark tuffen

Ltd (Vosselman, 2014).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1 The benefits of management accounting systems and their application

There is following benefits of management accounting and their application -

Cost accounting system -

It provides help management of tuffen mark Ltd and they can arrange the plan and

implement on the system for successful enterprises action of business. In this system, several

functional budget costs which are rearranged in section wise, department wise and product wise

for planning all resources that can well efficient use of resource to make management policies

and fully make plans and objectives of company so that the Tuffen mark ltd can analyse all risk

that can gather needs and requirements of an organisation.

Price optimization system: -

The actual performance of all business movement is compared and measured efficiently.

With the help of price optimization level and resources are well organized so that plans can be

utilized and knowledge can gain. If deviations are establishing that convenient, the management

of Tuffen mark ltd can decide guiding principle to exercise full control over management and

resources are well established (Adler, 2013). Both budgetary control system and standard costing

are related to price optimization that can highly help management in this aspect.

Inventory management system-

The system is used for identifying inventory item that can make products in efficient

manner. It is utilised in the manufacturing industry to create work order, bill of materials and

other production related documents that can help to organize inventory data to reorder the

product. The tuffent mark ltd with the help of this system track goods on every stages of

production and reduce wastages.

Job costing system: -

It can involve process to accumulate information about costs with a specific production

or service job. For example, Tuffen mark Ltd start up a job and in the month of first operations,

the job accumulates $10,000 of direct costs, $4,500 of direct labour costs, and allocated $2,000

of overhead expense. Thus at the end of month, system has compiled a total of $16,500 for job

they have started. This cost is temporarily stored of overhead expense. ABC then completes the

job and bills of customer. At that time $16,500 is transferred out of inventory in cost of goods

sold. Job costing of mark Tuffen mark Ltd are related to contact and batch costing methods are

used in construction, motion picture and shipping industries (Nitzl, 2016).

5

There is following benefits of management accounting and their application -

Cost accounting system -

It provides help management of tuffen mark Ltd and they can arrange the plan and

implement on the system for successful enterprises action of business. In this system, several

functional budget costs which are rearranged in section wise, department wise and product wise

for planning all resources that can well efficient use of resource to make management policies

and fully make plans and objectives of company so that the Tuffen mark ltd can analyse all risk

that can gather needs and requirements of an organisation.

Price optimization system: -

The actual performance of all business movement is compared and measured efficiently.

With the help of price optimization level and resources are well organized so that plans can be

utilized and knowledge can gain. If deviations are establishing that convenient, the management

of Tuffen mark ltd can decide guiding principle to exercise full control over management and

resources are well established (Adler, 2013). Both budgetary control system and standard costing

are related to price optimization that can highly help management in this aspect.

Inventory management system-

The system is used for identifying inventory item that can make products in efficient

manner. It is utilised in the manufacturing industry to create work order, bill of materials and

other production related documents that can help to organize inventory data to reorder the

product. The tuffent mark ltd with the help of this system track goods on every stages of

production and reduce wastages.

Job costing system: -

It can involve process to accumulate information about costs with a specific production

or service job. For example, Tuffen mark Ltd start up a job and in the month of first operations,

the job accumulates $10,000 of direct costs, $4,500 of direct labour costs, and allocated $2,000

of overhead expense. Thus at the end of month, system has compiled a total of $16,500 for job

they have started. This cost is temporarily stored of overhead expense. ABC then completes the

job and bills of customer. At that time $16,500 is transferred out of inventory in cost of goods

sold. Job costing of mark Tuffen mark Ltd are related to contact and batch costing methods are

used in construction, motion picture and shipping industries (Nitzl, 2016).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1 Management accounting systems and management reporting is integrated within Tuffen

Mark's processes

The management accounting system and management accounting reports both are

important of organisational process. The accounting system provides internal information of

company regarding to different management reports.

Types of reporting Integration with organisational processes

Budget report The integration between Tuffen Mark's processes and

budgeting reports makes a path for the organisation

activities to concentrate on targeted results and objectives in

better and effective way.

Project financial statements This report provides financial information of Tuffen Mark

and it helps to management to taking effective decision

regarding to organisational process.

Inventory and manufacturing

report

The integration between processes involved in Tuffen Mark

Ltd and this report provides better management. With the

help of this report know about different levels of inventory

and required stock on every stage. It helps to know

manufacturing cost at each stage of inventory and observe

manufacturing process to reduce waste of stock (Edwards

and Boyns, 2012).

Job cost report The job cost report provides to prepare pricing strategy of

Tuffen Mark and it will analysis cost of products and try to

reduce overall cost of stocks. It will help to determine the

objectives of company. With the help of this report know

about cost of organisational process in proper way.

Credit control report The report of credit control integrates with Tuffen Mark's

process for achieve objectives and collect information of

accounts receivable on timely. It create proper collection

policy on time for make effective organisational process in

6

Mark's processes

The management accounting system and management accounting reports both are

important of organisational process. The accounting system provides internal information of

company regarding to different management reports.

Types of reporting Integration with organisational processes

Budget report The integration between Tuffen Mark's processes and

budgeting reports makes a path for the organisation

activities to concentrate on targeted results and objectives in

better and effective way.

Project financial statements This report provides financial information of Tuffen Mark

and it helps to management to taking effective decision

regarding to organisational process.

Inventory and manufacturing

report

The integration between processes involved in Tuffen Mark

Ltd and this report provides better management. With the

help of this report know about different levels of inventory

and required stock on every stage. It helps to know

manufacturing cost at each stage of inventory and observe

manufacturing process to reduce waste of stock (Edwards

and Boyns, 2012).

Job cost report The job cost report provides to prepare pricing strategy of

Tuffen Mark and it will analysis cost of products and try to

reduce overall cost of stocks. It will help to determine the

objectives of company. With the help of this report know

about cost of organisational process in proper way.

Credit control report The report of credit control integrates with Tuffen Mark's

process for achieve objectives and collect information of

accounts receivable on timely. It create proper collection

policy on time for make effective organisational process in

6

accuracy and flexibility manner.

TASK 2

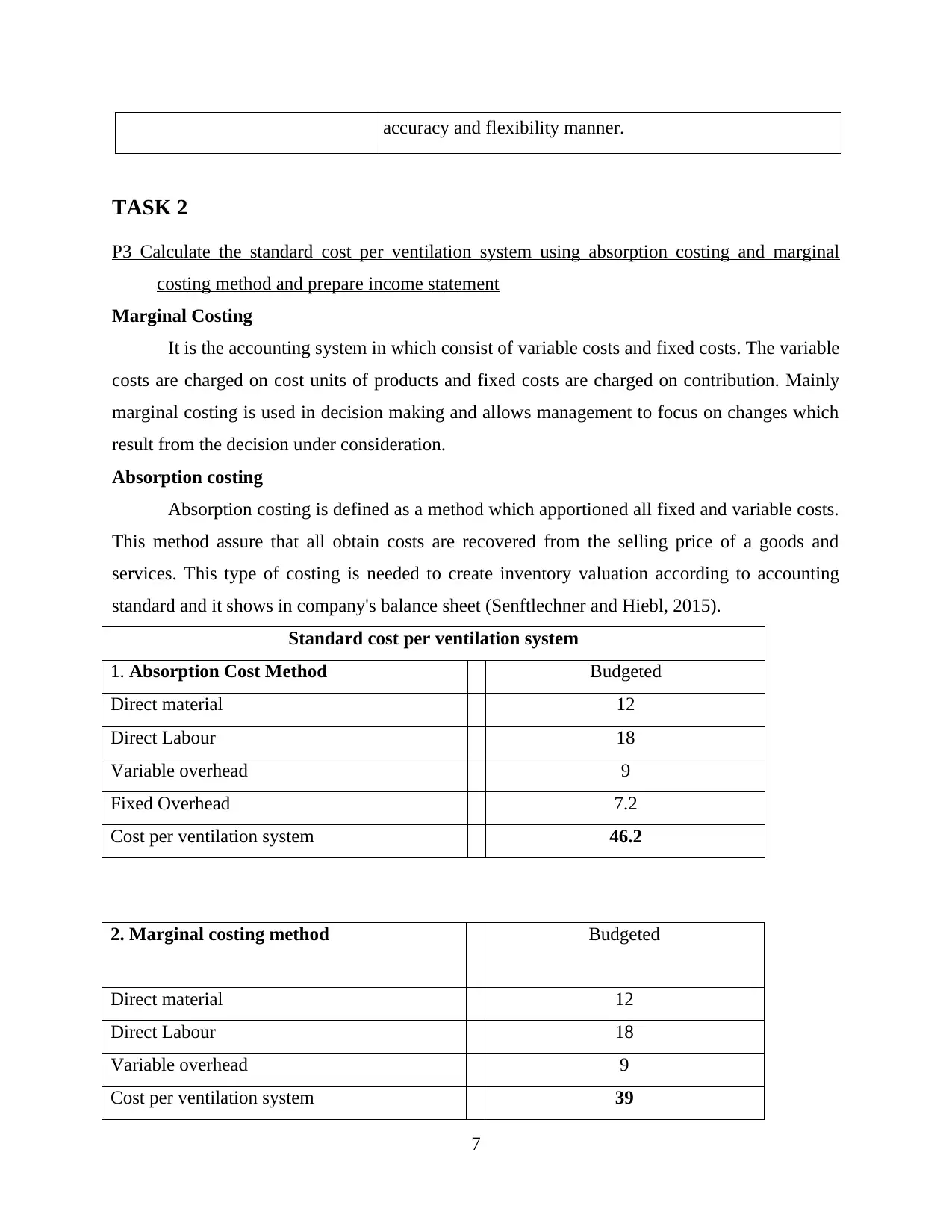

P3 Calculate the standard cost per ventilation system using absorption costing and marginal

costing method and prepare income statement

Marginal Costing

It is the accounting system in which consist of variable costs and fixed costs. The variable

costs are charged on cost units of products and fixed costs are charged on contribution. Mainly

marginal costing is used in decision making and allows management to focus on changes which

result from the decision under consideration.

Absorption costing

Absorption costing is defined as a method which apportioned all fixed and variable costs.

This method assure that all obtain costs are recovered from the selling price of a goods and

services. This type of costing is needed to create inventory valuation according to accounting

standard and it shows in company's balance sheet (Senftlechner and Hiebl, 2015).

Standard cost per ventilation system

1. Absorption Cost Method Budgeted

Direct material 12

Direct Labour 18

Variable overhead 9

Fixed Overhead 7.2

Cost per ventilation system 46.2

2. Marginal costing method Budgeted

Direct material 12

Direct Labour 18

Variable overhead 9

Cost per ventilation system 39

7

TASK 2

P3 Calculate the standard cost per ventilation system using absorption costing and marginal

costing method and prepare income statement

Marginal Costing

It is the accounting system in which consist of variable costs and fixed costs. The variable

costs are charged on cost units of products and fixed costs are charged on contribution. Mainly

marginal costing is used in decision making and allows management to focus on changes which

result from the decision under consideration.

Absorption costing

Absorption costing is defined as a method which apportioned all fixed and variable costs.

This method assure that all obtain costs are recovered from the selling price of a goods and

services. This type of costing is needed to create inventory valuation according to accounting

standard and it shows in company's balance sheet (Senftlechner and Hiebl, 2015).

Standard cost per ventilation system

1. Absorption Cost Method Budgeted

Direct material 12

Direct Labour 18

Variable overhead 9

Fixed Overhead 7.2

Cost per ventilation system 46.2

2. Marginal costing method Budgeted

Direct material 12

Direct Labour 18

Variable overhead 9

Cost per ventilation system 39

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

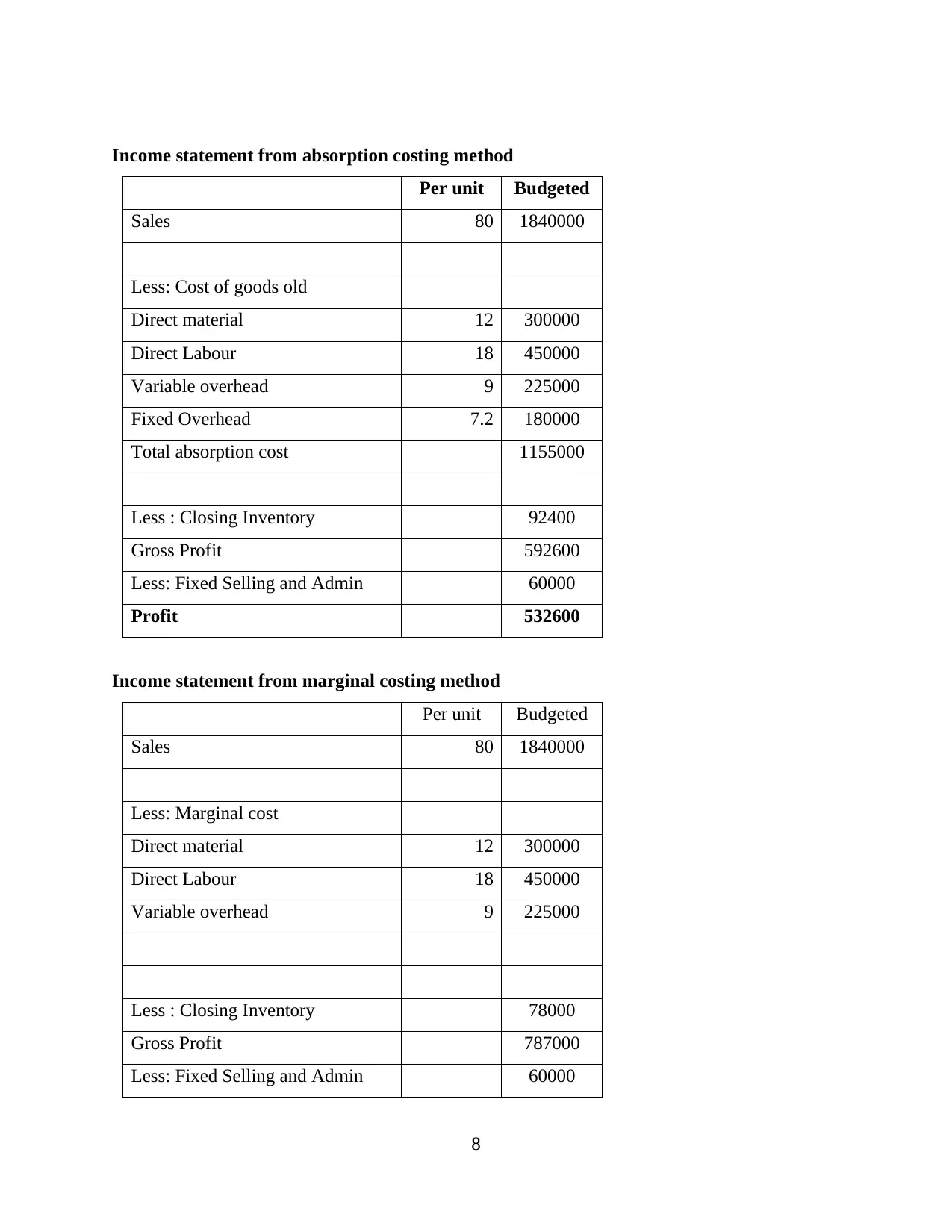

Income statement from absorption costing method

Per unit Budgeted

Sales 80 1840000

Less: Cost of goods old

Direct material 12 300000

Direct Labour 18 450000

Variable overhead 9 225000

Fixed Overhead 7.2 180000

Total absorption cost 1155000

Less : Closing Inventory 92400

Gross Profit 592600

Less: Fixed Selling and Admin 60000

Profit 532600

Income statement from marginal costing method

Per unit Budgeted

Sales 80 1840000

Less: Marginal cost

Direct material 12 300000

Direct Labour 18 450000

Variable overhead 9 225000

Less : Closing Inventory 78000

Gross Profit 787000

Less: Fixed Selling and Admin 60000

8

Per unit Budgeted

Sales 80 1840000

Less: Cost of goods old

Direct material 12 300000

Direct Labour 18 450000

Variable overhead 9 225000

Fixed Overhead 7.2 180000

Total absorption cost 1155000

Less : Closing Inventory 92400

Gross Profit 592600

Less: Fixed Selling and Admin 60000

Profit 532600

Income statement from marginal costing method

Per unit Budgeted

Sales 80 1840000

Less: Marginal cost

Direct material 12 300000

Direct Labour 18 450000

Variable overhead 9 225000

Less : Closing Inventory 78000

Gross Profit 787000

Less: Fixed Selling and Admin 60000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Overhead 180000

Profit 547000

M2 Apply a range of management accounting techniques and produce appropriate financial

reporting documents

Cost analysis

The cost analysis refers to the analysis of the cost in systematic way to predict the

strengths and weakness of transactions cost, function of business and business activities.

Standard cost from absorption cost method 46.2 budgeted and actual 48.4 and from marginal cost

method budgeted 39 and actual 39.285 units.

CVP analysis

Cost volume profit analysis is a method of cost accounting that impact to various levels

of costs. The analysis helps to make various assumptions related to sales price, fixed costs and

variable costs (Fourie and et. Al, 2015).

Cost variances

Cost variance analysis is the technique to quantitative approach to know difference

between actual and planned behaviour. The analysis helps to maintain business and also control

their activities.

D2 Interpret data for a range of business activities

As per above calculations of income statement by implementing marginal and absorption

costing profit is calculated as £625000 of budgeted and £625000 of actual units.

TASK 3

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control

Budgetary control – It is a process for managers to utilize budgets to evaluate and control

costs in particular time period. It helps to managers to set their financial and performance goals

with budgets. And compare actual results with forecasting result (Budgetary control, 2018.).

Budget - It is financial plan for a defined period often for one year that can include planned

sales volume and revenues, resource, qualities, cost and expenses, assets and liabilities and cash

flows.

9

Profit 547000

M2 Apply a range of management accounting techniques and produce appropriate financial

reporting documents

Cost analysis

The cost analysis refers to the analysis of the cost in systematic way to predict the

strengths and weakness of transactions cost, function of business and business activities.

Standard cost from absorption cost method 46.2 budgeted and actual 48.4 and from marginal cost

method budgeted 39 and actual 39.285 units.

CVP analysis

Cost volume profit analysis is a method of cost accounting that impact to various levels

of costs. The analysis helps to make various assumptions related to sales price, fixed costs and

variable costs (Fourie and et. Al, 2015).

Cost variances

Cost variance analysis is the technique to quantitative approach to know difference

between actual and planned behaviour. The analysis helps to maintain business and also control

their activities.

D2 Interpret data for a range of business activities

As per above calculations of income statement by implementing marginal and absorption

costing profit is calculated as £625000 of budgeted and £625000 of actual units.

TASK 3

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control

Budgetary control – It is a process for managers to utilize budgets to evaluate and control

costs in particular time period. It helps to managers to set their financial and performance goals

with budgets. And compare actual results with forecasting result (Budgetary control, 2018.).

Budget - It is financial plan for a defined period often for one year that can include planned

sales volume and revenues, resource, qualities, cost and expenses, assets and liabilities and cash

flows.

9

Different types of budgets-

Static budgeting - It is a classical form of budgeting that can creates model of expected

results and financial position for next year and can give expected results during a given period of

time. It also tends to introduce a rigidity into an organization to allow ongoing changes in

environment. They are basically compared with expected results. It can use to find actual cost

that can have competitive firms. A static budget is more useful when sales would be expected

and more result are required. This budget depends on single outcome which can be difficult to

achieve (Bobrysheva and et. Al, 2015).

Zero- based budgeting - It can determine what outcome that management wants to

develop package of expenditures that can support an organization. It can use in several service

entities such as government where services are paramount. The goal of zero-based budgeting is

to reduce spending by looking where cost has been cut.

Flexible budgeting - It allows to enter different sales, which will adjust planning expense

that has been entered. This approach can be different when sales are not required to estimate and

single proportion of expense vary with sales, it is difficult to prepare static budget because cost

can compare with actual results and distribution expense will vary with sales.

Incremental budgeting - It is a budget which is used to prepare that is used in period

budget or actual performance as a basis with incremental amounts added for new budget period

that allocate resources which is stable and can change gradual. There may be budget slack built

into budget, which is never reviewed managers might have overestimated their requirements in

the past (Sajady, Dastgir and Nejad, 2012).

Rolling budget - It is continually budget period as the most recent period completed.

Thus, rolling budget involves incremental extension of the existing budget model. It has

provided advantage of someone constantly attend to the budget model and revise budget

assumptions for the last incremental period of budget that can have some efficiency to make

rolling budget

Budgetary preparation acting as planning tool -

The process of preparing budgets provides certain benefits to company. Budgets are used

as planning tools for predict income and expenses of company and applied in better way. For

preparation of budget need to strategic tool and forecasting tool.

Strategic tools used for budgetary control planning with advantages and disadvantages

10

Static budgeting - It is a classical form of budgeting that can creates model of expected

results and financial position for next year and can give expected results during a given period of

time. It also tends to introduce a rigidity into an organization to allow ongoing changes in

environment. They are basically compared with expected results. It can use to find actual cost

that can have competitive firms. A static budget is more useful when sales would be expected

and more result are required. This budget depends on single outcome which can be difficult to

achieve (Bobrysheva and et. Al, 2015).

Zero- based budgeting - It can determine what outcome that management wants to

develop package of expenditures that can support an organization. It can use in several service

entities such as government where services are paramount. The goal of zero-based budgeting is

to reduce spending by looking where cost has been cut.

Flexible budgeting - It allows to enter different sales, which will adjust planning expense

that has been entered. This approach can be different when sales are not required to estimate and

single proportion of expense vary with sales, it is difficult to prepare static budget because cost

can compare with actual results and distribution expense will vary with sales.

Incremental budgeting - It is a budget which is used to prepare that is used in period

budget or actual performance as a basis with incremental amounts added for new budget period

that allocate resources which is stable and can change gradual. There may be budget slack built

into budget, which is never reviewed managers might have overestimated their requirements in

the past (Sajady, Dastgir and Nejad, 2012).

Rolling budget - It is continually budget period as the most recent period completed.

Thus, rolling budget involves incremental extension of the existing budget model. It has

provided advantage of someone constantly attend to the budget model and revise budget

assumptions for the last incremental period of budget that can have some efficiency to make

rolling budget

Budgetary preparation acting as planning tool -

The process of preparing budgets provides certain benefits to company. Budgets are used

as planning tools for predict income and expenses of company and applied in better way. For

preparation of budget need to strategic tool and forecasting tool.

Strategic tools used for budgetary control planning with advantages and disadvantages

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.