Management Accounting II: Orange Mount Bikes Case Study Report

VerifiedAdded on 2021/04/21

|8

|2086

|75

Report

AI Summary

This report, prepared for a Management Accounting II course, analyzes a case study involving Orange Mount Bikes and the implementation of a new braking system. The report examines the concept of target costing, a system used to determine the life-cycle cost of a product while maintaining a desired profit margin. It explores the formation of a team tasked with reducing manufacturing costs, including personnel from marketing, engineering, purchasing, accounting, and administration. The report details the team's strategies for cost reduction, such as redesigning the product and optimizing selling and distribution costs. Furthermore, it presents a cost structure analysis and discusses the advantages and limitations of target costing, emphasizing its role in marketing, product quality, and management control. The report concludes by highlighting the importance of target costing in today's competitive market, despite its potential drawbacks.

Running head: MANAGEMENT ACCOUNTING II

Management Accounting II

Name of the Student:

Name of the University:

Author Note

Management Accounting II

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING II

Table of Contents

Part A...............................................................................................................................................2

Answer to Question (i).................................................................................................................2

Answer to Question (ii)...............................................................................................................2

Answer to Question (iii)..............................................................................................................3

Part B...............................................................................................................................................4

References........................................................................................................................................7

MANAGEMENT ACCOUNTING II

Table of Contents

Part A...............................................................................................................................................2

Answer to Question (i).................................................................................................................2

Answer to Question (ii)...............................................................................................................2

Answer to Question (iii)..............................................................................................................3

Part B...............................................................................................................................................4

References........................................................................................................................................7

2

MANAGEMENT ACCOUNTING II

Part A

Answer to Question (i)

The issue presented in the case study is that Orange Mount Bikes had been considering

the introduction of the new braking system that permits the bikers for descending the slopes are

steep by utilizing the newly developed braking pattern. The firm has been considering launching

a new line of products having the newly developed design of brakes. However, it must be noted

here that the firm utilizes target costing as a part of the costing structure. Target costing refers to

the particular system of costing that determines the life-cycle cost of the product that would be

enough to develop the particulars of the product without compromising on the desired amount of

profit.

Now, the question that has been presented aims to look into the fact as to why Vanessa

had formed a team in order to manage the manufacturing design of the product. Vanessa carries

out such a task because the company follows the procedure of target costing and in order to

acquire the desired amount of profit, the target cost should be fixed at £855. However, with the

newly integrated biking system the cost is coming up at £905. Therefore, the team that has been

appointed by the Vanessa consists of a marketing expert who will think of the marketing

strategies that may be adopted in order to reduce the cost of manufacturing the bike. The team

also consists of the engineering, purchasing, accounting and administration personnel who can

further give their recommendation for reducing the cost of manufacturing the product. The

engineer might further redesign the product for reducing the cost. The primary purpose of the

formed team is to assemble information in regards to the current costs and develop methods for

reducing the cost of manufacturing the product.

Answer to Question (ii)

The structure of the team and the potential areas that are considered by the newly formed

team for reducing the cost of the product are as follows:

The team that has been formed by Vanessa consists of a marketing personnel, engineer,

purchasing personnel and accounting and administration personnel.

MANAGEMENT ACCOUNTING II

Part A

Answer to Question (i)

The issue presented in the case study is that Orange Mount Bikes had been considering

the introduction of the new braking system that permits the bikers for descending the slopes are

steep by utilizing the newly developed braking pattern. The firm has been considering launching

a new line of products having the newly developed design of brakes. However, it must be noted

here that the firm utilizes target costing as a part of the costing structure. Target costing refers to

the particular system of costing that determines the life-cycle cost of the product that would be

enough to develop the particulars of the product without compromising on the desired amount of

profit.

Now, the question that has been presented aims to look into the fact as to why Vanessa

had formed a team in order to manage the manufacturing design of the product. Vanessa carries

out such a task because the company follows the procedure of target costing and in order to

acquire the desired amount of profit, the target cost should be fixed at £855. However, with the

newly integrated biking system the cost is coming up at £905. Therefore, the team that has been

appointed by the Vanessa consists of a marketing expert who will think of the marketing

strategies that may be adopted in order to reduce the cost of manufacturing the bike. The team

also consists of the engineering, purchasing, accounting and administration personnel who can

further give their recommendation for reducing the cost of manufacturing the product. The

engineer might further redesign the product for reducing the cost. The primary purpose of the

formed team is to assemble information in regards to the current costs and develop methods for

reducing the cost of manufacturing the product.

Answer to Question (ii)

The structure of the team and the potential areas that are considered by the newly formed

team for reducing the cost of the product are as follows:

The team that has been formed by Vanessa consists of a marketing personnel, engineer,

purchasing personnel and accounting and administration personnel.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING II

Customer surveys have also been conducted which have helped the team to find out that

there are five features which matter the most in case of a customer. These are that the

weight of the bike, the withstanding power of the bike to take upon hard riding, the way

the bike looks and the degree of comfort that the bike can provide to its rider

These factors have been further analyzed and arrived at an initial price in regards to the

Mountain Braker

The engineer who is a member of the team will alter remodel the design of the bike for

the purpose of incorporating the new braking system into the model

The information in regards to the cost of the current model has also been calculated and

considered for the identification of the effective methods that could be utilized for

reducing the cost of the product

The manufacturing cost has been reduced by an amount of £30

The cost in regards to selling and distribution has been reduced by £5

The cost in regards to warranty and support has been reduced by £5

The Administration cost has been reduced by £10

These considerations give an overview into the fact that the team has considered the

reduction of cost in the most potential areas. However, it must be noted here that the team could

have reduced the cost of selling and distribution by £10 without reducing the cost of warranty

and support. This is because compromising with the after sales service that is warranty and

support could certainly hamper business (de Melo et al., 2016).

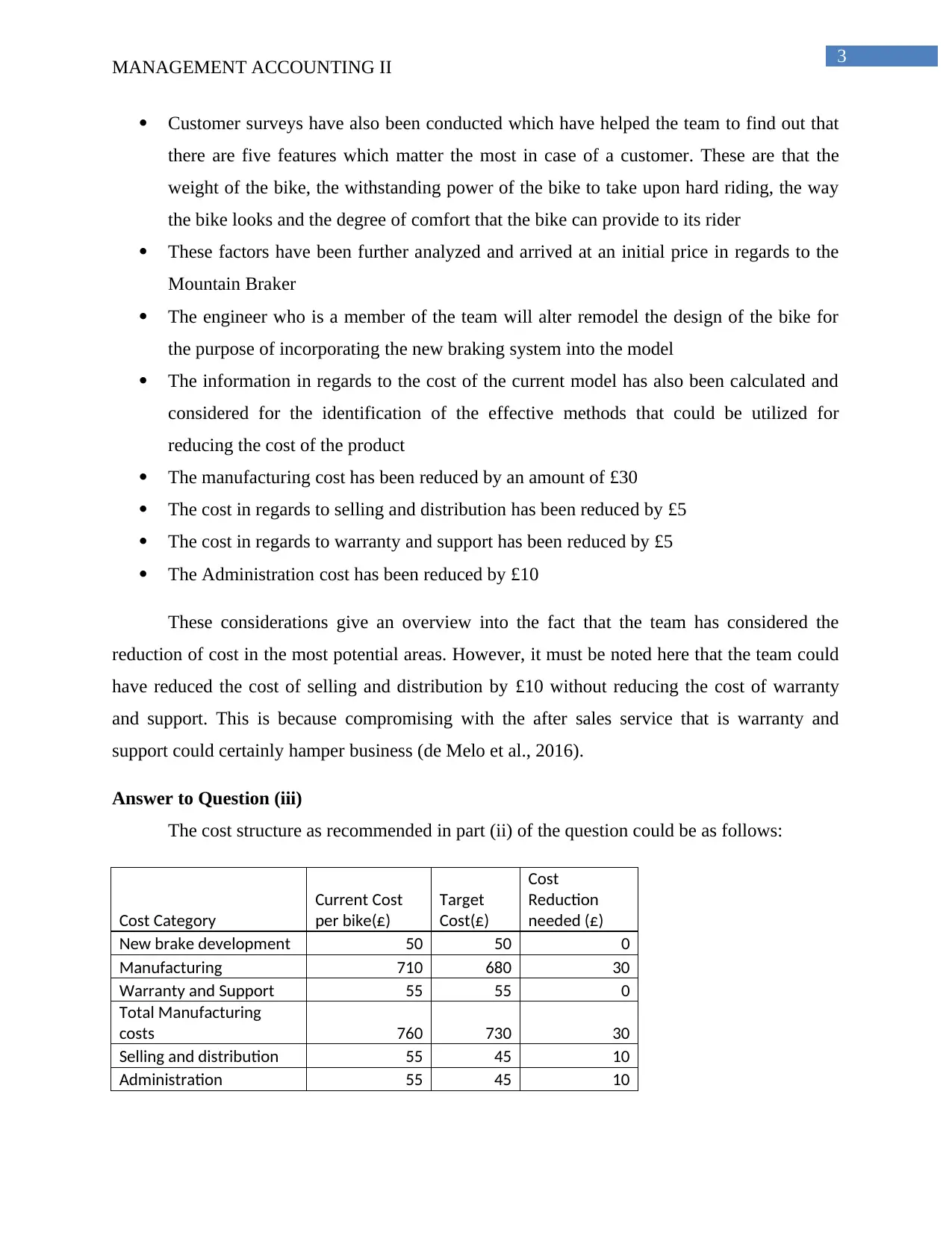

Answer to Question (iii)

The cost structure as recommended in part (ii) of the question could be as follows:

Cost Category

Current Cost

per bike(£)

Target

Cost(£)

Cost

Reduction

needed (£)

New brake development 50 50 0

Manufacturing 710 680 30

Warranty and Support 55 55 0

Total Manufacturing

costs 760 730 30

Selling and distribution 55 45 10

Administration 55 45 10

MANAGEMENT ACCOUNTING II

Customer surveys have also been conducted which have helped the team to find out that

there are five features which matter the most in case of a customer. These are that the

weight of the bike, the withstanding power of the bike to take upon hard riding, the way

the bike looks and the degree of comfort that the bike can provide to its rider

These factors have been further analyzed and arrived at an initial price in regards to the

Mountain Braker

The engineer who is a member of the team will alter remodel the design of the bike for

the purpose of incorporating the new braking system into the model

The information in regards to the cost of the current model has also been calculated and

considered for the identification of the effective methods that could be utilized for

reducing the cost of the product

The manufacturing cost has been reduced by an amount of £30

The cost in regards to selling and distribution has been reduced by £5

The cost in regards to warranty and support has been reduced by £5

The Administration cost has been reduced by £10

These considerations give an overview into the fact that the team has considered the

reduction of cost in the most potential areas. However, it must be noted here that the team could

have reduced the cost of selling and distribution by £10 without reducing the cost of warranty

and support. This is because compromising with the after sales service that is warranty and

support could certainly hamper business (de Melo et al., 2016).

Answer to Question (iii)

The cost structure as recommended in part (ii) of the question could be as follows:

Cost Category

Current Cost

per bike(£)

Target

Cost(£)

Cost

Reduction

needed (£)

New brake development 50 50 0

Manufacturing 710 680 30

Warranty and Support 55 55 0

Total Manufacturing

costs 760 730 30

Selling and distribution 55 45 10

Administration 55 45 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING II

The above table depicts the fact that the decrease in the warranty and support in regards

to the product have not been compromised. However, the figure of target cost has been arrived at

by the decreasing the selling and distribution costs by a larger percentage.

Part B

Target costing refers to that system of costing which aims to match the features of a

particular that is being manufactured by a firm with its current ongoing price in the market by

keeping in mind the profitability goals of the company. As evident from the provided case study

of Orange Mount Bikes, by the deducting the desired profit from the market price of the product

the amount of maximum permissible cost can be arrived at. This means that the determination of

the target cost is facilitated by the deduction of a profit margin from the market price of the

product (Ilg, Hoehne and Guenther 2016).

The advantages of target costing can be described as follows:

The implementation of a target costing system inside a business ensures the

implementation of a proper plan or schedule in regards to marketing and other essential

procedures of business (Ofileanu 2015)

Target costing is an essential feature of marketing and utilization of it ensures the

reaching of the top position in the marketing world (Ofileanu 2015)

The customers will be able to receive products that are of the optimum quality as a target

costing structure enables the business firm to satisfy its manufacturing needs at a cost that

is affordable (Ofileanu 2015)

Target costing also enables the employees to manufacture products that are of the

optimum quality (Segeth-Boniecka 2017)

Target costing also facilitates the utilization of the management control system for

establishing and reinforcing the management strategies in the company (Segeth-Boniecka

2017)

It further leads to the integration of the activities of the supplier with the requirements of

the customers for designing the product that is suitable for customer use. This can be

further explained by the example of the case study of the Orange Mount Bikes. The

Orange Mount Bikes before introducing the new product in the market had conducted a

MANAGEMENT ACCOUNTING II

The above table depicts the fact that the decrease in the warranty and support in regards

to the product have not been compromised. However, the figure of target cost has been arrived at

by the decreasing the selling and distribution costs by a larger percentage.

Part B

Target costing refers to that system of costing which aims to match the features of a

particular that is being manufactured by a firm with its current ongoing price in the market by

keeping in mind the profitability goals of the company. As evident from the provided case study

of Orange Mount Bikes, by the deducting the desired profit from the market price of the product

the amount of maximum permissible cost can be arrived at. This means that the determination of

the target cost is facilitated by the deduction of a profit margin from the market price of the

product (Ilg, Hoehne and Guenther 2016).

The advantages of target costing can be described as follows:

The implementation of a target costing system inside a business ensures the

implementation of a proper plan or schedule in regards to marketing and other essential

procedures of business (Ofileanu 2015)

Target costing is an essential feature of marketing and utilization of it ensures the

reaching of the top position in the marketing world (Ofileanu 2015)

The customers will be able to receive products that are of the optimum quality as a target

costing structure enables the business firm to satisfy its manufacturing needs at a cost that

is affordable (Ofileanu 2015)

Target costing also enables the employees to manufacture products that are of the

optimum quality (Segeth-Boniecka 2017)

Target costing also facilitates the utilization of the management control system for

establishing and reinforcing the management strategies in the company (Segeth-Boniecka

2017)

It further leads to the integration of the activities of the supplier with the requirements of

the customers for designing the product that is suitable for customer use. This can be

further explained by the example of the case study of the Orange Mount Bikes. The

Orange Mount Bikes before introducing the new product in the market had conducted a

5

MANAGEMENT ACCOUNTING II

customer survey which further identified the areas of the product that should be focused

upon in order to gain the support of the customers (Segeth-Boniecka 2017)

A major advantage of target costing is that it fixes the cost of a particular product on the

basis of the willingness of the customer to pay for it (Diefenbach, Wald and Gleich 2018)

Furthermore, target costing enables the management of a firm to identify the potential

market areas or opportunities. These are the areas that fix the target selling price at the

maximum level (Diefenbach, Wald and Gleich 2018)

Target costing also facilitates the reduction in the time period in regards to the

development cycle of a product (Diefenbach, Wald and Gleich 2018)

Target costing facilitates the reduction in the cost of the product significantly (Rybkowski

2016)

Lastly, target costing enhances the entire process beginning from product idea till the

introduction and distribution of the product in the market for the purpose of selling and

acquiring the desired profit (Rybkowski 2016)

The limitations of target costing can be listed down as follows:

The process in regards to development can be stretched to a certain extent that is longer

than assumed or expected. This is because target costing involves a handful number of

processes in order to devise a product at a lower cost for ensuring the fact that it meets

the target cost and the criteria that has been set. A major but common issue in regards to

target costing is that the manager of the business organization does not become ready to

stop a certain project on the account of the reason that its costing goals are not met with.

It must be noted here that a firm using the target costing method should be alert about the

fact that whether the project is moving towards a target cost within a shorter period of

time. If the scene is not so then the project should be dropped (Lima 2016)

Target costing involves rigorous cost cutting. This means that in order to arrive at the

targeted cost of the product the management of the firm might cut upon various costs that

the stakeholders of the firm feel necessary to include. Therefore, this may result in

employee dissatisfaction, which will ultimately result in drop in production rate by them

(Lima 2016)

MANAGEMENT ACCOUNTING II

customer survey which further identified the areas of the product that should be focused

upon in order to gain the support of the customers (Segeth-Boniecka 2017)

A major advantage of target costing is that it fixes the cost of a particular product on the

basis of the willingness of the customer to pay for it (Diefenbach, Wald and Gleich 2018)

Furthermore, target costing enables the management of a firm to identify the potential

market areas or opportunities. These are the areas that fix the target selling price at the

maximum level (Diefenbach, Wald and Gleich 2018)

Target costing also facilitates the reduction in the time period in regards to the

development cycle of a product (Diefenbach, Wald and Gleich 2018)

Target costing facilitates the reduction in the cost of the product significantly (Rybkowski

2016)

Lastly, target costing enhances the entire process beginning from product idea till the

introduction and distribution of the product in the market for the purpose of selling and

acquiring the desired profit (Rybkowski 2016)

The limitations of target costing can be listed down as follows:

The process in regards to development can be stretched to a certain extent that is longer

than assumed or expected. This is because target costing involves a handful number of

processes in order to devise a product at a lower cost for ensuring the fact that it meets

the target cost and the criteria that has been set. A major but common issue in regards to

target costing is that the manager of the business organization does not become ready to

stop a certain project on the account of the reason that its costing goals are not met with.

It must be noted here that a firm using the target costing method should be alert about the

fact that whether the project is moving towards a target cost within a shorter period of

time. If the scene is not so then the project should be dropped (Lima 2016)

Target costing involves rigorous cost cutting. This means that in order to arrive at the

targeted cost of the product the management of the firm might cut upon various costs that

the stakeholders of the firm feel necessary to include. Therefore, this may result in

employee dissatisfaction, which will ultimately result in drop in production rate by them

(Lima 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING II

A major portion of target costing involves designing of the product which in turn

involves opinion or suggestions from the different levels of business including different

departments. The different departmental executives have different perspective in regards

to the design of the product. Moreover, the design teams have their own viewpoint. This

leads to unnecessary confusion and results in a faulty layout or design of the product

(Lima 2016)

Thus, these are the limitations and benefits of target costing and it can be evidently stated

here that in spite of the potential disadvantages, the marketing world of the modern day demands

the utilization of target costing for the establishment of a profitable business.

MANAGEMENT ACCOUNTING II

A major portion of target costing involves designing of the product which in turn

involves opinion or suggestions from the different levels of business including different

departments. The different departmental executives have different perspective in regards

to the design of the product. Moreover, the design teams have their own viewpoint. This

leads to unnecessary confusion and results in a faulty layout or design of the product

(Lima 2016)

Thus, these are the limitations and benefits of target costing and it can be evidently stated

here that in spite of the potential disadvantages, the marketing world of the modern day demands

the utilization of target costing for the establishment of a profitable business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING II

References

de Melo, R.S.S., Do, D., Tillmann, P., Ballard, G. and Granja, A.D., 2016. Target value design in

the public sector: evidence from a hospital project in San Francisco, CA. Architectural

Engineering and Design Management, 12(2), pp.125-137.

Diefenbach, U., Wald, A. and Gleich, R., 2018. Between cost and benefit: investigating effects

of cost management control systems on cost efficiency and organisational performance. Journal

of Management Control, pp.1-27.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster analysis.

Journal of Business Research.

Ilg, P., Hoehne, C. and Guenther, E., 2016. High-performance materials in infrastructure: a

review of applied life cycle costing and its drivers–the case of fiber-reinforced composites.

Journal of Cleaner Production, 112, pp.926-945.

Jiang, L. and Hansen, C.Ø., 2016. Target costing as a strategic tool to commercialize the product

and service innovation.

Lima, A.C., da Silveira, J.A.G., da Silva, S.H.F. and Ching, H.Y., 2016. Target costing:

exploring the concept and its relation to competitiveness in agribusiness. CEP, 60, p.905.

Mörtl, M. and Schmied, C., 2016. Design for Cost—A Review of Methods, Tools and Research

Directions. Journal of the Indian Institute of Science, 95(4), pp.379-404.

Ofileanu, D., 2015. TARGET COSTING FUNCTIONS. Revista Economica, 67(5).

Rybkowski, Z.K., Munankami, M., Shepley, M.M. and Fernández-Solis, J.L., 2016, July.

Development and testing of a lean simulation to illustrate key principles of Target Value Design:

A first run study. Proceedings of the 24th annual conference of the International Group for Lean

Construction.

Segeth-Boniecka, K., 2017. Target costing as an element of the hard coal extraction cost

planning process. Zeszyty Teoretyczne Rachunkowości, (94 (150)), pp.145-157.

MANAGEMENT ACCOUNTING II

References

de Melo, R.S.S., Do, D., Tillmann, P., Ballard, G. and Granja, A.D., 2016. Target value design in

the public sector: evidence from a hospital project in San Francisco, CA. Architectural

Engineering and Design Management, 12(2), pp.125-137.

Diefenbach, U., Wald, A. and Gleich, R., 2018. Between cost and benefit: investigating effects

of cost management control systems on cost efficiency and organisational performance. Journal

of Management Control, pp.1-27.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster analysis.

Journal of Business Research.

Ilg, P., Hoehne, C. and Guenther, E., 2016. High-performance materials in infrastructure: a

review of applied life cycle costing and its drivers–the case of fiber-reinforced composites.

Journal of Cleaner Production, 112, pp.926-945.

Jiang, L. and Hansen, C.Ø., 2016. Target costing as a strategic tool to commercialize the product

and service innovation.

Lima, A.C., da Silveira, J.A.G., da Silva, S.H.F. and Ching, H.Y., 2016. Target costing:

exploring the concept and its relation to competitiveness in agribusiness. CEP, 60, p.905.

Mörtl, M. and Schmied, C., 2016. Design for Cost—A Review of Methods, Tools and Research

Directions. Journal of the Indian Institute of Science, 95(4), pp.379-404.

Ofileanu, D., 2015. TARGET COSTING FUNCTIONS. Revista Economica, 67(5).

Rybkowski, Z.K., Munankami, M., Shepley, M.M. and Fernández-Solis, J.L., 2016, July.

Development and testing of a lean simulation to illustrate key principles of Target Value Design:

A first run study. Proceedings of the 24th annual conference of the International Group for Lean

Construction.

Segeth-Boniecka, K., 2017. Target costing as an element of the hard coal extraction cost

planning process. Zeszyty Teoretyczne Rachunkowości, (94 (150)), pp.145-157.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.