Comprehensive Management Accounting Report for Unilever Inc. - Finance

VerifiedAdded on 2020/01/23

|20

|5901

|157

Report

AI Summary

This report delves into the realm of management accounting, focusing on its crucial role in financial control within a profit-seeking organization, specifically using Unilever Inc. as a case study. It explores the essential requirements of different managerial accounting systems, including cost accounting, job costing, and inventory management. The report examines various management accounting methods, such as absorption costing and marginal costing, and provides a comparison of their application. Furthermore, it discusses the advantages and disadvantages of planning tools in budgetary control, and compares processes organizations use to respond to financial problems. The report also provides an in-depth analysis of financial planning tools, including standard costing, process costing, and financial statement analysis, to manage financial resources effectively within the context of a large manufacturing firm. The analysis includes the importance of timely, relevant, reliable, and accurate information in making informed financial decisions.

MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.....................................................................................................................................3

1.0Task 1.........................................................................................................................................3

1.1 Explanation of management accounting and essential requirements of different types of

management accounting systems.................................................................................................3

1.1.1 Explanation of management accounting.........................................................................3

1.1.2 Requirements of different types of managerial accounting system ..........................5

1.2 Different methods of management accounting......................................................................6

2.0 Task 2 .......................................................................................................................................6

2.1 Income statement by considering Absorption costing and Marginal costing........................6

2.2 Explanation of the difference between Absorption costing and Marginal costing................8

3.0 Task 3........................................................................................................................................9

3.1 Advantages and disadvantages of different types of planning tools in budgetary control....9

Task 4............................................................................................................................................12

4.1 Comparison between the processes, which organisations use the management accounting

to respond the financial problems..............................................................................................12

Conclusion.....................................................................................................................................13

References.....................................................................................................................................14

2

Introduction.....................................................................................................................................3

1.0Task 1.........................................................................................................................................3

1.1 Explanation of management accounting and essential requirements of different types of

management accounting systems.................................................................................................3

1.1.1 Explanation of management accounting.........................................................................3

1.1.2 Requirements of different types of managerial accounting system ..........................5

1.2 Different methods of management accounting......................................................................6

2.0 Task 2 .......................................................................................................................................6

2.1 Income statement by considering Absorption costing and Marginal costing........................6

2.2 Explanation of the difference between Absorption costing and Marginal costing................8

3.0 Task 3........................................................................................................................................9

3.1 Advantages and disadvantages of different types of planning tools in budgetary control....9

Task 4............................................................................................................................................12

4.1 Comparison between the processes, which organisations use the management accounting

to respond the financial problems..............................................................................................12

Conclusion.....................................................................................................................................13

References.....................................................................................................................................14

2

Introduction

Managerial accounting in a profit seeking concern is to be considered as one of the most

important factors of financial control. As accounting is considered as an important aspect of

financial management, managers are to use suitable cost and financial accounting techniques in

order to put control over the financial facts of an organization. In the initial part of the study, the

researcher shall act as a Management Accountant and make report to the General Manager of a

profit seeking concern in order to describe the essential requirements of different types of

managerial accounting. The researcher shall make discussion on the different methods of

management accounting in the next part of the first part. In the next part of the study, the

researcher shall make calculations of cost in two different methods of managerial costing.

Financial budgeting and other planning tools are also to be discussed by the researcher after

making calculation of costs. Moreover, the budgetary control and the financial resource

allocation will also be discussed in order to select financial management problems. The

researcher shall make the discussions by considering Unilever Inc. In this context, the researcher

is to mention that the selected company belong to the manufacturing sector.

Task 1

To: Name- (General Manager)

From: - Your Name- Management Accounting Officer

Date: ................

Subject: Management Accounting & Management Accounting System

1.1 Explanation of management accounting and essential requirements of different types of

management accounting systems

1.1.1 Explanation of management accounting

Management accounting could be considered as one of the most crucial financial factors

that affects the financial controlling system of an organization as financial accounting is the most

3

Managerial accounting in a profit seeking concern is to be considered as one of the most

important factors of financial control. As accounting is considered as an important aspect of

financial management, managers are to use suitable cost and financial accounting techniques in

order to put control over the financial facts of an organization. In the initial part of the study, the

researcher shall act as a Management Accountant and make report to the General Manager of a

profit seeking concern in order to describe the essential requirements of different types of

managerial accounting. The researcher shall make discussion on the different methods of

management accounting in the next part of the first part. In the next part of the study, the

researcher shall make calculations of cost in two different methods of managerial costing.

Financial budgeting and other planning tools are also to be discussed by the researcher after

making calculation of costs. Moreover, the budgetary control and the financial resource

allocation will also be discussed in order to select financial management problems. The

researcher shall make the discussions by considering Unilever Inc. In this context, the researcher

is to mention that the selected company belong to the manufacturing sector.

Task 1

To: Name- (General Manager)

From: - Your Name- Management Accounting Officer

Date: ................

Subject: Management Accounting & Management Accounting System

1.1 Explanation of management accounting and essential requirements of different types of

management accounting systems

1.1.1 Explanation of management accounting

Management accounting could be considered as one of the most crucial financial factors

that affects the financial controlling system of an organization as financial accounting is the most

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

essential tool to record all the financial facts and figures. In this context, Vernimmen et al.

(2014) stated that the financial accounting records all the quantitative data for particular period

of time. On the other hand, the researcher is required to mention that the financial accounting

data are used in developing the managerial accounting. In the profit seeking organizations, the

management accountants are required to use the accounting information from the financial books

of accounts to prepare different managerial accounting statements such as budgetary reports,

variance statement and standard costing statements.

In case manufacturing firms like the company in the case study, the managerial

accounting is required to be considered as the most important aspect for putting control over the

financial facts of the company. As the company involves in manufacturing of goods, which

belongs to FMCG group, the company is required to make management of the financial results

and performance on the basis of the market demand. In the Unilever Inc, the objective of

management accountants are to compute per unit cost of sales along with the computation of the

variable costs and fixed costs.

As opined by Micheli and Mari (2014), manufacturing companies are needed to include

the managerial accounting tools in order to put control on the different cost centers. In this

context, the researcher is required to mention that as the company manufactures a large number

of goods, the company is required to prepare managerial accounting statements for each of the

cost centers. In managerial accounting, the accountant is required to analyze variances and

prepare budget. Moreover, the marginal costing is also to be found as important for the

management accountants to compute the profitability and break even for a product (Cornelissen,

2014). Therefore, the researcher could mention that the managerial accounting helps to make

financial planning and this process is helpful in case of large scale manufacturers. The

management accounting system of the company follows the computation of total cost of

production and the cost of sales. On the other hand, the management accounting system of the

company would facilitate the manufacturing managers to reduce the maintainable fixed costs.

Cost accounting system

In management accounting, managers could ascertain per unit cost of production. The

influence of fixed and variable costs could also be identified in cost accounting mechanism.

Moreover, cost accountants could also use the marginal costing approach in order to put control

4

(2014) stated that the financial accounting records all the quantitative data for particular period

of time. On the other hand, the researcher is required to mention that the financial accounting

data are used in developing the managerial accounting. In the profit seeking organizations, the

management accountants are required to use the accounting information from the financial books

of accounts to prepare different managerial accounting statements such as budgetary reports,

variance statement and standard costing statements.

In case manufacturing firms like the company in the case study, the managerial

accounting is required to be considered as the most important aspect for putting control over the

financial facts of the company. As the company involves in manufacturing of goods, which

belongs to FMCG group, the company is required to make management of the financial results

and performance on the basis of the market demand. In the Unilever Inc, the objective of

management accountants are to compute per unit cost of sales along with the computation of the

variable costs and fixed costs.

As opined by Micheli and Mari (2014), manufacturing companies are needed to include

the managerial accounting tools in order to put control on the different cost centers. In this

context, the researcher is required to mention that as the company manufactures a large number

of goods, the company is required to prepare managerial accounting statements for each of the

cost centers. In managerial accounting, the accountant is required to analyze variances and

prepare budget. Moreover, the marginal costing is also to be found as important for the

management accountants to compute the profitability and break even for a product (Cornelissen,

2014). Therefore, the researcher could mention that the managerial accounting helps to make

financial planning and this process is helpful in case of large scale manufacturers. The

management accounting system of the company follows the computation of total cost of

production and the cost of sales. On the other hand, the management accounting system of the

company would facilitate the manufacturing managers to reduce the maintainable fixed costs.

Cost accounting system

In management accounting, managers could ascertain per unit cost of production. The

influence of fixed and variable costs could also be identified in cost accounting mechanism.

Moreover, cost accountants could also use the marginal costing approach in order to put control

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

over the use of variable costs in the production process. In this context, the researcher could

mention that Company could consider the marginal accounting system to compute the breakeven

of the products that the company manufactures. In this context, the researcher is required to

mention that the breakeven point could help the management accountants of the company to

compute the number of units to be sold by the selling managers to make no profit and no loss. As

stated by Hill et al. (2014), in marginal costing, variable costs are considered as product related

cost and the fixed costs are assumed as time specific. Therefore, marginal costing could help the

management accountants to eliminate the fixed overheads from the production process of the

manufacturing companies.

Job costing:

Job costing facilitates the managers to compute cost for a certain job. Costs for different

jobs could be ascertained by using this approach of costing and planning.

As stated by Brown (2013), management accountants could compute the job cost by

considering the fixed and variable costs of the production process. In this context, it is to

mention that the company could consider job-costing system for putting control on the marginal

costs related to job.

Inventory management system:

For managing the inventories, managers could use EOQ model, Just in Time model and

ABC system for controlling the inventories. In this context, Cornelissen (2014) opined that

inventory management is one of the most crucial aspects in an organization as it affects the

pricing policies of the company.

Price optimization:

Price optimization strategy helps the managers to identify the change in demand due to

the change in the price level. Therefore, this method is required to be considered for managing

the price of the products.

1.1.2 Requirements of different types of managerial accounting system

In manufacturing companies, the managerial accounting is to be considered as the tool,

by which management accountants could examine the excessive costs in manufacturing process.

5

mention that Company could consider the marginal accounting system to compute the breakeven

of the products that the company manufactures. In this context, the researcher is required to

mention that the breakeven point could help the management accountants of the company to

compute the number of units to be sold by the selling managers to make no profit and no loss. As

stated by Hill et al. (2014), in marginal costing, variable costs are considered as product related

cost and the fixed costs are assumed as time specific. Therefore, marginal costing could help the

management accountants to eliminate the fixed overheads from the production process of the

manufacturing companies.

Job costing:

Job costing facilitates the managers to compute cost for a certain job. Costs for different

jobs could be ascertained by using this approach of costing and planning.

As stated by Brown (2013), management accountants could compute the job cost by

considering the fixed and variable costs of the production process. In this context, it is to

mention that the company could consider job-costing system for putting control on the marginal

costs related to job.

Inventory management system:

For managing the inventories, managers could use EOQ model, Just in Time model and

ABC system for controlling the inventories. In this context, Cornelissen (2014) opined that

inventory management is one of the most crucial aspects in an organization as it affects the

pricing policies of the company.

Price optimization:

Price optimization strategy helps the managers to identify the change in demand due to

the change in the price level. Therefore, this method is required to be considered for managing

the price of the products.

1.1.2 Requirements of different types of managerial accounting system

In manufacturing companies, the managerial accounting is to be considered as the tool,

by which management accountants could examine the excessive costs in manufacturing process.

5

On the other hand, service sector companies could also use the management accounting tools in

order to compute the cost of service and the loopholes in the process of servicing. In this context,

it is to mention that managerial accounting requires relevant, reliable and accurate information to

manage the financial resources of the organization. On the other hand, information is required to

be received timely in order understand the present condition of the business.

Relevance of information:

In management accounting, the data are required to be relevant as irrelevant data could

results in inappropriate forecasting. On the other hand, it is to mention that the relevant

information in management process could facilitate the managers in developing proper

budgeting as budgeting depends on the data used in managerial accounting.

Reliability:

Along with relevance information, the information is required to be reliable as the budget

as prepared by reliable data results in appropriate planning.

Accuracy:

Accurate data is also an important aspect of management accounting as use of accurate

data ensures the quality of budgeting. On the other hand, the accurate information could be

considered as the reason behind the appropriate planning. Therefore, the information in

management accounting is to be accurate.

Up to date information:

In management accounting, managers are required to use up to dated information in order

to make financial planning. In this context, it is to mention that the up to dated qualitative

information such as demand and price changes are also required to be considered as important

aspects of management accounting.

Timely receipt:

Management accounting also requires timely receipt of data to make planning. On the

other hand, the researcher is to mention that the managers are required to get relevant and

reliable information at the time of preparing budget.

6

order to compute the cost of service and the loopholes in the process of servicing. In this context,

it is to mention that managerial accounting requires relevant, reliable and accurate information to

manage the financial resources of the organization. On the other hand, information is required to

be received timely in order understand the present condition of the business.

Relevance of information:

In management accounting, the data are required to be relevant as irrelevant data could

results in inappropriate forecasting. On the other hand, it is to mention that the relevant

information in management process could facilitate the managers in developing proper

budgeting as budgeting depends on the data used in managerial accounting.

Reliability:

Along with relevance information, the information is required to be reliable as the budget

as prepared by reliable data results in appropriate planning.

Accuracy:

Accurate data is also an important aspect of management accounting as use of accurate

data ensures the quality of budgeting. On the other hand, the accurate information could be

considered as the reason behind the appropriate planning. Therefore, the information in

management accounting is to be accurate.

Up to date information:

In management accounting, managers are required to use up to dated information in order

to make financial planning. In this context, it is to mention that the up to dated qualitative

information such as demand and price changes are also required to be considered as important

aspects of management accounting.

Timely receipt:

Management accounting also requires timely receipt of data to make planning. On the

other hand, the researcher is to mention that the managers are required to get relevant and

reliable information at the time of preparing budget.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the other hand, Gibson (2014) stated that budgetary costing is the most relevant

costing system for the managers in large manufacturing concerns as this managerial accounting

system helps the management to set a target to the subordinate staffs. In this same context, Jung

et al. (2016) cited that target costing facilitates the management accountants to minimize waste

of financial resources. Therefore, the managerial accountant is required to mention that the

budgetary costing is required for the large manufacturing firms to minimize erosion of financial

resources.

Different management accounting reports including job cost, inventory management,

performance and profitability reports can be expressed that are useful to analyze financial

position of organization. On the basis of recognizing organization's position and making further

decisions regarding business operations can be described through following reports:-

Inventory management report: - By preparing and maintaining these reports,

inventories and different position of entity is gained through this way. However, proper

inventory management of resources and products of the organization is gained through

this report. Therefore, further plans are prepared to be implemented for proper

management of goods services produced by entity. Thus, inventory management report is

beneficial for any organization to enhance efficiencies of the company.

Profitability reports: - Through recording and reporting these reports, profit earning

capacity of entity is gained. However, earned profit is recorded that leads to making

decision for further production and supplement of goods. In this regard, profitability and

last years' performance of organization is described that is interlinked with business

operations and future development of entity.

Performance management reports: - This report is prepared for presenting

performance of organization and its workers as well their contribution in goal

accomplishment. However, these reports are able to improving working efficiencies of

workers and entity to achieve its effectiveness and different implementations. Therefore,

performance management reports are management accounting tools for better quality

services at high level.

Job cost reports: - Management accounting tools including costing and budgeting for

further decision making process. However, for job cost reporting cost incurred on

7

costing system for the managers in large manufacturing concerns as this managerial accounting

system helps the management to set a target to the subordinate staffs. In this same context, Jung

et al. (2016) cited that target costing facilitates the management accountants to minimize waste

of financial resources. Therefore, the managerial accountant is required to mention that the

budgetary costing is required for the large manufacturing firms to minimize erosion of financial

resources.

Different management accounting reports including job cost, inventory management,

performance and profitability reports can be expressed that are useful to analyze financial

position of organization. On the basis of recognizing organization's position and making further

decisions regarding business operations can be described through following reports:-

Inventory management report: - By preparing and maintaining these reports,

inventories and different position of entity is gained through this way. However, proper

inventory management of resources and products of the organization is gained through

this report. Therefore, further plans are prepared to be implemented for proper

management of goods services produced by entity. Thus, inventory management report is

beneficial for any organization to enhance efficiencies of the company.

Profitability reports: - Through recording and reporting these reports, profit earning

capacity of entity is gained. However, earned profit is recorded that leads to making

decision for further production and supplement of goods. In this regard, profitability and

last years' performance of organization is described that is interlinked with business

operations and future development of entity.

Performance management reports: - This report is prepared for presenting

performance of organization and its workers as well their contribution in goal

accomplishment. However, these reports are able to improving working efficiencies of

workers and entity to achieve its effectiveness and different implementations. Therefore,

performance management reports are management accounting tools for better quality

services at high level.

Job cost reports: - Management accounting tools including costing and budgeting for

further decision making process. However, for job cost reporting cost incurred on

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manufacturing of products are recorded. It involves different expenses incurred on

resources, labor and additional overhead. Thus, recording of all of these costs is created

that is helpful for proper price determination and financial management of entity.

1.2 Different methods of management accounting

Manufacturing firms are required to prepare managerial accounting reports and variance

analysis reports in order to examine the feasibility in the production process in terms of financial

figures. In this context, Armstrong et al. (2015) stated that managerial accounting statements are

not controlled by any boards, which are internationally approved. In this context, it is also

required to mention that the management accountants in manufacturing companies could adopt

marginal accounting techniques in order to ascertain profit or loss by selling a particular number

of units. On the other hand, the management accountants could prepare the cost schedule by

considering the absorption costing, in which the overheads are calculated by considering the

machine hours worked.

In this context, managers could consider financial planning tools such as standard costing

and process costing in order to put control over the financial aspects of the company. Moreover,

financial planning is also required to be considered as one of the most important aspects of

planning as it provides the financial managers the facility of managing the financial resources.

On the other hand, financial statement analysis is also required to be taken as another

method of managing the financial resources. In this context, it is to state that the cash flow

analysis and fund flow analysis are to be made for analyzing the application and sources of the

funds.

In cash flow statement, financial managers analyze the sources and application of cash in

different segments of the company. Therefore, this analysis tool is also required to be assumed as

an important tool of analysis. Ion the other hand, the budgetary control is also to be considered

as an important part of financial controlling as this facilitates the management of the company to

put control over the financial resources of the company.

8

resources, labor and additional overhead. Thus, recording of all of these costs is created

that is helpful for proper price determination and financial management of entity.

1.2 Different methods of management accounting

Manufacturing firms are required to prepare managerial accounting reports and variance

analysis reports in order to examine the feasibility in the production process in terms of financial

figures. In this context, Armstrong et al. (2015) stated that managerial accounting statements are

not controlled by any boards, which are internationally approved. In this context, it is also

required to mention that the management accountants in manufacturing companies could adopt

marginal accounting techniques in order to ascertain profit or loss by selling a particular number

of units. On the other hand, the management accountants could prepare the cost schedule by

considering the absorption costing, in which the overheads are calculated by considering the

machine hours worked.

In this context, managers could consider financial planning tools such as standard costing

and process costing in order to put control over the financial aspects of the company. Moreover,

financial planning is also required to be considered as one of the most important aspects of

planning as it provides the financial managers the facility of managing the financial resources.

On the other hand, financial statement analysis is also required to be taken as another

method of managing the financial resources. In this context, it is to state that the cash flow

analysis and fund flow analysis are to be made for analyzing the application and sources of the

funds.

In cash flow statement, financial managers analyze the sources and application of cash in

different segments of the company. Therefore, this analysis tool is also required to be assumed as

an important tool of analysis. Ion the other hand, the budgetary control is also to be considered

as an important part of financial controlling as this facilitates the management of the company to

put control over the financial resources of the company.

8

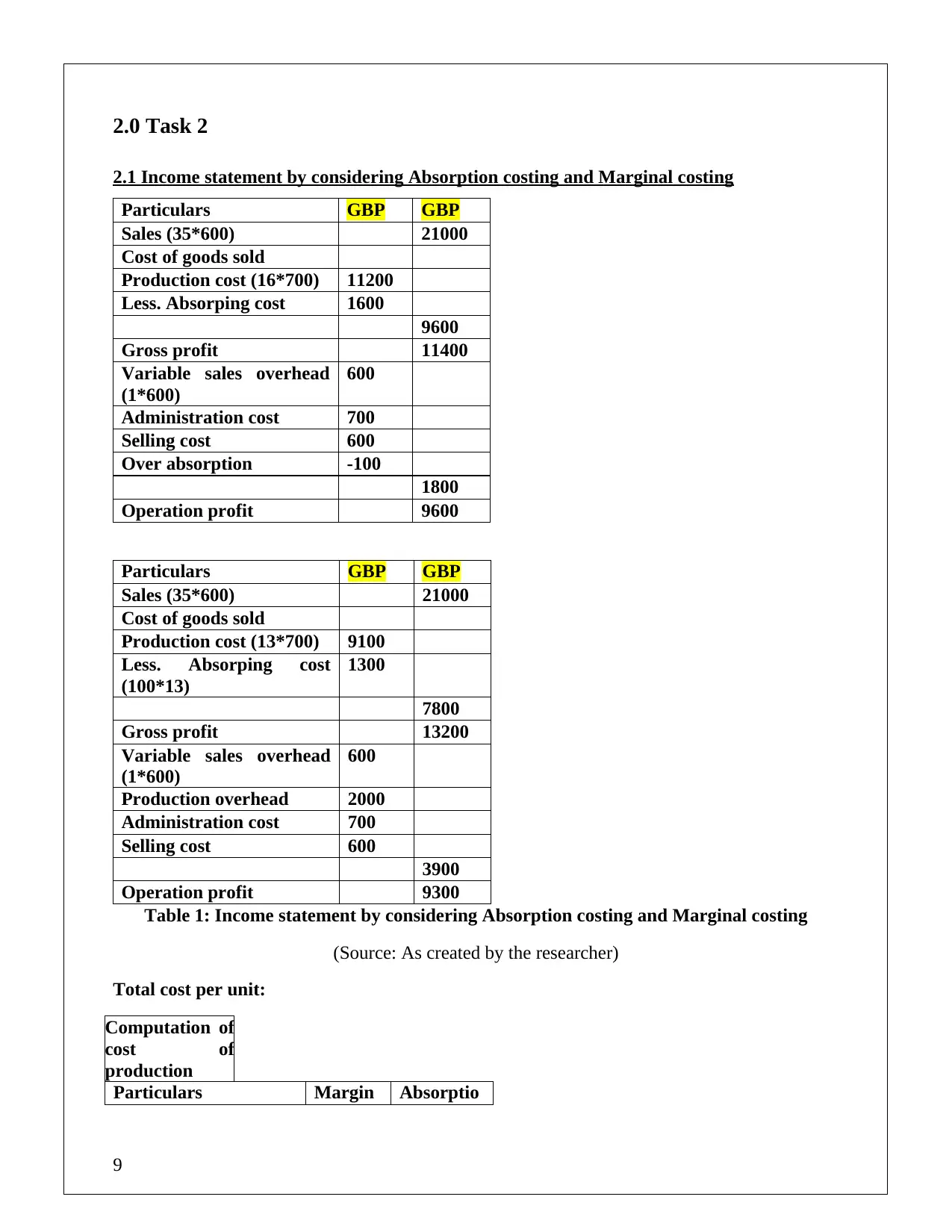

2.0 Task 2

2.1 Income statement by considering Absorption costing and Marginal costing

Particulars GBP GBP

Sales (35*600) 21000

Cost of goods sold

Production cost (16*700) 11200

Less. Absorping cost 1600

9600

Gross profit 11400

Variable sales overhead

(1*600)

600

Administration cost 700

Selling cost 600

Over absorption -100

1800

Operation profit 9600

Particulars GBP GBP

Sales (35*600) 21000

Cost of goods sold

Production cost (13*700) 9100

Less. Absorping cost

(100*13)

1300

7800

Gross profit 13200

Variable sales overhead

(1*600)

600

Production overhead 2000

Administration cost 700

Selling cost 600

3900

Operation profit 9300

Table 1: Income statement by considering Absorption costing and Marginal costing

(Source: As created by the researcher)

Total cost per unit:

Computation of

cost of

production

Particulars Margin Absorptio

9

2.1 Income statement by considering Absorption costing and Marginal costing

Particulars GBP GBP

Sales (35*600) 21000

Cost of goods sold

Production cost (16*700) 11200

Less. Absorping cost 1600

9600

Gross profit 11400

Variable sales overhead

(1*600)

600

Administration cost 700

Selling cost 600

Over absorption -100

1800

Operation profit 9600

Particulars GBP GBP

Sales (35*600) 21000

Cost of goods sold

Production cost (13*700) 9100

Less. Absorping cost

(100*13)

1300

7800

Gross profit 13200

Variable sales overhead

(1*600)

600

Production overhead 2000

Administration cost 700

Selling cost 600

3900

Operation profit 9300

Table 1: Income statement by considering Absorption costing and Marginal costing

(Source: As created by the researcher)

Total cost per unit:

Computation of

cost of

production

Particulars Margin Absorptio

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

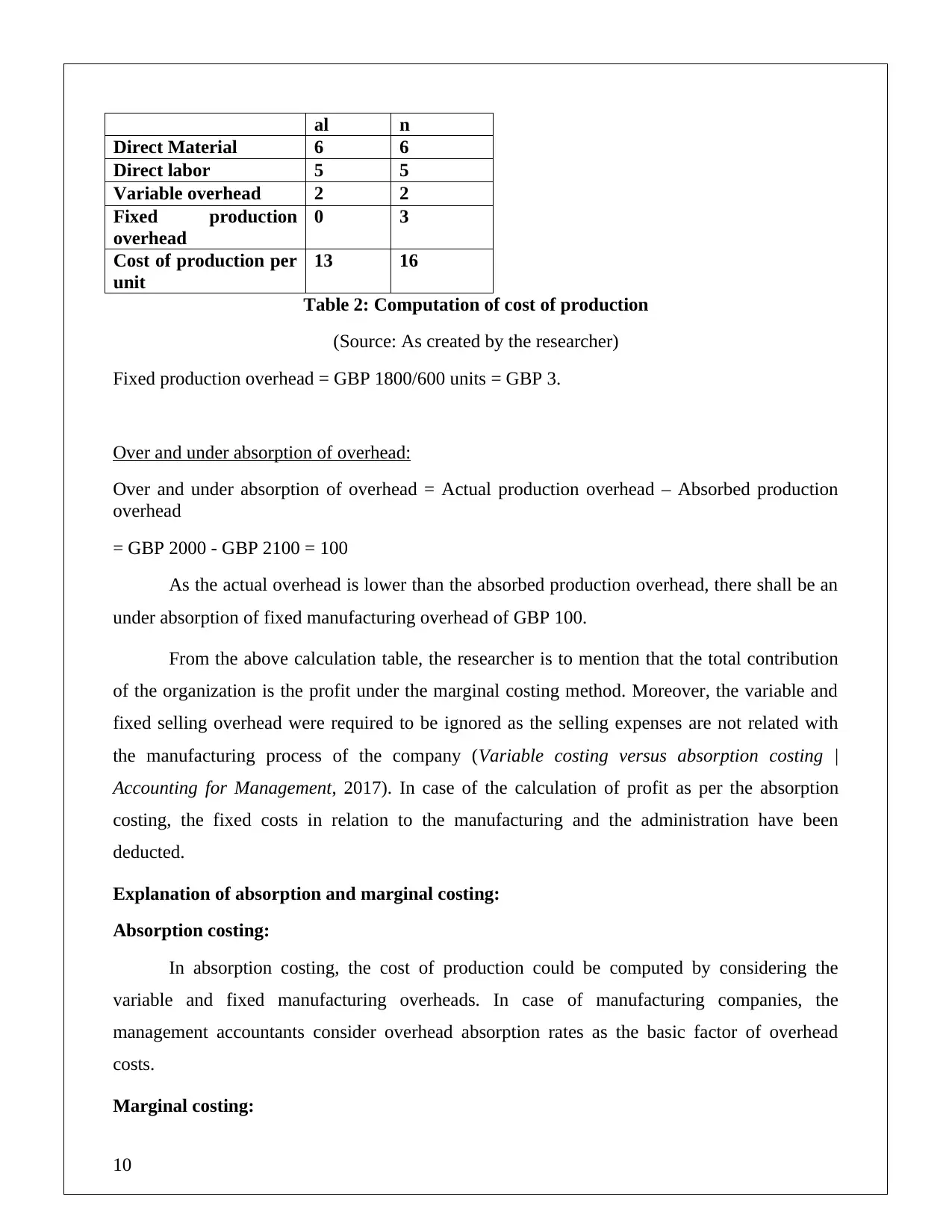

al n

Direct Material 6 6

Direct labor 5 5

Variable overhead 2 2

Fixed production

overhead

0 3

Cost of production per

unit

13 16

Table 2: Computation of cost of production

(Source: As created by the researcher)

Fixed production overhead = GBP 1800/600 units = GBP 3.

Over and under absorption of overhead:

Over and under absorption of overhead = Actual production overhead – Absorbed production

overhead

= GBP 2000 - GBP 2100 = 100

As the actual overhead is lower than the absorbed production overhead, there shall be an

under absorption of fixed manufacturing overhead of GBP 100.

From the above calculation table, the researcher is to mention that the total contribution

of the organization is the profit under the marginal costing method. Moreover, the variable and

fixed selling overhead were required to be ignored as the selling expenses are not related with

the manufacturing process of the company (Variable costing versus absorption costing |

Accounting for Management, 2017). In case of the calculation of profit as per the absorption

costing, the fixed costs in relation to the manufacturing and the administration have been

deducted.

Explanation of absorption and marginal costing:

Absorption costing:

In absorption costing, the cost of production could be computed by considering the

variable and fixed manufacturing overheads. In case of manufacturing companies, the

management accountants consider overhead absorption rates as the basic factor of overhead

costs.

Marginal costing:

10

Direct Material 6 6

Direct labor 5 5

Variable overhead 2 2

Fixed production

overhead

0 3

Cost of production per

unit

13 16

Table 2: Computation of cost of production

(Source: As created by the researcher)

Fixed production overhead = GBP 1800/600 units = GBP 3.

Over and under absorption of overhead:

Over and under absorption of overhead = Actual production overhead – Absorbed production

overhead

= GBP 2000 - GBP 2100 = 100

As the actual overhead is lower than the absorbed production overhead, there shall be an

under absorption of fixed manufacturing overhead of GBP 100.

From the above calculation table, the researcher is to mention that the total contribution

of the organization is the profit under the marginal costing method. Moreover, the variable and

fixed selling overhead were required to be ignored as the selling expenses are not related with

the manufacturing process of the company (Variable costing versus absorption costing |

Accounting for Management, 2017). In case of the calculation of profit as per the absorption

costing, the fixed costs in relation to the manufacturing and the administration have been

deducted.

Explanation of absorption and marginal costing:

Absorption costing:

In absorption costing, the cost of production could be computed by considering the

variable and fixed manufacturing overheads. In case of manufacturing companies, the

management accountants consider overhead absorption rates as the basic factor of overhead

costs.

Marginal costing:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In case of marginal costing, the variable costs are considered the only cost in the

manufacturing process. In this regard, the researcher is to mention that per unit variable costs are

considered as per unit cost of productions in marginal costing.

2.2 Explanation of the difference between Absorption costing and Marginal costing

In the above calculation of total cost and profit, the researcher has considered absorption

costing and marginal costing methods. In this regard, it is required to mention that both methods

consider different assumptions and techniques. If the discussion is to be made on the recognition

of cost, the researcher is required to mention that marginal costing method considers the fixed

costs as the period cost. On the other hand, absorption costing considers the fixed manufacturing

costs as the product costs.

On the other hand, Mahadevan (2015) stated that marginal costing method assumes the

profit volume ratio as the measurement of profit. But in the absorption costing, profitability

depends on the fixed costs related to the manufacturing process. Furthermore, it is to be

mentioned that the fixed costs affects the profitability in case of the absorption costing. In the

above table, it has been seen that the profit of the company was lower when the absorption

costing is considered. In this context, it is to state that the involvement of fixed cost in the

financial statement and cost schedule has resulted in low profit.

If the discussion is to be made on the decision making factors in the marginal costing, the

researcher is to mention that management accountants consider the contribution per unit as the

most crucial factor for making decisions. On the other hand, the absorption costing considers the

profit per unit as the most important factor for making decisions. As the marginal costing

method does not consider the fixed costs as the influencing factors in the cost schedule, the

contribution per unit could also be considered as per unit profit. On the other hand, the existence

of fixed costs in the cost schedule makes it compulsory for the cost and management accountants

to compute profit per unit by deducting the fixed costs from total contribution.

11

manufacturing process. In this regard, the researcher is to mention that per unit variable costs are

considered as per unit cost of productions in marginal costing.

2.2 Explanation of the difference between Absorption costing and Marginal costing

In the above calculation of total cost and profit, the researcher has considered absorption

costing and marginal costing methods. In this regard, it is required to mention that both methods

consider different assumptions and techniques. If the discussion is to be made on the recognition

of cost, the researcher is required to mention that marginal costing method considers the fixed

costs as the period cost. On the other hand, absorption costing considers the fixed manufacturing

costs as the product costs.

On the other hand, Mahadevan (2015) stated that marginal costing method assumes the

profit volume ratio as the measurement of profit. But in the absorption costing, profitability

depends on the fixed costs related to the manufacturing process. Furthermore, it is to be

mentioned that the fixed costs affects the profitability in case of the absorption costing. In the

above table, it has been seen that the profit of the company was lower when the absorption

costing is considered. In this context, it is to state that the involvement of fixed cost in the

financial statement and cost schedule has resulted in low profit.

If the discussion is to be made on the decision making factors in the marginal costing, the

researcher is to mention that management accountants consider the contribution per unit as the

most crucial factor for making decisions. On the other hand, the absorption costing considers the

profit per unit as the most important factor for making decisions. As the marginal costing

method does not consider the fixed costs as the influencing factors in the cost schedule, the

contribution per unit could also be considered as per unit profit. On the other hand, the existence

of fixed costs in the cost schedule makes it compulsory for the cost and management accountants

to compute profit per unit by deducting the fixed costs from total contribution.

11

3.0 Task 3

3.1 Advantages and disadvantages of different types of planning tools in budgetary control

Budget is to be considered as the financial planning of a company. In this context, it is to

mention that budget facilitates the managers to get the probable information regarding the

financial performance of the company. On the other hand, budgetary control helps the financial

managers to put control over the financial resources. In this context, it is to mention that the

budgetary control is made from the budget statements of the company.

Pros and corns of two budgetary tools:

Cash budget

Advantages:

1. Forecasting of cash balances for future,

2. Forecasting the payments is to be made for a certain period.

3. It facilitates to compute the inevitable money.

Disadvantages:

1. Cash budget is a time consuming process,

2. Cash budget considers assumptions therefore there could be a chance of inappropriate

forecasting.

3. As this budget tool considers cash basis of accounting, the actual incomes could not be

ascertained.

Performance budgeting:

Pros:

This budgeting helps the managers to get the forecast of manufacturing for a financial year.

Cons:

12

3.1 Advantages and disadvantages of different types of planning tools in budgetary control

Budget is to be considered as the financial planning of a company. In this context, it is to

mention that budget facilitates the managers to get the probable information regarding the

financial performance of the company. On the other hand, budgetary control helps the financial

managers to put control over the financial resources. In this context, it is to mention that the

budgetary control is made from the budget statements of the company.

Pros and corns of two budgetary tools:

Cash budget

Advantages:

1. Forecasting of cash balances for future,

2. Forecasting the payments is to be made for a certain period.

3. It facilitates to compute the inevitable money.

Disadvantages:

1. Cash budget is a time consuming process,

2. Cash budget considers assumptions therefore there could be a chance of inappropriate

forecasting.

3. As this budget tool considers cash basis of accounting, the actual incomes could not be

ascertained.

Performance budgeting:

Pros:

This budgeting helps the managers to get the forecast of manufacturing for a financial year.

Cons:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.