Comprehensive Management Accounting Report: Nero Ltd, UK Operations

VerifiedAdded on 2021/02/20

|16

|4756

|59

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of Nero Ltd, a medium-sized manufacturing enterprise based in London, UK. The report begins by defining management accounting and exploring the requirements for different systems, emphasizing their role in decision-making and organizational efficiency. It then details various management accounting methods, including job costing and price optimization systems. The report proceeds to analyze cost analysis techniques, such as fixed and variable costs, and demonstrates their use in preparing income statements. Furthermore, it delves into the advantages and disadvantages of budgetary control tools, alongside their applications in forecasting and financial planning. The report also examines how companies adapt their management accounting systems to address financial challenges, offering insights into sustainable success strategies. The report integrates the key concepts of management accounting system and reporting within an organisational context, including budgeting reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports. This comprehensive analysis aims to provide a practical understanding of management accounting in a business environment.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and requirements for different kinds of management

accounting systems.................................................................................................................1

P2 Various methods used for management accounting report ..............................................3

M1 Advantages of management accounting systems along with their applications in

organisational context ............................................................................................................4

D1 Critical evaluation of process through which management accounting system and

reporting integrates at organisational context.........................................................................5

TASK 2............................................................................................................................................5

P3 Measure costs by using different cost analysis techniques to prepare income statement 5

M2 Use different kind of management accounting techniques to produce financial reporting

document................................................................................................................................9

D2 Prepare a financial report which appropriately apply and interpret data for different

business activities...................................................................................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of using different kind of planning tools for budgetary

control ....................................................................................................................................9

M3 Define the use of various planning tools and their applications to prepare and forecast

budget...................................................................................................................................10

TASK 4 .........................................................................................................................................10

P5 Compare how companies adapt management accounting system to respond to financial

problems...............................................................................................................................10

M4 Analyse how in response with financial problems, management accounting can leads to

sustainable success...............................................................................................................11

D3 Various planning tools to resolve financial problemsD3 Various planning tools to resolve

financial problems................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Define management accounting and requirements for different kinds of management

accounting systems.................................................................................................................1

P2 Various methods used for management accounting report ..............................................3

M1 Advantages of management accounting systems along with their applications in

organisational context ............................................................................................................4

D1 Critical evaluation of process through which management accounting system and

reporting integrates at organisational context.........................................................................5

TASK 2............................................................................................................................................5

P3 Measure costs by using different cost analysis techniques to prepare income statement 5

M2 Use different kind of management accounting techniques to produce financial reporting

document................................................................................................................................9

D2 Prepare a financial report which appropriately apply and interpret data for different

business activities...................................................................................................................9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of using different kind of planning tools for budgetary

control ....................................................................................................................................9

M3 Define the use of various planning tools and their applications to prepare and forecast

budget...................................................................................................................................10

TASK 4 .........................................................................................................................................10

P5 Compare how companies adapt management accounting system to respond to financial

problems...............................................................................................................................10

M4 Analyse how in response with financial problems, management accounting can leads to

sustainable success...............................................................................................................11

D3 Various planning tools to resolve financial problemsD3 Various planning tools to resolve

financial problems................................................................................................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is referred to the procedure of evaluating business costs and

operations so that an appropriate financial report, accounts and records can be prepared in a

proper manner (Evans, Burritt and Guthrie, 2013). This will benefits the manager of an

organisation to take right decisions so that business goals can be achieved in proper manner. It is

a process by which costing and financial data is transformed into useful information. This

assignment is written in context with Nero Ltd which is a medium sized enterprise operating in

manufacturing sector. Company is headquartered in London, UK. This report will cover different

management accounting systems along with various methods used for management accounting

report. Also, cost analysis is performed by using absorption and marginal cost. Merits and

demerits of various planning tools for budgetary control are discussed. At last, comparison how

company adapt management account system to deal with financial issues are also mentioned.

TASK 1

P1 Define management accounting and requirements for different kinds of management

accounting systems

Management accounting is the procedure of translating estimates of managerial accounts

and data in desired knowledge so that proper guidance for decision-making can be achieved. It is

related with recording and analysing business activities for internal organisation so that overall

productivity of company can be enhanced. Management accounting system is a specialised

system that is related with the integral management of organisations with the assistance of non

financial and financial systems (Grabner and Moers, 2013). This accounting system will benefits

business firm in taking strategic decisions and plans. In case of Nero Ltd, management

accounting system will benefits the company in managing finances of company in a desired

manner. Different benefits of using management accounting systems are given below:

Increase in efficiency: These system will benefits in increasing the efficiency of various

business activities. With the help of accounting systems, main targets of company are set

on planning and forecasting so that actual performance of company can be analysed

properly.

Measurement of performance: It plays an essential role in evaluation of work

performance by using techniques associated with standard costings. This will benefits

1

Management accounting is referred to the procedure of evaluating business costs and

operations so that an appropriate financial report, accounts and records can be prepared in a

proper manner (Evans, Burritt and Guthrie, 2013). This will benefits the manager of an

organisation to take right decisions so that business goals can be achieved in proper manner. It is

a process by which costing and financial data is transformed into useful information. This

assignment is written in context with Nero Ltd which is a medium sized enterprise operating in

manufacturing sector. Company is headquartered in London, UK. This report will cover different

management accounting systems along with various methods used for management accounting

report. Also, cost analysis is performed by using absorption and marginal cost. Merits and

demerits of various planning tools for budgetary control are discussed. At last, comparison how

company adapt management account system to deal with financial issues are also mentioned.

TASK 1

P1 Define management accounting and requirements for different kinds of management

accounting systems

Management accounting is the procedure of translating estimates of managerial accounts

and data in desired knowledge so that proper guidance for decision-making can be achieved. It is

related with recording and analysing business activities for internal organisation so that overall

productivity of company can be enhanced. Management accounting system is a specialised

system that is related with the integral management of organisations with the assistance of non

financial and financial systems (Grabner and Moers, 2013). This accounting system will benefits

business firm in taking strategic decisions and plans. In case of Nero Ltd, management

accounting system will benefits the company in managing finances of company in a desired

manner. Different benefits of using management accounting systems are given below:

Increase in efficiency: These system will benefits in increasing the efficiency of various

business activities. With the help of accounting systems, main targets of company are set

on planning and forecasting so that actual performance of company can be analysed

properly.

Measurement of performance: It plays an essential role in evaluation of work

performance by using techniques associated with standard costings. This will benefits

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nero Ltd in acknowledging their overall business performance (Granlund and Lukka,

2017).

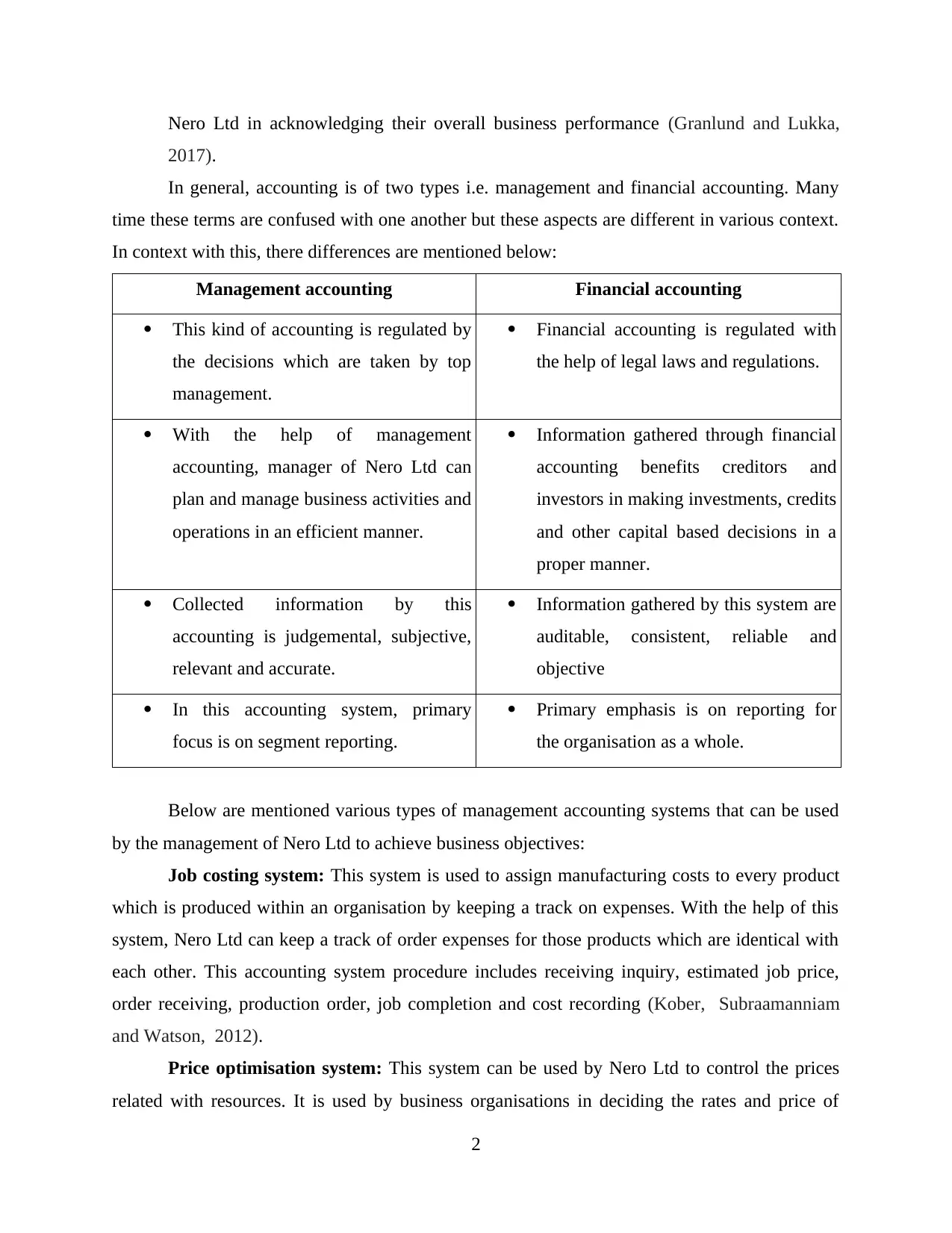

In general, accounting is of two types i.e. management and financial accounting. Many

time these terms are confused with one another but these aspects are different in various context.

In context with this, there differences are mentioned below:

Management accounting Financial accounting

This kind of accounting is regulated by

the decisions which are taken by top

management.

Financial accounting is regulated with

the help of legal laws and regulations.

With the help of management

accounting, manager of Nero Ltd can

plan and manage business activities and

operations in an efficient manner.

Information gathered through financial

accounting benefits creditors and

investors in making investments, credits

and other capital based decisions in a

proper manner.

Collected information by this

accounting is judgemental, subjective,

relevant and accurate.

Information gathered by this system are

auditable, consistent, reliable and

objective

In this accounting system, primary

focus is on segment reporting.

Primary emphasis is on reporting for

the organisation as a whole.

Below are mentioned various types of management accounting systems that can be used

by the management of Nero Ltd to achieve business objectives:

Job costing system: This system is used to assign manufacturing costs to every product

which is produced within an organisation by keeping a track on expenses. With the help of this

system, Nero Ltd can keep a track of order expenses for those products which are identical with

each other. This accounting system procedure includes receiving inquiry, estimated job price,

order receiving, production order, job completion and cost recording (Kober, Subraamanniam

and Watson, 2012).

Price optimisation system: This system can be used by Nero Ltd to control the prices

related with resources. It is used by business organisations in deciding the rates and price of

2

2017).

In general, accounting is of two types i.e. management and financial accounting. Many

time these terms are confused with one another but these aspects are different in various context.

In context with this, there differences are mentioned below:

Management accounting Financial accounting

This kind of accounting is regulated by

the decisions which are taken by top

management.

Financial accounting is regulated with

the help of legal laws and regulations.

With the help of management

accounting, manager of Nero Ltd can

plan and manage business activities and

operations in an efficient manner.

Information gathered through financial

accounting benefits creditors and

investors in making investments, credits

and other capital based decisions in a

proper manner.

Collected information by this

accounting is judgemental, subjective,

relevant and accurate.

Information gathered by this system are

auditable, consistent, reliable and

objective

In this accounting system, primary

focus is on segment reporting.

Primary emphasis is on reporting for

the organisation as a whole.

Below are mentioned various types of management accounting systems that can be used

by the management of Nero Ltd to achieve business objectives:

Job costing system: This system is used to assign manufacturing costs to every product

which is produced within an organisation by keeping a track on expenses. With the help of this

system, Nero Ltd can keep a track of order expenses for those products which are identical with

each other. This accounting system procedure includes receiving inquiry, estimated job price,

order receiving, production order, job completion and cost recording (Kober, Subraamanniam

and Watson, 2012).

Price optimisation system: This system can be used by Nero Ltd to control the prices

related with resources. It is used by business organisations in deciding the rates and price of

2

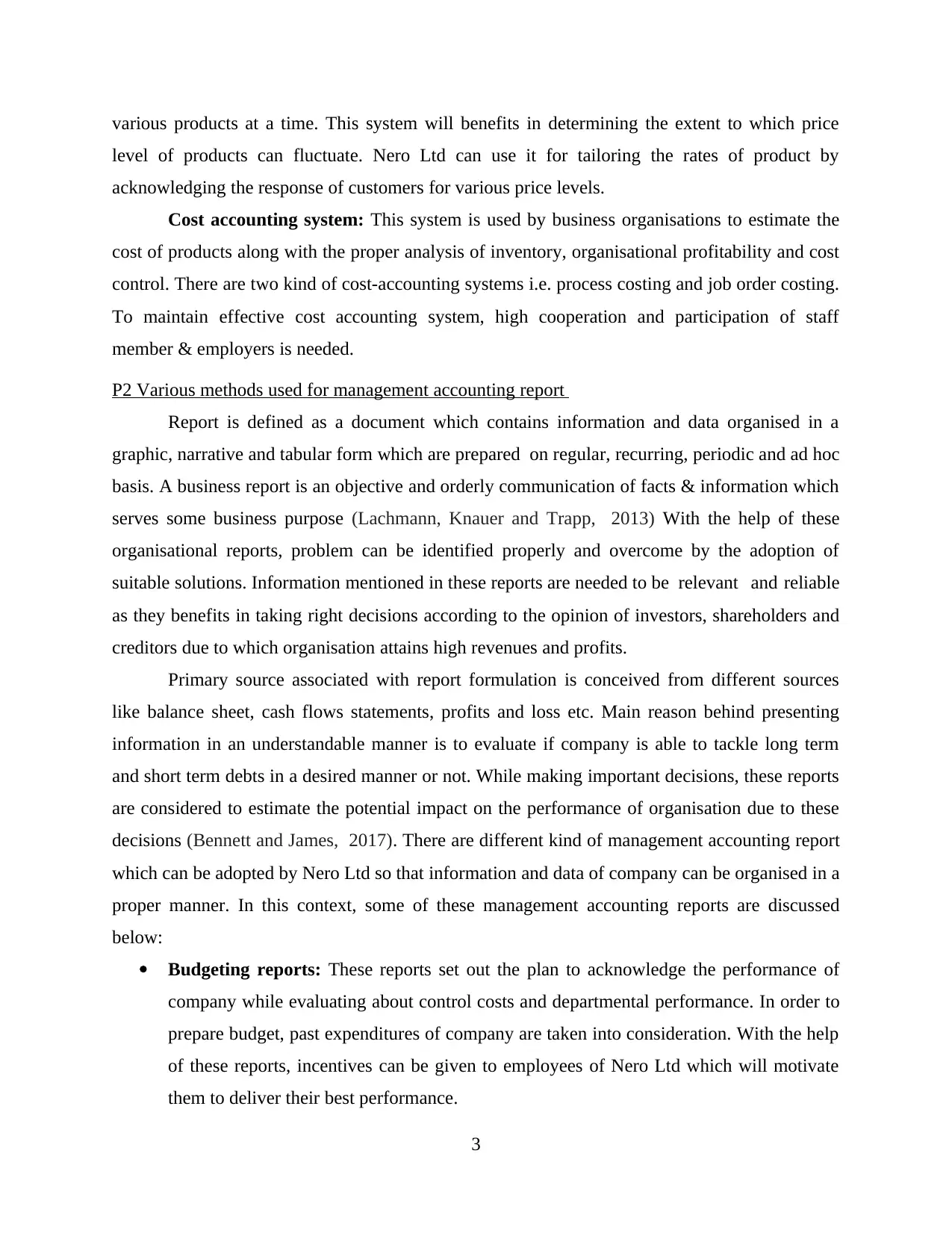

various products at a time. This system will benefits in determining the extent to which price

level of products can fluctuate. Nero Ltd can use it for tailoring the rates of product by

acknowledging the response of customers for various price levels.

Cost accounting system: This system is used by business organisations to estimate the

cost of products along with the proper analysis of inventory, organisational profitability and cost

control. There are two kind of cost-accounting systems i.e. process costing and job order costing.

To maintain effective cost accounting system, high cooperation and participation of staff

member & employers is needed.

P2 Various methods used for management accounting report

Report is defined as a document which contains information and data organised in a

graphic, narrative and tabular form which are prepared on regular, recurring, periodic and ad hoc

basis. A business report is an objective and orderly communication of facts & information which

serves some business purpose (Lachmann, Knauer and Trapp, 2013) With the help of these

organisational reports, problem can be identified properly and overcome by the adoption of

suitable solutions. Information mentioned in these reports are needed to be relevant and reliable

as they benefits in taking right decisions according to the opinion of investors, shareholders and

creditors due to which organisation attains high revenues and profits.

Primary source associated with report formulation is conceived from different sources

like balance sheet, cash flows statements, profits and loss etc. Main reason behind presenting

information in an understandable manner is to evaluate if company is able to tackle long term

and short term debts in a desired manner or not. While making important decisions, these reports

are considered to estimate the potential impact on the performance of organisation due to these

decisions (Bennett and James, 2017). There are different kind of management accounting report

which can be adopted by Nero Ltd so that information and data of company can be organised in a

proper manner. In this context, some of these management accounting reports are discussed

below:

Budgeting reports: These reports set out the plan to acknowledge the performance of

company while evaluating about control costs and departmental performance. In order to

prepare budget, past expenditures of company are taken into consideration. With the help

of these reports, incentives can be given to employees of Nero Ltd which will motivate

them to deliver their best performance.

3

level of products can fluctuate. Nero Ltd can use it for tailoring the rates of product by

acknowledging the response of customers for various price levels.

Cost accounting system: This system is used by business organisations to estimate the

cost of products along with the proper analysis of inventory, organisational profitability and cost

control. There are two kind of cost-accounting systems i.e. process costing and job order costing.

To maintain effective cost accounting system, high cooperation and participation of staff

member & employers is needed.

P2 Various methods used for management accounting report

Report is defined as a document which contains information and data organised in a

graphic, narrative and tabular form which are prepared on regular, recurring, periodic and ad hoc

basis. A business report is an objective and orderly communication of facts & information which

serves some business purpose (Lachmann, Knauer and Trapp, 2013) With the help of these

organisational reports, problem can be identified properly and overcome by the adoption of

suitable solutions. Information mentioned in these reports are needed to be relevant and reliable

as they benefits in taking right decisions according to the opinion of investors, shareholders and

creditors due to which organisation attains high revenues and profits.

Primary source associated with report formulation is conceived from different sources

like balance sheet, cash flows statements, profits and loss etc. Main reason behind presenting

information in an understandable manner is to evaluate if company is able to tackle long term

and short term debts in a desired manner or not. While making important decisions, these reports

are considered to estimate the potential impact on the performance of organisation due to these

decisions (Bennett and James, 2017). There are different kind of management accounting report

which can be adopted by Nero Ltd so that information and data of company can be organised in a

proper manner. In this context, some of these management accounting reports are discussed

below:

Budgeting reports: These reports set out the plan to acknowledge the performance of

company while evaluating about control costs and departmental performance. In order to

prepare budget, past expenditures of company are taken into consideration. With the help

of these reports, incentives can be given to employees of Nero Ltd which will motivate

them to deliver their best performance.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

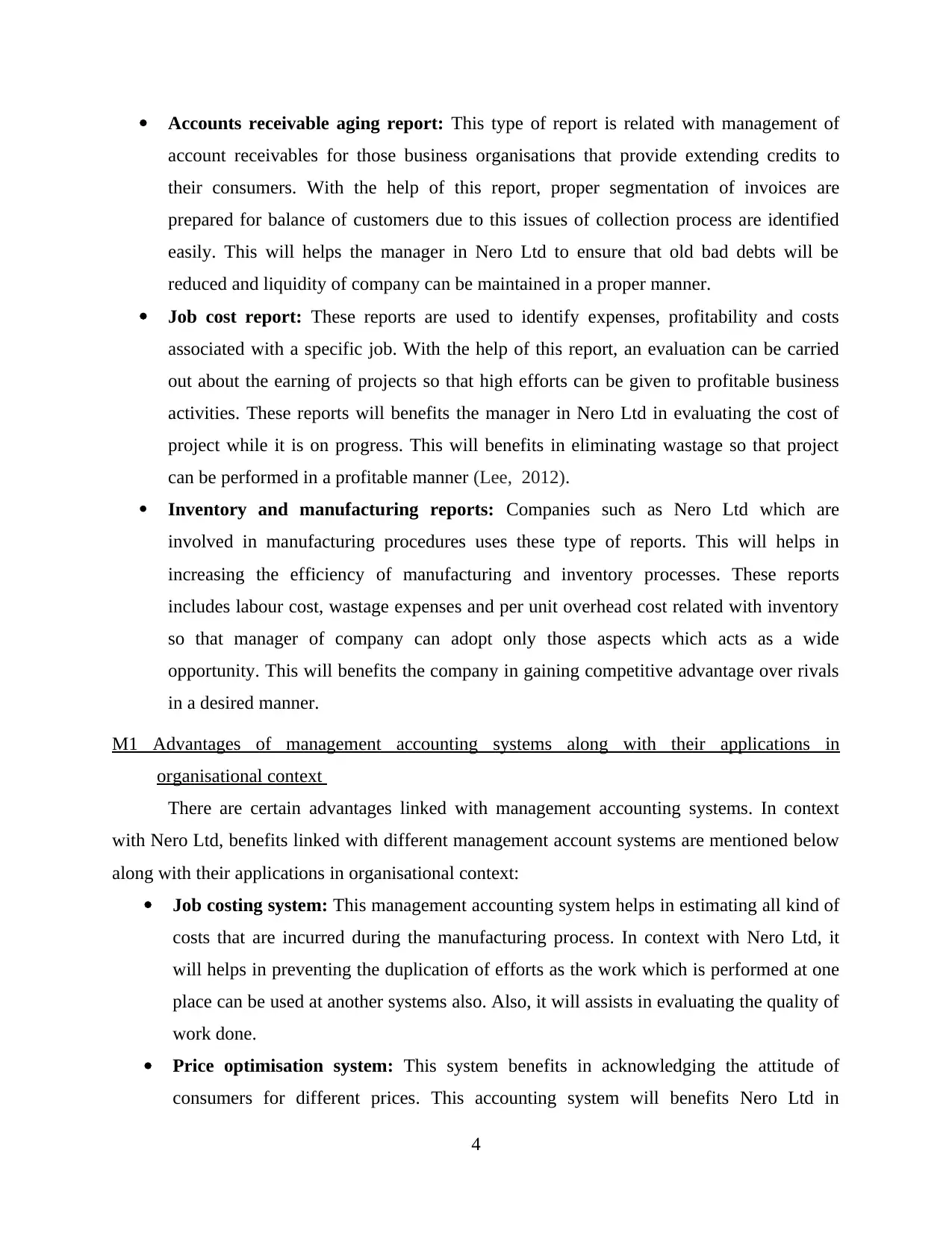

Accounts receivable aging report: This type of report is related with management of

account receivables for those business organisations that provide extending credits to

their consumers. With the help of this report, proper segmentation of invoices are

prepared for balance of customers due to this issues of collection process are identified

easily. This will helps the manager in Nero Ltd to ensure that old bad debts will be

reduced and liquidity of company can be maintained in a proper manner.

Job cost report: These reports are used to identify expenses, profitability and costs

associated with a specific job. With the help of this report, an evaluation can be carried

out about the earning of projects so that high efforts can be given to profitable business

activities. These reports will benefits the manager in Nero Ltd in evaluating the cost of

project while it is on progress. This will benefits in eliminating wastage so that project

can be performed in a profitable manner (Lee, 2012).

Inventory and manufacturing reports: Companies such as Nero Ltd which are

involved in manufacturing procedures uses these type of reports. This will helps in

increasing the efficiency of manufacturing and inventory processes. These reports

includes labour cost, wastage expenses and per unit overhead cost related with inventory

so that manager of company can adopt only those aspects which acts as a wide

opportunity. This will benefits the company in gaining competitive advantage over rivals

in a desired manner.

M1 Advantages of management accounting systems along with their applications in

organisational context

There are certain advantages linked with management accounting systems. In context

with Nero Ltd, benefits linked with different management account systems are mentioned below

along with their applications in organisational context:

Job costing system: This management accounting system helps in estimating all kind of

costs that are incurred during the manufacturing process. In context with Nero Ltd, it

will helps in preventing the duplication of efforts as the work which is performed at one

place can be used at another systems also. Also, it will assists in evaluating the quality of

work done.

Price optimisation system: This system benefits in acknowledging the attitude of

consumers for different prices. This accounting system will benefits Nero Ltd in

4

account receivables for those business organisations that provide extending credits to

their consumers. With the help of this report, proper segmentation of invoices are

prepared for balance of customers due to this issues of collection process are identified

easily. This will helps the manager in Nero Ltd to ensure that old bad debts will be

reduced and liquidity of company can be maintained in a proper manner.

Job cost report: These reports are used to identify expenses, profitability and costs

associated with a specific job. With the help of this report, an evaluation can be carried

out about the earning of projects so that high efforts can be given to profitable business

activities. These reports will benefits the manager in Nero Ltd in evaluating the cost of

project while it is on progress. This will benefits in eliminating wastage so that project

can be performed in a profitable manner (Lee, 2012).

Inventory and manufacturing reports: Companies such as Nero Ltd which are

involved in manufacturing procedures uses these type of reports. This will helps in

increasing the efficiency of manufacturing and inventory processes. These reports

includes labour cost, wastage expenses and per unit overhead cost related with inventory

so that manager of company can adopt only those aspects which acts as a wide

opportunity. This will benefits the company in gaining competitive advantage over rivals

in a desired manner.

M1 Advantages of management accounting systems along with their applications in

organisational context

There are certain advantages linked with management accounting systems. In context

with Nero Ltd, benefits linked with different management account systems are mentioned below

along with their applications in organisational context:

Job costing system: This management accounting system helps in estimating all kind of

costs that are incurred during the manufacturing process. In context with Nero Ltd, it

will helps in preventing the duplication of efforts as the work which is performed at one

place can be used at another systems also. Also, it will assists in evaluating the quality of

work done.

Price optimisation system: This system benefits in acknowledging the attitude of

consumers for different prices. This accounting system will benefits Nero Ltd in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operating profit margins with best prices (Morden, 2016). Using such system help Nero

Ltd. In identifying the actual perception of customers towards their current pricing policy

which makes easy for managers to make relevant changes in their existing pricing

strategy. This will increases the customer base as well as profitability of business.

Cost accounting system: It is capable to measure the efficiency of processes along with

carrying out improvements so that desired results can be achieved. This system will be

advantageous for the concerned organisation in fixing and reducing prices.

D1 Critical evaluation of process through which management accounting system and reporting

integrates at organisational context

Management accounting reports and systems are integrated with different process of an

organisation. This is due to the fact that various accounting systems are used by different

departments of company so that appropriate accounting reports can be prepared. For example,

finance department in Nero Ltd can use cost accounting system and manufacturing department

uses inventory management system to maintain the production of products (Bromwich and

Scapens, 2016). This shows that both these management accounting reports and system are used

in integrated manner so that organisational processes can be performed desirably. But if one of

these two aspects will not be effective, then it can results in organisational process failure.

TASK 2

P3 Measure costs by using different cost analysis techniques to prepare income statement

Cost is defied as a value of money which is used to develop anything and representing the

monitory evaluation of efforts, risks, resources, time, utilities and materials. There are different

kind of costs which are mentioned below:

Fixed cost: Fixed cost is a part of cost which remains constant for a certain time period

and doesn't get impacted with any kind of fluctuations. But due to increase in production,

per unit fixed costs of products get decreased (Soltes, 2014). It includes depreciation,

rents etc.

Variable cost: It represent the part of that cost which changes due to the variation in

production and manufacturing. This cost posses a direct relation with production,

therefore its increase or decrease depends upon output level. For example, labour, raw

material etc.

5

Ltd. In identifying the actual perception of customers towards their current pricing policy

which makes easy for managers to make relevant changes in their existing pricing

strategy. This will increases the customer base as well as profitability of business.

Cost accounting system: It is capable to measure the efficiency of processes along with

carrying out improvements so that desired results can be achieved. This system will be

advantageous for the concerned organisation in fixing and reducing prices.

D1 Critical evaluation of process through which management accounting system and reporting

integrates at organisational context

Management accounting reports and systems are integrated with different process of an

organisation. This is due to the fact that various accounting systems are used by different

departments of company so that appropriate accounting reports can be prepared. For example,

finance department in Nero Ltd can use cost accounting system and manufacturing department

uses inventory management system to maintain the production of products (Bromwich and

Scapens, 2016). This shows that both these management accounting reports and system are used

in integrated manner so that organisational processes can be performed desirably. But if one of

these two aspects will not be effective, then it can results in organisational process failure.

TASK 2

P3 Measure costs by using different cost analysis techniques to prepare income statement

Cost is defied as a value of money which is used to develop anything and representing the

monitory evaluation of efforts, risks, resources, time, utilities and materials. There are different

kind of costs which are mentioned below:

Fixed cost: Fixed cost is a part of cost which remains constant for a certain time period

and doesn't get impacted with any kind of fluctuations. But due to increase in production,

per unit fixed costs of products get decreased (Soltes, 2014). It includes depreciation,

rents etc.

Variable cost: It represent the part of that cost which changes due to the variation in

production and manufacturing. This cost posses a direct relation with production,

therefore its increase or decrease depends upon output level. For example, labour, raw

material etc.

5

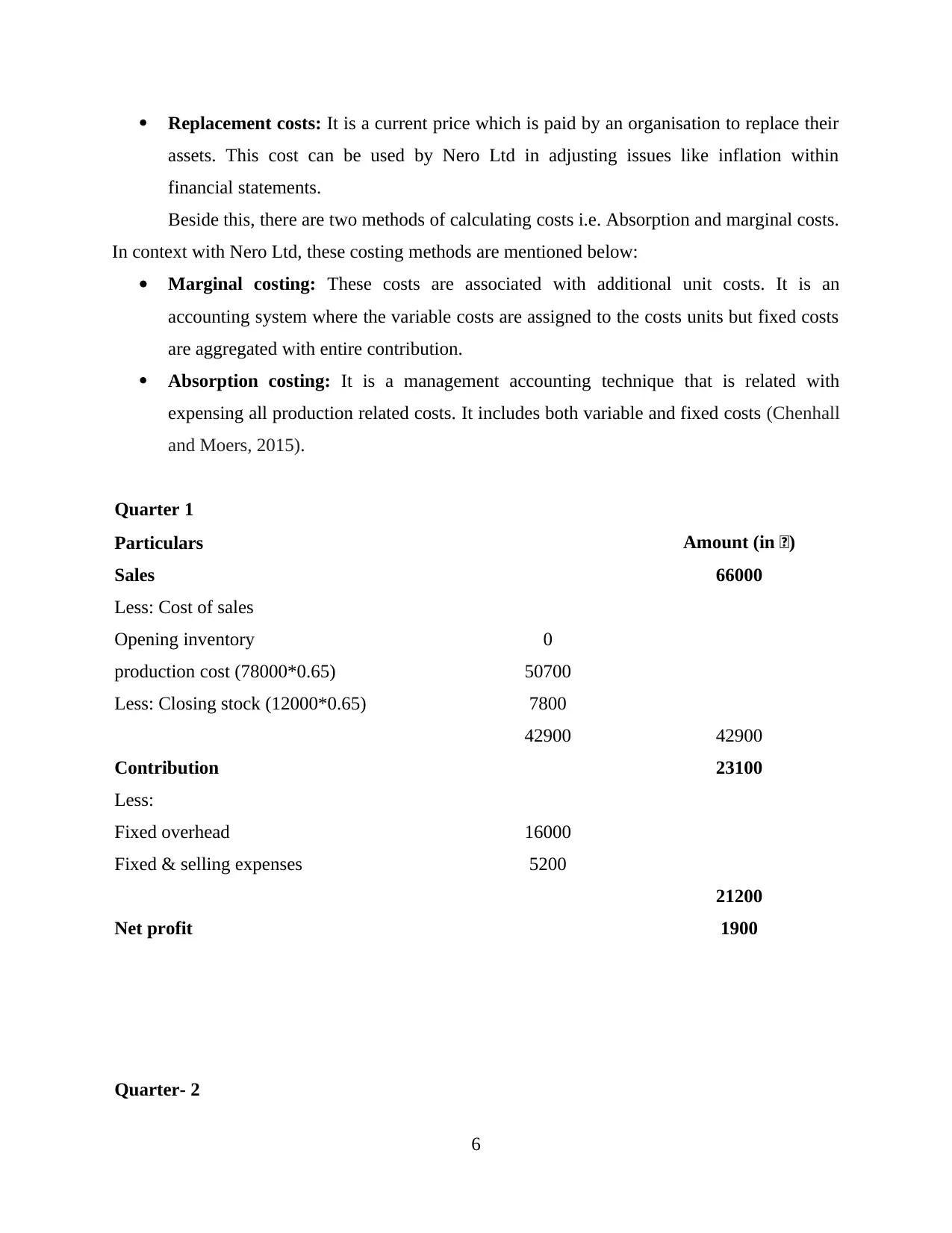

Replacement costs: It is a current price which is paid by an organisation to replace their

assets. This cost can be used by Nero Ltd in adjusting issues like inflation within

financial statements.

Beside this, there are two methods of calculating costs i.e. Absorption and marginal costs.

In context with Nero Ltd, these costing methods are mentioned below:

Marginal costing: These costs are associated with additional unit costs. It is an

accounting system where the variable costs are assigned to the costs units but fixed costs

are aggregated with entire contribution.

Absorption costing: It is a management accounting technique that is related with

expensing all production related costs. It includes both variable and fixed costs (Chenhall

and Moers, 2015).

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

6

assets. This cost can be used by Nero Ltd in adjusting issues like inflation within

financial statements.

Beside this, there are two methods of calculating costs i.e. Absorption and marginal costs.

In context with Nero Ltd, these costing methods are mentioned below:

Marginal costing: These costs are associated with additional unit costs. It is an

accounting system where the variable costs are assigned to the costs units but fixed costs

are aggregated with entire contribution.

Absorption costing: It is a management accounting technique that is related with

expensing all production related costs. It includes both variable and fixed costs (Chenhall

and Moers, 2015).

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

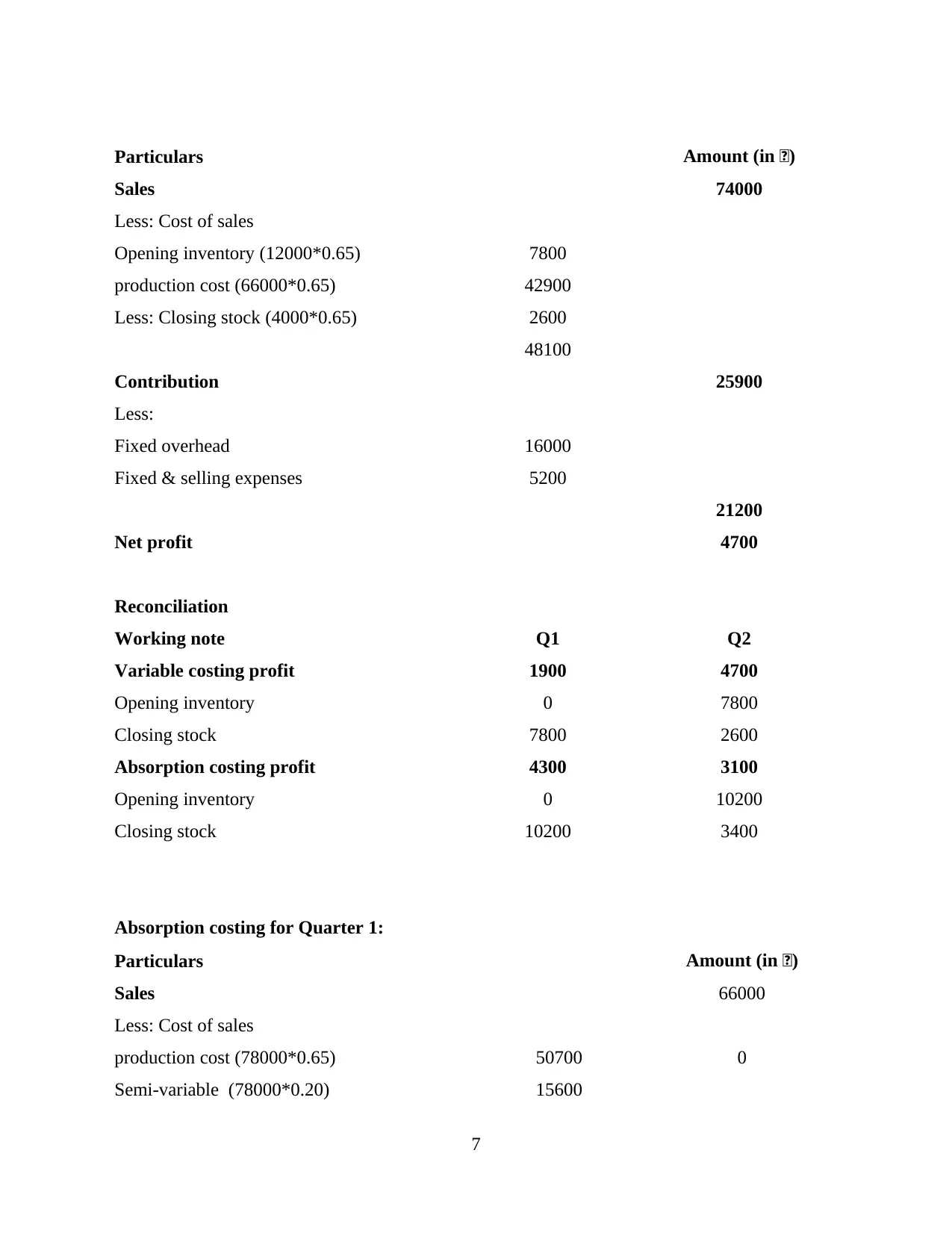

Particulars Amount (in £)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

7

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

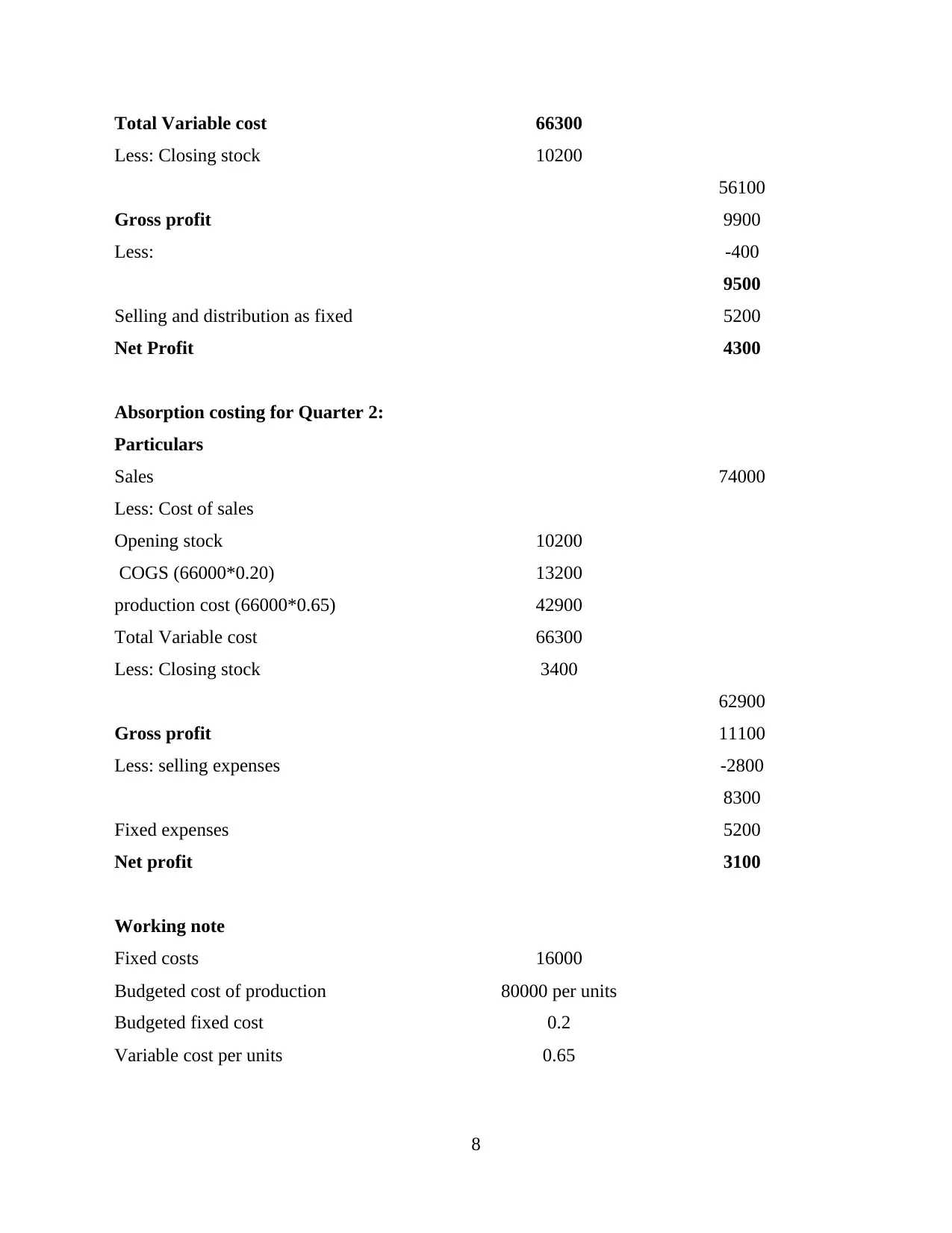

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production 80000 per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

8

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production 80000 per units

Budgeted fixed cost 0.2

Variable cost per units 0.65

8

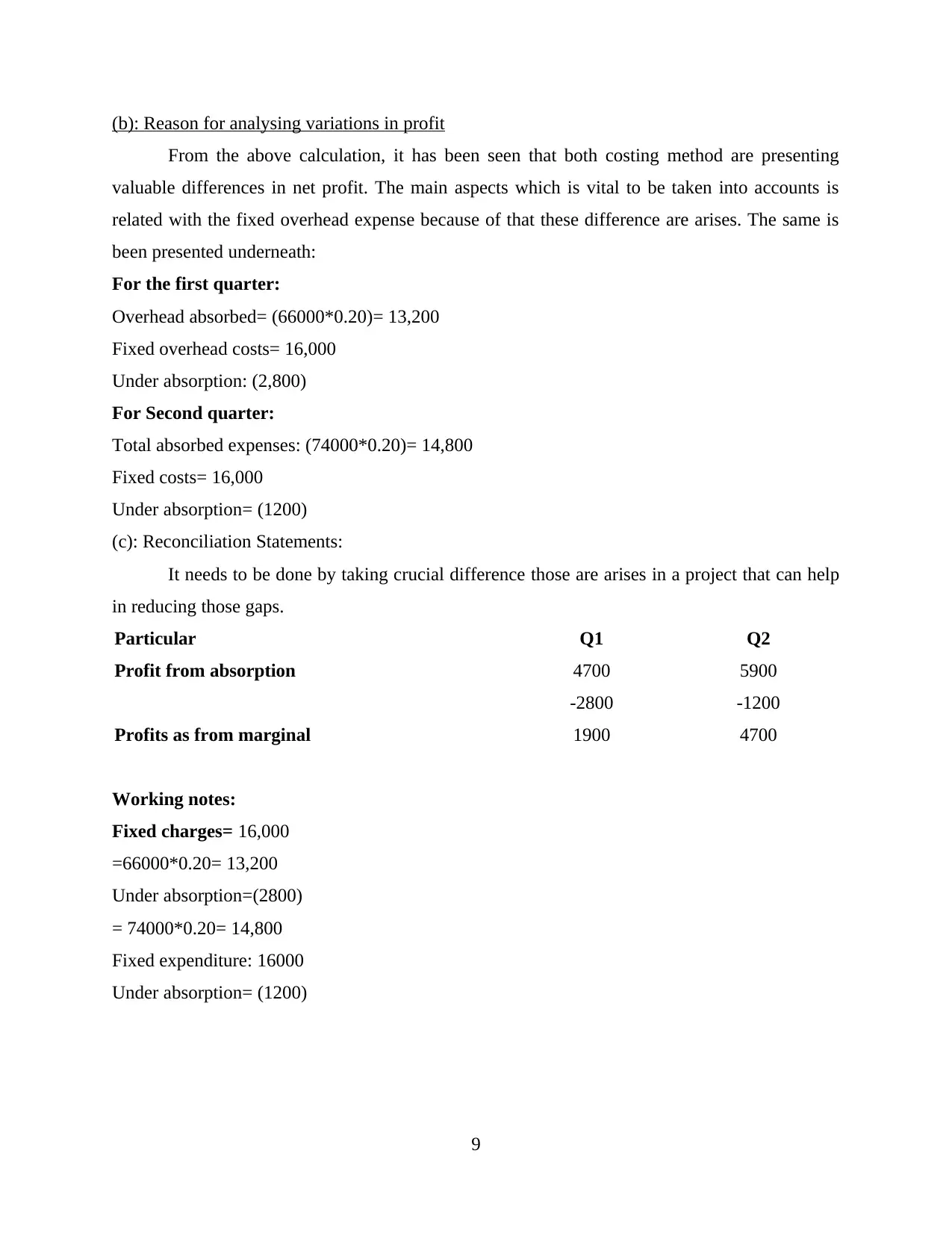

(b): Reason for analysing variations in profit

From the above calculation, it has been seen that both costing method are presenting

valuable differences in net profit. The main aspects which is vital to be taken into accounts is

related with the fixed overhead expense because of that these difference are arises. The same is

been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

(c): Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can help

in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

9

From the above calculation, it has been seen that both costing method are presenting

valuable differences in net profit. The main aspects which is vital to be taken into accounts is

related with the fixed overhead expense because of that these difference are arises. The same is

been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

(c): Reconciliation Statements:

It needs to be done by taking crucial difference those are arises in a project that can help

in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.