Management Accounting: Systems, Budgets, and Financial Issues

VerifiedAdded on 2019/12/28

|12

|4644

|341

Report

AI Summary

This report delves into the tools and techniques of management accounting, emphasizing its crucial role in business operations and financial decision-making. It differentiates between management and financial accounting, highlighting the former's focus on internal reporting for short-term decisions and performance management. The report explores various management accounting systems, including cost accounting, inventory management, job costing, and pricing optimization. It then presents income statements under marginal and absorption costing methods, demonstrating their application in financial analysis. Furthermore, the report examines different types of budgets, the budgeting process, and pricing strategies. Finally, it discusses the use of balanced scorecards to address financial issues and develop effective strategies for business growth. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in achieving organizational goals. This report will assist in the management of Imda Tech.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................................................3

TASK 1...........................................................................................................................................................................4

P1 (a) (i) What is management accounting and differentiate between management accounting and financial

accounting...................................................................................................................................................................4

(a) (ii) Importance of management accounting............................................................................................................5

P2 Describe the different systems of management accounting....................................................................................6

TASK 2...........................................................................................................................................................................7

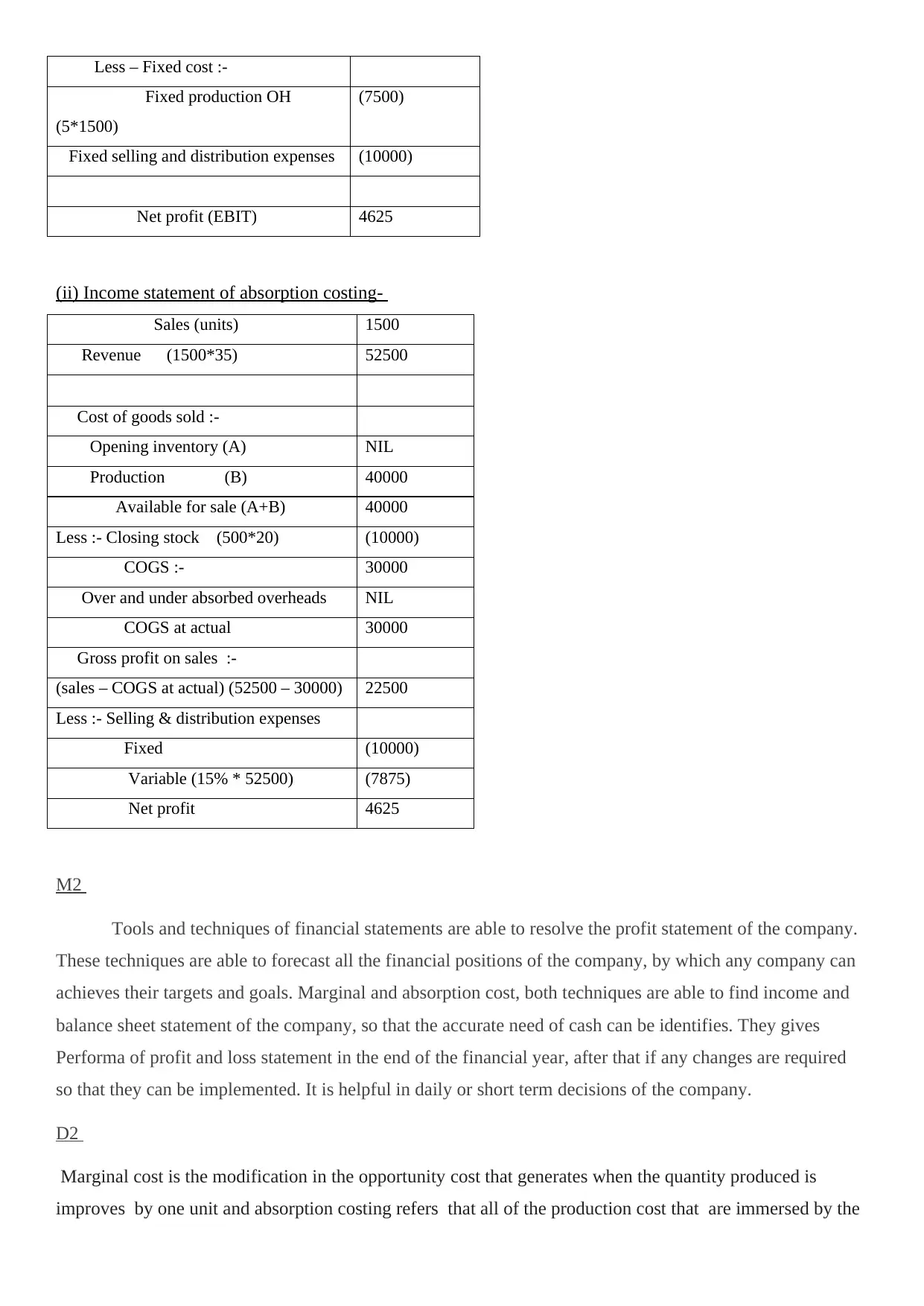

P2 (i) Income statement under marginal costing-.......................................................................................................7

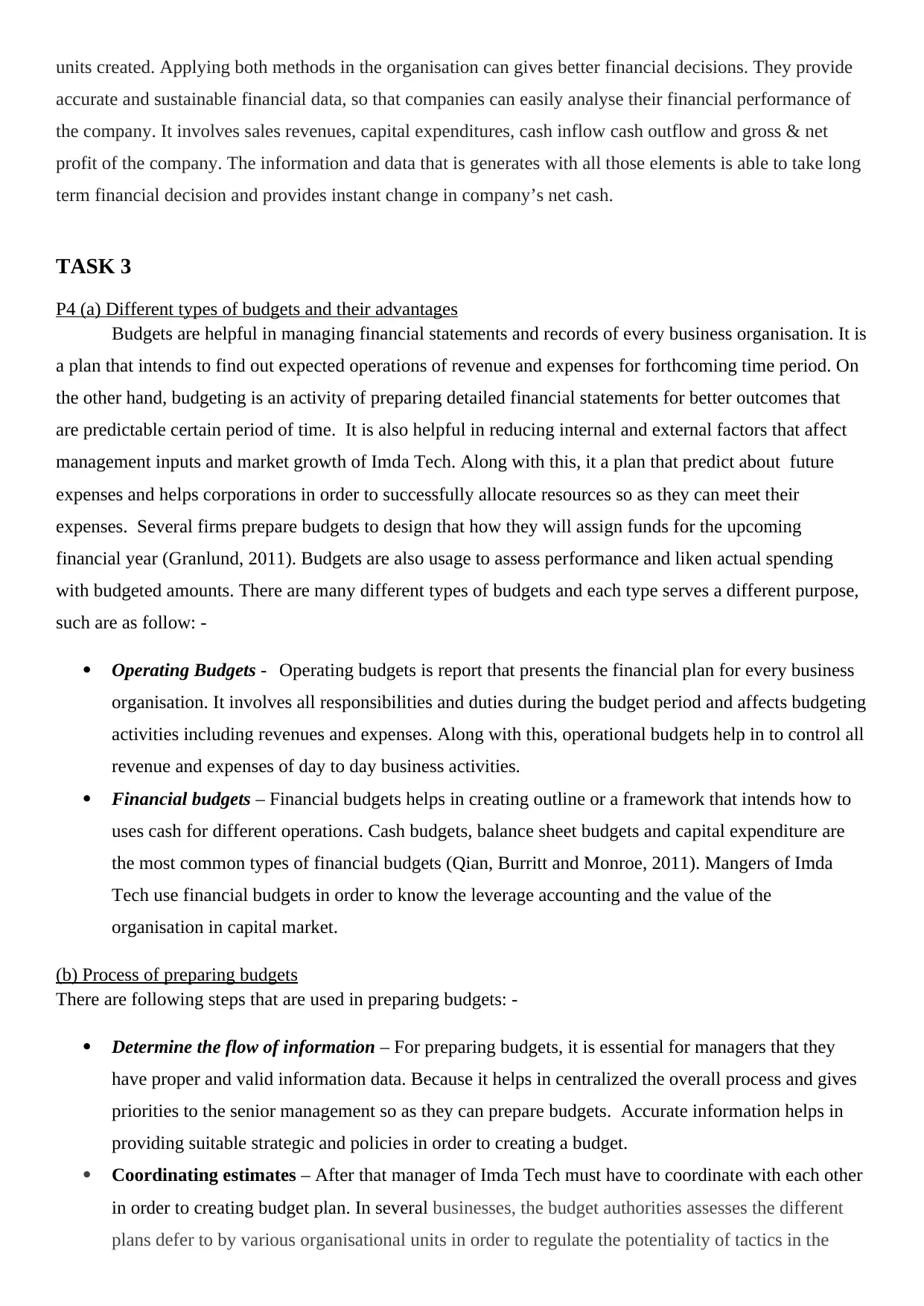

(ii) Income statement of absorption costing-...............................................................................................................8

TASK 3...........................................................................................................................................................................9

P4 (a) Different types of budgets and their advantages...............................................................................................9

(b) Process of preparing budgets.................................................................................................................................9

© What are pricing strategies....................................................................................................................................10

TASK 4......................................................................................................................................................................... 11

P5 How balanced scorecards can be used to resolve financial issues and developing effective strategies.................11

CONCLUSION.............................................................................................................................................................12

REFERENCES..............................................................................................................................................................12

INTRODUCTION...........................................................................................................................................................3

TASK 1...........................................................................................................................................................................4

P1 (a) (i) What is management accounting and differentiate between management accounting and financial

accounting...................................................................................................................................................................4

(a) (ii) Importance of management accounting............................................................................................................5

P2 Describe the different systems of management accounting....................................................................................6

TASK 2...........................................................................................................................................................................7

P2 (i) Income statement under marginal costing-.......................................................................................................7

(ii) Income statement of absorption costing-...............................................................................................................8

TASK 3...........................................................................................................................................................................9

P4 (a) Different types of budgets and their advantages...............................................................................................9

(b) Process of preparing budgets.................................................................................................................................9

© What are pricing strategies....................................................................................................................................10

TASK 4......................................................................................................................................................................... 11

P5 How balanced scorecards can be used to resolve financial issues and developing effective strategies.................11

CONCLUSION.............................................................................................................................................................12

REFERENCES..............................................................................................................................................................12

INTRODUCTION

This report is based upon tools and techniques of management accounting. Management accounting

is an essential tool of every business organisation and its day to day operations. It helps in to measure the

performance of company and provide necessary solution so as company can develop its market growth.

Along with this, management accounting is totally differ from financial accounting, because financial

accounting is make for an annual where management accounting is make for day to day and short term

financial decisions (Kaplan and Atkinson, 2015). Further for this, it is also helpful in creating budgets and

financial statements so as managers can easily analysis the actual position of company in capital market.

Budgets are also useful provide the accurate and timely financial conditions of the company and it also

assistive in where and how to spend money on business activities and functions.

TASK 1

P1 (a) (i) What is management accounting and differentiate between management accounting and financial

accounting

Management accounting is the term that is helpful in provides accounting information to managers

so as they can take better financial decisions, that is aid with their management and performance of control

activities. Along with this, it is helpful in order to take day to day or short term financial decision for the

betterment of business organisation. According to Institute of Management accountants, management

accounting is a system of performance management which controls to assists the formulation of

management functions and regulation of management strategy (Ward, 2012). In includes providing and

preparing timely financial reports and statements to the managers so as they can easily forecasting

forthcoming growth of Imda Tech. For a management accountant, it is very essential to he has a solid

knowledge of accounting practise, that is essential for every business organisation. Due to this, management

accounting is also called managerial accounting and cost accounting, that is totally differ from financial

accounting, in that it produces financial reports for an organisation’s internal stakeholder as opposed to

external stakeholders. So as management accounting is a combination of finance, management and

accounting that involves real values of business techniques and skills in order to add real value for any

business organisation. There is a difference between management accounting and financial accounting that

is as follow: -

Management Accounting Financial Accounting

Management accounting refers to collate information

such as outstanding debts, cash flow and revenue, so

that reports can be produces timely. It is also

assistive in delivering statistical information,

business decisions and day to day operations of

management (Burritt, Schaltegger and Zvezdov,

Financial accounting is helpful in preparing reports

and it is usually based upon the past performance of

manager; in line with reporting requirements.

This report is based upon tools and techniques of management accounting. Management accounting

is an essential tool of every business organisation and its day to day operations. It helps in to measure the

performance of company and provide necessary solution so as company can develop its market growth.

Along with this, management accounting is totally differ from financial accounting, because financial

accounting is make for an annual where management accounting is make for day to day and short term

financial decisions (Kaplan and Atkinson, 2015). Further for this, it is also helpful in creating budgets and

financial statements so as managers can easily analysis the actual position of company in capital market.

Budgets are also useful provide the accurate and timely financial conditions of the company and it also

assistive in where and how to spend money on business activities and functions.

TASK 1

P1 (a) (i) What is management accounting and differentiate between management accounting and financial

accounting

Management accounting is the term that is helpful in provides accounting information to managers

so as they can take better financial decisions, that is aid with their management and performance of control

activities. Along with this, it is helpful in order to take day to day or short term financial decision for the

betterment of business organisation. According to Institute of Management accountants, management

accounting is a system of performance management which controls to assists the formulation of

management functions and regulation of management strategy (Ward, 2012). In includes providing and

preparing timely financial reports and statements to the managers so as they can easily forecasting

forthcoming growth of Imda Tech. For a management accountant, it is very essential to he has a solid

knowledge of accounting practise, that is essential for every business organisation. Due to this, management

accounting is also called managerial accounting and cost accounting, that is totally differ from financial

accounting, in that it produces financial reports for an organisation’s internal stakeholder as opposed to

external stakeholders. So as management accounting is a combination of finance, management and

accounting that involves real values of business techniques and skills in order to add real value for any

business organisation. There is a difference between management accounting and financial accounting that

is as follow: -

Management Accounting Financial Accounting

Management accounting refers to collate information

such as outstanding debts, cash flow and revenue, so

that reports can be produces timely. It is also

assistive in delivering statistical information,

business decisions and day to day operations of

management (Burritt, Schaltegger and Zvezdov,

Financial accounting is helpful in preparing reports

and it is usually based upon the past performance of

manager; in line with reporting requirements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2011).

It is a combination of financial information and non-

financial information data in order to design a

complete image of organisation. This is usually used

in to drive business success.

It provides the essential financial information that is

used by others activities within the business, for

example- departmental managers.

The process of management accounting is preparing

reports and profit and loss statements, in order to provide

timely and accurate information to finance managers.

And creates weekly or monthly financial reports for

managers.

Financial accounting reports are helps in creating

annual business reports for any business

organisations. In that, all accounting functions are

involved.

Management accounting is based upon

assumptions, convention and various principles,

assumptions like consistency, realisation,

matching, materiality and going concern etc .

It is able to be responsible for both quantitative and

qualitative information’s and data as well that is

being assessed and captured by accounting

managers.

(a) (ii) Importance of management accounting

Management accounting plays a very essential role in growth and success of every business

organisation. There is mention below the advantage as well as importance of management accounting, such

as follow: -

Reduces Expenses – Management accounting is helpful in reduces expenses by providing effective

techniques for controlling damages and wastages. Along with this, in Imda Tech managers often use

management accounting data and information in order to review the prices of economic resources

and further business operations. So as, due to this information managers can easily analyse how

much money, need to run their business. Management accounting is also helpful in conducting

evaluation on the quality of economic resources that are used in producing products and services. So

as the quality of overall product cannot be suffer by its cheap and lower prices.

Improves Cash flow – Management accounting is also accommodating by improving cash flow of

company so as managers can easily understand how much spend on business functions and

operation. It is also helps in creating budgets; budgets are the important part of management

accounting. Managers of Imda Tech, must have to used budgets so as they can maintain their annual

balance sheets and financial reports as well. As along, the performance of organisation can be easily

evaluated and managers can develop their strategic in order to improve the productivity of

organisation. Management accounting enables the management in order to identify deviations among

actual cost and standard cost.

Business decisions – It is also helps in taking day to short term business decisions so as managers

can take risk in order to achieve growth and success. Sometimes it is very essential to take fast and

It is a combination of financial information and non-

financial information data in order to design a

complete image of organisation. This is usually used

in to drive business success.

It provides the essential financial information that is

used by others activities within the business, for

example- departmental managers.

The process of management accounting is preparing

reports and profit and loss statements, in order to provide

timely and accurate information to finance managers.

And creates weekly or monthly financial reports for

managers.

Financial accounting reports are helps in creating

annual business reports for any business

organisations. In that, all accounting functions are

involved.

Management accounting is based upon

assumptions, convention and various principles,

assumptions like consistency, realisation,

matching, materiality and going concern etc .

It is able to be responsible for both quantitative and

qualitative information’s and data as well that is

being assessed and captured by accounting

managers.

(a) (ii) Importance of management accounting

Management accounting plays a very essential role in growth and success of every business

organisation. There is mention below the advantage as well as importance of management accounting, such

as follow: -

Reduces Expenses – Management accounting is helpful in reduces expenses by providing effective

techniques for controlling damages and wastages. Along with this, in Imda Tech managers often use

management accounting data and information in order to review the prices of economic resources

and further business operations. So as, due to this information managers can easily analyse how

much money, need to run their business. Management accounting is also helpful in conducting

evaluation on the quality of economic resources that are used in producing products and services. So

as the quality of overall product cannot be suffer by its cheap and lower prices.

Improves Cash flow – Management accounting is also accommodating by improving cash flow of

company so as managers can easily understand how much spend on business functions and

operation. It is also helps in creating budgets; budgets are the important part of management

accounting. Managers of Imda Tech, must have to used budgets so as they can maintain their annual

balance sheets and financial reports as well. As along, the performance of organisation can be easily

evaluated and managers can develop their strategic in order to improve the productivity of

organisation. Management accounting enables the management in order to identify deviations among

actual cost and standard cost.

Business decisions – It is also helps in taking day to short term business decisions so as managers

can take risk in order to achieve growth and success. Sometimes it is very essential to take fast and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quick decision for accomplishing goals and objectives. Management accounting also provides

qualitative analysis for decision making process of Imda Tech, so as they can take effective and

impressive decision for developing organisation aims. It is easier the judgement and provides quality

services to managers. If managers are capable to take business decisions effectively therefore it is

beneficial for organisation for its growth and success.

Providing effective management control – The tool and techniques of management accounting are

also helpful in providing effective control on management activities and operations. Managers can

easily establishes their control on planning and coordinating activities so as the employees can

improves their performance level in order to accomplishes heights of success in capital market. It is

also helpful in maximising profit and growth by reducing inefficiencies and incapability. Along with

this, the information and data revived by management accounting is helps in safe and secure from

past trade cycle.

P2 Describe the different systems of management accounting

There are different types of management accounting that are as follow: -

Cost Accounting system – Cost accounting system is a framework that is used by companies in order

to estimate the cost of their products and services, it is helpful in cost controlling, profitable analysis

and inventory valuation. The system also called product costing system. It is critical for profitable

operations by estimation the actual cost of products and services. Cost accounting system helps for

Imda tech, in order to know that which products are beneficial for them or which are not. Job order

costing and process costing are the two main elements of cost accounting system (Parker, 2012).

Along with this, it is the process that aims to capture the production cost of the company by

evaluating the input costs each step of fixed as well as production cost.

Inventory management system – Inventory management system helps in to maintain the stocks and

inventories of every business originations. Managers applying various methods and techniques so as

they can easily manage their inventory in business organisation. It is an on-going process that helps

in moving out products and their parts from company’s location. Imda Tech also manages its

inventory on daily basis and place new orders accordingly, it is very essential that managers gain a

firm understanding of everything include in the inventory management process. With that, business

leaders are able to identify different ways of resolving management challenges or issues and also

figure out accurate solutions.

Job Costing system – Job costing system that tracks the revenues and costs by job. It involves the

process of accruing information about the costs related with a particular production or service

job. This information is required in order to acquiesce the cost information to a customer under

a contract where costs are reimbursed (Otley and Emmanuel, 2013). The information is also

useful for determining the accuracy of a company's estimating system, which should be able to

qualitative analysis for decision making process of Imda Tech, so as they can take effective and

impressive decision for developing organisation aims. It is easier the judgement and provides quality

services to managers. If managers are capable to take business decisions effectively therefore it is

beneficial for organisation for its growth and success.

Providing effective management control – The tool and techniques of management accounting are

also helpful in providing effective control on management activities and operations. Managers can

easily establishes their control on planning and coordinating activities so as the employees can

improves their performance level in order to accomplishes heights of success in capital market. It is

also helpful in maximising profit and growth by reducing inefficiencies and incapability. Along with

this, the information and data revived by management accounting is helps in safe and secure from

past trade cycle.

P2 Describe the different systems of management accounting

There are different types of management accounting that are as follow: -

Cost Accounting system – Cost accounting system is a framework that is used by companies in order

to estimate the cost of their products and services, it is helpful in cost controlling, profitable analysis

and inventory valuation. The system also called product costing system. It is critical for profitable

operations by estimation the actual cost of products and services. Cost accounting system helps for

Imda tech, in order to know that which products are beneficial for them or which are not. Job order

costing and process costing are the two main elements of cost accounting system (Parker, 2012).

Along with this, it is the process that aims to capture the production cost of the company by

evaluating the input costs each step of fixed as well as production cost.

Inventory management system – Inventory management system helps in to maintain the stocks and

inventories of every business originations. Managers applying various methods and techniques so as

they can easily manage their inventory in business organisation. It is an on-going process that helps

in moving out products and their parts from company’s location. Imda Tech also manages its

inventory on daily basis and place new orders accordingly, it is very essential that managers gain a

firm understanding of everything include in the inventory management process. With that, business

leaders are able to identify different ways of resolving management challenges or issues and also

figure out accurate solutions.

Job Costing system – Job costing system that tracks the revenues and costs by job. It involves the

process of accruing information about the costs related with a particular production or service

job. This information is required in order to acquiesce the cost information to a customer under

a contract where costs are reimbursed (Otley and Emmanuel, 2013). The information is also

useful for determining the accuracy of a company's estimating system, which should be able to

estimate prices that allow for a judicious profit. The information can also be used to allocate

inventorial costs to manufactured goods.

Pricing optimising system –Pricing optimising system is the mathematical analysis by an

organisation in order to know the respond of customers for different prices of a particular

product. The system is also helpful in order to maximising the operating profits of the company,

so as it can able to achieve its goals and objectives. The practice of price optimising can be used

in different industries such as retail, banking, casinos, car rental, insurance sectors hotels and

airlines industries etc. The information and the data used in price optimising system is based

upon historical prices, sales, operating cost and inventories.

M1

Management accounting is helpful in providing the financial data and records to the managers, so

that they can easily use it at the time of needed. Managers can easily take day to day and short term business

decisions for their managerial operations. It is also helpful in reduces expenses by reviewing the cost of

economic resources and other business operations and activities. It also improves cash flow of the company

by making annual budgets.

D1

Management accounting and reporting is a system by organisations can easily evaluate their financial

as well as corporate performance. It is related with day to day accounting operation and assistive in making

short term decisions. Along with this, it also helps in forecasting the upcoming position of business

organisation (Cadez and Guilding, 2012). It collects all the financial statements and reports by company can

able to assess its financial performance and position in market.

TASK 2

P2 (i) Income statement under marginal costing-

Sales (35 X 1500) 52500

Less - Variable cost :-

Labour (5 * 1500) (7500)

Material ( 5 * 1500) (12000)

Variable production OH (2*1500) (30000)

Variable selling and distribution

expenses

(52500* 15%)

(7875)

Contribution 22125

inventorial costs to manufactured goods.

Pricing optimising system –Pricing optimising system is the mathematical analysis by an

organisation in order to know the respond of customers for different prices of a particular

product. The system is also helpful in order to maximising the operating profits of the company,

so as it can able to achieve its goals and objectives. The practice of price optimising can be used

in different industries such as retail, banking, casinos, car rental, insurance sectors hotels and

airlines industries etc. The information and the data used in price optimising system is based

upon historical prices, sales, operating cost and inventories.

M1

Management accounting is helpful in providing the financial data and records to the managers, so

that they can easily use it at the time of needed. Managers can easily take day to day and short term business

decisions for their managerial operations. It is also helpful in reduces expenses by reviewing the cost of

economic resources and other business operations and activities. It also improves cash flow of the company

by making annual budgets.

D1

Management accounting and reporting is a system by organisations can easily evaluate their financial

as well as corporate performance. It is related with day to day accounting operation and assistive in making

short term decisions. Along with this, it also helps in forecasting the upcoming position of business

organisation (Cadez and Guilding, 2012). It collects all the financial statements and reports by company can

able to assess its financial performance and position in market.

TASK 2

P2 (i) Income statement under marginal costing-

Sales (35 X 1500) 52500

Less - Variable cost :-

Labour (5 * 1500) (7500)

Material ( 5 * 1500) (12000)

Variable production OH (2*1500) (30000)

Variable selling and distribution

expenses

(52500* 15%)

(7875)

Contribution 22125

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less – Fixed cost :-

Fixed production OH

(5*1500)

(7500)

Fixed selling and distribution expenses (10000)

Net profit (EBIT) 4625

(ii) Income statement of absorption costing-

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold :-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less :- Closing stock (500*20) (10000)

COGS :- 30000

Over and under absorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual) (52500 – 30000) 22500

Less :- Selling & distribution expenses

Fixed (10000)

Variable (15% * 52500) (7875)

Net profit 4625

M2

Tools and techniques of financial statements are able to resolve the profit statement of the company.

These techniques are able to forecast all the financial positions of the company, by which any company can

achieves their targets and goals. Marginal and absorption cost, both techniques are able to find income and

balance sheet statement of the company, so that the accurate need of cash can be identifies. They gives

Performa of profit and loss statement in the end of the financial year, after that if any changes are required

so that they can be implemented. It is helpful in daily or short term decisions of the company.

D2

Marginal cost is the modification in the opportunity cost that generates when the quantity produced is

improves by one unit and absorption costing refers that all of the production cost that are immersed by the

Fixed production OH

(5*1500)

(7500)

Fixed selling and distribution expenses (10000)

Net profit (EBIT) 4625

(ii) Income statement of absorption costing-

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold :-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less :- Closing stock (500*20) (10000)

COGS :- 30000

Over and under absorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual) (52500 – 30000) 22500

Less :- Selling & distribution expenses

Fixed (10000)

Variable (15% * 52500) (7875)

Net profit 4625

M2

Tools and techniques of financial statements are able to resolve the profit statement of the company.

These techniques are able to forecast all the financial positions of the company, by which any company can

achieves their targets and goals. Marginal and absorption cost, both techniques are able to find income and

balance sheet statement of the company, so that the accurate need of cash can be identifies. They gives

Performa of profit and loss statement in the end of the financial year, after that if any changes are required

so that they can be implemented. It is helpful in daily or short term decisions of the company.

D2

Marginal cost is the modification in the opportunity cost that generates when the quantity produced is

improves by one unit and absorption costing refers that all of the production cost that are immersed by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

units created. Applying both methods in the organisation can gives better financial decisions. They provide

accurate and sustainable financial data, so that companies can easily analyse their financial performance of

the company. It involves sales revenues, capital expenditures, cash inflow cash outflow and gross & net

profit of the company. The information and data that is generates with all those elements is able to take long

term financial decision and provides instant change in company’s net cash.

TASK 3

P4 (a) Different types of budgets and their advantages

Budgets are helpful in managing financial statements and records of every business organisation. It is

a plan that intends to find out expected operations of revenue and expenses for forthcoming time period. On

the other hand, budgeting is an activity of preparing detailed financial statements for better outcomes that

are predictable certain period of time. It is also helpful in reducing internal and external factors that affect

management inputs and market growth of Imda Tech. Along with this, it a plan that predict about future

expenses and helps corporations in order to successfully allocate resources so as they can meet their

expenses. Several firms prepare budgets to design that how they will assign funds for the upcoming

financial year (Granlund, 2011). Budgets are also usage to assess performance and liken actual spending

with budgeted amounts. There are many different types of budgets and each type serves a different purpose,

such are as follow: -

Operating Budgets - Operating budgets is report that presents the financial plan for every business

organisation. It involves all responsibilities and duties during the budget period and affects budgeting

activities including revenues and expenses. Along with this, operational budgets help in to control all

revenue and expenses of day to day business activities.

Financial budgets – Financial budgets helps in creating outline or a framework that intends how to

uses cash for different operations. Cash budgets, balance sheet budgets and capital expenditure are

the most common types of financial budgets (Qian, Burritt and Monroe, 2011). Mangers of Imda

Tech use financial budgets in order to know the leverage accounting and the value of the

organisation in capital market.

(b) Process of preparing budgets

There are following steps that are used in preparing budgets: -

Determine the flow of information – For preparing budgets, it is essential for managers that they

have proper and valid information data. Because it helps in centralized the overall process and gives

priorities to the senior management so as they can prepare budgets. Accurate information helps in

providing suitable strategic and policies in order to creating a budget.

Coordinating estimates – After that manager of Imda Tech must have to coordinate with each other

in order to creating budget plan. In several businesses, the budget authorities assesses the different

plans defer to by various organisational units in order to regulate the potentiality of tactics in the

accurate and sustainable financial data, so that companies can easily analyse their financial performance of

the company. It involves sales revenues, capital expenditures, cash inflow cash outflow and gross & net

profit of the company. The information and data that is generates with all those elements is able to take long

term financial decision and provides instant change in company’s net cash.

TASK 3

P4 (a) Different types of budgets and their advantages

Budgets are helpful in managing financial statements and records of every business organisation. It is

a plan that intends to find out expected operations of revenue and expenses for forthcoming time period. On

the other hand, budgeting is an activity of preparing detailed financial statements for better outcomes that

are predictable certain period of time. It is also helpful in reducing internal and external factors that affect

management inputs and market growth of Imda Tech. Along with this, it a plan that predict about future

expenses and helps corporations in order to successfully allocate resources so as they can meet their

expenses. Several firms prepare budgets to design that how they will assign funds for the upcoming

financial year (Granlund, 2011). Budgets are also usage to assess performance and liken actual spending

with budgeted amounts. There are many different types of budgets and each type serves a different purpose,

such are as follow: -

Operating Budgets - Operating budgets is report that presents the financial plan for every business

organisation. It involves all responsibilities and duties during the budget period and affects budgeting

activities including revenues and expenses. Along with this, operational budgets help in to control all

revenue and expenses of day to day business activities.

Financial budgets – Financial budgets helps in creating outline or a framework that intends how to

uses cash for different operations. Cash budgets, balance sheet budgets and capital expenditure are

the most common types of financial budgets (Qian, Burritt and Monroe, 2011). Mangers of Imda

Tech use financial budgets in order to know the leverage accounting and the value of the

organisation in capital market.

(b) Process of preparing budgets

There are following steps that are used in preparing budgets: -

Determine the flow of information – For preparing budgets, it is essential for managers that they

have proper and valid information data. Because it helps in centralized the overall process and gives

priorities to the senior management so as they can prepare budgets. Accurate information helps in

providing suitable strategic and policies in order to creating a budget.

Coordinating estimates – After that manager of Imda Tech must have to coordinate with each other

in order to creating budget plan. In several businesses, the budget authorities assesses the different

plans defer to by various organisational units in order to regulate the potentiality of tactics in the

overall interest of the enterprise and to appraisal what kind of resources are existing and how they

can be fairly allocated amid the several units of the organisation (Qian, Burritt and Monroe,2011.).

Communicating the budget – It is the responsibility of the managers that they communicate the

budgets among overall employees, so as everyone is being known about the budget plan and what is

company expects from them. Necessary changes and modifications should be done after creating any

final budget.

Implementation of budget plan – So as, now the final budget is ready to implement. Then managers

have to regulate the budget plan for upcoming budget period.

© What are pricing strategies-

Every business organisation uses pricing strategies in order to selling any products or services. The

price of the product is set to earn maximum profit for each unit of product from the overall market. It is

helpful in to increasing market share when a company entre into a new market. Pricing is one of the most

important components of marketing mix. It is helpful in order to understand the quality of products and

services. There are two main types of pricing strategies, are as follow: -

Penetration pricing – Penetration pricing polices is helpful for small business organisation in order

to sets their prices low. Along with this, low prices also help in when a company enter into a new

market so as it can attracts more customers (Soin and Collier, 2013).

Price skimming – price skimming refers when the prices of products are very high in order to

recover all expenditures of production and advertising. Many companies’ uses price skimming

methods so as they can achieve profit fast and quickly.

M3

Different planning methods of budgets are helpful in forecasting the financial situation of the company.

Planned budgets are always successful, because they have proper idea of how to spend cash of different

commercial activities, of the business. They gives support to the managers, in order to make another

specific policies for the next financial year, it is also supplying flexible cash flow in the company. It is also

accommodating in pinpoint of shortfalls and increases the instant changes in net cash. It gives a proper

format of sales revenue and expenditure to the business organisation (Cuganesan, Dunford and Palmer,

2012). Budget forecasting is helpful in making long term decision s for the organisation as well as day to

day operations also, by using this company can easily grow its market share in the overall capital market

place.

D3

Planning tools and techniques are able to reduce risk and uncertainties in the capital market. They are

responsible for organisational success and its growth & development. It is able to provide the long term

business polices and strategies, so that any business can compete with new entrants in the corporate market.

can be fairly allocated amid the several units of the organisation (Qian, Burritt and Monroe,2011.).

Communicating the budget – It is the responsibility of the managers that they communicate the

budgets among overall employees, so as everyone is being known about the budget plan and what is

company expects from them. Necessary changes and modifications should be done after creating any

final budget.

Implementation of budget plan – So as, now the final budget is ready to implement. Then managers

have to regulate the budget plan for upcoming budget period.

© What are pricing strategies-

Every business organisation uses pricing strategies in order to selling any products or services. The

price of the product is set to earn maximum profit for each unit of product from the overall market. It is

helpful in to increasing market share when a company entre into a new market. Pricing is one of the most

important components of marketing mix. It is helpful in order to understand the quality of products and

services. There are two main types of pricing strategies, are as follow: -

Penetration pricing – Penetration pricing polices is helpful for small business organisation in order

to sets their prices low. Along with this, low prices also help in when a company enter into a new

market so as it can attracts more customers (Soin and Collier, 2013).

Price skimming – price skimming refers when the prices of products are very high in order to

recover all expenditures of production and advertising. Many companies’ uses price skimming

methods so as they can achieve profit fast and quickly.

M3

Different planning methods of budgets are helpful in forecasting the financial situation of the company.

Planned budgets are always successful, because they have proper idea of how to spend cash of different

commercial activities, of the business. They gives support to the managers, in order to make another

specific policies for the next financial year, it is also supplying flexible cash flow in the company. It is also

accommodating in pinpoint of shortfalls and increases the instant changes in net cash. It gives a proper

format of sales revenue and expenditure to the business organisation (Cuganesan, Dunford and Palmer,

2012). Budget forecasting is helpful in making long term decision s for the organisation as well as day to

day operations also, by using this company can easily grow its market share in the overall capital market

place.

D3

Planning tools and techniques are able to reduce risk and uncertainties in the capital market. They are

responsible for organisational success and its growth & development. It is able to provide the long term

business polices and strategies, so that any business can compete with new entrants in the corporate market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning tools a makes easier the decision making process of the company, in that mangers can easily

communicate with their employees and take effective and efficient decisions. It identifies all the issues and

challenges in in business organisation and reduce them with the help of internal and external environmental

analysis.

TASK 4

P5 How balanced scorecards can be used to resolve financial issues and developing effective strategies

Balanced scorecard is a performance metrics that is helpful in identify and improves the various

functions of any business organisation in strategic management. It also regulates over their external

outcomes and results. The main role of balanced scorecards is to provide feedback for companies so as they

can develop their performance accordingly (Contrafatto and Burns, 2013). Data collection is critical in order

to providing quantitative outcomes as the information collected is taken by leaders and executives, and recycled

it to make better conclusions for Imda Tech.

Purpose of Balance Scorecards- It is helpful in order to reinforce good behaviour within an organisation.

Balanced scorecards are helpful in analysed these four areas, such as- finance, customers; involve learning &

growth and business process. It used in attained goals, measurements, initiatives and objectives. Along with this,

businesses can identifies those hinder factors of the company that affects its performance and exactness strategic

probabilities track by future scorecards (Van der Steen, 2011). When managers of Imda Tech, are view their

objective so as they are enable to see as the company whole, with the help of balance scorecard. It is also helpful

in add values in business organisations and resolving all financial issues and challenges by implementing

effective strategies and policies as well.

Uses of balanced scorecards in developing strategies-

Balance Scorecards are responsible for what they are trying to accomplishing. It align the day to day

activities so as everyone can uses strategies in their work. It prioritizes products, projects and services in order to

measuring and monitoring the actual progress towards strategic targets. Balanced scorecard work as strategic

management in order to developing strategies and polices to meet organisational objectives and goals. Therefore,

it also helps in translating the vision and mission of business organisations so as managers can better uderstahd

their roles and responsblities or perfrom accordingly.

Balance scorecards also communicate and linked strategies at all level of the organisation and it relates

with individuals and team goals. It also assistive in business planning and forces managers to take participate in

creating financial as well as business plans (Li and et. al., 2012). Along with this, it also provides timely

feedback to managers and employees so as they can improves performance and capabilities that consists with

learning and developing. With the help of balance scorecards, managers can easily develops financial position in

capital market.

M4

communicate with their employees and take effective and efficient decisions. It identifies all the issues and

challenges in in business organisation and reduce them with the help of internal and external environmental

analysis.

TASK 4

P5 How balanced scorecards can be used to resolve financial issues and developing effective strategies

Balanced scorecard is a performance metrics that is helpful in identify and improves the various

functions of any business organisation in strategic management. It also regulates over their external

outcomes and results. The main role of balanced scorecards is to provide feedback for companies so as they

can develop their performance accordingly (Contrafatto and Burns, 2013). Data collection is critical in order

to providing quantitative outcomes as the information collected is taken by leaders and executives, and recycled

it to make better conclusions for Imda Tech.

Purpose of Balance Scorecards- It is helpful in order to reinforce good behaviour within an organisation.

Balanced scorecards are helpful in analysed these four areas, such as- finance, customers; involve learning &

growth and business process. It used in attained goals, measurements, initiatives and objectives. Along with this,

businesses can identifies those hinder factors of the company that affects its performance and exactness strategic

probabilities track by future scorecards (Van der Steen, 2011). When managers of Imda Tech, are view their

objective so as they are enable to see as the company whole, with the help of balance scorecard. It is also helpful

in add values in business organisations and resolving all financial issues and challenges by implementing

effective strategies and policies as well.

Uses of balanced scorecards in developing strategies-

Balance Scorecards are responsible for what they are trying to accomplishing. It align the day to day

activities so as everyone can uses strategies in their work. It prioritizes products, projects and services in order to

measuring and monitoring the actual progress towards strategic targets. Balanced scorecard work as strategic

management in order to developing strategies and polices to meet organisational objectives and goals. Therefore,

it also helps in translating the vision and mission of business organisations so as managers can better uderstahd

their roles and responsblities or perfrom accordingly.

Balance scorecards also communicate and linked strategies at all level of the organisation and it relates

with individuals and team goals. It also assistive in business planning and forces managers to take participate in

creating financial as well as business plans (Li and et. al., 2012). Along with this, it also provides timely

feedback to managers and employees so as they can improves performance and capabilities that consists with

learning and developing. With the help of balance scorecards, managers can easily develops financial position in

capital market.

M4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting is helpful in resolving the financial problems of the company; it gives

proper suggestions and guidance in order to making decisions and strategies. It is the combination of finance

and management, so that if management accounting works effectively, the problems regarding finance are

automatically solves. It provides the better suggestions to the managers; by using them they can solve their

day to day operations as well as their long term activities. It is the process of reducing risk and generating

high profit in capital market (Pitkänen and Lukka, 2011). Management accounting makes business capable

to compete with their external competitors and also reduces the chances of internal conflict.

CONCLUSION

From the above mentioned file it has been concluded that management accounting is the essential

tool for business. It helps in short term and day to day to business decisions so as managers can easily take

profitable opportunities. Financial accounting is helpful in to providing financial information to managers

where-as management accounting is helpful in providing financial as well as non-financial information to

managers. It is very important in reduces expense, improves cash flow and better business decisions.

Budgets are also the important part of management accounting in order to provide better financial statements

and reports. Operations budgets and financial budgets are the two types of budgets. There are management

accounting systems, that are as follow;- cost accounting system, job costing system, inventory management

system and pricing optimising systems. Due to this, Pricing strategies helps in determining the prices of

products and services so as managers can easily achieve target market.

REFERENCES

Books and Journal

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Ward, K., 2012. Strategic management accounting. Routledge.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting: explaining practice in

leading German companies. Australian Accounting Review. 21(1). pp.80-98.

proper suggestions and guidance in order to making decisions and strategies. It is the combination of finance

and management, so that if management accounting works effectively, the problems regarding finance are

automatically solves. It provides the better suggestions to the managers; by using them they can solve their

day to day operations as well as their long term activities. It is the process of reducing risk and generating

high profit in capital market (Pitkänen and Lukka, 2011). Management accounting makes business capable

to compete with their external competitors and also reduces the chances of internal conflict.

CONCLUSION

From the above mentioned file it has been concluded that management accounting is the essential

tool for business. It helps in short term and day to day to business decisions so as managers can easily take

profitable opportunities. Financial accounting is helpful in to providing financial information to managers

where-as management accounting is helpful in providing financial as well as non-financial information to

managers. It is very important in reduces expense, improves cash flow and better business decisions.

Budgets are also the important part of management accounting in order to provide better financial statements

and reports. Operations budgets and financial budgets are the two types of budgets. There are management

accounting systems, that are as follow;- cost accounting system, job costing system, inventory management

system and pricing optimising systems. Due to this, Pricing strategies helps in determining the prices of

products and services so as managers can easily achieve target market.

REFERENCES

Books and Journal

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Ward, K., 2012. Strategic management accounting. Routledge.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting: explaining practice in

leading German companies. Australian Accounting Review. 21(1). pp.80-98.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A research

note. International Journal of Accounting Information Systems, 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society. 38(1). pp.50-71.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability Journal.

24(1). pp.93-128.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change and

management accounting: A processual view. Management Accounting Research. 24(4). pp.349-

365.

Van der Steen, M., 2011. The emergence and change of management accounting routines. Accounting,

Auditing & Accountability Journal. 24(4). pp.502-547.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on lean

implementation. International Journal of Technology Management. 57(1/2/3). pp.33-48

Pitkänen, H. and Lukka, K., 2011. Three dimensions of formal and informal feedback in management

accounting. Management Accounting Research. 22(2). pp.125-137.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy practices

within a public sector agency. Management Accounting Research. 23(4). pp.245-260.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Online

The Differences Between Financial Accounting & Management Accounting. 2017. [Online]. Available

through: < http://smallbusiness.chron.com/differences-between-financial-accounting-management-

accounting-3985.html>. [Accessed on 23rd April 2017].

Budget : Meaning, Features and Its Types | Accounting. 2016. [Online]. Available through: <

http://www.yourarticlelibrary.com/accounting/budget-accounting/budget-meaning-features-and-its-

types-accounting/65284/>. [Accessed on 23rd April 2017].

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A research

note. International Journal of Accounting Information Systems, 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society. 38(1). pp.50-71.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability Journal.

24(1). pp.93-128.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change and

management accounting: A processual view. Management Accounting Research. 24(4). pp.349-

365.

Van der Steen, M., 2011. The emergence and change of management accounting routines. Accounting,

Auditing & Accountability Journal. 24(4). pp.502-547.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on lean

implementation. International Journal of Technology Management. 57(1/2/3). pp.33-48

Pitkänen, H. and Lukka, K., 2011. Three dimensions of formal and informal feedback in management

accounting. Management Accounting Research. 22(2). pp.125-137.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy practices

within a public sector agency. Management Accounting Research. 23(4). pp.245-260.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Online

The Differences Between Financial Accounting & Management Accounting. 2017. [Online]. Available

through: < http://smallbusiness.chron.com/differences-between-financial-accounting-management-

accounting-3985.html>. [Accessed on 23rd April 2017].

Budget : Meaning, Features and Its Types | Accounting. 2016. [Online]. Available through: <

http://www.yourarticlelibrary.com/accounting/budget-accounting/budget-meaning-features-and-its-

types-accounting/65284/>. [Accessed on 23rd April 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.