Management Accounting Report: Taj Stores, UK - Costing and Planning

VerifiedAdded on 2020/06/06

|18

|5680

|41

Report

AI Summary

This report provides a detailed analysis of management accounting principles and practices, focusing on their application within a UK-based grocery store, Taj Stores. The report begins with an introduction to management accounting and its significance for businesses, followed by an examination of various management accounting systems, including inventory management and cost accounting. It delves into different methods of management accounting reporting, such as inventory control and budget reporting. A key section compares and contrasts marginal and absorption costing, highlighting their implications for income statements. The report further explores the merits and demerits of planning tools used in budgetary control and concludes with a discussion on adopting management accounting systems to address financial challenges. References are included to support the analysis.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Various management accounting system...............................................................................1

P2 Various method for management accounting reporting.........................................................3

TASK 2............................................................................................................................................4

P3 Income statement and difference between marginal and absorption costing.........................4

TASK 3............................................................................................................................................8

P4 Merit and demerit of many kind of planning tools which is used in budgetary control........8

TASK 4 .........................................................................................................................................11

P5 Adopting management accounting system for responding financial troubles.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Various management accounting system...............................................................................1

P2 Various method for management accounting reporting.........................................................3

TASK 2............................................................................................................................................4

P3 Income statement and difference between marginal and absorption costing.........................4

TASK 3............................................................................................................................................8

P4 Merit and demerit of many kind of planning tools which is used in budgetary control........8

TASK 4 .........................................................................................................................................11

P5 Adopting management accounting system for responding financial troubles.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is fundamental for each and every kind of company as with

assistance of this manager will get adequate results which are beneficial for them. It is

fundamental for company to combine their administration with procedure of accounting;

therefore, they will make their working operations more viable and in addition control their

expenditures (Ahmad and Mohamed Zabri, 2012). Along with this, by manage entire things in an

adequate way; employer will decrease their risk of business. Present report is based on Taj Stores

which is established in UK. They are providing variety of grocery goods to their clients as per

their requirements. In this report, there is description about various management accounting

system. This assignment is going to describe difference amongst marginal and absorption

costing. There are various methods which can be utilized by manager to take an adequate

decision for firm. As a result, entire work will fulfilled within specific time span.

TASK 1

P1 Various management accounting system

In previous era, it was not difficult for a person to begin their own business as he has to

identify a producer who will develop goods and then, he will sell it into market. Time goes and

this will become more tricky for an individual to start their own firm as lots of use of new

methods and techniques. As per current market trend it is required for companies to understand

importance which are associated with management accounting; thus, they can easily manage

entire operational exercises in an effective manner. This procedure is just like where manager try

to find out and examine financial as well as non financial data. Therefore, firm will use resources

adequately which is advantageous for them. With assistance of this, enterprise will manage their

fund properly (Aminbakhsh, Gunduz and Sonmez, 2013). By avoiding or resolve disputes an

association will easily attain desired goals within time.

Costing is much significance part which is associated with management accounting. This

will aid to reduce overall manufacturing cost. It can affect profits of company directly. By taking

decisions timely, firm will accomplish their targets within provided period of time. To improve

interaction amongst various levels manager will take aid of system of management accounting.

With assistance of this manager will easily understand strategies which are developed by

government. External environment will provide impact to firm either in a positive or negative

1

Management accounting is fundamental for each and every kind of company as with

assistance of this manager will get adequate results which are beneficial for them. It is

fundamental for company to combine their administration with procedure of accounting;

therefore, they will make their working operations more viable and in addition control their

expenditures (Ahmad and Mohamed Zabri, 2012). Along with this, by manage entire things in an

adequate way; employer will decrease their risk of business. Present report is based on Taj Stores

which is established in UK. They are providing variety of grocery goods to their clients as per

their requirements. In this report, there is description about various management accounting

system. This assignment is going to describe difference amongst marginal and absorption

costing. There are various methods which can be utilized by manager to take an adequate

decision for firm. As a result, entire work will fulfilled within specific time span.

TASK 1

P1 Various management accounting system

In previous era, it was not difficult for a person to begin their own business as he has to

identify a producer who will develop goods and then, he will sell it into market. Time goes and

this will become more tricky for an individual to start their own firm as lots of use of new

methods and techniques. As per current market trend it is required for companies to understand

importance which are associated with management accounting; thus, they can easily manage

entire operational exercises in an effective manner. This procedure is just like where manager try

to find out and examine financial as well as non financial data. Therefore, firm will use resources

adequately which is advantageous for them. With assistance of this, enterprise will manage their

fund properly (Aminbakhsh, Gunduz and Sonmez, 2013). By avoiding or resolve disputes an

association will easily attain desired goals within time.

Costing is much significance part which is associated with management accounting. This

will aid to reduce overall manufacturing cost. It can affect profits of company directly. By taking

decisions timely, firm will accomplish their targets within provided period of time. To improve

interaction amongst various levels manager will take aid of system of management accounting.

With assistance of this manager will easily understand strategies which are developed by

government. External environment will provide impact to firm either in a positive or negative

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manner. For evaluation of data and information in an adequate manner, it is required for superior

to consider extrinsic conditions. It is must for employer to manage cash; so that, they will ignore

their short term problems because this can affect their targets and goals (Burritt, Schaltegger and

Zvezdov, 2011).

Instead of many advantages, some disadvantages are associated with management

accounting. Decisions of various tools will always depend on cost and financial accounts. An

inappropriate judgement will cater adverse affect on firm. It is not easy for small firms to use

accounting system into their business as it takes high cost. Along with this, it has been

understood that management accounting will useful for management rather than bondholders.

Henceforth, some systems which are linked with it are described as below:

Inventory management system: With assistance of this technique, manager of company

will easily manage their entire inventory in effective manner. This help them to acquire adequate

data and information related to stock. As a result, risk as well as waste will get eliminate from

business. It is not easy for an association to find out appropriate stock which they will keep in

warehouse. If too much products are stored then, this will enhance carrying cost. Thus, they will

keep limited inventory which will aid them to accomplish need of customers.

To keep up profits, it is fundamental for Taj Stores to reduce their waste adequately and

appropriately. Recently, superior maintain their books of accounts with assistance of many

software (Chen, Weikart and Williams, 2014). As a result, entire data and information will get

recorded within limited time span. Instead of this, they will also use other manual techniques

which is less expansive. It is must for manager to keep up records regarding movement of

products.

There is an example in this relation that Tesco is using this technique to manage their

inventory in an effective way. It is much famous retail store who organise their crude material

adequately. This helps them to manage overall demand as well as supply effectively. They are

much able to decrease wastage risk. Organisation maintain inventory records for almost 22 days

which is high as comparison to Taj Stores (They keep up inventory for 6 days only).

Cost accounting system: This aids to improve profits of firm because this structure is

utilized by manager to estimate cost of goods and services. Along with this, with help of it

enterprise will examine their revenues, control cost and in addition they will do valuation of their

2

to consider extrinsic conditions. It is must for employer to manage cash; so that, they will ignore

their short term problems because this can affect their targets and goals (Burritt, Schaltegger and

Zvezdov, 2011).

Instead of many advantages, some disadvantages are associated with management

accounting. Decisions of various tools will always depend on cost and financial accounts. An

inappropriate judgement will cater adverse affect on firm. It is not easy for small firms to use

accounting system into their business as it takes high cost. Along with this, it has been

understood that management accounting will useful for management rather than bondholders.

Henceforth, some systems which are linked with it are described as below:

Inventory management system: With assistance of this technique, manager of company

will easily manage their entire inventory in effective manner. This help them to acquire adequate

data and information related to stock. As a result, risk as well as waste will get eliminate from

business. It is not easy for an association to find out appropriate stock which they will keep in

warehouse. If too much products are stored then, this will enhance carrying cost. Thus, they will

keep limited inventory which will aid them to accomplish need of customers.

To keep up profits, it is fundamental for Taj Stores to reduce their waste adequately and

appropriately. Recently, superior maintain their books of accounts with assistance of many

software (Chen, Weikart and Williams, 2014). As a result, entire data and information will get

recorded within limited time span. Instead of this, they will also use other manual techniques

which is less expansive. It is must for manager to keep up records regarding movement of

products.

There is an example in this relation that Tesco is using this technique to manage their

inventory in an effective way. It is much famous retail store who organise their crude material

adequately. This helps them to manage overall demand as well as supply effectively. They are

much able to decrease wastage risk. Organisation maintain inventory records for almost 22 days

which is high as comparison to Taj Stores (They keep up inventory for 6 days only).

Cost accounting system: This aids to improve profits of firm because this structure is

utilized by manager to estimate cost of goods and services. Along with this, with help of it

enterprise will examine their revenues, control cost and in addition they will do valuation of their

2

stock. It is not much easy to use this tool; so that, administrative division needs use it effectively

(Cokins, 2013).

This methodology will assist manager to reduce their manufacturing cost. As a result,

organisation will attain success as well as improvement because cost reduction leads to

maximisation of profits. Thus, it is necessary for enterprise to manage overall records in an

adequate and appropriate manner.

In context of Taj Stores, they implement this tool of accounting systems as it assists them

to improve their profits and productivity. Therefore, it is fundamental for employer to do their

task effectively so that they can easily evaluate entire expenditure which will occurred into their

project.

In Tesco, there is implementation of this method is done appropriately because working

abilities of superior is much adequate. As a result, they will easily improve their revenues and

reputation at marketplace (Delafrooz and Paim, 2011).

Job Costing: With assistance of this, employer can easily maintain cost of each job in an

adequate manner. As a result, profits associated with every occupation can be easily identified.

Therefore, by utilization of this technique, superior can find out the revenue which will be

occupy by them with aid of a single job. It is required for company to use this methodology into

their firm.

As indicated by manager of Tesco, they estimate their job costing which is related to

manufacturing is almost 41% but real cost find out at 33% which is much near. Rather than this,

Taj Stores estimates it at 49%. It is not easy for small firms to enhance their cost of

manufacturing; therefore, their actual cost is almost 16% which is much less. Thus, it is required

for superior to concentrate on it; as a result, they will easily improve their revenues (Ekbatani

and Sangeladji, 2011).

P2 Various method for management accounting reporting

It is required for superior to develop many sorts of report; so that, they can easily present

their plan to top management. Some tools and stated as beneath:

Inventory control reporting: With assistance of this, manager can easily formulate as

well as maintain adequate records which is associated with stock. Therefore, they can enhance

their revenues and will improve circumstances to acquire opportunities from marketplace. Many

kind of problems will develop if there is overstocking as well as under stocking of goods. Like,

3

(Cokins, 2013).

This methodology will assist manager to reduce their manufacturing cost. As a result,

organisation will attain success as well as improvement because cost reduction leads to

maximisation of profits. Thus, it is necessary for enterprise to manage overall records in an

adequate and appropriate manner.

In context of Taj Stores, they implement this tool of accounting systems as it assists them

to improve their profits and productivity. Therefore, it is fundamental for employer to do their

task effectively so that they can easily evaluate entire expenditure which will occurred into their

project.

In Tesco, there is implementation of this method is done appropriately because working

abilities of superior is much adequate. As a result, they will easily improve their revenues and

reputation at marketplace (Delafrooz and Paim, 2011).

Job Costing: With assistance of this, employer can easily maintain cost of each job in an

adequate manner. As a result, profits associated with every occupation can be easily identified.

Therefore, by utilization of this technique, superior can find out the revenue which will be

occupy by them with aid of a single job. It is required for company to use this methodology into

their firm.

As indicated by manager of Tesco, they estimate their job costing which is related to

manufacturing is almost 41% but real cost find out at 33% which is much near. Rather than this,

Taj Stores estimates it at 49%. It is not easy for small firms to enhance their cost of

manufacturing; therefore, their actual cost is almost 16% which is much less. Thus, it is required

for superior to concentrate on it; as a result, they will easily improve their revenues (Ekbatani

and Sangeladji, 2011).

P2 Various method for management accounting reporting

It is required for superior to develop many sorts of report; so that, they can easily present

their plan to top management. Some tools and stated as beneath:

Inventory control reporting: With assistance of this, manager can easily formulate as

well as maintain adequate records which is associated with stock. Therefore, they can enhance

their revenues and will improve circumstances to acquire opportunities from marketplace. Many

kind of problems will develop if there is overstocking as well as under stocking of goods. Like,

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation will not accomplish requirements of clients on time, if they do not have adequate

inventory.

Main purpose is to find out problems which is related to stock administration. Taj Stores

is doing their work at a small scale; therefore, it is not possible for them to stock maximum

material with them as it takes lots of cost which can not be bear by them (Foster, Hart and Lewis,

2011). Apart from this, under stocking will leads to lose their customers and they will switch to

another store for accomplishment of their requirements and demands. Therefore, to resolve this

sort of troubles they have to use techniques of management accounting. Like an example:

Economic order quantity, with aid of this, it will be easy for an employer to determine adequate

product amount which they have to keep in storage. This will help them diminish their unwanted

cost.

Budget reporting: With aid of an effective budget it is easy for a manager to maintain

their expenditures in an effective manner. Along with this, they will utilize fund adequately.

Instead of this, budget report is developed by superior of firm. It will consist information

regarding how much they will spend on their project. As a result, by maintaining their expenses,

enterprise will easily improve their revenues which is connected with business. For above stated

purpose, it is must for them assign resource to each task appropriately.

Fundamental aim of this report is to record and examine entire expenditures and incomes.

It helps to cover each and every unit; therefore, it is must for superior to formulate it because an

effective budget will help to provide direction to staff members. They will be able to complete

their task within provided fund. As a result, unwanted cost will get reduced and work will fulfil

in an adequate way (Fullerton, Kennedy and Widener, 2014). With assistance of proper spending

plan, association will able to maintain their goodwill at marketplace. Along with this, they will

easily compete their competitors at competitive world.

TASK 2

P3 Income statement and difference between marginal and absorption costing

Costing is consider as a most important part which is associated with management

accounting. With help of this, company can reduce their business cost; therefore, they can easily

improve their profits. In this relation, marginal and absorption costing is mentioned as below:

4

inventory.

Main purpose is to find out problems which is related to stock administration. Taj Stores

is doing their work at a small scale; therefore, it is not possible for them to stock maximum

material with them as it takes lots of cost which can not be bear by them (Foster, Hart and Lewis,

2011). Apart from this, under stocking will leads to lose their customers and they will switch to

another store for accomplishment of their requirements and demands. Therefore, to resolve this

sort of troubles they have to use techniques of management accounting. Like an example:

Economic order quantity, with aid of this, it will be easy for an employer to determine adequate

product amount which they have to keep in storage. This will help them diminish their unwanted

cost.

Budget reporting: With aid of an effective budget it is easy for a manager to maintain

their expenditures in an effective manner. Along with this, they will utilize fund adequately.

Instead of this, budget report is developed by superior of firm. It will consist information

regarding how much they will spend on their project. As a result, by maintaining their expenses,

enterprise will easily improve their revenues which is connected with business. For above stated

purpose, it is must for them assign resource to each task appropriately.

Fundamental aim of this report is to record and examine entire expenditures and incomes.

It helps to cover each and every unit; therefore, it is must for superior to formulate it because an

effective budget will help to provide direction to staff members. They will be able to complete

their task within provided fund. As a result, unwanted cost will get reduced and work will fulfil

in an adequate way (Fullerton, Kennedy and Widener, 2014). With assistance of proper spending

plan, association will able to maintain their goodwill at marketplace. Along with this, they will

easily compete their competitors at competitive world.

TASK 2

P3 Income statement and difference between marginal and absorption costing

Costing is consider as a most important part which is associated with management

accounting. With help of this, company can reduce their business cost; therefore, they can easily

improve their profits. In this relation, marginal and absorption costing is mentioned as below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

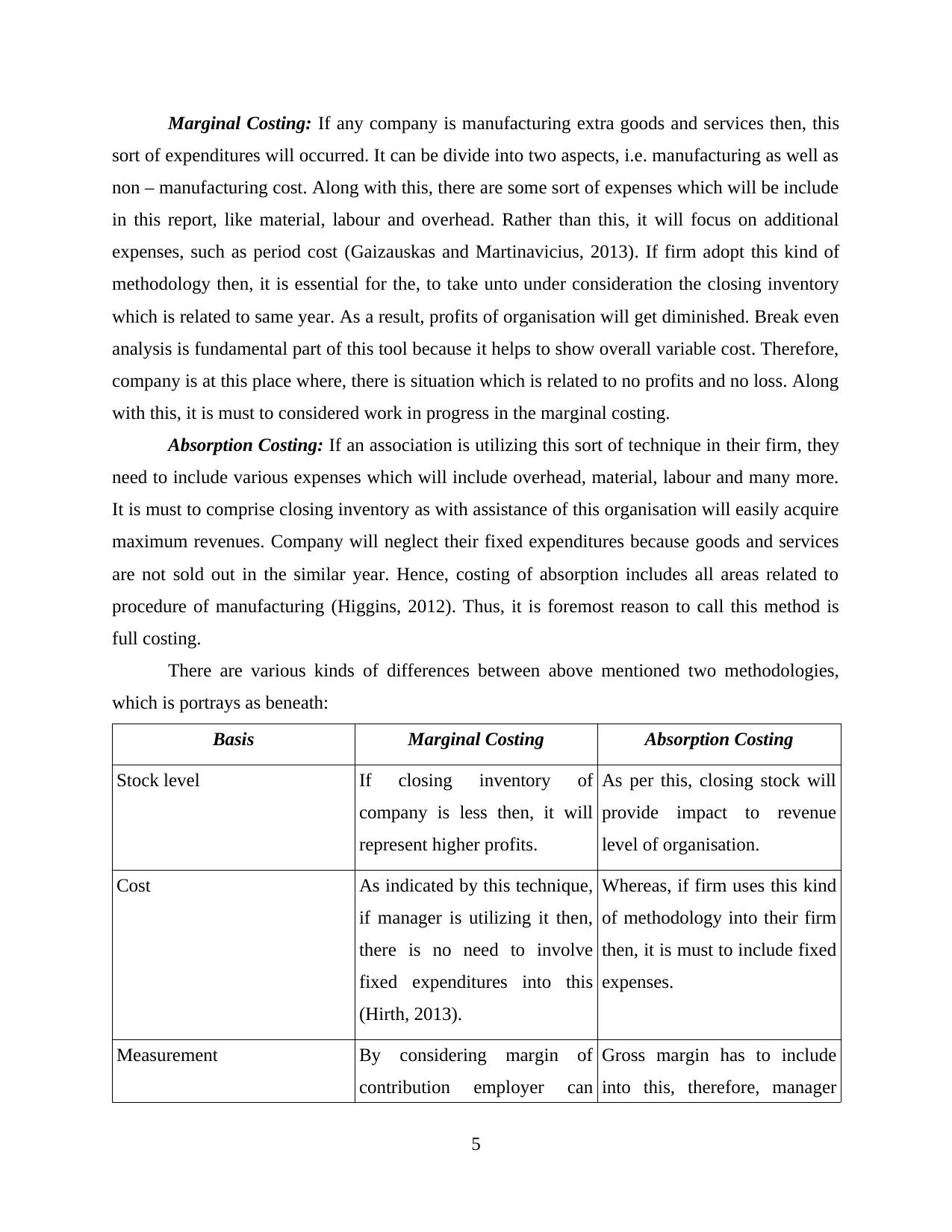

Marginal Costing: If any company is manufacturing extra goods and services then, this

sort of expenditures will occurred. It can be divide into two aspects, i.e. manufacturing as well as

non – manufacturing cost. Along with this, there are some sort of expenses which will be include

in this report, like material, labour and overhead. Rather than this, it will focus on additional

expenses, such as period cost (Gaizauskas and Martinavicius, 2013). If firm adopt this kind of

methodology then, it is essential for the, to take unto under consideration the closing inventory

which is related to same year. As a result, profits of organisation will get diminished. Break even

analysis is fundamental part of this tool because it helps to show overall variable cost. Therefore,

company is at this place where, there is situation which is related to no profits and no loss. Along

with this, it is must to considered work in progress in the marginal costing.

Absorption Costing: If an association is utilizing this sort of technique in their firm, they

need to include various expenses which will include overhead, material, labour and many more.

It is must to comprise closing inventory as with assistance of this organisation will easily acquire

maximum revenues. Company will neglect their fixed expenditures because goods and services

are not sold out in the similar year. Hence, costing of absorption includes all areas related to

procedure of manufacturing (Higgins, 2012). Thus, it is foremost reason to call this method is

full costing.

There are various kinds of differences between above mentioned two methodologies,

which is portrays as beneath:

Basis Marginal Costing Absorption Costing

Stock level If closing inventory of

company is less then, it will

represent higher profits.

As per this, closing stock will

provide impact to revenue

level of organisation.

Cost As indicated by this technique,

if manager is utilizing it then,

there is no need to involve

fixed expenditures into this

(Hirth, 2013).

Whereas, if firm uses this kind

of methodology into their firm

then, it is must to include fixed

expenses.

Measurement By considering margin of

contribution employer can

Gross margin has to include

into this, therefore, manager

5

sort of expenditures will occurred. It can be divide into two aspects, i.e. manufacturing as well as

non – manufacturing cost. Along with this, there are some sort of expenses which will be include

in this report, like material, labour and overhead. Rather than this, it will focus on additional

expenses, such as period cost (Gaizauskas and Martinavicius, 2013). If firm adopt this kind of

methodology then, it is essential for the, to take unto under consideration the closing inventory

which is related to same year. As a result, profits of organisation will get diminished. Break even

analysis is fundamental part of this tool because it helps to show overall variable cost. Therefore,

company is at this place where, there is situation which is related to no profits and no loss. Along

with this, it is must to considered work in progress in the marginal costing.

Absorption Costing: If an association is utilizing this sort of technique in their firm, they

need to include various expenses which will include overhead, material, labour and many more.

It is must to comprise closing inventory as with assistance of this organisation will easily acquire

maximum revenues. Company will neglect their fixed expenditures because goods and services

are not sold out in the similar year. Hence, costing of absorption includes all areas related to

procedure of manufacturing (Higgins, 2012). Thus, it is foremost reason to call this method is

full costing.

There are various kinds of differences between above mentioned two methodologies,

which is portrays as beneath:

Basis Marginal Costing Absorption Costing

Stock level If closing inventory of

company is less then, it will

represent higher profits.

As per this, closing stock will

provide impact to revenue

level of organisation.

Cost As indicated by this technique,

if manager is utilizing it then,

there is no need to involve

fixed expenditures into this

(Hirth, 2013).

Whereas, if firm uses this kind

of methodology into their firm

then, it is must to include fixed

expenses.

Measurement By considering margin of

contribution employer can

Gross margin has to include

into this, therefore, manager

5

easily examine revenues, but is

must to remove applied

expenses from this.

will evaluate net profits of

firm. Additionally, it is

required to comprise applied

cost at the time of using this

methodology.

Profitability Individual level of sales will

help to maximise revenues of

enterprise.

Rather than this, if company is

using this tool then, by

utilizing sales at individual

level there profits will get

reduced (Lambert and

Sponem, 2012).

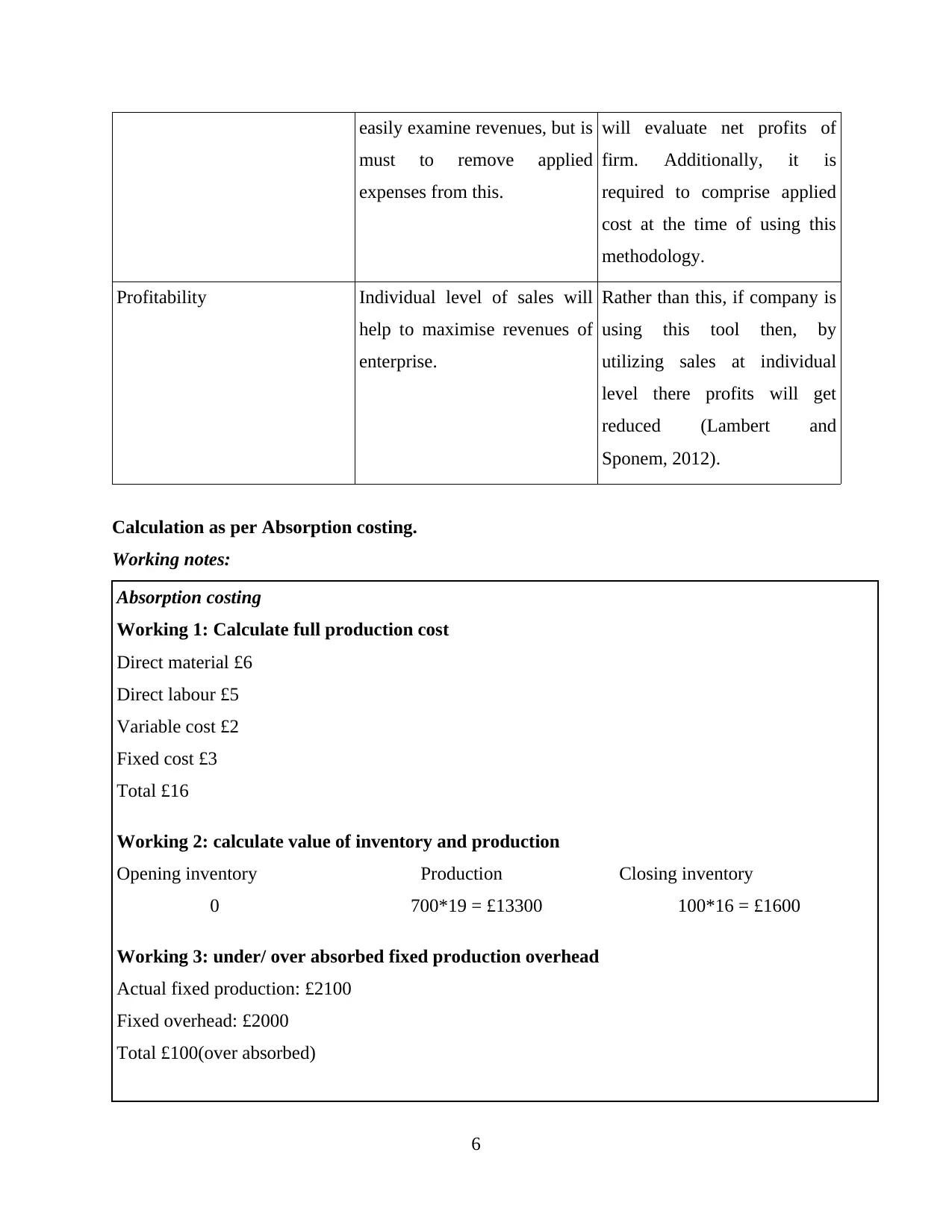

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

6

must to remove applied

expenses from this.

will evaluate net profits of

firm. Additionally, it is

required to comprise applied

cost at the time of using this

methodology.

Profitability Individual level of sales will

help to maximise revenues of

enterprise.

Rather than this, if company is

using this tool then, by

utilizing sales at individual

level there profits will get

reduced (Lambert and

Sponem, 2012).

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Administration Cost: In this budgeted cost is £800 and Actual cost is £700.

Production cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

7

Production cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

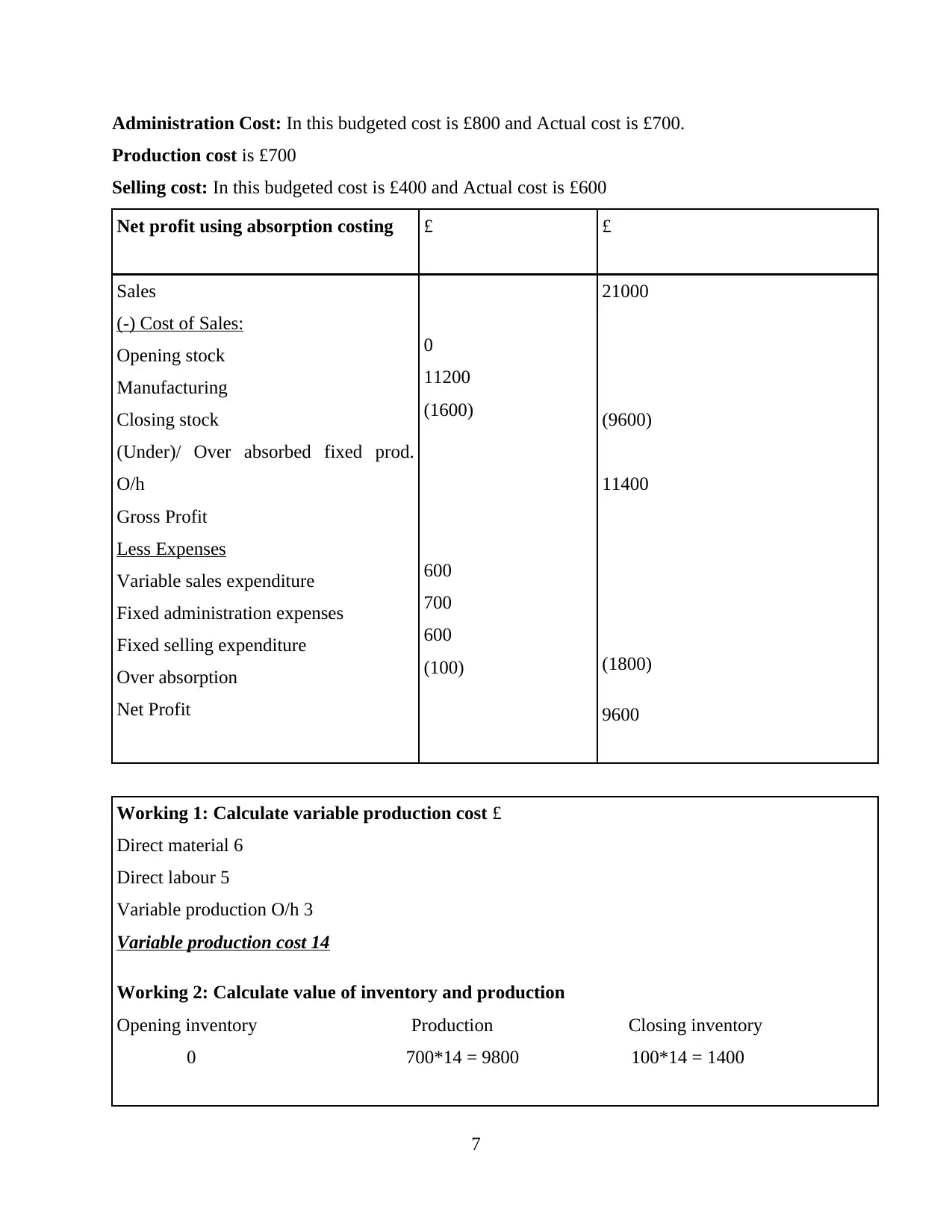

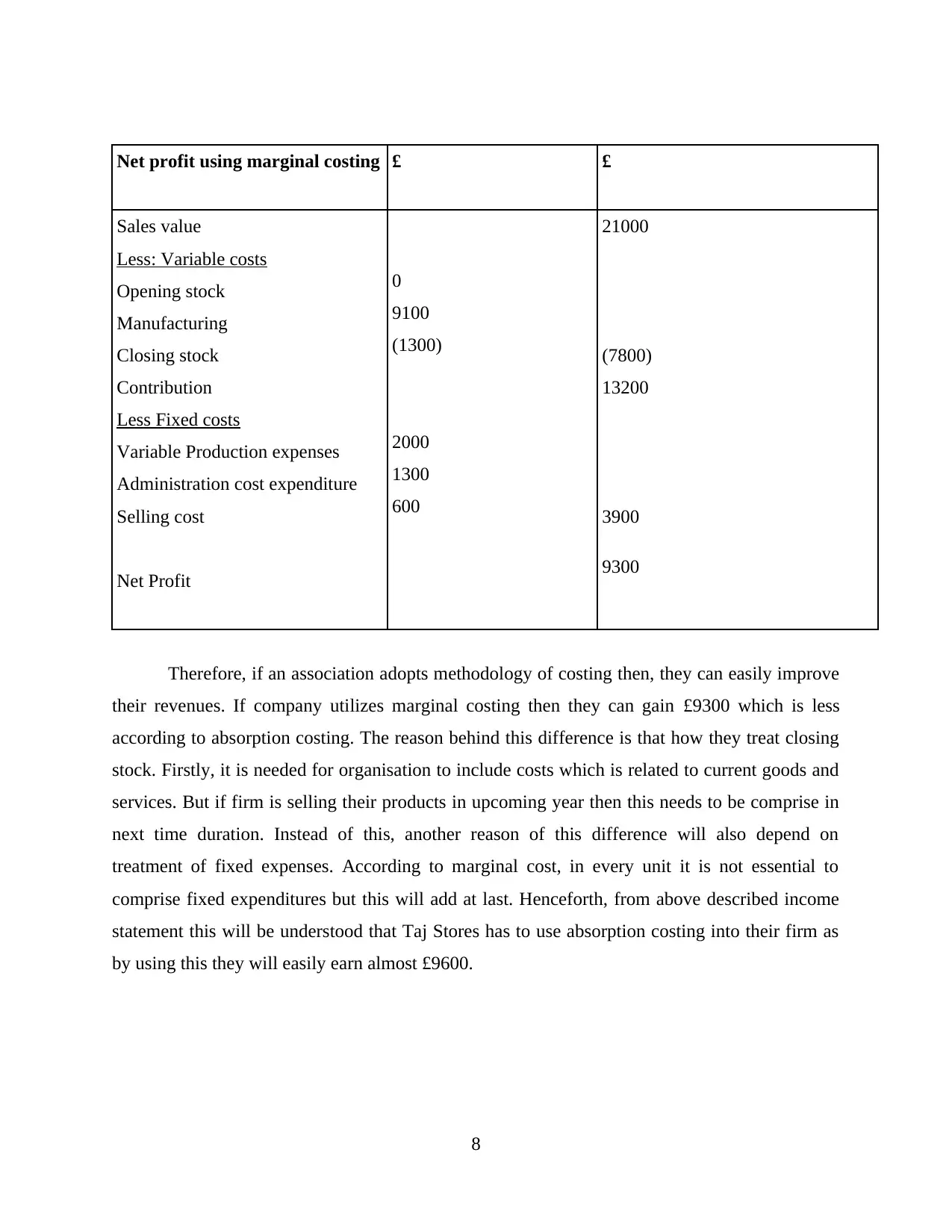

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

Therefore, if an association adopts methodology of costing then, they can easily improve

their revenues. If company utilizes marginal costing then they can gain £9300 which is less

according to absorption costing. The reason behind this difference is that how they treat closing

stock. Firstly, it is needed for organisation to include costs which is related to current goods and

services. But if firm is selling their products in upcoming year then this needs to be comprise in

next time duration. Instead of this, another reason of this difference will also depend on

treatment of fixed expenses. According to marginal cost, in every unit it is not essential to

comprise fixed expenditures but this will add at last. Henceforth, from above described income

statement this will be understood that Taj Stores has to use absorption costing into their firm as

by using this they will easily earn almost £9600.

8

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

Therefore, if an association adopts methodology of costing then, they can easily improve

their revenues. If company utilizes marginal costing then they can gain £9300 which is less

according to absorption costing. The reason behind this difference is that how they treat closing

stock. Firstly, it is needed for organisation to include costs which is related to current goods and

services. But if firm is selling their products in upcoming year then this needs to be comprise in

next time duration. Instead of this, another reason of this difference will also depend on

treatment of fixed expenses. According to marginal cost, in every unit it is not essential to

comprise fixed expenditures but this will add at last. Henceforth, from above described income

statement this will be understood that Taj Stores has to use absorption costing into their firm as

by using this they will easily earn almost £9600.

8

TASK 3

P4 Merit and demerit of many kind of planning tools which is used in budgetary control

By using budgetary control organisation will get stable because it is associated with a

specific time duration, like for one year (Langevin and Mendoza, 2013). As a result, various

confusions will get eliminated which will be in company. With assistance of an adequate plan of

budget manager will manage entire operational activities and in addition they will move their

entire work in a right direction. Rather than this, employer will also baffled due to distinguish

policies of their contenders. Furthermore, there strategy will assist them to do their work in

correct manner which will help them to attain their coveted goals and objectives effectively. This

will be of both kinds, one is short term and another is long term. It is required for persons to

maintain open conversation into company; therefore, they can easily share their views and

opinions with each other. Along with this, entire problems will sort out within specific time span.

To achieve best and effective results, it is mandatory for superior to develop proper coordination

between each and every division (Lavia López and Hiebl, 2014).

Instead of various pros there are many cons which are associated with budgetary control

and this can never ignored by manager of enterprise. Manager prepares budget and it is on

estimation basis which diminishes its reliableness. Future is uncertain and environment is

dynamic in nature; therefore, it is not must for employer to waste their entire time on budget

formulation. It is needed for management to take fast decisions for association. If there is no

flexibility in their budget then this will create major issue. As a result, many troubles will face by

superior to implement it into their working procedure (What is Budgetary control?, 2017).

Hence, several are popular methods which are connected with planning and will be used

by employer; as a result, they can improve overall performance of firm in an effective way. It

will be discussed as beneath:

Master Budget: If superior is going to do planning related to this then, it is required for

them consider an organisation as a particular unit. Each and every unit and in addition areas are

going to comprise in it. To formulate master budget, manager need to consider entire data as well

as information which is associated with their business. It is must for superior to provide duties to

all workers; therefore, they can do estimation more accurately. Apart from this, in this tool,

employer has to estimate entire financial gain as well as expenditure because this will be useful

for them proficiently (Maiyaki, 2011).

9

P4 Merit and demerit of many kind of planning tools which is used in budgetary control

By using budgetary control organisation will get stable because it is associated with a

specific time duration, like for one year (Langevin and Mendoza, 2013). As a result, various

confusions will get eliminated which will be in company. With assistance of an adequate plan of

budget manager will manage entire operational activities and in addition they will move their

entire work in a right direction. Rather than this, employer will also baffled due to distinguish

policies of their contenders. Furthermore, there strategy will assist them to do their work in

correct manner which will help them to attain their coveted goals and objectives effectively. This

will be of both kinds, one is short term and another is long term. It is required for persons to

maintain open conversation into company; therefore, they can easily share their views and

opinions with each other. Along with this, entire problems will sort out within specific time span.

To achieve best and effective results, it is mandatory for superior to develop proper coordination

between each and every division (Lavia López and Hiebl, 2014).

Instead of various pros there are many cons which are associated with budgetary control

and this can never ignored by manager of enterprise. Manager prepares budget and it is on

estimation basis which diminishes its reliableness. Future is uncertain and environment is

dynamic in nature; therefore, it is not must for employer to waste their entire time on budget

formulation. It is needed for management to take fast decisions for association. If there is no

flexibility in their budget then this will create major issue. As a result, many troubles will face by

superior to implement it into their working procedure (What is Budgetary control?, 2017).

Hence, several are popular methods which are connected with planning and will be used

by employer; as a result, they can improve overall performance of firm in an effective way. It

will be discussed as beneath:

Master Budget: If superior is going to do planning related to this then, it is required for

them consider an organisation as a particular unit. Each and every unit and in addition areas are

going to comprise in it. To formulate master budget, manager need to consider entire data as well

as information which is associated with their business. It is must for superior to provide duties to

all workers; therefore, they can do estimation more accurately. Apart from this, in this tool,

employer has to estimate entire financial gain as well as expenditure because this will be useful

for them proficiently (Maiyaki, 2011).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.