Management Accounting Report: Analysis for Nelson Hotel, UK (Finance)

VerifiedAdded on 2020/06/05

|19

|3738

|65

Report

AI Summary

This report, prepared for Nelson Hotel, delves into the intricacies of management accounting, offering a comprehensive overview of its systems and techniques. The report begins by defining management accounting and its significance, particularly within a medium-sized enterprise like Nelson Hotel, which is based in the UK. It outlines various types of management accounting systems, including cost accounting, inventory management, and price optimization models. The report then explores different management accounting reporting methods, such as cost reports, budget reports, job cost reports, performance reports, and inventory reports. Furthermore, the report applies cost analysis techniques, specifically absorption costing and marginal costing, to calculate costs and interpret findings to enhance profitability. Finally, the report examines planning tools used in management accounting, including financial control, operations management, budgetary control, quality control, and inventory control, emphasizing their advantages and disadvantages in controlling budgets and achieving organizational goals. The report provides a detailed analysis of management accounting concepts and their practical application within a business context.

MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Introduction

The process of management accounting enables an organization to prepare reports which gives

accurate and timely financial information to managers who are associated with short and long

term decisions. It also enables an organization to purse goal by measuring, communicating and

analyzing information (Agrawal and Cooper, 2017). Besides, organization carrying out proper

management helps in building positive variances and handles negative ones. The assignment will

be carried out on two identical scenarios. The scenario 1 will be presenting a report to general

manager from the management accounting officer. The other one will be presenting a report for

analyzing the issues that are related with accounting information function including budgetary

control and budgeting.

TASK 1:

LO1: To understand management accounting system

P1: Management accounting and different types of management accounting system

From: Management Accounting Officer,

To: General Manager of Nelson Hotel,

Sub: Management Accounting System.

Introduction: The particular task will give an understanding of management accounting and its

importance within an organization. The present assignment will be carried out by acting as

Management Accounting Officer who will be presenting a report to general management of

Nelson Hotel UK a medium sized enterprise. The company is not having more than 50

employees and the net turnover is not exceeding £500,000.

Management Accounting System: Baker et al. (2017) defined management accounting as a

system that collects financial data from an organization including sales data, changes in cost of

raw materials and inventory in order to change the information to analyze a report.

3

The process of management accounting enables an organization to prepare reports which gives

accurate and timely financial information to managers who are associated with short and long

term decisions. It also enables an organization to purse goal by measuring, communicating and

analyzing information (Agrawal and Cooper, 2017). Besides, organization carrying out proper

management helps in building positive variances and handles negative ones. The assignment will

be carried out on two identical scenarios. The scenario 1 will be presenting a report to general

manager from the management accounting officer. The other one will be presenting a report for

analyzing the issues that are related with accounting information function including budgetary

control and budgeting.

TASK 1:

LO1: To understand management accounting system

P1: Management accounting and different types of management accounting system

From: Management Accounting Officer,

To: General Manager of Nelson Hotel,

Sub: Management Accounting System.

Introduction: The particular task will give an understanding of management accounting and its

importance within an organization. The present assignment will be carried out by acting as

Management Accounting Officer who will be presenting a report to general management of

Nelson Hotel UK a medium sized enterprise. The company is not having more than 50

employees and the net turnover is not exceeding £500,000.

Management Accounting System: Baker et al. (2017) defined management accounting as a

system that collects financial data from an organization including sales data, changes in cost of

raw materials and inventory in order to change the information to analyze a report.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Types of Management accounting system:

Figure 1: Types of Management accounting system

(Source: Self Created)

Cost accounting system: This is also called product costing system which is used within business

enterprise for estimating cost of products in order to analyze organization profitability. For

example, Nelson hotel need to know which services will help in earning more profit and which

are not and it can be done by estimating correct price of products. Kim et al. (2013) added that

cost allocation is a technique of cost accounting system that helps in incorporating departments

and several services given by the hotel enterprise. For example, cost of furniture, food items and

many more. Besides, job order costing is another technique that takes cost of manufacturing for

each department of the organization. Such process is appropriate for the business enterprise

which is associated with production of distinctive products. Hou et al. (2017) stated that, activity

based costing is associated with calculation of several activities that is carried out within an

organization.

Inventory Management Systems: It is an ongoing progression used for planning and tracking

inventory activities. The inventory items are always tagged with a bar code number to make it

identical from one another. In case of hospitality industry the same happens where the inventory

4

Figure 1: Types of Management accounting system

(Source: Self Created)

Cost accounting system: This is also called product costing system which is used within business

enterprise for estimating cost of products in order to analyze organization profitability. For

example, Nelson hotel need to know which services will help in earning more profit and which

are not and it can be done by estimating correct price of products. Kim et al. (2013) added that

cost allocation is a technique of cost accounting system that helps in incorporating departments

and several services given by the hotel enterprise. For example, cost of furniture, food items and

many more. Besides, job order costing is another technique that takes cost of manufacturing for

each department of the organization. Such process is appropriate for the business enterprise

which is associated with production of distinctive products. Hou et al. (2017) stated that, activity

based costing is associated with calculation of several activities that is carried out within an

organization.

Inventory Management Systems: It is an ongoing progression used for planning and tracking

inventory activities. The inventory items are always tagged with a bar code number to make it

identical from one another. In case of hospitality industry the same happens where the inventory

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

items are brought to warehouse and the items are scanned by bar code. Hence, it becomes easier

for the business enterprise to figure out the products that are bought to the organization. With the

help of this system the business enterprise are able to carry out their operation in a systematic

manner. It also helps the business enterprise to stock goods in appropriate manner without any

kind of misplacement.

Price Optimization Models: Christensen et al. (2013) stated that price optimization model is a

mathematical process used in business enterprise to analyze the variation of changes in price

levels. Later the information is estimated for creating costs and inventory level with an

appropriate price cost. Such system can be used for implementing pricing and segments to target

right cost in order to attract right customers.

Job costing systems: It enables in collecting information and data that is associated with the

production or various range of services within the business enterprise. For example, Nelson hotel

gives various ranges of services including food and lodging where job costing system enables in

collecting data of each service.

M1

Benefits of management accounting system

Cost accounting

Advantages Disadvantages

Cost reduction

Helps in eliminating waste, loss and

inefficiencies

Assists in price fixation

It leads the issue of under and over-

absorption of overhead

It presents suitable view of cost only

when full capacity is utilized.

Job costing

Advantages Disadvantages

Helps in making estimation about cost

on the basis of past records

Requires clerical work

Highly expensive

5

for the business enterprise to figure out the products that are bought to the organization. With the

help of this system the business enterprise are able to carry out their operation in a systematic

manner. It also helps the business enterprise to stock goods in appropriate manner without any

kind of misplacement.

Price Optimization Models: Christensen et al. (2013) stated that price optimization model is a

mathematical process used in business enterprise to analyze the variation of changes in price

levels. Later the information is estimated for creating costs and inventory level with an

appropriate price cost. Such system can be used for implementing pricing and segments to target

right cost in order to attract right customers.

Job costing systems: It enables in collecting information and data that is associated with the

production or various range of services within the business enterprise. For example, Nelson hotel

gives various ranges of services including food and lodging where job costing system enables in

collecting data of each service.

M1

Benefits of management accounting system

Cost accounting

Advantages Disadvantages

Cost reduction

Helps in eliminating waste, loss and

inefficiencies

Assists in price fixation

It leads the issue of under and over-

absorption of overhead

It presents suitable view of cost only

when full capacity is utilized.

Job costing

Advantages Disadvantages

Helps in making estimation about cost

on the basis of past records

Requires clerical work

Highly expensive

5

Gives input for trend analysis and

budgetary control

P2 and D1: Different methods used for management accounting reporting

From: Management Accounting Officer

To: General Manager

Sub: Management Accounting Reports

Introduction: Here various methods that are usually used in management accounting reporting

will be discussed. Besides, the methods will be discussed in respect to the chosen organization

Nelson Hotel. Fuentes-Alabi et al. (2017) stared that management accounting is used for

planning, decision making and controlling. The management accountant of an organization

usually depends on normal financial statements such as balance sheet, cash flow statement,

income statement and other accounting reports that are used for interpreting and analyzing

company information. Hence, management accounting report enables small and medium sized

business to manage and monitor business performance. The methods used in management

accounting report are stated below:

6

CostReports

budgetary control

P2 and D1: Different methods used for management accounting reporting

From: Management Accounting Officer

To: General Manager

Sub: Management Accounting Reports

Introduction: Here various methods that are usually used in management accounting reporting

will be discussed. Besides, the methods will be discussed in respect to the chosen organization

Nelson Hotel. Fuentes-Alabi et al. (2017) stared that management accounting is used for

planning, decision making and controlling. The management accountant of an organization

usually depends on normal financial statements such as balance sheet, cash flow statement,

income statement and other accounting reports that are used for interpreting and analyzing

company information. Hence, management accounting report enables small and medium sized

business to manage and monitor business performance. The methods used in management

accounting report are stated below:

6

CostReports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 2: Methods used in management accounting report

(Source: Self created)

Methods used in management accounting report:

Cost Reports: In the managerial accounting process the cost is calculated for the items that are

produced. It is carried out by considering the raw material cost, additional cost if any, overhead

and labor cost. In cash report the total of all particulars are divided with the amount of products

or services that are given. Hence, all the essential information is summarized in cost report. ()

added that with the help of this report the managers gets the ability to estimate the cost price of

the items and selling prices. Thereby, it allows the managers to get a helping hand in planning

and controlling profit margin (Håkansson and Olsen, 2015).

Budget Reports: Preparing business budget is a major element in managerial accounting system.

Every organization sets a budget in while planning business operation so that they do not fall in

shortfall in between business operation. Budgets are usually created by using present year’s

budget by estimating with the future budget. While preparing a budget report all the essential

source of revenues and expenses are noted. This allows in accomplishing organization goal in an

appropriate manner as they stay in a budgeted amount. For example, Nelson hotel can use this

report to maximize sales and minimize expenses as well as cost of operation. Besides, it can

itemize the costs such as staffing, food, maintenance, taxes furniture and other necessary

equipments (Vasilakos and Nagano, 2017). However, on the critical note, it can be depicted that

budget report sometimes present high deviations when manager failed to set appropriate

standards. In this, budget report leads inappropriate decision making and negatively affects

organizational growth.

Job Cost Reports: Here the expenses are shown for a particular project. In order to evaluate the

profitability of job the business enterprise can estimate the revenue beforehand. It is an effective

procedure that allows in identifying high areas of earning that can able the business to focus

instead of wasting money and time. For example, Nelson hotel uses this report to assess the

expenses included in giving internet services, buying kitchen items and items used for keeping

the hotel clean and hygienic.

7

(Source: Self created)

Methods used in management accounting report:

Cost Reports: In the managerial accounting process the cost is calculated for the items that are

produced. It is carried out by considering the raw material cost, additional cost if any, overhead

and labor cost. In cash report the total of all particulars are divided with the amount of products

or services that are given. Hence, all the essential information is summarized in cost report. ()

added that with the help of this report the managers gets the ability to estimate the cost price of

the items and selling prices. Thereby, it allows the managers to get a helping hand in planning

and controlling profit margin (Håkansson and Olsen, 2015).

Budget Reports: Preparing business budget is a major element in managerial accounting system.

Every organization sets a budget in while planning business operation so that they do not fall in

shortfall in between business operation. Budgets are usually created by using present year’s

budget by estimating with the future budget. While preparing a budget report all the essential

source of revenues and expenses are noted. This allows in accomplishing organization goal in an

appropriate manner as they stay in a budgeted amount. For example, Nelson hotel can use this

report to maximize sales and minimize expenses as well as cost of operation. Besides, it can

itemize the costs such as staffing, food, maintenance, taxes furniture and other necessary

equipments (Vasilakos and Nagano, 2017). However, on the critical note, it can be depicted that

budget report sometimes present high deviations when manager failed to set appropriate

standards. In this, budget report leads inappropriate decision making and negatively affects

organizational growth.

Job Cost Reports: Here the expenses are shown for a particular project. In order to evaluate the

profitability of job the business enterprise can estimate the revenue beforehand. It is an effective

procedure that allows in identifying high areas of earning that can able the business to focus

instead of wasting money and time. For example, Nelson hotel uses this report to assess the

expenses included in giving internet services, buying kitchen items and items used for keeping

the hotel clean and hygienic.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Reports: McDonald (2013) stated that budget is used by management accountant

for comparing revenue and expenditure. In performance report the information regarding the

amounts are recorded for determining new budgets. Every year small and medium sized

enterprise calculates performance reports for creating monthly and quarterly report. It enables the

business manager to make effective planning for future demand. For example, in seasonal time

the hotel industry like Nelson hotel uses performance report to estimate the future demand which

will increase occasionally.

Accounts Receivable Aging Report: This is a significant report used for managing company’s

cash flow which widens customer’s credit. For example, Nelson hotel can use this report to find

organization problem. Sometimes problem are faced by them where customers fails in paying

their balance due to which they can tighten credit policies. Hence, the business can periodically

use this report to keep updated report of every department from overlooking old debts.

Inventory and Manufacturing: In order to make the manufacturing process more resourceful,

business enterprise can use this report to keep report of inventory waste, per-unit overhead cost

and labor hours cost. Hence, the manager of nelson hotel can use this report to compare different

departments and find the area that can improve their business performance (Messeghem et al.

2017). On the critical note, it can be presented that preparation and updation of stock report is

considered as highly time consuming process.

TASK 2:

LO2: To apply management accounting techniques

P3 and M2: Calculation of cost by using cost analysis techniques

i. Absorption Costing Method

Particulars Amount Amount

Sales

£

21,000.00

Less cost of production

Opening stock xx

8

for comparing revenue and expenditure. In performance report the information regarding the

amounts are recorded for determining new budgets. Every year small and medium sized

enterprise calculates performance reports for creating monthly and quarterly report. It enables the

business manager to make effective planning for future demand. For example, in seasonal time

the hotel industry like Nelson hotel uses performance report to estimate the future demand which

will increase occasionally.

Accounts Receivable Aging Report: This is a significant report used for managing company’s

cash flow which widens customer’s credit. For example, Nelson hotel can use this report to find

organization problem. Sometimes problem are faced by them where customers fails in paying

their balance due to which they can tighten credit policies. Hence, the business can periodically

use this report to keep updated report of every department from overlooking old debts.

Inventory and Manufacturing: In order to make the manufacturing process more resourceful,

business enterprise can use this report to keep report of inventory waste, per-unit overhead cost

and labor hours cost. Hence, the manager of nelson hotel can use this report to compare different

departments and find the area that can improve their business performance (Messeghem et al.

2017). On the critical note, it can be presented that preparation and updation of stock report is

considered as highly time consuming process.

TASK 2:

LO2: To apply management accounting techniques

P3 and M2: Calculation of cost by using cost analysis techniques

i. Absorption Costing Method

Particulars Amount Amount

Sales

£

21,000.00

Less cost of production

Opening stock xx

8

Direct materials

£

3,600.00

Direct labor

£

3,000.00

Variable production

overhead

£

1,200.00

Closing stock xx

Contribution

£

13,200.00

Less fixed cost

Production overhead

£

1,800.00

Administrative cost

£

800.00

Selling cost

£

400.00

Total profit and loss

£

10,200.00

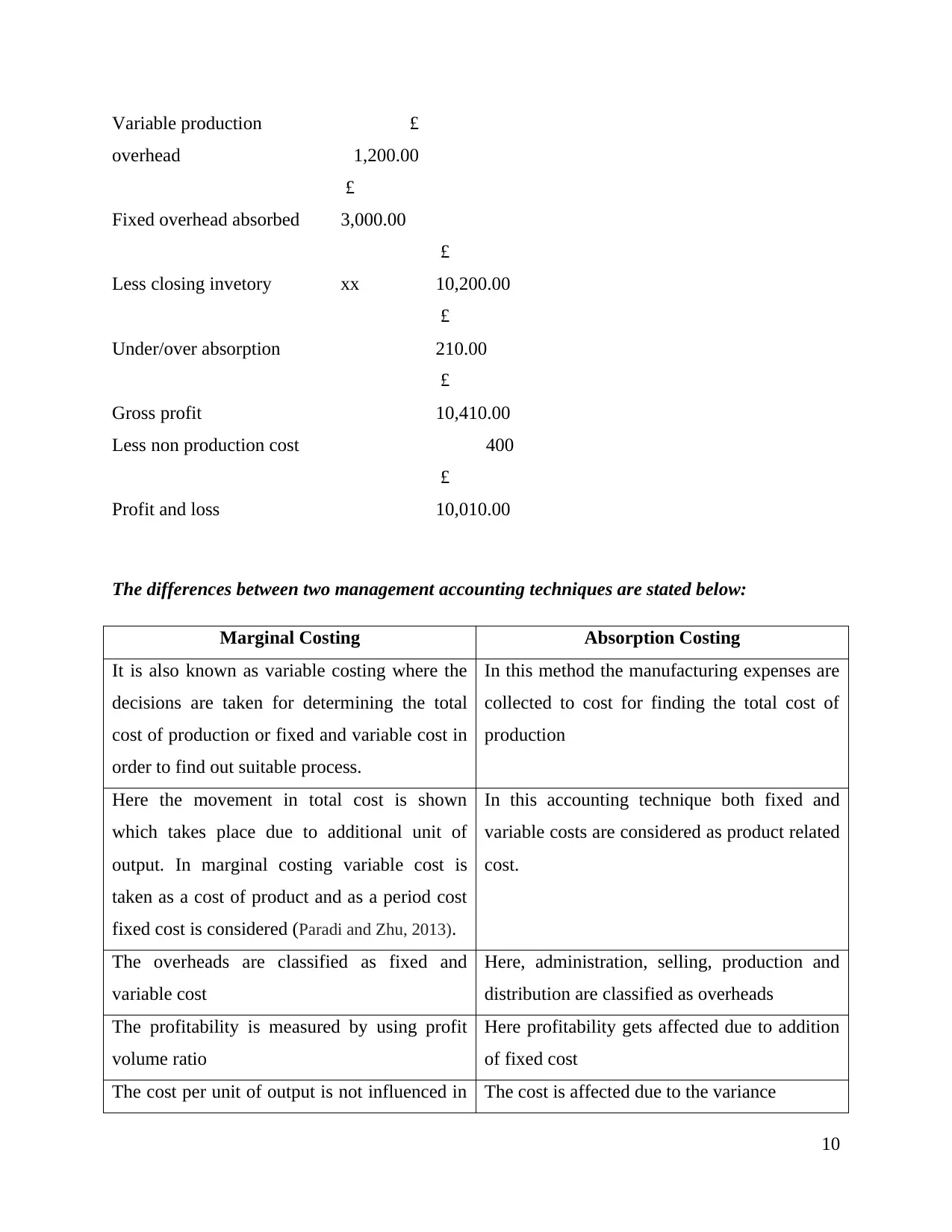

ii. Marginal Costing Method

Particulars Amount Amount

Sales

£

21,000.00

Less cost of sales

Opening inventory xx

Variable cost of production

Direct materials

£

3,600.00

Direct labour

£

3,000.00

9

£

3,600.00

Direct labor

£

3,000.00

Variable production

overhead

£

1,200.00

Closing stock xx

Contribution

£

13,200.00

Less fixed cost

Production overhead

£

1,800.00

Administrative cost

£

800.00

Selling cost

£

400.00

Total profit and loss

£

10,200.00

ii. Marginal Costing Method

Particulars Amount Amount

Sales

£

21,000.00

Less cost of sales

Opening inventory xx

Variable cost of production

Direct materials

£

3,600.00

Direct labour

£

3,000.00

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable production

overhead

£

1,200.00

Fixed overhead absorbed

£

3,000.00

Less closing invetory xx

£

10,200.00

Under/over absorption

£

210.00

Gross profit

£

10,410.00

Less non production cost 400

Profit and loss

£

10,010.00

The differences between two management accounting techniques are stated below:

Marginal Costing Absorption Costing

It is also known as variable costing where the

decisions are taken for determining the total

cost of production or fixed and variable cost in

order to find out suitable process.

In this method the manufacturing expenses are

collected to cost for finding the total cost of

production

Here the movement in total cost is shown

which takes place due to additional unit of

output. In marginal costing variable cost is

taken as a cost of product and as a period cost

fixed cost is considered (Paradi and Zhu, 2013).

In this accounting technique both fixed and

variable costs are considered as product related

cost.

The overheads are classified as fixed and

variable cost

Here, administration, selling, production and

distribution are classified as overheads

The profitability is measured by using profit

volume ratio

Here profitability gets affected due to addition

of fixed cost

The cost per unit of output is not influenced in The cost is affected due to the variance

10

overhead

£

1,200.00

Fixed overhead absorbed

£

3,000.00

Less closing invetory xx

£

10,200.00

Under/over absorption

£

210.00

Gross profit

£

10,410.00

Less non production cost 400

Profit and loss

£

10,010.00

The differences between two management accounting techniques are stated below:

Marginal Costing Absorption Costing

It is also known as variable costing where the

decisions are taken for determining the total

cost of production or fixed and variable cost in

order to find out suitable process.

In this method the manufacturing expenses are

collected to cost for finding the total cost of

production

Here the movement in total cost is shown

which takes place due to additional unit of

output. In marginal costing variable cost is

taken as a cost of product and as a period cost

fixed cost is considered (Paradi and Zhu, 2013).

In this accounting technique both fixed and

variable costs are considered as product related

cost.

The overheads are classified as fixed and

variable cost

Here, administration, selling, production and

distribution are classified as overheads

The profitability is measured by using profit

volume ratio

Here profitability gets affected due to addition

of fixed cost

The cost per unit of output is not influenced in The cost is affected due to the variance

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

variances in the opening and closing stock

The cost data is shown for outlining total

contribution of every product

The cost data is presented in conventional

manner

(Source: Sithole et al. 2017)

D2 Interpreting findings

Therefore, the management accounting officer can recommend the importance of two

management techniques for increasing profitability of Nelson Hotel. When the management

accounting will apply marginal cost it will help in finding profitability of each sales activity and

it will appear low under absorption cost.

TASK 3:

LO3: To use planning tools in management accounting

P4: Advantages and disadvantages of various planning tools used to control budget

Various planning tool that are used to control budget are financial control, operation

management, budgetary control, quality control and inventory control. By selecting appropriate

tool the business enterprise can enhance profitability and meet organization goals and standards.

Therefore, it becomes easier for the management accountant to forecast budget in an efficient

manner which able the business to monitor the resources that are required to run a business

operation. Such strategy enables the business to increase the revenue.

Financial System: The control system is used to control the financial resources like shareholders

investments and revenue that flow into the business enterprise. The technique is effective for the

managers in assessing the use of financial resources like cash, inventories, accounts receivable

and payable and long term debt. Moreover, such planning tool can help in achieving profitability

standards, liquidity and solvency (Stanley and Pamela, 2017).

Advantages:

11

The cost data is shown for outlining total

contribution of every product

The cost data is presented in conventional

manner

(Source: Sithole et al. 2017)

D2 Interpreting findings

Therefore, the management accounting officer can recommend the importance of two

management techniques for increasing profitability of Nelson Hotel. When the management

accounting will apply marginal cost it will help in finding profitability of each sales activity and

it will appear low under absorption cost.

TASK 3:

LO3: To use planning tools in management accounting

P4: Advantages and disadvantages of various planning tools used to control budget

Various planning tool that are used to control budget are financial control, operation

management, budgetary control, quality control and inventory control. By selecting appropriate

tool the business enterprise can enhance profitability and meet organization goals and standards.

Therefore, it becomes easier for the management accountant to forecast budget in an efficient

manner which able the business to monitor the resources that are required to run a business

operation. Such strategy enables the business to increase the revenue.

Financial System: The control system is used to control the financial resources like shareholders

investments and revenue that flow into the business enterprise. The technique is effective for the

managers in assessing the use of financial resources like cash, inventories, accounts receivable

and payable and long term debt. Moreover, such planning tool can help in achieving profitability

standards, liquidity and solvency (Stanley and Pamela, 2017).

Advantages:

11

It not only give the base to carry out present and future financial activities but also able to

check the actual performance. It enable in giving the manager a base for estimating future financial activities by guiding

the manager in an appropriate manner. The tool of financial control ensures that resources are used in an appropriate manner and

to make sure that financial discipline is proper within the organization. It gives financial stability by controlling productivity and increasing efficiency. Both

productivity and efficiency enables to enhance the earning.

Disadvantages:

Instead of having advantages the financial control technique have disadvantages as they

have to compare standard performance with actual performance. It possesses difficulty in implementing control measures during business operation. The standards are set rigid by considering the parameters. During the performance of

actual job the conditions are not the same. Implementing financial control requires high cost.

Operating Budget: Khodaverdi (2017) stated operating budget as a statement which presents

organization financial plan during the planning of budget period. It also reflects several

operational activities such as expenses, revenue and profit budget. Through this budget the

organization can make effective planning for a specific period. The operating budgets are of

several types. It includes sales or revenue budget which only focuses on organization income for

receiving normal operation. In case of expenses budget anticipated expenses can be specified.

For example, Nelson hotel need to project the budget beforehand to pint out upcoming expenses

and revenue.

Advantages:

It enable in keeping a track on the entire business such as the money spent or the income

earned. It helps the business to check that it is on track or the business it facing any

problem or not.

12

check the actual performance. It enable in giving the manager a base for estimating future financial activities by guiding

the manager in an appropriate manner. The tool of financial control ensures that resources are used in an appropriate manner and

to make sure that financial discipline is proper within the organization. It gives financial stability by controlling productivity and increasing efficiency. Both

productivity and efficiency enables to enhance the earning.

Disadvantages:

Instead of having advantages the financial control technique have disadvantages as they

have to compare standard performance with actual performance. It possesses difficulty in implementing control measures during business operation. The standards are set rigid by considering the parameters. During the performance of

actual job the conditions are not the same. Implementing financial control requires high cost.

Operating Budget: Khodaverdi (2017) stated operating budget as a statement which presents

organization financial plan during the planning of budget period. It also reflects several

operational activities such as expenses, revenue and profit budget. Through this budget the

organization can make effective planning for a specific period. The operating budgets are of

several types. It includes sales or revenue budget which only focuses on organization income for

receiving normal operation. In case of expenses budget anticipated expenses can be specified.

For example, Nelson hotel need to project the budget beforehand to pint out upcoming expenses

and revenue.

Advantages:

It enable in keeping a track on the entire business such as the money spent or the income

earned. It helps the business to check that it is on track or the business it facing any

problem or not.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.