Management Accounting Report: Financial Information and Budgeting

VerifiedAdded on 2020/06/06

|14

|3705

|30

Report

AI Summary

This management accounting report provides a comprehensive overview of management accounting principles and their application within Tech (UK) Limited. It begins by differentiating between management and financial accounting, highlighting the importance of management accounting tools for internal decision-making, including trend analysis, break-even analysis, and cost accounting systems like actual, normal, and standard costing. The report then explores the framing of financial information, detailing various managerial accounting reports such as budget reports, account receivable reports, and performance reports, emphasizing the importance of presenting financial data according to international accounting standards. Furthermore, the report includes an analysis of Tech (UK) Limited's financial performance, presenting income statements using both absorption and marginal costing techniques. The report concludes by explaining the use of budgets for planning and control, discussing the merits and demerits of master budgets and other types of budgets. Overall, the report provides a detailed analysis of management accounting concepts and their practical application in a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Explaining the management accounting and the important requirements.............................1

P2 Framing the Financial information........................................................................................3

Task 2...............................................................................................................................................5

P3 Determining the September month's financial information with respect to disclosure of

income statement.........................................................................................................................5

Task 3...............................................................................................................................................6

P4 Explaining the use of budgets for planning and purpose of control......................................6

Task 4...............................................................................................................................................9

P5 Interpreting the approaches of management accounting with respect to financial problems

in the organization.......................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Explaining the management accounting and the important requirements.............................1

P2 Framing the Financial information........................................................................................3

Task 2...............................................................................................................................................5

P3 Determining the September month's financial information with respect to disclosure of

income statement.........................................................................................................................5

Task 3...............................................................................................................................................6

P4 Explaining the use of budgets for planning and purpose of control......................................6

Task 4...............................................................................................................................................9

P5 Interpreting the approaches of management accounting with respect to financial problems

in the organization.......................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is very beneficial tool with respect to internal environment of

the organization. There is brief discussion about management accounting tools and techniques

with there significance for enhancing the operation of tech (UK) limited retail stores. There is

presence of different approaches of accounting which will be helpful to overcome all the

financial problems in Tech UK Limited. Further the income statement of Tech (UK) limited is

drawn on the basis of two costing techniques.

Task 1

P1 Explaining the management accounting and the important requirements

i. Difference between management accounting and financial accounting

Management accounting helps in making the decisions very effective related to business

and financial accounting helps in classifying, recording, summarising and analysing all the

organisation's financial affairs (Narasimhan, 2017). On the basis of application of management

accounting, it takes steps and strategies which are very meaningful to the organisation and on

contrary side, financial accounting is prepared for framing very accurate picture of financial

affairs. Scope of financial management is pervasive but in management accounting, the scope is

much broader. The measuring grid of management accounting is qualitative and quantitative but

financial accounting is only measured as quantitative. Management accounting is dependent on

financial accounting for taking right decisions but financial accounting is not dependent on

management accounting. No rule is followed in management accounting but financial accounting

has to be prepared on the basis of GAAP or IFRS.

ii. Management accounting information as a decision making tool for department

managers.

Small or large business owners or managers have to face many decisions on every

business days. The information of management accounting has been used for the operations

which are used to prepare report and ongoing insights have been given into the performance of

business like labour utilisation and profit margin. Managerial accounting gives the description of

business activities by collecting, reporting and analysing the activities which are related to

business and there main target is towards the internal mangers instead of external client of

business such as shareholders or lenders and banks. Internal managers use specific management

accounting tools for decision making of business. The specific management accounting tools are:

1

Management accounting is very beneficial tool with respect to internal environment of

the organization. There is brief discussion about management accounting tools and techniques

with there significance for enhancing the operation of tech (UK) limited retail stores. There is

presence of different approaches of accounting which will be helpful to overcome all the

financial problems in Tech UK Limited. Further the income statement of Tech (UK) limited is

drawn on the basis of two costing techniques.

Task 1

P1 Explaining the management accounting and the important requirements

i. Difference between management accounting and financial accounting

Management accounting helps in making the decisions very effective related to business

and financial accounting helps in classifying, recording, summarising and analysing all the

organisation's financial affairs (Narasimhan, 2017). On the basis of application of management

accounting, it takes steps and strategies which are very meaningful to the organisation and on

contrary side, financial accounting is prepared for framing very accurate picture of financial

affairs. Scope of financial management is pervasive but in management accounting, the scope is

much broader. The measuring grid of management accounting is qualitative and quantitative but

financial accounting is only measured as quantitative. Management accounting is dependent on

financial accounting for taking right decisions but financial accounting is not dependent on

management accounting. No rule is followed in management accounting but financial accounting

has to be prepared on the basis of GAAP or IFRS.

ii. Management accounting information as a decision making tool for department

managers.

Small or large business owners or managers have to face many decisions on every

business days. The information of management accounting has been used for the operations

which are used to prepare report and ongoing insights have been given into the performance of

business like labour utilisation and profit margin. Managerial accounting gives the description of

business activities by collecting, reporting and analysing the activities which are related to

business and there main target is towards the internal mangers instead of external client of

business such as shareholders or lenders and banks. Internal managers use specific management

accounting tools for decision making of business. The specific management accounting tools are:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trend analysis: It is helpful for forecasting future as it is a tool which tracks the changes to data

from the time when business conditions are changing.

Break even analysis: The calculation where is combination of unit volume and sales and it will

generate neutral revenue not even profit and not loss (Leotta, Rizza and Ruggeri, 2017).

Margin analysis: It can be referred as profit analysis which has been built around revenue which

is generated by some particular subset like region, product, business branch or customer.

Capital budgeting analysis: All the investment proposals are examined for allocating the

finance and to acquire the fixed asset.

Transaction analysis: Specific transactions are tracked like sales related to particular customer

or purchase of some certain goods.

Inventory analysis: This tool is very useful for determining cost of goods sold and even

allocating value on raw materials and even unsold products.

Constraint analysis: The primary bottlenecks of the business is examined and its effects on

profit and revenues.

iii. Cost accounting systems

Actual costing: It refers to an accounting system which exercises the rates of direct cost,

actual cost and all the actual qualities which are used in the production of identifying the specific

product's cost. Generally, actual costing tracks the direct cost which is related to cost object or

which helps in measuring cost. For example: For a plant of manufacturing plastic items such as

bottle, box etc. the actual material which is required for production of plastic, actual man hours

which are consumed are taken in account of actual cost.

Normal costing: It refers to the cost allocation method which helps in assigning the cost

on the basis of labour, material and overhead which is used for producing them. It is a process of

finding the price of product that is used. In other words, the costs of products which prepare

normal costing are manufacturing overhead, actual direct costs and actual material. The direct

cost and material are actual costs which are directly linked while producing labour and raw

material. Manufacturing overhead is an appropriate rate which can be example of normal

costing. In short, it is the way to identify the cost of item which is manufactured for applying the

cost of product.

Standard costing: It refers to costing which substitutes the cost which is expected from

the actual cost in the records of accounting and then by tracking the variance of actual costs and

2

from the time when business conditions are changing.

Break even analysis: The calculation where is combination of unit volume and sales and it will

generate neutral revenue not even profit and not loss (Leotta, Rizza and Ruggeri, 2017).

Margin analysis: It can be referred as profit analysis which has been built around revenue which

is generated by some particular subset like region, product, business branch or customer.

Capital budgeting analysis: All the investment proposals are examined for allocating the

finance and to acquire the fixed asset.

Transaction analysis: Specific transactions are tracked like sales related to particular customer

or purchase of some certain goods.

Inventory analysis: This tool is very useful for determining cost of goods sold and even

allocating value on raw materials and even unsold products.

Constraint analysis: The primary bottlenecks of the business is examined and its effects on

profit and revenues.

iii. Cost accounting systems

Actual costing: It refers to an accounting system which exercises the rates of direct cost,

actual cost and all the actual qualities which are used in the production of identifying the specific

product's cost. Generally, actual costing tracks the direct cost which is related to cost object or

which helps in measuring cost. For example: For a plant of manufacturing plastic items such as

bottle, box etc. the actual material which is required for production of plastic, actual man hours

which are consumed are taken in account of actual cost.

Normal costing: It refers to the cost allocation method which helps in assigning the cost

on the basis of labour, material and overhead which is used for producing them. It is a process of

finding the price of product that is used. In other words, the costs of products which prepare

normal costing are manufacturing overhead, actual direct costs and actual material. The direct

cost and material are actual costs which are directly linked while producing labour and raw

material. Manufacturing overhead is an appropriate rate which can be example of normal

costing. In short, it is the way to identify the cost of item which is manufactured for applying the

cost of product.

Standard costing: It refers to costing which substitutes the cost which is expected from

the actual cost in the records of accounting and then by tracking the variance of actual costs and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expected costs. This gives the representation to simplified alternative to layering system of cost

like LIFO and FIFO methods where huge amount of historical cost information has been

maintained. There is involvement of various estimation cost for the activities of the company.

iv. Inventory management systems

It is one of the most beneficial system which will be helping in tracing each transactions

related to inventory outflow and inflow. These records help the manager of the organisation for

analysing the adequate numbers of inventories which are requirement of the premises. All the

relevant operations like purchase, deliveries and sale of goods are recorded in the form of

transactions. It will create advantage to Tech (UK) limited as there managers will be able to

perform the deep analysis of inventory required for the coming period as it will be creating

ability to deliver such services and products to the customers.

v. Job costing system

This technique is very much beneficial to the business with the perspective of performing

adequate analysis of the batch, unit and job which has been produced by the company. It

generally refers to each product which is variable and has many differences in cost and style of

manufacturing. This cost will be incurred in the account of organisation. While undertaking the

operations of Tech (UK) limited, the cost which is relevant for the manufacturing of carry on

gadgets and mobile charger have various other manufacturing techniques and even the level of

finance which has been required for operations (Wachira, M., 2017.).

P2 Framing the Financial information

With the context of framing the financial information, it is compilation of many financial

transactions in a company. These informations are used by various owners and managers for

analyzing the financial performance and stability of the organisation and even the operation of

the company or to measure the performance of individuals such as managers and employees. It is

very important to present the financial information because of presence of national accounting

standards with respect to public disclosure of these financial documents.

i. Types of managerial accounting reports

There are four types of managerial accounting report which Tech (UK) limited will be using for

measuring there operations and in turn it will be implicating the measure to improve their level

of performance:

Budget report

3

like LIFO and FIFO methods where huge amount of historical cost information has been

maintained. There is involvement of various estimation cost for the activities of the company.

iv. Inventory management systems

It is one of the most beneficial system which will be helping in tracing each transactions

related to inventory outflow and inflow. These records help the manager of the organisation for

analysing the adequate numbers of inventories which are requirement of the premises. All the

relevant operations like purchase, deliveries and sale of goods are recorded in the form of

transactions. It will create advantage to Tech (UK) limited as there managers will be able to

perform the deep analysis of inventory required for the coming period as it will be creating

ability to deliver such services and products to the customers.

v. Job costing system

This technique is very much beneficial to the business with the perspective of performing

adequate analysis of the batch, unit and job which has been produced by the company. It

generally refers to each product which is variable and has many differences in cost and style of

manufacturing. This cost will be incurred in the account of organisation. While undertaking the

operations of Tech (UK) limited, the cost which is relevant for the manufacturing of carry on

gadgets and mobile charger have various other manufacturing techniques and even the level of

finance which has been required for operations (Wachira, M., 2017.).

P2 Framing the Financial information

With the context of framing the financial information, it is compilation of many financial

transactions in a company. These informations are used by various owners and managers for

analyzing the financial performance and stability of the organisation and even the operation of

the company or to measure the performance of individuals such as managers and employees. It is

very important to present the financial information because of presence of national accounting

standards with respect to public disclosure of these financial documents.

i. Types of managerial accounting reports

There are four types of managerial accounting report which Tech (UK) limited will be using for

measuring there operations and in turn it will be implicating the measure to improve their level

of performance:

Budget report

3

Account receivable report

Cost managerial accounting report

Performance report

Budget report: It is very captious for measuring the performance of the organisation and

it will be giving ability to generate a small business and in large business it will be created in

department wise. As every company forms the budget report for understanding the grand scheme

of their own business. It helps each stakeholders for controlling and understanding the operation

cost of the business. So with this perspective Tech (UK) limited will use this report for creating

accurate decisions for predicting the activity's cost which are going to be held in the future.

Account receivable report: This report is fully on the basis of credit, if any business has

too much credit and it is extending from day to day then the most accurate report is account

receivable aging report. The remaining balance of the clients has been break down for specific

period so this activity allows manager to determine the issues and defaulters related to company

collection process. To determine the capability of debtor is mentioned as 30, 60 and 90 days for

making payment.

Cost managerial accounting: This report gives the brief summary of every information

of the business. The cost of items which are manufactured is computed in this report. The cost

which are undertaken in this report are raw material cost, labour, overhead and any additional

cost. Managers are offered by this report, the capacity to realise the cost price of item as

compared to selling price. Along with this profit margins are also determined and observed with

these reports and even the clear picture is drawn of cost that is used in production and

procurement of the items (Chiwamit, Modell and Scapens, 2017).

Performance report: These report helps in reviewing the performance of the

organisation. Many organisations prepare it quarterly, half yearly and yearly. These reports are

used by the mangers to develop the strategic decisions for the future of the company. In big

organisations these reports are formed on the basis of department as well. On the basis of

performance there are many lays off and promotion if it is required. It is important for every

organisation to track the perfect measure of the strategy along with the mission.

ii. Financial information should be presentable

For the clear understanding of the information which is presented by internal stakeholders

in the form of financial subset which should be according to the international accounting

4

Cost managerial accounting report

Performance report

Budget report: It is very captious for measuring the performance of the organisation and

it will be giving ability to generate a small business and in large business it will be created in

department wise. As every company forms the budget report for understanding the grand scheme

of their own business. It helps each stakeholders for controlling and understanding the operation

cost of the business. So with this perspective Tech (UK) limited will use this report for creating

accurate decisions for predicting the activity's cost which are going to be held in the future.

Account receivable report: This report is fully on the basis of credit, if any business has

too much credit and it is extending from day to day then the most accurate report is account

receivable aging report. The remaining balance of the clients has been break down for specific

period so this activity allows manager to determine the issues and defaulters related to company

collection process. To determine the capability of debtor is mentioned as 30, 60 and 90 days for

making payment.

Cost managerial accounting: This report gives the brief summary of every information

of the business. The cost of items which are manufactured is computed in this report. The cost

which are undertaken in this report are raw material cost, labour, overhead and any additional

cost. Managers are offered by this report, the capacity to realise the cost price of item as

compared to selling price. Along with this profit margins are also determined and observed with

these reports and even the clear picture is drawn of cost that is used in production and

procurement of the items (Chiwamit, Modell and Scapens, 2017).

Performance report: These report helps in reviewing the performance of the

organisation. Many organisations prepare it quarterly, half yearly and yearly. These reports are

used by the mangers to develop the strategic decisions for the future of the company. In big

organisations these reports are formed on the basis of department as well. On the basis of

performance there are many lays off and promotion if it is required. It is important for every

organisation to track the perfect measure of the strategy along with the mission.

ii. Financial information should be presentable

For the clear understanding of the information which is presented by internal stakeholders

in the form of financial subset which should be according to the international accounting

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

standards. Along with this, board will present the financial statements with the influence of these

standards and they will be guiding the professionals for facilitating the framework which is

authenticated. The IFRS, IASB and GAAP are main international institutions which will be

giving adequate support for presenting the financial information. All the stakeholders and

investors will be influenced by these standards and board for having a clear picture of

profitability, liquidity and efficiency of the organization. So Tech (UK) limited has to perform

the accurate disclosure on the basis of accounting standards (Chenhall and Moers, 2015).

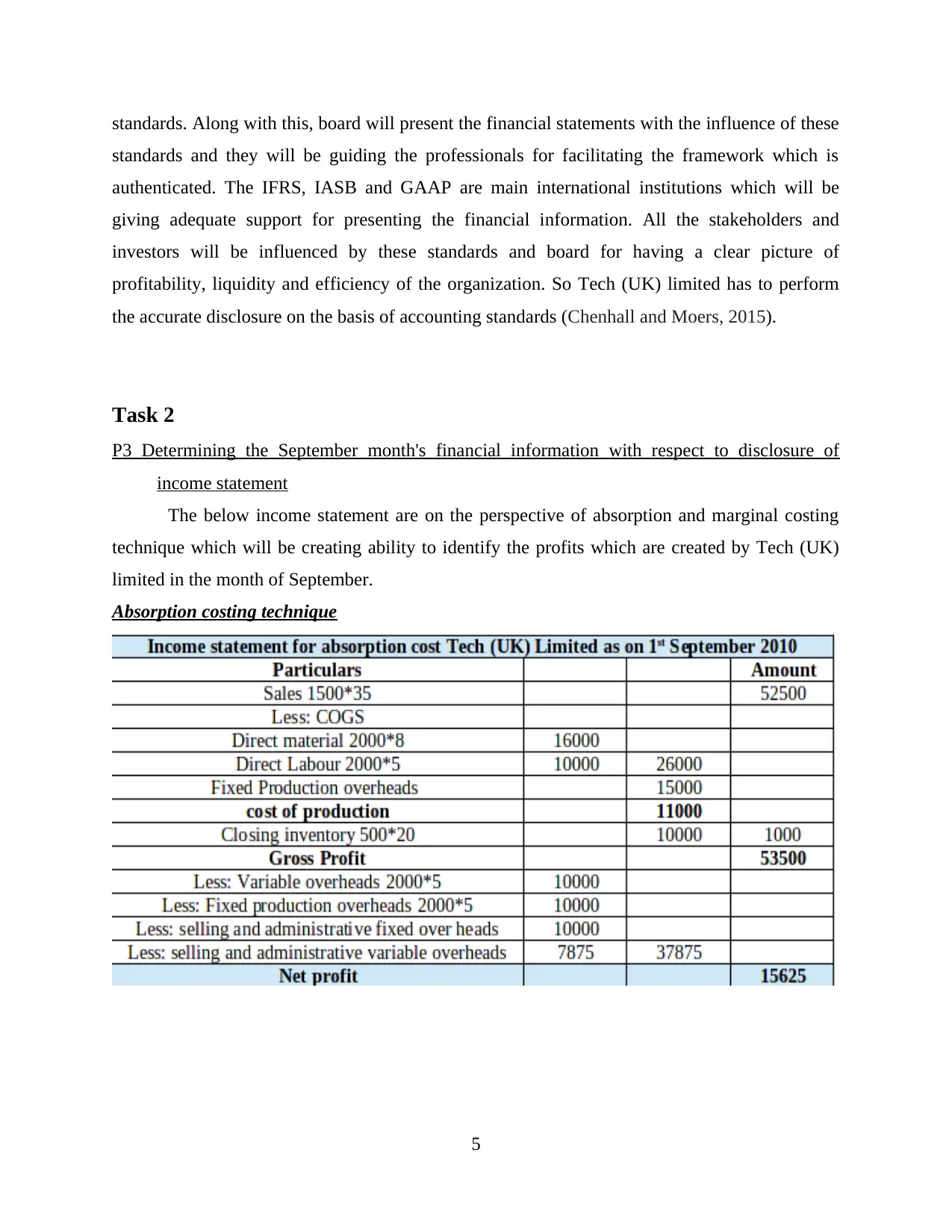

Task 2

P3 Determining the September month's financial information with respect to disclosure of

income statement

The below income statement are on the perspective of absorption and marginal costing

technique which will be creating ability to identify the profits which are created by Tech (UK)

limited in the month of September.

Absorption costing technique

5

standards and they will be guiding the professionals for facilitating the framework which is

authenticated. The IFRS, IASB and GAAP are main international institutions which will be

giving adequate support for presenting the financial information. All the stakeholders and

investors will be influenced by these standards and board for having a clear picture of

profitability, liquidity and efficiency of the organization. So Tech (UK) limited has to perform

the accurate disclosure on the basis of accounting standards (Chenhall and Moers, 2015).

Task 2

P3 Determining the September month's financial information with respect to disclosure of

income statement

The below income statement are on the perspective of absorption and marginal costing

technique which will be creating ability to identify the profits which are created by Tech (UK)

limited in the month of September.

Absorption costing technique

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

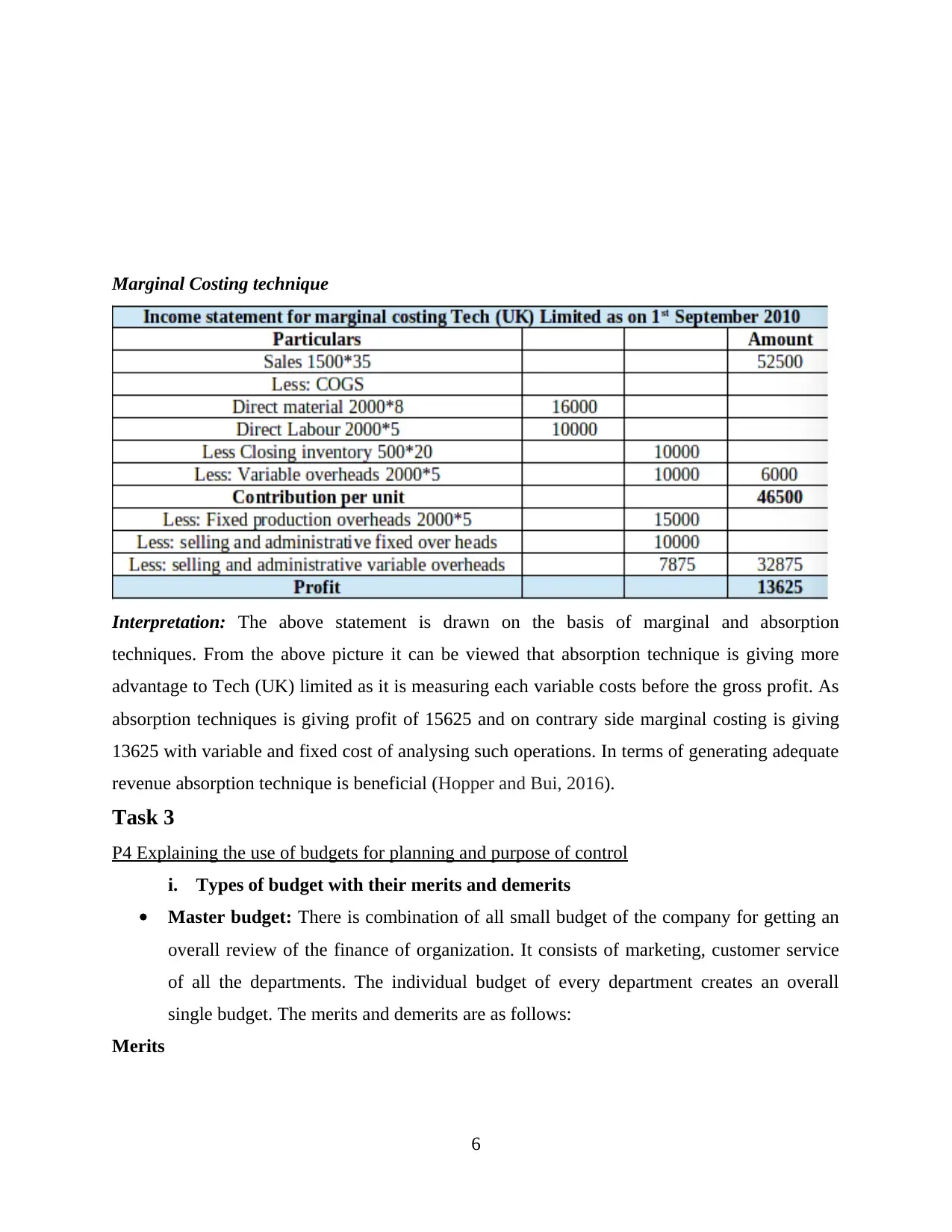

Marginal Costing technique

Interpretation: The above statement is drawn on the basis of marginal and absorption

techniques. From the above picture it can be viewed that absorption technique is giving more

advantage to Tech (UK) limited as it is measuring each variable costs before the gross profit. As

absorption techniques is giving profit of 15625 and on contrary side marginal costing is giving

13625 with variable and fixed cost of analysing such operations. In terms of generating adequate

revenue absorption technique is beneficial (Hopper and Bui, 2016).

Task 3

P4 Explaining the use of budgets for planning and purpose of control

i. Types of budget with their merits and demerits

Master budget: There is combination of all small budget of the company for getting an

overall review of the finance of organization. It consists of marketing, customer service

of all the departments. The individual budget of every department creates an overall

single budget. The merits and demerits are as follows:

Merits

6

Interpretation: The above statement is drawn on the basis of marginal and absorption

techniques. From the above picture it can be viewed that absorption technique is giving more

advantage to Tech (UK) limited as it is measuring each variable costs before the gross profit. As

absorption techniques is giving profit of 15625 and on contrary side marginal costing is giving

13625 with variable and fixed cost of analysing such operations. In terms of generating adequate

revenue absorption technique is beneficial (Hopper and Bui, 2016).

Task 3

P4 Explaining the use of budgets for planning and purpose of control

i. Types of budget with their merits and demerits

Master budget: There is combination of all small budget of the company for getting an

overall review of the finance of organization. It consists of marketing, customer service

of all the departments. The individual budget of every department creates an overall

single budget. The merits and demerits are as follows:

Merits

6

It provides an overview of the company's budget to the business owner and the company

executives in one budget. It gives the justification that where the organization is earning and

where it is spending. It also gives the interpretation that where the business is in good condition

and where it is becoming worse. It will be very beneficial for Tech (UK) for planning it very

effectively (Nielsen, Mitchell and Nørreklit , 2015).

Demerits

The main disadvantage of master budget is that there is lack of specificity as it does not

fulfil the particular requirement of the organisation and due to specificity it is very difficult to

understand, update and even read.

Zero based budget: It is a method in which all the expenses are determined with the

perspective of actual expenses which are to be incurred but not on incremental basis.

Every activity is been justified and zero is taken as base.

Merits

This method provides accuracy as it involves various arbitrary changes according to the

previous year budget. The main merit is that there is presence of efficient allocation of fund to

each and every department and even there is absence of budget inflation.

Demerits

This type of budgeting is very time consuming as there is requirement of huge manpower

and there is absence of expertise because each and every task need to be justified and for this

justification there is need of proper training to the managers which is very expensive.

Activity based budget : This method signifies every budget in the consideration of the

cost of overhead. For arriving at current year budget, past year budget is ignored in this

process. After the justification of cost driver, budgets are prepared.

Merits

In this method, all the cost drivers are evaluated which are involved in activity. It draws

competitive edge to the company by eliminating or substituting the activities which are not

required. It helps in improving the relation ship between customer and the company by providing

the best quality to the customers.

Demerits

There is huge requirement of deep understanding of different functional areas and for this

every manager should have ability to understand but it is not there. The nature of this method is

7

executives in one budget. It gives the justification that where the organization is earning and

where it is spending. It also gives the interpretation that where the business is in good condition

and where it is becoming worse. It will be very beneficial for Tech (UK) for planning it very

effectively (Nielsen, Mitchell and Nørreklit , 2015).

Demerits

The main disadvantage of master budget is that there is lack of specificity as it does not

fulfil the particular requirement of the organisation and due to specificity it is very difficult to

understand, update and even read.

Zero based budget: It is a method in which all the expenses are determined with the

perspective of actual expenses which are to be incurred but not on incremental basis.

Every activity is been justified and zero is taken as base.

Merits

This method provides accuracy as it involves various arbitrary changes according to the

previous year budget. The main merit is that there is presence of efficient allocation of fund to

each and every department and even there is absence of budget inflation.

Demerits

This type of budgeting is very time consuming as there is requirement of huge manpower

and there is absence of expertise because each and every task need to be justified and for this

justification there is need of proper training to the managers which is very expensive.

Activity based budget : This method signifies every budget in the consideration of the

cost of overhead. For arriving at current year budget, past year budget is ignored in this

process. After the justification of cost driver, budgets are prepared.

Merits

In this method, all the cost drivers are evaluated which are involved in activity. It draws

competitive edge to the company by eliminating or substituting the activities which are not

required. It helps in improving the relation ship between customer and the company by providing

the best quality to the customers.

Demerits

There is huge requirement of deep understanding of different functional areas and for this

every manager should have ability to understand but it is not there. The nature of this method is

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

very complex and various factors should be properly researched and analysed. It consumes too

many resources of the organization as it is very time consuming. It only focuses on short term

goals, long term perspective is totally avoided in this budget.

ii. Determining the price while budget preparation

For planning the steps of budget preparation Tech (UK) limited should take certain steps

so that every requirement of all departments should be fulfilled very efficiently.

Obtaining the Estimates

Coordinating

Communicating

Budget plan should be implemented

Interim progress should be reported towards objectives of budget

The first step gives the justification that each and every estimate of level of production,

sales, expected costs and resource availability from every department should be obtained by each

departmental heads or the mangers. After obtaining they should be properly coordinated with

every department and various units of the organisation and potential should be planned. The

budget should be properly communicated to all responsible managers and departments who are

concerned, they should give proper highlight to attain the goals and objectives of the

organisation. There is requirement of very effective communication in the process of budget. The

most important step is to implement budge plan in the coming period with various business units.

In last step interim should be properly observed if any feedback is there then it should be applied

as soon as possible, as it will be giving directly reflecting in the annual results of Tech (UK)

limited (Podgórski, 2015).

iii. Significance of budget as a tool for planning and control purpose

There are various tools for planning budget and for the purpose of controlling:

Net present value

Internal rate of return

Net present value: It is one of the best capital budgeting method which is used to

evaluate the investment project of physical assets in business might wants to invest. It is

calculated from the difference of present value of cash inflow and present value of cash outflow

over the period. Time factor is been considered in this method and risk and profitability is given

8

many resources of the organization as it is very time consuming. It only focuses on short term

goals, long term perspective is totally avoided in this budget.

ii. Determining the price while budget preparation

For planning the steps of budget preparation Tech (UK) limited should take certain steps

so that every requirement of all departments should be fulfilled very efficiently.

Obtaining the Estimates

Coordinating

Communicating

Budget plan should be implemented

Interim progress should be reported towards objectives of budget

The first step gives the justification that each and every estimate of level of production,

sales, expected costs and resource availability from every department should be obtained by each

departmental heads or the mangers. After obtaining they should be properly coordinated with

every department and various units of the organisation and potential should be planned. The

budget should be properly communicated to all responsible managers and departments who are

concerned, they should give proper highlight to attain the goals and objectives of the

organisation. There is requirement of very effective communication in the process of budget. The

most important step is to implement budge plan in the coming period with various business units.

In last step interim should be properly observed if any feedback is there then it should be applied

as soon as possible, as it will be giving directly reflecting in the annual results of Tech (UK)

limited (Podgórski, 2015).

iii. Significance of budget as a tool for planning and control purpose

There are various tools for planning budget and for the purpose of controlling:

Net present value

Internal rate of return

Net present value: It is one of the best capital budgeting method which is used to

evaluate the investment project of physical assets in business might wants to invest. It is

calculated from the difference of present value of cash inflow and present value of cash outflow

over the period. Time factor is been considered in this method and risk and profitability is given

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

prior importance. NPV is very typical and difficult to use and it does not provide accurate

decision if there is presence of mutually exclusive investment project.

Internal rate of return: It is method to determining the rate of return as it does not

involve the factors which are external. It considers the time value of money and the most

attractive factor that it is very simple to calculate and interpret. But there is ignorance of

economies of scale and it highly dependent or it has contingent projects.

Task 4

P5 Interpreting the approaches of management accounting with respect to financial problems in

the organization

Balanced Score card: It is one of the most important strategic tool for planning and utilising

resources of the company. It creates the priority for employees to perform well and what task

they have to do perform. It allocates and observe the strategic targets with ease. With the help of

BSC Tech (UK) limited can measure the financial resources which helps in attaining the

customer satisfaction and even product innovation (Zhang and et.al, 2015).

KPI (Key Performance Indicator): This metric is used to determine the organization's success

and the goals which have to be met by employees. Employees must be able to perform the task

with respect to goals. It is very effective tool for measuring the performance of employees within

specific time period. It can locate very effective and efficient employees with too much ease.

Financial governance: For performing better in the industry with better operational

performance so there is need to allocate the duties and responsibilities to the one who are capable

to make plans and motivate the staff with adequate resources. Tech (UK) limited will be

benefited in this tool as all the duties will be assigned according to the skills so it will be

generating more profit to the company.

CONCLUSION

From the above discussion it can be concluded that management accounting is very

essential for every organisation and in Tech (UK) limited it is playing very essential role. As

financial accounting and management accounting both are important for measuring the

performance whether qualitative or quantitative. The present report states that financial

information should be presented in very presentable and efficient manner. Budget preparation

process should not skip any of the step then it will lead to delay and mismatch in the balance

sheet.

9

decision if there is presence of mutually exclusive investment project.

Internal rate of return: It is method to determining the rate of return as it does not

involve the factors which are external. It considers the time value of money and the most

attractive factor that it is very simple to calculate and interpret. But there is ignorance of

economies of scale and it highly dependent or it has contingent projects.

Task 4

P5 Interpreting the approaches of management accounting with respect to financial problems in

the organization

Balanced Score card: It is one of the most important strategic tool for planning and utilising

resources of the company. It creates the priority for employees to perform well and what task

they have to do perform. It allocates and observe the strategic targets with ease. With the help of

BSC Tech (UK) limited can measure the financial resources which helps in attaining the

customer satisfaction and even product innovation (Zhang and et.al, 2015).

KPI (Key Performance Indicator): This metric is used to determine the organization's success

and the goals which have to be met by employees. Employees must be able to perform the task

with respect to goals. It is very effective tool for measuring the performance of employees within

specific time period. It can locate very effective and efficient employees with too much ease.

Financial governance: For performing better in the industry with better operational

performance so there is need to allocate the duties and responsibilities to the one who are capable

to make plans and motivate the staff with adequate resources. Tech (UK) limited will be

benefited in this tool as all the duties will be assigned according to the skills so it will be

generating more profit to the company.

CONCLUSION

From the above discussion it can be concluded that management accounting is very

essential for every organisation and in Tech (UK) limited it is playing very essential role. As

financial accounting and management accounting both are important for measuring the

performance whether qualitative or quantitative. The present report states that financial

information should be presented in very presentable and efficient manner. Budget preparation

process should not skip any of the step then it will lead to delay and mismatch in the balance

sheet.

9

REFERENCES

Books and Journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society .47. pp.1-13.

Chiwamit, P., Modell, S. and Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Narasimhan, M. S., 2017. Variance Analysis: General Framework.

Nielsen, L. B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1,

pp. 64-82). Elsevier.

Podgórski, D., 2015. Measuring operational performance of OSH management system–A

demonstration of AHP-based selection of leading key performance indicators. Safety

science. 73. pp.146-166.

Wachira, M., 2017. Determinants of corporate social disclosures in Kenya: A longitudinal study

of firms listed on the Nairobi securities exchange. European Scientific Journal,

ESJ. 13(11).

Zhang, K. and et.al, 2015. A comparison and evaluation of key performance indicator-based

multivariate statistics process monitoring approaches. Journal of Process Control. 33.

pp.112-126.

ONLINE

10

Books and Journals

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society .47. pp.1-13.

Chiwamit, P., Modell, S. and Scapens, R. W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31. pp.10-30.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Narasimhan, M. S., 2017. Variance Analysis: General Framework.

Nielsen, L. B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1,

pp. 64-82). Elsevier.

Podgórski, D., 2015. Measuring operational performance of OSH management system–A

demonstration of AHP-based selection of leading key performance indicators. Safety

science. 73. pp.146-166.

Wachira, M., 2017. Determinants of corporate social disclosures in Kenya: A longitudinal study

of firms listed on the Nairobi securities exchange. European Scientific Journal,

ESJ. 13(11).

Zhang, K. and et.al, 2015. A comparison and evaluation of key performance indicator-based

multivariate statistics process monitoring approaches. Journal of Process Control. 33.

pp.112-126.

ONLINE

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.