Management Accounting Report for Babcock International

VerifiedAdded on 2021/01/02

|22

|5466

|438

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role in decision-making, planning, and control within Babcock International Ltd. It explores various management accounting systems, including job costing and price optimization, and their impact on internal reporting. The report delves into different management accounting reports, such as budget reports, accounts receivable aging reports, and performance reports, highlighting their significance for internal stakeholders. Furthermore, it presents detailed income statements under both marginal and absorption costing methods for two periods, along with interpretations of the financial data. The analysis includes discussions on the advantages and disadvantages of different costing techniques and their implications for financial performance. The report also covers different planning tools and management accounting tools that can be utilized to solve financial problems and ensure financial stability. Annexes provide supporting data and calculations, making this a valuable resource for understanding the practical applications of management accounting principles.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

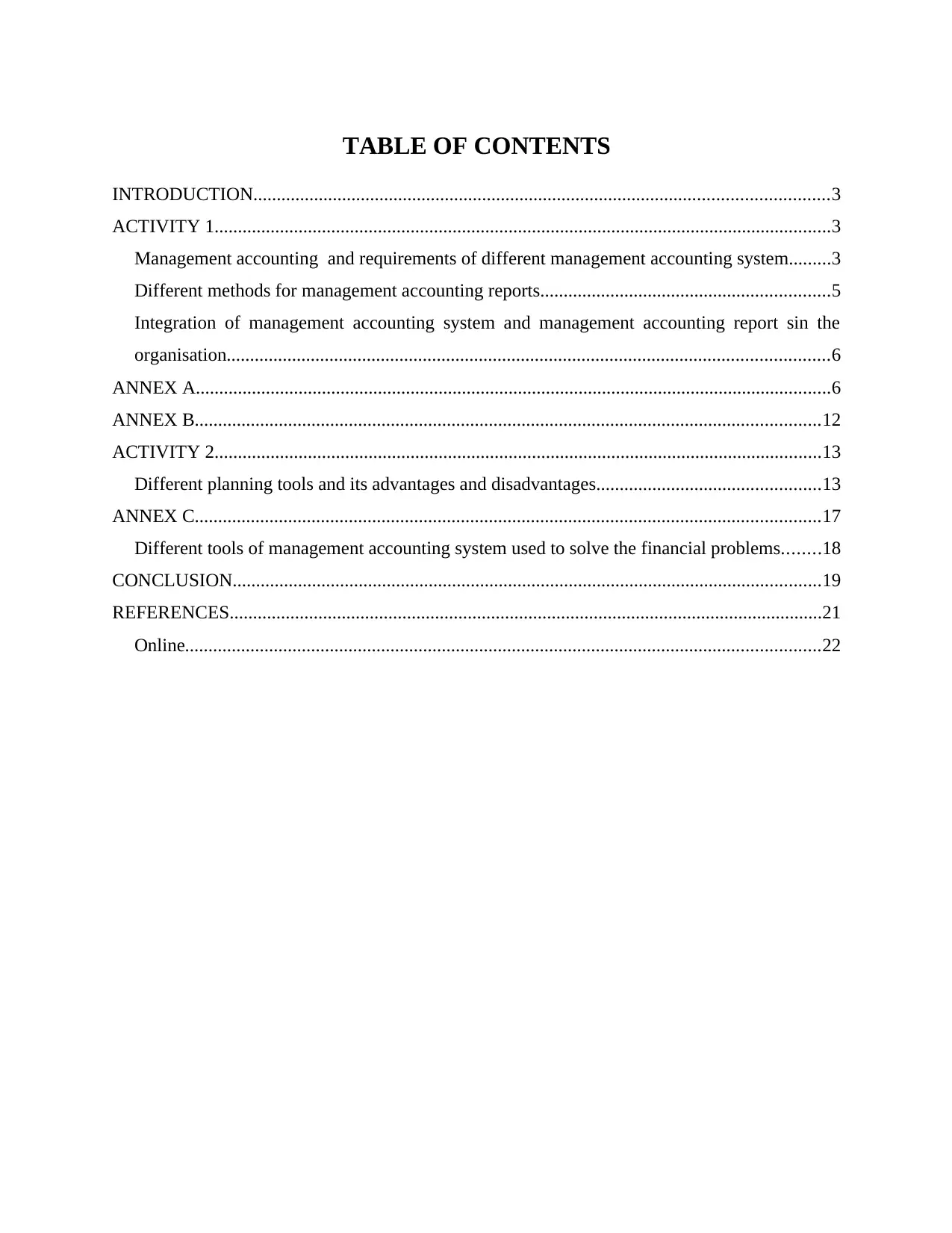

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

Management accounting and requirements of different management accounting system.........3

Different methods for management accounting reports..............................................................5

Integration of management accounting system and management accounting report sin the

organisation.................................................................................................................................6

ANNEX A........................................................................................................................................6

ANNEX B......................................................................................................................................12

ACTIVITY 2..................................................................................................................................13

Different planning tools and its advantages and disadvantages................................................13

ANNEX C......................................................................................................................................17

Different tools of management accounting system used to solve the financial problems........18

CONCLUSION..............................................................................................................................19

REFERENCES...............................................................................................................................21

Online........................................................................................................................................22

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

Management accounting and requirements of different management accounting system.........3

Different methods for management accounting reports..............................................................5

Integration of management accounting system and management accounting report sin the

organisation.................................................................................................................................6

ANNEX A........................................................................................................................................6

ANNEX B......................................................................................................................................12

ACTIVITY 2..................................................................................................................................13

Different planning tools and its advantages and disadvantages................................................13

ANNEX C......................................................................................................................................17

Different tools of management accounting system used to solve the financial problems........18

CONCLUSION..............................................................................................................................19

REFERENCES...............................................................................................................................21

Online........................................................................................................................................22

INTRODUCTION

Management accounting is the accounting which helps the managers in decision making

and it includes planning, decision making. management accounting system helps in preparation

of reports which is used by the internal stakeholders of the company.

Babcock International Ltd is the multinational business or corporation which is UK based

company . The company is specialised in managing the complex infrastructure and assets. this

also provides the skilled and engineering services which helps customers to improve their

performance with reduction ion costs.

The present study includes different types of Management accounting system and reports

which helps the managers in aiding decision making. Computation of income statement using

different costing techniques will also be explained in the report.

Furthermore, the report will include different planning tools and management accounting

tools which will helps the organisation in solving their financial problems and ensuring financial

stability.

ACTIVITY 1

Management accounting and requirements of different management accounting system

Management accounting is considered to be the accounting which involves partnership

of the management decision making, planning and performing the management systems and it

also leads in providing the expertise in the financial reporting and controlling in order to assist

management in the formation and implementation of the organisation strategy(Yigitbasioglu,

2016).

Management accounting system helps in efficiently preparation of the internal reports

which helps in aiding the managers of Babcock International Ltd to make effective and efficient

decisions. This system involves different systems of accounting which generally involves cos

accounting, job costing system, price optimisation etc( van Helden and Uddin, 2016). which

helps in making different decisions related to different activities in the organisation.

Management accounting plays essential role in the organisation as it performs different

function which includes effective and efficient planning, organisation, controlling and the

decision making . These are considered to be the most important role performed by mangers and

are possible with the efficient implementation of the management accounting systems.

Management accounting is the accounting which helps the managers in decision making

and it includes planning, decision making. management accounting system helps in preparation

of reports which is used by the internal stakeholders of the company.

Babcock International Ltd is the multinational business or corporation which is UK based

company . The company is specialised in managing the complex infrastructure and assets. this

also provides the skilled and engineering services which helps customers to improve their

performance with reduction ion costs.

The present study includes different types of Management accounting system and reports

which helps the managers in aiding decision making. Computation of income statement using

different costing techniques will also be explained in the report.

Furthermore, the report will include different planning tools and management accounting

tools which will helps the organisation in solving their financial problems and ensuring financial

stability.

ACTIVITY 1

Management accounting and requirements of different management accounting system

Management accounting is considered to be the accounting which involves partnership

of the management decision making, planning and performing the management systems and it

also leads in providing the expertise in the financial reporting and controlling in order to assist

management in the formation and implementation of the organisation strategy(Yigitbasioglu,

2016).

Management accounting system helps in efficiently preparation of the internal reports

which helps in aiding the managers of Babcock International Ltd to make effective and efficient

decisions. This system involves different systems of accounting which generally involves cos

accounting, job costing system, price optimisation etc( van Helden and Uddin, 2016). which

helps in making different decisions related to different activities in the organisation.

Management accounting plays essential role in the organisation as it performs different

function which includes effective and efficient planning, organisation, controlling and the

decision making . These are considered to be the most important role performed by mangers and

are possible with the efficient implementation of the management accounting systems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Some different management accounting system are as follows:

Job costing system

This system is considered to be the method of recording and accumulating the cost or

recording of the cost of a each product or manufacturing job rather than the entire process. With

the help of this method and system , mangers and accountant of the organisation' are able to track

the cots which incurred on each job in order to maintain the data which is used to be relevant

data in the operations of the business(Temelli,2018).

It is the system which helps in monitoring the costs and expenses which are assign to the

manufacturing cost to each of the product and also enables the managers to keep the track of the

job expenses.

Price optimization system

This method is the program or tool which helps the mangers in calculating that how much

demand varies at the different price levels which helps in combing the data and the information

on costs and the level of inventory which helps in recommending the best price to charges in

order to earn improve profits and also to make the most useful and efficient decisions in the

organisation. This method is generally used by the mangers to find out the best price of the goods

and service son order to generate good amount of profit( Sutheewasinnon, Hoque and Nyamori,

2016). This also use the mathematical analysis to determine that the customer's response to

different prices for the company's product and services through using different channels. Price

optimization also helps the business organisation in determining the best price which will help

them in achieving their objectives of maximising operating profit.

Management accounting reports are the reports which are generated by using the data

through financial accounting and is also used for making decisions , controlling and planning

functions. These reports helps the managers and organisation in planning, regulation, controlling,

decision making and also helps in measuring the performance.

These reports are generally different from the financial accounting as these reports helps

the internal stakeholders by providing them useful information which helps them in adding the

decision making and it also emphasis on the planning and controlling purpose( Schaltegger and

Burritt, 2017). This reports are basically generated by collecting and tracking the data from

different departments by measuring their performances and also helps in making them present in

more understandable manner .

Job costing system

This system is considered to be the method of recording and accumulating the cost or

recording of the cost of a each product or manufacturing job rather than the entire process. With

the help of this method and system , mangers and accountant of the organisation' are able to track

the cots which incurred on each job in order to maintain the data which is used to be relevant

data in the operations of the business(Temelli,2018).

It is the system which helps in monitoring the costs and expenses which are assign to the

manufacturing cost to each of the product and also enables the managers to keep the track of the

job expenses.

Price optimization system

This method is the program or tool which helps the mangers in calculating that how much

demand varies at the different price levels which helps in combing the data and the information

on costs and the level of inventory which helps in recommending the best price to charges in

order to earn improve profits and also to make the most useful and efficient decisions in the

organisation. This method is generally used by the mangers to find out the best price of the goods

and service son order to generate good amount of profit( Sutheewasinnon, Hoque and Nyamori,

2016). This also use the mathematical analysis to determine that the customer's response to

different prices for the company's product and services through using different channels. Price

optimization also helps the business organisation in determining the best price which will help

them in achieving their objectives of maximising operating profit.

Management accounting reports are the reports which are generated by using the data

through financial accounting and is also used for making decisions , controlling and planning

functions. These reports helps the managers and organisation in planning, regulation, controlling,

decision making and also helps in measuring the performance.

These reports are generally different from the financial accounting as these reports helps

the internal stakeholders by providing them useful information which helps them in adding the

decision making and it also emphasis on the planning and controlling purpose( Schaltegger and

Burritt, 2017). This reports are basically generated by collecting and tracking the data from

different departments by measuring their performances and also helps in making them present in

more understandable manner .

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different methods for management accounting reports

There are different type of management accounting reports which helps the internal

stakeholders of the Babcock International Ltd and some of them, are as follows:

Budget reports

Budge reports are considered to be the most essential reports of the organisation as it

helps the business in understanding the costs and expenses of the business and also helps them

to control the costs .this reports help in measuring the performance the company and in large

organisation, individual budget reports are made for each different departments(Otley, 2016).

Company focuses on achieving their goals and objective by matching their actual

performance by budged and through using these reports they are able to know the reasons for the

deviation so that in future they can take corrective measures in order to eliminate the deviations.

this reports help in analysing overall performance of the business for trimming cost and

improving the performance as well.

Account receivable ageing reports

This reports are considered to be the critical tool in the organisation as it helps in

managing the cash flow if they are extending the credit to the customer of the business. These

reports generally includes the maintenance of the separate columns for invoices which are 30

days late, 60 and 90 days late and by using these reports it can be helpful for the manger to find

out the problem for company' collection process( Sutheewasinnon, Hoque and Nyamori, 2016).

Through this reports, organisation can make the powerful and tighten policies for the customers

which are unable to pay their debts.

Performance reports

These reports are created by the organisation in order review the performance of the

company and its staff . In large organisation departmental performance are also generated so that

performance and activities scan be measured on the basis of departmental functions. For making

key strategic decisions mangers generally make use of these performance reports(Otley, 2016).

These reports also helps in awarding the individuals of the company on the basis of their

performance reports also helps in finding the reason foe the difference between the actual and

estimated performance in order to make further decision in context to direct the performance on

direction of the achievement of organisational goal( Muda, and et.al.,2017).

There are different type of management accounting reports which helps the internal

stakeholders of the Babcock International Ltd and some of them, are as follows:

Budget reports

Budge reports are considered to be the most essential reports of the organisation as it

helps the business in understanding the costs and expenses of the business and also helps them

to control the costs .this reports help in measuring the performance the company and in large

organisation, individual budget reports are made for each different departments(Otley, 2016).

Company focuses on achieving their goals and objective by matching their actual

performance by budged and through using these reports they are able to know the reasons for the

deviation so that in future they can take corrective measures in order to eliminate the deviations.

this reports help in analysing overall performance of the business for trimming cost and

improving the performance as well.

Account receivable ageing reports

This reports are considered to be the critical tool in the organisation as it helps in

managing the cash flow if they are extending the credit to the customer of the business. These

reports generally includes the maintenance of the separate columns for invoices which are 30

days late, 60 and 90 days late and by using these reports it can be helpful for the manger to find

out the problem for company' collection process( Sutheewasinnon, Hoque and Nyamori, 2016).

Through this reports, organisation can make the powerful and tighten policies for the customers

which are unable to pay their debts.

Performance reports

These reports are created by the organisation in order review the performance of the

company and its staff . In large organisation departmental performance are also generated so that

performance and activities scan be measured on the basis of departmental functions. For making

key strategic decisions mangers generally make use of these performance reports(Otley, 2016).

These reports also helps in awarding the individuals of the company on the basis of their

performance reports also helps in finding the reason foe the difference between the actual and

estimated performance in order to make further decision in context to direct the performance on

direction of the achievement of organisational goal( Muda, and et.al.,2017).

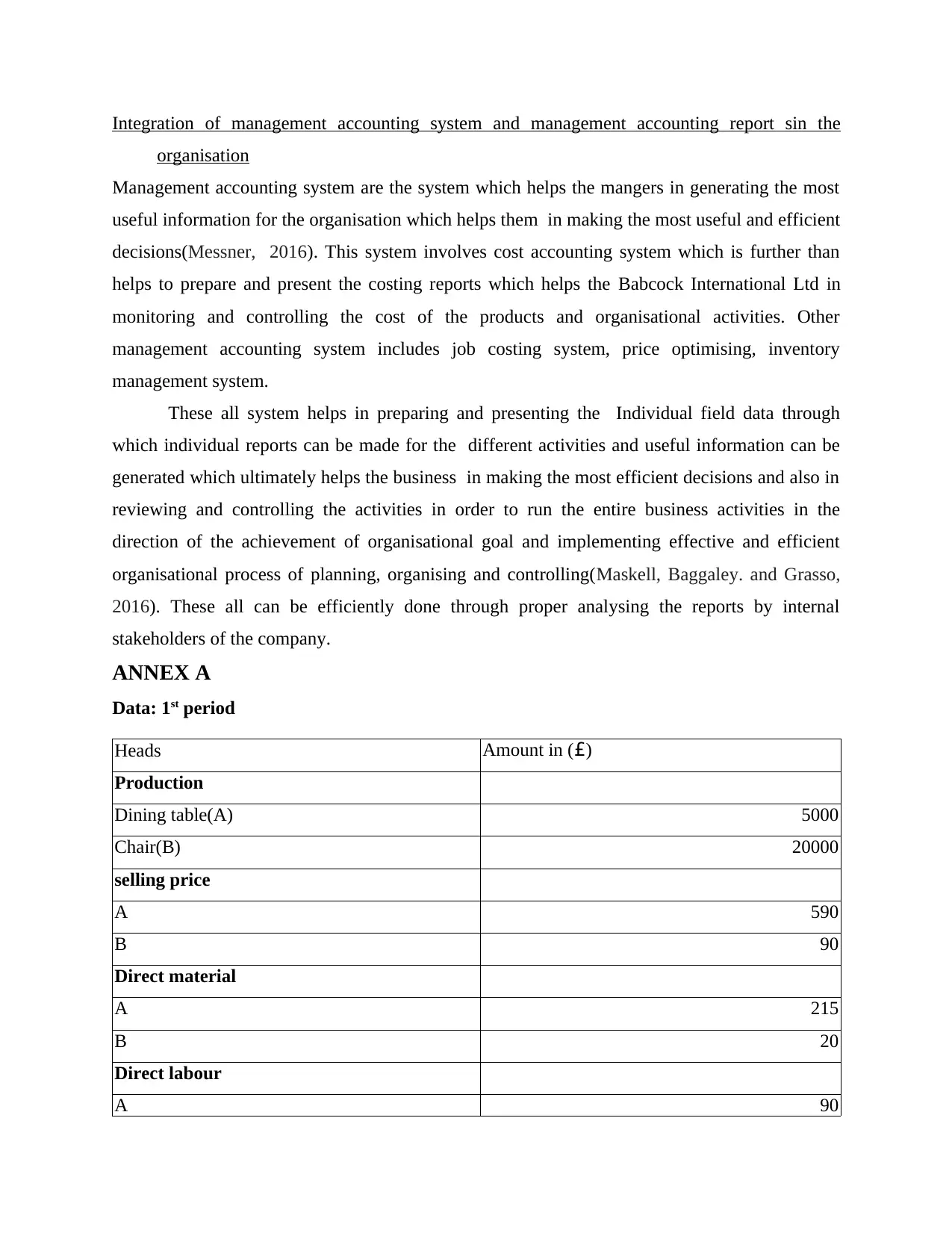

Integration of management accounting system and management accounting report sin the

organisation

Management accounting system are the system which helps the mangers in generating the most

useful information for the organisation which helps them in making the most useful and efficient

decisions(Messner, 2016). This system involves cost accounting system which is further than

helps to prepare and present the costing reports which helps the Babcock International Ltd in

monitoring and controlling the cost of the products and organisational activities. Other

management accounting system includes job costing system, price optimising, inventory

management system.

These all system helps in preparing and presenting the Individual field data through

which individual reports can be made for the different activities and useful information can be

generated which ultimately helps the business in making the most efficient decisions and also in

reviewing and controlling the activities in order to run the entire business activities in the

direction of the achievement of organisational goal and implementing effective and efficient

organisational process of planning, organising and controlling(Maskell, Baggaley. and Grasso,

2016). These all can be efficiently done through proper analysing the reports by internal

stakeholders of the company.

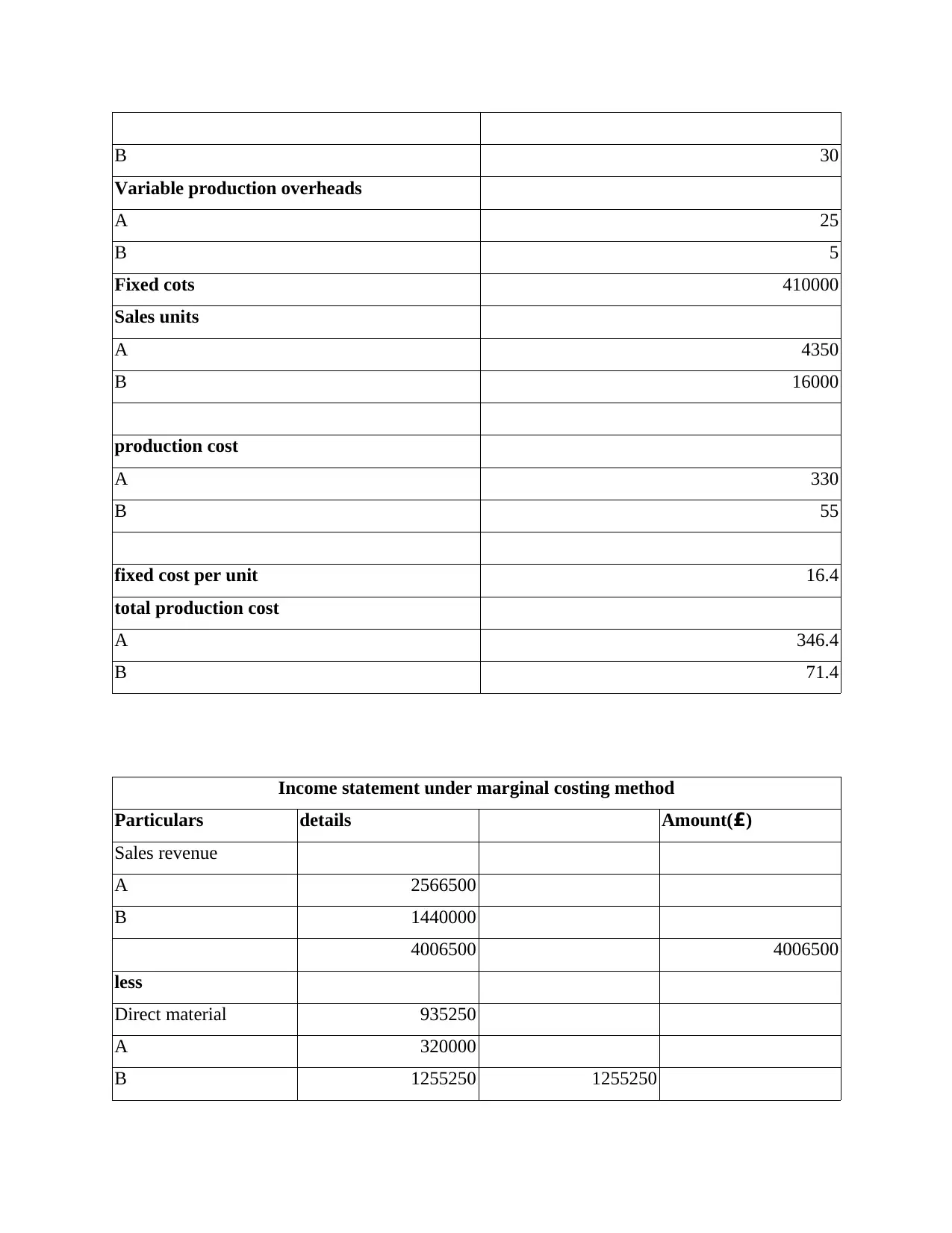

ANNEX A

Data: 1st period

Heads Amount in (£)

Production

Dining table(A) 5000

Chair(B) 20000

selling price

A 590

B 90

Direct material

A 215

B 20

Direct labour

A 90

organisation

Management accounting system are the system which helps the mangers in generating the most

useful information for the organisation which helps them in making the most useful and efficient

decisions(Messner, 2016). This system involves cost accounting system which is further than

helps to prepare and present the costing reports which helps the Babcock International Ltd in

monitoring and controlling the cost of the products and organisational activities. Other

management accounting system includes job costing system, price optimising, inventory

management system.

These all system helps in preparing and presenting the Individual field data through

which individual reports can be made for the different activities and useful information can be

generated which ultimately helps the business in making the most efficient decisions and also in

reviewing and controlling the activities in order to run the entire business activities in the

direction of the achievement of organisational goal and implementing effective and efficient

organisational process of planning, organising and controlling(Maskell, Baggaley. and Grasso,

2016). These all can be efficiently done through proper analysing the reports by internal

stakeholders of the company.

ANNEX A

Data: 1st period

Heads Amount in (£)

Production

Dining table(A) 5000

Chair(B) 20000

selling price

A 590

B 90

Direct material

A 215

B 20

Direct labour

A 90

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B 30

Variable production overheads

A 25

B 5

Fixed cots 410000

Sales units

A 4350

B 16000

production cost

A 330

B 55

fixed cost per unit 16.4

total production cost

A 346.4

B 71.4

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

A 2566500

B 1440000

4006500 4006500

less

Direct material 935250

A 320000

B 1255250 1255250

Variable production overheads

A 25

B 5

Fixed cots 410000

Sales units

A 4350

B 16000

production cost

A 330

B 55

fixed cost per unit 16.4

total production cost

A 346.4

B 71.4

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

A 2566500

B 1440000

4006500 4006500

less

Direct material 935250

A 320000

B 1255250 1255250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

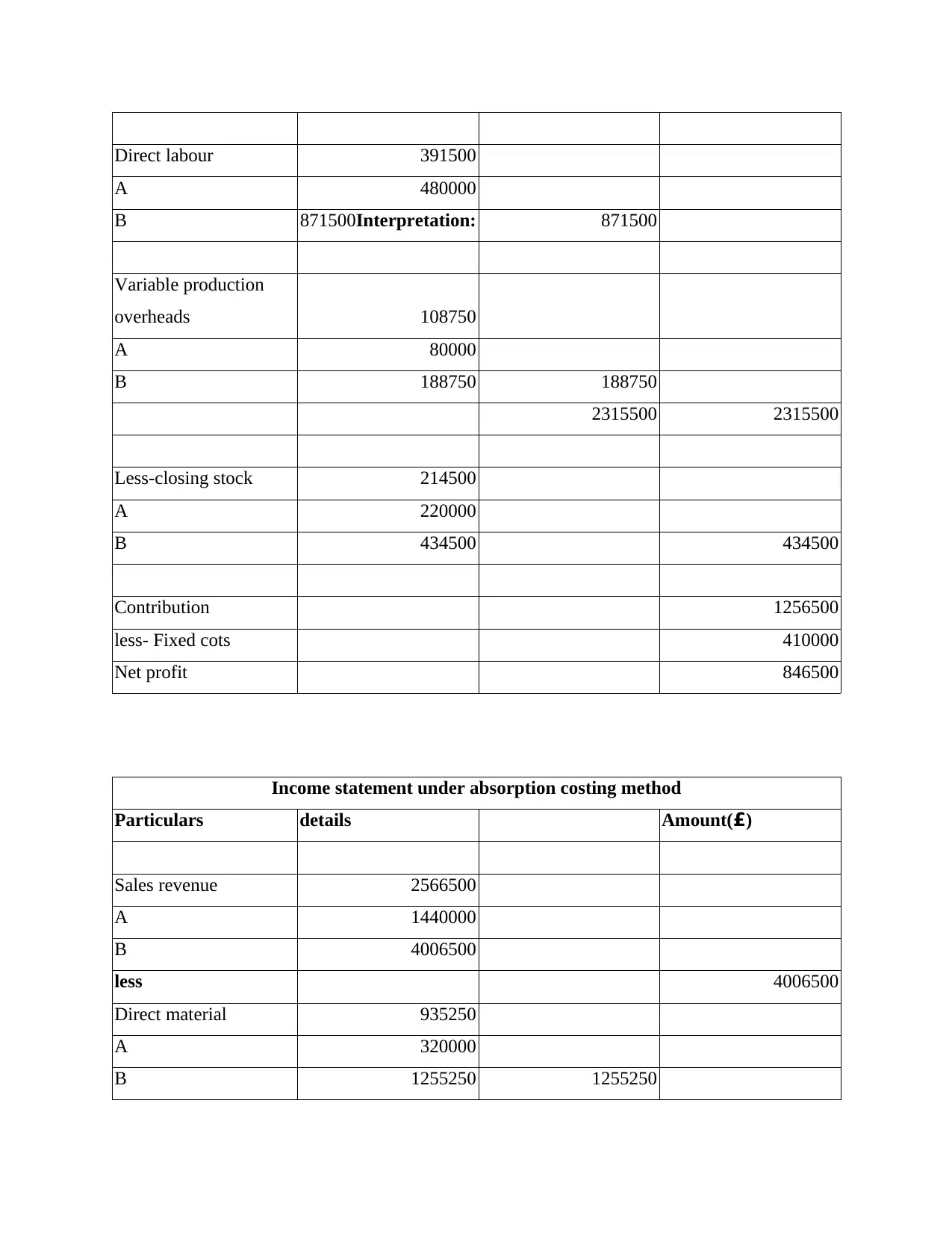

Direct labour 391500

A 480000

B 871500Interpretation: 871500

Variable production

overheads 108750

A 80000

B 188750 188750

2315500 2315500

Less-closing stock 214500

A 220000

B 434500 434500

Contribution 1256500

less- Fixed cots 410000

Net profit 846500

Income statement under absorption costing method

Particulars details Amount(£)

Sales revenue 2566500

A 1440000

B 4006500

less 4006500

Direct material 935250

A 320000

B 1255250 1255250

A 480000

B 871500Interpretation: 871500

Variable production

overheads 108750

A 80000

B 188750 188750

2315500 2315500

Less-closing stock 214500

A 220000

B 434500 434500

Contribution 1256500

less- Fixed cots 410000

Net profit 846500

Income statement under absorption costing method

Particulars details Amount(£)

Sales revenue 2566500

A 1440000

B 4006500

less 4006500

Direct material 935250

A 320000

B 1255250 1255250

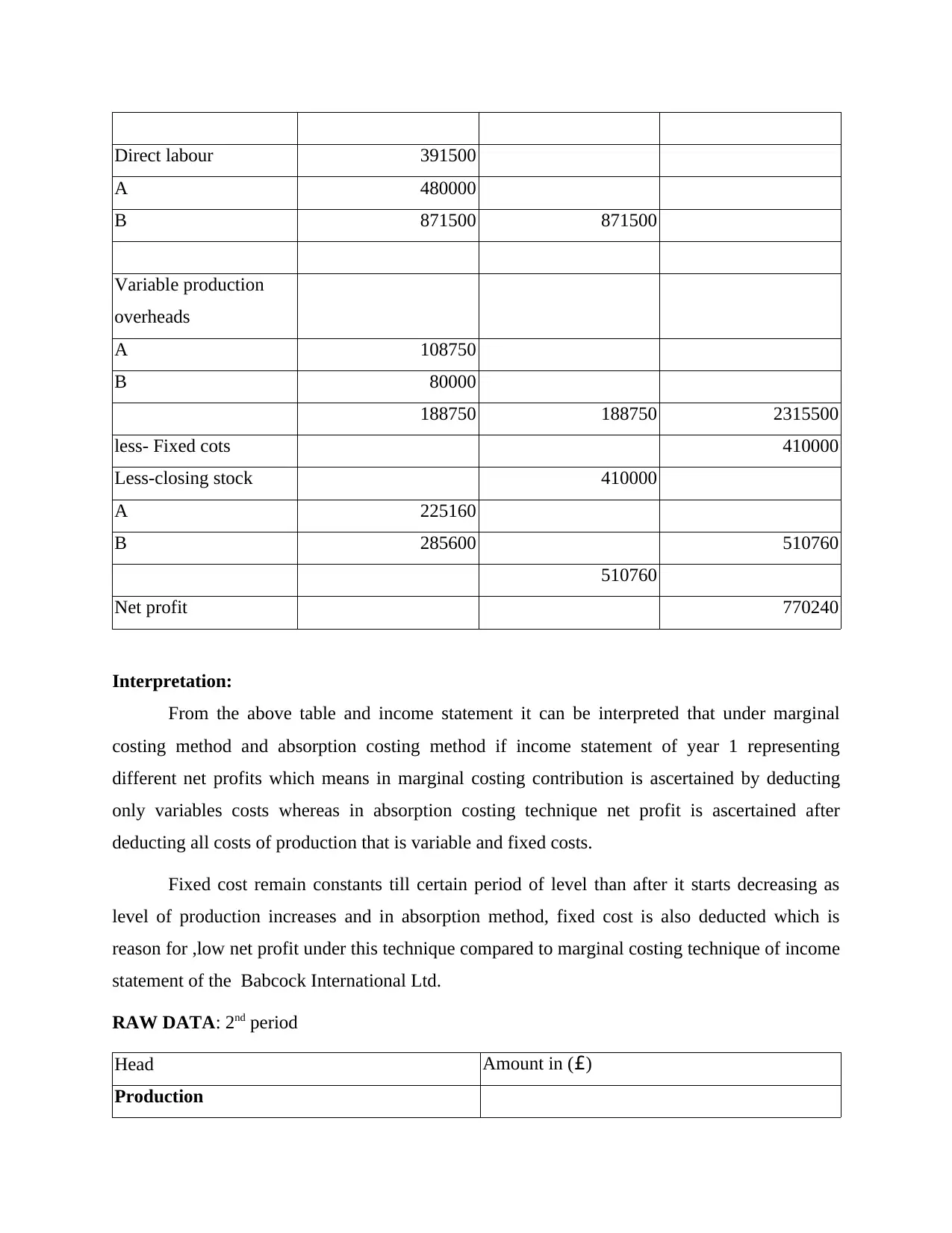

Direct labour 391500

A 480000

B 871500 871500

Variable production

overheads

A 108750

B 80000

188750 188750 2315500

less- Fixed cots 410000

Less-closing stock 410000

A 225160

B 285600 510760

510760

Net profit 770240

Interpretation:

From the above table and income statement it can be interpreted that under marginal

costing method and absorption costing method if income statement of year 1 representing

different net profits which means in marginal costing contribution is ascertained by deducting

only variables costs whereas in absorption costing technique net profit is ascertained after

deducting all costs of production that is variable and fixed costs.

Fixed cost remain constants till certain period of level than after it starts decreasing as

level of production increases and in absorption method, fixed cost is also deducted which is

reason for ,low net profit under this technique compared to marginal costing technique of income

statement of the Babcock International Ltd.

RAW DATA: 2nd period

Head Amount in (£)

Production

A 480000

B 871500 871500

Variable production

overheads

A 108750

B 80000

188750 188750 2315500

less- Fixed cots 410000

Less-closing stock 410000

A 225160

B 285600 510760

510760

Net profit 770240

Interpretation:

From the above table and income statement it can be interpreted that under marginal

costing method and absorption costing method if income statement of year 1 representing

different net profits which means in marginal costing contribution is ascertained by deducting

only variables costs whereas in absorption costing technique net profit is ascertained after

deducting all costs of production that is variable and fixed costs.

Fixed cost remain constants till certain period of level than after it starts decreasing as

level of production increases and in absorption method, fixed cost is also deducted which is

reason for ,low net profit under this technique compared to marginal costing technique of income

statement of the Babcock International Ltd.

RAW DATA: 2nd period

Head Amount in (£)

Production

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

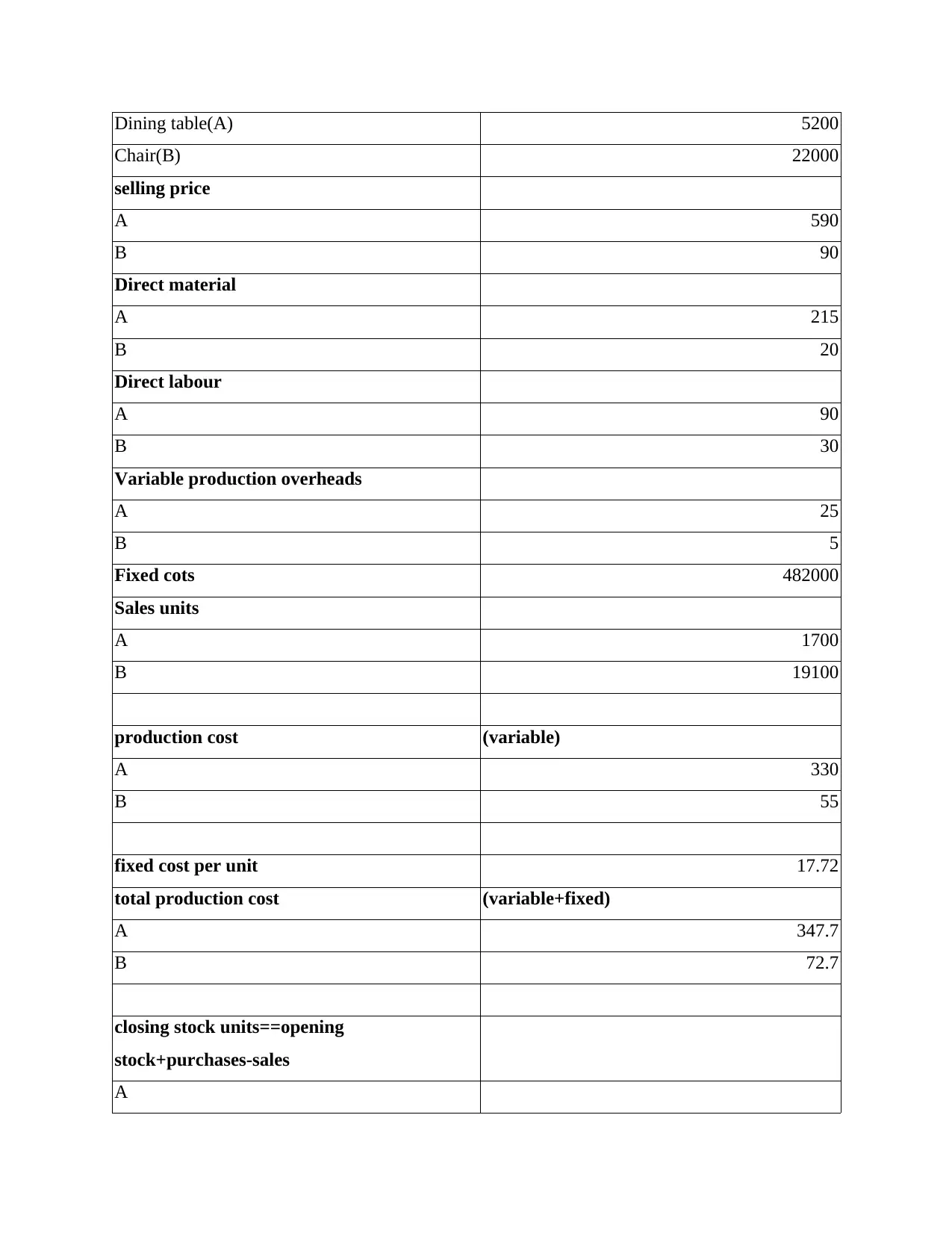

Dining table(A) 5200

Chair(B) 22000

selling price

A 590

B 90

Direct material

A 215

B 20

Direct labour

A 90

B 30

Variable production overheads

A 25

B 5

Fixed cots 482000

Sales units

A 1700

B 19100

production cost (variable)

A 330

B 55

fixed cost per unit 17.72

total production cost (variable+fixed)

A 347.7

B 72.7

closing stock units==opening

stock+purchases-sales

A

Chair(B) 22000

selling price

A 590

B 90

Direct material

A 215

B 20

Direct labour

A 90

B 30

Variable production overheads

A 25

B 5

Fixed cots 482000

Sales units

A 1700

B 19100

production cost (variable)

A 330

B 55

fixed cost per unit 17.72

total production cost (variable+fixed)

A 347.7

B 72.7

closing stock units==opening

stock+purchases-sales

A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

650

4000

opening stock

A 4150

B 6900

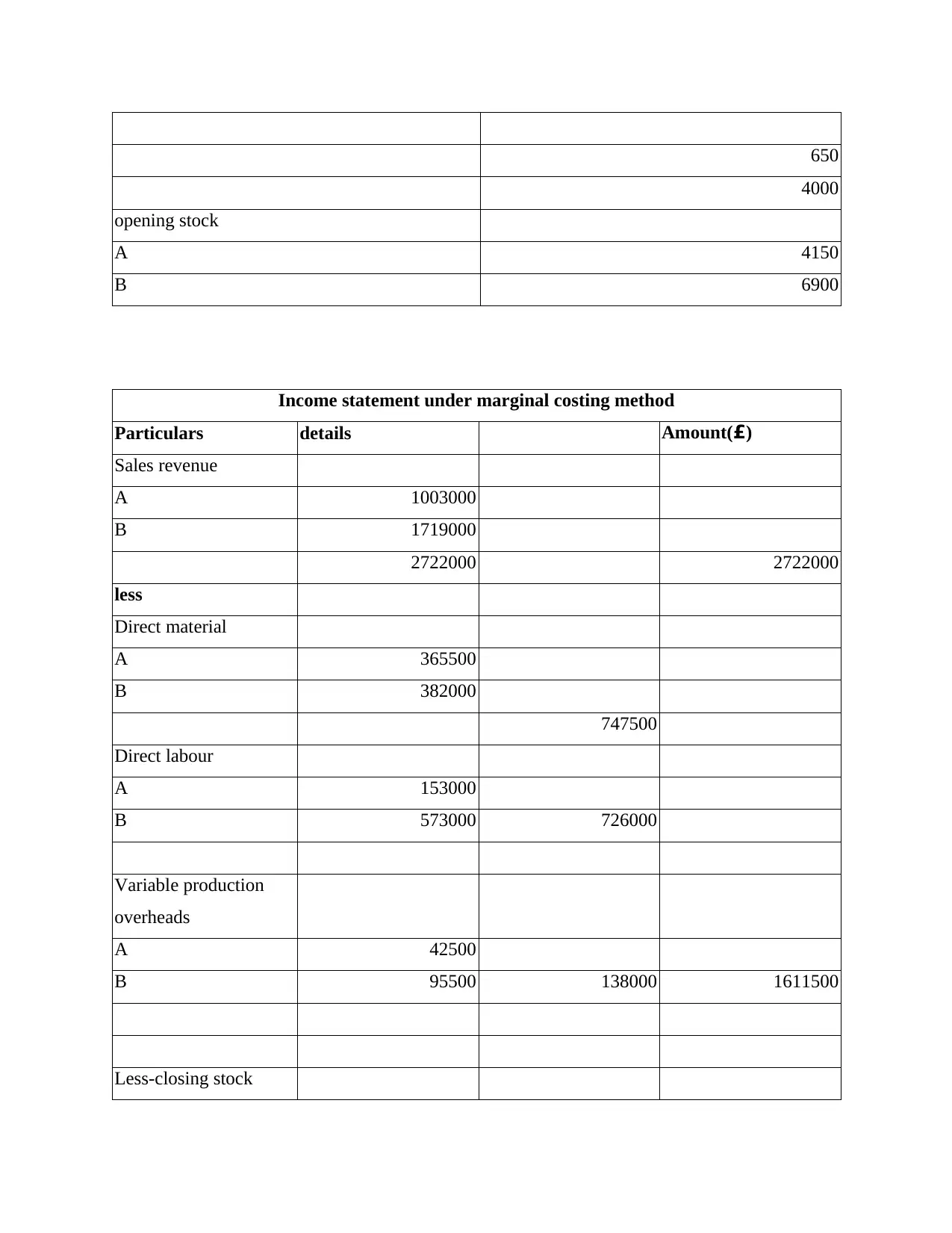

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

A 1003000

B 1719000

2722000 2722000

less

Direct material

A 365500

B 382000

747500

Direct labour

A 153000

B 573000 726000

Variable production

overheads

A 42500

B 95500 138000 1611500

Less-closing stock

4000

opening stock

A 4150

B 6900

Income statement under marginal costing method

Particulars details Amount(£)

Sales revenue

A 1003000

B 1719000

2722000 2722000

less

Direct material

A 365500

B 382000

747500

Direct labour

A 153000

B 573000 726000

Variable production

overheads

A 42500

B 95500 138000 1611500

Less-closing stock

A 1369500

B 379500 1749000 1749000

Contribution -638500

less- Fixed cots 482000 482000

Net loss -1120500

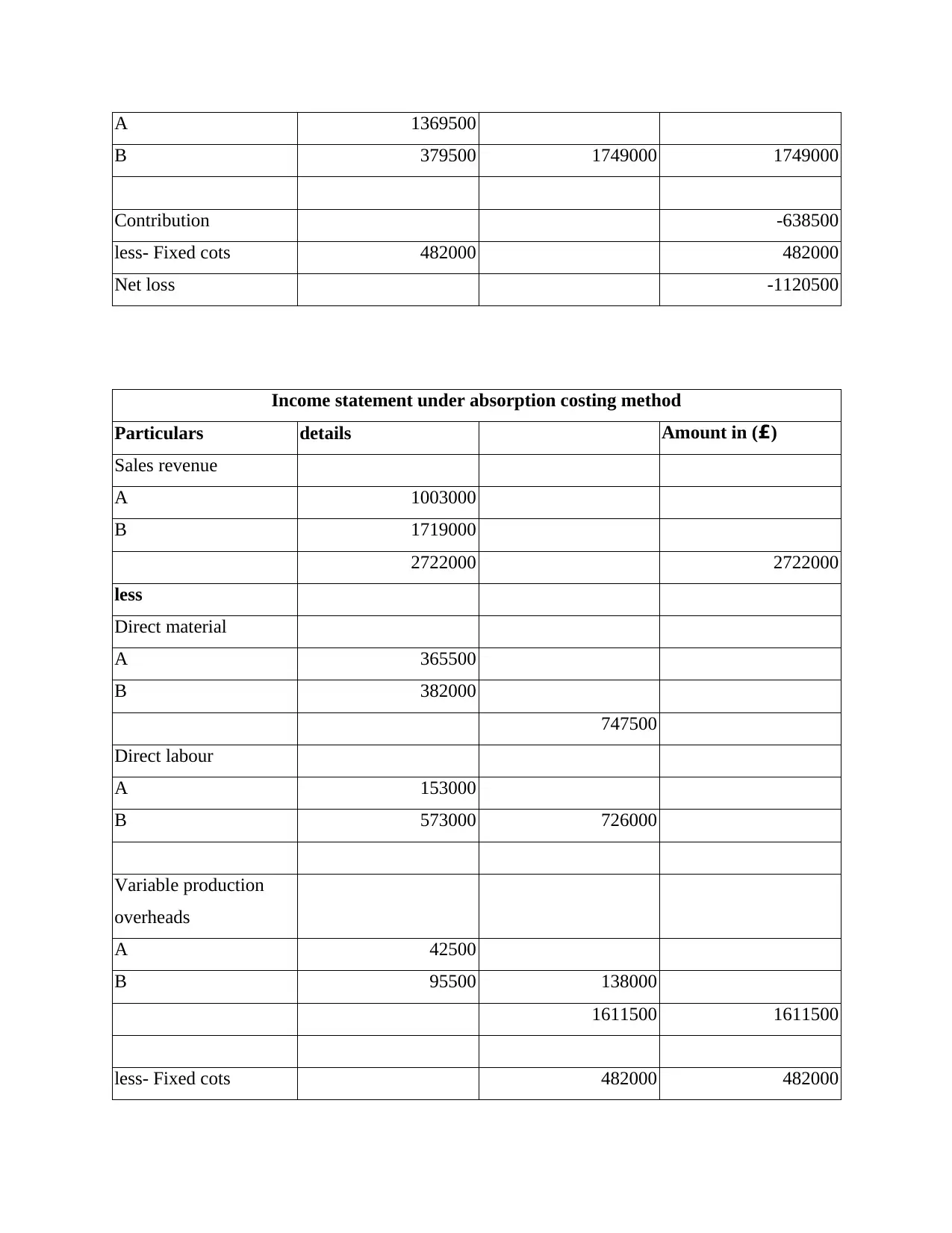

Income statement under absorption costing method

Particulars details Amount in (£)

Sales revenue

A 1003000

B 1719000

2722000 2722000

less

Direct material

A 365500

B 382000

747500

Direct labour

A 153000

B 573000 726000

Variable production

overheads

A 42500

B 95500 138000

1611500 1611500

less- Fixed cots 482000 482000

B 379500 1749000 1749000

Contribution -638500

less- Fixed cots 482000 482000

Net loss -1120500

Income statement under absorption costing method

Particulars details Amount in (£)

Sales revenue

A 1003000

B 1719000

2722000 2722000

less

Direct material

A 365500

B 382000

747500

Direct labour

A 153000

B 573000 726000

Variable production

overheads

A 42500

B 95500 138000

1611500 1611500

less- Fixed cots 482000 482000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.