Management Accounting Report: Costing and Budgeting for Imda Tech

VerifiedAdded on 2020/02/03

|14

|3916

|44

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application to Imda Tech Ltd (UK). It begins with an introduction to management accounting, differentiating it from financial accounting, and highlighting its importance in managerial decision-making. The report then explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization. It presents income statements using both absorption and marginal costing methods, providing a comparative analysis of these techniques. Furthermore, the report examines different types of budgets, their advantages, and disadvantages, along with the budgeting process itself. Pricing strategies are also discussed. The report concludes with an examination of the balance scorecard and performance measures, both financial and non-financial, and offers insights into improving financial governance and developing effective strategies for the company. This report provides a comprehensive overview of management accounting concepts and their practical application.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Management Accounting definition and difference between management account and

financial account..............................................................................................................................4

TASK 2.................................................................................................................................................6

2.1 Absorptions Costing...................................................................................................................6

2.2 Marginal costing .......................................................................................................................7

TASK 3 ................................................................................................................................................8

3.1 Different type of Budget and their advantages and disadvantages............................................8

3.2 Process of preparing budget.....................................................................................................10

3.3 Pricing Strategies.....................................................................................................................10

TASK 4...............................................................................................................................................11

4.1 Balance Score card and performance measure (financial and Non financial).........................11

4.2 Improvement in financial governance and development of strategies....................................12

CONCLUSION..................................................................................................................................12

References..........................................................................................................................................14

2

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Management Accounting definition and difference between management account and

financial account..............................................................................................................................4

TASK 2.................................................................................................................................................6

2.1 Absorptions Costing...................................................................................................................6

2.2 Marginal costing .......................................................................................................................7

TASK 3 ................................................................................................................................................8

3.1 Different type of Budget and their advantages and disadvantages............................................8

3.2 Process of preparing budget.....................................................................................................10

3.3 Pricing Strategies.....................................................................................................................10

TASK 4...............................................................................................................................................11

4.1 Balance Score card and performance measure (financial and Non financial).........................11

4.2 Improvement in financial governance and development of strategies....................................12

CONCLUSION..................................................................................................................................12

References..........................................................................................................................................14

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is accounting techniques used to identifying, measuring, analysing,

interpreting and communicating information for achieving organisational goals (Shiller, R. J. 2013).

It is process of analysing interpretation an presentation of accounting information collected with the

help of various techniques like cost accounting, auditing, budgeting and in order to assist and help

in taking managerial function and help management to take decisions and making plans and policies

(Sofat, R. & Hiro, P. 2011). So this project is regarding Management accounting reporting Imda

Tech Ltd (UK). So in this report function of management accounting, its importance and decision

making tool for department manager, different type of management accounting system like cost

accounting system, inventory management system, Job costing system and price optimisation

system are explained in study. Further income statement is made for Imda tech Ltd. using

Absorption costing and marginal costing method and different types of budget and their advantages

and disadvantages are explained. The process of preparing budget and pricing strategies, companies

balance score card and its effectiveness and development of effective strategies are made.

TASK 1

1.1 Management Accounting definition and difference between management account and financial

account.

Management Accounting is process of interpreting analysing, presenting of accounts related

information and collected with help of Cost and financial Accounting in order to help management

in taking decision (Rubin, D. B., 2014), making policies and help in day to day operations of

running business. As per Institute of management accounting "Management accounting is

professions that involve partnership and helps management in decision making, and provide

expertise financial reporting and control to assess management in formulation and implementation

of organisational strategies".

Difference between management and financial accounting:

Management accounting gives information to its employees within its internal management

organisation while Financial accounting is made for general outsiders like shareholders and

investors.

Law is required in Financial accounting (FA) while Management accounting (MA) not

require law. Special formats and standard are set for FA by IAS (International Accounting

Standard) in Europe.

FA cover whole organisation while MA may cover departmental function related to cost

4

Management accounting is accounting techniques used to identifying, measuring, analysing,

interpreting and communicating information for achieving organisational goals (Shiller, R. J. 2013).

It is process of analysing interpretation an presentation of accounting information collected with the

help of various techniques like cost accounting, auditing, budgeting and in order to assist and help

in taking managerial function and help management to take decisions and making plans and policies

(Sofat, R. & Hiro, P. 2011). So this project is regarding Management accounting reporting Imda

Tech Ltd (UK). So in this report function of management accounting, its importance and decision

making tool for department manager, different type of management accounting system like cost

accounting system, inventory management system, Job costing system and price optimisation

system are explained in study. Further income statement is made for Imda tech Ltd. using

Absorption costing and marginal costing method and different types of budget and their advantages

and disadvantages are explained. The process of preparing budget and pricing strategies, companies

balance score card and its effectiveness and development of effective strategies are made.

TASK 1

1.1 Management Accounting definition and difference between management account and financial

account.

Management Accounting is process of interpreting analysing, presenting of accounts related

information and collected with help of Cost and financial Accounting in order to help management

in taking decision (Rubin, D. B., 2014), making policies and help in day to day operations of

running business. As per Institute of management accounting "Management accounting is

professions that involve partnership and helps management in decision making, and provide

expertise financial reporting and control to assess management in formulation and implementation

of organisational strategies".

Difference between management and financial accounting:

Management accounting gives information to its employees within its internal management

organisation while Financial accounting is made for general outsiders like shareholders and

investors.

Law is required in Financial accounting (FA) while Management accounting (MA) not

require law. Special formats and standard are set for FA by IAS (International Accounting

Standard) in Europe.

FA cover whole organisation while MA may cover departmental function related to cost

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

centric product.

1.2 Importance of Management Accounting for decision making tool for department manage

Small business owner face many decision everyday(Qin, L. and Linetsky, V., 2017).

Managerial accounting provide data to come on decision of output on basis of decisions which can

improve decision making over long term(Berk, J. & et.al., 2013). Imda tech Ltd can use this tool to

make their business more successful by understanding how management accounting benefits their

business decision process.

Relevant cost analysis: MA information is used by company management to determine what

should be sold and how it should be sailed. For ex. a small businessman may be confuse

whether he need to focus on marketing activities(Gnanapragasam, V.J., 2016) . To execute

this accounting manager analyse the cost that varies between advertising alternative ignoring

common cost for each product. This is called relevant cost analysis that taught in

management accounting subject.

Activity based costing techniques: Once company made decision which product going to

sell, then they decide to whom they sell product (Bhimani, A. and et.al., 2013). By Using

ABC Imda Tech can determine the activities require to produce and service the product line.

ABC is costing technique that finds the activity in organisation and assign cost for each

activity by using resources in all product and service.

Make or buy analysis: A main use of management accounting is to provide information used

in manufacturing(D.B. and Mayer, J., 2009. By using this information they can decide the

buying cost and compare to manufacturing cost. So if cost of manufacturing is less then

buying then they can take decision.

1.3 Different type of Management Accounting System

Cost Accounting (Actual, normal and standard costing): Cost accounting is process of

collecting, record keeping, classify, allocate, summarise and evaluation of various

alternative course of action and controlling cost. Main type of costing is used in managemet

accounting are

Normal costing: It is used to find value of manufacturing goods with actual cost of material, direct

labour cost, and manufacturing overhead. These cost are referred to production cost and used for

cost of goods sold for evaluating of inventories

Standard costing: It value the manufactured product with planned material cost, planned direct

labour and overhead.

Normal Costing: In normal costing, the actual price are used for direct labour and material, and

5

1.2 Importance of Management Accounting for decision making tool for department manage

Small business owner face many decision everyday(Qin, L. and Linetsky, V., 2017).

Managerial accounting provide data to come on decision of output on basis of decisions which can

improve decision making over long term(Berk, J. & et.al., 2013). Imda tech Ltd can use this tool to

make their business more successful by understanding how management accounting benefits their

business decision process.

Relevant cost analysis: MA information is used by company management to determine what

should be sold and how it should be sailed. For ex. a small businessman may be confuse

whether he need to focus on marketing activities(Gnanapragasam, V.J., 2016) . To execute

this accounting manager analyse the cost that varies between advertising alternative ignoring

common cost for each product. This is called relevant cost analysis that taught in

management accounting subject.

Activity based costing techniques: Once company made decision which product going to

sell, then they decide to whom they sell product (Bhimani, A. and et.al., 2013). By Using

ABC Imda Tech can determine the activities require to produce and service the product line.

ABC is costing technique that finds the activity in organisation and assign cost for each

activity by using resources in all product and service.

Make or buy analysis: A main use of management accounting is to provide information used

in manufacturing(D.B. and Mayer, J., 2009. By using this information they can decide the

buying cost and compare to manufacturing cost. So if cost of manufacturing is less then

buying then they can take decision.

1.3 Different type of Management Accounting System

Cost Accounting (Actual, normal and standard costing): Cost accounting is process of

collecting, record keeping, classify, allocate, summarise and evaluation of various

alternative course of action and controlling cost. Main type of costing is used in managemet

accounting are

Normal costing: It is used to find value of manufacturing goods with actual cost of material, direct

labour cost, and manufacturing overhead. These cost are referred to production cost and used for

cost of goods sold for evaluating of inventories

Standard costing: It value the manufactured product with planned material cost, planned direct

labour and overhead.

Normal Costing: In normal costing, the actual price are used for direct labour and material, and

5

only overhead rate are estimated.

Inventory Management system: Inventory management is direction or supervision of non

capitalisation assets , inventory or stock item. Component of supply chain management,

inventory management supervises the flow of goods from manufacture to warehouse and

from these facilities to pint of sale.

Job costing System: Job costing assigns overhead cost such as depreciation on assets and

production equipment t one or more cost methods. At the end of each period the total

amount in each cost is assigned to various opens jobs based on some allocation methods that

general apply.

Price optimisation: It is mathematical tool used by company to know how customer will

respond to different price for the product and service through different channel.

TASK 2

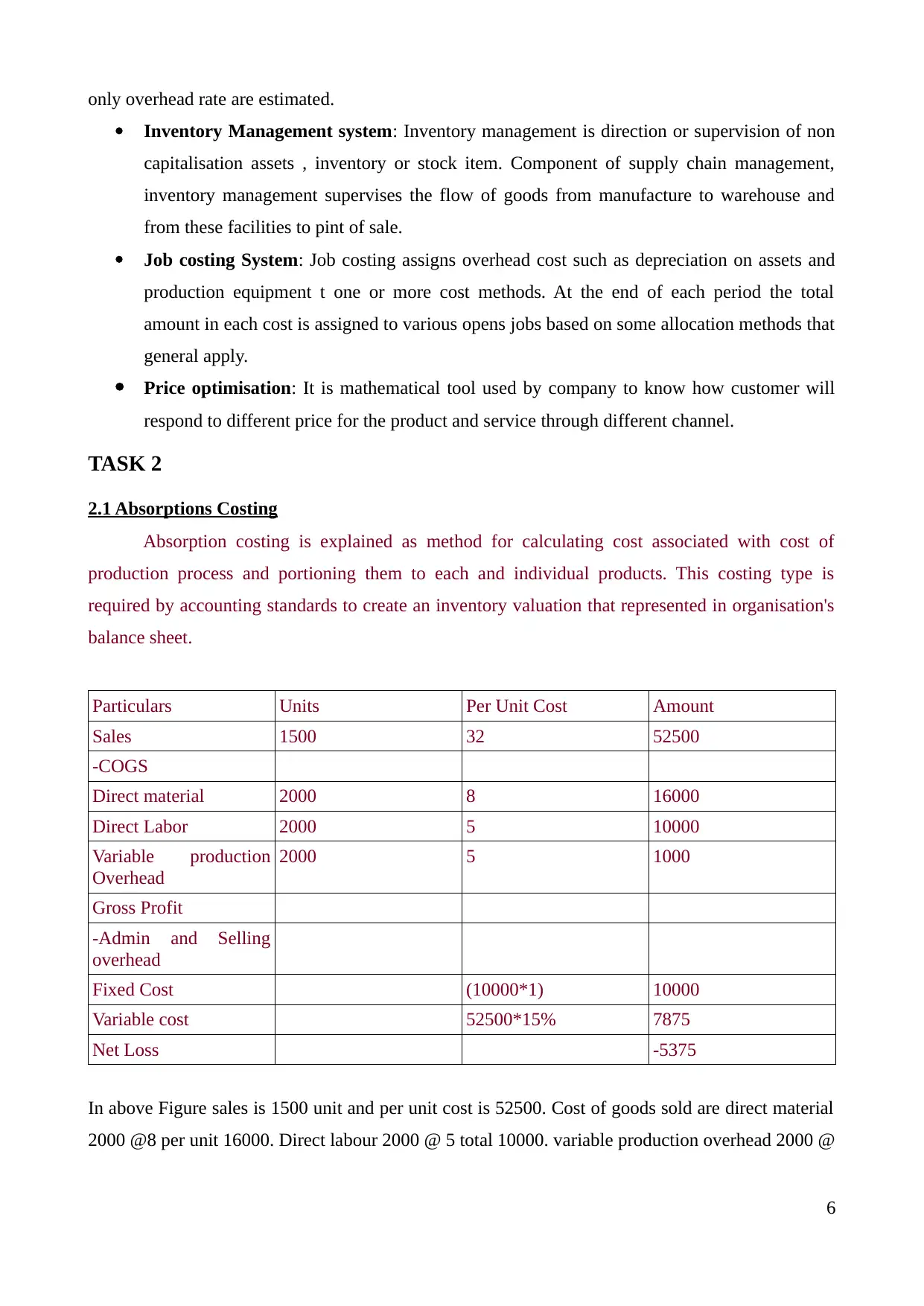

2.1 Absorptions Costing

Absorption costing is explained as method for calculating cost associated with cost of

production process and portioning them to each and individual products. This costing type is

required by accounting standards to create an inventory valuation that represented in organisation's

balance sheet.

Particulars Units Per Unit Cost Amount

Sales 1500 32 52500

-COGS

Direct material 2000 8 16000

Direct Labor 2000 5 10000

Variable production

Overhead

2000 5 1000

Gross Profit

-Admin and Selling

overhead

Fixed Cost (10000*1) 10000

Variable cost 52500*15% 7875

Net Loss -5375

In above Figure sales is 1500 unit and per unit cost is 52500. Cost of goods sold are direct material

2000 @8 per unit 16000. Direct labour 2000 @ 5 total 10000. variable production overhead 2000 @

6

Inventory Management system: Inventory management is direction or supervision of non

capitalisation assets , inventory or stock item. Component of supply chain management,

inventory management supervises the flow of goods from manufacture to warehouse and

from these facilities to pint of sale.

Job costing System: Job costing assigns overhead cost such as depreciation on assets and

production equipment t one or more cost methods. At the end of each period the total

amount in each cost is assigned to various opens jobs based on some allocation methods that

general apply.

Price optimisation: It is mathematical tool used by company to know how customer will

respond to different price for the product and service through different channel.

TASK 2

2.1 Absorptions Costing

Absorption costing is explained as method for calculating cost associated with cost of

production process and portioning them to each and individual products. This costing type is

required by accounting standards to create an inventory valuation that represented in organisation's

balance sheet.

Particulars Units Per Unit Cost Amount

Sales 1500 32 52500

-COGS

Direct material 2000 8 16000

Direct Labor 2000 5 10000

Variable production

Overhead

2000 5 1000

Gross Profit

-Admin and Selling

overhead

Fixed Cost (10000*1) 10000

Variable cost 52500*15% 7875

Net Loss -5375

In above Figure sales is 1500 unit and per unit cost is 52500. Cost of goods sold are direct material

2000 @8 per unit 16000. Direct labour 2000 @ 5 total 10000. variable production overhead 2000 @

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2 is 4000 and fixed production overhead is 2000 @ 5 is 10000. So gross profit is 12500. Selling and

distribution overhead In fixed is 10000 and variable is 52500*15% 7857 and net loss is - 5357

Absorption costing: Absorption costing is type of marginal costing method of expensing all

cost associated with manufacturing a particular product and is required for generally accepted

accounting principle external reporting. Some direct cost that associated with manufacturing a

product include wages for worker physically manufacturing a product and raw material used in

producing goods and all of the overhead cost, such as all utilities cost, used in producing the goods

as a cost base.

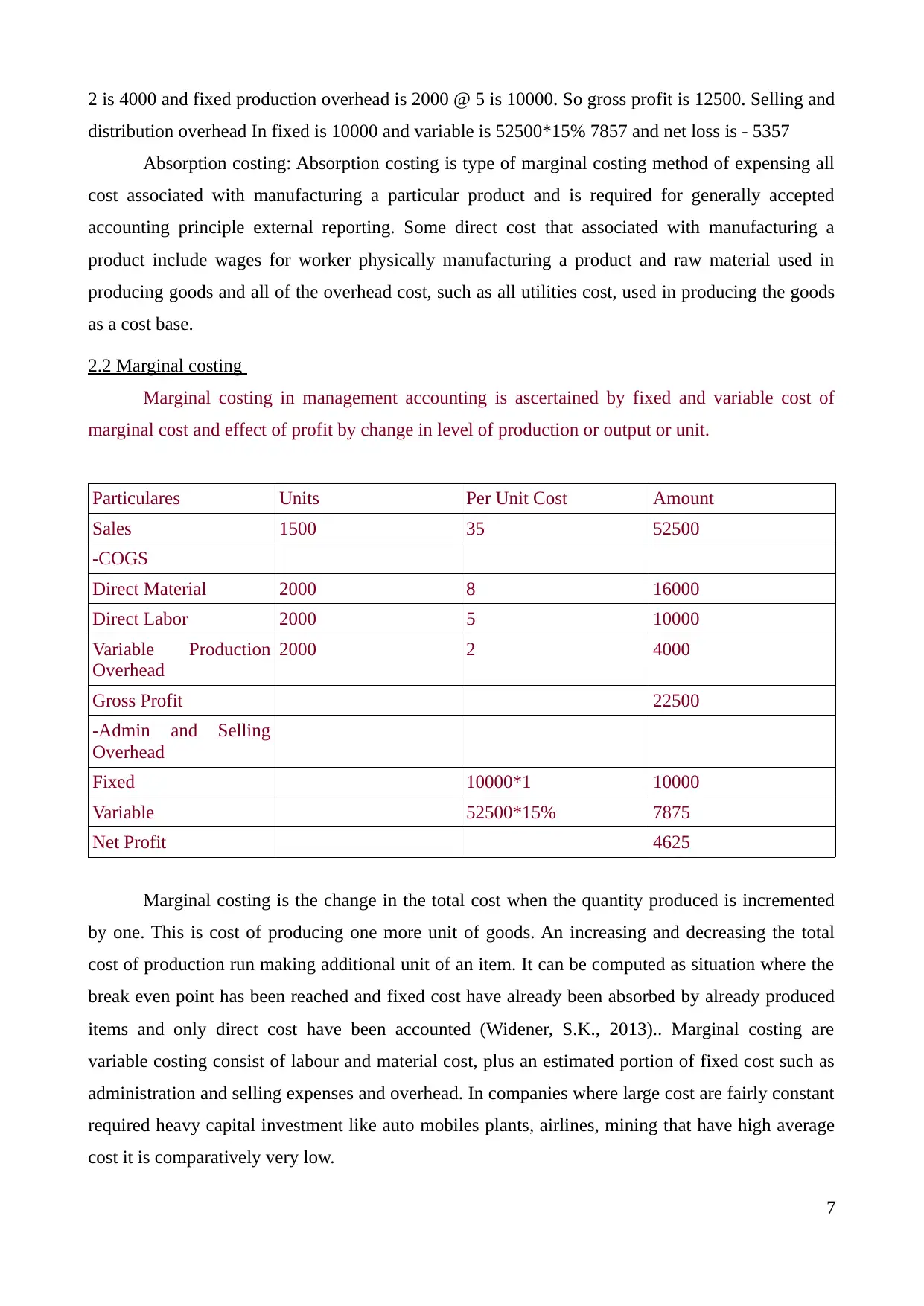

2.2 Marginal costing

Marginal costing in management accounting is ascertained by fixed and variable cost of

marginal cost and effect of profit by change in level of production or output or unit.

Particulares Units Per Unit Cost Amount

Sales 1500 35 52500

-COGS

Direct Material 2000 8 16000

Direct Labor 2000 5 10000

Variable Production

Overhead

2000 2 4000

Gross Profit 22500

-Admin and Selling

Overhead

Fixed 10000*1 10000

Variable 52500*15% 7875

Net Profit 4625

Marginal costing is the change in the total cost when the quantity produced is incremented

by one. This is cost of producing one more unit of goods. An increasing and decreasing the total

cost of production run making additional unit of an item. It can be computed as situation where the

break even point has been reached and fixed cost have already been absorbed by already produced

items and only direct cost have been accounted (Widener, S.K., 2013).. Marginal costing are

variable costing consist of labour and material cost, plus an estimated portion of fixed cost such as

administration and selling expenses and overhead. In companies where large cost are fairly constant

required heavy capital investment like auto mobiles plants, airlines, mining that have high average

cost it is comparatively very low.

7

distribution overhead In fixed is 10000 and variable is 52500*15% 7857 and net loss is - 5357

Absorption costing: Absorption costing is type of marginal costing method of expensing all

cost associated with manufacturing a particular product and is required for generally accepted

accounting principle external reporting. Some direct cost that associated with manufacturing a

product include wages for worker physically manufacturing a product and raw material used in

producing goods and all of the overhead cost, such as all utilities cost, used in producing the goods

as a cost base.

2.2 Marginal costing

Marginal costing in management accounting is ascertained by fixed and variable cost of

marginal cost and effect of profit by change in level of production or output or unit.

Particulares Units Per Unit Cost Amount

Sales 1500 35 52500

-COGS

Direct Material 2000 8 16000

Direct Labor 2000 5 10000

Variable Production

Overhead

2000 2 4000

Gross Profit 22500

-Admin and Selling

Overhead

Fixed 10000*1 10000

Variable 52500*15% 7875

Net Profit 4625

Marginal costing is the change in the total cost when the quantity produced is incremented

by one. This is cost of producing one more unit of goods. An increasing and decreasing the total

cost of production run making additional unit of an item. It can be computed as situation where the

break even point has been reached and fixed cost have already been absorbed by already produced

items and only direct cost have been accounted (Widener, S.K., 2013).. Marginal costing are

variable costing consist of labour and material cost, plus an estimated portion of fixed cost such as

administration and selling expenses and overhead. In companies where large cost are fairly constant

required heavy capital investment like auto mobiles plants, airlines, mining that have high average

cost it is comparatively very low.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal

In marginal costing after calculating direct material, direct labour, variable production and

calculating with Administration and selling overhead like fixed and variable Net profit is gained

4625.

TASK 3

3.1 Different type of Budget and their advantages and disadvantages

Master Budget: Master budget is the aggregation of all lower level budget produced by the

companies various functional areas and also include budgeted financial statement, cash forecasting

and financial planning for business. It is presented in either monthly of quarterly format and usually

cover entire financial year. The budget that include in master budget are Direct labour budget,

Direct material, finished good, Manufacturing overhead, production, sales and Administration

overhead budgets.

Advantages

Functional budget are given in one and available in one report

It can be checked with cross verification of information in master budget

It gives overall estimated profit of the organisation.

It gives information related to forecast balance sheet.

Disadvantages

Time consuming in producing such budget.

It can not be made if company is small and having small staff.

Participative budget: It is budgeting process under which those people are highly involved

who are impacted from budget and with help of them budget is created. So Imda Tech ltd senior

managers have more involvement in taking responsibility of departmental budget. This is bottom up

approach to budgeting tends to create budget that are more achievable then compared to top down

budget that are imposed to achieve target.

Advantages are: Increase in productivity, Job satisfaction, Motivation t o employees, Improved

quality.

Disadvantages are: Make decision making slow down, Securities issue

Zero based budgeting: Is a method of budgeting in which all expenses must be justified for

each new period. Zero based budgeting starts from zero base and every function of organisation is

8

In marginal costing after calculating direct material, direct labour, variable production and

calculating with Administration and selling overhead like fixed and variable Net profit is gained

4625.

TASK 3

3.1 Different type of Budget and their advantages and disadvantages

Master Budget: Master budget is the aggregation of all lower level budget produced by the

companies various functional areas and also include budgeted financial statement, cash forecasting

and financial planning for business. It is presented in either monthly of quarterly format and usually

cover entire financial year. The budget that include in master budget are Direct labour budget,

Direct material, finished good, Manufacturing overhead, production, sales and Administration

overhead budgets.

Advantages

Functional budget are given in one and available in one report

It can be checked with cross verification of information in master budget

It gives overall estimated profit of the organisation.

It gives information related to forecast balance sheet.

Disadvantages

Time consuming in producing such budget.

It can not be made if company is small and having small staff.

Participative budget: It is budgeting process under which those people are highly involved

who are impacted from budget and with help of them budget is created. So Imda Tech ltd senior

managers have more involvement in taking responsibility of departmental budget. This is bottom up

approach to budgeting tends to create budget that are more achievable then compared to top down

budget that are imposed to achieve target.

Advantages are: Increase in productivity, Job satisfaction, Motivation t o employees, Improved

quality.

Disadvantages are: Make decision making slow down, Securities issue

Zero based budgeting: Is a method of budgeting in which all expenses must be justified for

each new period. Zero based budgeting starts from zero base and every function of organisation is

8

analysed for its need and cost. Budget are then made around for upcoming time related to budget is

higher or lower compared to previous period. It allows top level strategy to be followed in

budgeting process by adding all functional area of organisation.

Advantages and disadvantages of Zero based budgeting

Advantages:

It is highly useful for non profit or service organisation

Cost may be saved in inefficient operation

Though resource is allocated on cost benefit analysis it helps in better utilisation of

resources

It ensures careful planing for utilisation of resources

Disadvantages of Zero based Budgeting:

It is time consuming processors

In large scale business organisation number of decision panned tools are made and prepared

which involved expenses

Fixed Budgeting: It is also called as static budget is financial plan based on assumption of

selling specific amount of goods and during period. In other word fixed are based on volume of

sales or revenue. This is an easy way to plan for management for expenses and operations when

they assume that sales revenue and total revenue set amount in during period.

Advantages and disadvantages of Fixed Budgeting

Advantages:

One advantages of static budget is it teacher organisation prioritise. It measures performance

of profit for both short and long term

Fixed budget keep cost down as long as the business abide by strict financial limits planed

on entire business.

Tax simplification, easy to use etc

Disadvantages: One problem with static budget is it does not account for life's unpredictable events,

variable expenses are difficult to predict. So exceeding a budget can cause stress. It is not accurate

way to track expenses. It is difficult to follow if business income varies.

Incremental Budgeting: Incremental budgeting is budgeting tools or technique based on

slight variation from previous period budget result or actual cost. This is common approach of

management where management does not want to involve in much time in formulating budget of

where it does not receive any need to evaluate business. This type of situation occur where there is

not great competition in market and profit expected year to year.

Advantages:

9

higher or lower compared to previous period. It allows top level strategy to be followed in

budgeting process by adding all functional area of organisation.

Advantages and disadvantages of Zero based budgeting

Advantages:

It is highly useful for non profit or service organisation

Cost may be saved in inefficient operation

Though resource is allocated on cost benefit analysis it helps in better utilisation of

resources

It ensures careful planing for utilisation of resources

Disadvantages of Zero based Budgeting:

It is time consuming processors

In large scale business organisation number of decision panned tools are made and prepared

which involved expenses

Fixed Budgeting: It is also called as static budget is financial plan based on assumption of

selling specific amount of goods and during period. In other word fixed are based on volume of

sales or revenue. This is an easy way to plan for management for expenses and operations when

they assume that sales revenue and total revenue set amount in during period.

Advantages and disadvantages of Fixed Budgeting

Advantages:

One advantages of static budget is it teacher organisation prioritise. It measures performance

of profit for both short and long term

Fixed budget keep cost down as long as the business abide by strict financial limits planed

on entire business.

Tax simplification, easy to use etc

Disadvantages: One problem with static budget is it does not account for life's unpredictable events,

variable expenses are difficult to predict. So exceeding a budget can cause stress. It is not accurate

way to track expenses. It is difficult to follow if business income varies.

Incremental Budgeting: Incremental budgeting is budgeting tools or technique based on

slight variation from previous period budget result or actual cost. This is common approach of

management where management does not want to involve in much time in formulating budget of

where it does not receive any need to evaluate business. This type of situation occur where there is

not great competition in market and profit expected year to year.

Advantages:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Simplicity: Simplicity of incremental budgeting is either based on recent financial results

that can be verified.

Funding Stability: If company require funding for multiple year in regard to certain outcome

incremental budgeting is made to keep flow in business.

It also provide operational ability to make stable all functions of all department in long term

and stable manner.

Disadvantages: Incremental in nature, Variance from actual result, Perceptual resource allocation,

Risk taking etc.

3.2 Process of preparing budget

Making assumptions: It review the companies business environment that where used as

the basis of last budget and updated as necessary.

Estimation is obtained: Estimation obtained of sales, production, expected cost,

capability of each sub division, unit or department source. The manager are require to

provide estimated of future condition and economy that will empact on company.

Estimation of proper coordination: In most companies budget committee evaluates the

different plans submitted by various companies and its unit to get the potential of plan

with interest of company and to estimate what resources are available for proper

allocation.

Communicating Budget: Communicating budget to affiliated manager and related

department. After individual plans have been approved related to organisational goals

and available resources the budget is communicated to related department. Changes and

modification made should be informed to responsible manager.

Implementation of planed budget: The final budget is presented to manager related to

planed adopted for operational department for upcoming period. The different service

unit are required to facilitate the material, labours, and other resources to cary out

budget.

Reporting Interim process toward budgeted objective: Final step in budgeting process is

performance report are prepared to inform top managers about performance achieved in

term of budgeted figure. For ex. if sales are low because of reduced production it is

advised to increase production.

3.3 Pricing Strategies

It refers to method companies use to price their product and services. So following are price

strategy companies follow

10

that can be verified.

Funding Stability: If company require funding for multiple year in regard to certain outcome

incremental budgeting is made to keep flow in business.

It also provide operational ability to make stable all functions of all department in long term

and stable manner.

Disadvantages: Incremental in nature, Variance from actual result, Perceptual resource allocation,

Risk taking etc.

3.2 Process of preparing budget

Making assumptions: It review the companies business environment that where used as

the basis of last budget and updated as necessary.

Estimation is obtained: Estimation obtained of sales, production, expected cost,

capability of each sub division, unit or department source. The manager are require to

provide estimated of future condition and economy that will empact on company.

Estimation of proper coordination: In most companies budget committee evaluates the

different plans submitted by various companies and its unit to get the potential of plan

with interest of company and to estimate what resources are available for proper

allocation.

Communicating Budget: Communicating budget to affiliated manager and related

department. After individual plans have been approved related to organisational goals

and available resources the budget is communicated to related department. Changes and

modification made should be informed to responsible manager.

Implementation of planed budget: The final budget is presented to manager related to

planed adopted for operational department for upcoming period. The different service

unit are required to facilitate the material, labours, and other resources to cary out

budget.

Reporting Interim process toward budgeted objective: Final step in budgeting process is

performance report are prepared to inform top managers about performance achieved in

term of budgeted figure. For ex. if sales are low because of reduced production it is

advised to increase production.

3.3 Pricing Strategies

It refers to method companies use to price their product and services. So following are price

strategy companies follow

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Penetration pricing: A small company that uses penetration pricing set low price of product

or services in hope of building market share. Primary objective is to gain lots of customer

with low price and then us various marketing strategies to retain them.

Price Skimming: Another type of pricing strategies in which company set high price of

product to quick recover cost of production or advertising cost. Profit is key objective of

Price skimming.

Product life cycle pricing: All product have life span. A product generally grow in different

stages like introduction, growth, maturity and decline stage. During growth small company

keep price high. For ex. with every launch of Apple product it priced high as it have unique

technology and demand.

Price based competitive advantage: Some times happen when company have to lower the

price to of competitors. A competitive based strategies is adopted when there is a little

difference between product in an industry.

Temporary Discount Pricing: Small companies use temporary discount to attract customer

like, coupons, percentage discount on sales, volume purchasing or seasonal price

discounting.

TASK 4

4.1 Balance Score card and performance measure (financial and Non financial)

Balance score cared includes financial measures (these reveals the result of action already

exist) and non financial measures- related to future financial performance. It include external as

well as internal information. It allows managers to look around all business from four important

perspective

Financial perspective: How do they look to share holders. Encourage the identification of a

few relevant high level financial measures. In particular, designs were encouraged to choose

measures that help inform the answer of question. How do Imda Tech company look to their

shareholders. For ex, cash flow, sales growth, operating income return on equity are

measured.

Non Financial Perspective: Rest three are non financial perspective

Internal Business Process: Encourage the identification of measurement of performance that

answer the question what must be produce execute like, cycle time, per unit cost, yield new

product introductory etc.

Innovation and learning: Encourage the identification of measurement that answer the

11

or services in hope of building market share. Primary objective is to gain lots of customer

with low price and then us various marketing strategies to retain them.

Price Skimming: Another type of pricing strategies in which company set high price of

product to quick recover cost of production or advertising cost. Profit is key objective of

Price skimming.

Product life cycle pricing: All product have life span. A product generally grow in different

stages like introduction, growth, maturity and decline stage. During growth small company

keep price high. For ex. with every launch of Apple product it priced high as it have unique

technology and demand.

Price based competitive advantage: Some times happen when company have to lower the

price to of competitors. A competitive based strategies is adopted when there is a little

difference between product in an industry.

Temporary Discount Pricing: Small companies use temporary discount to attract customer

like, coupons, percentage discount on sales, volume purchasing or seasonal price

discounting.

TASK 4

4.1 Balance Score card and performance measure (financial and Non financial)

Balance score cared includes financial measures (these reveals the result of action already

exist) and non financial measures- related to future financial performance. It include external as

well as internal information. It allows managers to look around all business from four important

perspective

Financial perspective: How do they look to share holders. Encourage the identification of a

few relevant high level financial measures. In particular, designs were encouraged to choose

measures that help inform the answer of question. How do Imda Tech company look to their

shareholders. For ex, cash flow, sales growth, operating income return on equity are

measured.

Non Financial Perspective: Rest three are non financial perspective

Internal Business Process: Encourage the identification of measurement of performance that

answer the question what must be produce execute like, cycle time, per unit cost, yield new

product introductory etc.

Innovation and learning: Encourage the identification of measurement that answer the

11

question how can company create value, improve product and innovation. In doing this new

product creativity and design is responsibility of research and development department.

Customer perspective: Encourage the identification of measurement that question what is

important to customer, investor or shareholders. Like Percentage of sales of new product to

distributors, time delivery, important customer share, purchase and ranking by important

customer.

Help in improving Financial problem: By balance score card technique it can improve

financial problems by improving sales growth, which was targeted in sales budget and found in

strategic planning. So Imda tech can improve sales by keeping low price of mobile charger and

equipment and increasing sales in retail outlet. It can increase operating income by cash inflow and

outflow by circulating manufacturing material supply and minimising overheads. By giving

discount also it can increase sales. Attracting new investor can improve financial problem by giving

giving return and percentage of profit.

4.2 Improvement in financial governance and development of strategies

Starting point of producing a balance scorecard is to identifying the strategic requirement for

the success of the firm. More importantly those strategic requirement will related to product,

market, growth and resources and human, intellectual, and capital structure. Imda tech might want

to below cost producer of mobile charger by achieving competitive advantages and selling

undifferentiated product like mobile components at low price than those competitor or business may

have product development strategy to become leader in technology and command a premium like

Apple. For developing strategies and good financial governance Imda tech need to follow following

steps:

Identifying overall objective of Businessman

determine a way to create value

Identify financial strategies and financial perspective

Clarify customer oriented strategies is related to customer perspective

Identify internal process that support strategies is internal related perspective

Identify skill and competencies related to learning growth and perspective

CONCLUSION

From the report, it can be concluded that departmental managers and executives must

analyse their internal business reports and financial statements, so that, proper policies and

strategies can be devised for fuelling successful growth. Besides this, it is founded that participative

12

product creativity and design is responsibility of research and development department.

Customer perspective: Encourage the identification of measurement that question what is

important to customer, investor or shareholders. Like Percentage of sales of new product to

distributors, time delivery, important customer share, purchase and ranking by important

customer.

Help in improving Financial problem: By balance score card technique it can improve

financial problems by improving sales growth, which was targeted in sales budget and found in

strategic planning. So Imda tech can improve sales by keeping low price of mobile charger and

equipment and increasing sales in retail outlet. It can increase operating income by cash inflow and

outflow by circulating manufacturing material supply and minimising overheads. By giving

discount also it can increase sales. Attracting new investor can improve financial problem by giving

giving return and percentage of profit.

4.2 Improvement in financial governance and development of strategies

Starting point of producing a balance scorecard is to identifying the strategic requirement for

the success of the firm. More importantly those strategic requirement will related to product,

market, growth and resources and human, intellectual, and capital structure. Imda tech might want

to below cost producer of mobile charger by achieving competitive advantages and selling

undifferentiated product like mobile components at low price than those competitor or business may

have product development strategy to become leader in technology and command a premium like

Apple. For developing strategies and good financial governance Imda tech need to follow following

steps:

Identifying overall objective of Businessman

determine a way to create value

Identify financial strategies and financial perspective

Clarify customer oriented strategies is related to customer perspective

Identify internal process that support strategies is internal related perspective

Identify skill and competencies related to learning growth and perspective

CONCLUSION

From the report, it can be concluded that departmental managers and executives must

analyse their internal business reports and financial statements, so that, proper policies and

strategies can be devised for fuelling successful growth. Besides this, it is founded that participative

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.