Report on Management Accounting Principles for Imda Tech (UK) Limited

VerifiedAdded on 2020/02/05

|13

|4203

|260

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on Imda Tech (UK) Limited. It begins by defining management accounting and contrasting it with financial accounting, highlighting its importance in decision-making. The report then delves into different management accounting systems, including cost accounting, inventory management, and job costing systems. It explores absorption costing and marginal costing methods, comparing their impact on profitability. Furthermore, the report examines various types of budgets, their advantages, and disadvantages, as well as the budgeting process. The report also covers the Balance Scorecard and its implementation for performance measurement. The report uses the case study of Imda Tech to illustrate the application of these concepts, analyzing financial problems and improvement strategies for effective financial management. The report provides a detailed overview of costing, budgeting, and decision-making tools within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION........................................................................................................................................3

TASK 1.........................................................................................................................................................3

a) Definition of management accounting and difference between management accounting from

financial accounting.................................................................................................................................3

b) Importance of management accounting information as a decision making tool.................................5

c) Types of management accounting system...........................................................................................5

TASK 2 ........................................................................................................................................................6

1. Absorption Costing..............................................................................................................................6

2. Marginal Costing Method....................................................................................................................7

TASK 3.........................................................................................................................................................8

a) Types of budget and there advantage/ disadvantages..........................................................................8

b) Process of preparing budgets...............................................................................................................9

TASK 4.......................................................................................................................................................10

1. Explain balance scorecard and how it can be implemented can deliver a range of performance

measure..................................................................................................................................................10

CONCLUSION..........................................................................................................................................11

REFERENCES...........................................................................................................................................12

INTRODUCTION........................................................................................................................................3

TASK 1.........................................................................................................................................................3

a) Definition of management accounting and difference between management accounting from

financial accounting.................................................................................................................................3

b) Importance of management accounting information as a decision making tool.................................5

c) Types of management accounting system...........................................................................................5

TASK 2 ........................................................................................................................................................6

1. Absorption Costing..............................................................................................................................6

2. Marginal Costing Method....................................................................................................................7

TASK 3.........................................................................................................................................................8

a) Types of budget and there advantage/ disadvantages..........................................................................8

b) Process of preparing budgets...............................................................................................................9

TASK 4.......................................................................................................................................................10

1. Explain balance scorecard and how it can be implemented can deliver a range of performance

measure..................................................................................................................................................10

CONCLUSION..........................................................................................................................................11

REFERENCES...........................................................................................................................................12

INTRODUCTION

Management accounting is a process which helps that managers to manage all the managerial

function that help the organization to accomplish there goals. In management accounting it includes all

the managerial functions such as planning, organizing, staffing and controlling all the activities which

can make smoothing in all organisational activity(Wajeetongratana, 2016). It also help to conduct more

effectively which can help by the effective management accounting. In this way management accounting

is a life blood of any organisation to run there business more effectively and efficiently. In this research

report, it describes the Imda Tech (UK) Limited, who are the producer of the special charger for mobile

and telephone and it also creates different gadgets for retail outlets in the UK.

In this research report, it describes the concept of management accounting and there importance,

and it also make the comparison between the management accounting and financial accounting. It also

describes the importance of management accounting information as a decision making tools in a

department for a department managers. It also explain the different management accounting systems that

helps the departments to make there reports. It also describes the different type to budget and there

advantages and disadvantages, process which enable to prepare a budgets and the pricing strategies of an

organisation. In this report it analysis the financial problems and improvement which are essential in

solving the financial problems in an organisation.

TASK 1

a) Definition of management accounting and difference between management accounting from financial

accounting

To: Imda Limited, Line Manager

From: Management Accounting Officer

Date: 17 May 2017

Subject: Management accounting meaning and its difference from the financial accounting

Management accounting includes the various strategies such as identifying, analysing, recording

and presenting the financial information which is used to making an effective planning, decision and

making an effective control in an organisation process(Vosselman, 2014). Management accounting also

increases the efficiency of an organisation, it also supplies the accounting facts and information and it is

concerned with forecasting of various information.

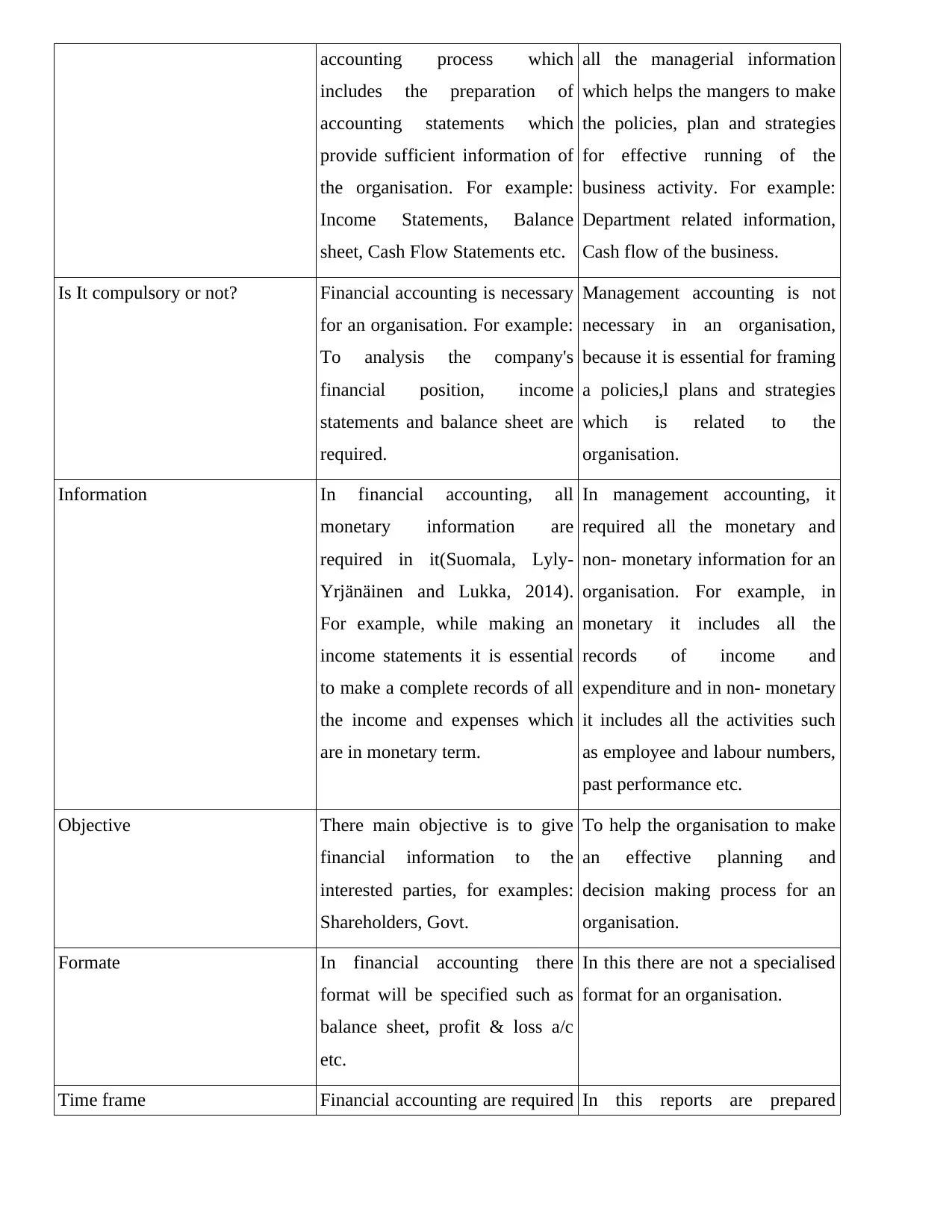

Difference between Financial and Management Accounting

Basis for Comparison Financial Accounting Management Accounting

Meaning Financial accounting is a Management accounting includes

Management accounting is a process which helps that managers to manage all the managerial

function that help the organization to accomplish there goals. In management accounting it includes all

the managerial functions such as planning, organizing, staffing and controlling all the activities which

can make smoothing in all organisational activity(Wajeetongratana, 2016). It also help to conduct more

effectively which can help by the effective management accounting. In this way management accounting

is a life blood of any organisation to run there business more effectively and efficiently. In this research

report, it describes the Imda Tech (UK) Limited, who are the producer of the special charger for mobile

and telephone and it also creates different gadgets for retail outlets in the UK.

In this research report, it describes the concept of management accounting and there importance,

and it also make the comparison between the management accounting and financial accounting. It also

describes the importance of management accounting information as a decision making tools in a

department for a department managers. It also explain the different management accounting systems that

helps the departments to make there reports. It also describes the different type to budget and there

advantages and disadvantages, process which enable to prepare a budgets and the pricing strategies of an

organisation. In this report it analysis the financial problems and improvement which are essential in

solving the financial problems in an organisation.

TASK 1

a) Definition of management accounting and difference between management accounting from financial

accounting

To: Imda Limited, Line Manager

From: Management Accounting Officer

Date: 17 May 2017

Subject: Management accounting meaning and its difference from the financial accounting

Management accounting includes the various strategies such as identifying, analysing, recording

and presenting the financial information which is used to making an effective planning, decision and

making an effective control in an organisation process(Vosselman, 2014). Management accounting also

increases the efficiency of an organisation, it also supplies the accounting facts and information and it is

concerned with forecasting of various information.

Difference between Financial and Management Accounting

Basis for Comparison Financial Accounting Management Accounting

Meaning Financial accounting is a Management accounting includes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting process which

includes the preparation of

accounting statements which

provide sufficient information of

the organisation. For example:

Income Statements, Balance

sheet, Cash Flow Statements etc.

all the managerial information

which helps the mangers to make

the policies, plan and strategies

for effective running of the

business activity. For example:

Department related information,

Cash flow of the business.

Is It compulsory or not? Financial accounting is necessary

for an organisation. For example:

To analysis the company's

financial position, income

statements and balance sheet are

required.

Management accounting is not

necessary in an organisation,

because it is essential for framing

a policies,l plans and strategies

which is related to the

organisation.

Information In financial accounting, all

monetary information are

required in it(Suomala, Lyly-

Yrjänäinen and Lukka, 2014).

For example, while making an

income statements it is essential

to make a complete records of all

the income and expenses which

are in monetary term.

In management accounting, it

required all the monetary and

non- monetary information for an

organisation. For example, in

monetary it includes all the

records of income and

expenditure and in non- monetary

it includes all the activities such

as employee and labour numbers,

past performance etc.

Objective There main objective is to give

financial information to the

interested parties, for examples:

Shareholders, Govt.

To help the organisation to make

an effective planning and

decision making process for an

organisation.

Formate In financial accounting there

format will be specified such as

balance sheet, profit & loss a/c

etc.

In this there are not a specialised

format for an organisation.

Time frame Financial accounting are required In this reports are prepared

includes the preparation of

accounting statements which

provide sufficient information of

the organisation. For example:

Income Statements, Balance

sheet, Cash Flow Statements etc.

all the managerial information

which helps the mangers to make

the policies, plan and strategies

for effective running of the

business activity. For example:

Department related information,

Cash flow of the business.

Is It compulsory or not? Financial accounting is necessary

for an organisation. For example:

To analysis the company's

financial position, income

statements and balance sheet are

required.

Management accounting is not

necessary in an organisation,

because it is essential for framing

a policies,l plans and strategies

which is related to the

organisation.

Information In financial accounting, all

monetary information are

required in it(Suomala, Lyly-

Yrjänäinen and Lukka, 2014).

For example, while making an

income statements it is essential

to make a complete records of all

the income and expenses which

are in monetary term.

In management accounting, it

required all the monetary and

non- monetary information for an

organisation. For example, in

monetary it includes all the

records of income and

expenditure and in non- monetary

it includes all the activities such

as employee and labour numbers,

past performance etc.

Objective There main objective is to give

financial information to the

interested parties, for examples:

Shareholders, Govt.

To help the organisation to make

an effective planning and

decision making process for an

organisation.

Formate In financial accounting there

format will be specified such as

balance sheet, profit & loss a/c

etc.

In this there are not a specialised

format for an organisation.

Time frame Financial accounting are required In this reports are prepared

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

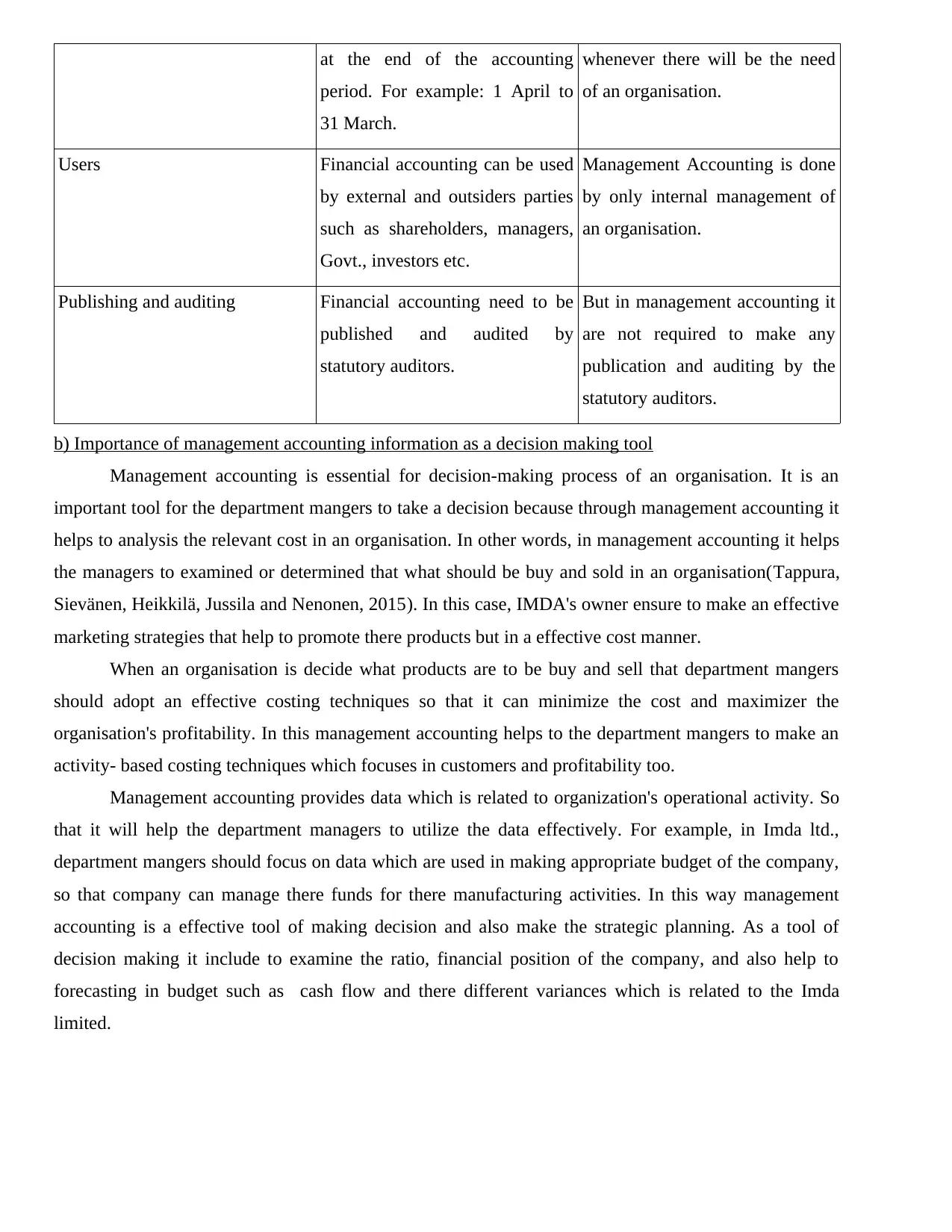

at the end of the accounting

period. For example: 1 April to

31 March.

whenever there will be the need

of an organisation.

Users Financial accounting can be used

by external and outsiders parties

such as shareholders, managers,

Govt., investors etc.

Management Accounting is done

by only internal management of

an organisation.

Publishing and auditing Financial accounting need to be

published and audited by

statutory auditors.

But in management accounting it

are not required to make any

publication and auditing by the

statutory auditors.

b) Importance of management accounting information as a decision making tool

Management accounting is essential for decision-making process of an organisation. It is an

important tool for the department mangers to take a decision because through management accounting it

helps to analysis the relevant cost in an organisation. In other words, in management accounting it helps

the managers to examined or determined that what should be buy and sold in an organisation(Tappura,

Sievänen, Heikkilä, Jussila and Nenonen, 2015). In this case, IMDA's owner ensure to make an effective

marketing strategies that help to promote there products but in a effective cost manner.

When an organisation is decide what products are to be buy and sell that department mangers

should adopt an effective costing techniques so that it can minimize the cost and maximizer the

organisation's profitability. In this management accounting helps to the department mangers to make an

activity- based costing techniques which focuses in customers and profitability too.

Management accounting provides data which is related to organization's operational activity. So

that it will help the department managers to utilize the data effectively. For example, in Imda ltd.,

department mangers should focus on data which are used in making appropriate budget of the company,

so that company can manage there funds for there manufacturing activities. In this way management

accounting is a effective tool of making decision and also make the strategic planning. As a tool of

decision making it include to examine the ratio, financial position of the company, and also help to

forecasting in budget such as cash flow and there different variances which is related to the Imda

limited.

period. For example: 1 April to

31 March.

whenever there will be the need

of an organisation.

Users Financial accounting can be used

by external and outsiders parties

such as shareholders, managers,

Govt., investors etc.

Management Accounting is done

by only internal management of

an organisation.

Publishing and auditing Financial accounting need to be

published and audited by

statutory auditors.

But in management accounting it

are not required to make any

publication and auditing by the

statutory auditors.

b) Importance of management accounting information as a decision making tool

Management accounting is essential for decision-making process of an organisation. It is an

important tool for the department mangers to take a decision because through management accounting it

helps to analysis the relevant cost in an organisation. In other words, in management accounting it helps

the managers to examined or determined that what should be buy and sold in an organisation(Tappura,

Sievänen, Heikkilä, Jussila and Nenonen, 2015). In this case, IMDA's owner ensure to make an effective

marketing strategies that help to promote there products but in a effective cost manner.

When an organisation is decide what products are to be buy and sell that department mangers

should adopt an effective costing techniques so that it can minimize the cost and maximizer the

organisation's profitability. In this management accounting helps to the department mangers to make an

activity- based costing techniques which focuses in customers and profitability too.

Management accounting provides data which is related to organization's operational activity. So

that it will help the department managers to utilize the data effectively. For example, in Imda ltd.,

department mangers should focus on data which are used in making appropriate budget of the company,

so that company can manage there funds for there manufacturing activities. In this way management

accounting is a effective tool of making decision and also make the strategic planning. As a tool of

decision making it include to examine the ratio, financial position of the company, and also help to

forecasting in budget such as cash flow and there different variances which is related to the Imda

limited.

c) Types of management accounting system

Cost Accounting system- Cost accounting system is helps to estimates the cost so that it can

analysis profitability in an organization. For example, cost accounting can help the different departments

by estimating the accurate cost of product which is based on there normal, actual and standard cost. To

make cost accounting, job order costing and process costing can be done to improver the reports by

department mangers. In job order costing, cost can be separated for each job, but in process costing, cost

are separated for each process(Simons, 2013).

Inventory management system- It is a computer- based system which help the organisation for

tracking the level of inventory, orders, sales etc. It also used by creating a order of work, bill for all the

materials and other documents which is related to the purchases. So that different department can

improve there reports by managing there orders, tracking there assets, managing there services,

identifying there products and by optimizing there inventory. For example: wireless tracking, radio-

frequency identification etc. are the tool of inventory management system.

Job costing system- Job costing system is used in organisation when the products which are

manufacture are properly different with each other. For example, department can use job costing to

improve there reports by using custom equipments so that it will track the production costs in each items

or jobs.

Price optimizing system- It is a system in which company can determine that how much

customers can take the prices of the products and services which are rendered by an

organisation(Schaltegger, Gibassier and Zvezdov, 2013). In this way different department can set or

optimizing there prices so that it will maximizes the profitability of the organization. For example: Price

optimizing can be done by the retail, banking, airlines, hotels, insurance industries etc.

TASK 2

1. Absorption Costing

In this method, cost of the product is to be taken into account by indirect expenses as well as

direct costs.

Cost Accounting system- Cost accounting system is helps to estimates the cost so that it can

analysis profitability in an organization. For example, cost accounting can help the different departments

by estimating the accurate cost of product which is based on there normal, actual and standard cost. To

make cost accounting, job order costing and process costing can be done to improver the reports by

department mangers. In job order costing, cost can be separated for each job, but in process costing, cost

are separated for each process(Simons, 2013).

Inventory management system- It is a computer- based system which help the organisation for

tracking the level of inventory, orders, sales etc. It also used by creating a order of work, bill for all the

materials and other documents which is related to the purchases. So that different department can

improve there reports by managing there orders, tracking there assets, managing there services,

identifying there products and by optimizing there inventory. For example: wireless tracking, radio-

frequency identification etc. are the tool of inventory management system.

Job costing system- Job costing system is used in organisation when the products which are

manufacture are properly different with each other. For example, department can use job costing to

improve there reports by using custom equipments so that it will track the production costs in each items

or jobs.

Price optimizing system- It is a system in which company can determine that how much

customers can take the prices of the products and services which are rendered by an

organisation(Schaltegger, Gibassier and Zvezdov, 2013). In this way different department can set or

optimizing there prices so that it will maximizes the profitability of the organization. For example: Price

optimizing can be done by the retail, banking, airlines, hotels, insurance industries etc.

TASK 2

1. Absorption Costing

In this method, cost of the product is to be taken into account by indirect expenses as well as

direct costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

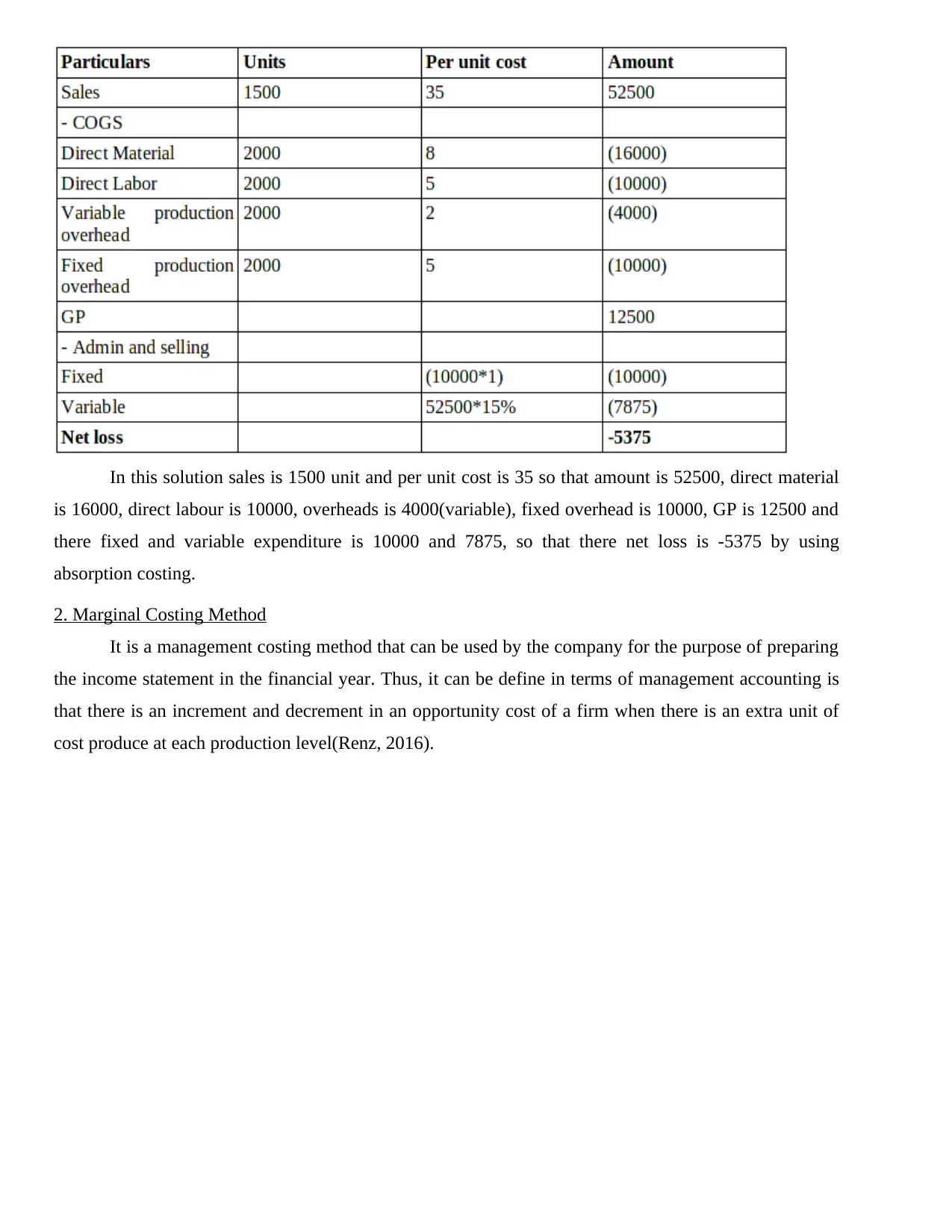

In this solution sales is 1500 unit and per unit cost is 35 so that amount is 52500, direct material

is 16000, direct labour is 10000, overheads is 4000(variable), fixed overhead is 10000, GP is 12500 and

there fixed and variable expenditure is 10000 and 7875, so that there net loss is -5375 by using

absorption costing.

2. Marginal Costing Method

It is a management costing method that can be used by the company for the purpose of preparing

the income statement in the financial year. Thus, it can be define in terms of management accounting is

that there is an increment and decrement in an opportunity cost of a firm when there is an extra unit of

cost produce at each production level(Renz, 2016).

is 16000, direct labour is 10000, overheads is 4000(variable), fixed overhead is 10000, GP is 12500 and

there fixed and variable expenditure is 10000 and 7875, so that there net loss is -5375 by using

absorption costing.

2. Marginal Costing Method

It is a management costing method that can be used by the company for the purpose of preparing

the income statement in the financial year. Thus, it can be define in terms of management accounting is

that there is an increment and decrement in an opportunity cost of a firm when there is an extra unit of

cost produce at each production level(Renz, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

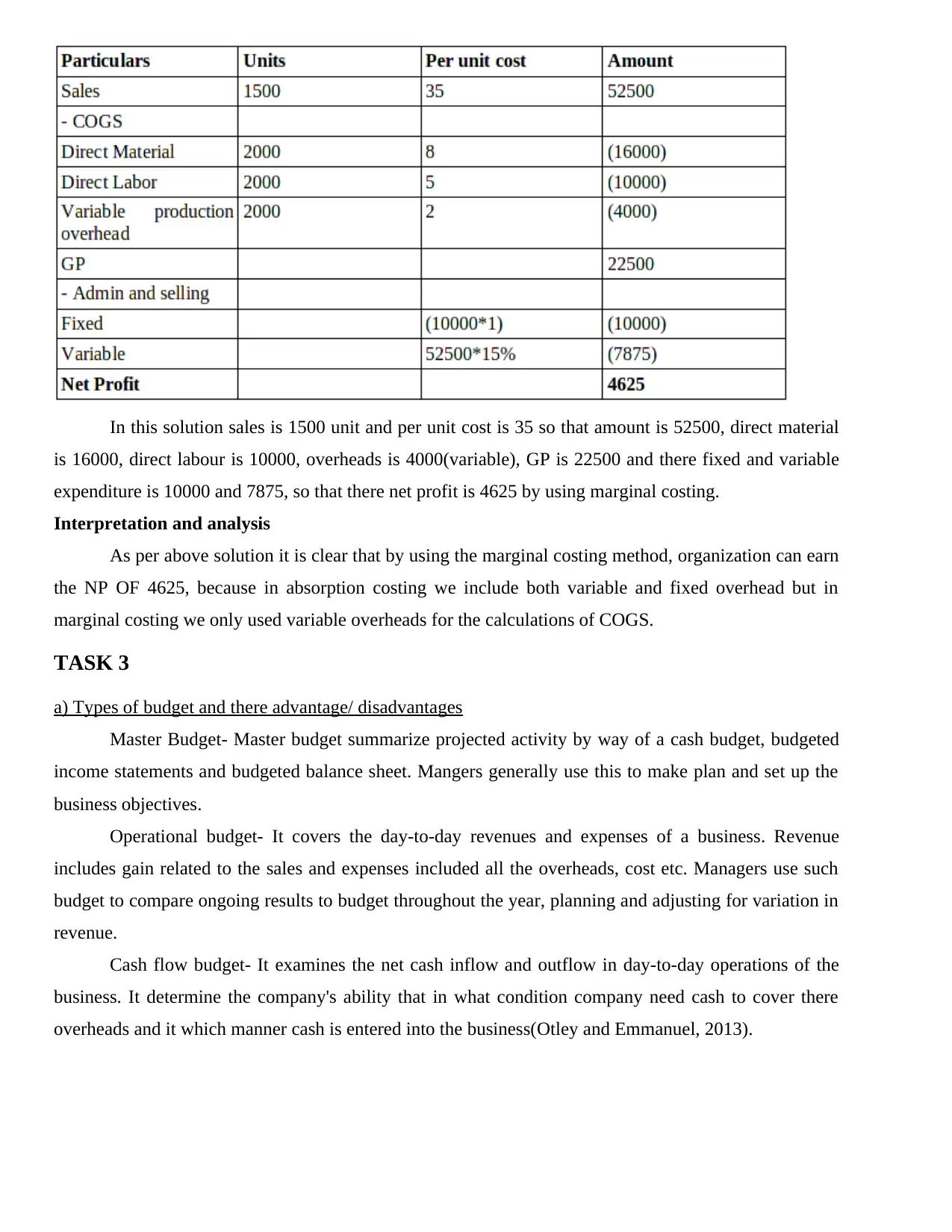

In this solution sales is 1500 unit and per unit cost is 35 so that amount is 52500, direct material

is 16000, direct labour is 10000, overheads is 4000(variable), GP is 22500 and there fixed and variable

expenditure is 10000 and 7875, so that there net profit is 4625 by using marginal costing.

Interpretation and analysis

As per above solution it is clear that by using the marginal costing method, organization can earn

the NP OF 4625, because in absorption costing we include both variable and fixed overhead but in

marginal costing we only used variable overheads for the calculations of COGS.

TASK 3

a) Types of budget and there advantage/ disadvantages

Master Budget- Master budget summarize projected activity by way of a cash budget, budgeted

income statements and budgeted balance sheet. Mangers generally use this to make plan and set up the

business objectives.

Operational budget- It covers the day-to-day revenues and expenses of a business. Revenue

includes gain related to the sales and expenses included all the overheads, cost etc. Managers use such

budget to compare ongoing results to budget throughout the year, planning and adjusting for variation in

revenue.

Cash flow budget- It examines the net cash inflow and outflow in day-to-day operations of the

business. It determine the company's ability that in what condition company need cash to cover there

overheads and it which manner cash is entered into the business(Otley and Emmanuel, 2013).

is 16000, direct labour is 10000, overheads is 4000(variable), GP is 22500 and there fixed and variable

expenditure is 10000 and 7875, so that there net profit is 4625 by using marginal costing.

Interpretation and analysis

As per above solution it is clear that by using the marginal costing method, organization can earn

the NP OF 4625, because in absorption costing we include both variable and fixed overhead but in

marginal costing we only used variable overheads for the calculations of COGS.

TASK 3

a) Types of budget and there advantage/ disadvantages

Master Budget- Master budget summarize projected activity by way of a cash budget, budgeted

income statements and budgeted balance sheet. Mangers generally use this to make plan and set up the

business objectives.

Operational budget- It covers the day-to-day revenues and expenses of a business. Revenue

includes gain related to the sales and expenses included all the overheads, cost etc. Managers use such

budget to compare ongoing results to budget throughout the year, planning and adjusting for variation in

revenue.

Cash flow budget- It examines the net cash inflow and outflow in day-to-day operations of the

business. It determine the company's ability that in what condition company need cash to cover there

overheads and it which manner cash is entered into the business(Otley and Emmanuel, 2013).

Financial budget- Financial budget are made to check business financial requirement that how

much money can spend or receive from there operational activities and how much are required for

making future prediction.

Advantage of budget- Budget is useful for successful business operations. It is useful to identify

the current business performance by using many ideas and techniques. It is a best tool that optimising the

resources so that it can be effectively used. Budget also increases the profitability and productivity of the

firm by using suitable approaches. So that to make a good relationship between employer and employees

a suitable budget are helpful for making effective performance management. So that budget is

considered as essential tool for allocating the assets and funds in an organisation(Lavia López and Hiebl,

2014).

Disadvantage of budget- Wrong estimation of budget make a drawback of effective planning and

operations of a business. Basically budget are made as per the past, future events. But such events are

unpredictable in nature so that it make negative effect in business operational activity. Budget making

process is very costly and time consuming process which need a person who have specific knowledge, so

that it also a disadvantage of budget in a business(Kaplan and Atkinson, 2015).

b) Process of preparing budgets

Update budget assumptions- For preparing a budget, the first step is to updating the assumptions

of budget. In this way management accountant of Imda Ltd. should analysis the assumption so that it

will help to make effective management of performance(Hiebl, 2014). As per the data which are

collected, is helpful to determine the assumption of budget and as per the performance budget can be

update in a business.

Review bottleneck- In this process an organisation can achieved maximum effectiveness,

management should reviewed all the business activities. In this way, organisation capability can be

determined which are suitable for investment and completion of action plan of Imda Limited.

Available funding- After checking all the operations and budget assumption, the next step is that

to determine the funds which are available for successful completion of organisation activity. In this

management of Imda Ltd can identify the net gain and net expenses during the year so that fund can be

allocated effectively.

Obtain revenue forecast and department budget- After creating a budget package, revenue and

function in departments can be forecasted in this stage. For forecasting the department budget, Imda lid

can make a decisions which are made for implementation. In this income of the department and there

performance can be estimated in it. By preparing a action plan are useful for effective allocation of funds

much money can spend or receive from there operational activities and how much are required for

making future prediction.

Advantage of budget- Budget is useful for successful business operations. It is useful to identify

the current business performance by using many ideas and techniques. It is a best tool that optimising the

resources so that it can be effectively used. Budget also increases the profitability and productivity of the

firm by using suitable approaches. So that to make a good relationship between employer and employees

a suitable budget are helpful for making effective performance management. So that budget is

considered as essential tool for allocating the assets and funds in an organisation(Lavia López and Hiebl,

2014).

Disadvantage of budget- Wrong estimation of budget make a drawback of effective planning and

operations of a business. Basically budget are made as per the past, future events. But such events are

unpredictable in nature so that it make negative effect in business operational activity. Budget making

process is very costly and time consuming process which need a person who have specific knowledge, so

that it also a disadvantage of budget in a business(Kaplan and Atkinson, 2015).

b) Process of preparing budgets

Update budget assumptions- For preparing a budget, the first step is to updating the assumptions

of budget. In this way management accountant of Imda Ltd. should analysis the assumption so that it

will help to make effective management of performance(Hiebl, 2014). As per the data which are

collected, is helpful to determine the assumption of budget and as per the performance budget can be

update in a business.

Review bottleneck- In this process an organisation can achieved maximum effectiveness,

management should reviewed all the business activities. In this way, organisation capability can be

determined which are suitable for investment and completion of action plan of Imda Limited.

Available funding- After checking all the operations and budget assumption, the next step is that

to determine the funds which are available for successful completion of organisation activity. In this

management of Imda Ltd can identify the net gain and net expenses during the year so that fund can be

allocated effectively.

Obtain revenue forecast and department budget- After creating a budget package, revenue and

function in departments can be forecasted in this stage. For forecasting the department budget, Imda lid

can make a decisions which are made for implementation. In this income of the department and there

performance can be estimated in it. By preparing a action plan are useful for effective allocation of funds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and resources(Fullerton, Kennedy and Widener, 2014). Hence by follow up above all steps a suitable

budget can be made for the Imda Limited for there successful completion of the activity.

c) Pricing Strategies

Management accountant of Imda Limited set prices of there products for production and

distribution system. In this way they decided there cost as per the demand in market, competition and

product value. In this way pricing strategies which are followed by the Imda Limited that firstly they

decide there cost. In this way, they should determined there factors such as how much material is used in

manufacturing process and production activity(Fullerton, Kennedy and Widener, 2013). This type of

strategies is used for making effective fund allocation in an organisation. To setting up a new pricing

strategy, company should focus in the market position that market was good and in there favour or not.

Company also determined the competitor's position and there pricing strategy that in which price they

sell there products in a market. Company also determined the commercialisation activity such as making

promotion of there product and determining the cost which is charged in promotional activities. In this

way, various tools and techniques are used for setting up a new price of there products. So that company

can make an effective pricing strategy so that it can attract there customers for the products which they

are rendered to the. Company also analysis the market by using trend ratio, regression analysis etc. After

that they can set up a price of there products. In this way all the activities are done only to focus in there

customers and profitability of an organisation(DRURY, 2013).

TASK 4

1. Explain balance scorecard and how it can be implemented can deliver a range of performance measure

It is a process in which government, non-profit organisation, industry and business can use in

managing the system and making an effective strategic planning in an organisation(Cooper, Ezzamel and

Qu, 2017). So that it is most important activity because by which it can make a effective communication

between external and internal factors which affect the organisation. Imda limited using balance scorecard

which contain two type: such as financial and non- financial approach. By using such approach it can

help to measure the investment in suppliers, process, techniques which are used, innovation and

employee etc. So that the two perspectives are:

Non- financial perspective- It include learning and growth perspectives, business process

perspective and customer process perspective. In legal and growth perspective, it include the corporate

culture attitudes, employees training that are related to both corporate self improvement and individual.

In this way this perspective is focus in knowledge of worker and people of firm which considered as

main resources(Brandau, Endenich, Trapp and Hoffjan, 2013). It include the techniques which are

advances as per the environment which are ever changing in nature which play an important role to train

budget can be made for the Imda Limited for there successful completion of the activity.

c) Pricing Strategies

Management accountant of Imda Limited set prices of there products for production and

distribution system. In this way they decided there cost as per the demand in market, competition and

product value. In this way pricing strategies which are followed by the Imda Limited that firstly they

decide there cost. In this way, they should determined there factors such as how much material is used in

manufacturing process and production activity(Fullerton, Kennedy and Widener, 2013). This type of

strategies is used for making effective fund allocation in an organisation. To setting up a new pricing

strategy, company should focus in the market position that market was good and in there favour or not.

Company also determined the competitor's position and there pricing strategy that in which price they

sell there products in a market. Company also determined the commercialisation activity such as making

promotion of there product and determining the cost which is charged in promotional activities. In this

way, various tools and techniques are used for setting up a new price of there products. So that company

can make an effective pricing strategy so that it can attract there customers for the products which they

are rendered to the. Company also analysis the market by using trend ratio, regression analysis etc. After

that they can set up a price of there products. In this way all the activities are done only to focus in there

customers and profitability of an organisation(DRURY, 2013).

TASK 4

1. Explain balance scorecard and how it can be implemented can deliver a range of performance measure

It is a process in which government, non-profit organisation, industry and business can use in

managing the system and making an effective strategic planning in an organisation(Cooper, Ezzamel and

Qu, 2017). So that it is most important activity because by which it can make a effective communication

between external and internal factors which affect the organisation. Imda limited using balance scorecard

which contain two type: such as financial and non- financial approach. By using such approach it can

help to measure the investment in suppliers, process, techniques which are used, innovation and

employee etc. So that the two perspectives are:

Non- financial perspective- It include learning and growth perspectives, business process

perspective and customer process perspective. In legal and growth perspective, it include the corporate

culture attitudes, employees training that are related to both corporate self improvement and individual.

In this way this perspective is focus in knowledge of worker and people of firm which considered as

main resources(Brandau, Endenich, Trapp and Hoffjan, 2013). It include the techniques which are

advances as per the environment which are ever changing in nature which play an important role to train

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

there employees as per the new techniques. So that it can describes that knowledge is more important

and necessary for the success of the business. But in business- perspective, it is also known as internal

business perspective and it help the organisation to running effectively. It also refers that the customers

are satisfied with there products or services. So that in this , all those person are focused in it which have

there unique mission. In customer process perspective, it is basically focus on customer and there

satisfaction which was provided by the different organisation. In this way, if a customers is not satisfied

properly, than organisation has shift to there another suppliers so that they can easily meet there needs in

an effective manner. So that if a company can perform poorly than there is a decline in the future, if the

company have goof financial position.

Financial perspective- In this type of perspective, company have to maintained there funds

because it is main issue which are faced by the finance mangers. So that financial perspective that are

major includes into it is cost- benefit data and risk assessment(Bodie, 2013).

CONCLUSION

The report is concluded that management accounting is an approach of organization by which

general business transaction get managed. Therefore, different management accounting tools are

determined for allocating fund for Imda limited. Including this, costing such as absorption and marginal

is considered for preparing income statement that presents financial position of organization. Moreover,

critical evaluation on budget is presented for forecasting and decision making for further business

operations. In accordance to this, several kinds of budget and its preparation process is considered

through this assignment. However, pricing strategies for setting costs according to different determinants

are described for cost effectiveness as well proper management of entity is recognized. Apart from this,

financial statement analysis is obtained by which current business performance is analysed that is

effective to reduce economic problems occur at workplace. Including this, significance of management

accounting is expressed which is used to improve governance and developing effective strategies at high

level. Thus, through this study, different management accounting tools and systems are presented for

effectiveness of entity and enhancing its financial performance systematically(Armstrong, 2014).

and necessary for the success of the business. But in business- perspective, it is also known as internal

business perspective and it help the organisation to running effectively. It also refers that the customers

are satisfied with there products or services. So that in this , all those person are focused in it which have

there unique mission. In customer process perspective, it is basically focus on customer and there

satisfaction which was provided by the different organisation. In this way, if a customers is not satisfied

properly, than organisation has shift to there another suppliers so that they can easily meet there needs in

an effective manner. So that if a company can perform poorly than there is a decline in the future, if the

company have goof financial position.

Financial perspective- In this type of perspective, company have to maintained there funds

because it is main issue which are faced by the finance mangers. So that financial perspective that are

major includes into it is cost- benefit data and risk assessment(Bodie, 2013).

CONCLUSION

The report is concluded that management accounting is an approach of organization by which

general business transaction get managed. Therefore, different management accounting tools are

determined for allocating fund for Imda limited. Including this, costing such as absorption and marginal

is considered for preparing income statement that presents financial position of organization. Moreover,

critical evaluation on budget is presented for forecasting and decision making for further business

operations. In accordance to this, several kinds of budget and its preparation process is considered

through this assignment. However, pricing strategies for setting costs according to different determinants

are described for cost effectiveness as well proper management of entity is recognized. Apart from this,

financial statement analysis is obtained by which current business performance is analysed that is

effective to reduce economic problems occur at workplace. Including this, significance of management

accounting is expressed which is used to improve governance and developing effective strategies at high

level. Thus, through this study, different management accounting tools and systems are presented for

effectiveness of entity and enhancing its financial performance systematically(Armstrong, 2014).

REFERENCES

Journals and Books

Armstrong, P., 2014. Limits and possibilities for HRM in an age of management accountancy. New

Perspectives On Human Resource Management op. cit. at, pp.154-166.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brandau, M., Endenich, C., Trapp, R. and Hoffjan, A., 2013. Institutional drivers of conformity–

Evidence for management accounting from Brazil and Germany. International Business Review.

22(2). pp.466-479.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea: The case

of the balanced scorecard. Contemporary Accounting Research.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society. 38(1).

pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices. Journal of Operations

Management. 32(7). pp.414-428.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research. Journal of

Management Control,.24(3). pp.223-240.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lavia López, O. and Hiebl, M. R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Morales, J. and Lambert, C., 2013. Dirty work and the construction of identity. An ethnographic study of

management accounting practices. Accounting, Organizations and Society. 38(3). pp.228-244.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control. Springer.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John Wiley &

Sons.

Journals and Books

Armstrong, P., 2014. Limits and possibilities for HRM in an age of management accountancy. New

Perspectives On Human Resource Management op. cit. at, pp.154-166.

Bodie, Z., 2013. Investments. McGraw-Hill.

Brandau, M., Endenich, C., Trapp, R. and Hoffjan, A., 2013. Institutional drivers of conformity–

Evidence for management accounting from Brazil and Germany. International Business Review.

22(2). pp.466-479.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea: The case

of the balanced scorecard. Contemporary Accounting Research.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society. 38(1).

pp.50-71.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm performance:

The incremental contribution of lean management accounting practices. Journal of Operations

Management. 32(7). pp.414-428.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research. Journal of

Management Control,.24(3). pp.223-240.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Lavia López, O. and Hiebl, M. R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Morales, J. and Lambert, C., 2013. Dirty work and the construction of identity. An ethnographic study of

management accounting practices. Accounting, Organizations and Society. 38(3). pp.228-244.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control. Springer.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John Wiley &

Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.