Management Accounting: Introduction, Types, and Techniques Report

VerifiedAdded on 2020/11/12

|21

|5005

|212

Report

AI Summary

This report provides a comprehensive overview of management accounting, beginning with an introduction to the field and its differences from financial accounting. It delves into various cost accounting systems, including standard costing and direct costing, and explores different inventory management systems like job costing. The report also examines the importance of management accounting in financial planning, decision-making, and cost analysis. Furthermore, it details the types of management accounting reports, such as financial reports and budget reports, highlighting their advantages and benefits. The report also covers key costing methods like absorption costing and marginal costing, and the planning tools of budgetary control including sales, cash, and performance budgets. Finally, the report concludes with an analysis of managerial accounting techniques like break-even analysis and cost-profit analysis, used by companies to address financial challenges. This document is a valuable resource for students on Desklib, offering insights into financial analysis and accounting techniques.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

MA is the procedure of preparing the financial reports and documents that analysis the

financial condition of the organisation which help them to undertake their operations according

to those financial statistics. Moreover, the report will highlight about the variation between the

MA and financial accounting and along with it will outline cost accounting systems and their

types namely; direct cost and standard costing. Furthermore, the project will frame about the

various costing system (Calabrò,2017).

On the flip side, the assignment will comment on the types of managerial accounting

reports which is inclusive of cash report, budget report, financial report, performance report etc.

However, the report will outline about the absorption costing and marginal costing including

their advantages and disadvantages and along with it will frame about the three planning tools of

budgetary control namely, sales budget, cash budget, performance budget. Eventually, the

project will frame about the various managerial accounting techniques used by the company to

solve their financial issues like break even analysis, cost profit analysis etc.

LO1

P1 Understanding of MA

Management accounting (MA)

MA, also known as managerial accounting. It is the procedure of studying organisation

expenses and operations to prepare financial file, statistics, and account to support managers’

choice making technique in achieving business objectives. However, it is the method of

preparing monetary and costing information and translating that statistics into beneficial

information for administration and officers within a company (Collis, and Hussey, 2017).

Financial accounting

Financial Accounting is the system of determining, recording, concise and reporting the

infinite of transactions as a result of enterprise operations over a time frame. Further, these

transactions are sum-up in the formulation of financial statements, inclusive of the balance sheet,

earnings assertion and cash flow statement, that document the organization's operating overall

performance over a designated period.

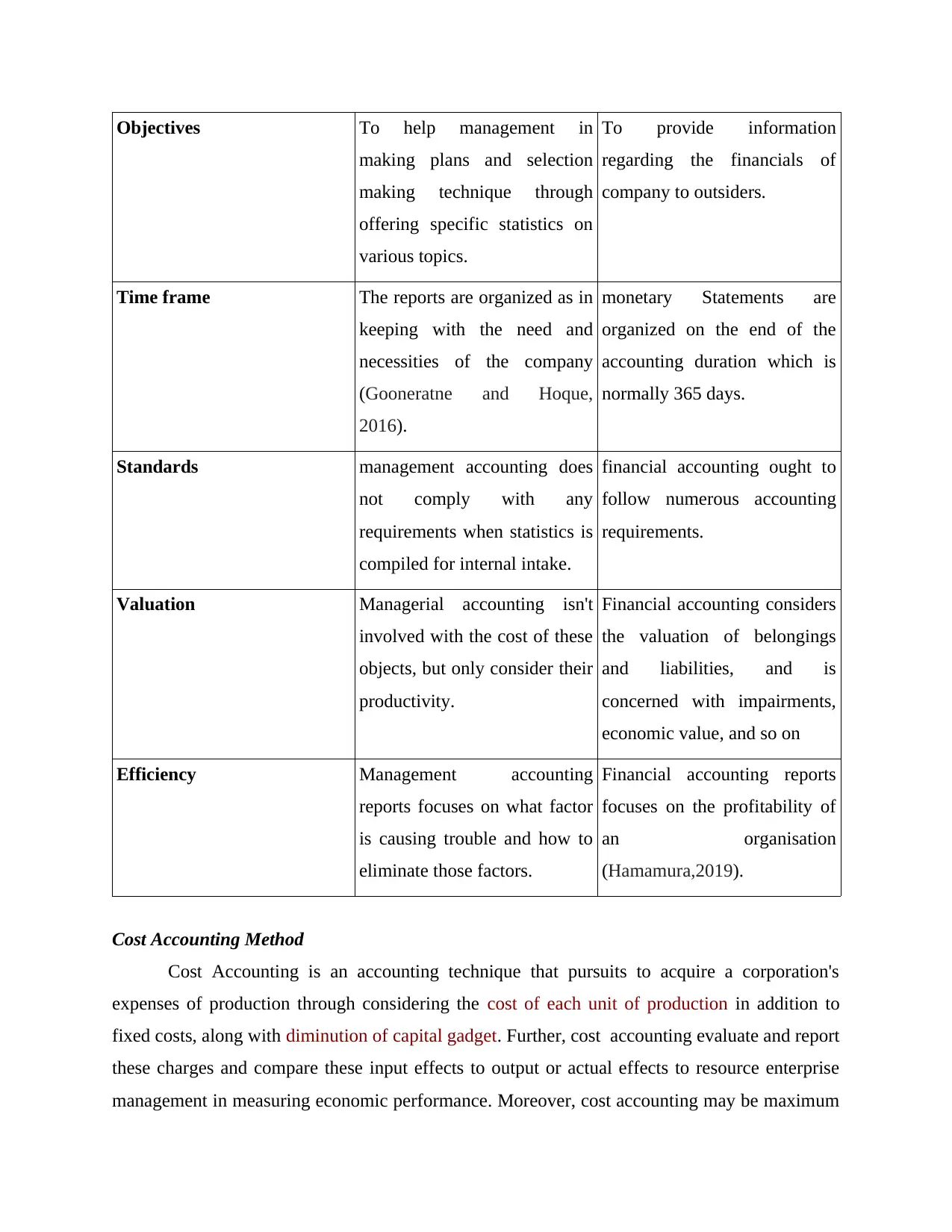

Difference Between Management Accounting And Financial Accounting

Comparison Management Accounting Financial Accounting

MA is the procedure of preparing the financial reports and documents that analysis the

financial condition of the organisation which help them to undertake their operations according

to those financial statistics. Moreover, the report will highlight about the variation between the

MA and financial accounting and along with it will outline cost accounting systems and their

types namely; direct cost and standard costing. Furthermore, the project will frame about the

various costing system (Calabrò,2017).

On the flip side, the assignment will comment on the types of managerial accounting

reports which is inclusive of cash report, budget report, financial report, performance report etc.

However, the report will outline about the absorption costing and marginal costing including

their advantages and disadvantages and along with it will frame about the three planning tools of

budgetary control namely, sales budget, cash budget, performance budget. Eventually, the

project will frame about the various managerial accounting techniques used by the company to

solve their financial issues like break even analysis, cost profit analysis etc.

LO1

P1 Understanding of MA

Management accounting (MA)

MA, also known as managerial accounting. It is the procedure of studying organisation

expenses and operations to prepare financial file, statistics, and account to support managers’

choice making technique in achieving business objectives. However, it is the method of

preparing monetary and costing information and translating that statistics into beneficial

information for administration and officers within a company (Collis, and Hussey, 2017).

Financial accounting

Financial Accounting is the system of determining, recording, concise and reporting the

infinite of transactions as a result of enterprise operations over a time frame. Further, these

transactions are sum-up in the formulation of financial statements, inclusive of the balance sheet,

earnings assertion and cash flow statement, that document the organization's operating overall

performance over a designated period.

Difference Between Management Accounting And Financial Accounting

Comparison Management Accounting Financial Accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Objectives To help management in

making plans and selection

making technique through

offering specific statistics on

various topics.

To provide information

regarding the financials of

company to outsiders.

Time frame The reports are organized as in

keeping with the need and

necessities of the company

(Gooneratne and Hoque,

2016).

monetary Statements are

organized on the end of the

accounting duration which is

normally 365 days.

Standards management accounting does

not comply with any

requirements when statistics is

compiled for internal intake.

financial accounting ought to

follow numerous accounting

requirements.

Valuation Managerial accounting isn't

involved with the cost of these

objects, but only consider their

productivity.

Financial accounting considers

the valuation of belongings

and liabilities, and is

concerned with impairments,

economic value, and so on

Efficiency Management accounting

reports focuses on what factor

is causing trouble and how to

eliminate those factors.

Financial accounting reports

focuses on the profitability of

an organisation

(Hamamura,2019).

Cost Accounting Method

Cost Accounting is an accounting technique that pursuits to acquire a corporation's

expenses of production through considering the cost of each unit of production in addition to

fixed costs, along with diminution of capital gadget. Further, cost accounting evaluate and report

these charges and compare these input effects to output or actual effects to resource enterprise

management in measuring economic performance. Moreover, cost accounting may be maximum

making plans and selection

making technique through

offering specific statistics on

various topics.

To provide information

regarding the financials of

company to outsiders.

Time frame The reports are organized as in

keeping with the need and

necessities of the company

(Gooneratne and Hoque,

2016).

monetary Statements are

organized on the end of the

accounting duration which is

normally 365 days.

Standards management accounting does

not comply with any

requirements when statistics is

compiled for internal intake.

financial accounting ought to

follow numerous accounting

requirements.

Valuation Managerial accounting isn't

involved with the cost of these

objects, but only consider their

productivity.

Financial accounting considers

the valuation of belongings

and liabilities, and is

concerned with impairments,

economic value, and so on

Efficiency Management accounting

reports focuses on what factor

is causing trouble and how to

eliminate those factors.

Financial accounting reports

focuses on the profitability of

an organisation

(Hamamura,2019).

Cost Accounting Method

Cost Accounting is an accounting technique that pursuits to acquire a corporation's

expenses of production through considering the cost of each unit of production in addition to

fixed costs, along with diminution of capital gadget. Further, cost accounting evaluate and report

these charges and compare these input effects to output or actual effects to resource enterprise

management in measuring economic performance. Moreover, cost accounting may be maximum

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

useful as a device for control in budgeting and in putting price manipulate applications, that may

enhance net margins for the organisation within the future. Further, there are three major

objectives of cost accounting:

Cost Control: the first objective of cost accounting is to manipulate the price in the

budgetary management that has set for a specific services or products. However, this function is

essential as management allocates restricted assets to specific initiatives or production tactics

(Hatch and et.al., 2017).

Cost Calculation: this is the main objective of cost accounting and is the source of all

different features of cost accounting. Further, with the help of this function company can see

how they will evaluate the cost of sales per unit for a selected product.

Cost Reducing: This function allows the business enterprise to reduce fees on projects

and tactics. Therefore, reduction in expenses helps to get extra earnings so that margin can

increase.

Types of cost accounting

Standard-costing method: This form of cost accounting makes use of ratios to evaluate

effective use of worker and materials to produce items or offerings below trendy situations.

Therefore, evaluating those variations is known as a variance evaluation. Further, traditional cost

accounting essentially allocates fee based totally on measure, exertions or system hours. Thus,

overhead value has risen proportional to exertions cost for the reason that beginning of standard

value accounting, assigning o/h cost as a standard cost has ended up generating once in a while

deceptive vision.

Direct cost: Direct costs are at once concerned in producing items which means direct

costs can be immediately identified as being used inside the production of goods. As An

Example, direct fabric and direct labour that is used in generating goods. Thus, these costs are

considered as direct costs.

Inventory Management Systems

Inventory Management System track the production and inventory levels. It helps in

delivering chain or the part of it a companies activities run in which covers the lot from

manufacturing to retail, warehousing to delivery, and all the change of stock and components

between. Further, through this method the company can observe all the small transferring parts

of its operations, allowing it to make higher choices and investments. Moreover, distinctive

enhance net margins for the organisation within the future. Further, there are three major

objectives of cost accounting:

Cost Control: the first objective of cost accounting is to manipulate the price in the

budgetary management that has set for a specific services or products. However, this function is

essential as management allocates restricted assets to specific initiatives or production tactics

(Hatch and et.al., 2017).

Cost Calculation: this is the main objective of cost accounting and is the source of all

different features of cost accounting. Further, with the help of this function company can see

how they will evaluate the cost of sales per unit for a selected product.

Cost Reducing: This function allows the business enterprise to reduce fees on projects

and tactics. Therefore, reduction in expenses helps to get extra earnings so that margin can

increase.

Types of cost accounting

Standard-costing method: This form of cost accounting makes use of ratios to evaluate

effective use of worker and materials to produce items or offerings below trendy situations.

Therefore, evaluating those variations is known as a variance evaluation. Further, traditional cost

accounting essentially allocates fee based totally on measure, exertions or system hours. Thus,

overhead value has risen proportional to exertions cost for the reason that beginning of standard

value accounting, assigning o/h cost as a standard cost has ended up generating once in a while

deceptive vision.

Direct cost: Direct costs are at once concerned in producing items which means direct

costs can be immediately identified as being used inside the production of goods. As An

Example, direct fabric and direct labour that is used in generating goods. Thus, these costs are

considered as direct costs.

Inventory Management Systems

Inventory Management System track the production and inventory levels. It helps in

delivering chain or the part of it a companies activities run in which covers the lot from

manufacturing to retail, warehousing to delivery, and all the change of stock and components

between. Further, through this method the company can observe all the small transferring parts

of its operations, allowing it to make higher choices and investments. Moreover, distinctive

inventory managers concentrates on one of an element of supply chain even though small

companies are typically interested in the ordering and ending the chain of sales (Isaac, Lawal and

Okoli,2015).

Job costing system

A job costing method entails the technique of gather records about the prices related to a

selected production or carrier task. Further, this data can be used so one can put up the cost

records to a purchaser below a settlement where charges are refund. Further, the statistics is

likewise useful for deciding the accuracy of an organisation calculation system, which helps in

predicting charges that permit for a sensible and sustainable earning. Moreover, the information

also can be used to allot inventory charges to synthetic items. However, the job costing system

includes three types of cost namely; direct labour, material, and o/h.

Direct Labour: The job costing method have to analyse the value of the labor utilized on

a activity. Further, activities related with services, direct labour may additionally contain almost

all the process cost. Moreover, Direct labour is generally assigned to a task with a time

card, time sheet or with a computerized time clock software and this data can also b e taped on a

smart electronic equipment or through the computer network. Therefore, the user must become

aware of the task, in order that the value facts can be carried out to the appropriate task.

Direct Material: The job costing method can evaluate the value of materials that are

used throughout the performance of the task. As a result, if a company is framing a custom-made

system, the value of the sheet used in the business enterprise ought to be accumulated and

charged to the activity. However, the method can collect this cost through the manual

observation of materials on costing sheets, or the statistics may be charged via using online

terminals inside the storehouse and manufacture location (Kaplan and Atkinson,2015).

Overhead: The job costing method distribute o/h costs like diminution on manufacturing

machine, rent of building etc., to one or greater cost organisation. Further, at the end of every

accountancy duration, the entire amount in each price pool is allotted to the diverse jobs

primarily based on some allotment method that is systematically practical.

Moreover, a job costing system additionally can be custom-made to the necessities of the

customer as some clients permit prices to be charged to their business. However, this is most

usual in cost compensation conditions where the patron has agreed to reimburse a company for

all charges charged to a particular job. Therefore, a job costing method may additionally

companies are typically interested in the ordering and ending the chain of sales (Isaac, Lawal and

Okoli,2015).

Job costing system

A job costing method entails the technique of gather records about the prices related to a

selected production or carrier task. Further, this data can be used so one can put up the cost

records to a purchaser below a settlement where charges are refund. Further, the statistics is

likewise useful for deciding the accuracy of an organisation calculation system, which helps in

predicting charges that permit for a sensible and sustainable earning. Moreover, the information

also can be used to allot inventory charges to synthetic items. However, the job costing system

includes three types of cost namely; direct labour, material, and o/h.

Direct Labour: The job costing method have to analyse the value of the labor utilized on

a activity. Further, activities related with services, direct labour may additionally contain almost

all the process cost. Moreover, Direct labour is generally assigned to a task with a time

card, time sheet or with a computerized time clock software and this data can also b e taped on a

smart electronic equipment or through the computer network. Therefore, the user must become

aware of the task, in order that the value facts can be carried out to the appropriate task.

Direct Material: The job costing method can evaluate the value of materials that are

used throughout the performance of the task. As a result, if a company is framing a custom-made

system, the value of the sheet used in the business enterprise ought to be accumulated and

charged to the activity. However, the method can collect this cost through the manual

observation of materials on costing sheets, or the statistics may be charged via using online

terminals inside the storehouse and manufacture location (Kaplan and Atkinson,2015).

Overhead: The job costing method distribute o/h costs like diminution on manufacturing

machine, rent of building etc., to one or greater cost organisation. Further, at the end of every

accountancy duration, the entire amount in each price pool is allotted to the diverse jobs

primarily based on some allotment method that is systematically practical.

Moreover, a job costing system additionally can be custom-made to the necessities of the

customer as some clients permit prices to be charged to their business. However, this is most

usual in cost compensation conditions where the patron has agreed to reimburse a company for

all charges charged to a particular job. Therefore, a job costing method may additionally

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

incorporate a huge quantity of differentiated rules that aren't broadly applicable to all jobs for

which it's far assembling facts.

Importance Of Management Accounting

Management Accounting makes applicable effort to the company’s profitability

forecasting and economic planning by offering facts on future expenses and income. Further,

management accounting additionally enables the company for preparing the budget preparation,

tracking and manipulate technique in step with agreed regulations and procedures.

Moreover, management accounting method help in placing the pre-decided performance

and corporation standards with real consequences and analysing if any deviation occur which is

accomplished through a way called Variance analysis (Macve,2015).

Furthermore, management accounting develops proper data and information for the cause

of selection making. Thus, the statistics derived from the management accounting procedure

enables management become well knowledgeable to make applicable selections. Moreover,

another vital function of MA is that it helps the management of company in analysing the

opportunities of activities open to management in selection making.

However, The essential function of the management accounting is to develop an accurate

cost analysis to determine the present charges and provide suggestions for the future activities.

Moreover, before an enterprise takes any action, it desires to look into all prospects and

analyse the best plan of action to growth the earnings which indicates that management

accounting can evaluate various sales paths, products, offerings, and advertising activities with a

purpose to find the maximum profitable enterprise version. Therefore, as soon as the

management accounting is done with cost analysis, the company can make better and evidence-

primarily based selections (Morano and Tajani,2017).

P2 Types of Management Accounting Report.

MA report is an effectual approach which helps in efficaciously analysing the fiscal

position of the organisation. It helps in effectively identifying the aims and objectives of the

organization (Appelbaum and et.al, 2017). Management accounting report helps in taking

strategic decision and make proper plans to reduce the problem. It helps management in taking

necessary action to control the deviation and monitor the progress of the Excite Limited.

Financial report: Financial report also known as financial statements of the company are

formal records of all the financial activities and transaction which are carried to achieve gaols

which it's far assembling facts.

Importance Of Management Accounting

Management Accounting makes applicable effort to the company’s profitability

forecasting and economic planning by offering facts on future expenses and income. Further,

management accounting additionally enables the company for preparing the budget preparation,

tracking and manipulate technique in step with agreed regulations and procedures.

Moreover, management accounting method help in placing the pre-decided performance

and corporation standards with real consequences and analysing if any deviation occur which is

accomplished through a way called Variance analysis (Macve,2015).

Furthermore, management accounting develops proper data and information for the cause

of selection making. Thus, the statistics derived from the management accounting procedure

enables management become well knowledgeable to make applicable selections. Moreover,

another vital function of MA is that it helps the management of company in analysing the

opportunities of activities open to management in selection making.

However, The essential function of the management accounting is to develop an accurate

cost analysis to determine the present charges and provide suggestions for the future activities.

Moreover, before an enterprise takes any action, it desires to look into all prospects and

analyse the best plan of action to growth the earnings which indicates that management

accounting can evaluate various sales paths, products, offerings, and advertising activities with a

purpose to find the maximum profitable enterprise version. Therefore, as soon as the

management accounting is done with cost analysis, the company can make better and evidence-

primarily based selections (Morano and Tajani,2017).

P2 Types of Management Accounting Report.

MA report is an effectual approach which helps in efficaciously analysing the fiscal

position of the organisation. It helps in effectively identifying the aims and objectives of the

organization (Appelbaum and et.al, 2017). Management accounting report helps in taking

strategic decision and make proper plans to reduce the problem. It helps management in taking

necessary action to control the deviation and monitor the progress of the Excite Limited.

Financial report: Financial report also known as financial statements of the company are

formal records of all the financial activities and transaction which are carried to achieve gaols

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and objectives of the company (Lev, 2018). This leads to high functional performance and

profitability for the Excite Limited company. Financial reports mainly includes financial

statements like P& L statements, balance sheet, shareholders equity statement and cash flow

statement. It helps managers in determining the financial position of the company and take

strategic decision for high growth of the Excite Limited company.

Advantages and benefits of Financial reports:

Financial report is important and beneficial for the organization as it outlines all the

financial transaction of the company. This reports are beneficial for all the stakeholders of the

company to take informed decision. It also helps in taking informed decisions and avoid

potential roadblocks. Financial reports helps in improving debt management and identify current

trends to improve overall health of the business. Financial reports helps in managing capital,

assets and liabilities of the company.

Budget report:

Budget report is one of the most important report in managerial accounting. This report

helps in managing and controlling the cost of the company. These reports are prepared in order

to compare the actual performance with the budgeted performance of the company. This report

helps in managing the performance of the company and set budget to each activities. Budget

report helps in effectively comparing the actual performance with the budgeted plan and if

management founds any deviations then they take corrective actions in order to achieve the

targets of Excite Limited company (Brown and et.al., 2016).

Advantages and benefits of Budget report:

Budget report helps in controlling the cost of the company by setting budget to carry out

a particular activity in the company. These report helps in cutting cost and offer better employee

incentive, renegotiation with suppliers. Budget report helps in effectively forecasting the future

and take informed decision accordingly for Excite Limited company.

Performance report: Performance report helps stakeholders in determining and

evaluating the performance of the particular project. It helps in evaluating financial and

operational performance of the Excite Limited company (Maas and Verdoorn, 2017). It also

profitability for the Excite Limited company. Financial reports mainly includes financial

statements like P& L statements, balance sheet, shareholders equity statement and cash flow

statement. It helps managers in determining the financial position of the company and take

strategic decision for high growth of the Excite Limited company.

Advantages and benefits of Financial reports:

Financial report is important and beneficial for the organization as it outlines all the

financial transaction of the company. This reports are beneficial for all the stakeholders of the

company to take informed decision. It also helps in taking informed decisions and avoid

potential roadblocks. Financial reports helps in improving debt management and identify current

trends to improve overall health of the business. Financial reports helps in managing capital,

assets and liabilities of the company.

Budget report:

Budget report is one of the most important report in managerial accounting. This report

helps in managing and controlling the cost of the company. These reports are prepared in order

to compare the actual performance with the budgeted performance of the company. This report

helps in managing the performance of the company and set budget to each activities. Budget

report helps in effectively comparing the actual performance with the budgeted plan and if

management founds any deviations then they take corrective actions in order to achieve the

targets of Excite Limited company (Brown and et.al., 2016).

Advantages and benefits of Budget report:

Budget report helps in controlling the cost of the company by setting budget to carry out

a particular activity in the company. These report helps in cutting cost and offer better employee

incentive, renegotiation with suppliers. Budget report helps in effectively forecasting the future

and take informed decision accordingly for Excite Limited company.

Performance report: Performance report helps stakeholders in determining and

evaluating the performance of the particular project. It helps in evaluating financial and

operational performance of the Excite Limited company (Maas and Verdoorn, 2017). It also

helps in determining the performance of each department in the organization and in case of any

deviation take necessary action accordingly.

Advantages and benefits of Performance report:

Performance report helps in effectively identifying the deviation in the activity with the

help of various management accounting techniques. This report helps in analysing the

performance result with the benchmark to get desired results and outcomes. It helps in

forecasting future progress, utilization of resources, forecasting future progress, communicating

project progress for the Excite Limited company. Performance report saves time, ensures

efficiency, improved productivity, reduction in conflicts and consistency.

Cost analysis report: Cost analysis report helps in effectively identifying the cost

attached with each activity to attain goals and objectives in the cost efficient manner. Cost

analysis report helps in identifying the cost attached with raw material, labour, resources and

overhead. It helps in reducing wastage and optimally utilize the resources of the Excite Limited

company which leads to higher profitability.

Advantages and benefits of Cost analysis report:

Cost analysis report helps in determining whether the project is sound, feasible and

justifiable. It helps in analysing how much cost must be attached to carry out activity and how it

adds value to gain profitability in the business (Ramsey and et.al., 2015). It helps in assigning

cost to the project and evaluate the economic value in return. It is simple and convenient to take

informed decision.

Assessment Of Information Presented In Managerial Accounting Reports

Management accounting report is beneficial for Excite Limited company as it helps in

taking strategic and informed decision. The information disclosed in the management accounting

report must be reliable, transparent and true. The report should be in compliance with various

accounting standards for higher accuracy and reliability of the data. Accurate and reliable

information helps managers in taking informed decision which eventually helps in further growth

and development of Excite Limited company (Herremans and Nazari 2016). The report should

be presented on the timely manner so that proper goals can be set for the future and evaluate the

present performance of the company effectively. Management accounting report helps in

developing effective strategies for higher growth of the business. It also helps in taking necessary

deviation take necessary action accordingly.

Advantages and benefits of Performance report:

Performance report helps in effectively identifying the deviation in the activity with the

help of various management accounting techniques. This report helps in analysing the

performance result with the benchmark to get desired results and outcomes. It helps in

forecasting future progress, utilization of resources, forecasting future progress, communicating

project progress for the Excite Limited company. Performance report saves time, ensures

efficiency, improved productivity, reduction in conflicts and consistency.

Cost analysis report: Cost analysis report helps in effectively identifying the cost

attached with each activity to attain goals and objectives in the cost efficient manner. Cost

analysis report helps in identifying the cost attached with raw material, labour, resources and

overhead. It helps in reducing wastage and optimally utilize the resources of the Excite Limited

company which leads to higher profitability.

Advantages and benefits of Cost analysis report:

Cost analysis report helps in determining whether the project is sound, feasible and

justifiable. It helps in analysing how much cost must be attached to carry out activity and how it

adds value to gain profitability in the business (Ramsey and et.al., 2015). It helps in assigning

cost to the project and evaluate the economic value in return. It is simple and convenient to take

informed decision.

Assessment Of Information Presented In Managerial Accounting Reports

Management accounting report is beneficial for Excite Limited company as it helps in

taking strategic and informed decision. The information disclosed in the management accounting

report must be reliable, transparent and true. The report should be in compliance with various

accounting standards for higher accuracy and reliability of the data. Accurate and reliable

information helps managers in taking informed decision which eventually helps in further growth

and development of Excite Limited company (Herremans and Nazari 2016). The report should

be presented on the timely manner so that proper goals can be set for the future and evaluate the

present performance of the company effectively. Management accounting report helps in

developing effective strategies for higher growth of the business. It also helps in taking necessary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

action in case of any deviation. True, reliable, accurate and relevant management accounting

report is very useful for the stakeholders of the company to take informed decision with utmost

accuracy.

LO 2

P 3 Income statement using absorption and marginal costing

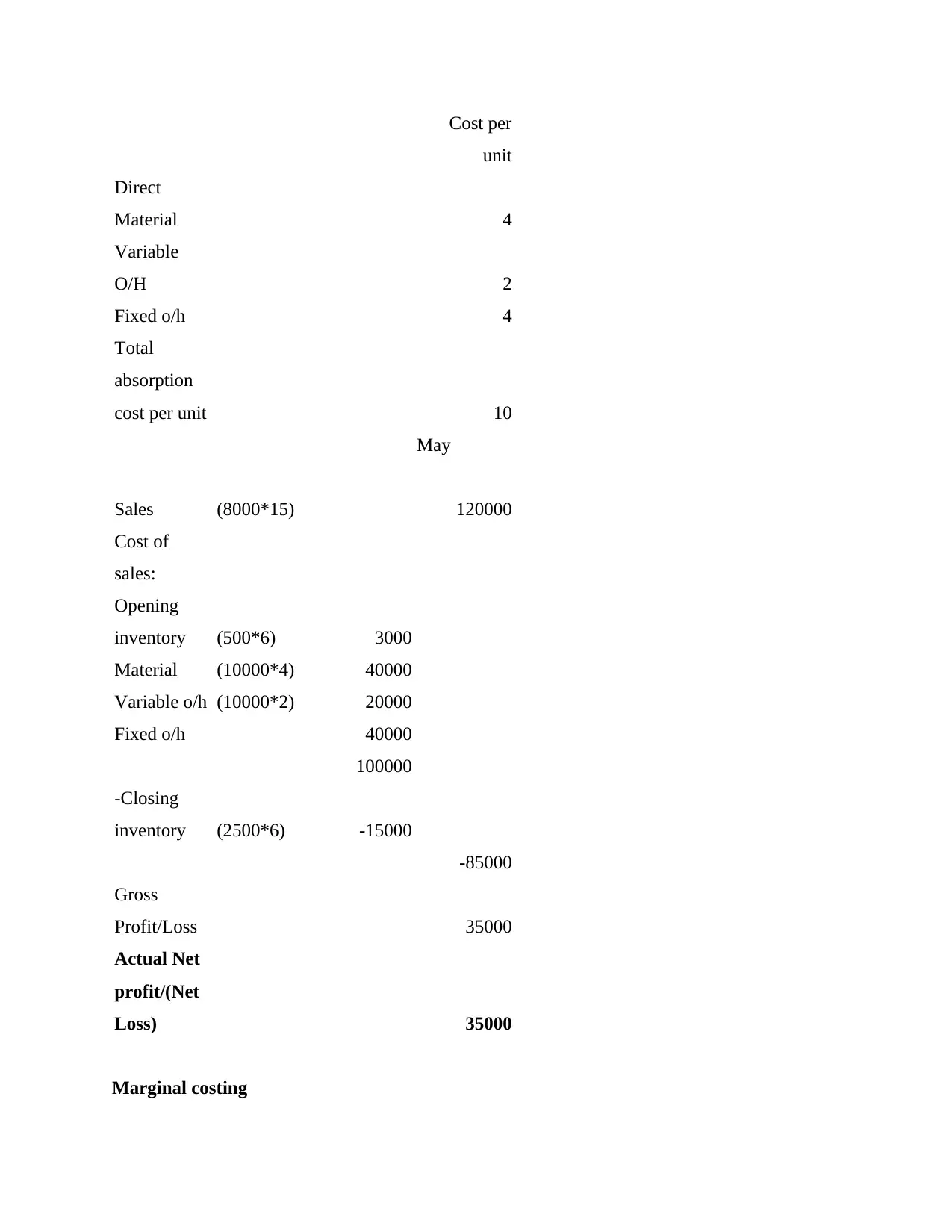

Absorption Costing

Absorption costing also called full costing method which is a formulaic approach of

determining cost. Further, it is the method of charging all fees both variable and fixed to

transaction, procedures and products. Moreover, it's miles the oldest and extensively used

method of figuring out fee. However, under absorption method, cost is made from direct prices

plus overhead fees absorbed on some appropriate foundation (Mullinova,2016).

Advantages

Absorption Costing is the most appropriate method for maintaining the accounting

system of company. However, this is the method which is satisfactory below the

generally accepted Accounting ideas(GAAP ). Therefore, the principle reason for that is

that under absorption costing inventory isn't always under-valued as it responsible for the

attributable expenses but also the constant business overheads.

The absorption costing is the best method of costing for companies. Further, absorption

costing makes calculations less difficult for organisation. Moreover, it makes these

agencies capable of absorb constant charges in advance and promote their merchandise

on a higher selling charge in addition to income.

Disadvantages

Absorption Costing can't be used as an effective device to assess profitability of a

business enterprise that is due to the fact the absorption costing includes constant charges

within the cost of the product, that will be fixed regardless of the output or production.

Income Statement (Absorption Costing)

as on 30th May 2019

Under Absorption Costing

report is very useful for the stakeholders of the company to take informed decision with utmost

accuracy.

LO 2

P 3 Income statement using absorption and marginal costing

Absorption Costing

Absorption costing also called full costing method which is a formulaic approach of

determining cost. Further, it is the method of charging all fees both variable and fixed to

transaction, procedures and products. Moreover, it's miles the oldest and extensively used

method of figuring out fee. However, under absorption method, cost is made from direct prices

plus overhead fees absorbed on some appropriate foundation (Mullinova,2016).

Advantages

Absorption Costing is the most appropriate method for maintaining the accounting

system of company. However, this is the method which is satisfactory below the

generally accepted Accounting ideas(GAAP ). Therefore, the principle reason for that is

that under absorption costing inventory isn't always under-valued as it responsible for the

attributable expenses but also the constant business overheads.

The absorption costing is the best method of costing for companies. Further, absorption

costing makes calculations less difficult for organisation. Moreover, it makes these

agencies capable of absorb constant charges in advance and promote their merchandise

on a higher selling charge in addition to income.

Disadvantages

Absorption Costing can't be used as an effective device to assess profitability of a

business enterprise that is due to the fact the absorption costing includes constant charges

within the cost of the product, that will be fixed regardless of the output or production.

Income Statement (Absorption Costing)

as on 30th May 2019

Under Absorption Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost per

unit

Direct

Material 4

Variable

O/H 2

Fixed o/h 4

Total

absorption

cost per unit 10

May

Sales (8000*15) 120000

Cost of

sales:

Opening

inventory (500*6) 3000

Material (10000*4) 40000

Variable o/h (10000*2) 20000

Fixed o/h 40000

100000

-Closing

inventory (2500*6) -15000

-85000

Gross

Profit/Loss 35000

Actual Net

profit/(Net

Loss) 35000

Marginal costing

unit

Direct

Material 4

Variable

O/H 2

Fixed o/h 4

Total

absorption

cost per unit 10

May

Sales (8000*15) 120000

Cost of

sales:

Opening

inventory (500*6) 3000

Material (10000*4) 40000

Variable o/h (10000*2) 20000

Fixed o/h 40000

100000

-Closing

inventory (2500*6) -15000

-85000

Gross

Profit/Loss 35000

Actual Net

profit/(Net

Loss) 35000

Marginal costing

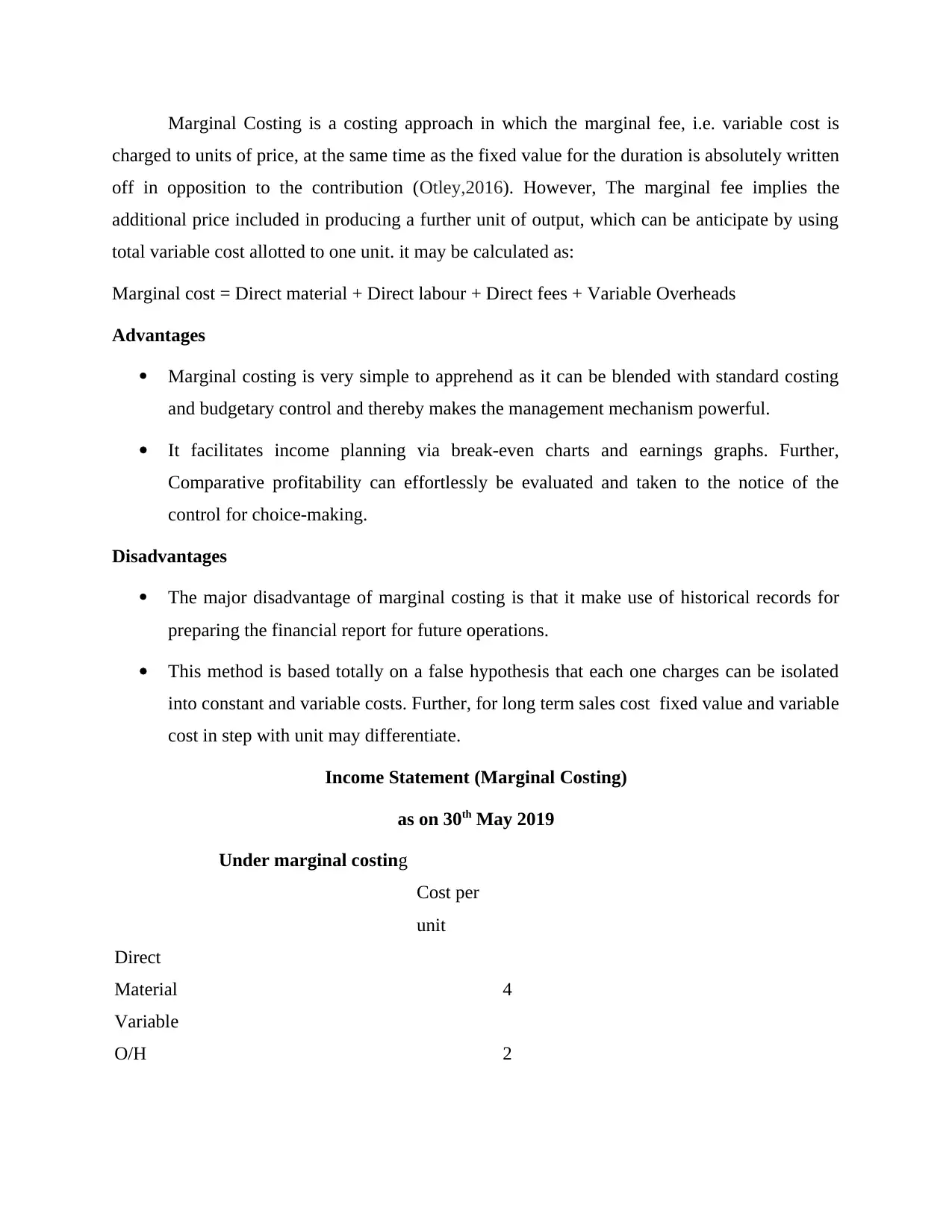

Marginal Costing is a costing approach in which the marginal fee, i.e. variable cost is

charged to units of price, at the same time as the fixed value for the duration is absolutely written

off in opposition to the contribution (Otley,2016). However, The marginal fee implies the

additional price included in producing a further unit of output, which can be anticipate by using

total variable cost allotted to one unit. it may be calculated as:

Marginal cost = Direct material + Direct labour + Direct fees + Variable Overheads

Advantages

Marginal costing is very simple to apprehend as it can be blended with standard costing

and budgetary control and thereby makes the management mechanism powerful.

It facilitates income planning via break-even charts and earnings graphs. Further,

Comparative profitability can effortlessly be evaluated and taken to the notice of the

control for choice-making.

Disadvantages

The major disadvantage of marginal costing is that it make use of historical records for

preparing the financial report for future operations.

This method is based totally on a false hypothesis that each one charges can be isolated

into constant and variable costs. Further, for long term sales cost fixed value and variable

cost in step with unit may differentiate.

Income Statement (Marginal Costing)

as on 30th May 2019

Under marginal costing

Cost per

unit

Direct

Material 4

Variable

O/H 2

charged to units of price, at the same time as the fixed value for the duration is absolutely written

off in opposition to the contribution (Otley,2016). However, The marginal fee implies the

additional price included in producing a further unit of output, which can be anticipate by using

total variable cost allotted to one unit. it may be calculated as:

Marginal cost = Direct material + Direct labour + Direct fees + Variable Overheads

Advantages

Marginal costing is very simple to apprehend as it can be blended with standard costing

and budgetary control and thereby makes the management mechanism powerful.

It facilitates income planning via break-even charts and earnings graphs. Further,

Comparative profitability can effortlessly be evaluated and taken to the notice of the

control for choice-making.

Disadvantages

The major disadvantage of marginal costing is that it make use of historical records for

preparing the financial report for future operations.

This method is based totally on a false hypothesis that each one charges can be isolated

into constant and variable costs. Further, for long term sales cost fixed value and variable

cost in step with unit may differentiate.

Income Statement (Marginal Costing)

as on 30th May 2019

Under marginal costing

Cost per

unit

Direct

Material 4

Variable

O/H 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.