Management Accounting Systems, Reports and Planning Techniques

VerifiedAdded on 2020/06/06

|16

|4110

|70

AI Summary

This report provides a comprehensive analysis of management accounting practices within Nisa Retail, a UK-based retail enterprise. The report begins by defining management accounting and exploring key systems such as price optimization, cost accounting, job costing, and inventory management, emphasizing their importance for internal decision-making. It then details various management accounting reporting methods, including performance reports, accounts receivables aging, stock management, segmental reports, and operating budget reports. The core of the report involves a comparative analysis of marginal and absorption costing methods, including the preparation of income statements using both approaches. The report highlights the differences in net profit generated by each method and discusses the advantages and disadvantages of each. Finally, the report evaluates different budgeting techniques, such as zero-based, fixed, and incremental budgeting, outlining their respective merits and demerits within the context of Nisa Retail's financial planning processes. The report concludes by explaining how management accounting systems help to resolve a wide range of financial issues.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting (MA) is a concept through which an enterprise able to make

financial plan, implement, monitor and execute at the workplace in proper direction. Further, for

making internal business decisions also this mentioned aspect is one of the highly appropriate. In

the current project, Nisa Retail Store is taken as a base which is UK based small business

enterprise and operates in retail sector. Through the present assignment, systems and reports of

MA are described which help to take various decisions and accomplish reporting of MA in

effective direction respectively. Apart from this, for chosen company income statements (I/S) are

prepared after considering two major method i.e. marginal and absorption costing. Moreover,

planning techniques which are used for controlling budgets are evaluated with reference to Nisa

Retail store. At the end of project, systems of MA considered resolving wide range of financial

issues are explained.

TASK 1

P1 Describing MA and key needs of its several systems in Nisa Retail store

Business Report

From: Management Accounting Officer

To: General manager

Nisa Retail Store

Subject: Several systems of MA

A term which helps to every organisation in order to take those business judgements which are

fruitful and related to only internal environment is referred as MA. It comprises with several

numbers of systems and approaches which are implemented at the working place (Groot and

Selto, 2013). Some important systems of MA are explained below along with their necessities:

Price optimisation system: In accordance to this system of MA, company makes

decision that which level of price of retail items is required to charge from customers.

Under this, all the pricing level are evaluated and then analysed that at which price

majority of the people gave response. Further, one particular price at the which products

sold in higher proportion as compared to others then that will be selected. Hence, to opt

1

Management accounting (MA) is a concept through which an enterprise able to make

financial plan, implement, monitor and execute at the workplace in proper direction. Further, for

making internal business decisions also this mentioned aspect is one of the highly appropriate. In

the current project, Nisa Retail Store is taken as a base which is UK based small business

enterprise and operates in retail sector. Through the present assignment, systems and reports of

MA are described which help to take various decisions and accomplish reporting of MA in

effective direction respectively. Apart from this, for chosen company income statements (I/S) are

prepared after considering two major method i.e. marginal and absorption costing. Moreover,

planning techniques which are used for controlling budgets are evaluated with reference to Nisa

Retail store. At the end of project, systems of MA considered resolving wide range of financial

issues are explained.

TASK 1

P1 Describing MA and key needs of its several systems in Nisa Retail store

Business Report

From: Management Accounting Officer

To: General manager

Nisa Retail Store

Subject: Several systems of MA

A term which helps to every organisation in order to take those business judgements which are

fruitful and related to only internal environment is referred as MA. It comprises with several

numbers of systems and approaches which are implemented at the working place (Groot and

Selto, 2013). Some important systems of MA are explained below along with their necessities:

Price optimisation system: In accordance to this system of MA, company makes

decision that which level of price of retail items is required to charge from customers.

Under this, all the pricing level are evaluated and then analysed that at which price

majority of the people gave response. Further, one particular price at the which products

sold in higher proportion as compared to others then that will be selected. Hence, to opt

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

one specific price where more customers purchase products price optimisation system is

needed for Nisa Retail.

Cost accounting: On the basis of this, expenditures which incurred in the company

within particular period of time like quarterly, half yearly etc. are computed.

Management of selected firm easily able to know amount of costing associated to

manufacture and sale goods and services at the workplace. Therefore, Nisa Retail

requires this system to analyse and compute total cost of production. On the basis of

this, judgement to apply one pricing strategy can be made profitably (Hald and Thrane,

2016).

Job costing: Another system is job costing which is used for analysing costs associated

for producing and selling every product comes under one batch. As per the case of Nisa

Retail, it sales different range of goods like food, shoes, grocery, cloths etc. With the

help of job costing, chosen firm will become able to know that at which level of costs

products are sold in the market (The job costing system, 2015). Therefore, company will

become able to select one attractive price of the product for selling in the market and

enhance revenue at the end of year.

Inventory management: At the last, it is necessary to manage available stock in the

company decline it. The reason is that if there is higher inventory remained every year

then it will affect capacity of generating revenue at the end of year. Moreover, higher

the level of this aspect leads to reduce stock turnover ratio of Nisa Retail store. Further,

essential necessity of this system is to manage stock and boost up turnover ratio in an

efficient way (Joshi and Li, 2016). While going to make valuation of inventory at the

business place of every firm basic three methods included. Such techniques of stock

valuation are like LIFO, weighted average as well as FIFO.

P2 Explaining methods which are used by Nisa Retail store for completing management

accounting reporting

Business Report

2

needed for Nisa Retail.

Cost accounting: On the basis of this, expenditures which incurred in the company

within particular period of time like quarterly, half yearly etc. are computed.

Management of selected firm easily able to know amount of costing associated to

manufacture and sale goods and services at the workplace. Therefore, Nisa Retail

requires this system to analyse and compute total cost of production. On the basis of

this, judgement to apply one pricing strategy can be made profitably (Hald and Thrane,

2016).

Job costing: Another system is job costing which is used for analysing costs associated

for producing and selling every product comes under one batch. As per the case of Nisa

Retail, it sales different range of goods like food, shoes, grocery, cloths etc. With the

help of job costing, chosen firm will become able to know that at which level of costs

products are sold in the market (The job costing system, 2015). Therefore, company will

become able to select one attractive price of the product for selling in the market and

enhance revenue at the end of year.

Inventory management: At the last, it is necessary to manage available stock in the

company decline it. The reason is that if there is higher inventory remained every year

then it will affect capacity of generating revenue at the end of year. Moreover, higher

the level of this aspect leads to reduce stock turnover ratio of Nisa Retail store. Further,

essential necessity of this system is to manage stock and boost up turnover ratio in an

efficient way (Joshi and Li, 2016). While going to make valuation of inventory at the

business place of every firm basic three methods included. Such techniques of stock

valuation are like LIFO, weighted average as well as FIFO.

P2 Explaining methods which are used by Nisa Retail store for completing management

accounting reporting

Business Report

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From: Management Accounting Officer

To: General manager

Nisa Retail Store

Subject: Different reports come under MA reporting

A term various kinds of reports are made at the working environment and after clubbing them

financial statements are prepared is known as reporting of MA. In order to complete this stated

method wide range of techniques and aspects are taken into consideration in Nisa Retail.

Further, explanation of reports which are used for completing process of MA reporting is

mentioned below:

Performance report: In order to measure performance of a company by considering

past or estimated and pre sent or actual information this stated report is used. Under this,

data from budgets are taken initially which are forecasted for the next accounting period.

Once the year completed then whatever actual data comes, compared with budgeted

information (Messner, 2016). If Nisa Retail store unable to perform well in industry then

corrective actions are to be taken by the firm. It is used for making required changes and

implement needed strategies so that performance will enhance in upcoming years.

Accounts receivables ageing: As per this, sum of money which will be received in next

year of after sometimes is transacted in this type of report. Higher the amount of this

method shows that, Nisa Retail made more credit sales in the year as compared to cash

sales. Amount of total credit sales which incurred in one year is to be recorded in this

stated kind of report of MA. Further, total of this is treated in balance sheet as current

assets in form of debtors. As the management reduces credit sales and enhance cash

sales in one year then total of accounts receivable ageing report will decline.

Stock management: Another report is related to stock which is used for managing as

well as declining total inventory available in the Nisa Retail store. When this factor

reduce on consistent basis then company able to raise stock turnover ratio and generate

high level of profit (Soheilirad and Sofian, 2016). It includes major two aspects which

are like closing as well as opening inventory. Total of this report treated under non-

3

To: General manager

Nisa Retail Store

Subject: Different reports come under MA reporting

A term various kinds of reports are made at the working environment and after clubbing them

financial statements are prepared is known as reporting of MA. In order to complete this stated

method wide range of techniques and aspects are taken into consideration in Nisa Retail.

Further, explanation of reports which are used for completing process of MA reporting is

mentioned below:

Performance report: In order to measure performance of a company by considering

past or estimated and pre sent or actual information this stated report is used. Under this,

data from budgets are taken initially which are forecasted for the next accounting period.

Once the year completed then whatever actual data comes, compared with budgeted

information (Messner, 2016). If Nisa Retail store unable to perform well in industry then

corrective actions are to be taken by the firm. It is used for making required changes and

implement needed strategies so that performance will enhance in upcoming years.

Accounts receivables ageing: As per this, sum of money which will be received in next

year of after sometimes is transacted in this type of report. Higher the amount of this

method shows that, Nisa Retail made more credit sales in the year as compared to cash

sales. Amount of total credit sales which incurred in one year is to be recorded in this

stated kind of report of MA. Further, total of this is treated in balance sheet as current

assets in form of debtors. As the management reduces credit sales and enhance cash

sales in one year then total of accounts receivable ageing report will decline.

Stock management: Another report is related to stock which is used for managing as

well as declining total inventory available in the Nisa Retail store. When this factor

reduce on consistent basis then company able to raise stock turnover ratio and generate

high level of profit (Soheilirad and Sofian, 2016). It includes major two aspects which

are like closing as well as opening inventory. Total of this report treated under non-

3

current assets of balance sheet of Nisa Retail.

Segmental report: Apart from the above, as per this method, small reports are to be

made on the basis of department wise. For example: report of human resource, financial,

information technology, production, research and development etc. According to this,

cash payments as well as receipts incurred within one financial year in each segment are

recorded. Therefore, Nisa Retail can assess cash position of every organisational

function and analyse performance of it.

Operating budget report: At the last, under this kind of reporting method each and

every income as well as outcome are recorded related to operation department. Apart

from this, it reflects amount of cash position which will be remained in the next year

from operating in market. In this, purchase of raw materials, labour charges,

maintenance of equipments etc. are involved (Vaivio, 2008). Total amount of this stated

report is treated in the books of profit and loss in terms of operating expenses. Further, it

helps to determine or calculate operating income generated at the end of financial year.

TASK 2

P3 Computing costs and preparing I/S using two costing methods

In order to formulate account of profit and loss at the workplace there are various

techniques considered by firm. As per the current scenario, Nisa Retail Store uses generally two

ways which are like marginal as well as absorption. On the basis of these two ways P/L prepared

below:

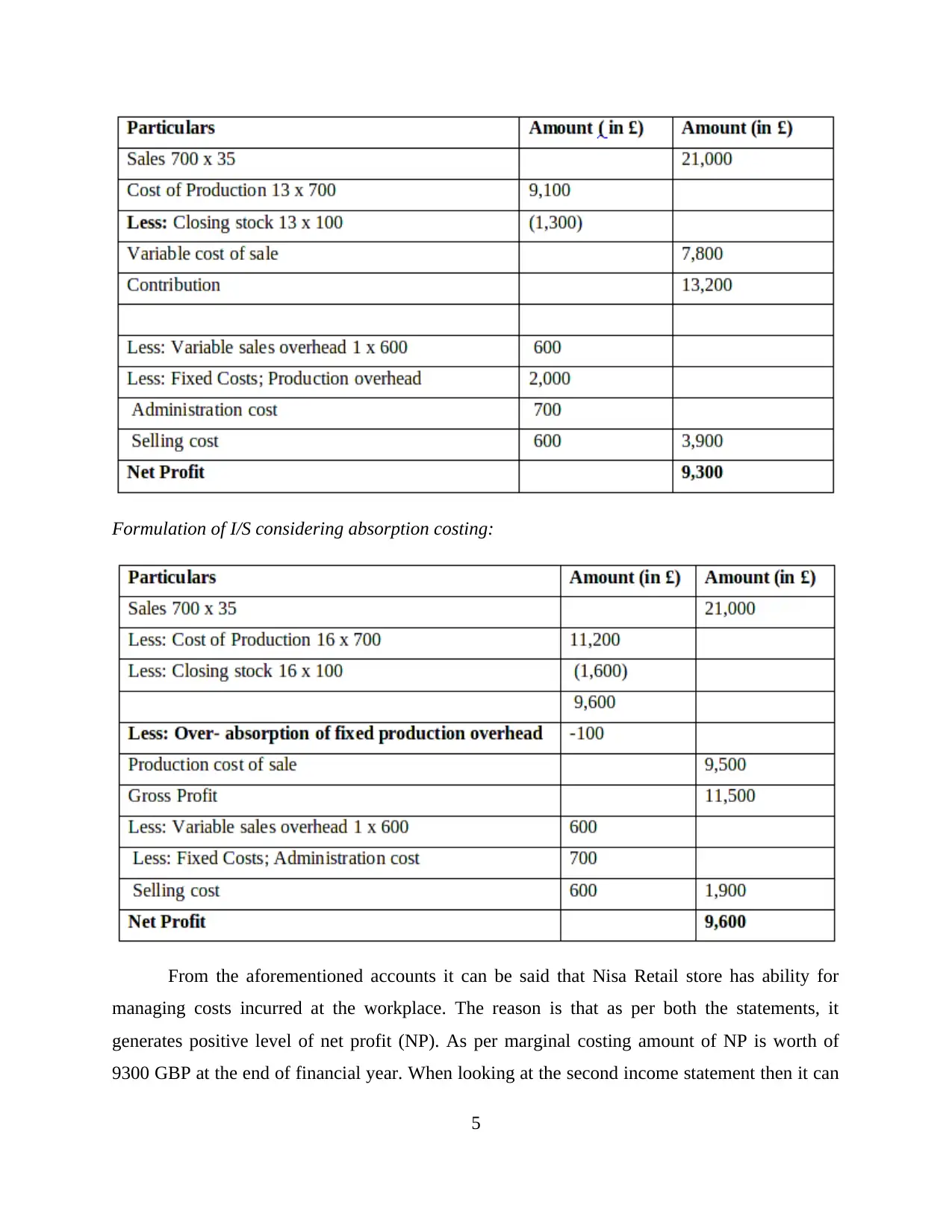

Formulation of I/S considering marginal costing:

4

Segmental report: Apart from the above, as per this method, small reports are to be

made on the basis of department wise. For example: report of human resource, financial,

information technology, production, research and development etc. According to this,

cash payments as well as receipts incurred within one financial year in each segment are

recorded. Therefore, Nisa Retail can assess cash position of every organisational

function and analyse performance of it.

Operating budget report: At the last, under this kind of reporting method each and

every income as well as outcome are recorded related to operation department. Apart

from this, it reflects amount of cash position which will be remained in the next year

from operating in market. In this, purchase of raw materials, labour charges,

maintenance of equipments etc. are involved (Vaivio, 2008). Total amount of this stated

report is treated in the books of profit and loss in terms of operating expenses. Further, it

helps to determine or calculate operating income generated at the end of financial year.

TASK 2

P3 Computing costs and preparing I/S using two costing methods

In order to formulate account of profit and loss at the workplace there are various

techniques considered by firm. As per the current scenario, Nisa Retail Store uses generally two

ways which are like marginal as well as absorption. On the basis of these two ways P/L prepared

below:

Formulation of I/S considering marginal costing:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

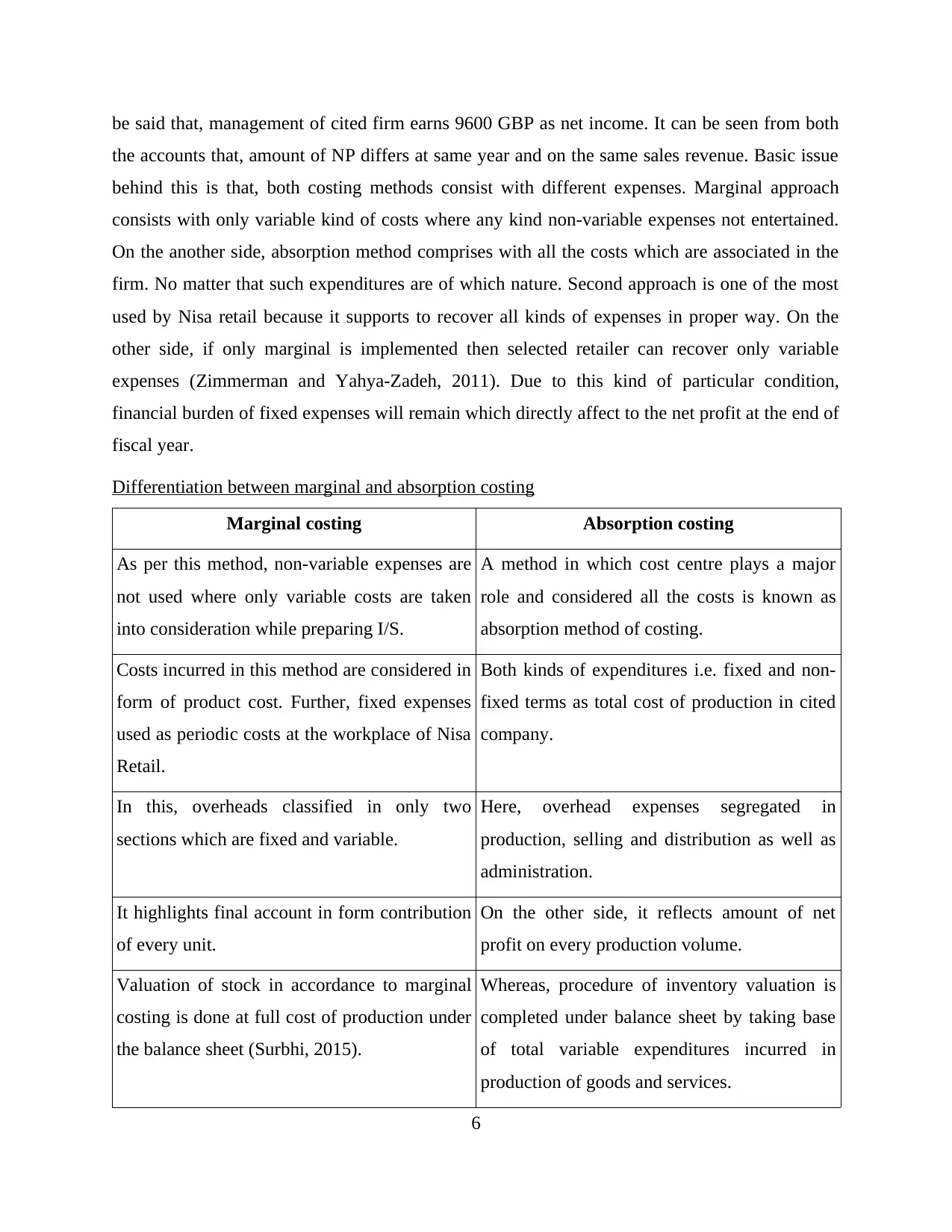

Formulation of I/S considering absorption costing:

From the aforementioned accounts it can be said that Nisa Retail store has ability for

managing costs incurred at the workplace. The reason is that as per both the statements, it

generates positive level of net profit (NP). As per marginal costing amount of NP is worth of

9300 GBP at the end of financial year. When looking at the second income statement then it can

5

From the aforementioned accounts it can be said that Nisa Retail store has ability for

managing costs incurred at the workplace. The reason is that as per both the statements, it

generates positive level of net profit (NP). As per marginal costing amount of NP is worth of

9300 GBP at the end of financial year. When looking at the second income statement then it can

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be said that, management of cited firm earns 9600 GBP as net income. It can be seen from both

the accounts that, amount of NP differs at same year and on the same sales revenue. Basic issue

behind this is that, both costing methods consist with different expenses. Marginal approach

consists with only variable kind of costs where any kind non-variable expenses not entertained.

On the another side, absorption method comprises with all the costs which are associated in the

firm. No matter that such expenditures are of which nature. Second approach is one of the most

used by Nisa retail because it supports to recover all kinds of expenses in proper way. On the

other side, if only marginal is implemented then selected retailer can recover only variable

expenses (Zimmerman and Yahya-Zadeh, 2011). Due to this kind of particular condition,

financial burden of fixed expenses will remain which directly affect to the net profit at the end of

fiscal year.

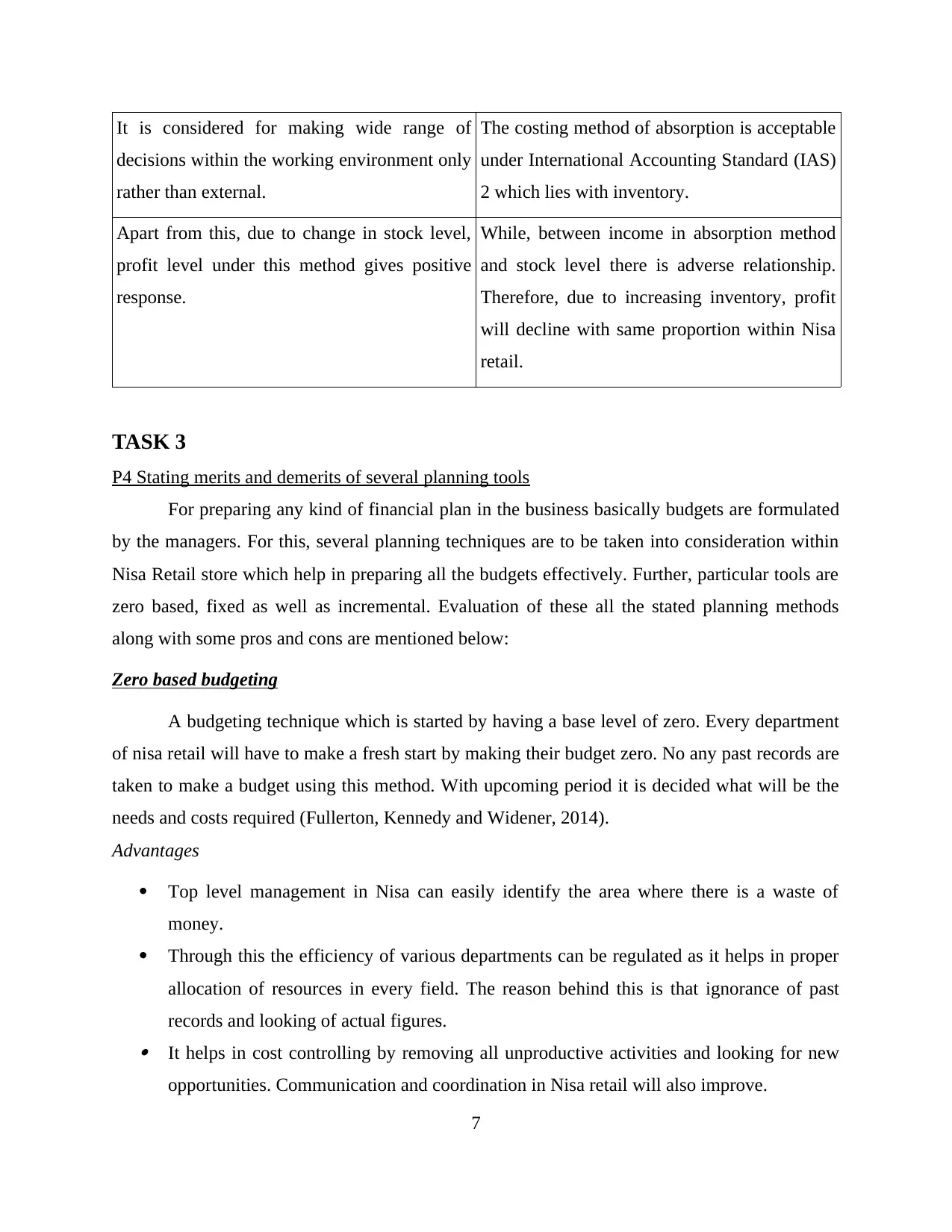

Differentiation between marginal and absorption costing

Marginal costing Absorption costing

As per this method, non-variable expenses are

not used where only variable costs are taken

into consideration while preparing I/S.

A method in which cost centre plays a major

role and considered all the costs is known as

absorption method of costing.

Costs incurred in this method are considered in

form of product cost. Further, fixed expenses

used as periodic costs at the workplace of Nisa

Retail.

Both kinds of expenditures i.e. fixed and non-

fixed terms as total cost of production in cited

company.

In this, overheads classified in only two

sections which are fixed and variable.

Here, overhead expenses segregated in

production, selling and distribution as well as

administration.

It highlights final account in form contribution

of every unit.

On the other side, it reflects amount of net

profit on every production volume.

Valuation of stock in accordance to marginal

costing is done at full cost of production under

the balance sheet (Surbhi, 2015).

Whereas, procedure of inventory valuation is

completed under balance sheet by taking base

of total variable expenditures incurred in

production of goods and services.

6

the accounts that, amount of NP differs at same year and on the same sales revenue. Basic issue

behind this is that, both costing methods consist with different expenses. Marginal approach

consists with only variable kind of costs where any kind non-variable expenses not entertained.

On the another side, absorption method comprises with all the costs which are associated in the

firm. No matter that such expenditures are of which nature. Second approach is one of the most

used by Nisa retail because it supports to recover all kinds of expenses in proper way. On the

other side, if only marginal is implemented then selected retailer can recover only variable

expenses (Zimmerman and Yahya-Zadeh, 2011). Due to this kind of particular condition,

financial burden of fixed expenses will remain which directly affect to the net profit at the end of

fiscal year.

Differentiation between marginal and absorption costing

Marginal costing Absorption costing

As per this method, non-variable expenses are

not used where only variable costs are taken

into consideration while preparing I/S.

A method in which cost centre plays a major

role and considered all the costs is known as

absorption method of costing.

Costs incurred in this method are considered in

form of product cost. Further, fixed expenses

used as periodic costs at the workplace of Nisa

Retail.

Both kinds of expenditures i.e. fixed and non-

fixed terms as total cost of production in cited

company.

In this, overheads classified in only two

sections which are fixed and variable.

Here, overhead expenses segregated in

production, selling and distribution as well as

administration.

It highlights final account in form contribution

of every unit.

On the other side, it reflects amount of net

profit on every production volume.

Valuation of stock in accordance to marginal

costing is done at full cost of production under

the balance sheet (Surbhi, 2015).

Whereas, procedure of inventory valuation is

completed under balance sheet by taking base

of total variable expenditures incurred in

production of goods and services.

6

It is considered for making wide range of

decisions within the working environment only

rather than external.

The costing method of absorption is acceptable

under International Accounting Standard (IAS)

2 which lies with inventory.

Apart from this, due to change in stock level,

profit level under this method gives positive

response.

While, between income in absorption method

and stock level there is adverse relationship.

Therefore, due to increasing inventory, profit

will decline with same proportion within Nisa

retail.

TASK 3

P4 Stating merits and demerits of several planning tools

For preparing any kind of financial plan in the business basically budgets are formulated

by the managers. For this, several planning techniques are to be taken into consideration within

Nisa Retail store which help in preparing all the budgets effectively. Further, particular tools are

zero based, fixed as well as incremental. Evaluation of these all the stated planning methods

along with some pros and cons are mentioned below:

Zero based budgeting

A budgeting technique which is started by having a base level of zero. Every department

of nisa retail will have to make a fresh start by making their budget zero. No any past records are

taken to make a budget using this method. With upcoming period it is decided what will be the

needs and costs required (Fullerton, Kennedy and Widener, 2014).

Advantages

Top level management in Nisa can easily identify the area where there is a waste of

money.

Through this the efficiency of various departments can be regulated as it helps in proper

allocation of resources in every field. The reason behind this is that ignorance of past

records and looking of actual figures. It helps in cost controlling by removing all unproductive activities and looking for new

opportunities. Communication and coordination in Nisa retail will also improve.

7

decisions within the working environment only

rather than external.

The costing method of absorption is acceptable

under International Accounting Standard (IAS)

2 which lies with inventory.

Apart from this, due to change in stock level,

profit level under this method gives positive

response.

While, between income in absorption method

and stock level there is adverse relationship.

Therefore, due to increasing inventory, profit

will decline with same proportion within Nisa

retail.

TASK 3

P4 Stating merits and demerits of several planning tools

For preparing any kind of financial plan in the business basically budgets are formulated

by the managers. For this, several planning techniques are to be taken into consideration within

Nisa Retail store which help in preparing all the budgets effectively. Further, particular tools are

zero based, fixed as well as incremental. Evaluation of these all the stated planning methods

along with some pros and cons are mentioned below:

Zero based budgeting

A budgeting technique which is started by having a base level of zero. Every department

of nisa retail will have to make a fresh start by making their budget zero. No any past records are

taken to make a budget using this method. With upcoming period it is decided what will be the

needs and costs required (Fullerton, Kennedy and Widener, 2014).

Advantages

Top level management in Nisa can easily identify the area where there is a waste of

money.

Through this the efficiency of various departments can be regulated as it helps in proper

allocation of resources in every field. The reason behind this is that ignorance of past

records and looking of actual figures. It helps in cost controlling by removing all unproductive activities and looking for new

opportunities. Communication and coordination in Nisa retail will also improve.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages

A lot of time and effort is required for making a zero base budget. Oppose of new ideas

and changes may be developed within a manger. Department like research development may not implement this as it would be very

difficult to justify every expenses involved in it (Grabner and Moers, 2013).

Fixed budgeting

It also known as static budget where there is no change in budget even when the sales

volumes changes. It stats that it will not change irrespective of change in level of production or

expenditures.

Advantages

As there are no changes made during a year it is very easy to implement and follow this

budget in Nisa retail.

The retail store can make changes in its strategy by estimating its revenue and expenses

by altering it in coming year. It helps to Nisa retail to take smart decisions on how to control their costs.

Disadvantages

Due to its lack of flexibility it resists the retail store to allocate additional resources for

further growth which will have negative an impact on revenues.

As it operates on one degree of activity it is not useful for unpredictable activity. It is not useful for small business or constantly fluctuating markets where decisions are

taken according to market situation (Lee, 2011).

Incremental budgeting

A budget of current fiscal year becomes the base for coming year's budget. A fixed

percentage is increased every year in budget.

Advantages

With greater amount of flexibility it allows for changing budget very quickly either in a

month or a year.

8

A lot of time and effort is required for making a zero base budget. Oppose of new ideas

and changes may be developed within a manger. Department like research development may not implement this as it would be very

difficult to justify every expenses involved in it (Grabner and Moers, 2013).

Fixed budgeting

It also known as static budget where there is no change in budget even when the sales

volumes changes. It stats that it will not change irrespective of change in level of production or

expenditures.

Advantages

As there are no changes made during a year it is very easy to implement and follow this

budget in Nisa retail.

The retail store can make changes in its strategy by estimating its revenue and expenses

by altering it in coming year. It helps to Nisa retail to take smart decisions on how to control their costs.

Disadvantages

Due to its lack of flexibility it resists the retail store to allocate additional resources for

further growth which will have negative an impact on revenues.

As it operates on one degree of activity it is not useful for unpredictable activity. It is not useful for small business or constantly fluctuating markets where decisions are

taken according to market situation (Lee, 2011).

Incremental budgeting

A budget of current fiscal year becomes the base for coming year's budget. A fixed

percentage is increased every year in budget.

Advantages

With greater amount of flexibility it allows for changing budget very quickly either in a

month or a year.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Helps in building value of equality among departments thus by avoiding conflicts

between various departments of the selected retailer thus by keeping everyone on same

page. As it is very simple to understand it allows to have stable budget every year and can

make gradual changes within Nisa retail.

Disadvantages

It often leads to unnecessary spendings on funds by managers which encourages higher

spendings in next year.

Method of working is same which leads to lack of new ideas and incentive for managers

and employees to reduce cost (Kotas, 2014.).

It does not allow few departments in Nisa to take larger risk as funds allocated by the

firm may be insufficient.

TASK 4

P5 Comparing ways through which Nisa Retail consider system of MA

When Nisa Retail store operates in the industry then various kinds of problems come into

consideration and for solving them some tools and methods are applied. This project talking

about financial issues and for resolving them some systems of MA are used by Nisa retailer

which are such as follows:

MA systems Description of such systems for resolving financial issues

Financial governance It is one of the small part of corporate governance which helps to

analyse outcomes generated from using financial resources at the

workplace of Nisa Retail store. Higher the implementation of this

particular system is highly supportive to determine that employees are

giving response using resources in which manner. When the

management finds that workers are giving positive response and

generates targeted income by utilising resources in optimum way then

performance will be considered as better (Grabner and Moers, 2013).

However, if the firm unable to perform well in retail industry of UK

then financial governance will support to assess causes and find put

9

between various departments of the selected retailer thus by keeping everyone on same

page. As it is very simple to understand it allows to have stable budget every year and can

make gradual changes within Nisa retail.

Disadvantages

It often leads to unnecessary spendings on funds by managers which encourages higher

spendings in next year.

Method of working is same which leads to lack of new ideas and incentive for managers

and employees to reduce cost (Kotas, 2014.).

It does not allow few departments in Nisa to take larger risk as funds allocated by the

firm may be insufficient.

TASK 4

P5 Comparing ways through which Nisa Retail consider system of MA

When Nisa Retail store operates in the industry then various kinds of problems come into

consideration and for solving them some tools and methods are applied. This project talking

about financial issues and for resolving them some systems of MA are used by Nisa retailer

which are such as follows:

MA systems Description of such systems for resolving financial issues

Financial governance It is one of the small part of corporate governance which helps to

analyse outcomes generated from using financial resources at the

workplace of Nisa Retail store. Higher the implementation of this

particular system is highly supportive to determine that employees are

giving response using resources in which manner. When the

management finds that workers are giving positive response and

generates targeted income by utilising resources in optimum way then

performance will be considered as better (Grabner and Moers, 2013).

However, if the firm unable to perform well in retail industry of UK

then financial governance will support to assess causes and find put

9

possible solutions.

Budgetary control The system in which basically two kinds of information compared

which are like budgeted or expected and then actual figures which will

be incurred at the end of year. If Nisa Retail Store finds that its targeted

data not achieved which is like enhance net profit or decrease cost etc.

then reasons will be also easily identified in this. In addition to this, it is

widely considered system as compared to all the other mentioned in the

current scenario. The reason is that, only two information required

which can be compared by non-financial employees also in the firm. In

addition to this, it is very simple as well as easy system of MA for

applying in the business smoothly and analyse performance in an

effectual direction.

Key performance

indicators

A procedure in which some basic symbols are used to identify business

performance of Nisa store in the retail sector. Herein, two types of

indicators are applied at the working environment which are like

financial and non-financial (Baldvinsdottir, Mitchell and Nørreklit,

2010). In order to determine that in terms of monetary concept

management capable to perform well or not then financial KPIs are

used. Some KPIs which belong from financials are such as net income,

sales revenue, return on investment, cost or expenses etc. On the

another side, some KPIs to measure non-financial performance are like

quality of products and services, satisfaction level of customers,

enhance market share etc. This system of MA is beneficial for assessing

both kinds of the performance in the industry.

Balanced scorecard At the end, an approach which helps to measure generally four kinds of

the business performance of Nisa Retail store is referred as balanced

scorecard (BSC). Under this four perspectives involved which are like

financial, learning and growth, customer as well as internal business

process. Considering to only financial perspective, management of

selected firm able to measure that whether it performs well or not

10

Budgetary control The system in which basically two kinds of information compared

which are like budgeted or expected and then actual figures which will

be incurred at the end of year. If Nisa Retail Store finds that its targeted

data not achieved which is like enhance net profit or decrease cost etc.

then reasons will be also easily identified in this. In addition to this, it is

widely considered system as compared to all the other mentioned in the

current scenario. The reason is that, only two information required

which can be compared by non-financial employees also in the firm. In

addition to this, it is very simple as well as easy system of MA for

applying in the business smoothly and analyse performance in an

effectual direction.

Key performance

indicators

A procedure in which some basic symbols are used to identify business

performance of Nisa store in the retail sector. Herein, two types of

indicators are applied at the working environment which are like

financial and non-financial (Baldvinsdottir, Mitchell and Nørreklit,

2010). In order to determine that in terms of monetary concept

management capable to perform well or not then financial KPIs are

used. Some KPIs which belong from financials are such as net income,

sales revenue, return on investment, cost or expenses etc. On the

another side, some KPIs to measure non-financial performance are like

quality of products and services, satisfaction level of customers,

enhance market share etc. This system of MA is beneficial for assessing

both kinds of the performance in the industry.

Balanced scorecard At the end, an approach which helps to measure generally four kinds of

the business performance of Nisa Retail store is referred as balanced

scorecard (BSC). Under this four perspectives involved which are like

financial, learning and growth, customer as well as internal business

process. Considering to only financial perspective, management of

selected firm able to measure that whether it performs well or not

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.