Detailed Analysis of Management Accounting for Flour Ltd - Report

VerifiedAdded on 2021/02/20

|16

|3370

|22

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on their practical application within Flour Ltd., an engineering company. It covers various aspects, including the significance of different management accounting systems like cost accounting and inventory management, and their role in integrating business activities with management reports. The report details costing methods, such as marginal and absorption costing, and reconciles income statements. It further explores the advantages and disadvantages of planning tools like variance analysis and zero-based budgeting, providing insights into budgetary control. The study also examines how organizations utilize management accounting systems to address financial challenges, identifying key performance indicators and budgetary targets. Numerical examples and case studies support the analysis, offering a comprehensive understanding of management accounting principles and their real-world application. The report provides a thorough overview of how management accounting supports effective decision-making and financial management within a business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

P1:-Management accounting and essential requirements of different types of management

accounting system..................................................................................................................3

P2:-Different methods used for management accounting reporting:.....................................5

LO2..................................................................................................................................................6

P3:-Calculation of Costs using techniques of Cost Analysis:-...............................................6

LO3..................................................................................................................................................7

P4:-Different Types of Planning tools of Budgetary Control and their advantages and

disadvantages:-.......................................................................................................................7

LO4 .................................................................................................................................................9

P5:- Organizations are adopting management accounting systems to respond to financial

problems:................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

P1:-Management accounting and essential requirements of different types of management

accounting system..................................................................................................................3

P2:-Different methods used for management accounting reporting:.....................................5

LO2..................................................................................................................................................6

P3:-Calculation of Costs using techniques of Cost Analysis:-...............................................6

LO3..................................................................................................................................................7

P4:-Different Types of Planning tools of Budgetary Control and their advantages and

disadvantages:-.......................................................................................................................7

LO4 .................................................................................................................................................9

P5:- Organizations are adopting management accounting systems to respond to financial

problems:................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION

Management accounting can be described as application to manage accounts of business

unit so that firm can take effective funds decision to generate more revenues applying knowledge

and skills for preparing accounting reports. These reports helps management in preparing

strategies and policies to control and plan activities of undertaking. Flour Ltd. is a leading

engineering company offers procurement, project management and maintenance and engineering

services for clients in the UK. This study includes the description of activities like importance of

various systems of management accounting, and their importance for integrating activities of

business with reports of management accounting. It will show calculations of various costing

methods like marginal and absorption. Difference in income statements of the methods are

reconciled by preparing reconciliation statement. In addition, strength and weakness of planning

tools will be explained. Report will cover explanation on different budgetary control planning

tools. Report will give understanding about various concepts of management accounting using

numerical examples.

LO1

P1:-

MA deals with interpreting, analyzing, identifying and presenting accounting information

that is obtained with help of cost and financial accounting. It helps executives of company in

formulating policies, taking decisions and for carrying out daily operations of company. It is

used for preparing management accounts and reports which give timely and accurate financial &

statistical to executives for framing short term & long term decision. Management accounting

tool is used for analyzing the business information and its financial activities. It is useful device

which supports in making sound decision for daily activities. This is the process which makes the

person able to analyses unnecessary cost and find proper solution to handle overcasting issues in

the organization (Ibarrondo-Dávila and et.al., 2015).

types of management accounting system and essential requirements:

Requirements of different management accounting system are explained as below

Cost accounting : This is used to manage cost and minimize production cost of

company. By using this technique form can control over the cost and can raise profit as

well.

Management accounting can be described as application to manage accounts of business

unit so that firm can take effective funds decision to generate more revenues applying knowledge

and skills for preparing accounting reports. These reports helps management in preparing

strategies and policies to control and plan activities of undertaking. Flour Ltd. is a leading

engineering company offers procurement, project management and maintenance and engineering

services for clients in the UK. This study includes the description of activities like importance of

various systems of management accounting, and their importance for integrating activities of

business with reports of management accounting. It will show calculations of various costing

methods like marginal and absorption. Difference in income statements of the methods are

reconciled by preparing reconciliation statement. In addition, strength and weakness of planning

tools will be explained. Report will cover explanation on different budgetary control planning

tools. Report will give understanding about various concepts of management accounting using

numerical examples.

LO1

P1:-

MA deals with interpreting, analyzing, identifying and presenting accounting information

that is obtained with help of cost and financial accounting. It helps executives of company in

formulating policies, taking decisions and for carrying out daily operations of company. It is

used for preparing management accounts and reports which give timely and accurate financial &

statistical to executives for framing short term & long term decision. Management accounting

tool is used for analyzing the business information and its financial activities. It is useful device

which supports in making sound decision for daily activities. This is the process which makes the

person able to analyses unnecessary cost and find proper solution to handle overcasting issues in

the organization (Ibarrondo-Dávila and et.al., 2015).

types of management accounting system and essential requirements:

Requirements of different management accounting system are explained as below

Cost accounting : This is used to manage cost and minimize production cost of

company. By using this technique form can control over the cost and can raise profit as

well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There is requirements to have great cooperation between several departments. This

helps in utilizing resources in efficient manner.

Apart from this, there is need to have flexible process so that requirements of

different stakeholders can be met effectively. (Eldenburg and et.al., 2019).

Inventory management system:- This is another system which ensure effective

controlling and monitoring over stock. Organizational processes of Flour ltd for

achieving effective and efficient flow of stock in organization & at point of sales. By this

way wastage of inventory can be avoided. Firm has to involve only such stock that is

demand of market otherwise it may increase cost of the firm. The essential requirements

in MA are follows:

Forecasting: It is helpful in preparing proper plan to manage cost so that company’s

requirements can be matched. (Ammar, 2017).

This is helpful in reducing cost of the organization and effectively managing the

inventory.

Job Costing System:- It records actual cost of material & labor relating to specific job

and overheads are assigned over a predetermined rate to jobs. It comes in use when

products manufactured are different from one another and are having significant costs. It

pays attention on cost related to specific job, it ensures that no job is there which has over

costing issue. It is the tool which is used to record all cost in effective manner. By this

way order receiving can be managed properly so that correct pricing can be set

(Steccolini, 2019). Manager of company prepare report and estimate cost by looking at

various jobs. Essentials of this costing system includes receiving inquiry, estimate job

costing, receiving order, production order, cost recording and job completion.

Price Optimizing System:-This is another system which helps in controlling over

resource pricing. It is the beneficial tool which aids in determining the level of prices in

proper manner. By this way company can manage demand and can set prices as per the

requirements of consumers. This also enables company to decide prices of different

products at single point of time. This system is used to determine price levels for

customers by gathering responses over different price level.

helps in utilizing resources in efficient manner.

Apart from this, there is need to have flexible process so that requirements of

different stakeholders can be met effectively. (Eldenburg and et.al., 2019).

Inventory management system:- This is another system which ensure effective

controlling and monitoring over stock. Organizational processes of Flour ltd for

achieving effective and efficient flow of stock in organization & at point of sales. By this

way wastage of inventory can be avoided. Firm has to involve only such stock that is

demand of market otherwise it may increase cost of the firm. The essential requirements

in MA are follows:

Forecasting: It is helpful in preparing proper plan to manage cost so that company’s

requirements can be matched. (Ammar, 2017).

This is helpful in reducing cost of the organization and effectively managing the

inventory.

Job Costing System:- It records actual cost of material & labor relating to specific job

and overheads are assigned over a predetermined rate to jobs. It comes in use when

products manufactured are different from one another and are having significant costs. It

pays attention on cost related to specific job, it ensures that no job is there which has over

costing issue. It is the tool which is used to record all cost in effective manner. By this

way order receiving can be managed properly so that correct pricing can be set

(Steccolini, 2019). Manager of company prepare report and estimate cost by looking at

various jobs. Essentials of this costing system includes receiving inquiry, estimate job

costing, receiving order, production order, cost recording and job completion.

Price Optimizing System:-This is another system which helps in controlling over

resource pricing. It is the beneficial tool which aids in determining the level of prices in

proper manner. By this way company can manage demand and can set prices as per the

requirements of consumers. This also enables company to decide prices of different

products at single point of time. This system is used to determine price levels for

customers by gathering responses over different price level.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2

There are several reports which are used to prepare accounts. This is the tool which helps

management in making sound decisions and analyzing data in reliable manner. By this way

organisation can generate profit in significant manner. Various reports that are prepared by

management & their advantages are discussed as below:

Budgeting Reports:- This is the tool that helps in analyzing the actual expenses which

are occurring in daily operations. By this way firm can know where is over allocation or

where is over expenses. By this way enterprise can prepare good budget where all the

overall allocation of funds can be managed properly. (McLean, McGovern and Davie,

2015).

Cost report:-These report are prepared by considering prices of product, overheads,

labour costs both variable & fixed. In cost reports, the cost informations are collected &

final reports are prepared to made available the production cost of goods and selling price

of goods. It also helps the manager in planning income and expenses limits.

Execution report:- These reports give information related to status of tests efforts &

tests execution progress as against planned progress. Management accountants with the

use of budgeted plan made applicable income and expenses in appropriate manner. Every

year, the performance report is made to analyse the strength and weakness every month

and the help of these analysis reports, the company owner can prepare the future

strategies and plans to achieve the long term success. The other account reports are made

by the skilled accountants and the reports of the orders gives the information about the

order summery and by this way, the higher authorities or the personnels like managers

evaluate the performance and this reports gives the clear vision of growth in present and

future. (Sands, and.et.al., 2015).

Inventory & manufacturing report:- Companies also prepares the manufacturing and

inventory reports identifying dispatch & inwards of orders and this process makes the

organization more efficient. This kind of report contains the per labour cost, e-waste

which is useless for the company and the data mining helps the managers to compare the

obtained budget with the original budget and also evaluate the area which requires an

improvement.

There are several reports which are used to prepare accounts. This is the tool which helps

management in making sound decisions and analyzing data in reliable manner. By this way

organisation can generate profit in significant manner. Various reports that are prepared by

management & their advantages are discussed as below:

Budgeting Reports:- This is the tool that helps in analyzing the actual expenses which

are occurring in daily operations. By this way firm can know where is over allocation or

where is over expenses. By this way enterprise can prepare good budget where all the

overall allocation of funds can be managed properly. (McLean, McGovern and Davie,

2015).

Cost report:-These report are prepared by considering prices of product, overheads,

labour costs both variable & fixed. In cost reports, the cost informations are collected &

final reports are prepared to made available the production cost of goods and selling price

of goods. It also helps the manager in planning income and expenses limits.

Execution report:- These reports give information related to status of tests efforts &

tests execution progress as against planned progress. Management accountants with the

use of budgeted plan made applicable income and expenses in appropriate manner. Every

year, the performance report is made to analyse the strength and weakness every month

and the help of these analysis reports, the company owner can prepare the future

strategies and plans to achieve the long term success. The other account reports are made

by the skilled accountants and the reports of the orders gives the information about the

order summery and by this way, the higher authorities or the personnels like managers

evaluate the performance and this reports gives the clear vision of growth in present and

future. (Sands, and.et.al., 2015).

Inventory & manufacturing report:- Companies also prepares the manufacturing and

inventory reports identifying dispatch & inwards of orders and this process makes the

organization more efficient. This kind of report contains the per labour cost, e-waste

which is useless for the company and the data mining helps the managers to compare the

obtained budget with the original budget and also evaluate the area which requires an

improvement.

Job costing report:-This report helps to identify the costs, expenses & the profits

generated from the project or the task. This report also analyse the important aspects of

the project required which helps the company in giving more efforts on the projects and

the company which are more profitable than the less profitable business activities.

Performance report – It addresses outcomes of activity or work of individuals. This

report enables comparison between actual outcomes and standards. Variances are

identified between two reports are identified. Performance reports are use to analyse the

performance of activities that are performed in company.

Account receivable report:-This kind of reports deals with managing account of the

company which are more into the customary services or deals with the customers on a

daily basis. The proper organization of amount of credit available, paid, received during

the year. It analyses the problem related to the collection. This collected data helps in

reducing the loss percentage and the debts of the company to maintain the liquidity.

(Chenhall and Moers, 2015).

LO2

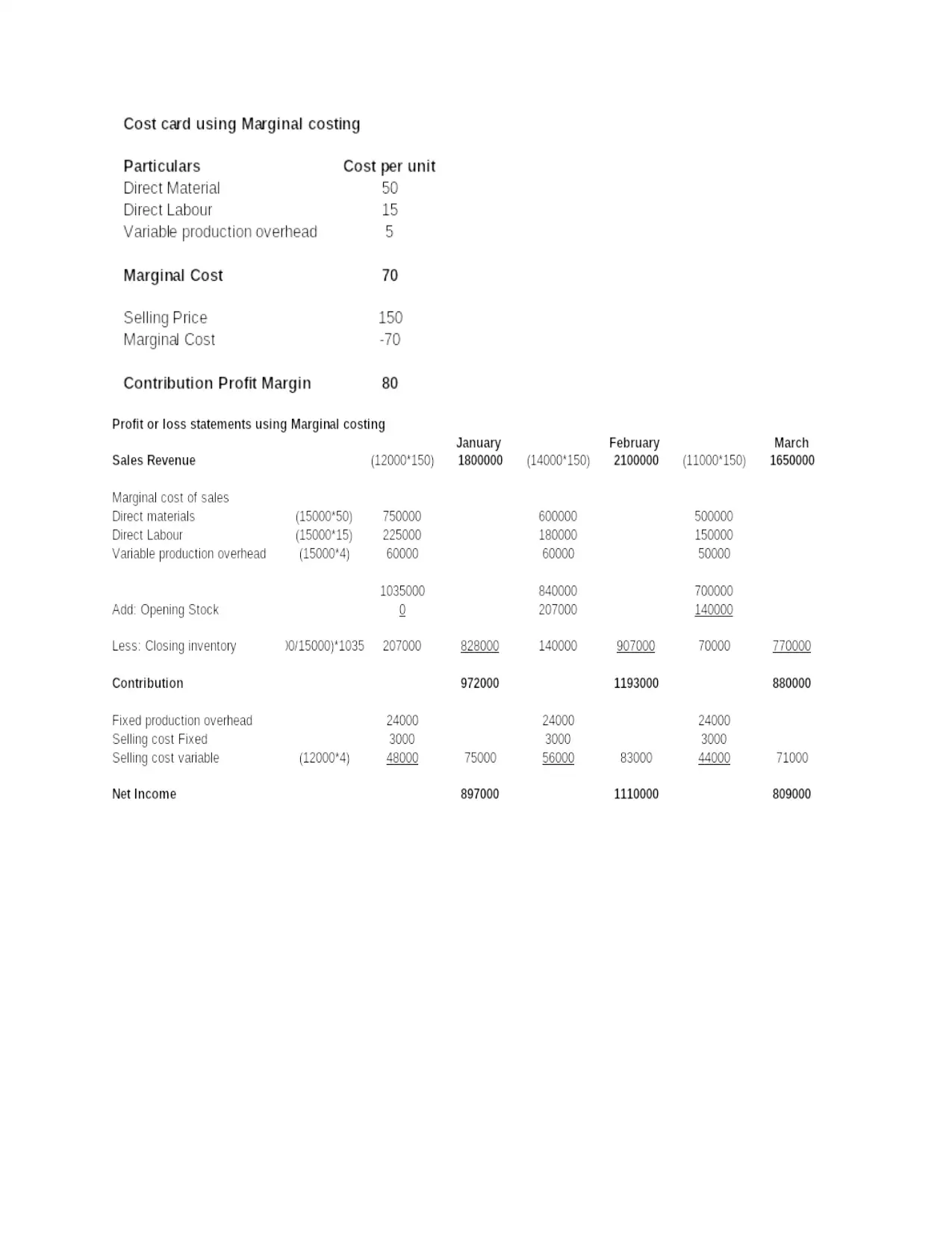

P3:

Annex A:-Case 1

Annex B:-Case 2

LO3

P4:-Types of Planning tools for Budgetary Control and the suitable advantages and

disadvantages:-

Planning tools in budgetary control are used for forecasting and planning company's

budget which will be executed in performing the operations of Fluor Ltd. to achieve its

objectives. These days the Fluor Ltd. is becoming more advance in preparing their strategies as

the management has shifted its focus from traditional budgeting tool to cloud based budgeting

tools and soft-wares. These tools offer better options to the company for planning their budgets

in a systematic and organized manner:-

Variance Analysis:- It refers to quantitative examination of variations between planned and

actual performance. The analysis of variances is used for controlling the operations of Fluor Ltd.

generated from the project or the task. This report also analyse the important aspects of

the project required which helps the company in giving more efforts on the projects and

the company which are more profitable than the less profitable business activities.

Performance report – It addresses outcomes of activity or work of individuals. This

report enables comparison between actual outcomes and standards. Variances are

identified between two reports are identified. Performance reports are use to analyse the

performance of activities that are performed in company.

Account receivable report:-This kind of reports deals with managing account of the

company which are more into the customary services or deals with the customers on a

daily basis. The proper organization of amount of credit available, paid, received during

the year. It analyses the problem related to the collection. This collected data helps in

reducing the loss percentage and the debts of the company to maintain the liquidity.

(Chenhall and Moers, 2015).

LO2

P3:

Annex A:-Case 1

Annex B:-Case 2

LO3

P4:-Types of Planning tools for Budgetary Control and the suitable advantages and

disadvantages:-

Planning tools in budgetary control are used for forecasting and planning company's

budget which will be executed in performing the operations of Fluor Ltd. to achieve its

objectives. These days the Fluor Ltd. is becoming more advance in preparing their strategies as

the management has shifted its focus from traditional budgeting tool to cloud based budgeting

tools and soft-wares. These tools offer better options to the company for planning their budgets

in a systematic and organized manner:-

Variance Analysis:- It refers to quantitative examination of variations between planned and

actual performance. The analysis of variances is used for controlling the operations of Fluor Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

When the management analyses amount of variances over trend line than this analysis becomes

more effective as sudden monthly changes in variance level are more apparent. This level of

variance helps management in understanding the fluctuations occurring in business & for

knowing ways for changing the situations(Speckbacher, 2017).

Advantages:-The variance analysis helps to identify the reasons behind overall

variances so that remedial decisions can be taken by company. It also focuses on

inefficient performances of Fluor Ltd and its extent of inefficiency. Sub-divisions of

Variances reveals the relationship among various variances. this variance analysis is

useful for fixing responsibilities of a departments or individuals or sections for every

variances separately & also for cost control(Weetman and.et.al.2019).

Disadvantages:-The accounts manager of Fluor Ltd ensures the variances at the end of

the month but the management requires feedback much faster than a month so this leads

to delay in work. The accounts executive has to sort through various information such as

labor routing, bills of materials and overtime records to ascertain the reasons of the

problems as these reasons are not located in the accounting records. Since Variance

analysis determines the comparison of actual performance with planned performance

which can also derive from political bargaining so consequently it does not ascertain any

useful information(Uyar and Kuzey, 2016).

Zero Based Budgeting:-Any activity at the starting of each year is set at zero in Zero Based

Budget. All expenses must be justified on a cost or benefit basis which also involves justification

of continuing existence. These Budgets help the Fluor Ltd. to integrate the managerial functions

of planning and control. Sometimes the previous year's budget of the Fluor Ltd. may have some

drawbacks so all these errors are corrected in Zero Based Budget.

Advantages:-The Fluor Ltd receives many benefits of Zero Based Budgeting. This

budgeting helps in cost saving as various expenses are incurred by the company in

inefficient performances so it is useful for controlling the cost. The cost saving also leads

to better utilization of resources of Fluor Ltd. The Zero Based Budgeting forces the

management to actively participate in the budgeting process which is useful for careful

planning of Fluor Ltd(Dekker, 2016).

Disadvantages:-Since Fluor Ltd. large number of decision packages are prepared and it

includes more expenses. It also includes more paper work which is a time consuming

more effective as sudden monthly changes in variance level are more apparent. This level of

variance helps management in understanding the fluctuations occurring in business & for

knowing ways for changing the situations(Speckbacher, 2017).

Advantages:-The variance analysis helps to identify the reasons behind overall

variances so that remedial decisions can be taken by company. It also focuses on

inefficient performances of Fluor Ltd and its extent of inefficiency. Sub-divisions of

Variances reveals the relationship among various variances. this variance analysis is

useful for fixing responsibilities of a departments or individuals or sections for every

variances separately & also for cost control(Weetman and.et.al.2019).

Disadvantages:-The accounts manager of Fluor Ltd ensures the variances at the end of

the month but the management requires feedback much faster than a month so this leads

to delay in work. The accounts executive has to sort through various information such as

labor routing, bills of materials and overtime records to ascertain the reasons of the

problems as these reasons are not located in the accounting records. Since Variance

analysis determines the comparison of actual performance with planned performance

which can also derive from political bargaining so consequently it does not ascertain any

useful information(Uyar and Kuzey, 2016).

Zero Based Budgeting:-Any activity at the starting of each year is set at zero in Zero Based

Budget. All expenses must be justified on a cost or benefit basis which also involves justification

of continuing existence. These Budgets help the Fluor Ltd. to integrate the managerial functions

of planning and control. Sometimes the previous year's budget of the Fluor Ltd. may have some

drawbacks so all these errors are corrected in Zero Based Budget.

Advantages:-The Fluor Ltd receives many benefits of Zero Based Budgeting. This

budgeting helps in cost saving as various expenses are incurred by the company in

inefficient performances so it is useful for controlling the cost. The cost saving also leads

to better utilization of resources of Fluor Ltd. The Zero Based Budgeting forces the

management to actively participate in the budgeting process which is useful for careful

planning of Fluor Ltd(Dekker, 2016).

Disadvantages:-Since Fluor Ltd. large number of decision packages are prepared and it

includes more expenses. It also includes more paper work which is a time consuming

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

process. The communication and administration of Zero Based Budgeting may create

many problems and even there can be partiality in the ranking of decision packages.

Operating Budget:-An operational budget is financial strategy prepared to meet debt obligations

and to sustain growth of Fluor Ltd. This budget helps the management to identify the essential

requirements of spending the cash of company(Van der Stede, 2016).

Advantages:- Operational budget helps Fluor Ltd. to predict its cost and analyse its short

term spending to face its long term financial liabilities. Preparing of operational budget

gives financial freedom for meeting unanticipated costs and seizing new opportunities. It

also helps to keep information accurate.

Disadvantages:-In preparation of operating budget the actual costs for performing the

functions of each department may vary from the allocations made by the management.

This budget specifies the amount of spending but it does not determine the way of

allocating these spending evenly to each department(Booth, 2018).

Case Solutions

Annex C:-

Annex D:-

Annex E:-

LO4

P5: Identification of financial problems by using benchmarks, financial and non financial key

performance indicators & budgetary targets

There are several techniques of accounts management which set some threshold value in

identifying the financial and non-financial factors and this factors helps in analyzing the

performance of an organization and helps to achieve long-term objectives efficiently. The

Budgetary control also helps to plan and execute different activities of business which give

success to Fluor and assist organization in focusing over goals and achievements which are

required to complete the objective and also support the organization to achieve long term

objectives and goals.(Zeng, 2018).

Key performance indicator is used for measuring performance of an organization which can be

financial and non-financial or any other factors that helps the organization for achieving long

term goal which are given as follows-

many problems and even there can be partiality in the ranking of decision packages.

Operating Budget:-An operational budget is financial strategy prepared to meet debt obligations

and to sustain growth of Fluor Ltd. This budget helps the management to identify the essential

requirements of spending the cash of company(Van der Stede, 2016).

Advantages:- Operational budget helps Fluor Ltd. to predict its cost and analyse its short

term spending to face its long term financial liabilities. Preparing of operational budget

gives financial freedom for meeting unanticipated costs and seizing new opportunities. It

also helps to keep information accurate.

Disadvantages:-In preparation of operating budget the actual costs for performing the

functions of each department may vary from the allocations made by the management.

This budget specifies the amount of spending but it does not determine the way of

allocating these spending evenly to each department(Booth, 2018).

Case Solutions

Annex C:-

Annex D:-

Annex E:-

LO4

P5: Identification of financial problems by using benchmarks, financial and non financial key

performance indicators & budgetary targets

There are several techniques of accounts management which set some threshold value in

identifying the financial and non-financial factors and this factors helps in analyzing the

performance of an organization and helps to achieve long-term objectives efficiently. The

Budgetary control also helps to plan and execute different activities of business which give

success to Fluor and assist organization in focusing over goals and achievements which are

required to complete the objective and also support the organization to achieve long term

objectives and goals.(Zeng, 2018).

Key performance indicator is used for measuring performance of an organization which can be

financial and non-financial or any other factors that helps the organization for achieving long

term goal which are given as follows-

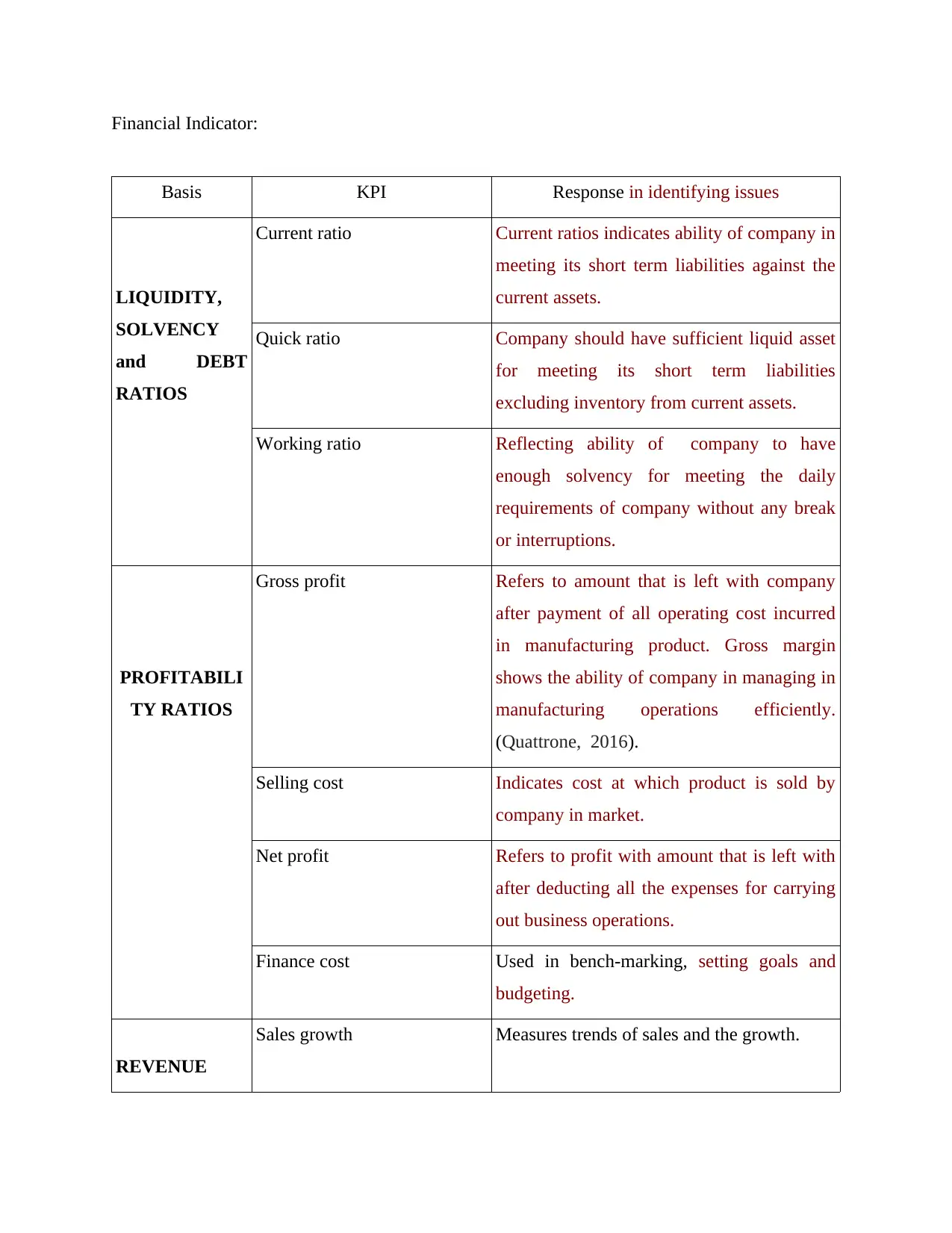

Financial Indicator:

Basis KPI Response in identifying issues

LIQUIDITY,

SOLVENCY

and DEBT

RATIOS

Current ratio Current ratios indicates ability of company in

meeting its short term liabilities against the

current assets.

Quick ratio Company should have sufficient liquid asset

for meeting its short term liabilities

excluding inventory from current assets.

Working ratio Reflecting ability of company to have

enough solvency for meeting the daily

requirements of company without any break

or interruptions.

PROFITABILI

TY RATIOS

Gross profit Refers to amount that is left with company

after payment of all operating cost incurred

in manufacturing product. Gross margin

shows the ability of company in managing in

manufacturing operations efficiently.

(Quattrone, 2016).

Selling cost Indicates cost at which product is sold by

company in market.

Net profit Refers to profit with amount that is left with

after deducting all the expenses for carrying

out business operations.

Finance cost Used in bench-marking, setting goals and

budgeting.

REVENUE

Sales growth Measures trends of sales and the growth.

Basis KPI Response in identifying issues

LIQUIDITY,

SOLVENCY

and DEBT

RATIOS

Current ratio Current ratios indicates ability of company in

meeting its short term liabilities against the

current assets.

Quick ratio Company should have sufficient liquid asset

for meeting its short term liabilities

excluding inventory from current assets.

Working ratio Reflecting ability of company to have

enough solvency for meeting the daily

requirements of company without any break

or interruptions.

PROFITABILI

TY RATIOS

Gross profit Refers to amount that is left with company

after payment of all operating cost incurred

in manufacturing product. Gross margin

shows the ability of company in managing in

manufacturing operations efficiently.

(Quattrone, 2016).

Selling cost Indicates cost at which product is sold by

company in market.

Net profit Refers to profit with amount that is left with

after deducting all the expenses for carrying

out business operations.

Finance cost Used in bench-marking, setting goals and

budgeting.

REVENUE

Sales growth Measures trends of sales and the growth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

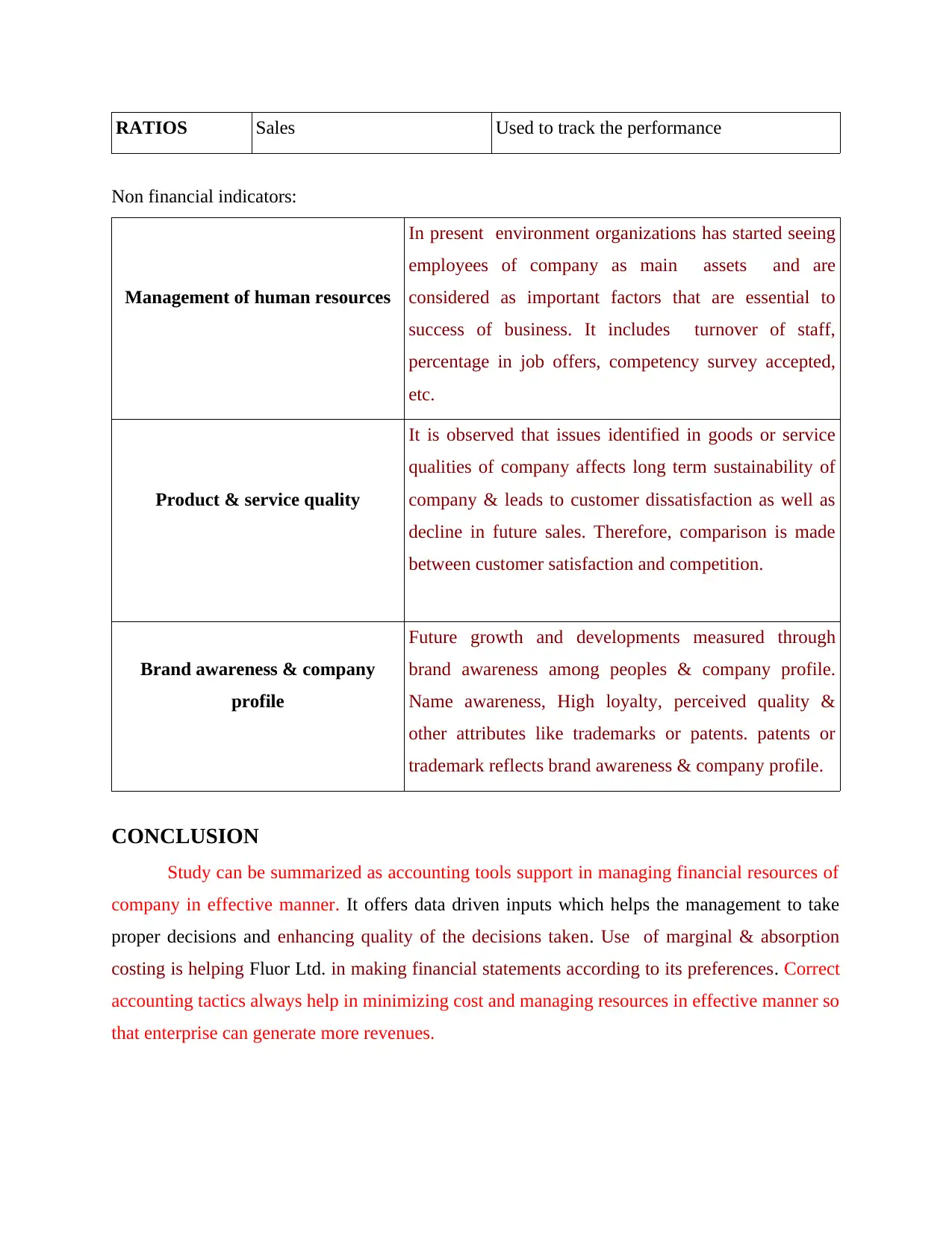

RATIOS Sales Used to track the performance

Non financial indicators:

Management of human resources

In present environment organizations has started seeing

employees of company as main assets and are

considered as important factors that are essential to

success of business. It includes turnover of staff,

percentage in job offers, competency survey accepted,

etc.

Product & service quality

It is observed that issues identified in goods or service

qualities of company affects long term sustainability of

company & leads to customer dissatisfaction as well as

decline in future sales. Therefore, comparison is made

between customer satisfaction and competition.

Brand awareness & company

profile

Future growth and developments measured through

brand awareness among peoples & company profile.

Name awareness, High loyalty, perceived quality &

other attributes like trademarks or patents. patents or

trademark reflects brand awareness & company profile.

CONCLUSION

Study can be summarized as accounting tools support in managing financial resources of

company in effective manner. It offers data driven inputs which helps the management to take

proper decisions and enhancing quality of the decisions taken. Use of marginal & absorption

costing is helping Fluor Ltd. in making financial statements according to its preferences. Correct

accounting tactics always help in minimizing cost and managing resources in effective manner so

that enterprise can generate more revenues.

Non financial indicators:

Management of human resources

In present environment organizations has started seeing

employees of company as main assets and are

considered as important factors that are essential to

success of business. It includes turnover of staff,

percentage in job offers, competency survey accepted,

etc.

Product & service quality

It is observed that issues identified in goods or service

qualities of company affects long term sustainability of

company & leads to customer dissatisfaction as well as

decline in future sales. Therefore, comparison is made

between customer satisfaction and competition.

Brand awareness & company

profile

Future growth and developments measured through

brand awareness among peoples & company profile.

Name awareness, High loyalty, perceived quality &

other attributes like trademarks or patents. patents or

trademark reflects brand awareness & company profile.

CONCLUSION

Study can be summarized as accounting tools support in managing financial resources of

company in effective manner. It offers data driven inputs which helps the management to take

proper decisions and enhancing quality of the decisions taken. Use of marginal & absorption

costing is helping Fluor Ltd. in making financial statements according to its preferences. Correct

accounting tactics always help in minimizing cost and managing resources in effective manner so

that enterprise can generate more revenues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:-

AbRahman, N.A., and.et.al., 2016. Improving employees accountability and firm performance

through management accounting practices. Procedia Economics and Finance, 35, pp.92-

98.

Ammar, S., 2017. Enterprise systems, business process management and UK-management

accounting practices: Cross-sectional case studies. Qualitative Research in Accounting &

Management. 14(3). pp.230-281.

Bedford, D.S. and Spekle, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Dekker, H.C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research. 31. pp.86-99.

Kaplan, R.S. and et.al., 2015. Advanced management accounting. PHI Learning.

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and the

management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review. 47(2). pp.177-190.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Sands, J., and.et.al., 2015. Environmental Management Accounting (EMA) for environmental

management and organizational change. Journal of Accounting & Organizational Change.

Speckbacher, G., 2017. Creativity research in management accounting: A commentary. Journal

of Management Accounting Research.29(3).pp.49-54.

Uyar, A. and Kuzey, C., 2016. Does management accounting mediate the relationship between

cost system design and performance?. Advances in accounting. 35. pp.170-176.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

Weetman, P., and.et.al., 2019. Financial and management accounting. Pearson UK.

Zeng, H., 2018. Reciprocal Interaction between Management Accounting and Other

Management Roles. Open Access Library Journal. 5(11). p.1.

APPENDIX

Annex A

Books and Journals:-

AbRahman, N.A., and.et.al., 2016. Improving employees accountability and firm performance

through management accounting practices. Procedia Economics and Finance, 35, pp.92-

98.

Ammar, S., 2017. Enterprise systems, business process management and UK-management

accounting practices: Cross-sectional case studies. Qualitative Research in Accounting &

Management. 14(3). pp.230-281.

Bedford, D.S. and Spekle, R.F., 2018. Construct validity in survey-based management

accounting and control research. Journal of Management Accounting Research. 30(2).

pp.23-58.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

Dekker, H.C., 2016. On the boundaries between intrafirm and interfirm management accounting

research. Management Accounting Research. 31. pp.86-99.

Kaplan, R.S. and et.al., 2015. Advanced management accounting. PHI Learning.

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and the

management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review. 47(2). pp.177-190.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Sands, J., and.et.al., 2015. Environmental Management Accounting (EMA) for environmental

management and organizational change. Journal of Accounting & Organizational Change.

Speckbacher, G., 2017. Creativity research in management accounting: A commentary. Journal

of Management Accounting Research.29(3).pp.49-54.

Uyar, A. and Kuzey, C., 2016. Does management accounting mediate the relationship between

cost system design and performance?. Advances in accounting. 35. pp.170-176.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

Weetman, P., and.et.al., 2019. Financial and management accounting. Pearson UK.

Zeng, H., 2018. Reciprocal Interaction between Management Accounting and Other

Management Roles. Open Access Library Journal. 5(11). p.1.

APPENDIX

Annex A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.