Management Accounting Report: Antonio Ltd and Toscanini Ltd

VerifiedAdded on 2020/02/03

|17

|3877

|118

Report

AI Summary

This management accounting report delves into cost classification, exploring various cost elements and behaviors for Bittern Manufacturers Ltd. It examines costing methods, comparing variable and absorption costing systems, and analyzes cost data using appropriate techniques. The report further covers budgeting processes, preparing trade payable, cash, and raw material budgets for Antonio Ltd, with recommendations for improvement. Finally, it analyzes variances for Toscanini Ltd, identifying causes and suggesting corrective actions, culminating in an operating statement and findings report for management. The report provides a comprehensive overview of financial analysis and decision-making within a business context.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Classify different types of cost with examples for Bittern Manufacturers Ltd..........................4

1.3 Meaning and comparative evaluation of variable and absorption costing system....................6

1.4 Analysis of cost data using appropriate technique and its purpose............................................7

TASK 2 ................................................................................................................................................8

TASK 3 ................................................................................................................................................8

3.1 Explain the purpose and nature of budgeting process adopted..................................................8

3.2 Meaning of budgeting method used for Antonio Ltd and its need with required advices and

suggestions.......................................................................................................................................9

3.3 Preparation of budget and purpose of the method...................................................................10

3.4 Preparing budgets for Antonio Ltd..........................................................................................10

TASK 4...............................................................................................................................................11

4.1 Identify calculation of variances and its possible causes and corrective actions.....................11

4.2 Preparing operating statement to deduce budgeting profit......................................................13

4.3 Report findings to the management.........................................................................................14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................16

2

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 Classify different types of cost with examples for Bittern Manufacturers Ltd..........................4

1.3 Meaning and comparative evaluation of variable and absorption costing system....................6

1.4 Analysis of cost data using appropriate technique and its purpose............................................7

TASK 2 ................................................................................................................................................8

TASK 3 ................................................................................................................................................8

3.1 Explain the purpose and nature of budgeting process adopted..................................................8

3.2 Meaning of budgeting method used for Antonio Ltd and its need with required advices and

suggestions.......................................................................................................................................9

3.3 Preparation of budget and purpose of the method...................................................................10

3.4 Preparing budgets for Antonio Ltd..........................................................................................10

TASK 4...............................................................................................................................................11

4.1 Identify calculation of variances and its possible causes and corrective actions.....................11

4.2 Preparing operating statement to deduce budgeting profit......................................................13

4.3 Report findings to the management.........................................................................................14

CONCLUSION..................................................................................................................................14

REFERENCES...................................................................................................................................16

2

Index of Tables

Table 1: Comparative analysis of variable and absorption costing......................................................7

Table 2: Calculation of Bittern Ltd's cost and profitability using variable costing .............................8

Table 3: Calculation of Bittern Ltd's cost and profitability using absorption costing ........................9

Table 4: Material purchase budget of Antonio Ltd ............................................................................11

Table 5: Trade payable budget of Antonio Ltd ..................................................................................11

Table 6: Cash budget of Antonio Ltd. ................................................................................................11

Table 7: Calculation of total sales ......................................................................................................12

Table 8: Calculation of variances for Toscanini Ltd...........................................................................12

Table 9: Reasons for variance and corrective actions ........................................................................13

Table 10: Operating reconciliation statement of Toscanini Ltd..........................................................14

Illustration Index

Illustration 1: Element of cost .............................................................................................................5

Illustration 2: Cost behaviour ..............................................................................................................6

3

Table 1: Comparative analysis of variable and absorption costing......................................................7

Table 2: Calculation of Bittern Ltd's cost and profitability using variable costing .............................8

Table 3: Calculation of Bittern Ltd's cost and profitability using absorption costing ........................9

Table 4: Material purchase budget of Antonio Ltd ............................................................................11

Table 5: Trade payable budget of Antonio Ltd ..................................................................................11

Table 6: Cash budget of Antonio Ltd. ................................................................................................11

Table 7: Calculation of total sales ......................................................................................................12

Table 8: Calculation of variances for Toscanini Ltd...........................................................................12

Table 9: Reasons for variance and corrective actions ........................................................................13

Table 10: Operating reconciliation statement of Toscanini Ltd..........................................................14

Illustration Index

Illustration 1: Element of cost .............................................................................................................5

Illustration 2: Cost behaviour ..............................................................................................................6

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of examining and evaluating financial business

performance, cost report and market analysis to take better decisions for the success of an

organizations. Bittern Ltd is a manufacturing organization which sell single product to the

customers on a uniform selling price. This assignment explore the study of cost classification,

methods and techniques to ascertain product cost. Moreover, various types of performance

indicators will be determined and suggestions will be acquired to reduce cost, and improve quality

and business value for Next Plc. Furthermore, budgeting methods and budgets like trade payable,

cash and raw material budget will be prepared for Antonio Ltd. In end, variance will be analysed to

take decisions to remove negative results and achieve targets.

TASK 1

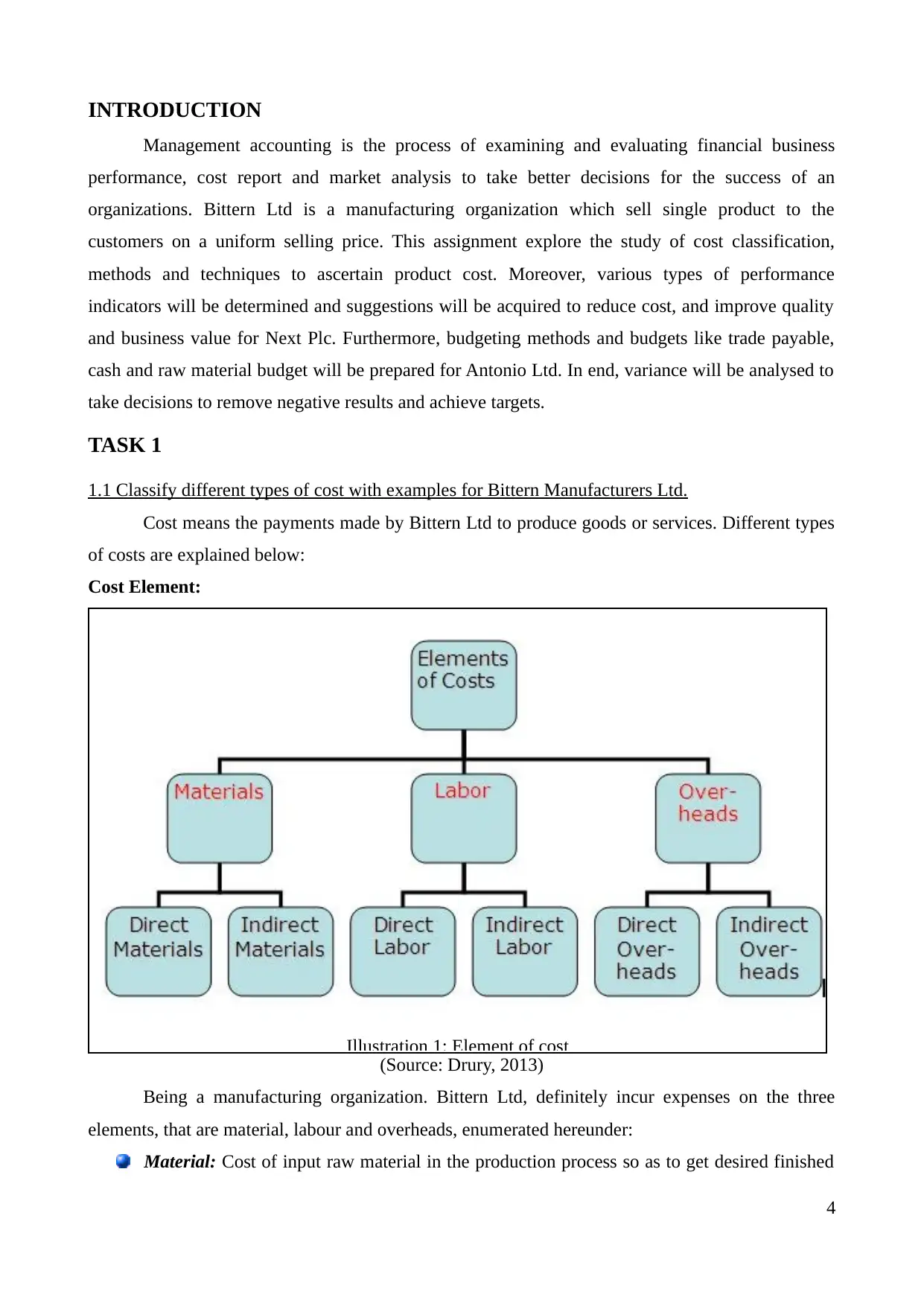

1.1 Classify different types of cost with examples for Bittern Manufacturers Ltd.

Cost means the payments made by Bittern Ltd to produce goods or services. Different types

of costs are explained below:

Cost Element:

Illustration 1: Element of cost

(Source: Drury, 2013)

Being a manufacturing organization. Bittern Ltd, definitely incur expenses on the three

elements, that are material, labour and overheads, enumerated hereunder:

Material: Cost of input raw material in the production process so as to get desired finished

4

Management accounting is the process of examining and evaluating financial business

performance, cost report and market analysis to take better decisions for the success of an

organizations. Bittern Ltd is a manufacturing organization which sell single product to the

customers on a uniform selling price. This assignment explore the study of cost classification,

methods and techniques to ascertain product cost. Moreover, various types of performance

indicators will be determined and suggestions will be acquired to reduce cost, and improve quality

and business value for Next Plc. Furthermore, budgeting methods and budgets like trade payable,

cash and raw material budget will be prepared for Antonio Ltd. In end, variance will be analysed to

take decisions to remove negative results and achieve targets.

TASK 1

1.1 Classify different types of cost with examples for Bittern Manufacturers Ltd.

Cost means the payments made by Bittern Ltd to produce goods or services. Different types

of costs are explained below:

Cost Element:

Illustration 1: Element of cost

(Source: Drury, 2013)

Being a manufacturing organization. Bittern Ltd, definitely incur expenses on the three

elements, that are material, labour and overheads, enumerated hereunder:

Material: Cost of input raw material in the production process so as to get desired finished

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

goods is called material cost includes both direct or indirect cost.

Labour: Cost of hiring workers to put their best efforts in handling machines and producing

required quantity of goods, is known as labour cost (Drury, 2013). For instance, Bittern Ltd

has to pay wages to the labourers is called labour cost.

Overhead: Expenditures except material and labour that are incur in the manufacturing

process are known as overheads like excise duty, royalty, cost of moulds etc.

Cost behaviour:

Illustration 2: Cost behaviour

(Source: Stewart, Wang and Willgoose, 2013)

Fixed cost: All the expenditures which do not change in the proportionate to the volume

produced by Bittern Ltd, called fixed cost. Example, cost of depreciation, insurance, rent

etc. With reference to the case study, Bittern Ltd incurred fixed cost of 5000 GBP.

Variable cost: Expenses which are directly related to the volume of production are called

variable cost (Different types of cost, 2013). At higher production, variable cost will be

increase or vice versa. Like, material and labour's wages etc. Bittern Ltd production material

and distribution are considered as variable cost @ 10 and 1 GBP on each unit manufactured.

Semi-variable cost: It is a mixture of both fixed or variable as it remains fixed up to a pre-

specified production level and thereafter, fluctuates with the increase or decrease in output

such as electricity and telephone bill. Bittern Ltd labour cost is semi-variable, in which,

5000 GBP is a fixed expenditure and beyond this level, company incurred a variable cost of

2 GBP each unit produced.

Cost nature:

5

Labour: Cost of hiring workers to put their best efforts in handling machines and producing

required quantity of goods, is known as labour cost (Drury, 2013). For instance, Bittern Ltd

has to pay wages to the labourers is called labour cost.

Overhead: Expenditures except material and labour that are incur in the manufacturing

process are known as overheads like excise duty, royalty, cost of moulds etc.

Cost behaviour:

Illustration 2: Cost behaviour

(Source: Stewart, Wang and Willgoose, 2013)

Fixed cost: All the expenditures which do not change in the proportionate to the volume

produced by Bittern Ltd, called fixed cost. Example, cost of depreciation, insurance, rent

etc. With reference to the case study, Bittern Ltd incurred fixed cost of 5000 GBP.

Variable cost: Expenses which are directly related to the volume of production are called

variable cost (Different types of cost, 2013). At higher production, variable cost will be

increase or vice versa. Like, material and labour's wages etc. Bittern Ltd production material

and distribution are considered as variable cost @ 10 and 1 GBP on each unit manufactured.

Semi-variable cost: It is a mixture of both fixed or variable as it remains fixed up to a pre-

specified production level and thereafter, fluctuates with the increase or decrease in output

such as electricity and telephone bill. Bittern Ltd labour cost is semi-variable, in which,

5000 GBP is a fixed expenditure and beyond this level, company incurred a variable cost of

2 GBP each unit produced.

Cost nature:

5

Direct cost: All the Bittern Ltd's expenditures which have direct relationship with its

manufacturing operations are called direct expenses. All the direct expenditures are variable

in nature such as direct material, direct labour and direct overhead (Ruiz and et.al., 2013)

Indirect cost: Expenditures which can't be identifiable in relation to the production process

or a department are called indirect cost. This expenses may or may not be of variable nature

such as cost of factory building, machinery etc (Stewart, Wang and Willgoose, 2013).

1.2 Different costing method and explaining the costing method for Bittern Ltd

Costing method is regarded as the process to ascertain the production cost of Bittern Ltd. As

per CIMA, London, some of the costing methods available to Bittern Ltd are presented here below:

Job costing: This method helps to determine the cost of each work order which is separately

known as job. Every job order contains less quantity of goods than aggregate production and

have own specification (Braun, 2013). It is mainly used by car repairers, painters and

decorates who provide services according to customers orders.

Batch costing: This method is used by the enterprises where units are produced in batch. All

the batch are uniform in the terms of nature as well as design (Methods of costing and Types

of costing, 2016). In order to determine cost, each batch is treated as separate job. It is

highly used by bakeries and pharmaceutical firms to assess their product cost.

Process costing: In companies, where production is carried out into several stages or

processes than they use process costing to determine the cost of each completed process and

in end, total cost of the production can be identified easily.

Contract costing: Building contractors and engineers greatly use this method to assess the

cost of work done on long term contracts (Fisher and Krumwiede, 2015). For this purpose,

they keep a separate account for all the contracted work.

Absorption costing: Bittern Ltd, may use this method in which all the incurred direct and

indirect expenses are accumulated to measure total production cost and thereby take better

pricing decisions (Krumwiede and Walden, 2013).

1.3 Meaning and comparative evaluation of variable and absorption costing system

Costing techniques defines the process of cost calculation and thereby maintain effective

control and take decisions.

Absorption costing: This technique takes into account all the cost whether fixed or variable

in nature to identify total production cost. Henceforth, it is also called full costing method.

Variable Costing: This technique considers only the variable expenditures incurred by

Bittern Ltd to produce goods in required quantity. It avoids fixed cost as they are not affected by the

6

manufacturing operations are called direct expenses. All the direct expenditures are variable

in nature such as direct material, direct labour and direct overhead (Ruiz and et.al., 2013)

Indirect cost: Expenditures which can't be identifiable in relation to the production process

or a department are called indirect cost. This expenses may or may not be of variable nature

such as cost of factory building, machinery etc (Stewart, Wang and Willgoose, 2013).

1.2 Different costing method and explaining the costing method for Bittern Ltd

Costing method is regarded as the process to ascertain the production cost of Bittern Ltd. As

per CIMA, London, some of the costing methods available to Bittern Ltd are presented here below:

Job costing: This method helps to determine the cost of each work order which is separately

known as job. Every job order contains less quantity of goods than aggregate production and

have own specification (Braun, 2013). It is mainly used by car repairers, painters and

decorates who provide services according to customers orders.

Batch costing: This method is used by the enterprises where units are produced in batch. All

the batch are uniform in the terms of nature as well as design (Methods of costing and Types

of costing, 2016). In order to determine cost, each batch is treated as separate job. It is

highly used by bakeries and pharmaceutical firms to assess their product cost.

Process costing: In companies, where production is carried out into several stages or

processes than they use process costing to determine the cost of each completed process and

in end, total cost of the production can be identified easily.

Contract costing: Building contractors and engineers greatly use this method to assess the

cost of work done on long term contracts (Fisher and Krumwiede, 2015). For this purpose,

they keep a separate account for all the contracted work.

Absorption costing: Bittern Ltd, may use this method in which all the incurred direct and

indirect expenses are accumulated to measure total production cost and thereby take better

pricing decisions (Krumwiede and Walden, 2013).

1.3 Meaning and comparative evaluation of variable and absorption costing system

Costing techniques defines the process of cost calculation and thereby maintain effective

control and take decisions.

Absorption costing: This technique takes into account all the cost whether fixed or variable

in nature to identify total production cost. Henceforth, it is also called full costing method.

Variable Costing: This technique considers only the variable expenditures incurred by

Bittern Ltd to produce goods in required quantity. It avoids fixed cost as they are not affected by the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

changes in production output (Surbhi, 2015).

Table 1: Comparative analysis of variable and absorption costing

Difference basis Variable/Marginal costing Absorption/Full costing

Cost recognition Variable Fixed and variable

Profitability It is determined by identifying profit

volume ratio (PVR). Thus, fixed

expenditures do not have any impact

on Bittern Ltd's profitability (Surbhi,

2015).

Inclusion of fixed cost affect business

profit as higher the fixed cost

decrease profit or vice-versa.

Focus It pay focus on contribution per unit

which can be determined by

subtracting total variable cost from the

total revenue and then divided by the

number of units produced (Methods of

costing and Types of costing, 2016).

It pay focus on net profit per unit

determined by subtracting total cost

from the turnover and divided by the

total production volume of Bittern

Ltd (Krumwiede and Walden, 2013).

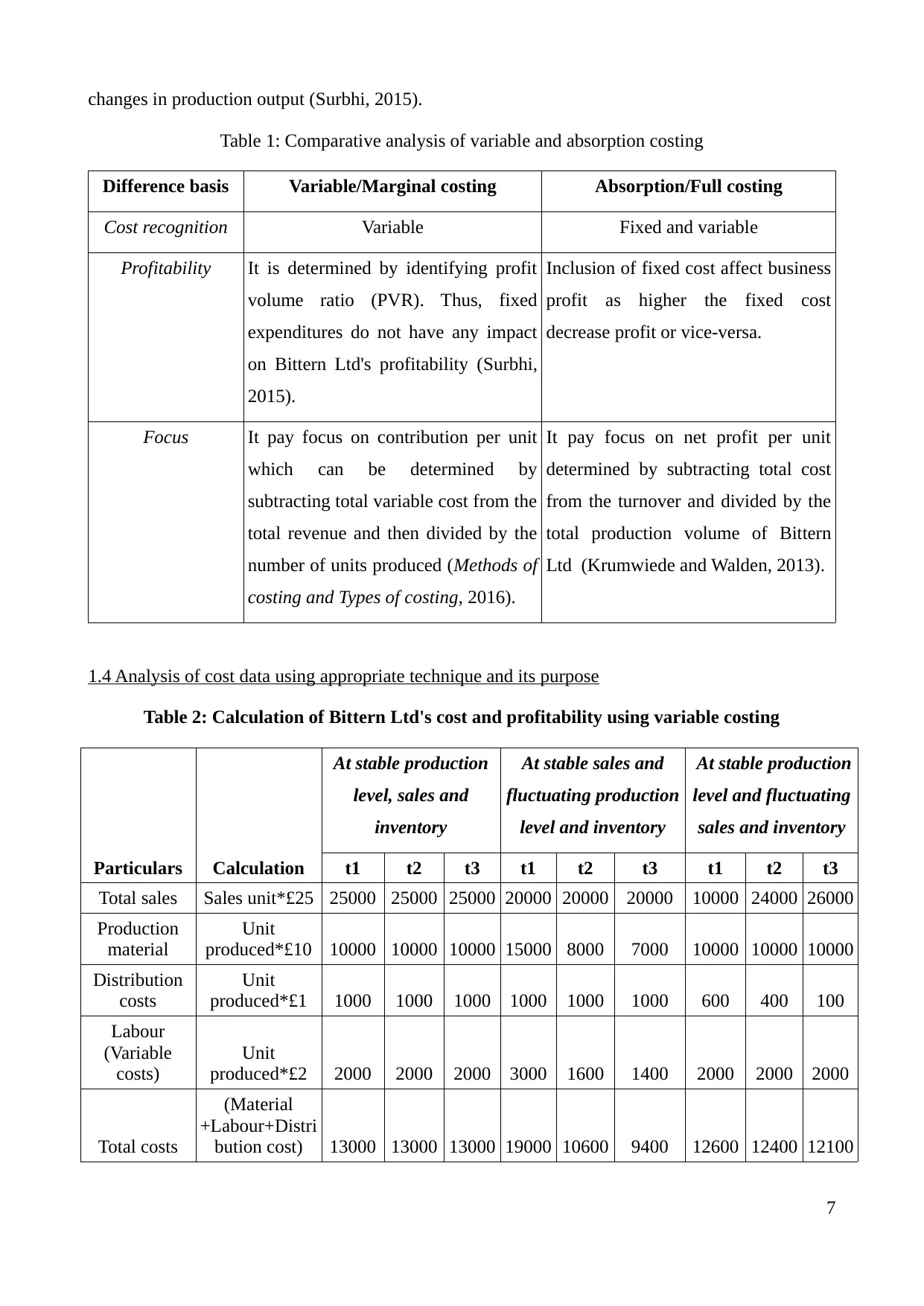

1.4 Analysis of cost data using appropriate technique and its purpose

Table 2: Calculation of Bittern Ltd's cost and profitability using variable costing

Particulars Calculation

At stable production

level, sales and

inventory

At stable sales and

fluctuating production

level and inventory

At stable production

level and fluctuating

sales and inventory

t1 t2 t3 t1 t2 t3 t1 t2 t3

Total sales Sales unit*£25 25000 25000 25000 20000 20000 20000 10000 24000 26000

Production

material

Unit

produced*£10 10000 10000 10000 15000 8000 7000 10000 10000 10000

Distribution

costs

Unit

produced*£1 1000 1000 1000 1000 1000 1000 600 400 100

Labour

(Variable

costs)

Unit

produced*£2 2000 2000 2000 3000 1600 1400 2000 2000 2000

Total costs

(Material

+Labour+Distri

bution cost) 13000 13000 13000 19000 10600 9400 12600 12400 12100

7

Table 1: Comparative analysis of variable and absorption costing

Difference basis Variable/Marginal costing Absorption/Full costing

Cost recognition Variable Fixed and variable

Profitability It is determined by identifying profit

volume ratio (PVR). Thus, fixed

expenditures do not have any impact

on Bittern Ltd's profitability (Surbhi,

2015).

Inclusion of fixed cost affect business

profit as higher the fixed cost

decrease profit or vice-versa.

Focus It pay focus on contribution per unit

which can be determined by

subtracting total variable cost from the

total revenue and then divided by the

number of units produced (Methods of

costing and Types of costing, 2016).

It pay focus on net profit per unit

determined by subtracting total cost

from the turnover and divided by the

total production volume of Bittern

Ltd (Krumwiede and Walden, 2013).

1.4 Analysis of cost data using appropriate technique and its purpose

Table 2: Calculation of Bittern Ltd's cost and profitability using variable costing

Particulars Calculation

At stable production

level, sales and

inventory

At stable sales and

fluctuating production

level and inventory

At stable production

level and fluctuating

sales and inventory

t1 t2 t3 t1 t2 t3 t1 t2 t3

Total sales Sales unit*£25 25000 25000 25000 20000 20000 20000 10000 24000 26000

Production

material

Unit

produced*£10 10000 10000 10000 15000 8000 7000 10000 10000 10000

Distribution

costs

Unit

produced*£1 1000 1000 1000 1000 1000 1000 600 400 100

Labour

(Variable

costs)

Unit

produced*£2 2000 2000 2000 3000 1600 1400 2000 2000 2000

Total costs

(Material

+Labour+Distri

bution cost) 13000 13000 13000 19000 10600 9400 12600 12400 12100

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitability

(Sales-Total

cost) 12000 12000 12000 1000 9400 10600 -2600 11600 13900

Cost per unit

Total

cost/Number of

units produced 13 13 13 12.67 13.25 13.43 12.6 12.4 12.1

Closing stock

(Units) Given 100 100 100 600 400 100 600 400 100

Closing stock

(in £)

Inventory

units*£13 1300 1300 1300 7600 5300 1342.86 7560 4960 1210

Table 3: Calculation of Bittern Ltd's cost and profitability using absorption costing

Particulars Calculation

At stable production

level, sales and

inventory

At stable sales and

fluctuating production

level and inventory

At stable production

level and fluctuating

sales and inventory

t1 t2 t3 t1 t2 t3 t1 t2 t3

Sales Sales unit*£25 25000 25000 25000 20000 20000 20000 10000 24000 26000

Production

material

Unit

produced*£10 10000 10000 10000 15000 8000 7000 10000 10000 10000

Distribution

costs

Unit

produced*£1 1000 1000 1000 1000 1000 1000 600 400 100

Labour

[£5000+(Unit

produced*£2)] 7000 7000 7000 8000 6600 6400 7000 7000 7000

Overheads 5000 5000 5000 5000 5000 5000 5000 5000 5000

Total costs

(Material

+Labour+Distri

bution

+Overheads) 23000 23000 23000 29000 20600 19400 22600 22400 22100

Profitability

(Sales-Total

cost) 2000 2000 2000 -9000 -600 600

-

12600 1600 3900

Cost per unit

Total

cost/Number of

units produced 23 23 23 19.33 25.75 27.71 22.6 22.4 22.1

Closing stock

(Units) Given 100 100 100 600 400 100 600 400 100

Closing stock

(in value)

Inventory

units*£13 2300 2300 2300 11600 10300 2771.43 13560 8960 2210

TASK 2

Enclosed in power point presentation.

8

(Sales-Total

cost) 12000 12000 12000 1000 9400 10600 -2600 11600 13900

Cost per unit

Total

cost/Number of

units produced 13 13 13 12.67 13.25 13.43 12.6 12.4 12.1

Closing stock

(Units) Given 100 100 100 600 400 100 600 400 100

Closing stock

(in £)

Inventory

units*£13 1300 1300 1300 7600 5300 1342.86 7560 4960 1210

Table 3: Calculation of Bittern Ltd's cost and profitability using absorption costing

Particulars Calculation

At stable production

level, sales and

inventory

At stable sales and

fluctuating production

level and inventory

At stable production

level and fluctuating

sales and inventory

t1 t2 t3 t1 t2 t3 t1 t2 t3

Sales Sales unit*£25 25000 25000 25000 20000 20000 20000 10000 24000 26000

Production

material

Unit

produced*£10 10000 10000 10000 15000 8000 7000 10000 10000 10000

Distribution

costs

Unit

produced*£1 1000 1000 1000 1000 1000 1000 600 400 100

Labour

[£5000+(Unit

produced*£2)] 7000 7000 7000 8000 6600 6400 7000 7000 7000

Overheads 5000 5000 5000 5000 5000 5000 5000 5000 5000

Total costs

(Material

+Labour+Distri

bution

+Overheads) 23000 23000 23000 29000 20600 19400 22600 22400 22100

Profitability

(Sales-Total

cost) 2000 2000 2000 -9000 -600 600

-

12600 1600 3900

Cost per unit

Total

cost/Number of

units produced 23 23 23 19.33 25.75 27.71 22.6 22.4 22.1

Closing stock

(Units) Given 100 100 100 600 400 100 600 400 100

Closing stock

(in value)

Inventory

units*£13 2300 2300 2300 11600 10300 2771.43 13560 8960 2210

TASK 2

Enclosed in power point presentation.

8

TASK 3

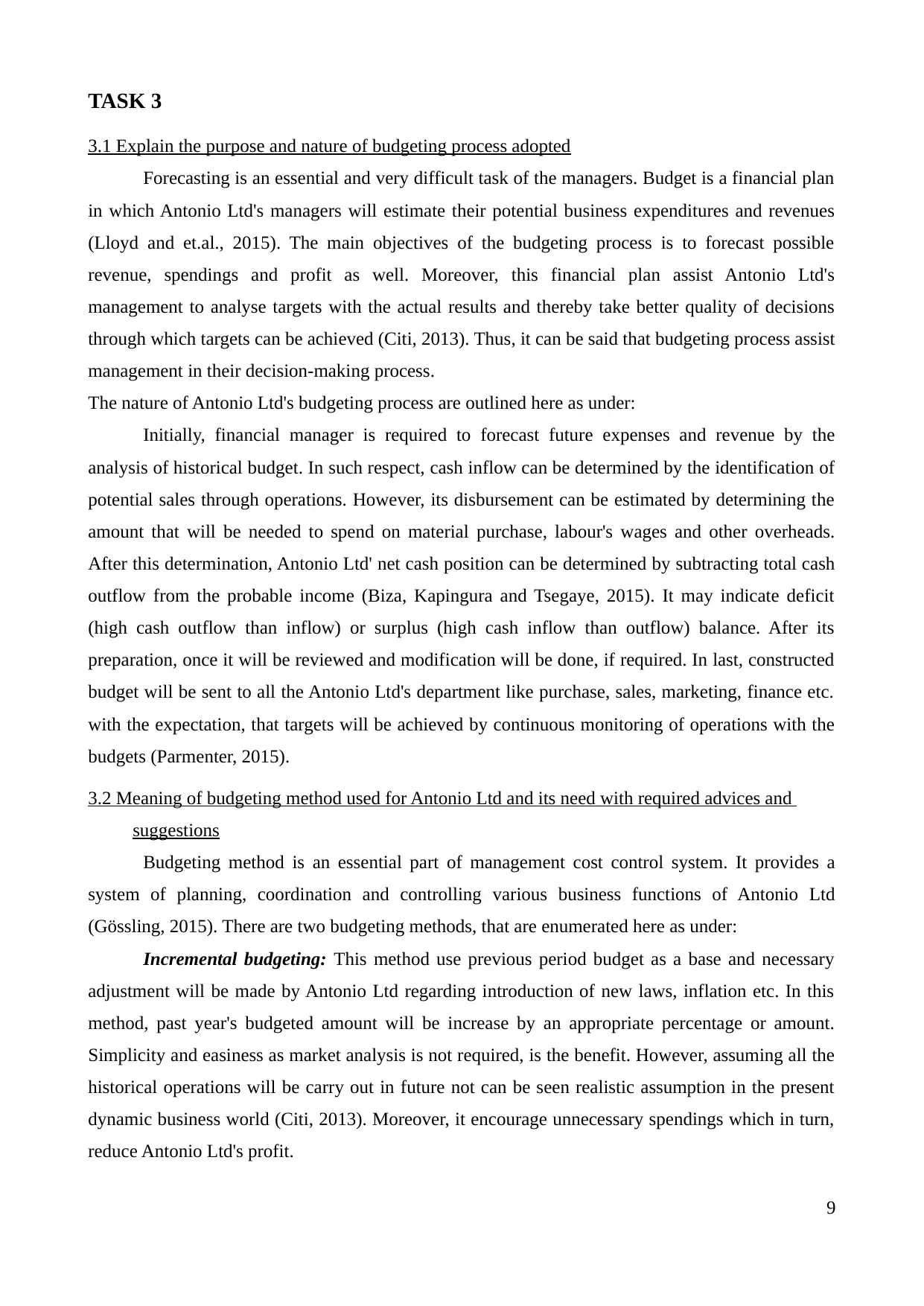

3.1 Explain the purpose and nature of budgeting process adopted

Forecasting is an essential and very difficult task of the managers. Budget is a financial plan

in which Antonio Ltd's managers will estimate their potential business expenditures and revenues

(Lloyd and et.al., 2015). The main objectives of the budgeting process is to forecast possible

revenue, spendings and profit as well. Moreover, this financial plan assist Antonio Ltd's

management to analyse targets with the actual results and thereby take better quality of decisions

through which targets can be achieved (Citi, 2013). Thus, it can be said that budgeting process assist

management in their decision-making process.

The nature of Antonio Ltd's budgeting process are outlined here as under:

Initially, financial manager is required to forecast future expenses and revenue by the

analysis of historical budget. In such respect, cash inflow can be determined by the identification of

potential sales through operations. However, its disbursement can be estimated by determining the

amount that will be needed to spend on material purchase, labour's wages and other overheads.

After this determination, Antonio Ltd' net cash position can be determined by subtracting total cash

outflow from the probable income (Biza, Kapingura and Tsegaye, 2015). It may indicate deficit

(high cash outflow than inflow) or surplus (high cash inflow than outflow) balance. After its

preparation, once it will be reviewed and modification will be done, if required. In last, constructed

budget will be sent to all the Antonio Ltd's department like purchase, sales, marketing, finance etc.

with the expectation, that targets will be achieved by continuous monitoring of operations with the

budgets (Parmenter, 2015).

3.2 Meaning of budgeting method used for Antonio Ltd and its need with required advices and

suggestions

Budgeting method is an essential part of management cost control system. It provides a

system of planning, coordination and controlling various business functions of Antonio Ltd

(Gössling, 2015). There are two budgeting methods, that are enumerated here as under:

Incremental budgeting: This method use previous period budget as a base and necessary

adjustment will be made by Antonio Ltd regarding introduction of new laws, inflation etc. In this

method, past year's budgeted amount will be increase by an appropriate percentage or amount.

Simplicity and easiness as market analysis is not required, is the benefit. However, assuming all the

historical operations will be carry out in future not can be seen realistic assumption in the present

dynamic business world (Citi, 2013). Moreover, it encourage unnecessary spendings which in turn,

reduce Antonio Ltd's profit.

9

3.1 Explain the purpose and nature of budgeting process adopted

Forecasting is an essential and very difficult task of the managers. Budget is a financial plan

in which Antonio Ltd's managers will estimate their potential business expenditures and revenues

(Lloyd and et.al., 2015). The main objectives of the budgeting process is to forecast possible

revenue, spendings and profit as well. Moreover, this financial plan assist Antonio Ltd's

management to analyse targets with the actual results and thereby take better quality of decisions

through which targets can be achieved (Citi, 2013). Thus, it can be said that budgeting process assist

management in their decision-making process.

The nature of Antonio Ltd's budgeting process are outlined here as under:

Initially, financial manager is required to forecast future expenses and revenue by the

analysis of historical budget. In such respect, cash inflow can be determined by the identification of

potential sales through operations. However, its disbursement can be estimated by determining the

amount that will be needed to spend on material purchase, labour's wages and other overheads.

After this determination, Antonio Ltd' net cash position can be determined by subtracting total cash

outflow from the probable income (Biza, Kapingura and Tsegaye, 2015). It may indicate deficit

(high cash outflow than inflow) or surplus (high cash inflow than outflow) balance. After its

preparation, once it will be reviewed and modification will be done, if required. In last, constructed

budget will be sent to all the Antonio Ltd's department like purchase, sales, marketing, finance etc.

with the expectation, that targets will be achieved by continuous monitoring of operations with the

budgets (Parmenter, 2015).

3.2 Meaning of budgeting method used for Antonio Ltd and its need with required advices and

suggestions

Budgeting method is an essential part of management cost control system. It provides a

system of planning, coordination and controlling various business functions of Antonio Ltd

(Gössling, 2015). There are two budgeting methods, that are enumerated here as under:

Incremental budgeting: This method use previous period budget as a base and necessary

adjustment will be made by Antonio Ltd regarding introduction of new laws, inflation etc. In this

method, past year's budgeted amount will be increase by an appropriate percentage or amount.

Simplicity and easiness as market analysis is not required, is the benefit. However, assuming all the

historical operations will be carry out in future not can be seen realistic assumption in the present

dynamic business world (Citi, 2013). Moreover, it encourage unnecessary spendings which in turn,

reduce Antonio Ltd's profit.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Zero-based budgeting: This method makes proper market evaluation so as to identify

activities or function which will be conducted in future. It is consider as an appropriate budgeting

method for Antonio Ltd to prepare their budgets. The reason behind such suggestion is managers

will focus their efforts to ensure optimum utilization of resources by effective allocation (Callaghan,

Hawke and Mignerey, 2014). Moreover, maximizing turnover and minimizing cost in order to drive

more profitability are the benefits of it. Through this, more realistic targets can be set and

communicated to the departments to achieve it in more effectual manner.

Flexible budget: Budget which can be adjusted according to the changes in production level

or level of activity is called flexible budget. It enables managers of the Antonio Ltd to compare their

actual results with the targets and helps to make solid decisions for the growth.

Fixed budget: Unlike flexible budgeting, fixed budget gives information regarding cost and

revenue at a certain or specified volume or activity may cause difficulties in deviation analysis.

3.3 Preparation of budget and purpose of the method

Antonio Ltd can identify the material quantity and cost which it will incur in the

forthcoming period to produce goods in required quantity (Biza, Kapingura and Tsegaye, 2015).

Table 4: Material purchase budget of Antonio Ltd

Particular June July Aug. Sept. Oct. Nov

Required material units 400 500 600 600 700 750

Add: Ending inventory 500 500 500 500 500 500

Total 900 1000 1100 1100 1200 1250

Less: Begining inventory 500 500 500 500 500 500

Material quantity need to be

purchased 400 500 600 600 700 750

Raw material price per unit 8 8 8 8 8 8

Total cost of material 3200 4000 4800 4800 5600 6000

Antonio Ltd, can determine their accounts or trade payable by constructing trade payable

budget, prepared hereunder:

Table 5: Trade payable budget of Antonio Ltd

Particulars June July August Sept. Oct. Nov.

Material trade payable 3200 4000 4800 4800 5600 6000

Overhead trade payable 280 320 320 320 320 400

Total trade payables 3480 4320 5120 5120 5920 6400

10

activities or function which will be conducted in future. It is consider as an appropriate budgeting

method for Antonio Ltd to prepare their budgets. The reason behind such suggestion is managers

will focus their efforts to ensure optimum utilization of resources by effective allocation (Callaghan,

Hawke and Mignerey, 2014). Moreover, maximizing turnover and minimizing cost in order to drive

more profitability are the benefits of it. Through this, more realistic targets can be set and

communicated to the departments to achieve it in more effectual manner.

Flexible budget: Budget which can be adjusted according to the changes in production level

or level of activity is called flexible budget. It enables managers of the Antonio Ltd to compare their

actual results with the targets and helps to make solid decisions for the growth.

Fixed budget: Unlike flexible budgeting, fixed budget gives information regarding cost and

revenue at a certain or specified volume or activity may cause difficulties in deviation analysis.

3.3 Preparation of budget and purpose of the method

Antonio Ltd can identify the material quantity and cost which it will incur in the

forthcoming period to produce goods in required quantity (Biza, Kapingura and Tsegaye, 2015).

Table 4: Material purchase budget of Antonio Ltd

Particular June July Aug. Sept. Oct. Nov

Required material units 400 500 600 600 700 750

Add: Ending inventory 500 500 500 500 500 500

Total 900 1000 1100 1100 1200 1250

Less: Begining inventory 500 500 500 500 500 500

Material quantity need to be

purchased 400 500 600 600 700 750

Raw material price per unit 8 8 8 8 8 8

Total cost of material 3200 4000 4800 4800 5600 6000

Antonio Ltd, can determine their accounts or trade payable by constructing trade payable

budget, prepared hereunder:

Table 5: Trade payable budget of Antonio Ltd

Particulars June July August Sept. Oct. Nov.

Material trade payable 3200 4000 4800 4800 5600 6000

Overhead trade payable 280 320 320 320 320 400

Total trade payables 3480 4320 5120 5120 5920 6400

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

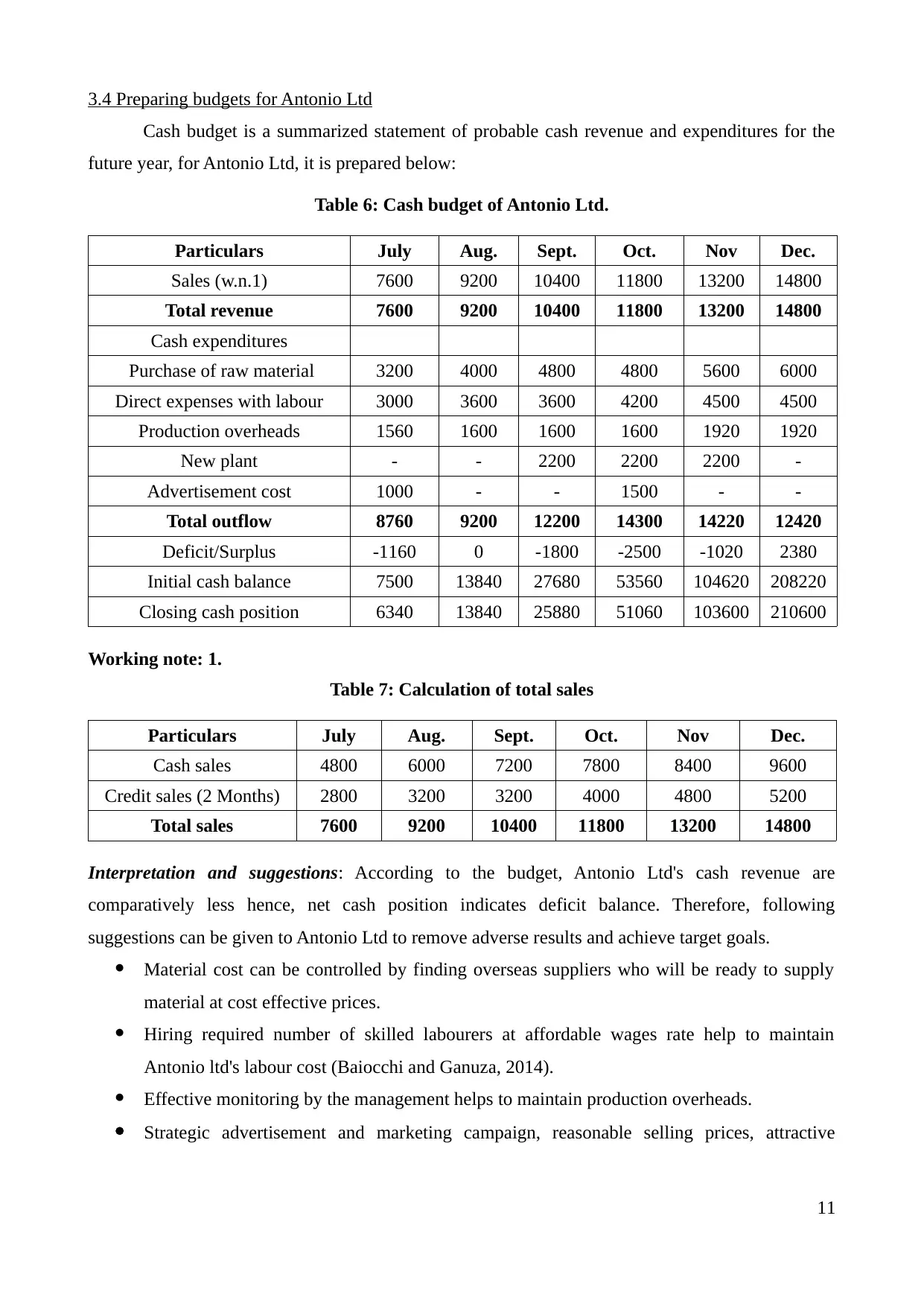

3.4 Preparing budgets for Antonio Ltd

Cash budget is a summarized statement of probable cash revenue and expenditures for the

future year, for Antonio Ltd, it is prepared below:

Table 6: Cash budget of Antonio Ltd.

Particulars July Aug. Sept. Oct. Nov Dec.

Sales (w.n.1) 7600 9200 10400 11800 13200 14800

Total revenue 7600 9200 10400 11800 13200 14800

Cash expenditures

Purchase of raw material 3200 4000 4800 4800 5600 6000

Direct expenses with labour 3000 3600 3600 4200 4500 4500

Production overheads 1560 1600 1600 1600 1920 1920

New plant - - 2200 2200 2200 -

Advertisement cost 1000 - - 1500 - -

Total outflow 8760 9200 12200 14300 14220 12420

Deficit/Surplus -1160 0 -1800 -2500 -1020 2380

Initial cash balance 7500 13840 27680 53560 104620 208220

Closing cash position 6340 13840 25880 51060 103600 210600

Working note: 1.

Table 7: Calculation of total sales

Particulars July Aug. Sept. Oct. Nov Dec.

Cash sales 4800 6000 7200 7800 8400 9600

Credit sales (2 Months) 2800 3200 3200 4000 4800 5200

Total sales 7600 9200 10400 11800 13200 14800

Interpretation and suggestions: According to the budget, Antonio Ltd's cash revenue are

comparatively less hence, net cash position indicates deficit balance. Therefore, following

suggestions can be given to Antonio Ltd to remove adverse results and achieve target goals.

Material cost can be controlled by finding overseas suppliers who will be ready to supply

material at cost effective prices.

Hiring required number of skilled labourers at affordable wages rate help to maintain

Antonio ltd's labour cost (Baiocchi and Ganuza, 2014).

Effective monitoring by the management helps to maintain production overheads.

Strategic advertisement and marketing campaign, reasonable selling prices, attractive

11

Cash budget is a summarized statement of probable cash revenue and expenditures for the

future year, for Antonio Ltd, it is prepared below:

Table 6: Cash budget of Antonio Ltd.

Particulars July Aug. Sept. Oct. Nov Dec.

Sales (w.n.1) 7600 9200 10400 11800 13200 14800

Total revenue 7600 9200 10400 11800 13200 14800

Cash expenditures

Purchase of raw material 3200 4000 4800 4800 5600 6000

Direct expenses with labour 3000 3600 3600 4200 4500 4500

Production overheads 1560 1600 1600 1600 1920 1920

New plant - - 2200 2200 2200 -

Advertisement cost 1000 - - 1500 - -

Total outflow 8760 9200 12200 14300 14220 12420

Deficit/Surplus -1160 0 -1800 -2500 -1020 2380

Initial cash balance 7500 13840 27680 53560 104620 208220

Closing cash position 6340 13840 25880 51060 103600 210600

Working note: 1.

Table 7: Calculation of total sales

Particulars July Aug. Sept. Oct. Nov Dec.

Cash sales 4800 6000 7200 7800 8400 9600

Credit sales (2 Months) 2800 3200 3200 4000 4800 5200

Total sales 7600 9200 10400 11800 13200 14800

Interpretation and suggestions: According to the budget, Antonio Ltd's cash revenue are

comparatively less hence, net cash position indicates deficit balance. Therefore, following

suggestions can be given to Antonio Ltd to remove adverse results and achieve target goals.

Material cost can be controlled by finding overseas suppliers who will be ready to supply

material at cost effective prices.

Hiring required number of skilled labourers at affordable wages rate help to maintain

Antonio ltd's labour cost (Baiocchi and Ganuza, 2014).

Effective monitoring by the management helps to maintain production overheads.

Strategic advertisement and marketing campaign, reasonable selling prices, attractive

11

discounting offers helps to maximize Antonio Ltd's sales and profitability as well (Citi,

2013).

TASK 4

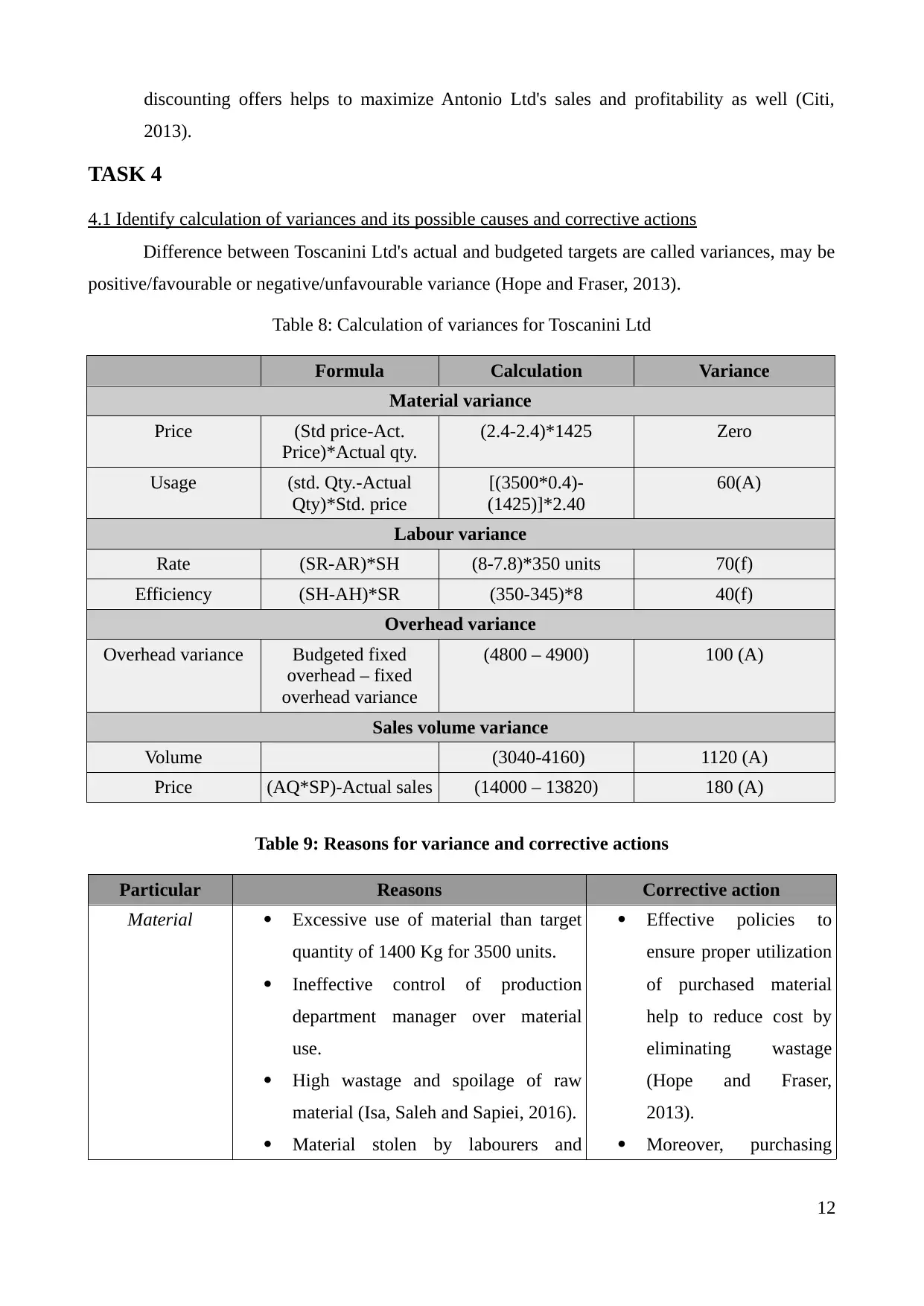

4.1 Identify calculation of variances and its possible causes and corrective actions

Difference between Toscanini Ltd's actual and budgeted targets are called variances, may be

positive/favourable or negative/unfavourable variance (Hope and Fraser, 2013).

Table 8: Calculation of variances for Toscanini Ltd

Formula Calculation Variance

Material variance

Price (Std price-Act.

Price)*Actual qty.

(2.4-2.4)*1425 Zero

Usage (std. Qty.-Actual

Qty)*Std. price

[(3500*0.4)-

(1425)]*2.40

60(A)

Labour variance

Rate (SR-AR)*SH (8-7.8)*350 units 70(f)

Efficiency (SH-AH)*SR (350-345)*8 40(f)

Overhead variance

Overhead variance Budgeted fixed

overhead – fixed

overhead variance

(4800 – 4900) 100 (A)

Sales volume variance

Volume (3040-4160) 1120 (A)

Price (AQ*SP)-Actual sales (14000 – 13820) 180 (A)

Table 9: Reasons for variance and corrective actions

Particular Reasons Corrective action

Material Excessive use of material than target

quantity of 1400 Kg for 3500 units.

Ineffective control of production

department manager over material

use.

High wastage and spoilage of raw

material (Isa, Saleh and Sapiei, 2016).

Material stolen by labourers and

Effective policies to

ensure proper utilization

of purchased material

help to reduce cost by

eliminating wastage

(Hope and Fraser,

2013).

Moreover, purchasing

12

2013).

TASK 4

4.1 Identify calculation of variances and its possible causes and corrective actions

Difference between Toscanini Ltd's actual and budgeted targets are called variances, may be

positive/favourable or negative/unfavourable variance (Hope and Fraser, 2013).

Table 8: Calculation of variances for Toscanini Ltd

Formula Calculation Variance

Material variance

Price (Std price-Act.

Price)*Actual qty.

(2.4-2.4)*1425 Zero

Usage (std. Qty.-Actual

Qty)*Std. price

[(3500*0.4)-

(1425)]*2.40

60(A)

Labour variance

Rate (SR-AR)*SH (8-7.8)*350 units 70(f)

Efficiency (SH-AH)*SR (350-345)*8 40(f)

Overhead variance

Overhead variance Budgeted fixed

overhead – fixed

overhead variance

(4800 – 4900) 100 (A)

Sales volume variance

Volume (3040-4160) 1120 (A)

Price (AQ*SP)-Actual sales (14000 – 13820) 180 (A)

Table 9: Reasons for variance and corrective actions

Particular Reasons Corrective action

Material Excessive use of material than target

quantity of 1400 Kg for 3500 units.

Ineffective control of production

department manager over material

use.

High wastage and spoilage of raw

material (Isa, Saleh and Sapiei, 2016).

Material stolen by labourers and

Effective policies to

ensure proper utilization

of purchased material

help to reduce cost by

eliminating wastage

(Hope and Fraser,

2013).

Moreover, purchasing

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.