Unit 5: Management Accounting Report for Connect Catering Services

VerifiedAdded on 2022/12/22

|16

|4746

|78

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Connect Catering Services (CCS). It begins by explaining different types of management accounting, such as cost accounting systems, price optimization, job costing systems, and inventory management systems, highlighting their benefits and drawbacks. The report then examines various methods used for management accounting reports, including account receivable aging, cost managerial accounting, performance reports, and budget reports. Furthermore, the report provides detailed calculations of costs, including marginal costing, absorption costing, and a reconciliation statement. It also explores fixed and variable costs, margin of safety, break-even point analysis, break-even graphs, and variance analysis. The report then evaluates the advantages and disadvantages of different planning tools used for budgetary control and discusses the use of management accounting systems to respond to financial problems, culminating in a conclusion and references.

UNIT- 5 MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining different types of management Accounting and their benefits and drawbacks. . .1

P2 Explaining different methods used for management accounting reports...............................3

TASK 2............................................................................................................................................5

P- 3 Calculation of the costs........................................................................................................5

Statement of Marginal costing.....................................................................................................5

Statement of Absorption costing..................................................................................................6

Reconciliation statement..............................................................................................................6

Fixed and variable cost................................................................................................................6

Margin of safety...........................................................................................................................7

Break-even point analysis............................................................................................................7

Break-even graph.........................................................................................................................8

Variance analysis report...............................................................................................................8

TASK 3............................................................................................................................................9

P- 4 Advantages and disadvantages of the different planning tools used for budgetary control.9

M-3.............................................................................................................................................11

P5 Use of management accounting system to respond financial problems...............................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining different types of management Accounting and their benefits and drawbacks. . .1

P2 Explaining different methods used for management accounting reports...............................3

TASK 2............................................................................................................................................5

P- 3 Calculation of the costs........................................................................................................5

Statement of Marginal costing.....................................................................................................5

Statement of Absorption costing..................................................................................................6

Reconciliation statement..............................................................................................................6

Fixed and variable cost................................................................................................................6

Margin of safety...........................................................................................................................7

Break-even point analysis............................................................................................................7

Break-even graph.........................................................................................................................8

Variance analysis report...............................................................................................................8

TASK 3............................................................................................................................................9

P- 4 Advantages and disadvantages of the different planning tools used for budgetary control.9

M-3.............................................................................................................................................11

P5 Use of management accounting system to respond financial problems...............................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting refers to the process in which the financial reports of the

business are being communicated to the internal management, and they are used in the process of

decision-making. The report shall be reflecting the concept of management accounting, its

systems and the methods used for management accounting reporting. It shall be demonstrating

the statements as per the absorption and marginal costing and the calculation of the break-even

point. Apart from that the report highlights the various planning tools that are used by the

business to forecast and budget the activities that are related to the future time period. And lastly

the report will be discussing how the management accounting systems are used in responding to

the various financial problems of the business and comparison with the competitor regarding its

application.

MAIN BODY

TASK 1

P1 Explaining different types of management Accounting and their benefits and drawbacks

Management Accounting (MA) is process of examining, interpreting and communicating

information to manager that helps him to take strategic decision within company (What is

management accounting?, 2021). Connect Catering Service (CCS) will get various advantages

from usage of different types of accounting system. It includes job costing, inventory

management, cost accounting system and price optimization.

Cost Accounting System (CAS)

It is process which assist an organization to evaluate cost of products, profits, inventor

value and monitoring expenditures. CSS will be in position to analyse expenses regarding its raw

material before production process (Drobyazko and et.al., 2019). In addition to this, cost

accounting system provide assistance to company in gathering all information regarding cost

incurred in operation of firm.

Advantages Disadvantages

It permits organization to get into

process that reduces cost of firm.

Decisions are taken on the basis of past

records which does not provide

accurate guidelines to firm

1

Management accounting refers to the process in which the financial reports of the

business are being communicated to the internal management, and they are used in the process of

decision-making. The report shall be reflecting the concept of management accounting, its

systems and the methods used for management accounting reporting. It shall be demonstrating

the statements as per the absorption and marginal costing and the calculation of the break-even

point. Apart from that the report highlights the various planning tools that are used by the

business to forecast and budget the activities that are related to the future time period. And lastly

the report will be discussing how the management accounting systems are used in responding to

the various financial problems of the business and comparison with the competitor regarding its

application.

MAIN BODY

TASK 1

P1 Explaining different types of management Accounting and their benefits and drawbacks

Management Accounting (MA) is process of examining, interpreting and communicating

information to manager that helps him to take strategic decision within company (What is

management accounting?, 2021). Connect Catering Service (CCS) will get various advantages

from usage of different types of accounting system. It includes job costing, inventory

management, cost accounting system and price optimization.

Cost Accounting System (CAS)

It is process which assist an organization to evaluate cost of products, profits, inventor

value and monitoring expenditures. CSS will be in position to analyse expenses regarding its raw

material before production process (Drobyazko and et.al., 2019). In addition to this, cost

accounting system provide assistance to company in gathering all information regarding cost

incurred in operation of firm.

Advantages Disadvantages

It permits organization to get into

process that reduces cost of firm.

Decisions are taken on the basis of past

records which does not provide

accurate guidelines to firm

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAS will help CSS to fix roles and

responsibilities which leads to

effectiveness.

Previous data is utilized for succeeding

year thus information is not useful for

future reference

Frauds can be prevented from this type

of management accounting system.

CAS do not get success in studying

areas like operation research, time, etc.

Price Optimization system (POS)

POS is analysis of customers reaction against of changing product's price levels. It is

utilized by organization to determine the best price for the commodity that can fulfil its

objectives of profit & sales maximization, cost reduction, etc. CSS will get various kinds of

benefits by utilization of this price optimization system.

Benefits Drawbacks

It is easy to implement in turn

efficiency optimization is received

Sometimes become non optimal in case

of irregular update in procedure

This provides flexibility in

communication process

Price optimization consider only small

problems and avoids competitive issues

POS leads to quality performance

which enhancer productivity of firm

It becomes quite difficult to adapt in

new changing circumstances of markets

Market transparency is achieved

through this particular methodology

CSS may find it complex while using it

(Ameen and et.al., 2018)

CSS can save time by attaining

economic scale of operation.

Another challenge that can face by

Connect Catering service is security

Job Costing System (JCS)

It is considered with aggregation of cost related to particular service or job. Organization

widely use it to get details of information regarding all expenses under particular head so that

price can be estimated accurately (Kesumawati and et.al., 2019). CCS will be able to obtain data

of expenditure occurred in applying direct & indirect material and overhead of company's

operation. All scale of firm utilizes to attain various merits that make procedure of functioning

2

responsibilities which leads to

effectiveness.

Previous data is utilized for succeeding

year thus information is not useful for

future reference

Frauds can be prevented from this type

of management accounting system.

CAS do not get success in studying

areas like operation research, time, etc.

Price Optimization system (POS)

POS is analysis of customers reaction against of changing product's price levels. It is

utilized by organization to determine the best price for the commodity that can fulfil its

objectives of profit & sales maximization, cost reduction, etc. CSS will get various kinds of

benefits by utilization of this price optimization system.

Benefits Drawbacks

It is easy to implement in turn

efficiency optimization is received

Sometimes become non optimal in case

of irregular update in procedure

This provides flexibility in

communication process

Price optimization consider only small

problems and avoids competitive issues

POS leads to quality performance

which enhancer productivity of firm

It becomes quite difficult to adapt in

new changing circumstances of markets

Market transparency is achieved

through this particular methodology

CSS may find it complex while using it

(Ameen and et.al., 2018)

CSS can save time by attaining

economic scale of operation.

Another challenge that can face by

Connect Catering service is security

Job Costing System (JCS)

It is considered with aggregation of cost related to particular service or job. Organization

widely use it to get details of information regarding all expenses under particular head so that

price can be estimated accurately (Kesumawati and et.al., 2019). CCS will be able to obtain data

of expenditure occurred in applying direct & indirect material and overhead of company's

operation. All scale of firm utilizes to attain various merits that make procedure of functioning

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

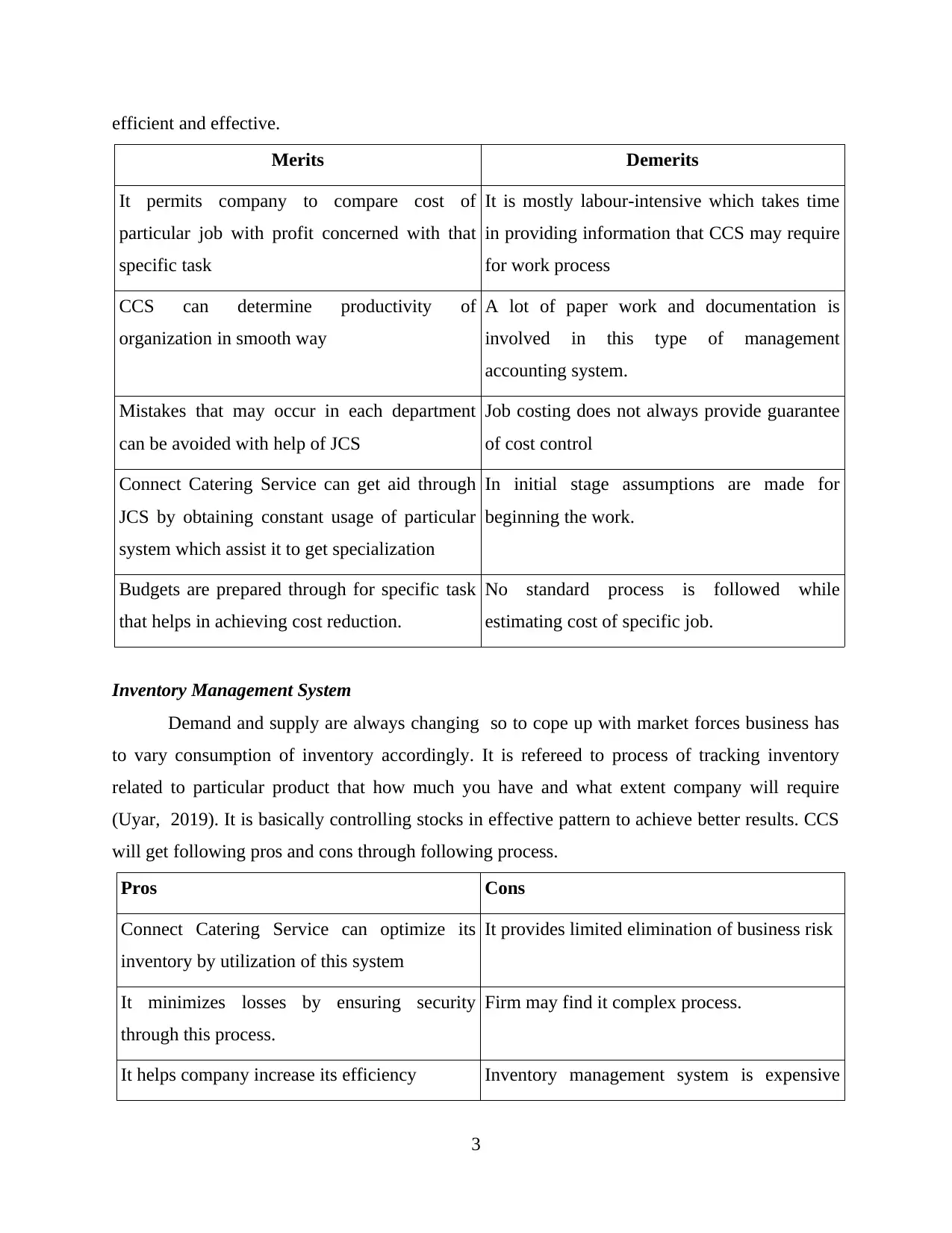

efficient and effective.

Merits Demerits

It permits company to compare cost of

particular job with profit concerned with that

specific task

It is mostly labour-intensive which takes time

in providing information that CCS may require

for work process

CCS can determine productivity of

organization in smooth way

A lot of paper work and documentation is

involved in this type of management

accounting system.

Mistakes that may occur in each department

can be avoided with help of JCS

Job costing does not always provide guarantee

of cost control

Connect Catering Service can get aid through

JCS by obtaining constant usage of particular

system which assist it to get specialization

In initial stage assumptions are made for

beginning the work.

Budgets are prepared through for specific task

that helps in achieving cost reduction.

No standard process is followed while

estimating cost of specific job.

Inventory Management System

Demand and supply are always changing so to cope up with market forces business has

to vary consumption of inventory accordingly. It is refereed to process of tracking inventory

related to particular product that how much you have and what extent company will require

(Uyar, 2019). It is basically controlling stocks in effective pattern to achieve better results. CCS

will get following pros and cons through following process.

Pros Cons

Connect Catering Service can optimize its

inventory by utilization of this system

It provides limited elimination of business risk

It minimizes losses by ensuring security

through this process.

Firm may find it complex process.

It helps company increase its efficiency Inventory management system is expensive

3

Merits Demerits

It permits company to compare cost of

particular job with profit concerned with that

specific task

It is mostly labour-intensive which takes time

in providing information that CCS may require

for work process

CCS can determine productivity of

organization in smooth way

A lot of paper work and documentation is

involved in this type of management

accounting system.

Mistakes that may occur in each department

can be avoided with help of JCS

Job costing does not always provide guarantee

of cost control

Connect Catering Service can get aid through

JCS by obtaining constant usage of particular

system which assist it to get specialization

In initial stage assumptions are made for

beginning the work.

Budgets are prepared through for specific task

that helps in achieving cost reduction.

No standard process is followed while

estimating cost of specific job.

Inventory Management System

Demand and supply are always changing so to cope up with market forces business has

to vary consumption of inventory accordingly. It is refereed to process of tracking inventory

related to particular product that how much you have and what extent company will require

(Uyar, 2019). It is basically controlling stocks in effective pattern to achieve better results. CCS

will get following pros and cons through following process.

Pros Cons

Connect Catering Service can optimize its

inventory by utilization of this system

It provides limited elimination of business risk

It minimizes losses by ensuring security

through this process.

Firm may find it complex process.

It helps company increase its efficiency Inventory management system is expensive

3

procedure.

P2 Explaining different methods used for management accounting reports

Reports show performance of company at specific period. Management accounting report

combines all financial information of company and present position in respect to market.

Connect catering service can utilize it to plan, organize, decision-making, evaluation efforts, etc.

The different methodologies of management accounting are account receivable ageing, cost

managerial accounting, performance, budget and other reports.

Account Receivable Ageing Report

There are various kinds that assist organization to reach at conclusion so that strategic

decision can be ascertained. The one of important written summary which is known as account

receivable ageing report that refers to categorizing company's account receivable according to

durations of time. CCS can use this to determine financial health of its clients. In case of more

bad debts it can get an idea of tightening its credit policies so that better policy can derived

(Hlaciuc and et.al., 2017). To prepare an effective report firm should segregate unpaid invoices

of clients with number of days it is outstanding. It aids institution to formulate best credit dealing

strategies so CCS can be safe from becoming insolvent due to more bad debts and fraud clients.

It can be differentiated on the basis of account, note & other receivable that provide ease in

preparing report.

Cost Managerial Accounting Report

It takes all labour, overhead, direct & indirect material for estimation of cost reporting. It

provides overview of all expenditure that has incurred in production of product. Connect

Catering Service can determine price of its products or services so that value of item verses

selling cost can be compared (Zaree and Barzegar, 2017). It provides summary of all information

in turn important decision formation can be exerted. Inventory waste, labour hours, overhead

cost are evaluated through this kind ODF management accounting replot. Connect Catering

services will get assistance planning, evaluating, measuring and taking crucial decision that can

help in improving functioning of business.

Performance Report

This is created to review efforts of company in particular context. It comprises status,

variance, forecasting, trend, evaluation, project management, trend and earned value

4

P2 Explaining different methods used for management accounting reports

Reports show performance of company at specific period. Management accounting report

combines all financial information of company and present position in respect to market.

Connect catering service can utilize it to plan, organize, decision-making, evaluation efforts, etc.

The different methodologies of management accounting are account receivable ageing, cost

managerial accounting, performance, budget and other reports.

Account Receivable Ageing Report

There are various kinds that assist organization to reach at conclusion so that strategic

decision can be ascertained. The one of important written summary which is known as account

receivable ageing report that refers to categorizing company's account receivable according to

durations of time. CCS can use this to determine financial health of its clients. In case of more

bad debts it can get an idea of tightening its credit policies so that better policy can derived

(Hlaciuc and et.al., 2017). To prepare an effective report firm should segregate unpaid invoices

of clients with number of days it is outstanding. It aids institution to formulate best credit dealing

strategies so CCS can be safe from becoming insolvent due to more bad debts and fraud clients.

It can be differentiated on the basis of account, note & other receivable that provide ease in

preparing report.

Cost Managerial Accounting Report

It takes all labour, overhead, direct & indirect material for estimation of cost reporting. It

provides overview of all expenditure that has incurred in production of product. Connect

Catering Service can determine price of its products or services so that value of item verses

selling cost can be compared (Zaree and Barzegar, 2017). It provides summary of all information

in turn important decision formation can be exerted. Inventory waste, labour hours, overhead

cost are evaluated through this kind ODF management accounting replot. Connect Catering

services will get assistance planning, evaluating, measuring and taking crucial decision that can

help in improving functioning of business.

Performance Report

This is created to review efforts of company in particular context. It comprises status,

variance, forecasting, trend, evaluation, project management, trend and earned value

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance Report (PR). The purpose of preparing this kind of written document is giving clear

and precise picture of efforts to firm managements. With help of this information CCS would be

in position to take improvement actions that better outcome can be derived. Procedure involves

decoding present efforts, setting realistic goal, evaluating weakness for modification. By

reviewing these individuals are awarded for committent towards organization and performer of

below set standards are provided with training & development programs (Campanale, Cinquini

and Grossi, 2021.). It aims at achieving firm's goal along with employees personal development.

PR is utilized by various type of company to keep its mission accurate by matching actual

performance with established standards.

Budget Report

There are various types of budgets such a business, corporate level, etc. It's all are

prepared with aim of comparing established standards with current performance of institutions.

Accuracy of funds consumption related to specific department is ascertained from this kind of

report. It provides basic guidelines to all employees of operations, sales, marketing, finance, etc.

that how they are expected to used allocated funds. Period for which it is formulated varies from

company to company that incudes, one month, quarterly, half-yearly and yearly. From the

reference of this prepared report unforeseen circumstances can be handled. Budget report

provide assurance of proper accumulation of financial resources so that desire outcome can be

obtained. It also serves basic guidelines for rewarding employees with incentives, bonus, etc.

Effective solutions for making rectification in functioning of business is acquired through these

methodologies.

Other Reports

Analytical, proposal, process, vertical & horizontal reports, any many more play vital role

in influencing performance of organization (Jia, 2020). These reports are generally outsourced

from specialized professionals in turn better productivity, cost & efforts are as well saved.

Moreover, skills and knowledge of specialize workers expected performance can be attained in

exchange for asked fees.

TASK 2

P- 3 Calculation of the costs

Statement of Marginal costing

Particulars April May

5

and precise picture of efforts to firm managements. With help of this information CCS would be

in position to take improvement actions that better outcome can be derived. Procedure involves

decoding present efforts, setting realistic goal, evaluating weakness for modification. By

reviewing these individuals are awarded for committent towards organization and performer of

below set standards are provided with training & development programs (Campanale, Cinquini

and Grossi, 2021.). It aims at achieving firm's goal along with employees personal development.

PR is utilized by various type of company to keep its mission accurate by matching actual

performance with established standards.

Budget Report

There are various types of budgets such a business, corporate level, etc. It's all are

prepared with aim of comparing established standards with current performance of institutions.

Accuracy of funds consumption related to specific department is ascertained from this kind of

report. It provides basic guidelines to all employees of operations, sales, marketing, finance, etc.

that how they are expected to used allocated funds. Period for which it is formulated varies from

company to company that incudes, one month, quarterly, half-yearly and yearly. From the

reference of this prepared report unforeseen circumstances can be handled. Budget report

provide assurance of proper accumulation of financial resources so that desire outcome can be

obtained. It also serves basic guidelines for rewarding employees with incentives, bonus, etc.

Effective solutions for making rectification in functioning of business is acquired through these

methodologies.

Other Reports

Analytical, proposal, process, vertical & horizontal reports, any many more play vital role

in influencing performance of organization (Jia, 2020). These reports are generally outsourced

from specialized professionals in turn better productivity, cost & efforts are as well saved.

Moreover, skills and knowledge of specialize workers expected performance can be attained in

exchange for asked fees.

TASK 2

P- 3 Calculation of the costs

Statement of Marginal costing

Particulars April May

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue from Operations (Sales) (2000 units* 8)= 16000 (2000 units* 8)= 16000

Less Variable costs (2500 units*4)= 10000 (3000 units*4)= 12000

Add Opening stock Nil (500 units*4)= 2000

Less Closing stock (500 units*4)= 2000 (1500 units*4)= 6000

Cost of goods sold (10000-2000)= 8000 (12000+2000-6000)= 8000

Contribution (16000-8000)= 8000 (16000-8000)= 8000

Less Fixed manufacturing overhead 15000 15000

Less Fixed non-manufacturing

overhead 4000 4000

Loss -11000 -11000

As per the statement of the marginal costing it can be analysed that in both the months April and

May the company Connect Catering services is earning the same amount of loss that is -11000.

In this method all the variable costs are charged to the product in deriving at the cost of goods

sold. Post that the fixed overheads are subtracted to find out the profitability for the period.

Statement of Absorption costing

Particulars April May

Revenue from Operations (Sales) (2000 units* 8)= 16000 (2000 units* 8)= 16000

Less Variable costs (2500 units*4)= 10000 (3000 units*4)= 12000

Less Fixed manufacturing overhead 15000 15000

Cost of goods available for sale (10000+15000)= 25000 (12000+15000)= 27000

Add Opening stock Nil (500 units*10)= 5000

Less Closing stock (500 units*10)= 5000 (1500 units*9)= 13500

Cost of goods sold (25000-5000)= 20000

(27000+5000-13500)=

18500

Gross profit (16000-20000)= -4000 (16000-18500)= -2500

Less Fixed non-manufacturing

overhead 4000 4000

Net loss -8000 -6500

As per the statement prepared through the absorption costing it can be analysed that the company

is incurring loss of 8000 in April and loss of 6500 in May. In this method all the manufacturing

costs are charged to the product in assessing its cost and the remaining non-manufacturing

overheads shall be subtracted to find out the profitability.

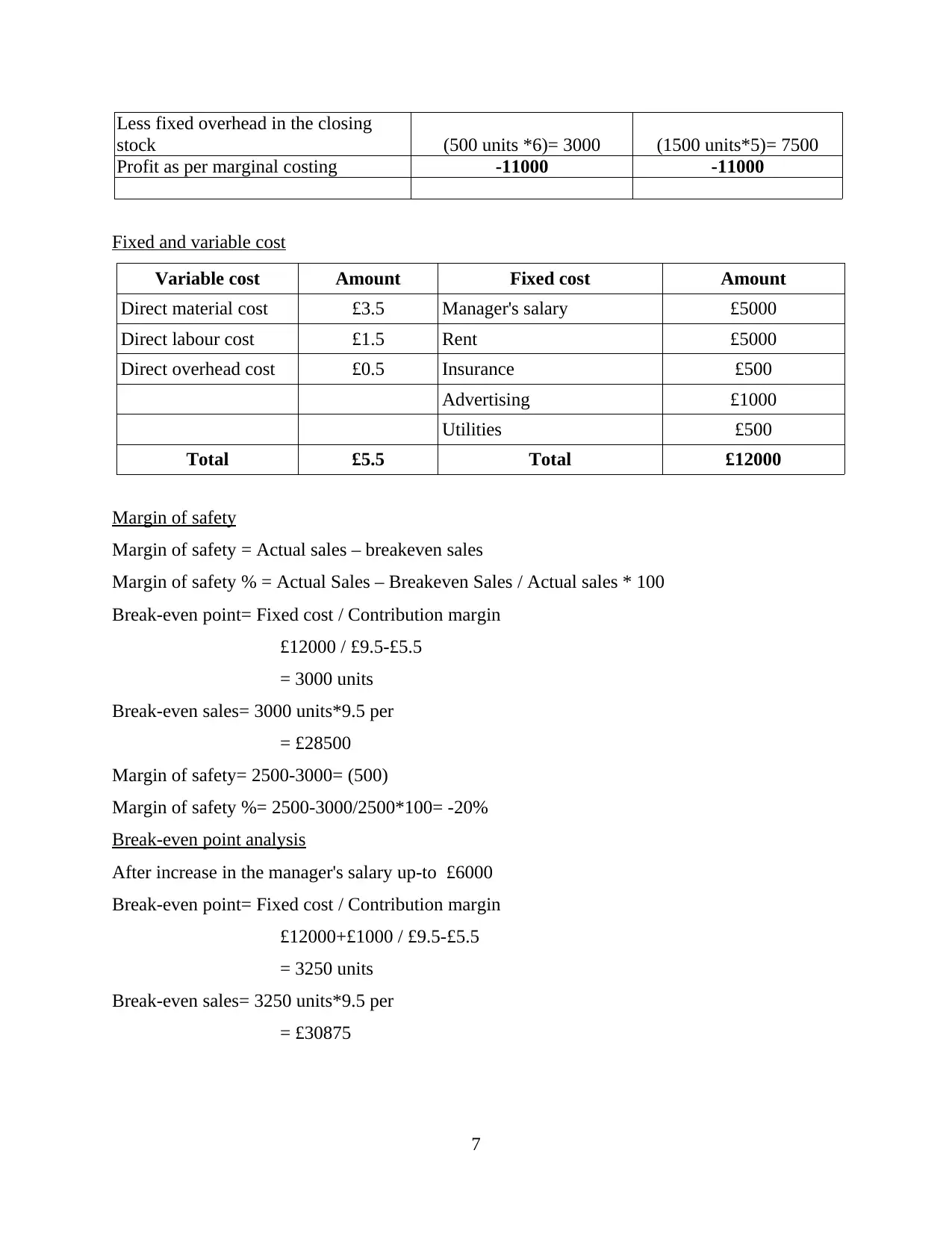

Reconciliation statement

Particulars April May

Profit as per absorption costing -8000 -6500

Add Opening stock Nil (500 units *6)= 3000

6

Less Variable costs (2500 units*4)= 10000 (3000 units*4)= 12000

Add Opening stock Nil (500 units*4)= 2000

Less Closing stock (500 units*4)= 2000 (1500 units*4)= 6000

Cost of goods sold (10000-2000)= 8000 (12000+2000-6000)= 8000

Contribution (16000-8000)= 8000 (16000-8000)= 8000

Less Fixed manufacturing overhead 15000 15000

Less Fixed non-manufacturing

overhead 4000 4000

Loss -11000 -11000

As per the statement of the marginal costing it can be analysed that in both the months April and

May the company Connect Catering services is earning the same amount of loss that is -11000.

In this method all the variable costs are charged to the product in deriving at the cost of goods

sold. Post that the fixed overheads are subtracted to find out the profitability for the period.

Statement of Absorption costing

Particulars April May

Revenue from Operations (Sales) (2000 units* 8)= 16000 (2000 units* 8)= 16000

Less Variable costs (2500 units*4)= 10000 (3000 units*4)= 12000

Less Fixed manufacturing overhead 15000 15000

Cost of goods available for sale (10000+15000)= 25000 (12000+15000)= 27000

Add Opening stock Nil (500 units*10)= 5000

Less Closing stock (500 units*10)= 5000 (1500 units*9)= 13500

Cost of goods sold (25000-5000)= 20000

(27000+5000-13500)=

18500

Gross profit (16000-20000)= -4000 (16000-18500)= -2500

Less Fixed non-manufacturing

overhead 4000 4000

Net loss -8000 -6500

As per the statement prepared through the absorption costing it can be analysed that the company

is incurring loss of 8000 in April and loss of 6500 in May. In this method all the manufacturing

costs are charged to the product in assessing its cost and the remaining non-manufacturing

overheads shall be subtracted to find out the profitability.

Reconciliation statement

Particulars April May

Profit as per absorption costing -8000 -6500

Add Opening stock Nil (500 units *6)= 3000

6

Less fixed overhead in the closing

stock (500 units *6)= 3000 (1500 units*5)= 7500

Profit as per marginal costing -11000 -11000

Fixed and variable cost

Variable cost Amount Fixed cost Amount

Direct material cost £3.5 Manager's salary £5000

Direct labour cost £1.5 Rent £5000

Direct overhead cost £0.5 Insurance £500

Advertising £1000

Utilities £500

Total £5.5 Total £12000

Margin of safety

Margin of safety = Actual sales – breakeven sales

Margin of safety % = Actual Sales – Breakeven Sales / Actual sales * 100

Break-even point= Fixed cost / Contribution margin

£12000 / £9.5-£5.5

= 3000 units

Break-even sales= 3000 units*9.5 per

= £28500

Margin of safety= 2500-3000= (500)

Margin of safety %= 2500-3000/2500*100= -20%

Break-even point analysis

After increase in the manager's salary up-to £6000

Break-even point= Fixed cost / Contribution margin

£12000+£1000 / £9.5-£5.5

= 3250 units

Break-even sales= 3250 units*9.5 per

= £30875

7

stock (500 units *6)= 3000 (1500 units*5)= 7500

Profit as per marginal costing -11000 -11000

Fixed and variable cost

Variable cost Amount Fixed cost Amount

Direct material cost £3.5 Manager's salary £5000

Direct labour cost £1.5 Rent £5000

Direct overhead cost £0.5 Insurance £500

Advertising £1000

Utilities £500

Total £5.5 Total £12000

Margin of safety

Margin of safety = Actual sales – breakeven sales

Margin of safety % = Actual Sales – Breakeven Sales / Actual sales * 100

Break-even point= Fixed cost / Contribution margin

£12000 / £9.5-£5.5

= 3000 units

Break-even sales= 3000 units*9.5 per

= £28500

Margin of safety= 2500-3000= (500)

Margin of safety %= 2500-3000/2500*100= -20%

Break-even point analysis

After increase in the manager's salary up-to £6000

Break-even point= Fixed cost / Contribution margin

£12000+£1000 / £9.5-£5.5

= 3250 units

Break-even sales= 3250 units*9.5 per

= £30875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

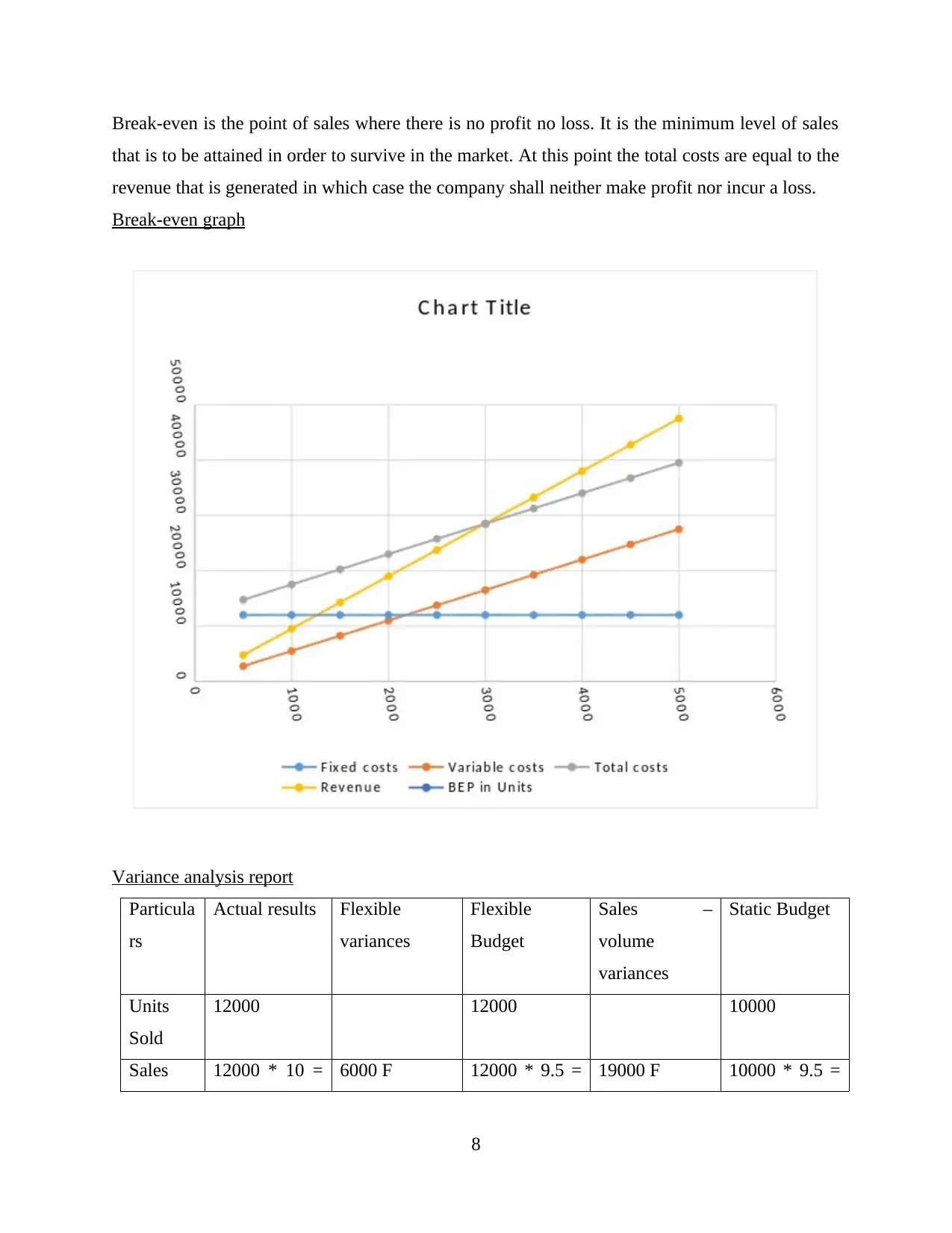

Break-even is the point of sales where there is no profit no loss. It is the minimum level of sales

that is to be attained in order to survive in the market. At this point the total costs are equal to the

revenue that is generated in which case the company shall neither make profit nor incur a loss.

Break-even graph

Variance analysis report

Particula

rs

Actual results Flexible

variances

Flexible

Budget

Sales –

volume

variances

Static Budget

Units

Sold

12000 12000 10000

Sales 12000 * 10 = 6000 F 12000 * 9.5 = 19000 F 10000 * 9.5 =

8

that is to be attained in order to survive in the market. At this point the total costs are equal to the

revenue that is generated in which case the company shall neither make profit nor incur a loss.

Break-even graph

Variance analysis report

Particula

rs

Actual results Flexible

variances

Flexible

Budget

Sales –

volume

variances

Static Budget

Units

Sold

12000 12000 10000

Sales 12000 * 10 = 6000 F 12000 * 9.5 = 19000 F 10000 * 9.5 =

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

120000 114000 95000

Variable

cost

12000 * 5

= 60000

6000 F 12000 * 5.5 =

66000

11000 U 10000 * 5.5 =

55000

Contribu

tion

Margin

60000 12000 F 48000 8000 F 40000

Fixed

Costs

15000 3000 U 12000 0 12000

Profit 45000 9000 F 36000 8000 F 28000

Flexible Budget variance = 9000 (F)

Sales Volume Variance = 8000 (F)

TASK 3

P- 4 Advantages and disadvantages of the different planning tools used for budgetary control

The planning tools that are used for the purpose of budgetary control are the various

types of budgets that assists the business in forecasting the future activities and the level of

operations that can be undertaken and its simultaneous costs.

Cash Budgets:- The cash budget is the planning tool that is used to estimate the cash flows that

shall be taking place in the future. It shall be measuring the inflows and the disbursements that

shall be taking place. This will assists in managing the liquidity in an efficient manner so that

shortage as well as idle cash both is avoided (Chen, 2017).

Advantages:-

One of the most significant benefit is that it shall ensure the credibility of the brand by

timely efficiently meeting all the debts of the company.

The budgeting related to the cash makes the company more resourceful in terms of

managing its finances and also avoiding wasteful expenditures.

Helps in maintaining the liquidity position in the company and identifying the deficits of

the business.

Disadvantage:-

The major disadvantage is that it limits the power to spend or the flexibility of the

decisions that are associated with the usage of cash and equivalents.

9

Variable

cost

12000 * 5

= 60000

6000 F 12000 * 5.5 =

66000

11000 U 10000 * 5.5 =

55000

Contribu

tion

Margin

60000 12000 F 48000 8000 F 40000

Fixed

Costs

15000 3000 U 12000 0 12000

Profit 45000 9000 F 36000 8000 F 28000

Flexible Budget variance = 9000 (F)

Sales Volume Variance = 8000 (F)

TASK 3

P- 4 Advantages and disadvantages of the different planning tools used for budgetary control

The planning tools that are used for the purpose of budgetary control are the various

types of budgets that assists the business in forecasting the future activities and the level of

operations that can be undertaken and its simultaneous costs.

Cash Budgets:- The cash budget is the planning tool that is used to estimate the cash flows that

shall be taking place in the future. It shall be measuring the inflows and the disbursements that

shall be taking place. This will assists in managing the liquidity in an efficient manner so that

shortage as well as idle cash both is avoided (Chen, 2017).

Advantages:-

One of the most significant benefit is that it shall ensure the credibility of the brand by

timely efficiently meeting all the debts of the company.

The budgeting related to the cash makes the company more resourceful in terms of

managing its finances and also avoiding wasteful expenditures.

Helps in maintaining the liquidity position in the company and identifying the deficits of

the business.

Disadvantage:-

The major disadvantage is that it limits the power to spend or the flexibility of the

decisions that are associated with the usage of cash and equivalents.

9

The details related to the balances of cash can be dangerous for criminal activities like

theft and confidentiality. Also, it only reflects the liquidity position but offers no idea related to the profitability or

the financial position of the company.

Expenditure budgets:- The expenditure budget shall be forecasting regarding the revenue and

the capital expenditure that shall be undertaken by the business in the coming period (Cools,

Stouthuysen and Van den Abbeele, 2017). Based on these expenditures the cost-benefit analysis

can be undertaken and help the management decide regarding the profit margins.

Advantages:-

This budgeting shall assist in the optimization of the expenses and avoiding the

unnecessary expenditures.

It shall help in ascertaining the selling price of the product based on the expenses that are

done over it.

Disadvantages:- It reduces the flexibility of planning related to generating the operational efficiency in the

business.

Flexible Budgets:- A flexible budget is one in which the forecasting is done for the various

levels of activity that can be undertaken in the business. These budgets gets adjusted as per the

various different levels of operations.

Advantages:-

It shall develop the understanding regarding the performance at various levels of

operations (Barr and McClellan, 2018).

The most optimum level generating the highest profitability for the company shall be

applied. It shall facilitate comparison.

Disadvantages:- The formulation of such flex budget is a complicated procedure as it shall be defining all

the components of the cost and the adjustment is also a tedious job.

Zero-based budgeting:- Zero based budgeting refers to estimations made from the scratch that is

by taking the base as zero. In this method of budgeting the data from the previous year is not

used and all the expenses and revenues are applied in the budget through proper justification of

the same (Zubarevich, 2020).

10

theft and confidentiality. Also, it only reflects the liquidity position but offers no idea related to the profitability or

the financial position of the company.

Expenditure budgets:- The expenditure budget shall be forecasting regarding the revenue and

the capital expenditure that shall be undertaken by the business in the coming period (Cools,

Stouthuysen and Van den Abbeele, 2017). Based on these expenditures the cost-benefit analysis

can be undertaken and help the management decide regarding the profit margins.

Advantages:-

This budgeting shall assist in the optimization of the expenses and avoiding the

unnecessary expenditures.

It shall help in ascertaining the selling price of the product based on the expenses that are

done over it.

Disadvantages:- It reduces the flexibility of planning related to generating the operational efficiency in the

business.

Flexible Budgets:- A flexible budget is one in which the forecasting is done for the various

levels of activity that can be undertaken in the business. These budgets gets adjusted as per the

various different levels of operations.

Advantages:-

It shall develop the understanding regarding the performance at various levels of

operations (Barr and McClellan, 2018).

The most optimum level generating the highest profitability for the company shall be

applied. It shall facilitate comparison.

Disadvantages:- The formulation of such flex budget is a complicated procedure as it shall be defining all

the components of the cost and the adjustment is also a tedious job.

Zero-based budgeting:- Zero based budgeting refers to estimations made from the scratch that is

by taking the base as zero. In this method of budgeting the data from the previous year is not

used and all the expenses and revenues are applied in the budget through proper justification of

the same (Zubarevich, 2020).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.