Management Accounting Report: ABC Company's Financial Strategies

VerifiedAdded on 2023/01/10

|24

|3992

|21

Report

AI Summary

This report delves into management accounting practices, focusing on ABC Company's financial strategies. It examines cost classifications, including marginal and opportunity costs, and applies absorption and marginal costing methods to calculate unit costs for Personal Computers (PC) and Video Players (VP). The report analyzes the impact of limited direct labor hours on production mix, advising on profit maximization. Furthermore, it explores the budgeting process, its functions, and the advantages and disadvantages of budgetary control systems. The report also includes the preparation of various budgets and raw material variance calculations. It concludes with recommendations based on the findings, emphasizing the importance of marginal costing for special orders and break-even analysis.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

1.1 Management Accounting and its diverse systems.................................................................4

1.2 Different accounting reports used by the ABC Company and its importance:......................4

2.1 Explain the classification of costs that would help the management decision-making.........5

2.2 Calculate the unit costs of PC and VP based on absorption costing and marginal costing

methods........................................................................................................................................6

2.3 Given that direct labour available is limited to 60,000 hours per month, advise the

optimum production mix of PC and VP to maximize profit......................................................12

Part A.............................................................................................................................................13

Following are the management accounting techniques which are discussed as below:............13

Part B Budgeting Process:.............................................................................................................13

3.1 The major functions of budgeting process...........................................................................13

3.1 Advantages and disadvantages in operating a budgetary control system............................14

Part C: Budgetary Planning:..........................................................................................................16

Preparation of various budgets as follows:................................................................................16

Part D.............................................................................................................................................19

4.1 Calculate the raw material variance.....................................................................................19

Conclusion.....................................................................................................................................21

References......................................................................................................................................22

2

Introduction......................................................................................................................................3

1.1 Management Accounting and its diverse systems.................................................................4

1.2 Different accounting reports used by the ABC Company and its importance:......................4

2.1 Explain the classification of costs that would help the management decision-making.........5

2.2 Calculate the unit costs of PC and VP based on absorption costing and marginal costing

methods........................................................................................................................................6

2.3 Given that direct labour available is limited to 60,000 hours per month, advise the

optimum production mix of PC and VP to maximize profit......................................................12

Part A.............................................................................................................................................13

Following are the management accounting techniques which are discussed as below:............13

Part B Budgeting Process:.............................................................................................................13

3.1 The major functions of budgeting process...........................................................................13

3.1 Advantages and disadvantages in operating a budgetary control system............................14

Part C: Budgetary Planning:..........................................................................................................16

Preparation of various budgets as follows:................................................................................16

Part D.............................................................................................................................................19

4.1 Calculate the raw material variance.....................................................................................19

Conclusion.....................................................................................................................................21

References......................................................................................................................................22

2

Introduction

Management accounting is become the most crucial filed for the business for making the

operations of the company easier and cheaper by deducting unnecessary cost from the product.

However, in this report, ABC Company is take which ultimately work for producing electronic

products. Its main aim to produce personal computers and video players. In order to produce

these products, cited company would use various management accounting techniques along with

diverse method that used in accounting reporting. Various budgetary tools are used in this report

along with various management accounting systems which are used for addressing financial

problems for a particular period of time.

3

Management accounting is become the most crucial filed for the business for making the

operations of the company easier and cheaper by deducting unnecessary cost from the product.

However, in this report, ABC Company is take which ultimately work for producing electronic

products. Its main aim to produce personal computers and video players. In order to produce

these products, cited company would use various management accounting techniques along with

diverse method that used in accounting reporting. Various budgetary tools are used in this report

along with various management accounting systems which are used for addressing financial

problems for a particular period of time.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.1 Management Accounting and its diverse systems

Management Accounting: This is the process of analyzing financial and non- financial

information for the management in order to meet the overall objectives. This is the system which

is required tool used by the ABC company for optimizing its operational process (Ax and Greve,

2017).

Here is diverse kind management accounting systems which are elaborated as under:

Cost Accounting System: This is one of the best accounting tools which is used by the

management for optimizing its production process in order to eliminate unnecessary cost from

the cost of product. Apart from that, ABC Company uses this system in order to optimize the

product costs so that it could maximize the profits by selling the product at a cheaper cost in the

market (Boučková, 2015).

Profit optimization System: This is the system which fix up the price of the product as per the

consumer set of mind along with its rivals. This is considered to be the crucial task ever. It is

fixed by setting diverse price of the product and then checks the market demand so that the

company could fix the price and optimize the profits (Hilton and Platt, 2013).

Inventory Management System: Under this, various inventory values is determined as per

using LIFO, FIFO or AVGO. By using this, ABC Company would optimize its resources and get

to know about the product cycling process which will ultimately assist to gain the competitive

advantage (RW Hiebl, 2013). Additionally, this assists in reducing the costs and optimizing the

profits over the product by knowing in advance an inventory needs in future production of the

product (Weygandt, et. al., 2015).

1.2 Different accounting reports used by the ABC Company and its importance:

There are so many management accounting reports which are used by the management for each

department and render reliable information to the managers within the organization. However,

management makes various reports and their advantages are specified as under:

4

Management Accounting: This is the process of analyzing financial and non- financial

information for the management in order to meet the overall objectives. This is the system which

is required tool used by the ABC company for optimizing its operational process (Ax and Greve,

2017).

Here is diverse kind management accounting systems which are elaborated as under:

Cost Accounting System: This is one of the best accounting tools which is used by the

management for optimizing its production process in order to eliminate unnecessary cost from

the cost of product. Apart from that, ABC Company uses this system in order to optimize the

product costs so that it could maximize the profits by selling the product at a cheaper cost in the

market (Boučková, 2015).

Profit optimization System: This is the system which fix up the price of the product as per the

consumer set of mind along with its rivals. This is considered to be the crucial task ever. It is

fixed by setting diverse price of the product and then checks the market demand so that the

company could fix the price and optimize the profits (Hilton and Platt, 2013).

Inventory Management System: Under this, various inventory values is determined as per

using LIFO, FIFO or AVGO. By using this, ABC Company would optimize its resources and get

to know about the product cycling process which will ultimately assist to gain the competitive

advantage (RW Hiebl, 2013). Additionally, this assists in reducing the costs and optimizing the

profits over the product by knowing in advance an inventory needs in future production of the

product (Weygandt, et. al., 2015).

1.2 Different accounting reports used by the ABC Company and its importance:

There are so many management accounting reports which are used by the management for each

department and render reliable information to the managers within the organization. However,

management makes various reports and their advantages are specified as under:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget Reports: This is the report which is used by the management in each of the department

within the organization. While making the report, past information are used and then make the

budget reports for the future period of time. With the help of this report, company would make

their plans and forecast their spending accordingly (Maynard, 2017).

Performance Report: This is the report which is made on the past performance. As, this

comprises overall firm performance. Hereunder, firm actual performance is made with the

forecasted performance which ultimately gives assistance for the company to record performance

in each department (Senftlechner and Hiebl, 2015).

Inventory Report: This report is totally made upon the inventory. This report assists

organization for knowing inventory level which is present. They likewise render information

about inventory which is going to use in the business for producing output.

2.1 Explain the classification of costs that would help the management decision-

making

Following there are five main types of classification of costs which are listed below:

Cost Classification in Relation to Cost Centre

Cost Classification by Nature of Production Process

Cost Classification for Decision Making

Cost Classification by Nature

Cost Classification for Decision Making

i. Marginal Cost: Marginal cost is the additional or extra cost incurred for the manufacturing of

an extra unit of output. In other words, it is a variable cost of one unit of goods or service (Drury,

2013).

ii. Opportunity Cost: For an alternative course of action, it is the value of a benefit which is

sacrificed. It is the good or service cost measured in terms of profits or revenue which could have

been received by using that product or service in some other alternative uses (Ax and Greve,

2017).

5

within the organization. While making the report, past information are used and then make the

budget reports for the future period of time. With the help of this report, company would make

their plans and forecast their spending accordingly (Maynard, 2017).

Performance Report: This is the report which is made on the past performance. As, this

comprises overall firm performance. Hereunder, firm actual performance is made with the

forecasted performance which ultimately gives assistance for the company to record performance

in each department (Senftlechner and Hiebl, 2015).

Inventory Report: This report is totally made upon the inventory. This report assists

organization for knowing inventory level which is present. They likewise render information

about inventory which is going to use in the business for producing output.

2.1 Explain the classification of costs that would help the management decision-

making

Following there are five main types of classification of costs which are listed below:

Cost Classification in Relation to Cost Centre

Cost Classification by Nature of Production Process

Cost Classification for Decision Making

Cost Classification by Nature

Cost Classification for Decision Making

i. Marginal Cost: Marginal cost is the additional or extra cost incurred for the manufacturing of

an extra unit of output. In other words, it is a variable cost of one unit of goods or service (Drury,

2013).

ii. Opportunity Cost: For an alternative course of action, it is the value of a benefit which is

sacrificed. It is the good or service cost measured in terms of profits or revenue which could have

been received by using that product or service in some other alternative uses (Ax and Greve,

2017).

5

iii. Sunk Cost: It is the cost or expenditure which incurred in the past and this cost is not easily

affected by a particular decision under consideration. Sunk costs are utilized in a project and if

the project is terminated it will not be recovered (Frischmann and Hogendorn, 2015).

iv. Differential Cost or Incremental Cost: Differential cost is the change in total cost and this

change will arise due to alternative selection. In other words, it is an added cost of a change in

the activity level (Vanderbeck, 2012).

The above cost helps management in decision making process which minimizes various cost

and expenditure and also helps them to maximize profits or revenue for the company

growth and success.

2.2 Calculate the unit costs of PC and VP based on absorption costing and marginal

costing methods

Definition of Absorption and Marginal costing

Marginal costing is an important costing technique in which the variable cost or marginal cost is

charged to units of costs on the other hand the fixed cost is totally written off against the

contribution (Armitage et al., 2016).

Absorption costing is a system of costing in which all production costs; including fixed costs and

variable costs are categorized as part of product costs (Cokins, 2013).

Classification of overheads in absorption and marginal costing

In marginal costing, overheads are classified into variable and fixed overheads.

In absorption costing, overheads are classified into selling and distribution, production and

administration overheads.

Compliance of GAAP

Marginal Costing is not GAAP compliant

Absorption Costing is GAAP compliant

6

affected by a particular decision under consideration. Sunk costs are utilized in a project and if

the project is terminated it will not be recovered (Frischmann and Hogendorn, 2015).

iv. Differential Cost or Incremental Cost: Differential cost is the change in total cost and this

change will arise due to alternative selection. In other words, it is an added cost of a change in

the activity level (Vanderbeck, 2012).

The above cost helps management in decision making process which minimizes various cost

and expenditure and also helps them to maximize profits or revenue for the company

growth and success.

2.2 Calculate the unit costs of PC and VP based on absorption costing and marginal

costing methods

Definition of Absorption and Marginal costing

Marginal costing is an important costing technique in which the variable cost or marginal cost is

charged to units of costs on the other hand the fixed cost is totally written off against the

contribution (Armitage et al., 2016).

Absorption costing is a system of costing in which all production costs; including fixed costs and

variable costs are categorized as part of product costs (Cokins, 2013).

Classification of overheads in absorption and marginal costing

In marginal costing, overheads are classified into variable and fixed overheads.

In absorption costing, overheads are classified into selling and distribution, production and

administration overheads.

Compliance of GAAP

Marginal Costing is not GAAP compliant

Absorption Costing is GAAP compliant

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

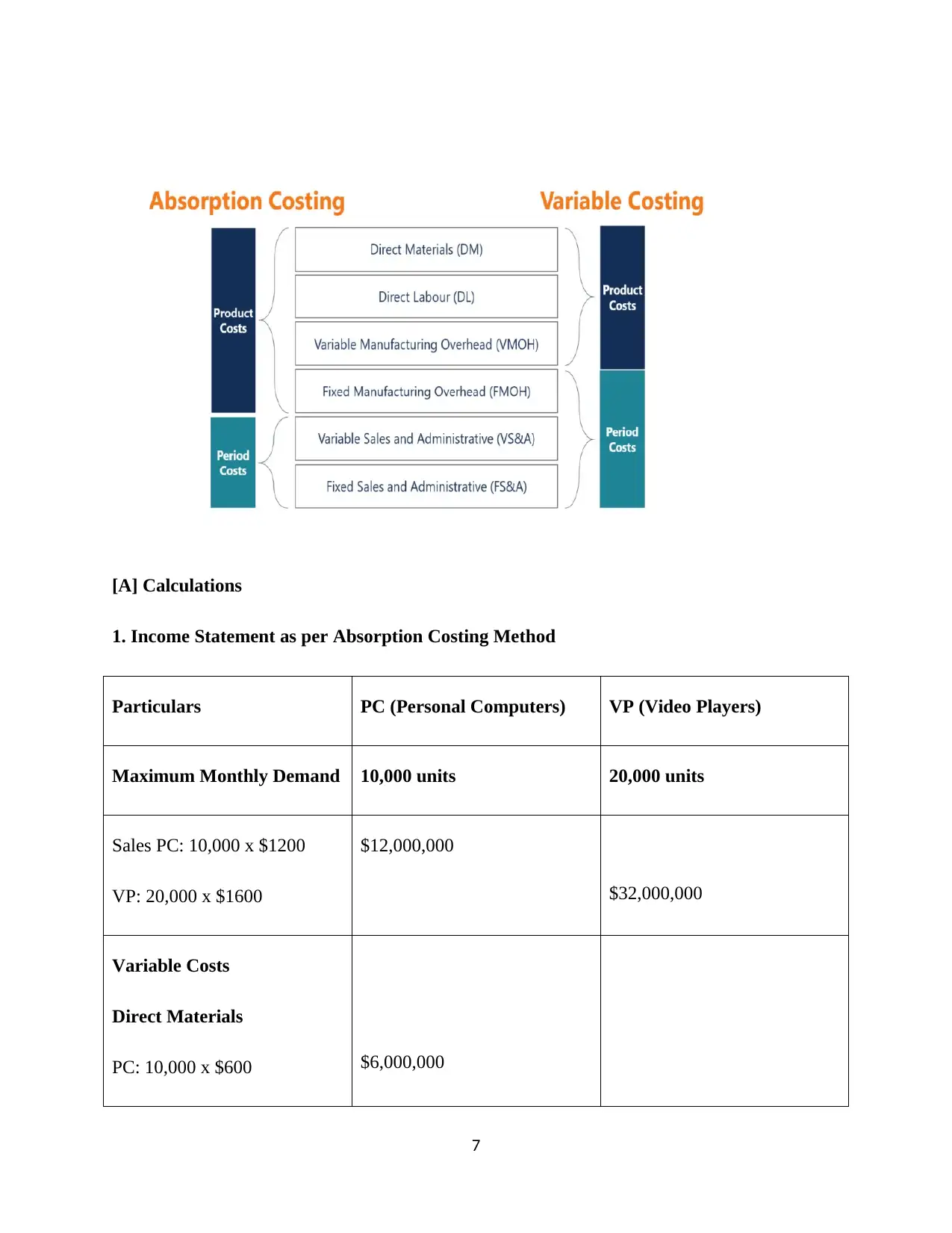

[A] Calculations

1. Income Statement as per Absorption Costing Method

Particulars PC (Personal Computers) VP (Video Players)

Maximum Monthly Demand 10,000 units 20,000 units

Sales PC: 10,000 x $1200

VP: 20,000 x $1600

$12,000,000

$32,000,000

Variable Costs

Direct Materials

PC: 10,000 x $600 $6,000,000

7

1. Income Statement as per Absorption Costing Method

Particulars PC (Personal Computers) VP (Video Players)

Maximum Monthly Demand 10,000 units 20,000 units

Sales PC: 10,000 x $1200

VP: 20,000 x $1600

$12,000,000

$32,000,000

Variable Costs

Direct Materials

PC: 10,000 x $600 $6,000,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

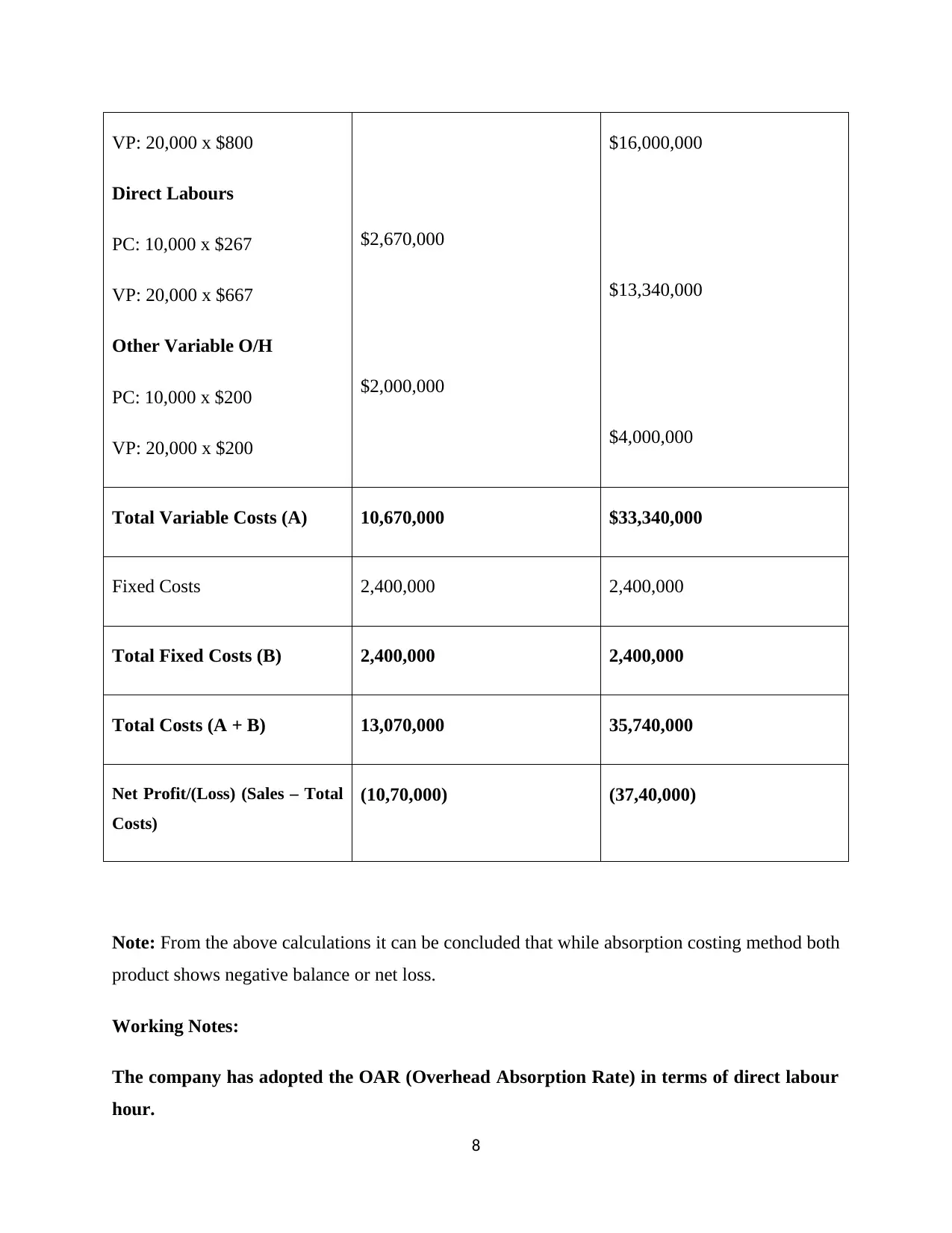

VP: 20,000 x $800

Direct Labours

PC: 10,000 x $267

VP: 20,000 x $667

Other Variable O/H

PC: 10,000 x $200

VP: 20,000 x $200

$2,670,000

$2,000,000

$16,000,000

$13,340,000

$4,000,000

Total Variable Costs (A) 10,670,000 $33,340,000

Fixed Costs 2,400,000 2,400,000

Total Fixed Costs (B) 2,400,000 2,400,000

Total Costs (A + B) 13,070,000 35,740,000

Net Profit/(Loss) (Sales – Total

Costs)

(10,70,000) (37,40,000)

Note: From the above calculations it can be concluded that while absorption costing method both

product shows negative balance or net loss.

Working Notes:

The company has adopted the OAR (Overhead Absorption Rate) in terms of direct labour

hour.

8

Direct Labours

PC: 10,000 x $267

VP: 20,000 x $667

Other Variable O/H

PC: 10,000 x $200

VP: 20,000 x $200

$2,670,000

$2,000,000

$16,000,000

$13,340,000

$4,000,000

Total Variable Costs (A) 10,670,000 $33,340,000

Fixed Costs 2,400,000 2,400,000

Total Fixed Costs (B) 2,400,000 2,400,000

Total Costs (A + B) 13,070,000 35,740,000

Net Profit/(Loss) (Sales – Total

Costs)

(10,70,000) (37,40,000)

Note: From the above calculations it can be concluded that while absorption costing method both

product shows negative balance or net loss.

Working Notes:

The company has adopted the OAR (Overhead Absorption Rate) in terms of direct labour

hour.

8

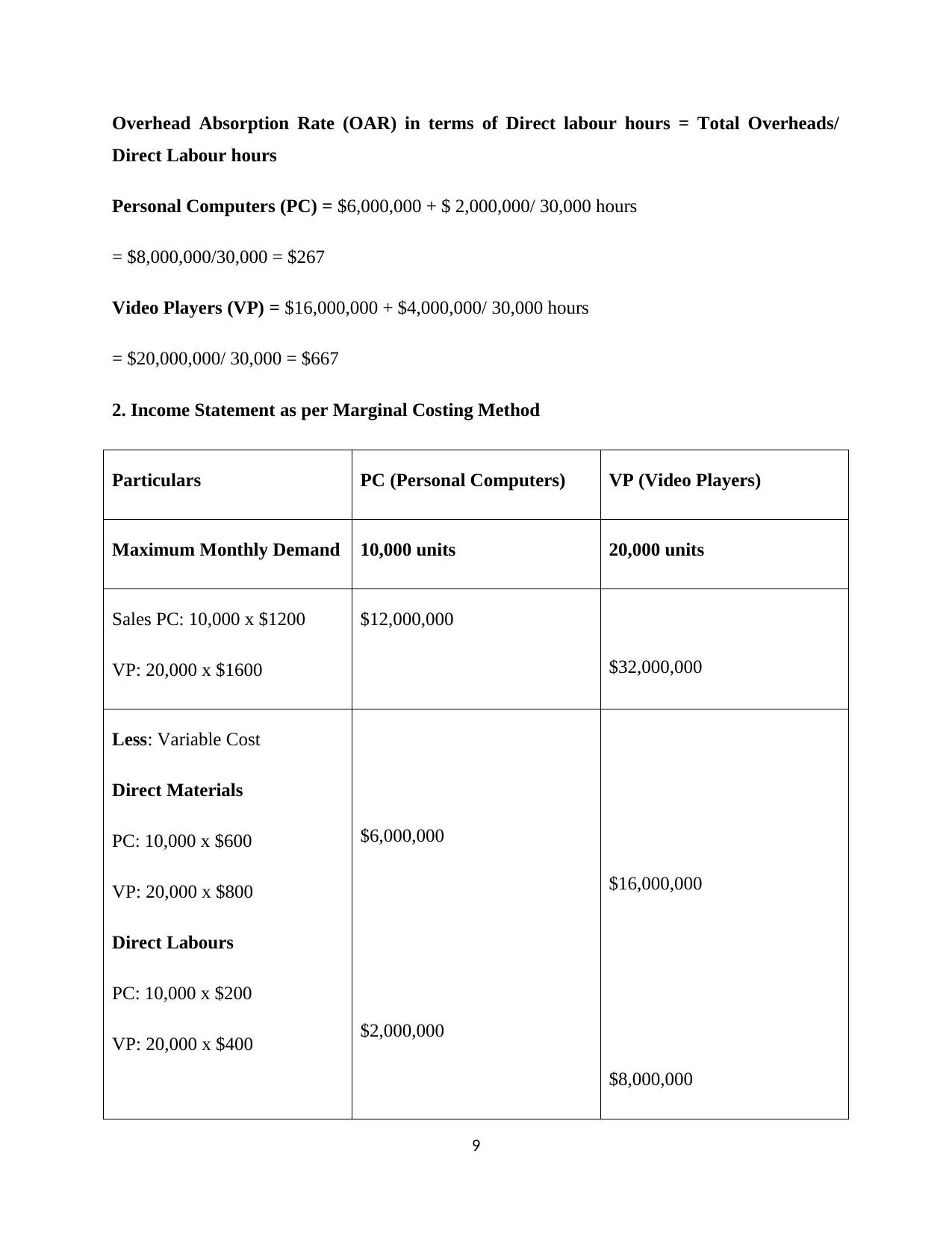

Overhead Absorption Rate (OAR) in terms of Direct labour hours = Total Overheads/

Direct Labour hours

Personal Computers (PC) = $6,000,000 + $ 2,000,000/ 30,000 hours

= $8,000,000/30,000 = $267

Video Players (VP) = $16,000,000 + $4,000,000/ 30,000 hours

= $20,000,000/ 30,000 = $667

2. Income Statement as per Marginal Costing Method

Particulars PC (Personal Computers) VP (Video Players)

Maximum Monthly Demand 10,000 units 20,000 units

Sales PC: 10,000 x $1200

VP: 20,000 x $1600

$12,000,000

$32,000,000

Less: Variable Cost

Direct Materials

PC: 10,000 x $600

VP: 20,000 x $800

Direct Labours

PC: 10,000 x $200

VP: 20,000 x $400

$6,000,000

$2,000,000

$16,000,000

$8,000,000

9

Direct Labour hours

Personal Computers (PC) = $6,000,000 + $ 2,000,000/ 30,000 hours

= $8,000,000/30,000 = $267

Video Players (VP) = $16,000,000 + $4,000,000/ 30,000 hours

= $20,000,000/ 30,000 = $667

2. Income Statement as per Marginal Costing Method

Particulars PC (Personal Computers) VP (Video Players)

Maximum Monthly Demand 10,000 units 20,000 units

Sales PC: 10,000 x $1200

VP: 20,000 x $1600

$12,000,000

$32,000,000

Less: Variable Cost

Direct Materials

PC: 10,000 x $600

VP: 20,000 x $800

Direct Labours

PC: 10,000 x $200

VP: 20,000 x $400

$6,000,000

$2,000,000

$16,000,000

$8,000,000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

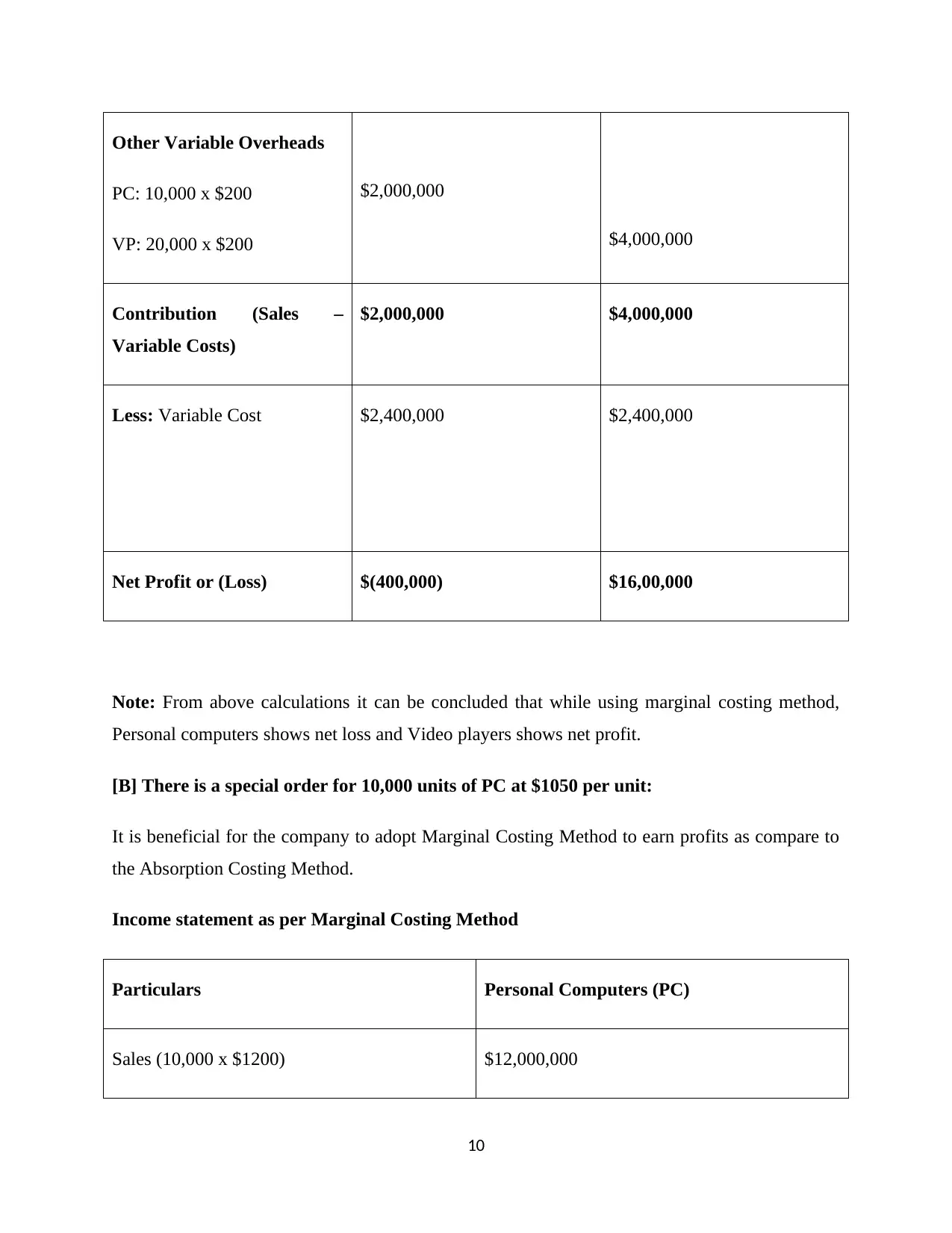

Other Variable Overheads

PC: 10,000 x $200

VP: 20,000 x $200

$2,000,000

$4,000,000

Contribution (Sales –

Variable Costs)

$2,000,000 $4,000,000

Less: Variable Cost $2,400,000 $2,400,000

Net Profit or (Loss) $(400,000) $16,00,000

Note: From above calculations it can be concluded that while using marginal costing method,

Personal computers shows net loss and Video players shows net profit.

[B] There is a special order for 10,000 units of PC at $1050 per unit:

It is beneficial for the company to adopt Marginal Costing Method to earn profits as compare to

the Absorption Costing Method.

Income statement as per Marginal Costing Method

Particulars Personal Computers (PC)

Sales (10,000 x $1200) $12,000,000

10

PC: 10,000 x $200

VP: 20,000 x $200

$2,000,000

$4,000,000

Contribution (Sales –

Variable Costs)

$2,000,000 $4,000,000

Less: Variable Cost $2,400,000 $2,400,000

Net Profit or (Loss) $(400,000) $16,00,000

Note: From above calculations it can be concluded that while using marginal costing method,

Personal computers shows net loss and Video players shows net profit.

[B] There is a special order for 10,000 units of PC at $1050 per unit:

It is beneficial for the company to adopt Marginal Costing Method to earn profits as compare to

the Absorption Costing Method.

Income statement as per Marginal Costing Method

Particulars Personal Computers (PC)

Sales (10,000 x $1200) $12,000,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

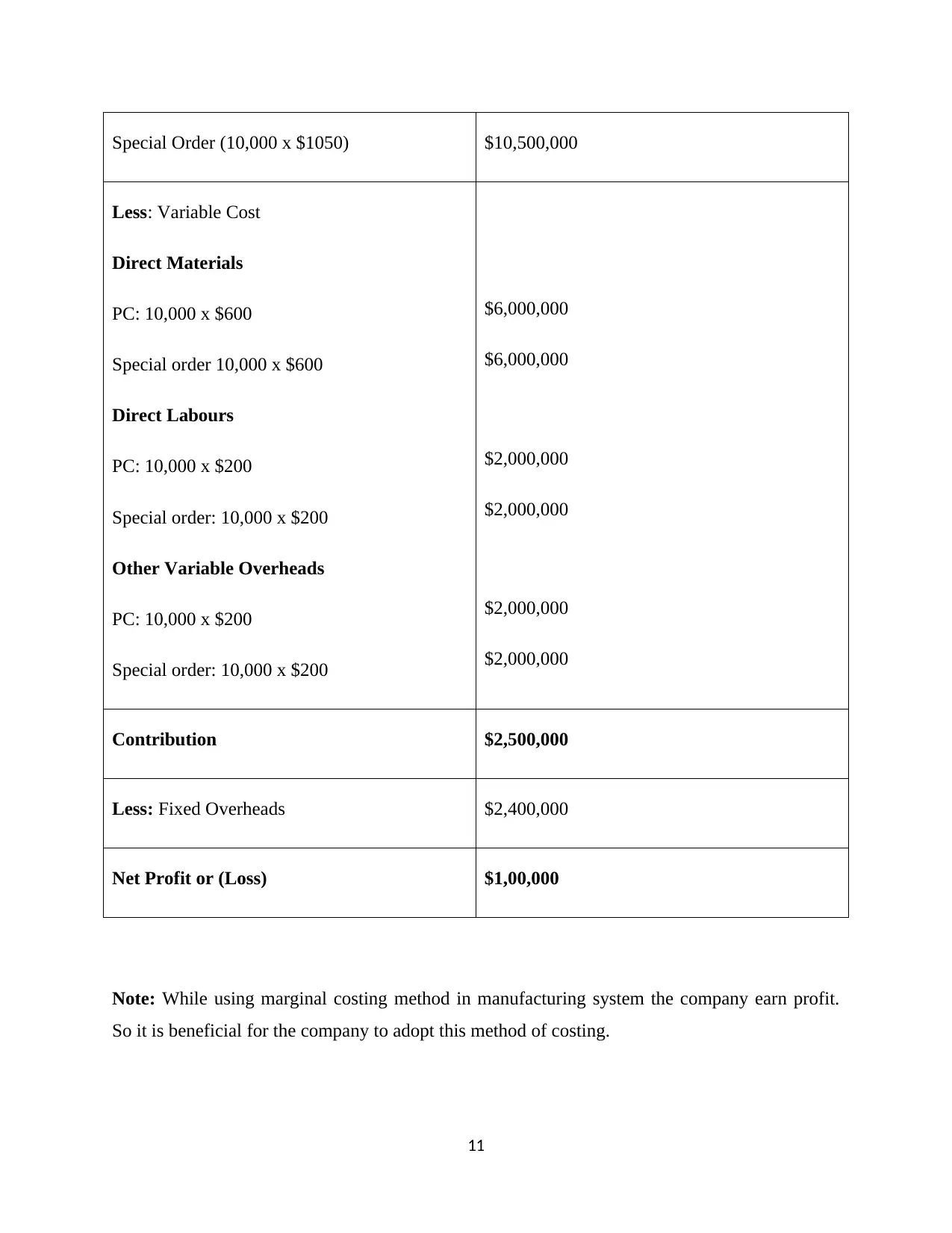

Special Order (10,000 x $1050) $10,500,000

Less: Variable Cost

Direct Materials

PC: 10,000 x $600

Special order 10,000 x $600

Direct Labours

PC: 10,000 x $200

Special order: 10,000 x $200

Other Variable Overheads

PC: 10,000 x $200

Special order: 10,000 x $200

$6,000,000

$6,000,000

$2,000,000

$2,000,000

$2,000,000

$2,000,000

Contribution $2,500,000

Less: Fixed Overheads $2,400,000

Net Profit or (Loss) $1,00,000

Note: While using marginal costing method in manufacturing system the company earn profit.

So it is beneficial for the company to adopt this method of costing.

11

Less: Variable Cost

Direct Materials

PC: 10,000 x $600

Special order 10,000 x $600

Direct Labours

PC: 10,000 x $200

Special order: 10,000 x $200

Other Variable Overheads

PC: 10,000 x $200

Special order: 10,000 x $200

$6,000,000

$6,000,000

$2,000,000

$2,000,000

$2,000,000

$2,000,000

Contribution $2,500,000

Less: Fixed Overheads $2,400,000

Net Profit or (Loss) $1,00,000

Note: While using marginal costing method in manufacturing system the company earn profit.

So it is beneficial for the company to adopt this method of costing.

11

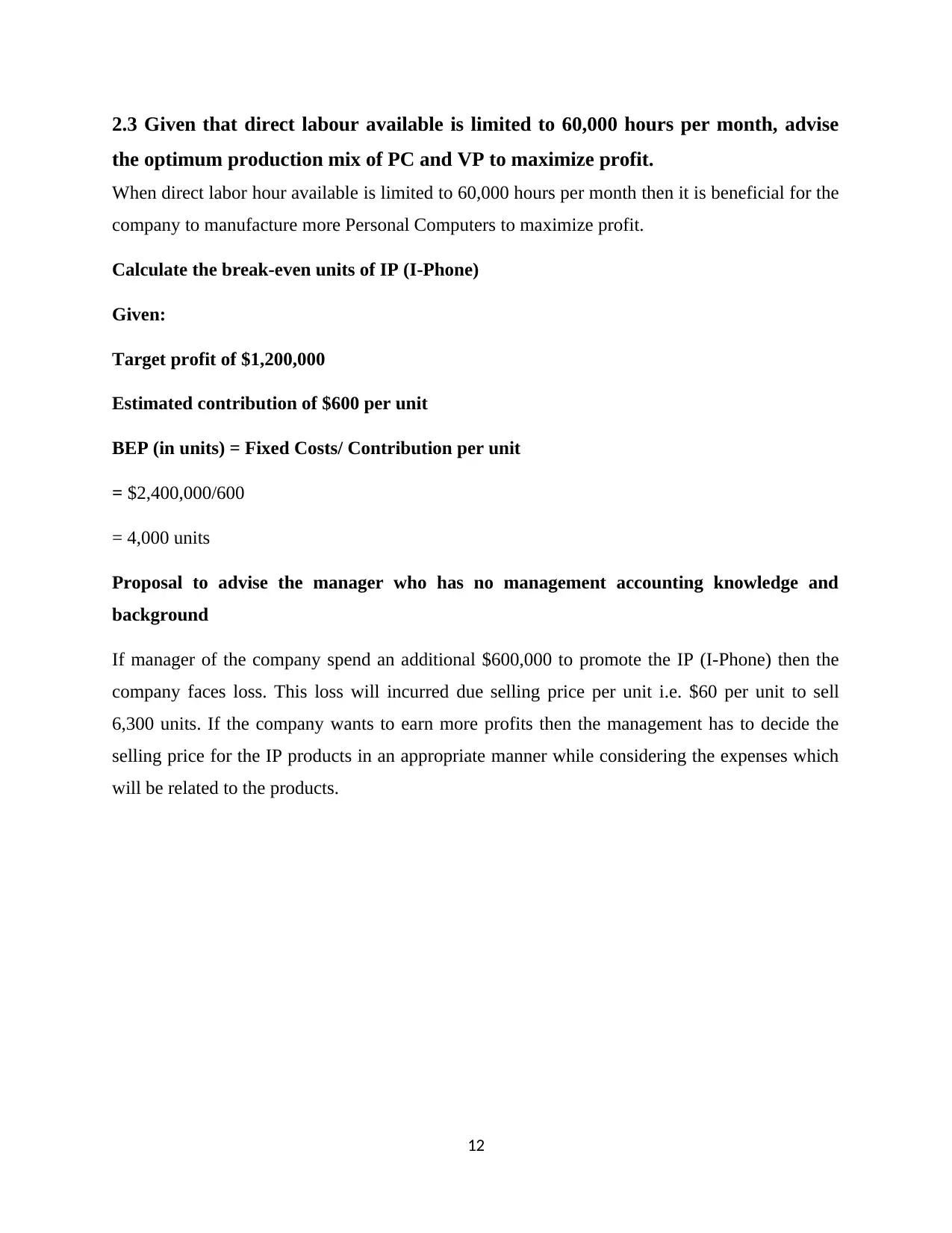

2.3 Given that direct labour available is limited to 60,000 hours per month, advise

the optimum production mix of PC and VP to maximize profit.

When direct labor hour available is limited to 60,000 hours per month then it is beneficial for the

company to manufacture more Personal Computers to maximize profit.

Calculate the break-even units of IP (I-Phone)

Given:

Target profit of $1,200,000

Estimated contribution of $600 per unit

BEP (in units) = Fixed Costs/ Contribution per unit

= $2,400,000/600

= 4,000 units

Proposal to advise the manager who has no management accounting knowledge and

background

If manager of the company spend an additional $600,000 to promote the IP (I-Phone) then the

company faces loss. This loss will incurred due selling price per unit i.e. $60 per unit to sell

6,300 units. If the company wants to earn more profits then the management has to decide the

selling price for the IP products in an appropriate manner while considering the expenses which

will be related to the products.

12

the optimum production mix of PC and VP to maximize profit.

When direct labor hour available is limited to 60,000 hours per month then it is beneficial for the

company to manufacture more Personal Computers to maximize profit.

Calculate the break-even units of IP (I-Phone)

Given:

Target profit of $1,200,000

Estimated contribution of $600 per unit

BEP (in units) = Fixed Costs/ Contribution per unit

= $2,400,000/600

= 4,000 units

Proposal to advise the manager who has no management accounting knowledge and

background

If manager of the company spend an additional $600,000 to promote the IP (I-Phone) then the

company faces loss. This loss will incurred due selling price per unit i.e. $60 per unit to sell

6,300 units. If the company wants to earn more profits then the management has to decide the

selling price for the IP products in an appropriate manner while considering the expenses which

will be related to the products.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.