Management Accounting Report: Absorption, ABC, Break Even Analysis

VerifiedAdded on 2023/01/11

|15

|3826

|41

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive overview of costing methods and break-even analysis. It begins by examining absorption costing and activity-based costing (ABC), detailing their respective advantages and disadvantages, and includes calculations to illustrate their application. The report then transitions to break-even analysis, explaining its significance in modern business environments characterized by both single and multi-product scenarios. It covers the calculation of break-even points, both in units and sales value, and discusses the key components such as fixed costs, variable costs, revenues, and contribution margin. Furthermore, the report outlines the benefits of break-even analysis, including its role in setting revenue targets, arranging business funding, and improving pricing strategies, while also exploring its practical applications in cost calculation, budgeting, and motivation. Overall, the report aims to provide a thorough understanding of these essential management accounting tools and their practical implications for business decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

PART A.......................................................................................................................................................3

Methods of costing..................................................................................................................................3

PART B.......................................................................................................................................................7

Break even analysis.................................................................................................................................7

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

INTRODUCTION.......................................................................................................................................3

PART A.......................................................................................................................................................3

Methods of costing..................................................................................................................................3

PART B.......................................................................................................................................................7

Break even analysis.................................................................................................................................7

CONCLUSION.........................................................................................................................................13

REFERENCES..........................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is providing financial details in this kind of manner as to

facilitate administrators in developing a company's strategy and day-to-day activities. It concerns

the company's overuse accounting data gathered with the assistance of financial accounting and

cost analysis for policy implementation, preparation, monitoring and action taking. Management

accounting is the process of determining, tracking, reviewing, understanding and relating

financial information to supervisors for the purpose of achieving the objectives of an enterprise.

The area of management accounting takes on a very important role in companies in current

market climate as critical choices are made contributing to income maximization and value

formation. Companies choose to monitor quality research that goes well beyond the value-based

information given by conventional managerial accounting records from historical general ledger

structures. This report is consisting of absorption and activity based costing with their advantages

and disadvantages. Additionally, relevance of break even analysis in the 21st century companies

produces multiple products and single products.

PART A

Methods of costing

1. Absorption cost of each type of stove

Information given in question of Hoffman Ltd

Light weight Megarange

Production units 4500 500

Direct Material 3 cost per unit 10 cost per unit

Direct labour 6.30 per hours (9hours) 6.30 (7 hours)

16 hours per stove 15 hours per stove

Statement of absorption cost

Particular LWs MRs

Management accounting is providing financial details in this kind of manner as to

facilitate administrators in developing a company's strategy and day-to-day activities. It concerns

the company's overuse accounting data gathered with the assistance of financial accounting and

cost analysis for policy implementation, preparation, monitoring and action taking. Management

accounting is the process of determining, tracking, reviewing, understanding and relating

financial information to supervisors for the purpose of achieving the objectives of an enterprise.

The area of management accounting takes on a very important role in companies in current

market climate as critical choices are made contributing to income maximization and value

formation. Companies choose to monitor quality research that goes well beyond the value-based

information given by conventional managerial accounting records from historical general ledger

structures. This report is consisting of absorption and activity based costing with their advantages

and disadvantages. Additionally, relevance of break even analysis in the 21st century companies

produces multiple products and single products.

PART A

Methods of costing

1. Absorption cost of each type of stove

Information given in question of Hoffman Ltd

Light weight Megarange

Production units 4500 500

Direct Material 3 cost per unit 10 cost per unit

Direct labour 6.30 per hours (9hours) 6.30 (7 hours)

16 hours per stove 15 hours per stove

Statement of absorption cost

Particular LWs MRs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

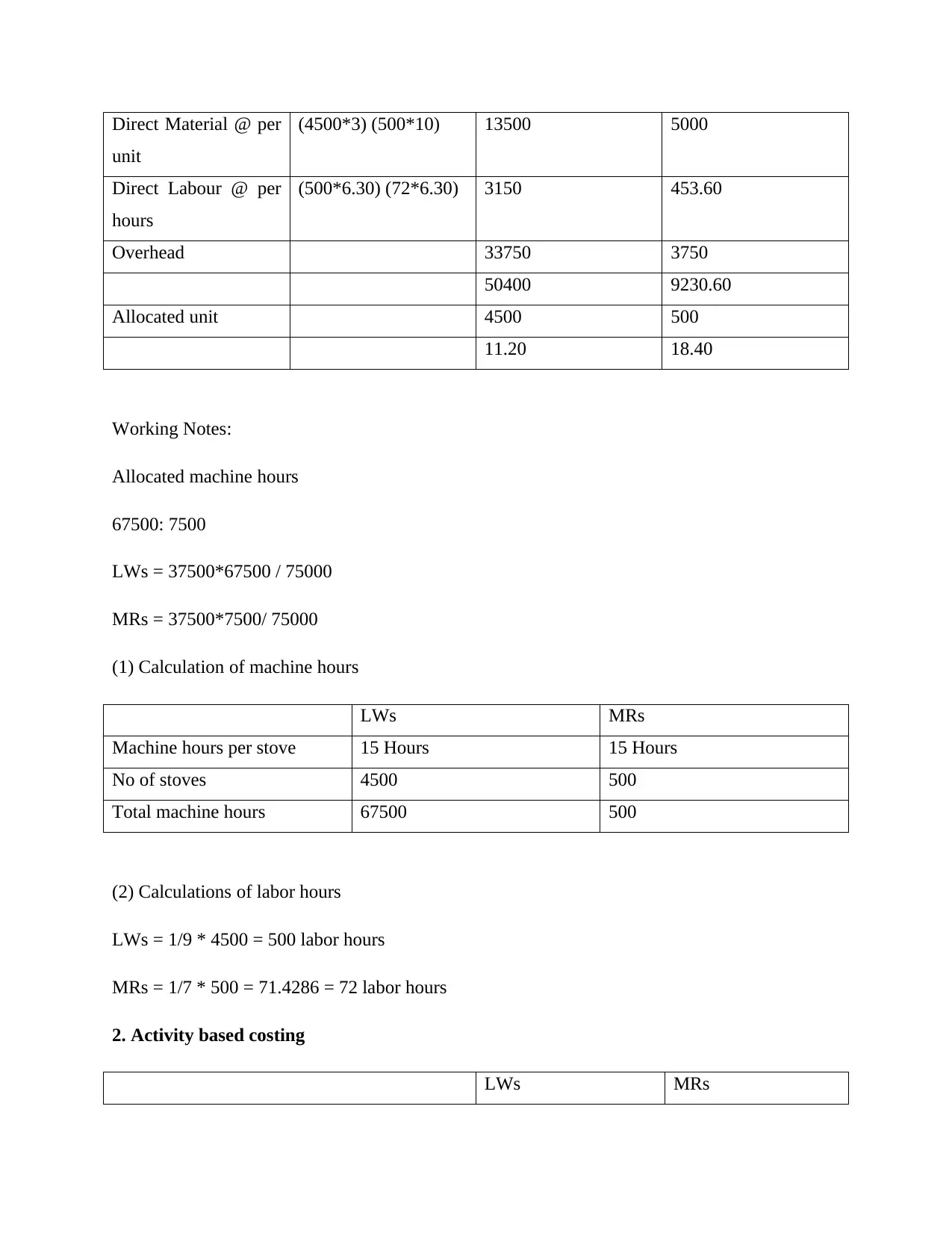

Direct Material @ per

unit

(4500*3) (500*10) 13500 5000

Direct Labour @ per

hours

(500*6.30) (72*6.30) 3150 453.60

Overhead 33750 3750

50400 9230.60

Allocated unit 4500 500

11.20 18.40

Working Notes:

Allocated machine hours

67500: 7500

LWs = 37500*67500 / 75000

MRs = 37500*7500/ 75000

(1) Calculation of machine hours

LWs MRs

Machine hours per stove 15 Hours 15 Hours

No of stoves 4500 500

Total machine hours 67500 500

(2) Calculations of labor hours

LWs = 1/9 * 4500 = 500 labor hours

MRs = 1/7 * 500 = 71.4286 = 72 labor hours

2. Activity based costing

LWs MRs

unit

(4500*3) (500*10) 13500 5000

Direct Labour @ per

hours

(500*6.30) (72*6.30) 3150 453.60

Overhead 33750 3750

50400 9230.60

Allocated unit 4500 500

11.20 18.40

Working Notes:

Allocated machine hours

67500: 7500

LWs = 37500*67500 / 75000

MRs = 37500*7500/ 75000

(1) Calculation of machine hours

LWs MRs

Machine hours per stove 15 Hours 15 Hours

No of stoves 4500 500

Total machine hours 67500 500

(2) Calculations of labor hours

LWs = 1/9 * 4500 = 500 labor hours

MRs = 1/7 * 500 = 71.4286 = 72 labor hours

2. Activity based costing

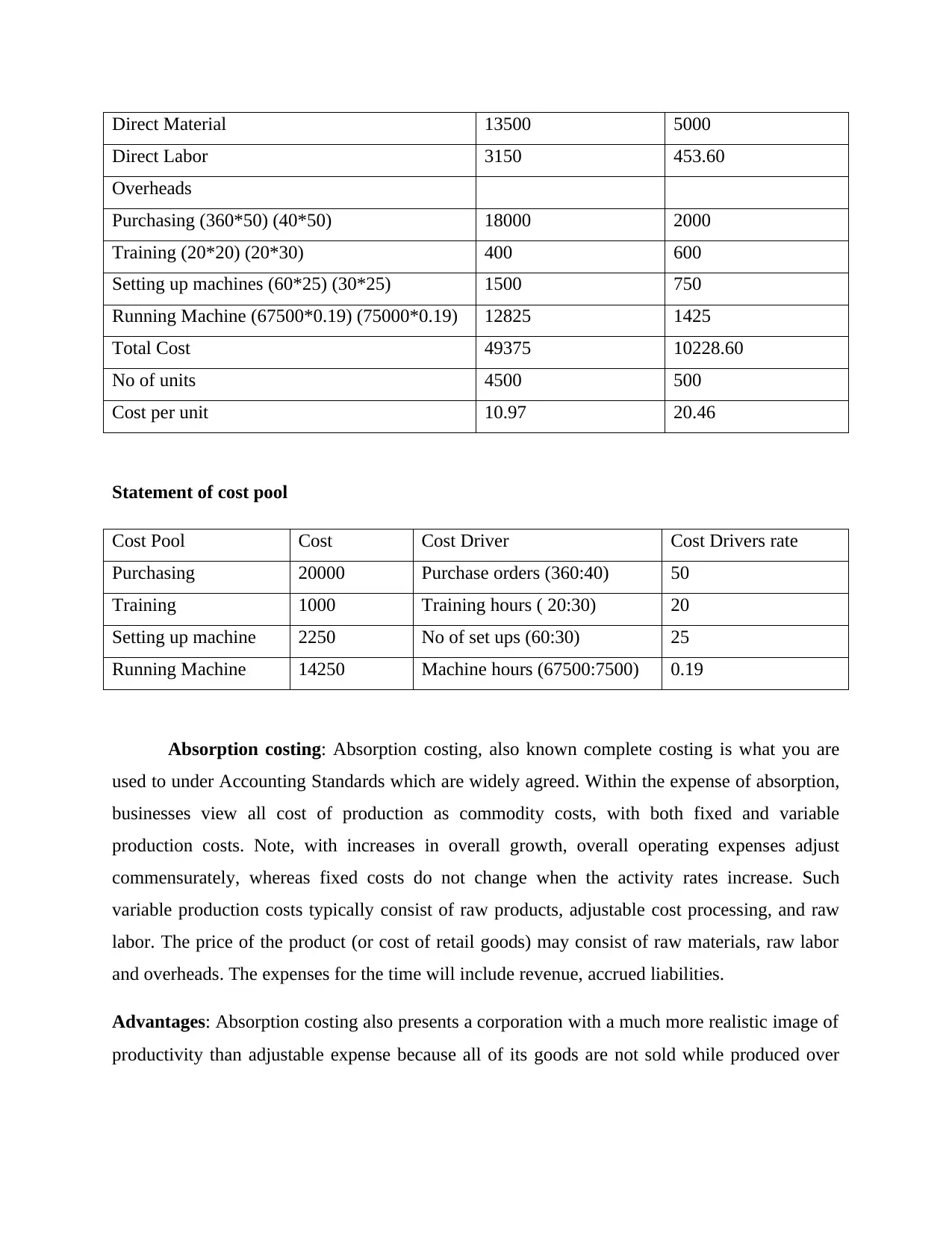

LWs MRs

Direct Material 13500 5000

Direct Labor 3150 453.60

Overheads

Purchasing (360*50) (40*50) 18000 2000

Training (20*20) (20*30) 400 600

Setting up machines (60*25) (30*25) 1500 750

Running Machine (67500*0.19) (75000*0.19) 12825 1425

Total Cost 49375 10228.60

No of units 4500 500

Cost per unit 10.97 20.46

Statement of cost pool

Cost Pool Cost Cost Driver Cost Drivers rate

Purchasing 20000 Purchase orders (360:40) 50

Training 1000 Training hours ( 20:30) 20

Setting up machine 2250 No of set ups (60:30) 25

Running Machine 14250 Machine hours (67500:7500) 0.19

Absorption costing: Absorption costing, also known complete costing is what you are

used to under Accounting Standards which are widely agreed. Within the expense of absorption,

businesses view all cost of production as commodity costs, with both fixed and variable

production costs. Note, with increases in overall growth, overall operating expenses adjust

commensurately, whereas fixed costs do not change when the activity rates increase. Such

variable production costs typically consist of raw products, adjustable cost processing, and raw

labor. The price of the product (or cost of retail goods) may consist of raw materials, raw labor

and overheads. The expenses for the time will include revenue, accrued liabilities.

Advantages: Absorption costing also presents a corporation with a much more realistic image of

productivity than adjustable expense because all of its goods are not sold while produced over

Direct Labor 3150 453.60

Overheads

Purchasing (360*50) (40*50) 18000 2000

Training (20*20) (20*30) 400 600

Setting up machines (60*25) (30*25) 1500 750

Running Machine (67500*0.19) (75000*0.19) 12825 1425

Total Cost 49375 10228.60

No of units 4500 500

Cost per unit 10.97 20.46

Statement of cost pool

Cost Pool Cost Cost Driver Cost Drivers rate

Purchasing 20000 Purchase orders (360:40) 50

Training 1000 Training hours ( 20:30) 20

Setting up machine 2250 No of set ups (60:30) 25

Running Machine 14250 Machine hours (67500:7500) 0.19

Absorption costing: Absorption costing, also known complete costing is what you are

used to under Accounting Standards which are widely agreed. Within the expense of absorption,

businesses view all cost of production as commodity costs, with both fixed and variable

production costs. Note, with increases in overall growth, overall operating expenses adjust

commensurately, whereas fixed costs do not change when the activity rates increase. Such

variable production costs typically consist of raw products, adjustable cost processing, and raw

labor. The price of the product (or cost of retail goods) may consist of raw materials, raw labor

and overheads. The expenses for the time will include revenue, accrued liabilities.

Advantages: Absorption costing also presents a corporation with a much more realistic image of

productivity than adjustable expense because all of its goods are not sold while produced over

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that same operating cycle. This can be particularly relevant for a corporation that is ramping up

manufacturing well ahead of a predicted big sales boost.

Disadvantages: When an organization wants to make comparisons the future productivity of

specific product routes, differential going to cost is more beneficial than uptake costs. By looking

purely at the input costs directly connected to manufacturing it is easier to determine the

discrepancies in income from manufacturing one ingredient over others.

Activity based costing: Activity-based costing (ABC) is a technique for distributing

operating costs more effectively by transferring them to the tasks. When activity costs are

allocated, the costs may be attributed to the items that have those practices. The program can be

used to minimize operating costs in a manageable way. ABC functions well in complicated

settings, where several devices and goods are available and convoluted systems are not difficult

to figure out. Moreover, in a simplified world where manufacturing cycles are condensed, it is of

less benefit.

Advantages: Costing focused on operation offers a more reliable way of measuring the product /

service, which results in much more reliable purchasing judgments. This improves awareness of

administrative costs and expense riders; and improves the exposure of costly and anti-value

enhancing operations, helping administrators to decrease or remove them. ABC allows for the

successful running expense task to find efficient ways to distribute and reduce overheads. This

also allows for greater measurement of product and consumer productivity. It promotes methods

for performance evaluation such as process improvement, and betting odds.

Disadvantages: ABC has varying rates of usefulness for various organizations because it can be

used more meaningfully by large industrial corporations than by smaller businesses. It is also

possible that businesses will take full advantage of ABC based on cost-plus marketing, because it

offers precise commodity costs. But certain businesses that make use of industry-based rates may

not prefer ABC. ABC's implementation also influences the degree of innovation and production

atmosphere existing in various companies. The key costs and drawbacks of an ABC program are

the required steps for its implementation. ABC systems allow administration to calculate the

costs of clusters of operation and to define and calculate cost generators to function as basis for

cost distribution.

manufacturing well ahead of a predicted big sales boost.

Disadvantages: When an organization wants to make comparisons the future productivity of

specific product routes, differential going to cost is more beneficial than uptake costs. By looking

purely at the input costs directly connected to manufacturing it is easier to determine the

discrepancies in income from manufacturing one ingredient over others.

Activity based costing: Activity-based costing (ABC) is a technique for distributing

operating costs more effectively by transferring them to the tasks. When activity costs are

allocated, the costs may be attributed to the items that have those practices. The program can be

used to minimize operating costs in a manageable way. ABC functions well in complicated

settings, where several devices and goods are available and convoluted systems are not difficult

to figure out. Moreover, in a simplified world where manufacturing cycles are condensed, it is of

less benefit.

Advantages: Costing focused on operation offers a more reliable way of measuring the product /

service, which results in much more reliable purchasing judgments. This improves awareness of

administrative costs and expense riders; and improves the exposure of costly and anti-value

enhancing operations, helping administrators to decrease or remove them. ABC allows for the

successful running expense task to find efficient ways to distribute and reduce overheads. This

also allows for greater measurement of product and consumer productivity. It promotes methods

for performance evaluation such as process improvement, and betting odds.

Disadvantages: ABC has varying rates of usefulness for various organizations because it can be

used more meaningfully by large industrial corporations than by smaller businesses. It is also

possible that businesses will take full advantage of ABC based on cost-plus marketing, because it

offers precise commodity costs. But certain businesses that make use of industry-based rates may

not prefer ABC. ABC's implementation also influences the degree of innovation and production

atmosphere existing in various companies. The key costs and drawbacks of an ABC program are

the required steps for its implementation. ABC systems allow administration to calculate the

costs of clusters of operation and to define and calculate cost generators to function as basis for

cost distribution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Break even analysis

A break-even evaluation is a mathematical tool that allows deciding how get success

existing corporation, or a new platform or commodity, would be at. In certain words, it is a

numerical measurement to measure the number of good or service a business can sell (especially

overhead costs) to support its expenses. Break-even is a scenario where they don't make money

or lose money, but it has absorbed all of the expenses. Analysis of break-even is important in

analyzing the relationship between the marginal cost, fixed cost and income. A business with

less fixed costs should usually have a higher break-even selling price. Following the equation

above, the company will decide how several items it generates to break-even. When the company

achieved this stage, all expenses (fixed costs) were collected in revenue or unit sales (Quinn and

Jackson, 2014). Any incremental product selling above this stage will lead to increased revenue

for the company. The increase in income should be by the quantity of unit expenditure profit, and

that is the quantity of extra income to support operational costs and benefit. It is calculable as

follows:

Unit contribution margin = Sales Price – Variable costs

Two types of Break even calculations – Units and Sales

Calculation of Break-even point in units: Break-even point is usually measured in

kilograms that offer the organization the amount of kilograms it has to generate to break-even. It

can be determined by multiplying participation profit by overall fixed expenses:

Break even unit (in points) = Fixed costs/Contribution margin per unit

Calculation of Break-even point in sales value: The break-even level was determined

in form of unit amount in the earlier example. Break-even point can also be measured in the

volume of sales). It can be achieved by multiplying the overall fixed costs of a business by ratio

of investment profit.

Contribution margin = Contribution margin per units/Sales per unit

Components of break even analysis

Break even analysis

A break-even evaluation is a mathematical tool that allows deciding how get success

existing corporation, or a new platform or commodity, would be at. In certain words, it is a

numerical measurement to measure the number of good or service a business can sell (especially

overhead costs) to support its expenses. Break-even is a scenario where they don't make money

or lose money, but it has absorbed all of the expenses. Analysis of break-even is important in

analyzing the relationship between the marginal cost, fixed cost and income. A business with

less fixed costs should usually have a higher break-even selling price. Following the equation

above, the company will decide how several items it generates to break-even. When the company

achieved this stage, all expenses (fixed costs) were collected in revenue or unit sales (Quinn and

Jackson, 2014). Any incremental product selling above this stage will lead to increased revenue

for the company. The increase in income should be by the quantity of unit expenditure profit, and

that is the quantity of extra income to support operational costs and benefit. It is calculable as

follows:

Unit contribution margin = Sales Price – Variable costs

Two types of Break even calculations – Units and Sales

Calculation of Break-even point in units: Break-even point is usually measured in

kilograms that offer the organization the amount of kilograms it has to generate to break-even. It

can be determined by multiplying participation profit by overall fixed expenses:

Break even unit (in points) = Fixed costs/Contribution margin per unit

Calculation of Break-even point in sales value: The break-even level was determined

in form of unit amount in the earlier example. Break-even point can also be measured in the

volume of sales). It can be achieved by multiplying the overall fixed costs of a business by ratio

of investment profit.

Contribution margin = Contribution margin per units/Sales per unit

Components of break even analysis

Fixed cost: Also called fixed costs, as the overhead cost. Such overhead costs arise after

the decision is made to start a commercial operation and these expenses are directly

linked to manufacturing costs, but not output quantities. Fixed costs comprise (but not

restricted to) inflation, taxation, wages, mortgage, value of maintenance, labor costs, cost

of electricity, etc. No cares how often selling certain expenses are static.

Variable cost: Variable costs are expenses which will significantly reduce in particular

terms of the amount of output. Such expenses comprise production prices, shipping costs,

transport costs as well as other costs directly connected to the manufacturing.

Revenues: Revenue is the income a company directly collects from its clients over a

given time for the sale of goods and facilities. Rebates and discounts are already being

modified, meaning that it is the accumulated profits through which specific expenses are

then excluded for the purpose of measuring capital gain. Total income can be determined

by calculating the value the amount of copies sold sell products or services at.

Contribution margin: It can measure the investment profit by deducting adjustable

expenditures from the profits. The investment margin demonstrates that much of the

business's income would contribute to paying the economies of scale. It can be

represented either per component, or for the entire sum. It can also manifest itself as a

proportion of gross profit.

Benefit of break even analysis

Catch missing expenses: When companies are planning a new venture, it's very likely

that could worry about a few expenditures. Furthermore, if they are carrying out a break-even

report, it will examine all financial obligations to assess break-even. Surely, this review reduces

the amount of uncertainties down the track.

Set revenues target: When the break-even assessment is done, they'll find out how much

require to legitimately making a return. This will allow to manager and their sales team set

further achievable revenue objectives.

Arrange fund for business: In any marketing plan, the evaluation is a vital aspect. When

some choose to finance company it is usually a necessity. They have to demonstrate that the

the decision is made to start a commercial operation and these expenses are directly

linked to manufacturing costs, but not output quantities. Fixed costs comprise (but not

restricted to) inflation, taxation, wages, mortgage, value of maintenance, labor costs, cost

of electricity, etc. No cares how often selling certain expenses are static.

Variable cost: Variable costs are expenses which will significantly reduce in particular

terms of the amount of output. Such expenses comprise production prices, shipping costs,

transport costs as well as other costs directly connected to the manufacturing.

Revenues: Revenue is the income a company directly collects from its clients over a

given time for the sale of goods and facilities. Rebates and discounts are already being

modified, meaning that it is the accumulated profits through which specific expenses are

then excluded for the purpose of measuring capital gain. Total income can be determined

by calculating the value the amount of copies sold sell products or services at.

Contribution margin: It can measure the investment profit by deducting adjustable

expenditures from the profits. The investment margin demonstrates that much of the

business's income would contribute to paying the economies of scale. It can be

represented either per component, or for the entire sum. It can also manifest itself as a

proportion of gross profit.

Benefit of break even analysis

Catch missing expenses: When companies are planning a new venture, it's very likely

that could worry about a few expenditures. Furthermore, if they are carrying out a break-even

report, it will examine all financial obligations to assess break-even. Surely, this review reduces

the amount of uncertainties down the track.

Set revenues target: When the break-even assessment is done, they'll find out how much

require to legitimately making a return. This will allow to manager and their sales team set

further achievable revenue objectives.

Arrange fund for business: In any marketing plan, the evaluation is a vital aspect. When

some choose to finance company it is usually a necessity. They have to demonstrate that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

proposal is feasible for enterprise to finance. In addition, if the research looks fine, it will be

confident sufficient to take on the pressure of multiple sources of funding.

Better pricing: The break-even point would lead to improved selling the goods. This

technique will be used widely to provide the best deal for a commodity that can get full benefit

without growing the current value (Kotas, 2014).

Application of Break even Analysis

Cost calculation: Break-even calculation is commonly used it to assess how many items

the client has to sell to prevent expenses. This measure allows the company to assess price of

product, variable costs and fixed costs. When those statistics are calculated, the measurement of

break-even stage in quantities or selling cost is relatively straightforward.

Budgeting and setting targets: Break-even maps and measurement is used for the cycle

of money management, because the company knows precisely how often products it is

appropriate to sell to break-even. In fact, the business is always mindful of the income that the

company would be able to gain at different times, which can conveniently be demonstrated on a

clear break-even map. This will help businesses set concrete, measurable objectives for

themselves (Osborne and Ball, 2010).

Motivation tool: Break-even analysis also actually motivates workers, specifically the

selling workers, as it clearly illustrates the earnings at different points of sales. The graph shows

specifically what effect additional revenues will have on the business's competitiveness.

Cover fixed cost: A break even analysis is supported to covering all the fixed costs.

Make smarter decision: Business people often undertake emotionally driven actions

about their companies. Excitement is essential, that is to say how feel, although it is not

sufficient. To be a good businessman all choices should be supported by evidence.

How break even analysis works

In 21st century many organizations are using break even analysis whether manufacturing

single product and multi products. There are discussing how to use this tool as per the

requirement such as:

confident sufficient to take on the pressure of multiple sources of funding.

Better pricing: The break-even point would lead to improved selling the goods. This

technique will be used widely to provide the best deal for a commodity that can get full benefit

without growing the current value (Kotas, 2014).

Application of Break even Analysis

Cost calculation: Break-even calculation is commonly used it to assess how many items

the client has to sell to prevent expenses. This measure allows the company to assess price of

product, variable costs and fixed costs. When those statistics are calculated, the measurement of

break-even stage in quantities or selling cost is relatively straightforward.

Budgeting and setting targets: Break-even maps and measurement is used for the cycle

of money management, because the company knows precisely how often products it is

appropriate to sell to break-even. In fact, the business is always mindful of the income that the

company would be able to gain at different times, which can conveniently be demonstrated on a

clear break-even map. This will help businesses set concrete, measurable objectives for

themselves (Osborne and Ball, 2010).

Motivation tool: Break-even analysis also actually motivates workers, specifically the

selling workers, as it clearly illustrates the earnings at different points of sales. The graph shows

specifically what effect additional revenues will have on the business's competitiveness.

Cover fixed cost: A break even analysis is supported to covering all the fixed costs.

Make smarter decision: Business people often undertake emotionally driven actions

about their companies. Excitement is essential, that is to say how feel, although it is not

sufficient. To be a good businessman all choices should be supported by evidence.

How break even analysis works

In 21st century many organizations are using break even analysis whether manufacturing

single product and multi products. There are discussing how to use this tool as per the

requirement such as:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break even analysis for Multi product

It is necessary to know the principle of a revenue mix in respect to execute a break-even

calculation for a business that sells numerous goods or offers additional resources. A market mix

reflects the binding affinities of the goods a business manufactures — that is, the ratio of overall

company money coming from Commodity A, Commodity B, Commodity C, etc. For business

owners and employees, sales mix is critical since they pursue a mix that enhances income, while

not all goods get the same profitability.

In the break-even stage evaluation study that approach of measuring break-even level of a

particular product business was addressed. It will clarify a multi-product business's method of

measuring break-even point. A non-product enterprise indicates an organization that offers two

or even more goods. A multiple brand business's computation break-even process is somewhat

more complex than just a particular product business's.

The break-even point in a multi-product setting ultimately depends on the combination of

goods offered. Furthermore, as the consumer composition varies, the break-even stage varies as

well. If market changes and consumers buy more minimal-margin goods, the break-even point

will then increase. Alternatively, the break-even level decreases if consumers buy further strong-

margin goods. However, while overall sales dollars remain intact, the break-even stage can vary

depending on the product combination (Maskell, Baggaley and Grasso, 2017).

A multi product organisation can apply this formula for breakeven point:

Break-even point = Total fixed expenses / Weighted average selling price – weighted average

variable expenses

As per the particular formula the weighted average selling price is worked defined as below:

(Sale price of commodity A * Sale percentage of Commodity A) + (Sale price of commodity B *

Sale percentage of Commodity B) + (Sale price of commodity C * Sale percentage of

Commodity C)...

In a corporation with double and sometimes more items to compute break-even point, they need

to consider the number of revenues of particular goods in the overall revenue mix. Such

It is necessary to know the principle of a revenue mix in respect to execute a break-even

calculation for a business that sells numerous goods or offers additional resources. A market mix

reflects the binding affinities of the goods a business manufactures — that is, the ratio of overall

company money coming from Commodity A, Commodity B, Commodity C, etc. For business

owners and employees, sales mix is critical since they pursue a mix that enhances income, while

not all goods get the same profitability.

In the break-even stage evaluation study that approach of measuring break-even level of a

particular product business was addressed. It will clarify a multi-product business's method of

measuring break-even point. A non-product enterprise indicates an organization that offers two

or even more goods. A multiple brand business's computation break-even process is somewhat

more complex than just a particular product business's.

The break-even point in a multi-product setting ultimately depends on the combination of

goods offered. Furthermore, as the consumer composition varies, the break-even stage varies as

well. If market changes and consumers buy more minimal-margin goods, the break-even point

will then increase. Alternatively, the break-even level decreases if consumers buy further strong-

margin goods. However, while overall sales dollars remain intact, the break-even stage can vary

depending on the product combination (Maskell, Baggaley and Grasso, 2017).

A multi product organisation can apply this formula for breakeven point:

Break-even point = Total fixed expenses / Weighted average selling price – weighted average

variable expenses

As per the particular formula the weighted average selling price is worked defined as below:

(Sale price of commodity A * Sale percentage of Commodity A) + (Sale price of commodity B *

Sale percentage of Commodity B) + (Sale price of commodity C * Sale percentage of

Commodity C)...

In a corporation with double and sometimes more items to compute break-even point, they need

to consider the number of revenues of particular goods in the overall revenue mix. Such

knowledge is used for estimating total weighted sale price and total average adjustable

expenditures.

The weighted average variable expenses are as adopts:

(Variable expenses of manufactured goods A * sales percentage of commodity A) + (Variable

expenses of manufactured goods B * sales percentage of commodity B) + (Variable expenses of

manufactured goods C * sales percentage of commodity C)…

They get weighted average investment profit each product once weighted average contingent

expenditures every item are removed from the weighted average sales wholesale price. So the

equation here can be described as obeys:

Break-even point = Total fixed expenses / weighted average contribution margin per unit

There are presenting an example of the multi product and sort out through formulas

A B C

Selling price 100 120 50

Variable cost per unit 60 90 40

Contribution margin per unit 40 30 10

Contribution margin ratio 40% 25% 20%

The company sells out about 5 units of C for each unit of A and 2 units of B for each unit of A.

Therefore, the sales mix is 1:2:5. The organisation consists in $120,000 total fixed costs:

BEP in units: Total fixed costs/ Weighted average CM per unit

= 120,000 / 18.75

= 64000 units

a. Computation of weighted average CM per unit:

∑(CM per unit x Unit sales mix ratio)

Product A ($40 x 1/8) $ 5.00

expenditures.

The weighted average variable expenses are as adopts:

(Variable expenses of manufactured goods A * sales percentage of commodity A) + (Variable

expenses of manufactured goods B * sales percentage of commodity B) + (Variable expenses of

manufactured goods C * sales percentage of commodity C)…

They get weighted average investment profit each product once weighted average contingent

expenditures every item are removed from the weighted average sales wholesale price. So the

equation here can be described as obeys:

Break-even point = Total fixed expenses / weighted average contribution margin per unit

There are presenting an example of the multi product and sort out through formulas

A B C

Selling price 100 120 50

Variable cost per unit 60 90 40

Contribution margin per unit 40 30 10

Contribution margin ratio 40% 25% 20%

The company sells out about 5 units of C for each unit of A and 2 units of B for each unit of A.

Therefore, the sales mix is 1:2:5. The organisation consists in $120,000 total fixed costs:

BEP in units: Total fixed costs/ Weighted average CM per unit

= 120,000 / 18.75

= 64000 units

a. Computation of weighted average CM per unit:

∑(CM per unit x Unit sales mix ratio)

Product A ($40 x 1/8) $ 5.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.