Management Accounting Report: Analyzing Financial Performance of EECL

VerifiedAdded on 2022/12/09

|16

|4607

|466

Report

AI Summary

This comprehensive management accounting report analyzes the financial practices of Eastern Engineering Co. Ltd (EECL), a medium-sized manufacturing organization. The report begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its role in internal decision-making. It then delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, detailing their benefits and drawbacks for EECL. The report further examines different types of management accounting reports such as budget reports, operating budgets, accounts receivable aging reports, job cost reports, inventory and manufacturing reports, and profit & loss statements. It includes a detailed analysis of marginal and absorption costing techniques with income statements for each, demonstrating their application in cost calculation. Furthermore, the report explores the significance of planning tools used in budgetary control, outlining their advantages and disadvantages. Finally, it discusses how management accounting can help organizations like EECL respond effectively to financial problems. Overall, the report provides a thorough overview of management accounting principles and their practical application in a business context.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

Management accounting system............................................................................................3

TASK 2......................................................................................................................................5

Management Accounting Reports (MAR).............................................................................5

TASK 3......................................................................................................................................8

Calculating cost using appropriate MA techniques...............................................................8

TASK 4....................................................................................................................................10

Different types of planning tools for budgetary control.......................................................10

TASK 5....................................................................................................................................12

Comparing the ways in which organization could use management accounting to respond

to financial problems............................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................3

TASK 1......................................................................................................................................3

Management accounting system............................................................................................3

TASK 2......................................................................................................................................5

Management Accounting Reports (MAR).............................................................................5

TASK 3......................................................................................................................................8

Calculating cost using appropriate MA techniques...............................................................8

TASK 4....................................................................................................................................10

Different types of planning tools for budgetary control.......................................................10

TASK 5....................................................................................................................................12

Comparing the ways in which organization could use management accounting to respond

to financial problems............................................................................................................12

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION

Management accounting (MA) accounts for the accounting system which involves the

practice of identifying, measuring, analysing and interpreting the end result along with

communication the outcome to the end users. This is different from the financial accounting

in the context that it is being utilized by the internal managerial team for undertaking n

various business decisions. The accounting team provides relevant information to the

managerial accounting team, which then carries out the in-depth analysis of the information

which helps in identifying the areas of weaknesses or loopholes so that corrective actions can

be undertaken on a timely basis. This report is based on the Eastern Engineering Co. Ltd

(EECL) which is a medium sized organization into the manufacturing industry. This report

provides an in-depth insight into the concept of management accounting along with the

different methods used for the MA reporting purpose. It also involves determining the usage

of various MA techniques in cost analysis, in addition to the pros and cons of planning tools

and how organizations are adapting different MA system in order to respond to the financial

problems they face.

TASK 1

Management accounting system

Management Accounting (MA) is procedure of analyzing, summarizing and

providing information regarding financial data in order to make strategic decisions (What is

management accounting? 2021). Eastern Engineering Company Ltd. will be benefited by

implementing management accounting procedure in business. Management accounting

system (MAS) is used to provide relevant information to so that proper operational decisions

can be taken. The following are the types of MAS which will aid business to accomplish its

goals in effective manner.

Cost Accounting System:

It is one of the crucial systems of management accounting which aids firm to

estimate the cost of product so that profitability can be determined. Eastern Engineering

Company Limited (EECL) would be benefited by using this particular method in its business

process. Following are the benefits and drawbacks of implementing it.

Benefits :

Estimation of cost can be exerted by EECL for getting deeper insights into

expenditures of firm

Management accounting (MA) accounts for the accounting system which involves the

practice of identifying, measuring, analysing and interpreting the end result along with

communication the outcome to the end users. This is different from the financial accounting

in the context that it is being utilized by the internal managerial team for undertaking n

various business decisions. The accounting team provides relevant information to the

managerial accounting team, which then carries out the in-depth analysis of the information

which helps in identifying the areas of weaknesses or loopholes so that corrective actions can

be undertaken on a timely basis. This report is based on the Eastern Engineering Co. Ltd

(EECL) which is a medium sized organization into the manufacturing industry. This report

provides an in-depth insight into the concept of management accounting along with the

different methods used for the MA reporting purpose. It also involves determining the usage

of various MA techniques in cost analysis, in addition to the pros and cons of planning tools

and how organizations are adapting different MA system in order to respond to the financial

problems they face.

TASK 1

Management accounting system

Management Accounting (MA) is procedure of analyzing, summarizing and

providing information regarding financial data in order to make strategic decisions (What is

management accounting? 2021). Eastern Engineering Company Ltd. will be benefited by

implementing management accounting procedure in business. Management accounting

system (MAS) is used to provide relevant information to so that proper operational decisions

can be taken. The following are the types of MAS which will aid business to accomplish its

goals in effective manner.

Cost Accounting System:

It is one of the crucial systems of management accounting which aids firm to

estimate the cost of product so that profitability can be determined. Eastern Engineering

Company Limited (EECL) would be benefited by using this particular method in its business

process. Following are the benefits and drawbacks of implementing it.

Benefits :

Estimation of cost can be exerted by EECL for getting deeper insights into

expenditures of firm

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency and measures can be increased by specified organization which will lead it

to identify the irrelevant expenditures

Price determinations would be possible through implementing this system. EECL can

control cost with help of cost accounting system.

Distinguishing between profitable and unprofitable activities can be done with help of

this system. Eastern Engineering Company Limited can get guidance in reducing the

expenses of unnecessary components of operational activity.

It is important to implement in organization due to its above mentioned benefits so

that EECL can derive various advantages to increase efficiency of working.

Inventory Management System (IMS)

This is related with planning, buying, monitoring, etc stock of company. The

purpose for executing this in Eastern Engineering Company Limited is to meet market forces

in effectual manner. It is one of the key determinants of success as assistance is provided in

cooperating with changing circumstances of industry (Krishnan and Pavithran, 2018). EECL

can increase its way of conducting operational practices by executing this management

accounting system. It is important to integrate with business activities to derive following

advantages of IMS:

Advantages Costs saving become possible for the Eastern Engineering Company Limited after

implementing this particular accounting system into its business procedure. It is considered to be significant for the purpose of avoiding excess stock will

ultimately reduce the storage cost and better planning for production can be exerted

(Swain, 2021). Increased profits is one of the essential character of IMS in turn better understanding

regarding inventory turnover can be obtained (Uyar, 2019). This leads EECL to move

towards right direction by evaluating the inventory turnover in effectual pattern. More organized Warehouse and customer experience can be attained with usage of

inventory management system in EECL.

Job Costing System (JCS)

JCS provide instructions regarding cost of each job or task established in

organization. It is important for EECL to establish the particular system in enterprise in

order to obtain clarity regarding each job’s cost and profitability (Drury, 2018). In

addition to this, unprofitable task can be eliminated for reducing expenses and increasing

to identify the irrelevant expenditures

Price determinations would be possible through implementing this system. EECL can

control cost with help of cost accounting system.

Distinguishing between profitable and unprofitable activities can be done with help of

this system. Eastern Engineering Company Limited can get guidance in reducing the

expenses of unnecessary components of operational activity.

It is important to implement in organization due to its above mentioned benefits so

that EECL can derive various advantages to increase efficiency of working.

Inventory Management System (IMS)

This is related with planning, buying, monitoring, etc stock of company. The

purpose for executing this in Eastern Engineering Company Limited is to meet market forces

in effectual manner. It is one of the key determinants of success as assistance is provided in

cooperating with changing circumstances of industry (Krishnan and Pavithran, 2018). EECL

can increase its way of conducting operational practices by executing this management

accounting system. It is important to integrate with business activities to derive following

advantages of IMS:

Advantages Costs saving become possible for the Eastern Engineering Company Limited after

implementing this particular accounting system into its business procedure. It is considered to be significant for the purpose of avoiding excess stock will

ultimately reduce the storage cost and better planning for production can be exerted

(Swain, 2021). Increased profits is one of the essential character of IMS in turn better understanding

regarding inventory turnover can be obtained (Uyar, 2019). This leads EECL to move

towards right direction by evaluating the inventory turnover in effectual pattern. More organized Warehouse and customer experience can be attained with usage of

inventory management system in EECL.

Job Costing System (JCS)

JCS provide instructions regarding cost of each job or task established in

organization. It is important for EECL to establish the particular system in enterprise in

order to obtain clarity regarding each job’s cost and profitability (Drury, 2018). In

addition to this, unprofitable task can be eliminated for reducing expenses and increasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit margins. For acquiring various benefits ECCL should give emphasis on following

factors:

Pros

Estimation of cost related to job at any stage can be done with help of JCS. EECL

can identify that prevailing task in business for accomplishing the business

objectives requires the specified task significantly or not.

Eastern Engineering Company Limited can determine the price of products by

analyzing JCS in operational activity. There are various reasons that help

company to accomplish its goals in effective way by using it.

Comparison of actual elements like profits, cost, etc with previous becomes

possible by implementing it. Cost control and evaluation can be exerted by EECL

for achieving desirable outcome.

Price Optimization System (POS)

Estimation of price according to market forces is done by this system of

management accounting (Helms, 2021). With changing customers preference and

taste willingness for paying also get modified which can be observed by Eastern

Engineering Company Limited through POS.

Benefits

It is essential for EECL take it into consideration for achieving the immediate

financial benefits. Concentration on different parts of markets for determining

appropriate pricing for products can be done by firm.

On the basis of available information quick decision can be taken by EECL as

it is considered to be important.

TASK 2

Management Accounting Reports (MAR)

It presents the financial position of organization for specified period of time. There

are several types of management accounting reports which are as mentioned below. It

is crucial for EECL to utilize these reports for gaining deeper insights into company’s

activities for comparing actual with standard.

Budget Report

This is one of the fundamental report used by organization to get details of

company’s performance. It is prepared by taking the historical information for

factors:

Pros

Estimation of cost related to job at any stage can be done with help of JCS. EECL

can identify that prevailing task in business for accomplishing the business

objectives requires the specified task significantly or not.

Eastern Engineering Company Limited can determine the price of products by

analyzing JCS in operational activity. There are various reasons that help

company to accomplish its goals in effective way by using it.

Comparison of actual elements like profits, cost, etc with previous becomes

possible by implementing it. Cost control and evaluation can be exerted by EECL

for achieving desirable outcome.

Price Optimization System (POS)

Estimation of price according to market forces is done by this system of

management accounting (Helms, 2021). With changing customers preference and

taste willingness for paying also get modified which can be observed by Eastern

Engineering Company Limited through POS.

Benefits

It is essential for EECL take it into consideration for achieving the immediate

financial benefits. Concentration on different parts of markets for determining

appropriate pricing for products can be done by firm.

On the basis of available information quick decision can be taken by EECL as

it is considered to be important.

TASK 2

Management Accounting Reports (MAR)

It presents the financial position of organization for specified period of time. There

are several types of management accounting reports which are as mentioned below. It

is crucial for EECL to utilize these reports for gaining deeper insights into company’s

activities for comparing actual with standard.

Budget Report

This is one of the fundamental report used by organization to get details of

company’s performance. It is prepared by taking the historical information for

creating the road map for future activities. Unforeseen circumstances can be identified

with help of this report.

Advantages

It is beneficial for Eastern Engineering Company Limited to prepare budget report for

having details regarding estimated cost for future course of action (Hlaciuc and

et.al.,2017).

Financial requirements can be fulfill by referring the budget so that urgent needs can

be attained in convenient manner. It is an indicator of actual financial performance so

that improvement measures can be identified.

EECL can compare its current performance with past for recognizing causing factors

for low outcomes.

An Operating Budget

It represents the expenditure and income generated from daily operational activities

of Eastern Engineering Company Limited. The firm should give emphasis on this

management accounting report for deriving several positive impact on performance of

company.

Merits

Financial ditch can be avoided by EECL as this provides guidance in planning for day

to day operations. It can be prepared for short, medium and long term fro getting

convenience (Saliy and et.al., 2021).

Building financial reserve is one of the significant role of an operating budget in turn

Eastern Engineering Company Limited can attain the reduce debt occurring situation.

Flexibility for carrying business operational practices can be obtained by executing

this management accounting report

From the analysis of its advantages it can be stated that it is important for Eastern

Engineering Company Limited to utilize operating budget.

Account Receivable aging Report

This is vital for organization to formulate mentioned report in order to evaluate its

credit providing policies. It provide assistance in identifying the duration of credit so

that defaulters can be assessed. In case of larger credit providing practices EECL can

evaluate lacking areas in debtor collection period policies. Eastern Engineering

Company Limited will receive following benefits by applying and using account

receivable aging report in its business:

with help of this report.

Advantages

It is beneficial for Eastern Engineering Company Limited to prepare budget report for

having details regarding estimated cost for future course of action (Hlaciuc and

et.al.,2017).

Financial requirements can be fulfill by referring the budget so that urgent needs can

be attained in convenient manner. It is an indicator of actual financial performance so

that improvement measures can be identified.

EECL can compare its current performance with past for recognizing causing factors

for low outcomes.

An Operating Budget

It represents the expenditure and income generated from daily operational activities

of Eastern Engineering Company Limited. The firm should give emphasis on this

management accounting report for deriving several positive impact on performance of

company.

Merits

Financial ditch can be avoided by EECL as this provides guidance in planning for day

to day operations. It can be prepared for short, medium and long term fro getting

convenience (Saliy and et.al., 2021).

Building financial reserve is one of the significant role of an operating budget in turn

Eastern Engineering Company Limited can attain the reduce debt occurring situation.

Flexibility for carrying business operational practices can be obtained by executing

this management accounting report

From the analysis of its advantages it can be stated that it is important for Eastern

Engineering Company Limited to utilize operating budget.

Account Receivable aging Report

This is vital for organization to formulate mentioned report in order to evaluate its

credit providing policies. It provide assistance in identifying the duration of credit so

that defaulters can be assessed. In case of larger credit providing practices EECL can

evaluate lacking areas in debtor collection period policies. Eastern Engineering

Company Limited will receive following benefits by applying and using account

receivable aging report in its business:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefits It is important for organization to give emphasis on account aging report for the

purpose of evaluating the credit collection efficiency. In addition to this, it will

provide opportunity for improving prevailing policies in turn improvement can be

conducted. Bad debts can be reduced by sending required reminders to customers for increasing

liquidity position of EECL.

Job Costing Report

There are numerous types of jobs established in business for fulfilling the

company’s predetermined objectives. The purpose of implementing this report in

EECL is available of information regarding expense and profit of specific task. It can

be determined at any stage of completion of task. In addition to this, Eastern

Engineering Company Limited will be benefited by using it

Advantages

It is easy to execute and gives understandable outcome which will provide

convenience to EECL in respect to making comparison between actual and estimated.

Detail analysis becomes possible for Eastern Engineering Company Limited for

making valuation for efficiency in accomplishing organizational goals.

Inventory and manufacturing report

Company prepares report on the basis of need but formulation of this report is

essential (May, Atkinson and Ferrer, 2017). It provides values of sale and inventory

along with indication of growth or declination, etc. There are various reasons that

Eastern Engineering Company Limited should take this report into consideration such

as:

Benefits

Accuracy of available inputs for production procedure can be done by EECL.

It reduces the risk of losing selling opportunities by having sufficient availability of

stock of Eastern Engineering Company Limited

Profit and loss statement

Firm’s revenue and expenditure for particular period of time can be known. EECL

will get benefit by preparing this report.

purpose of evaluating the credit collection efficiency. In addition to this, it will

provide opportunity for improving prevailing policies in turn improvement can be

conducted. Bad debts can be reduced by sending required reminders to customers for increasing

liquidity position of EECL.

Job Costing Report

There are numerous types of jobs established in business for fulfilling the

company’s predetermined objectives. The purpose of implementing this report in

EECL is available of information regarding expense and profit of specific task. It can

be determined at any stage of completion of task. In addition to this, Eastern

Engineering Company Limited will be benefited by using it

Advantages

It is easy to execute and gives understandable outcome which will provide

convenience to EECL in respect to making comparison between actual and estimated.

Detail analysis becomes possible for Eastern Engineering Company Limited for

making valuation for efficiency in accomplishing organizational goals.

Inventory and manufacturing report

Company prepares report on the basis of need but formulation of this report is

essential (May, Atkinson and Ferrer, 2017). It provides values of sale and inventory

along with indication of growth or declination, etc. There are various reasons that

Eastern Engineering Company Limited should take this report into consideration such

as:

Benefits

Accuracy of available inputs for production procedure can be done by EECL.

It reduces the risk of losing selling opportunities by having sufficient availability of

stock of Eastern Engineering Company Limited

Profit and loss statement

Firm’s revenue and expenditure for particular period of time can be known. EECL

will get benefit by preparing this report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage

Breakdown between revenues and expenditure provide fair estimation of financial

position of EECL.

Keeping things in balance can be done with help of this report.

TASK 3

Calculating cost using appropriate MA techniques

There are number of MA techniques which can be utilized by the organization for

the purpose of effectively meeting up with the business requirement pertaining to effectively

handling its costs. Some of the most widely used MA techniques are provided below:

Marginal costing

This technique assists in determining the marginal cost per unit along with its effect

over the profit of the company considering the sales volume. Under this, the variable cost

varies with the change in the sales units while on the other hand, the fixed cost remains

constant within a specific limit (MirbagheriRoodbari and Kordestani, 2020). From the total

sales revenue the marginal cost of production s deducted which results into getting the

amount of contribution. After which the fixed cost is subtracted from it for determining the

profitability. This technique is mainly utilized by the management for the purposeof

undertaking the decision for the business expansion as it helps in deriving the break-even

point at various production levels.

Absorption costing

This technique involves the incorporation of both the type of cost which is fixed and

variable while determining the cost of production. Under this, the fixed overhead in relation

to the production is also included while calculating the cost of product (Altin, Akgün and

Kasimoğlu, 2020). This technique is highly required by GAAP for the purposeof external

financial reporting.Under this, the fixed cost is allocated to the cost of the product

irrespective of the fact whether the product is sold or not.

Income statement under Absorption costing

Particulars January February

Sales (a) (9800 * 135)

132300

0 (11200*140) 1568000

Less: Cost of goods sold

Breakdown between revenues and expenditure provide fair estimation of financial

position of EECL.

Keeping things in balance can be done with help of this report.

TASK 3

Calculating cost using appropriate MA techniques

There are number of MA techniques which can be utilized by the organization for

the purpose of effectively meeting up with the business requirement pertaining to effectively

handling its costs. Some of the most widely used MA techniques are provided below:

Marginal costing

This technique assists in determining the marginal cost per unit along with its effect

over the profit of the company considering the sales volume. Under this, the variable cost

varies with the change in the sales units while on the other hand, the fixed cost remains

constant within a specific limit (MirbagheriRoodbari and Kordestani, 2020). From the total

sales revenue the marginal cost of production s deducted which results into getting the

amount of contribution. After which the fixed cost is subtracted from it for determining the

profitability. This technique is mainly utilized by the management for the purposeof

undertaking the decision for the business expansion as it helps in deriving the break-even

point at various production levels.

Absorption costing

This technique involves the incorporation of both the type of cost which is fixed and

variable while determining the cost of production. Under this, the fixed overhead in relation

to the production is also included while calculating the cost of product (Altin, Akgün and

Kasimoğlu, 2020). This technique is highly required by GAAP for the purposeof external

financial reporting.Under this, the fixed cost is allocated to the cost of the product

irrespective of the fact whether the product is sold or not.

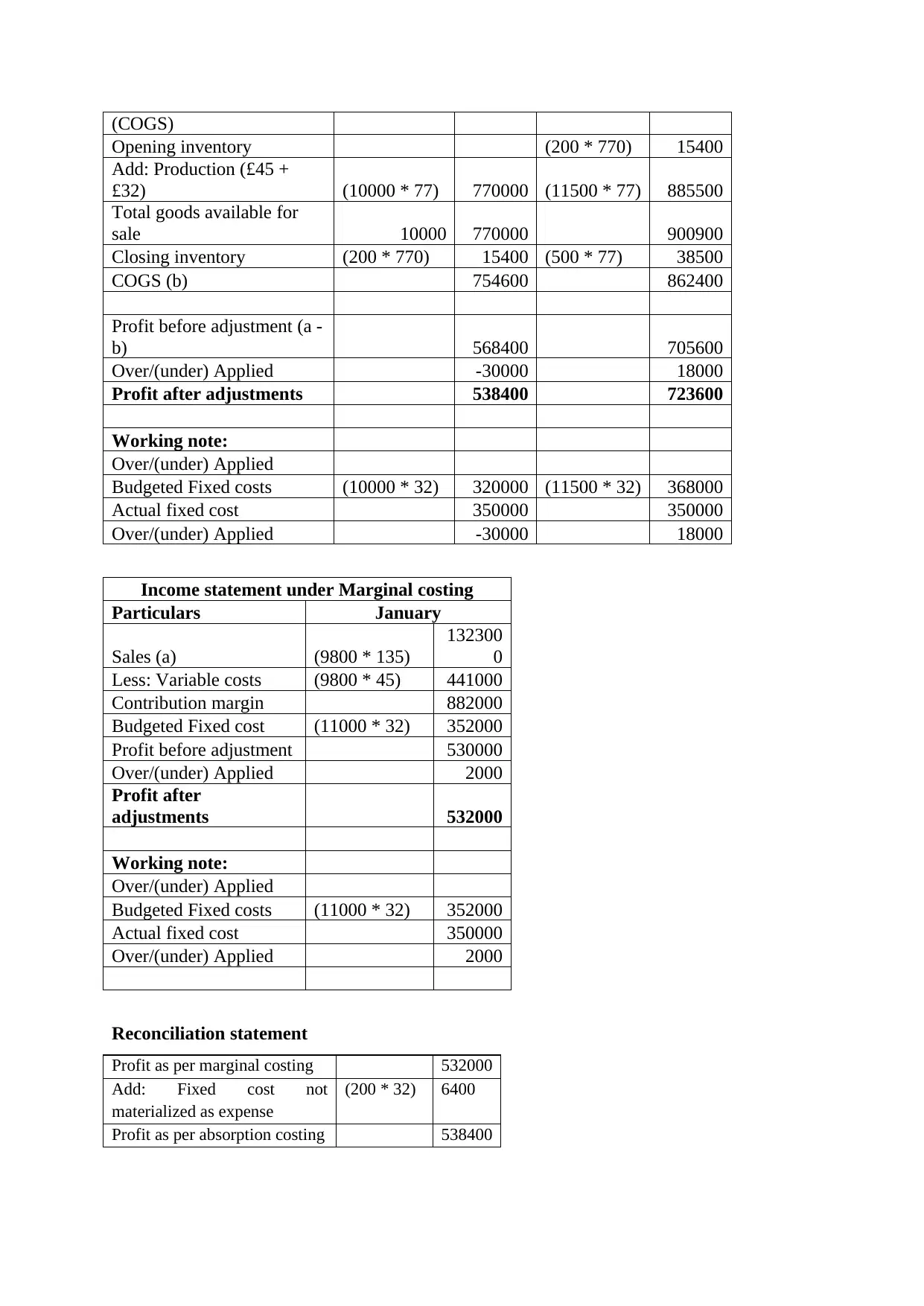

Income statement under Absorption costing

Particulars January February

Sales (a) (9800 * 135)

132300

0 (11200*140) 1568000

Less: Cost of goods sold

(COGS)

Opening inventory (200 * 770) 15400

Add: Production (£45 +

£32) (10000 * 77) 770000 (11500 * 77) 885500

Total goods available for

sale 10000 770000 900900

Closing inventory (200 * 770) 15400 (500 * 77) 38500

COGS (b) 754600 862400

Profit before adjustment (a -

b) 568400 705600

Over/(under) Applied -30000 18000

Profit after adjustments 538400 723600

Working note:

Over/(under) Applied

Budgeted Fixed costs (10000 * 32) 320000 (11500 * 32) 368000

Actual fixed cost 350000 350000

Over/(under) Applied -30000 18000

Income statement under Marginal costing

Particulars January

Sales (a) (9800 * 135)

132300

0

Less: Variable costs (9800 * 45) 441000

Contribution margin 882000

Budgeted Fixed cost (11000 * 32) 352000

Profit before adjustment 530000

Over/(under) Applied 2000

Profit after

adjustments 532000

Working note:

Over/(under) Applied

Budgeted Fixed costs (11000 * 32) 352000

Actual fixed cost 350000

Over/(under) Applied 2000

Reconciliation statement

Profit as per marginal costing 532000

Add: Fixed cost not

materialized as expense

(200 * 32) 6400

Profit as per absorption costing 538400

Opening inventory (200 * 770) 15400

Add: Production (£45 +

£32) (10000 * 77) 770000 (11500 * 77) 885500

Total goods available for

sale 10000 770000 900900

Closing inventory (200 * 770) 15400 (500 * 77) 38500

COGS (b) 754600 862400

Profit before adjustment (a -

b) 568400 705600

Over/(under) Applied -30000 18000

Profit after adjustments 538400 723600

Working note:

Over/(under) Applied

Budgeted Fixed costs (10000 * 32) 320000 (11500 * 32) 368000

Actual fixed cost 350000 350000

Over/(under) Applied -30000 18000

Income statement under Marginal costing

Particulars January

Sales (a) (9800 * 135)

132300

0

Less: Variable costs (9800 * 45) 441000

Contribution margin 882000

Budgeted Fixed cost (11000 * 32) 352000

Profit before adjustment 530000

Over/(under) Applied 2000

Profit after

adjustments 532000

Working note:

Over/(under) Applied

Budgeted Fixed costs (11000 * 32) 352000

Actual fixed cost 350000

Over/(under) Applied 2000

Reconciliation statement

Profit as per marginal costing 532000

Add: Fixed cost not

materialized as expense

(200 * 32) 6400

Profit as per absorption costing 538400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under the absorption costing technique, both fixed and variable cost is taken into

account in determining the cost of the product. In contrast to it, in marginal costing, only

variable cost is being taken while determining the production cost and the fixed cost is

classified as the period costs. Thus, the difference between the two is the fixed cost which is

not yet materialized as an expense in the month of January, which is, £6400.

It can be stated from the above analysis of the MA technique that the absorption is

better than marginal costing. Absorption costing technique supports the business association

in taking a better look at the expense totally and so that it will be able toformulate procedures

and strategies dependent on the cost adequately. It considers both fixed and variable expense

while computing cost of manufacturing (VatanParast, Tasaddi Kari and AhmadzadeLayegh,

2018). Additionally, it puts accentuation on cost of every unit and change in opening and

closinginventory influences the expense per unit. Marginal costing is valuable for the

organizations who have quite recently begun their business and needs to know the

contribution per unit along with the BEP analysisfor undertaking a better and effective

decisions.But the absorption costing is generally utilized and furthermore needed by GAAP

for financial reporting reason. In this manner, absorption costing technique is considered right

for the valuation of stock.

TASK 4

Different types of planning tools for budgetary control

There are various types of budgets which are being creating for the purpose of

exercising control over the business expenditure. Budget is usually the future planning and

measurement of the business needs.

Zero based budgeting

Under this method of budgeting, the process of creation of budget initiates from the

base level or the scratch. As the previous year budget is not used in this, it separately

incorporates each item with the cost. Every department provides with their requirement for

the specific period along with the proper justification (Beredugo, Azubike and Okon, 2019).

In this there are complete chances that the budget might go higher or lower in comparison to

the previous year.

Advantages:

It helps in eliminating unnecessary business and operational expenditure by

identifying obsolete process.

This budget help in efficient allocation of the financial resources.

account in determining the cost of the product. In contrast to it, in marginal costing, only

variable cost is being taken while determining the production cost and the fixed cost is

classified as the period costs. Thus, the difference between the two is the fixed cost which is

not yet materialized as an expense in the month of January, which is, £6400.

It can be stated from the above analysis of the MA technique that the absorption is

better than marginal costing. Absorption costing technique supports the business association

in taking a better look at the expense totally and so that it will be able toformulate procedures

and strategies dependent on the cost adequately. It considers both fixed and variable expense

while computing cost of manufacturing (VatanParast, Tasaddi Kari and AhmadzadeLayegh,

2018). Additionally, it puts accentuation on cost of every unit and change in opening and

closinginventory influences the expense per unit. Marginal costing is valuable for the

organizations who have quite recently begun their business and needs to know the

contribution per unit along with the BEP analysisfor undertaking a better and effective

decisions.But the absorption costing is generally utilized and furthermore needed by GAAP

for financial reporting reason. In this manner, absorption costing technique is considered right

for the valuation of stock.

TASK 4

Different types of planning tools for budgetary control

There are various types of budgets which are being creating for the purpose of

exercising control over the business expenditure. Budget is usually the future planning and

measurement of the business needs.

Zero based budgeting

Under this method of budgeting, the process of creation of budget initiates from the

base level or the scratch. As the previous year budget is not used in this, it separately

incorporates each item with the cost. Every department provides with their requirement for

the specific period along with the proper justification (Beredugo, Azubike and Okon, 2019).

In this there are complete chances that the budget might go higher or lower in comparison to

the previous year.

Advantages:

It helps in eliminating unnecessary business and operational expenditure by

identifying obsolete process.

This budget help in efficient allocation of the financial resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages:

This is built on the cost benefit analysis, the outcome of which can be accomplished

in long term.

There are chances of manipulation being done by managers of department for getting

more resources.

Incremental budget

It is based on the idea that newly prepared budget will give accurate road map for moving

towards success. Organization will receive several types of advantages and disadvantages

from this type of planning tool which are as follows:

Advantages

Reductions in internal rivals can be obtained by business with help of incremental budgeting

tool

Funds stability with consistent and operational efficiency can be derived by specified

organization which will lead firm to accomplish desirable position.

Disadvantages

It is expensive as promotes unnecessary spending in business.

This is unable to cope with changing circumstances due to external factors as well

discourages innovative in organization.

Activity based budgeting

Company uses this as planning tool as it provides opportunity of identifying, analyze and

recording the activities that incur cost to firm (Tenhunen, 2018). It is considered as

traditional form of planning tool which is makes adjustment in previous budget.

Advantages

Competitive edge can be derived by institution by taking this mode of planning tool into

consideration as eliminates bottleneck by removing unnecessary business practices.

Improves the relationship by making an Identity as single unit

Disadvantages

Being a short term procedure requires deep understanding of complex activity.

Large number of resources are consumed in this planning tool

Flexible Budgeting

It gets adjust with varying volume level of company’s operational activities. There are

various types of benefits and drawbacks that firm faces while using this mode of planning

This is built on the cost benefit analysis, the outcome of which can be accomplished

in long term.

There are chances of manipulation being done by managers of department for getting

more resources.

Incremental budget

It is based on the idea that newly prepared budget will give accurate road map for moving

towards success. Organization will receive several types of advantages and disadvantages

from this type of planning tool which are as follows:

Advantages

Reductions in internal rivals can be obtained by business with help of incremental budgeting

tool

Funds stability with consistent and operational efficiency can be derived by specified

organization which will lead firm to accomplish desirable position.

Disadvantages

It is expensive as promotes unnecessary spending in business.

This is unable to cope with changing circumstances due to external factors as well

discourages innovative in organization.

Activity based budgeting

Company uses this as planning tool as it provides opportunity of identifying, analyze and

recording the activities that incur cost to firm (Tenhunen, 2018). It is considered as

traditional form of planning tool which is makes adjustment in previous budget.

Advantages

Competitive edge can be derived by institution by taking this mode of planning tool into

consideration as eliminates bottleneck by removing unnecessary business practices.

Improves the relationship by making an Identity as single unit

Disadvantages

Being a short term procedure requires deep understanding of complex activity.

Large number of resources are consumed in this planning tool

Flexible Budgeting

It gets adjust with varying volume level of company’s operational activities. There are

various types of benefits and drawbacks that firm faces while using this mode of planning

tool. Flexibility while cooperating with changing circumstances can be achieved by flexible

budget.

Benefits

Cost variance can be analyzed by using flexible budget as inefficiencies can be identified by

management.

Better profit planning can be done by specified business which increases management

performance.

Drawbacks Under this method of budgeting there is requirement of skilled labor for proper implementing

of process. Forecast may not be accurate all time due to highly volatile nature of flexible budget.

Cash budget

It break downs the incoming and outgoing cash flow in business which give clear picture of

firm’s financial position.

Advantages

It coordinates all the activities by maximizing the profitability and gives details regarding

cash balance remaining after payment of expenses.

Segregation between receipts and payment become possible for evaluating financial policies

of company.

Disadvantages

It limits the spending power of company and ability of building credit profile.

TASK 5

Comparing the ways in which organization could use management accounting to respond to

financial problems

There are number of financial problems which are being faced by the businesses but

in order to identify the same, the company can make use of various performance

measurement tools which will help in attaining sustainable performance.A detailed

description is given below.

Benchmarking

budget.

Benefits

Cost variance can be analyzed by using flexible budget as inefficiencies can be identified by

management.

Better profit planning can be done by specified business which increases management

performance.

Drawbacks Under this method of budgeting there is requirement of skilled labor for proper implementing

of process. Forecast may not be accurate all time due to highly volatile nature of flexible budget.

Cash budget

It break downs the incoming and outgoing cash flow in business which give clear picture of

firm’s financial position.

Advantages

It coordinates all the activities by maximizing the profitability and gives details regarding

cash balance remaining after payment of expenses.

Segregation between receipts and payment become possible for evaluating financial policies

of company.

Disadvantages

It limits the spending power of company and ability of building credit profile.

TASK 5

Comparing the ways in which organization could use management accounting to respond to

financial problems

There are number of financial problems which are being faced by the businesses but

in order to identify the same, the company can make use of various performance

measurement tools which will help in attaining sustainable performance.A detailed

description is given below.

Benchmarking

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.