Management Accounting Report: Make or Buy Decision for FamaQ - XLG

VerifiedAdded on 2023/01/09

|11

|3061

|98

Report

AI Summary

This management accounting report analyzes the financial performance of XLG Company, a producer of cleaning products, focusing on variance analysis and make-or-buy decisions. Part A examines sales price and volume contribution variances, material price variances, and their role in assessing manager performance. It includes calculations and explanations of these variances. Part B evaluates the make-or-buy decision for FamaQ, a key material, considering costs and capacity. The report provides an introduction to management accounting, highlighting its importance in internal decision-making and performance evaluation. The report also includes a discussion of the advantages and disadvantages of using variance analysis to measure the performance of managers. The report concludes with a recommendation for the company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

i) Sales price variance and sales volume contribution variance..................................................1

ii) Material price planning variance and the material price operational variance.......................2

iii) Variance analysis for assessing the performance of managers..............................................3

PART B...........................................................................................................................................6

To evaluate make or buy decision for FamaQ.............................................................................6

CONCUSION..................................................................................................................................8

REFERENCES................................................................................................................................9

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

i) Sales price variance and sales volume contribution variance..................................................1

ii) Material price planning variance and the material price operational variance.......................2

iii) Variance analysis for assessing the performance of managers..............................................3

PART B...........................................................................................................................................6

To evaluate make or buy decision for FamaQ.............................................................................6

CONCUSION..................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUTION

Management accounting could be defined as process of identifying, analysing,

measuring, interpreting and communicating the information to the managers. MA focuses over

accounting aimed in informing the management about the operational metric. It includes

information related to the cost or product or services purchased by company. Budget often used

for quantifying decisions made in the operational planning. Performance reports are used by the

management for identifying the variances between budgeted and actual budgets. The major

difference between management and financial accounting is that FA is collection of the

accounting data for creating financial statement and MA is internal process used for accounting

the business transactions. Present report is based on the concepts of MA and XLG Company. It is

producer of cleaning products which is prepared using the material called FamaQ and it has

secured patent for the material. Company wants to study the variances and the merits and

demerits of using variances in analysing the performance of managers. It wants to analyse the

make or buy decision for the FamaQ as the imported materials is costing high to company.

PART A

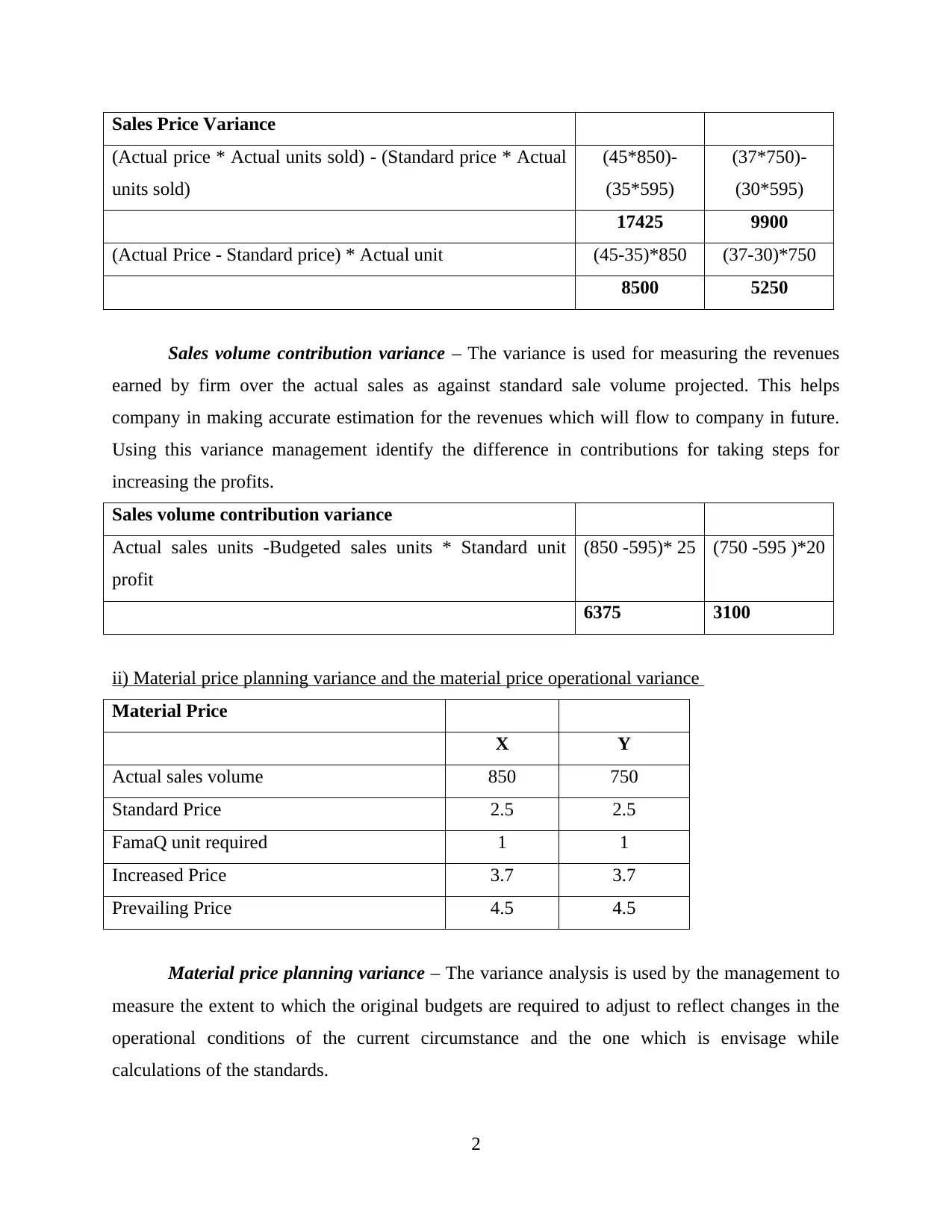

i) Sales price variance and sales volume contribution variance

Sales and Contribution

X Y

Total Sales 595 595

Actual sales volume 850 750

Standard Sales Price 35 30

Actual Sales price 45 37

Standard Margin 25 20

Sales Price Variance – This variance analysis is used for measuring changes in sales

revenues as the result of variations between the actual & standard sales price. Actual sales of the

products could differ from the budgeted sales because of various reasons such as increase in

demand of product. There are various factors that influence the sales like change in tastes or

preferences, prices, trend and such other factors (Chiu and et.al., 2018). The variance quantifies

the difference in sales that results from the difference in market and standard price.

1

Management accounting could be defined as process of identifying, analysing,

measuring, interpreting and communicating the information to the managers. MA focuses over

accounting aimed in informing the management about the operational metric. It includes

information related to the cost or product or services purchased by company. Budget often used

for quantifying decisions made in the operational planning. Performance reports are used by the

management for identifying the variances between budgeted and actual budgets. The major

difference between management and financial accounting is that FA is collection of the

accounting data for creating financial statement and MA is internal process used for accounting

the business transactions. Present report is based on the concepts of MA and XLG Company. It is

producer of cleaning products which is prepared using the material called FamaQ and it has

secured patent for the material. Company wants to study the variances and the merits and

demerits of using variances in analysing the performance of managers. It wants to analyse the

make or buy decision for the FamaQ as the imported materials is costing high to company.

PART A

i) Sales price variance and sales volume contribution variance

Sales and Contribution

X Y

Total Sales 595 595

Actual sales volume 850 750

Standard Sales Price 35 30

Actual Sales price 45 37

Standard Margin 25 20

Sales Price Variance – This variance analysis is used for measuring changes in sales

revenues as the result of variations between the actual & standard sales price. Actual sales of the

products could differ from the budgeted sales because of various reasons such as increase in

demand of product. There are various factors that influence the sales like change in tastes or

preferences, prices, trend and such other factors (Chiu and et.al., 2018). The variance quantifies

the difference in sales that results from the difference in market and standard price.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales Price Variance

(Actual price * Actual units sold) - (Standard price * Actual

units sold)

(45*850)-

(35*595)

(37*750)-

(30*595)

17425 9900

(Actual Price - Standard price) * Actual unit (45-35)*850 (37-30)*750

8500 5250

Sales volume contribution variance – The variance is used for measuring the revenues

earned by firm over the actual sales as against standard sale volume projected. This helps

company in making accurate estimation for the revenues which will flow to company in future.

Using this variance management identify the difference in contributions for taking steps for

increasing the profits.

Sales volume contribution variance

Actual sales units -Budgeted sales units * Standard unit

profit

(850 -595)* 25 (750 -595 )*20

6375 3100

ii) Material price planning variance and the material price operational variance

Material Price

X Y

Actual sales volume 850 750

Standard Price 2.5 2.5

FamaQ unit required 1 1

Increased Price 3.7 3.7

Prevailing Price 4.5 4.5

Material price planning variance – The variance analysis is used by the management to

measure the extent to which the original budgets are required to adjust to reflect changes in the

operational conditions of the current circumstance and the one which is envisage while

calculations of the standards.

2

(Actual price * Actual units sold) - (Standard price * Actual

units sold)

(45*850)-

(35*595)

(37*750)-

(30*595)

17425 9900

(Actual Price - Standard price) * Actual unit (45-35)*850 (37-30)*750

8500 5250

Sales volume contribution variance – The variance is used for measuring the revenues

earned by firm over the actual sales as against standard sale volume projected. This helps

company in making accurate estimation for the revenues which will flow to company in future.

Using this variance management identify the difference in contributions for taking steps for

increasing the profits.

Sales volume contribution variance

Actual sales units -Budgeted sales units * Standard unit

profit

(850 -595)* 25 (750 -595 )*20

6375 3100

ii) Material price planning variance and the material price operational variance

Material Price

X Y

Actual sales volume 850 750

Standard Price 2.5 2.5

FamaQ unit required 1 1

Increased Price 3.7 3.7

Prevailing Price 4.5 4.5

Material price planning variance – The variance analysis is used by the management to

measure the extent to which the original budgets are required to adjust to reflect changes in the

operational conditions of the current circumstance and the one which is envisage while

calculations of the standards.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

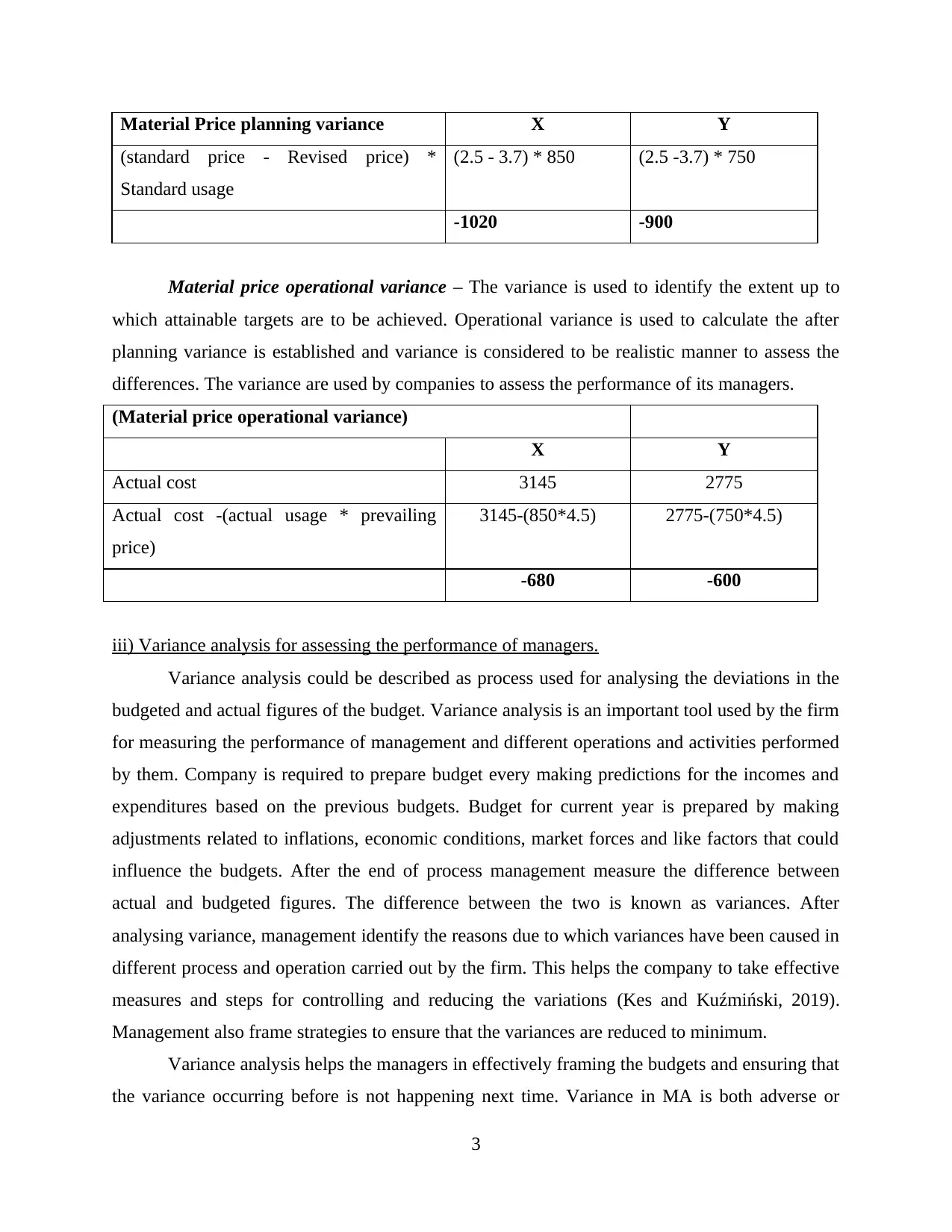

Material Price planning variance X Y

(standard price - Revised price) *

Standard usage

(2.5 - 3.7) * 850 (2.5 -3.7) * 750

-1020 -900

Material price operational variance – The variance is used to identify the extent up to

which attainable targets are to be achieved. Operational variance is used to calculate the after

planning variance is established and variance is considered to be realistic manner to assess the

differences. The variance are used by companies to assess the performance of its managers.

(Material price operational variance)

X Y

Actual cost 3145 2775

Actual cost -(actual usage * prevailing

price)

3145-(850*4.5) 2775-(750*4.5)

-680 -600

iii) Variance analysis for assessing the performance of managers.

Variance analysis could be described as process used for analysing the deviations in the

budgeted and actual figures of the budget. Variance analysis is an important tool used by the firm

for measuring the performance of management and different operations and activities performed

by them. Company is required to prepare budget every making predictions for the incomes and

expenditures based on the previous budgets. Budget for current year is prepared by making

adjustments related to inflations, economic conditions, market forces and like factors that could

influence the budgets. After the end of process management measure the difference between

actual and budgeted figures. The difference between the two is known as variances. After

analysing variance, management identify the reasons due to which variances have been caused in

different process and operation carried out by the firm. This helps the company to take effective

measures and steps for controlling and reducing the variations (Kes and Kuźmiński, 2019).

Management also frame strategies to ensure that the variances are reduced to minimum.

Variance analysis helps the managers in effectively framing the budgets and ensuring that

the variance occurring before is not happening next time. Variance in MA is both adverse or

3

(standard price - Revised price) *

Standard usage

(2.5 - 3.7) * 850 (2.5 -3.7) * 750

-1020 -900

Material price operational variance – The variance is used to identify the extent up to

which attainable targets are to be achieved. Operational variance is used to calculate the after

planning variance is established and variance is considered to be realistic manner to assess the

differences. The variance are used by companies to assess the performance of its managers.

(Material price operational variance)

X Y

Actual cost 3145 2775

Actual cost -(actual usage * prevailing

price)

3145-(850*4.5) 2775-(750*4.5)

-680 -600

iii) Variance analysis for assessing the performance of managers.

Variance analysis could be described as process used for analysing the deviations in the

budgeted and actual figures of the budget. Variance analysis is an important tool used by the firm

for measuring the performance of management and different operations and activities performed

by them. Company is required to prepare budget every making predictions for the incomes and

expenditures based on the previous budgets. Budget for current year is prepared by making

adjustments related to inflations, economic conditions, market forces and like factors that could

influence the budgets. After the end of process management measure the difference between

actual and budgeted figures. The difference between the two is known as variances. After

analysing variance, management identify the reasons due to which variances have been caused in

different process and operation carried out by the firm. This helps the company to take effective

measures and steps for controlling and reducing the variations (Kes and Kuźmiński, 2019).

Management also frame strategies to ensure that the variances are reduced to minimum.

Variance analysis helps the managers in effectively framing the budgets and ensuring that

the variance occurring before is not happening next time. Variance in MA is both adverse or

3

favourable. Both positive and negative variances also reflect negatively over the budgeting

effectiveness unless it is caused due to extreme events. Variance both adverse and favourable

reflects the inefficiency of management in framing accurate budgets or to manage the operations

with the available resources. It could be seen that the management using variance analysis

enhance the budgeting activities which it wishes to have less deviations from the budgeted

figures. Low deviations lead managers to make forward looking and detailed decisions. This

works as control mechanism for the management. Conducting variance analysis of the major

deviations of the essential items enables company to identify the issues and to help management

to look for possible methods about variations or differences that management can avoid.

Using variance managers ensures that effective utilisation of the resources is made in the

operations of processes to derive the maximum benefits out of them. Also it helps the

management in allocating the roles and responsibilities to staff at which they are good and

specialise. It also engages control mechanism in the departments to ensure optimum utilisation of

the resources is done. Managers are required to have strong control and governance over the

processes and operations for increasing the efficiency and productivity of the company.

Advantages and disadvantages of variance analysis to measure the performance of

managers

Variance analysis could be said as an simple and easy method or tool used by the

organisations. It is act of comparing actual with the standards for identifying variations.

Performance is judged on the basis of extent of variations between the actual and budgeted

figures. Standards are set by the top management by effectively analysing the present and past

experiences and trends. It is part of budgetary control where managers are required to apply their

professional skills and knowledge to prevent any harm and use budgeting process.

Performance of the managers is also measured using variance analysis and how effective

they are in managing the operations. There are managers that see favourable or the adverse

variance only as bad or good. Variance analysis is more deeper than just adverse or favourable.

Budgets are to be framed by properly evaluating the previous budgets and factors that could

influence current budgets and ensure that costly mistakes are not made and also assumptions are

taken on more accurate terms that does not leads the company to face losses.

In variance analysis responsibility accounting is the phrase that is applied for analysing

how managers can be held accountable for actions which are taken (Annamalai, 2018).

4

effectiveness unless it is caused due to extreme events. Variance both adverse and favourable

reflects the inefficiency of management in framing accurate budgets or to manage the operations

with the available resources. It could be seen that the management using variance analysis

enhance the budgeting activities which it wishes to have less deviations from the budgeted

figures. Low deviations lead managers to make forward looking and detailed decisions. This

works as control mechanism for the management. Conducting variance analysis of the major

deviations of the essential items enables company to identify the issues and to help management

to look for possible methods about variations or differences that management can avoid.

Using variance managers ensures that effective utilisation of the resources is made in the

operations of processes to derive the maximum benefits out of them. Also it helps the

management in allocating the roles and responsibilities to staff at which they are good and

specialise. It also engages control mechanism in the departments to ensure optimum utilisation of

the resources is done. Managers are required to have strong control and governance over the

processes and operations for increasing the efficiency and productivity of the company.

Advantages and disadvantages of variance analysis to measure the performance of

managers

Variance analysis could be said as an simple and easy method or tool used by the

organisations. It is act of comparing actual with the standards for identifying variations.

Performance is judged on the basis of extent of variations between the actual and budgeted

figures. Standards are set by the top management by effectively analysing the present and past

experiences and trends. It is part of budgetary control where managers are required to apply their

professional skills and knowledge to prevent any harm and use budgeting process.

Performance of the managers is also measured using variance analysis and how effective

they are in managing the operations. There are managers that see favourable or the adverse

variance only as bad or good. Variance analysis is more deeper than just adverse or favourable.

Budgets are to be framed by properly evaluating the previous budgets and factors that could

influence current budgets and ensure that costly mistakes are not made and also assumptions are

taken on more accurate terms that does not leads the company to face losses.

In variance analysis responsibility accounting is the phrase that is applied for analysing

how managers can be held accountable for actions which are taken (Annamalai, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Organisations are generally structured in segments and it is responsibility of the managers to

ensure that effective and efficient allocation of the resources is made in between different

departments or activities. Budgets and variance are carried out by the managers on departmental

basis that makes easy for management to be accountable for material variations from the planned

operations. Responsibility accounting ensures that worked is performed by the managers with

due care and diligence.

Significant and material variations attract the attentions of managers and executives over

the areas that are showing major differences between planned and actual activities. It requires

great care to be taken by management while using variance analysis as the management tools for

enhancing the performance of business.

Variance analysis with the number of advantages has also disadvantages. The method is

used for identifying the variations between actual and budgeted outcomes but does not provides

the ways how they could be reduced. Managers by only identifying the variance could not

achieve effectiveness as they do not provide about the main causes of difference. Investigation

and research is to be made for analysing the causes of variances based on which optimum

decisions could be taken. Without identifying the main reasons of variations performance of

managers could not be identified. Foremost reaction of managers can be for praising buyers that

are responsible to purchase the materials from the cheap sources than anticipated & reprimand

managers or departments using such materials. There may be chances that the variance are

caused due to controllable factors but are shown as uncontrollable by managers for reflecting

accurate performance.

Setting standards for price of materials based on previous prices where the prices in

actual have raised. Managers for achieving the budgeted targets could use material of inferior

quality that may lead to decline in demand of products which turns variance analysis to be

disadvantage for the company (Septria and Heryanto, 2019). Also the actual performance of

managers could not be measured as there are uncontrollable factors such as inflations, market

forces, etc, that makes it difficult to achieve the budgeted. It also takes considerable time to

identify and examine the effects of variances over for which measures are to be taken by the

management.

Performance of the managers could be measures by how effectively they have managed

the situations of change. Managers have the responsibility of achieving the desired goals and

5

ensure that effective and efficient allocation of the resources is made in between different

departments or activities. Budgets and variance are carried out by the managers on departmental

basis that makes easy for management to be accountable for material variations from the planned

operations. Responsibility accounting ensures that worked is performed by the managers with

due care and diligence.

Significant and material variations attract the attentions of managers and executives over

the areas that are showing major differences between planned and actual activities. It requires

great care to be taken by management while using variance analysis as the management tools for

enhancing the performance of business.

Variance analysis with the number of advantages has also disadvantages. The method is

used for identifying the variations between actual and budgeted outcomes but does not provides

the ways how they could be reduced. Managers by only identifying the variance could not

achieve effectiveness as they do not provide about the main causes of difference. Investigation

and research is to be made for analysing the causes of variances based on which optimum

decisions could be taken. Without identifying the main reasons of variations performance of

managers could not be identified. Foremost reaction of managers can be for praising buyers that

are responsible to purchase the materials from the cheap sources than anticipated & reprimand

managers or departments using such materials. There may be chances that the variance are

caused due to controllable factors but are shown as uncontrollable by managers for reflecting

accurate performance.

Setting standards for price of materials based on previous prices where the prices in

actual have raised. Managers for achieving the budgeted targets could use material of inferior

quality that may lead to decline in demand of products which turns variance analysis to be

disadvantage for the company (Septria and Heryanto, 2019). Also the actual performance of

managers could not be measured as there are uncontrollable factors such as inflations, market

forces, etc, that makes it difficult to achieve the budgeted. It also takes considerable time to

identify and examine the effects of variances over for which measures are to be taken by the

management.

Performance of the managers could be measures by how effectively they have managed

the situations of change. Managers have the responsibility of achieving the desired goals and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

targets by effectively utilising the resources and ensuring that quality material is used for the

production of goods and services.

PART B

To evaluate make or buy decision for FamaQ

It is one of the most important aspect to decide whether to make in-house or to purchase

from the outside buyers. It is an important analysis for the company as it involves significant

amount of money and time of company decided to make the product in-house. A company has to

effectively evaluate the make or buy decision before any steps are taken. It involves evaluating

which will be more beneficial for the company to make or to buy from third part. Outcomes of

the decision should maximise long term financial outcomes for company. There are number of

factors that are required to be considered by XLG before making the decisions are :

Cost – Company is required to analyse the alternative that causes lowest out of pocket

expenses. it is also required to add the fixed cost when adding the internal costs that is

considered incorrect (Serrano, Ramírez and Gascó, 2018). Firms are only required to include the

direct costs in compilation of internal costs for manufacturing the FamaQ in house. Cost quoted

by the supplier is 3.7 where the in house production will cost only 3 for the unit. Though cost of

making is lower but other factors are also required to be analysed.

Capacity – XLG has to analyse the capacity of company to produce or manufacture the

product in-house. Supplier capacity is also analysed for meeting the demands of company is

sufficient and also in timely manner. Company is proposed to have increased demand by 45%

due to which it may not be able to meet the demand from in house production. The suppliers are

large manufacturers that could meet the demand of company to significant extent.

Expertise – Company is also required to analyse the expert knowledge and experience in

manufacturing the products. Manufacturing products apart from their main stream could make

the company to suffer issues or problems. Manufacturing product will also divert the focus of

company from its main products to the new material as it is not having experience in the

producing the materials (Borg and et.al., 2019). Over this it is more beneficial for the company to

buy it from the third party as losses if suffered in products are significantly high in comparison

with the increased cost.

6

production of goods and services.

PART B

To evaluate make or buy decision for FamaQ

It is one of the most important aspect to decide whether to make in-house or to purchase

from the outside buyers. It is an important analysis for the company as it involves significant

amount of money and time of company decided to make the product in-house. A company has to

effectively evaluate the make or buy decision before any steps are taken. It involves evaluating

which will be more beneficial for the company to make or to buy from third part. Outcomes of

the decision should maximise long term financial outcomes for company. There are number of

factors that are required to be considered by XLG before making the decisions are :

Cost – Company is required to analyse the alternative that causes lowest out of pocket

expenses. it is also required to add the fixed cost when adding the internal costs that is

considered incorrect (Serrano, Ramírez and Gascó, 2018). Firms are only required to include the

direct costs in compilation of internal costs for manufacturing the FamaQ in house. Cost quoted

by the supplier is 3.7 where the in house production will cost only 3 for the unit. Though cost of

making is lower but other factors are also required to be analysed.

Capacity – XLG has to analyse the capacity of company to produce or manufacture the

product in-house. Supplier capacity is also analysed for meeting the demands of company is

sufficient and also in timely manner. Company is proposed to have increased demand by 45%

due to which it may not be able to meet the demand from in house production. The suppliers are

large manufacturers that could meet the demand of company to significant extent.

Expertise – Company is also required to analyse the expert knowledge and experience in

manufacturing the products. Manufacturing products apart from their main stream could make

the company to suffer issues or problems. Manufacturing product will also divert the focus of

company from its main products to the new material as it is not having experience in the

producing the materials (Borg and et.al., 2019). Over this it is more beneficial for the company to

buy it from the third party as losses if suffered in products are significantly high in comparison

with the increased cost.

6

Funds – Only deciding to manufacture product in-house is not enough even if it has the

capacity and the expertise of funds required for manufacturing are not enough. Manufacturing in

house requires investments of plant, machinery and equipments. It will also be required to

purchase raw material, incur labour and overhead costs. It has to analyse whether the material

produced could be sold alone in the market. It has to identify whether it is able to arrange for the

required funds to start the in house manufacturing of materials. XLG will be required to raise

funds from the market to establish the manufacturing unit for the materials which will take

considerable time. Also it involves risks and returns where buying it from the third party will not

require company to consider the risks.

Bottlenecks – It has to analyse whether producing in-house will be easing the burden of

bottleneck operations of company. If bottleneck operations are reduced in buying from third

party company should go for purchasing from outside rather than making in house.

Shipping Options – Supplier may provide the company with facility to store goods on its

own and ship the material to company on demand. Carrying cost of the products are to be

considered by the company as it may have to incur high storage cost for keeping the products

manufactured. The material purchased from outside will also require company to incur carrying

cost as the materials are purchased from abroad and it takes considerable time which is 14 days

to reach company premises (Hillebrand and Pishchulov, 2016). Carrying cost is lower in in-

house production and higher in purchasing from outside as imported and company is required to

store the product for future needs by maintain safety stocks.

Strategic importance – Importance of the product to corporate strategy of the company play

major role in decision making. It is beneficial if it is important, to manufacture the material for

maintain complete control over the product. Option is adopted if company possess proprietary

production facility which it will not be required to share with suppliers.

From the above analysis it could be evaluated that cost of manufacturing in house will cost 3

where purchase from outside cost 3.7. Also company is not having knowledge and the required

funds to manufacture the products. It will be more beneficial for the company to import the

FamaQ as increase in prices is due to pandemic which may by decreased after the virus and

company will focus over its main stream of cleaning product X & Y.

7

capacity and the expertise of funds required for manufacturing are not enough. Manufacturing in

house requires investments of plant, machinery and equipments. It will also be required to

purchase raw material, incur labour and overhead costs. It has to analyse whether the material

produced could be sold alone in the market. It has to identify whether it is able to arrange for the

required funds to start the in house manufacturing of materials. XLG will be required to raise

funds from the market to establish the manufacturing unit for the materials which will take

considerable time. Also it involves risks and returns where buying it from the third party will not

require company to consider the risks.

Bottlenecks – It has to analyse whether producing in-house will be easing the burden of

bottleneck operations of company. If bottleneck operations are reduced in buying from third

party company should go for purchasing from outside rather than making in house.

Shipping Options – Supplier may provide the company with facility to store goods on its

own and ship the material to company on demand. Carrying cost of the products are to be

considered by the company as it may have to incur high storage cost for keeping the products

manufactured. The material purchased from outside will also require company to incur carrying

cost as the materials are purchased from abroad and it takes considerable time which is 14 days

to reach company premises (Hillebrand and Pishchulov, 2016). Carrying cost is lower in in-

house production and higher in purchasing from outside as imported and company is required to

store the product for future needs by maintain safety stocks.

Strategic importance – Importance of the product to corporate strategy of the company play

major role in decision making. It is beneficial if it is important, to manufacture the material for

maintain complete control over the product. Option is adopted if company possess proprietary

production facility which it will not be required to share with suppliers.

From the above analysis it could be evaluated that cost of manufacturing in house will cost 3

where purchase from outside cost 3.7. Also company is not having knowledge and the required

funds to manufacture the products. It will be more beneficial for the company to import the

FamaQ as increase in prices is due to pandemic which may by decreased after the virus and

company will focus over its main stream of cleaning product X & Y.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCUSION

It could be summarised from the above report that management accounting plays an

important role in the success of the organisation. Variance analysis helps company in improving

the existing operations of the business by framing cost effective strategies. It also makes

effective allocation of the resources among different departments for optimum utilisation and

achieving the targeted goals and objectives.

8

It could be summarised from the above report that management accounting plays an

important role in the success of the organisation. Variance analysis helps company in improving

the existing operations of the business by framing cost effective strategies. It also makes

effective allocation of the resources among different departments for optimum utilisation and

achieving the targeted goals and objectives.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chiu, C.H. and et.al., 2018. Optimal advertising budget allocation in luxury fashion markets with

social influences: a mean‐variance analysis. Production and Operations

Management.27(8).pp.1611-1629.

Kes, Z. and Kuźmiński, Ł., 2019. Application of extreme value analysis in the assessment of

budget variance risk. Econometrics.23(2). pp.80-98.

Septria, D. and Heryanto, H., 2019. Performance Capability Analysis and Regional Budget

Evaluation in Implementing Regional Autonomy in Dharmasraya District. Archives of

Business Research.7(7). pp.180-187.

Annamalai, H., 2018. Moist static energy and its variance budget diagnostics for ENSO-related

Precipitation anomalies along the Equatorial Pacific in Climate Models. AGUFM, 2018,

pp.A12F-06.

Serrano, R.M., Ramírez, M.R.G. and Gascó, J.L.G., 2018. Should we make or buy? An update

and review. European Research on Management and Business Economics.24(3). pp.137-

148.

Borg, M. and et.al., 2019. Selecting component sourcing options: a survey of software

engineering’s broader make-or-buy decisions. Information and Software Technology. 112.

pp.18-34.

Hillebrand, B. and Pishchulov, G., 2016. Integrated make-or-buy and facility layout problem

with multiple products. In Logistics Management (pp. 121-132). Springer, Cham.

9

Books and Journals

Chiu, C.H. and et.al., 2018. Optimal advertising budget allocation in luxury fashion markets with

social influences: a mean‐variance analysis. Production and Operations

Management.27(8).pp.1611-1629.

Kes, Z. and Kuźmiński, Ł., 2019. Application of extreme value analysis in the assessment of

budget variance risk. Econometrics.23(2). pp.80-98.

Septria, D. and Heryanto, H., 2019. Performance Capability Analysis and Regional Budget

Evaluation in Implementing Regional Autonomy in Dharmasraya District. Archives of

Business Research.7(7). pp.180-187.

Annamalai, H., 2018. Moist static energy and its variance budget diagnostics for ENSO-related

Precipitation anomalies along the Equatorial Pacific in Climate Models. AGUFM, 2018,

pp.A12F-06.

Serrano, R.M., Ramírez, M.R.G. and Gascó, J.L.G., 2018. Should we make or buy? An update

and review. European Research on Management and Business Economics.24(3). pp.137-

148.

Borg, M. and et.al., 2019. Selecting component sourcing options: a survey of software

engineering’s broader make-or-buy decisions. Information and Software Technology. 112.

pp.18-34.

Hillebrand, B. and Pishchulov, G., 2016. Integrated make-or-buy and facility layout problem

with multiple products. In Logistics Management (pp. 121-132). Springer, Cham.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.