Management Accounting Systems, Costing, and Budgeting Analysis

VerifiedAdded on 2022/12/28

|17

|2907

|88

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within an organization, using Marshals Ltd. as a case study. It begins with an introduction to management accounting, detailing its role in decision-making, planning, and control. The report then explores various management accounting systems, including cost accounting, inventory management, and price optimization systems. It delves into management accounting reporting methods, such as budgetary, cost, and performance reports. Furthermore, the report examines costing methods, comparing marginal and absorption costing through income statements. It also analyzes different types of planning tools used for budgetary control, discussing the advantages and disadvantages of cash flow, flexible, variance analysis, and operational budgets. Finally, the report addresses how organizations adapt management accounting systems to solve financial problems, emphasizing the identification of core competencies. This report serves as a valuable resource for understanding the practical applications of management accounting principles.

Management

Accounting System

Accounting System

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting and types of management accounting systems along with their

requirements...........................................................................................................................3

P2: Management accounting reporting and its methods.........................................................4

TASK 2............................................................................................................................................5

P3: Calculation of costs using marginal and absorption costs...............................................5

TASK 3............................................................................................................................................6

P4: The advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................6

TASK 4............................................................................................................................................8

P5: Adaptation of management accounting systems by the organisations to face and solve

financial problems..................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting and types of management accounting systems along with their

requirements...........................................................................................................................3

P2: Management accounting reporting and its methods.........................................................4

TASK 2............................................................................................................................................5

P3: Calculation of costs using marginal and absorption costs...............................................5

TASK 3............................................................................................................................................6

P4: The advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................6

TASK 4............................................................................................................................................8

P5: Adaptation of management accounting systems by the organisations to face and solve

financial problems..................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

This report will put light on the basics of management accounting. Management

accounting helps the business or any organisation to analyse data from financial information

provided by financial accounting (Abdusalomova, 2019). Management accounting is the

procedure of identifying analysing, interpreting and communicating the financial information

which helps the business to achieve its goals. Management accounting with the help of financial

information helps in planning decisions, and also keeps a check and control on the finance within

the organisation. In this report management accounting is further explained with practicals and a

case study of Marshals Ltd.

Marshals Ltd is the UK's leading supplier of superior natural stone and concrete

landscaping products. It was founded in the late 1880s. Marshals was the first company to label

its entire range and was the first in the landscaping industry to work with the Carbon Trust’s

labelling scheme.

TASK 1

P1: Management accounting and types of management accounting systems along with their

requirements

Management accounting provides information to the management to assist them in the

process of decision making, planning and controlling and performance measurement.

Management accounting will enable Marshall Ltd. to get organisational reports and these reports

will help it to make necessary changes and take required decisions in the organisation itself and

the management. Management accounting provides the management with the information that

they need to plan and control the operations of the business or organisation.

Management accounting helps the management to form reports and analyse the financial

information which further helps the organisation to carry out its operations effectively and

efficiently and make better decisions by considering all the alternatives.

There are various Management Accounting Systems, some of them are:

Cost Accounting System: It is one of the major management accounting system

which consists of various accounting techniques which helps the business to

assess cost of specific tasks and projects. With the help of this assessment the

management will be able to compare the profits with costs and take necessary

This report will put light on the basics of management accounting. Management

accounting helps the business or any organisation to analyse data from financial information

provided by financial accounting (Abdusalomova, 2019). Management accounting is the

procedure of identifying analysing, interpreting and communicating the financial information

which helps the business to achieve its goals. Management accounting with the help of financial

information helps in planning decisions, and also keeps a check and control on the finance within

the organisation. In this report management accounting is further explained with practicals and a

case study of Marshals Ltd.

Marshals Ltd is the UK's leading supplier of superior natural stone and concrete

landscaping products. It was founded in the late 1880s. Marshals was the first company to label

its entire range and was the first in the landscaping industry to work with the Carbon Trust’s

labelling scheme.

TASK 1

P1: Management accounting and types of management accounting systems along with their

requirements

Management accounting provides information to the management to assist them in the

process of decision making, planning and controlling and performance measurement.

Management accounting will enable Marshall Ltd. to get organisational reports and these reports

will help it to make necessary changes and take required decisions in the organisation itself and

the management. Management accounting provides the management with the information that

they need to plan and control the operations of the business or organisation.

Management accounting helps the management to form reports and analyse the financial

information which further helps the organisation to carry out its operations effectively and

efficiently and make better decisions by considering all the alternatives.

There are various Management Accounting Systems, some of them are:

Cost Accounting System: It is one of the major management accounting system

which consists of various accounting techniques which helps the business to

assess cost of specific tasks and projects. With the help of this assessment the

management will be able to compare the profits with costs and take necessary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions and plan to cover the shortfall. In context to Marshal Ltd., the company

uses Cost Accounting System with which they are able to manage all their

relevant cost like that of raw material, processes and of distribution of products.

Inventory Management System: This system has techniques that help the

management to maintain the level of stock. This system involves the process of

stocking and restocking the organisation's inventory so as to increase overall sales

as stock will be available when the customers, retailers and who. Basically, it

combines the characteristics of technologies and processes (hardware and

software) and processes which track and maintain stock goods, whether they are

business properties, commodities and supplies or finished goods ready to be

shipped to salesmen or customers. Marshal Ltd. uses this system with its various

techniques to manage inventory. Techniques may include LIFO, FIFO, JIT and

ABC analysis (Pedroso and Gomes, 2020).

Price optimization system- This helps companies to determine the selling price

in line with recent trends in the market. In the above company and even their

competitor’s actions, their sales team sets the cost of furniture as per clients'

wishes. Price optimization systems are statistical systems that measure the

variations in competition at various levels of price and then integrate the data with

actual inventory knowledge to suggest values that increase income.

P2: Management accounting reporting and its methods

Management accounting reporting will aid the accountant to represent management

accounting information in a clear form which helps in taking important strategic decisions for the

smooth working of the organisation. This helps in highlighting the profitable operations of the

business so that they are easily visible to the stakeholders. This segment has various techniques

like inventory report, budgetary report, job costs report, account receivable ageing report.

Budgetary Reports: Budget reports are important in measuring the performance

of a company. Budget reports are made for small companies but they are also

used in large-scale organisations as per the department. They are made on the

basis of past experiences and have power to give insight of future unfavourable

situations. Budgets are prepared on the basis of current expenditure and costs as

compared to expected costs and expenditure. Accounting reports that are related

uses Cost Accounting System with which they are able to manage all their

relevant cost like that of raw material, processes and of distribution of products.

Inventory Management System: This system has techniques that help the

management to maintain the level of stock. This system involves the process of

stocking and restocking the organisation's inventory so as to increase overall sales

as stock will be available when the customers, retailers and who. Basically, it

combines the characteristics of technologies and processes (hardware and

software) and processes which track and maintain stock goods, whether they are

business properties, commodities and supplies or finished goods ready to be

shipped to salesmen or customers. Marshal Ltd. uses this system with its various

techniques to manage inventory. Techniques may include LIFO, FIFO, JIT and

ABC analysis (Pedroso and Gomes, 2020).

Price optimization system- This helps companies to determine the selling price

in line with recent trends in the market. In the above company and even their

competitor’s actions, their sales team sets the cost of furniture as per clients'

wishes. Price optimization systems are statistical systems that measure the

variations in competition at various levels of price and then integrate the data with

actual inventory knowledge to suggest values that increase income.

P2: Management accounting reporting and its methods

Management accounting reporting will aid the accountant to represent management

accounting information in a clear form which helps in taking important strategic decisions for the

smooth working of the organisation. This helps in highlighting the profitable operations of the

business so that they are easily visible to the stakeholders. This segment has various techniques

like inventory report, budgetary report, job costs report, account receivable ageing report.

Budgetary Reports: Budget reports are important in measuring the performance

of a company. Budget reports are made for small companies but they are also

used in large-scale organisations as per the department. They are made on the

basis of past experiences and have power to give insight of future unfavourable

situations. Budgets are prepared on the basis of current expenditure and costs as

compared to expected costs and expenditure. Accounting reports that are related

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to budgets help managers to provide with insight of more ways to earn profit,

lowers cost and gives a chance to bargain with the suppliers and stakeholders. It

will enable Marshall Ltd. to evaluate current performance with the expected

performance. With the budget report Marshall Ltd. estimates the value of

expected profit and filter out activities that can become the cause of failure in

achieving so. It also helps in analysing new opportunities which are there in the

market and also which will arrive in the near future.

Cost Reports: Procurement of raw materials, labours, overheads are the costs for

a company. The total of these costs are divided by the amount of the produce. The

cost report has the information about the cost of items with the selling prices of

the product. Through this report companies decide upon the profit margins for

their products. It will help the manager to evaluate critical expenditure areas, and

have a systematic analysis of total costs involved in specific projects (GOVDYA

and KHROMOVA, 2018). Marshall's management makes report to identifying the

reason of excessive cash outflow or costs which are not beneficial for the

business.

Performance Reports: These are the reports that are made to review the

performance of an organisation and the workforce of a company. In large-scale

organisations performance reports of departments are also developed. These

reports are developed to aid in decision making for the future of the company.

Exceptional workers who achieve targets on time and even exceed their goals are

appreciated for their performance in the organisation and under performers are

given warning and also motivation to work effectively. Marshall Ltd. form

performance report to identify departments which are not working effectively and

efficiently (Vakhrushina and et. al., 2018).

TASK 2

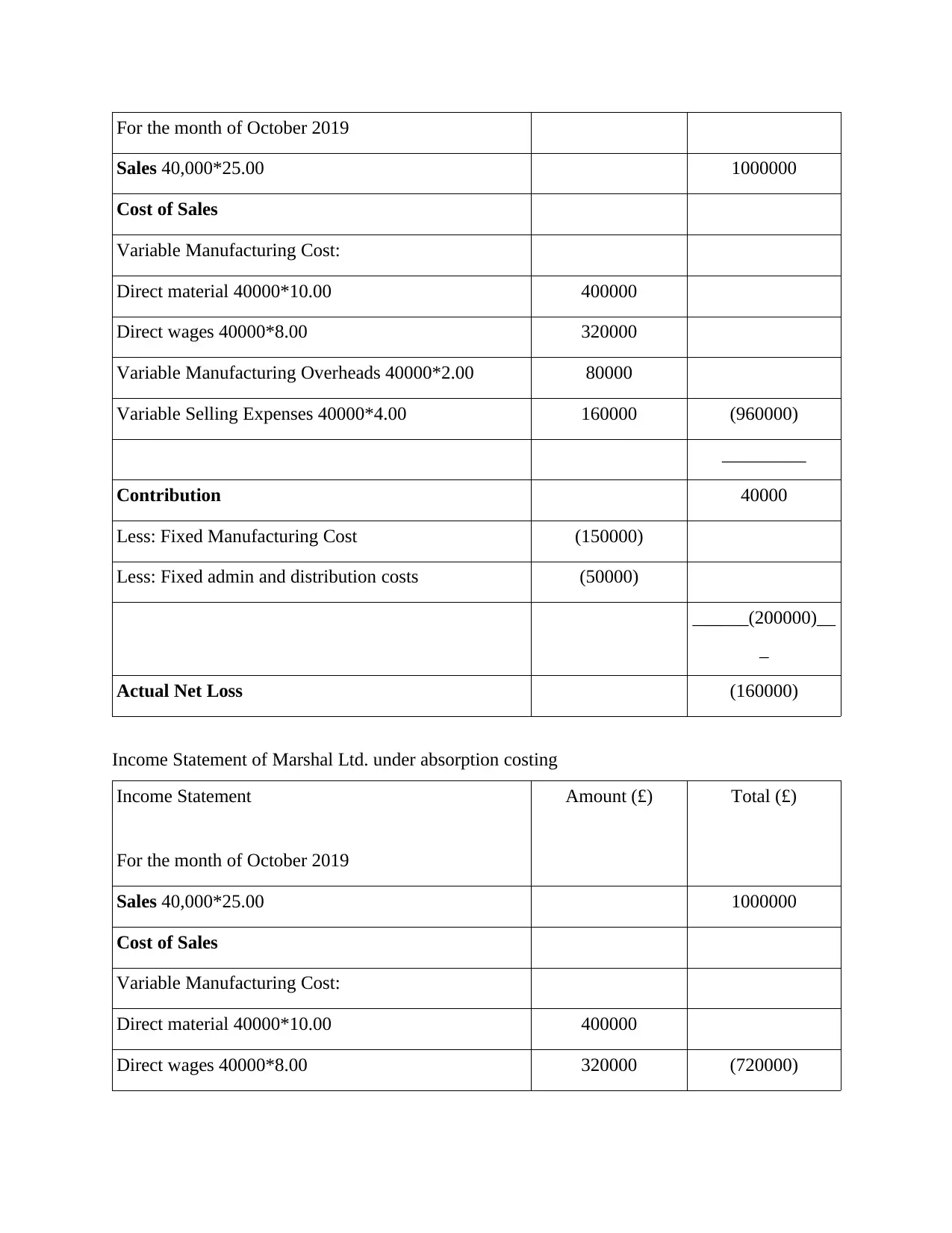

P3: Calculation of costs using marginal and absorption costs

Income Statement of Marshall Ltd. under marginal costing

Income Statement Amount (£) Total (£)

lowers cost and gives a chance to bargain with the suppliers and stakeholders. It

will enable Marshall Ltd. to evaluate current performance with the expected

performance. With the budget report Marshall Ltd. estimates the value of

expected profit and filter out activities that can become the cause of failure in

achieving so. It also helps in analysing new opportunities which are there in the

market and also which will arrive in the near future.

Cost Reports: Procurement of raw materials, labours, overheads are the costs for

a company. The total of these costs are divided by the amount of the produce. The

cost report has the information about the cost of items with the selling prices of

the product. Through this report companies decide upon the profit margins for

their products. It will help the manager to evaluate critical expenditure areas, and

have a systematic analysis of total costs involved in specific projects (GOVDYA

and KHROMOVA, 2018). Marshall's management makes report to identifying the

reason of excessive cash outflow or costs which are not beneficial for the

business.

Performance Reports: These are the reports that are made to review the

performance of an organisation and the workforce of a company. In large-scale

organisations performance reports of departments are also developed. These

reports are developed to aid in decision making for the future of the company.

Exceptional workers who achieve targets on time and even exceed their goals are

appreciated for their performance in the organisation and under performers are

given warning and also motivation to work effectively. Marshall Ltd. form

performance report to identify departments which are not working effectively and

efficiently (Vakhrushina and et. al., 2018).

TASK 2

P3: Calculation of costs using marginal and absorption costs

Income Statement of Marshall Ltd. under marginal costing

Income Statement Amount (£) Total (£)

For the month of October 2019

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000

Variable Manufacturing Overheads 40000*2.00 80000

Variable Selling Expenses 40000*4.00 160000 (960000)

_________

Contribution 40000

Less: Fixed Manufacturing Cost (150000)

Less: Fixed admin and distribution costs (50000)

______(200000)__

_

Actual Net Loss (160000)

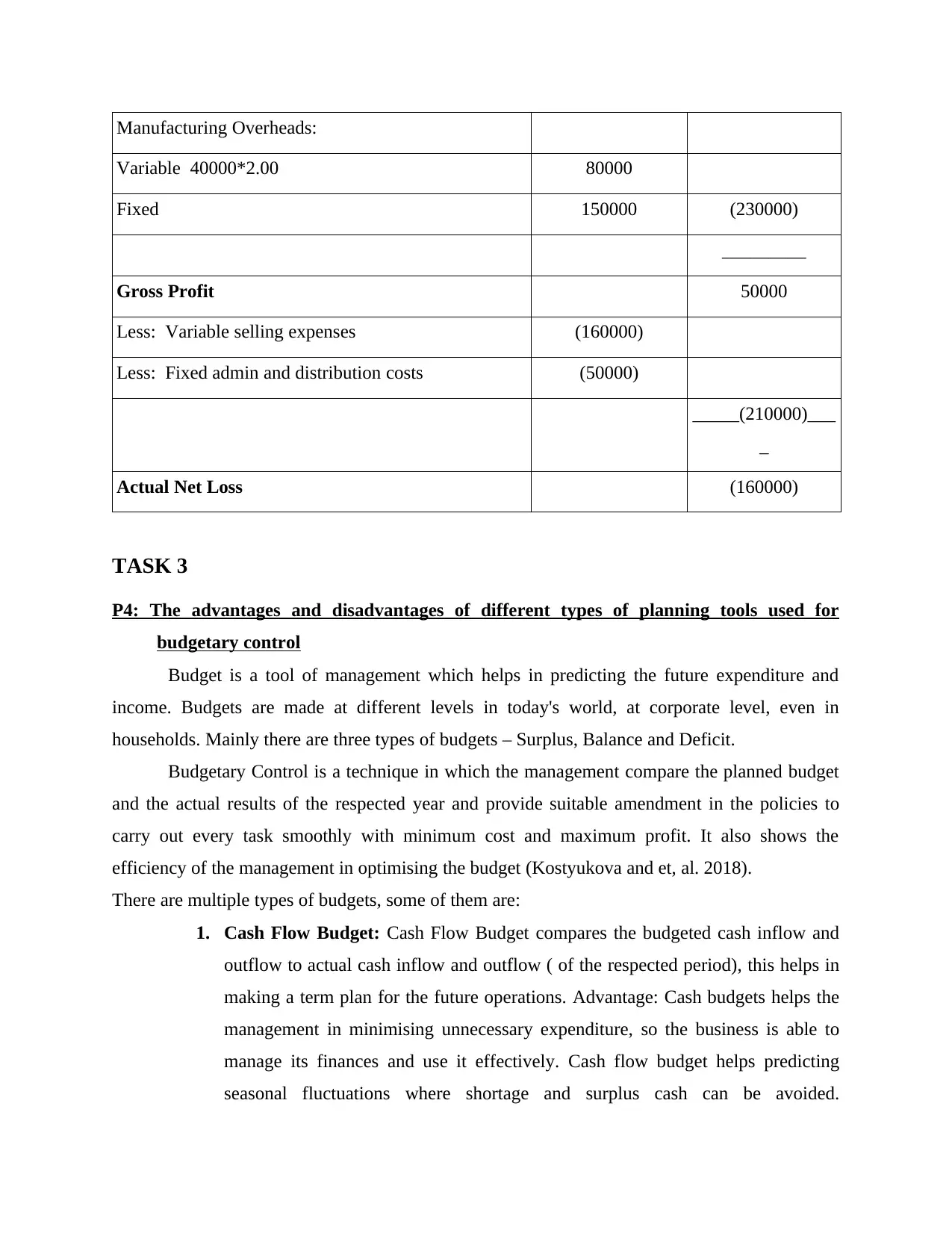

Income Statement of Marshal Ltd. under absorption costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000 (720000)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000

Variable Manufacturing Overheads 40000*2.00 80000

Variable Selling Expenses 40000*4.00 160000 (960000)

_________

Contribution 40000

Less: Fixed Manufacturing Cost (150000)

Less: Fixed admin and distribution costs (50000)

______(200000)__

_

Actual Net Loss (160000)

Income Statement of Marshal Ltd. under absorption costing

Income Statement

For the month of October 2019

Amount (£) Total (£)

Sales 40,000*25.00 1000000

Cost of Sales

Variable Manufacturing Cost:

Direct material 40000*10.00 400000

Direct wages 40000*8.00 320000 (720000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Manufacturing Overheads:

Variable 40000*2.00 80000

Fixed 150000 (230000)

_________

Gross Profit 50000

Less: Variable selling expenses (160000)

Less: Fixed admin and distribution costs (50000)

_____(210000)___

_

Actual Net Loss (160000)

TASK 3

P4: The advantages and disadvantages of different types of planning tools used for

budgetary control

Budget is a tool of management which helps in predicting the future expenditure and

income. Budgets are made at different levels in today's world, at corporate level, even in

households. Mainly there are three types of budgets – Surplus, Balance and Deficit.

Budgetary Control is a technique in which the management compare the planned budget

and the actual results of the respected year and provide suitable amendment in the policies to

carry out every task smoothly with minimum cost and maximum profit. It also shows the

efficiency of the management in optimising the budget (Kostyukova and et, al. 2018).

There are multiple types of budgets, some of them are:

1. Cash Flow Budget: Cash Flow Budget compares the budgeted cash inflow and

outflow to actual cash inflow and outflow ( of the respected period), this helps in

making a term plan for the future operations. Advantage: Cash budgets helps the

management in minimising unnecessary expenditure, so the business is able to

manage its finances and use it effectively. Cash flow budget helps predicting

seasonal fluctuations where shortage and surplus cash can be avoided.

Variable 40000*2.00 80000

Fixed 150000 (230000)

_________

Gross Profit 50000

Less: Variable selling expenses (160000)

Less: Fixed admin and distribution costs (50000)

_____(210000)___

_

Actual Net Loss (160000)

TASK 3

P4: The advantages and disadvantages of different types of planning tools used for

budgetary control

Budget is a tool of management which helps in predicting the future expenditure and

income. Budgets are made at different levels in today's world, at corporate level, even in

households. Mainly there are three types of budgets – Surplus, Balance and Deficit.

Budgetary Control is a technique in which the management compare the planned budget

and the actual results of the respected year and provide suitable amendment in the policies to

carry out every task smoothly with minimum cost and maximum profit. It also shows the

efficiency of the management in optimising the budget (Kostyukova and et, al. 2018).

There are multiple types of budgets, some of them are:

1. Cash Flow Budget: Cash Flow Budget compares the budgeted cash inflow and

outflow to actual cash inflow and outflow ( of the respected period), this helps in

making a term plan for the future operations. Advantage: Cash budgets helps the

management in minimising unnecessary expenditure, so the business is able to

manage its finances and use it effectively. Cash flow budget helps predicting

seasonal fluctuations where shortage and surplus cash can be avoided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

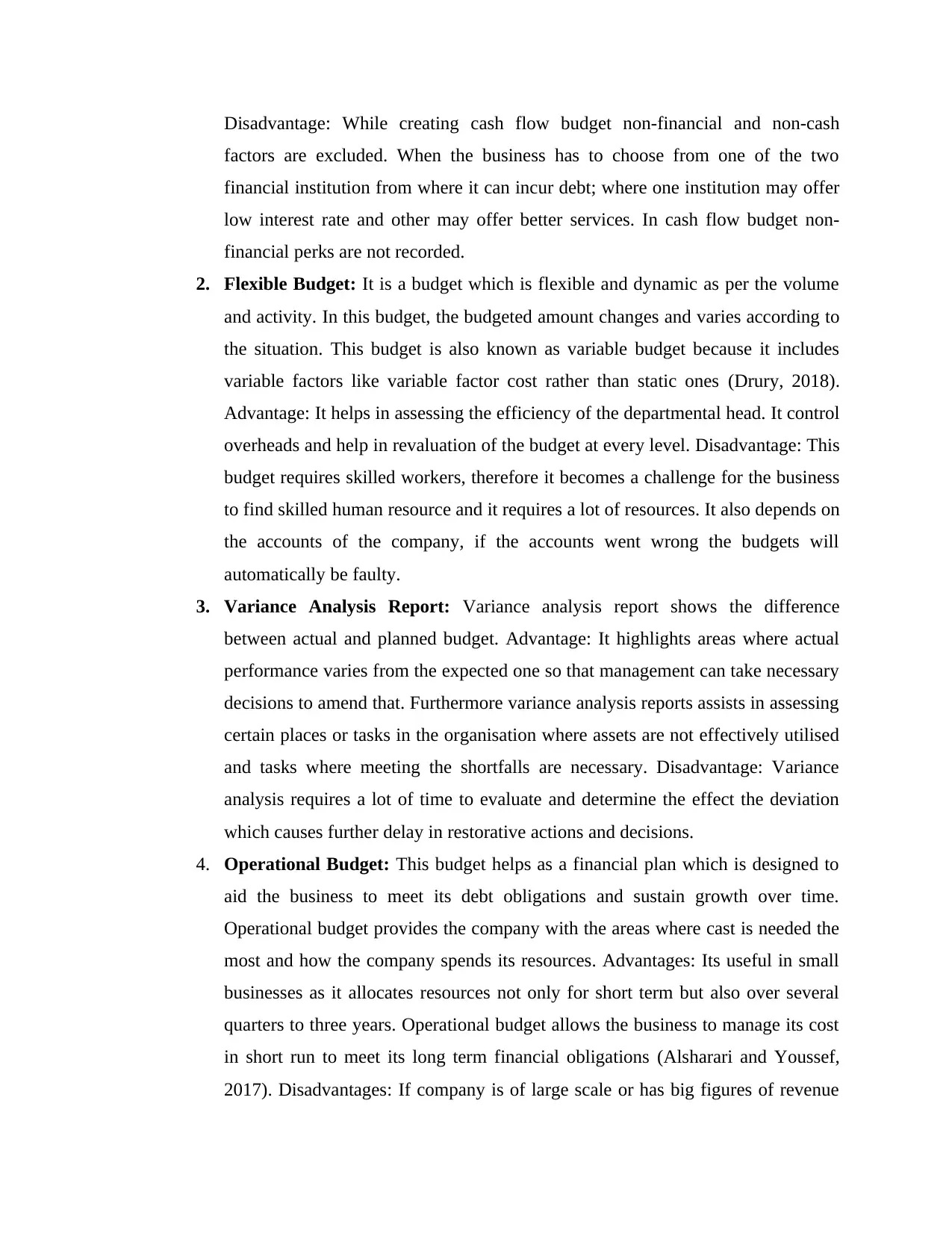

Disadvantage: While creating cash flow budget non-financial and non-cash

factors are excluded. When the business has to choose from one of the two

financial institution from where it can incur debt; where one institution may offer

low interest rate and other may offer better services. In cash flow budget non-

financial perks are not recorded.

2. Flexible Budget: It is a budget which is flexible and dynamic as per the volume

and activity. In this budget, the budgeted amount changes and varies according to

the situation. This budget is also known as variable budget because it includes

variable factors like variable factor cost rather than static ones (Drury, 2018).

Advantage: It helps in assessing the efficiency of the departmental head. It control

overheads and help in revaluation of the budget at every level. Disadvantage: This

budget requires skilled workers, therefore it becomes a challenge for the business

to find skilled human resource and it requires a lot of resources. It also depends on

the accounts of the company, if the accounts went wrong the budgets will

automatically be faulty.

3. Variance Analysis Report: Variance analysis report shows the difference

between actual and planned budget. Advantage: It highlights areas where actual

performance varies from the expected one so that management can take necessary

decisions to amend that. Furthermore variance analysis reports assists in assessing

certain places or tasks in the organisation where assets are not effectively utilised

and tasks where meeting the shortfalls are necessary. Disadvantage: Variance

analysis requires a lot of time to evaluate and determine the effect the deviation

which causes further delay in restorative actions and decisions.

4. Operational Budget: This budget helps as a financial plan which is designed to

aid the business to meet its debt obligations and sustain growth over time.

Operational budget provides the company with the areas where cast is needed the

most and how the company spends its resources. Advantages: Its useful in small

businesses as it allocates resources not only for short term but also over several

quarters to three years. Operational budget allows the business to manage its cost

in short run to meet its long term financial obligations (Alsharari and Youssef,

2017). Disadvantages: If company is of large scale or has big figures of revenue

factors are excluded. When the business has to choose from one of the two

financial institution from where it can incur debt; where one institution may offer

low interest rate and other may offer better services. In cash flow budget non-

financial perks are not recorded.

2. Flexible Budget: It is a budget which is flexible and dynamic as per the volume

and activity. In this budget, the budgeted amount changes and varies according to

the situation. This budget is also known as variable budget because it includes

variable factors like variable factor cost rather than static ones (Drury, 2018).

Advantage: It helps in assessing the efficiency of the departmental head. It control

overheads and help in revaluation of the budget at every level. Disadvantage: This

budget requires skilled workers, therefore it becomes a challenge for the business

to find skilled human resource and it requires a lot of resources. It also depends on

the accounts of the company, if the accounts went wrong the budgets will

automatically be faulty.

3. Variance Analysis Report: Variance analysis report shows the difference

between actual and planned budget. Advantage: It highlights areas where actual

performance varies from the expected one so that management can take necessary

decisions to amend that. Furthermore variance analysis reports assists in assessing

certain places or tasks in the organisation where assets are not effectively utilised

and tasks where meeting the shortfalls are necessary. Disadvantage: Variance

analysis requires a lot of time to evaluate and determine the effect the deviation

which causes further delay in restorative actions and decisions.

4. Operational Budget: This budget helps as a financial plan which is designed to

aid the business to meet its debt obligations and sustain growth over time.

Operational budget provides the company with the areas where cast is needed the

most and how the company spends its resources. Advantages: Its useful in small

businesses as it allocates resources not only for short term but also over several

quarters to three years. Operational budget allows the business to manage its cost

in short run to meet its long term financial obligations (Alsharari and Youssef,

2017). Disadvantages: If company is of large scale or has big figures of revenue

and costs the making an operational budget becomes time-consuming and prone

to errors. It also requires extensive research to assess long term insight of

financial needs of the company.

TASK 4

P5: Adaptation of management accounting systems by the organisations to face and solve

financial problems.

Financial Problems: Sufficient financial resources are needed for the smooth

functioning of any business or organisation. There may come many financial problems for the

business where the finance is inadequate. These problems come when decisions taken by the

management are not efficient. Commonly this is faced by small and medium-sized businesses

and organisations, because they are not able to take efficient management decisions as they do

not follow management accounting systems. Marshall Ltd. is working on getting more financial

resources which can be managed by Management Accounting Systems.

Problems in recognising core competencies: Marshal Ltd. is suffering from this

problem because they are not able to recognise and identify competencies of various

departments. It face issues related to finance and is unable to identify the weaknesses and flaws

of departments. That's why the company suffers from finance related problems and which further

leads to losses and unprofitably operations of the business.

Below cited techniques can help Marshal Ltd. to overcome its drawbacks:

Management accounting

techniques

Reverting to the financial problems by using management

accounting system

Marshall Ltd. Pedragon Plc

Benchmarking Marshall Ltd. face problems in

financial resource segment

because it is unable to measure

department's performance and

its sales are also decreasing.

Management of the company

can use benchmarking, this

The company faces financial

problem due to their inability

to identify weaknesses and

strengths of their departments.

With the usage of key

performance indicator method,

management with the help of

to errors. It also requires extensive research to assess long term insight of

financial needs of the company.

TASK 4

P5: Adaptation of management accounting systems by the organisations to face and solve

financial problems.

Financial Problems: Sufficient financial resources are needed for the smooth

functioning of any business or organisation. There may come many financial problems for the

business where the finance is inadequate. These problems come when decisions taken by the

management are not efficient. Commonly this is faced by small and medium-sized businesses

and organisations, because they are not able to take efficient management decisions as they do

not follow management accounting systems. Marshall Ltd. is working on getting more financial

resources which can be managed by Management Accounting Systems.

Problems in recognising core competencies: Marshal Ltd. is suffering from this

problem because they are not able to recognise and identify competencies of various

departments. It face issues related to finance and is unable to identify the weaknesses and flaws

of departments. That's why the company suffers from finance related problems and which further

leads to losses and unprofitably operations of the business.

Below cited techniques can help Marshal Ltd. to overcome its drawbacks:

Management accounting

techniques

Reverting to the financial problems by using management

accounting system

Marshall Ltd. Pedragon Plc

Benchmarking Marshall Ltd. face problems in

financial resource segment

because it is unable to measure

department's performance and

its sales are also decreasing.

Management of the company

can use benchmarking, this

The company faces financial

problem due to their inability

to identify weaknesses and

strengths of their departments.

With the usage of key

performance indicator method,

management with the help of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

tool helps to set bars, standards

and benchmarks. With these

standards management can

identify performance and

measure efforts and

performance of each

department. With the help of

benchmarking they can form

policies to solve problems

(Hertati and Safkaur, 2019).

indicator can identify the

department which is providing

strength to the company (Uyar,

2019).

Advising to Marshall Ltd. to

use technique of

benchmarking:

With the application of Key

performance indicator,

Marshall Ltd. will be able to

form a plan for the future to

solve and control problems

related to finance. By setting

KPI they will be able to

control cash outflows of

business activities.

CONCLUSION

Management Accounting System is a major factor that determines the sustainability of

business in the industry. It helps the organisation to take important decisions related to the

functionality and management. Marshall Ltd. is taking the right step to adopt Management

Accounting Systems. This will help the company from coming out of the financial crises that has

overpowered the company's growth. Implementation of management accounting systems along

with financial accounting systems would enable them to strengthen its decision making which

will help the enterprise to survive in the long run and in this competitive market.

and benchmarks. With these

standards management can

identify performance and

measure efforts and

performance of each

department. With the help of

benchmarking they can form

policies to solve problems

(Hertati and Safkaur, 2019).

indicator can identify the

department which is providing

strength to the company (Uyar,

2019).

Advising to Marshall Ltd. to

use technique of

benchmarking:

With the application of Key

performance indicator,

Marshall Ltd. will be able to

form a plan for the future to

solve and control problems

related to finance. By setting

KPI they will be able to

control cash outflows of

business activities.

CONCLUSION

Management Accounting System is a major factor that determines the sustainability of

business in the industry. It helps the organisation to take important decisions related to the

functionality and management. Marshall Ltd. is taking the right step to adopt Management

Accounting Systems. This will help the company from coming out of the financial crises that has

overpowered the company's growth. Implementation of management accounting systems along

with financial accounting systems would enable them to strengthen its decision making which

will help the enterprise to survive in the long run and in this competitive market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3), p.2.

Alsharari, N. M. and Youssef, M. A. E. A., 2017. Management accounting change and the

implementation of GFMIS: a Jordanian case study. Asian Review of Accounting.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

GOVDYA, V. and KHROMOVA, I., 2018. Methodical Aspects of the Decomposition Approach

to the Formation of the Managerial Cost Accounting System in the Organizations of the

Russian Agroindustrial Complex. Journal of Applied Economic Sciences, 13(3).

Hertati, L. and Safkaur, O., 2019. Impact of Business Strategy on the Management Accounting:

The Case of the Production of State-Owned Enterprises in Indonesia, South Sumatra.

Journal of Asian Business Strategy, 9(1), pp.29-39.

Kostyukova, E. I. and et, al. 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical Sciences, 9(2),

pp.775-779.

Laela, S. F. and et. al., 2018. Management accounting-strategy coalignment in Islamic banking.

International Journal of Islamic and Middle Eastern Finance and Management.

Pedroso, E. and Gomes, C. F., 2020. The effectiveness of management accounting systems in

SMEs: a multidimensional measurement approach. Journal of Applied Accounting

Research.

Uyar, M., 2019. The management accounting and the business strategy development at SMEs.

Problems and perspectives in management, (17, Iss. 1), pp.1-10.

Vakhrushina, M. A. and et. al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 9(3), pp.808-813.

Books and Journals

Abdusalomova, N., 2019. PROBLEMS OF MANAGEMENT ACCOUNTING AND WAYS TO

SOLVE THEM. International Finance and Accounting, 2019(3), p.2.

Alsharari, N. M. and Youssef, M. A. E. A., 2017. Management accounting change and the

implementation of GFMIS: a Jordanian case study. Asian Review of Accounting.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

GOVDYA, V. and KHROMOVA, I., 2018. Methodical Aspects of the Decomposition Approach

to the Formation of the Managerial Cost Accounting System in the Organizations of the

Russian Agroindustrial Complex. Journal of Applied Economic Sciences, 13(3).

Hertati, L. and Safkaur, O., 2019. Impact of Business Strategy on the Management Accounting:

The Case of the Production of State-Owned Enterprises in Indonesia, South Sumatra.

Journal of Asian Business Strategy, 9(1), pp.29-39.

Kostyukova, E. I. and et, al. 2018. Improvement cost management system for management

accounting. Research Journal of Pharmaceutical, Biological and Chemical Sciences, 9(2),

pp.775-779.

Laela, S. F. and et. al., 2018. Management accounting-strategy coalignment in Islamic banking.

International Journal of Islamic and Middle Eastern Finance and Management.

Pedroso, E. and Gomes, C. F., 2020. The effectiveness of management accounting systems in

SMEs: a multidimensional measurement approach. Journal of Applied Accounting

Research.

Uyar, M., 2019. The management accounting and the business strategy development at SMEs.

Problems and perspectives in management, (17, Iss. 1), pp.1-10.

Vakhrushina, M. A. and et. al., 2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences, 9(3), pp.808-813.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.