Management Accounting Report: Costing, Reporting, and Systems

VerifiedAdded on 2020/06/06

|19

|5507

|58

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on their application within a grocery store context. It begins by defining management accounting and its significance, particularly for small businesses like Taj Store, and differentiates it from financial accounting. The report then delves into various management accounting systems, including inventory management, cost accounting, and job costing, highlighting their benefits in decision-making and resource allocation. It further examines different reporting methods, such as inventory control, accounts receivable, performance, accounts payable, and budget reporting, explaining their roles in monitoring and evaluating business performance. The report also explores the difference between marginal and absorption costing methods, including their implications for income statement preparation. Finally, it discusses the advantages and disadvantages of planning tools used for budgetary control and the adaptation of management accounting systems to address financial challenges.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting systems......................................................................................1

P2 Methods of management accounting reporting.................................................................5

TASK 2............................................................................................................................................6

P3 Difference between income statement made through marginal and absorption costing...6

TASK 3 ........................................................................................................................................10

P4 Advantages and disadvantages of planning tools which are used for budgetary control10

P5 Adopting management accounting systems for responding financial troubles .............12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

.......................................................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting systems......................................................................................1

P2 Methods of management accounting reporting.................................................................5

TASK 2............................................................................................................................................6

P3 Difference between income statement made through marginal and absorption costing...6

TASK 3 ........................................................................................................................................10

P4 Advantages and disadvantages of planning tools which are used for budgetary control10

P5 Adopting management accounting systems for responding financial troubles .............12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

.......................................................................................................................................................16

Report

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM covering management accounting and management accounting

system together with different costing techniques and reporting to enable the organization

implement them.

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM covering management accounting and management accounting

system together with different costing techniques and reporting to enable the organization

implement them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of recording and identifying financial as well as

non-financial data for making crucial decisions relating to investment and operational control.

Most of the enterprises face various kind of issues in their business because of changing external

environment and organisational policies (Cokins, 2013). Managerial accounting focuses on

increasing revenue by minimising wastage and finding new markets where investment can be

done for earning more profit. Earlier, companies were mainly coping up with financial problems

like maintaining right amount of cash in the firm etc. but now, complexity in doing business has

increased importance of management accounting because it does not only resolve troubles

relating to managing money but it also assist different departments of a company like marketing,

operations etc. Taj Store is a grocery shop in London. They are operating at low level but this

organisation was founded in 1936. This assignment will explain various types of management

accounting system along with their essential requirement. Some methods of management

accounting reporting will also become part of this report. Income statement will be made by

using marginal and absorption costing and difference between them will get discussed. Topics

like planning tools and adaption of management accounting systems will be explained at the end

of this file.

TASK 1

P1 Management accounting systems

Making right decision in appropriate time is a difficult task, most of the managers started

using various systems of management accounting because they know that this form of accounts

can resolve many issues relating to financial and non-financial problems. For a small company

like Taj Store, raising finds is not easy. They seek high amount of loan at low rate and try to

locate correct areas where investment can be made for attaining high returns. Financial

accounting can help in making significant decisions up-to a limit (Chen, Weikart and Williams,

2014). They mainly concentrate on recording of data instead of analysing them for the benefit of

managers. Difference between financial and managerial accounting:

Management accounting is the process of recording and identifying financial as well as

non-financial data for making crucial decisions relating to investment and operational control.

Most of the enterprises face various kind of issues in their business because of changing external

environment and organisational policies (Cokins, 2013). Managerial accounting focuses on

increasing revenue by minimising wastage and finding new markets where investment can be

done for earning more profit. Earlier, companies were mainly coping up with financial problems

like maintaining right amount of cash in the firm etc. but now, complexity in doing business has

increased importance of management accounting because it does not only resolve troubles

relating to managing money but it also assist different departments of a company like marketing,

operations etc. Taj Store is a grocery shop in London. They are operating at low level but this

organisation was founded in 1936. This assignment will explain various types of management

accounting system along with their essential requirement. Some methods of management

accounting reporting will also become part of this report. Income statement will be made by

using marginal and absorption costing and difference between them will get discussed. Topics

like planning tools and adaption of management accounting systems will be explained at the end

of this file.

TASK 1

P1 Management accounting systems

Making right decision in appropriate time is a difficult task, most of the managers started

using various systems of management accounting because they know that this form of accounts

can resolve many issues relating to financial and non-financial problems. For a small company

like Taj Store, raising finds is not easy. They seek high amount of loan at low rate and try to

locate correct areas where investment can be made for attaining high returns. Financial

accounting can help in making significant decisions up-to a limit (Chen, Weikart and Williams,

2014). They mainly concentrate on recording of data instead of analysing them for the benefit of

managers. Difference between financial and managerial accounting:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting Management accounting

It is made for external parties like shareholders

of company.

It is used by internal stakeholders like

employees, managers, senior board members

of the enterprise etc.

Historical data is used for making accounts and

delaying in normal in this form of accounting.

It is future oriented and formed in present time.

Reporting of whole organisation is done. Reporting of particular areas is done.

It measures financial records. Both financial and non-financial like

operational data is measured in it.

Making financial statements is compulsory for

limited company because of legal

requirements.

There is no legal binding for making any report

under management accounting.

Different managerial accounting systems are used by many small enterprises because of

various advantages. Small firms do not have much resources, they cannot afford wastage of

limited funds. Process of management accounts assist in finding the mistakes which managers

are repeating by using inventory control and price optimisation system (Burritt, Schaltegger and

Zvezdov, 2011). It decreases confusion among different division and reduces the time that is

taken for making a call. Costing accounting and job costing are some other kind of systems

which concentrate of techniques for minimising expenses on production. Below is complete

explanation of these processes:

Inventory management system – If an enterprise will keep more than needed good in

the warehouse then it will increase significant expenses like carrying cost. If number of

inventory is less than required then supply chain of company will hamper and customer will not

get desired good in needed time. Inventory management system is a software which is used for

tracking deliveries, available and sold stock. Significant method of EOQ (economic order

quantity) is used for finding the right time and quantity of making an order. This system plays

significant role in decreasing wastage of resources, it also assures smooth flow of business by

It is made for external parties like shareholders

of company.

It is used by internal stakeholders like

employees, managers, senior board members

of the enterprise etc.

Historical data is used for making accounts and

delaying in normal in this form of accounting.

It is future oriented and formed in present time.

Reporting of whole organisation is done. Reporting of particular areas is done.

It measures financial records. Both financial and non-financial like

operational data is measured in it.

Making financial statements is compulsory for

limited company because of legal

requirements.

There is no legal binding for making any report

under management accounting.

Different managerial accounting systems are used by many small enterprises because of

various advantages. Small firms do not have much resources, they cannot afford wastage of

limited funds. Process of management accounts assist in finding the mistakes which managers

are repeating by using inventory control and price optimisation system (Burritt, Schaltegger and

Zvezdov, 2011). It decreases confusion among different division and reduces the time that is

taken for making a call. Costing accounting and job costing are some other kind of systems

which concentrate of techniques for minimising expenses on production. Below is complete

explanation of these processes:

Inventory management system – If an enterprise will keep more than needed good in

the warehouse then it will increase significant expenses like carrying cost. If number of

inventory is less than required then supply chain of company will hamper and customer will not

get desired good in needed time. Inventory management system is a software which is used for

tracking deliveries, available and sold stock. Significant method of EOQ (economic order

quantity) is used for finding the right time and quantity of making an order. This system plays

significant role in decreasing wastage of resources, it also assures smooth flow of business by

storing appropriate amount of goods in the warehouse (Aminbakhsh, Gunduz and Sonmez,

2013). Some organisation keeps record of products on the basis of margin. If an item earns more

profit to company then special attention will be provided on its supply and vice-a-versa.

Cost accounting system – It can be considered as one of the most important part of

management accounting system because it finds the ways for checking and stopping insignificant

wastages. It mainly deals with production unit but it has huge scope. Most of the managers use it

for analysing profitability of a product. Reducing direct labour cost and material expenses are

some of its prime area of focus.

Job costing – This is a different type of system where profit generation capacity of every

job is analysed. So, firm can increase the number of ''Jobs'' which are providing more benefit to

organisation and find various number of tasks that do not have an important contribution in

earning revenue (Ahmad and Mohamed Zabri, 2012). It is also related to production process and

normally used when customer have specific demands.

Price optimisation – Demand of an item is also affected by its price. This system of

management accounting determines the right rate of a product at which it should be available in

the stores. If value of goods is high then customer will not buy it, this will make negative affect

on revenue of organisation. If price is low then also enterprise has to bear loss because in this

situation, buyers are ready to pay more sum for same commodity. Price optimisation assist in

ascertaining appropriate rate of the product.

2013). Some organisation keeps record of products on the basis of margin. If an item earns more

profit to company then special attention will be provided on its supply and vice-a-versa.

Cost accounting system – It can be considered as one of the most important part of

management accounting system because it finds the ways for checking and stopping insignificant

wastages. It mainly deals with production unit but it has huge scope. Most of the managers use it

for analysing profitability of a product. Reducing direct labour cost and material expenses are

some of its prime area of focus.

Job costing – This is a different type of system where profit generation capacity of every

job is analysed. So, firm can increase the number of ''Jobs'' which are providing more benefit to

organisation and find various number of tasks that do not have an important contribution in

earning revenue (Ahmad and Mohamed Zabri, 2012). It is also related to production process and

normally used when customer have specific demands.

Price optimisation – Demand of an item is also affected by its price. This system of

management accounting determines the right rate of a product at which it should be available in

the stores. If value of goods is high then customer will not buy it, this will make negative affect

on revenue of organisation. If price is low then also enterprise has to bear loss because in this

situation, buyers are ready to pay more sum for same commodity. Price optimisation assist in

ascertaining appropriate rate of the product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management

Accounting

system

Inventory

management

System

Cost

Accounting System

Price

Optimisation

Job Costing

Accounting

system

Inventory

management

System

Cost

Accounting System

Price

Optimisation

Job Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Methods of management accounting reporting

Every organisation whether small or large, make different type of report for evaluating

the work which they have done in past. These documents are made for finding flaws in past

policies and analysing successful plans. Report depicts variance between actual targets and pre-

determined objectives. Various kind of management accounting reporting is as follows:

Inventory control reporting – This report is made for analysing whether the stock is

managed in the proper way or not and what are the areas which can be improved in upcoming

time so the major problems in relating to stock i.e. over and under-stocking can be resolved

without getting delayed (Delafrooz and Paim, 2011). This report shows how much goods are

present in the company in present position and what was the sale of enterprise is a particular time

period. Taj Store can adopt this method of reporting because it will help them in decreasing

ordering and carry cost and they can find the proper need of stock which should be present in a

specific time period in their stores. They are selling variety of goods, inventory control reporting

can support in finding expected quantity of good which customer may buy in forthcoming time.

This work can be done by checking past records and identifying old mistakes.

Accounts receivable reporting – Taj store is operating from a long time ago in London.

They are many permanent customer who buy good from them on credit basis. Account

receivable report is used for recording the amount of credit which company has to given to their

different debtors. This report shows money which debtors are going to pay to the organisation

along with the time period in which they are going to pay. Some firms makes this document on

weekly, quarterly or monthly basis while other keep their focus on the amount and instead of

considering time period they check the sum which every debtor owe to them. Taj Store will get

great assistance by making this report, on monthly or any other basis which suits them, because it

reduces amount of bad debts. If they will use this report in best way then they can find and make

strict rules for debtor are not paying money is committed time.

Performance reporting – Normally this report is created for analysing performance of

different division of a company. But Taj store is small organisation and they do not have any

department. This does not means that they cannot make and use this report. They can utilise this

document for finding the difference between expected work and actual performance of the

Every organisation whether small or large, make different type of report for evaluating

the work which they have done in past. These documents are made for finding flaws in past

policies and analysing successful plans. Report depicts variance between actual targets and pre-

determined objectives. Various kind of management accounting reporting is as follows:

Inventory control reporting – This report is made for analysing whether the stock is

managed in the proper way or not and what are the areas which can be improved in upcoming

time so the major problems in relating to stock i.e. over and under-stocking can be resolved

without getting delayed (Delafrooz and Paim, 2011). This report shows how much goods are

present in the company in present position and what was the sale of enterprise is a particular time

period. Taj Store can adopt this method of reporting because it will help them in decreasing

ordering and carry cost and they can find the proper need of stock which should be present in a

specific time period in their stores. They are selling variety of goods, inventory control reporting

can support in finding expected quantity of good which customer may buy in forthcoming time.

This work can be done by checking past records and identifying old mistakes.

Accounts receivable reporting – Taj store is operating from a long time ago in London.

They are many permanent customer who buy good from them on credit basis. Account

receivable report is used for recording the amount of credit which company has to given to their

different debtors. This report shows money which debtors are going to pay to the organisation

along with the time period in which they are going to pay. Some firms makes this document on

weekly, quarterly or monthly basis while other keep their focus on the amount and instead of

considering time period they check the sum which every debtor owe to them. Taj Store will get

great assistance by making this report, on monthly or any other basis which suits them, because it

reduces amount of bad debts. If they will use this report in best way then they can find and make

strict rules for debtor are not paying money is committed time.

Performance reporting – Normally this report is created for analysing performance of

different division of a company. But Taj store is small organisation and they do not have any

department. This does not means that they cannot make and use this report. They can utilise this

document for finding the difference between expected work and actual performance of the

employees (Ekbatani, and Sangeladji, 2011). Mistakes done by worker can be recorded in this

report and details of their good work will also become part of this document. Manager will get

essential support from this report because it can tell them information about which employees

should get how much incentives and promotions in upcoming time.

Account payable reporting – This report provide details about the money which an

organisation has paid or will pay to their suppliers. Seller are important part of business and if

they will receive their payment in promised time then relation between company and suppliers

will always remain fine (Foster, Hart and Lewis, 2011). Like account receivable report, it can

also be made on the basis of time or amount. It depends on policy of firm. If Taj stores will make

this report then they can easily keep positive relations with their supplier and it can assist them in

getting timely delivery of the products along with some special discount. This report can also be

used for determining cash balance which may be required in next period.

Budget reporting – Budget is made for comparing difference between actual and

budgeted performance. Budget is the planning of income and expenditure for a particular period

of time generally one year. Budget report shows performance of complete organisation, not one

or two departments or employees. Taj stores will get necessary assistance from this report, they

can remove confusion from the mind of worker and synchronise their effort in attaining long

term goals of the firm. Formation of this report can be bit expensive but an enterprise can earn

various advantages from using this method as it covered whole organisation. Most of the

conflicts in the firm can get resolve if workers has complete idea about the resources which are

available to them.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

Income statement in the document which reveal revenue earned by firm along with

expenditure done by them (Fullerton, Kennedy and Widener, 2014). In management accounting,

there are more than one method of making income statement also known by name of profit and

loss account. One is through marginal costing approach and other is through absorption costing.

Below is their proper explanation:

report and details of their good work will also become part of this document. Manager will get

essential support from this report because it can tell them information about which employees

should get how much incentives and promotions in upcoming time.

Account payable reporting – This report provide details about the money which an

organisation has paid or will pay to their suppliers. Seller are important part of business and if

they will receive their payment in promised time then relation between company and suppliers

will always remain fine (Foster, Hart and Lewis, 2011). Like account receivable report, it can

also be made on the basis of time or amount. It depends on policy of firm. If Taj stores will make

this report then they can easily keep positive relations with their supplier and it can assist them in

getting timely delivery of the products along with some special discount. This report can also be

used for determining cash balance which may be required in next period.

Budget reporting – Budget is made for comparing difference between actual and

budgeted performance. Budget is the planning of income and expenditure for a particular period

of time generally one year. Budget report shows performance of complete organisation, not one

or two departments or employees. Taj stores will get necessary assistance from this report, they

can remove confusion from the mind of worker and synchronise their effort in attaining long

term goals of the firm. Formation of this report can be bit expensive but an enterprise can earn

various advantages from using this method as it covered whole organisation. Most of the

conflicts in the firm can get resolve if workers has complete idea about the resources which are

available to them.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

Income statement in the document which reveal revenue earned by firm along with

expenditure done by them (Fullerton, Kennedy and Widener, 2014). In management accounting,

there are more than one method of making income statement also known by name of profit and

loss account. One is through marginal costing approach and other is through absorption costing.

Below is their proper explanation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing – In this method, fixed cost is taken on period basis and variable cost of

treat in normal way i.e. subtracted after contribution. When an organisation make some addition

unit of an item, then they have to spend extra money on manufacturing of this product. Direct

material, labour and overhead will be charged, in this approach, when they are actually incurred.

On the other hand, fixed expenses, selling and administration cost will be charged at the time of

their incurring (What is Budgetary control? 2017).

Absorption costing – This method is very different from above one. Whether the cost is

fixed or variable, it will be allocated on the basis of units sold. Some significant expenses like

selling and administration cost is not taken in account at the time of making income statement by

using this approach (Gaizauskas and Martinavicius, 2013). This is an old approach and it was

used in traditional accounting methods.

Difference between marginal and absorption costing is mentioned below:

Basis Marginal Absorption

Use It is used as a decision making

tool by managers.

It is utilised in external

reporting.

Accounting standards At the time of inventory

valuation, this approach cannot

be used according to the rules

of mentioned in accounting

standards.

International accounting

standards allow use of

absorption costing in inventory

valuation.

Fixed cost In this approach, fixed cost is

fully subtracted from the

contribution. It does matter

whether goods are sold in

present year or next year.

Fixed cost incurred on sold

goods are treated in this year.

Inventory valuation Variable cost of production is

used for inventory valuation.

Total cost is considered for

inventory valuation

treat in normal way i.e. subtracted after contribution. When an organisation make some addition

unit of an item, then they have to spend extra money on manufacturing of this product. Direct

material, labour and overhead will be charged, in this approach, when they are actually incurred.

On the other hand, fixed expenses, selling and administration cost will be charged at the time of

their incurring (What is Budgetary control? 2017).

Absorption costing – This method is very different from above one. Whether the cost is

fixed or variable, it will be allocated on the basis of units sold. Some significant expenses like

selling and administration cost is not taken in account at the time of making income statement by

using this approach (Gaizauskas and Martinavicius, 2013). This is an old approach and it was

used in traditional accounting methods.

Difference between marginal and absorption costing is mentioned below:

Basis Marginal Absorption

Use It is used as a decision making

tool by managers.

It is utilised in external

reporting.

Accounting standards At the time of inventory

valuation, this approach cannot

be used according to the rules

of mentioned in accounting

standards.

International accounting

standards allow use of

absorption costing in inventory

valuation.

Fixed cost In this approach, fixed cost is

fully subtracted from the

contribution. It does matter

whether goods are sold in

present year or next year.

Fixed cost incurred on sold

goods are treated in this year.

Inventory valuation Variable cost of production is

used for inventory valuation.

Total cost is considered for

inventory valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

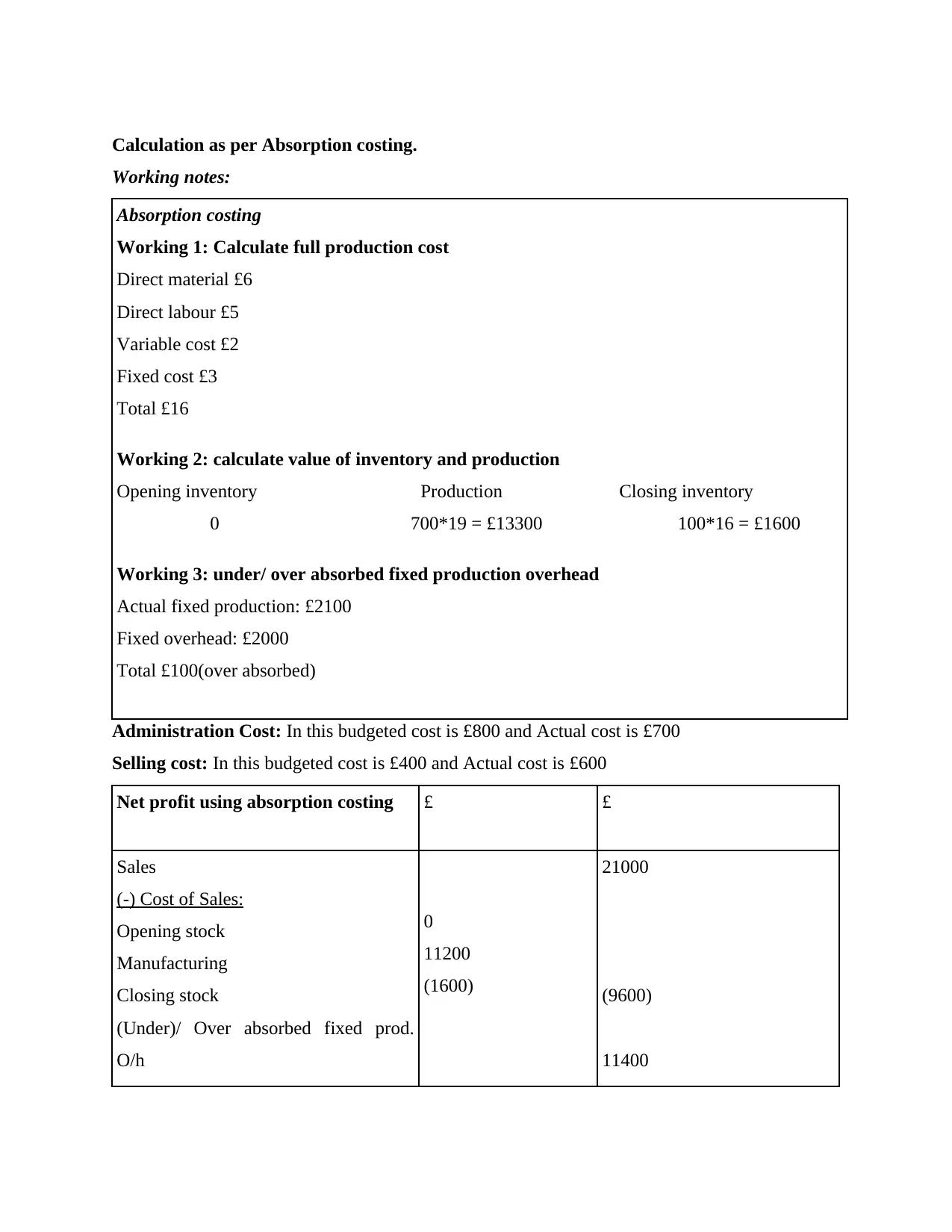

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

11200

(1600)

21000

(9600)

11400

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

11200

(1600)

21000

(9600)

11400

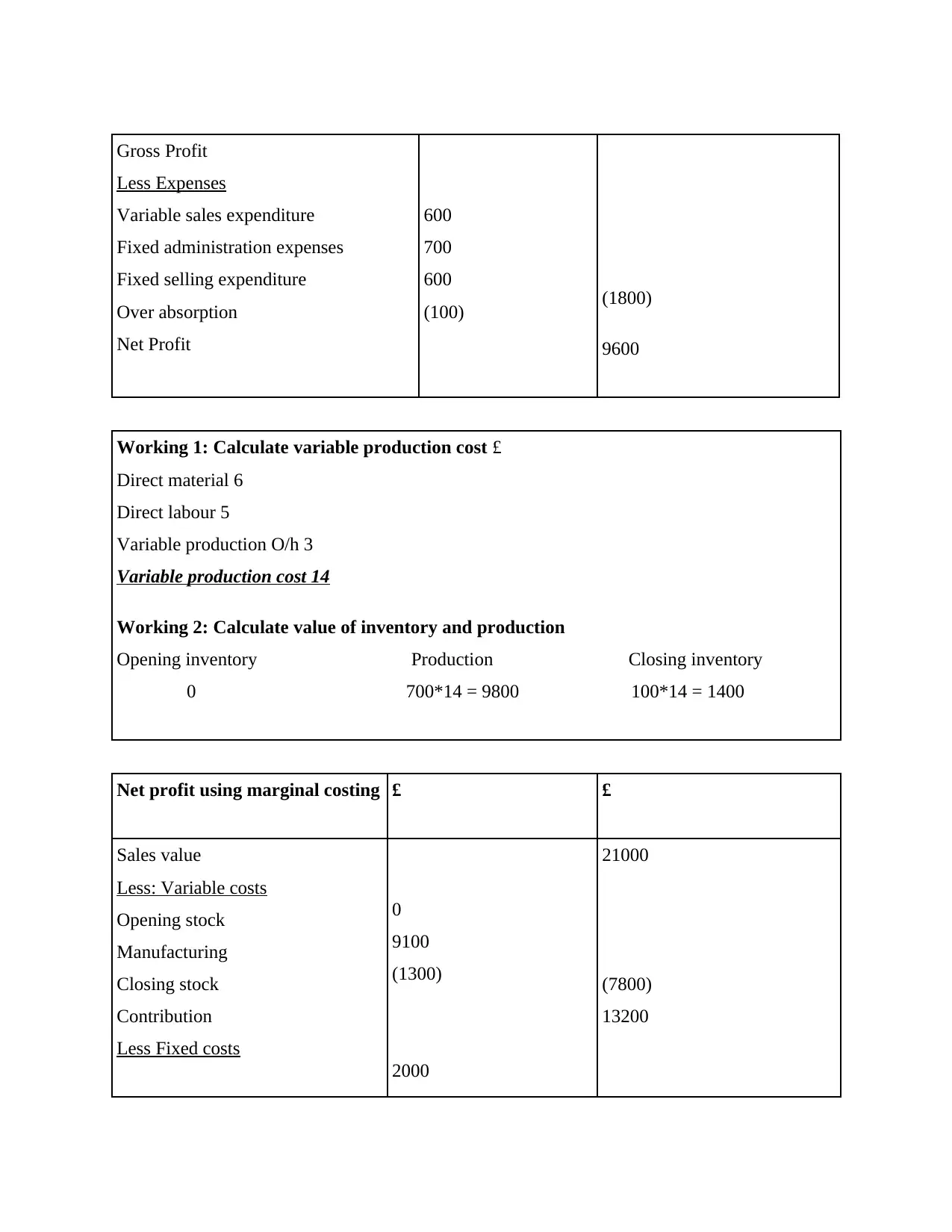

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100) (1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

0

9100

(1300)

2000

21000

(7800)

13200

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100) (1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

0

9100

(1300)

2000

21000

(7800)

13200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.