Management Accounting Report: Systems, Techniques, and Problem Solving

VerifiedAdded on 2022/12/30

|17

|4978

|63

Report

AI Summary

This report on management accounting, prepared for MSD Lighting Ltd., covers various aspects of management accounting systems, including cost accounting, inventory management, and job costing. It explores different methods for management accounting reporting, such as performance reports, budget reports, and inventory management reports. The report delves into marginal and absorption costing for preparing income statements, analyzing their applications, and presents reconciliation statements. It also examines planning tools and their advantages and disadvantages, as well as methods for adopting management accounting systems to solve financial problems, ultimately aiming to achieve sustainable success. The report concludes by integrating these elements to offer a comprehensive understanding of management accounting's role in organizational decision-making and financial management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Different types of management accounting system and their essential requirements:..........3

P2: Different methods for management accounting reporting:....................................................5

M1: Benefits of management accounting system and their application within an organisation: 6

D1: How management accounting system and management accounting reports are integrated

within an organisation:.................................................................................................................6

TASK 2............................................................................................................................................7

P3: Marginal and absorption costing for preparing income statements:......................................7

M2: Range of management accounting techniques for financial reporting:..............................10

D2: Explanation of financial reports in range of business activities:........................................10

TASK 3..........................................................................................................................................10

P4: Planning tools and their advantages and disadvantages:.........................................................10

TASK 4..........................................................................................................................................13

P5: Methods of adopting management accounting system for solving financial problems:.....13

M4: Analyse financial problems in management accounting can lead organisation to

sustainable success:....................................................................................................................15

D3: planning tools helps in order to solving financial problems:..............................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Different types of management accounting system and their essential requirements:..........3

P2: Different methods for management accounting reporting:....................................................5

M1: Benefits of management accounting system and their application within an organisation: 6

D1: How management accounting system and management accounting reports are integrated

within an organisation:.................................................................................................................6

TASK 2............................................................................................................................................7

P3: Marginal and absorption costing for preparing income statements:......................................7

M2: Range of management accounting techniques for financial reporting:..............................10

D2: Explanation of financial reports in range of business activities:........................................10

TASK 3..........................................................................................................................................10

P4: Planning tools and their advantages and disadvantages:.........................................................10

TASK 4..........................................................................................................................................13

P5: Methods of adopting management accounting system for solving financial problems:.....13

M4: Analyse financial problems in management accounting can lead organisation to

sustainable success:....................................................................................................................15

D3: planning tools helps in order to solving financial problems:..............................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management is the process of preparing reports and managing things for the organisation

which helps managers for making firms short term and long term decisions. It helps business for

identifying, measuring, analysing, interpreting, budgeting, communicating organisations

information to managers. Management helps firms to organise its resources in such way so that

firm can accomplish its objectives effectively and efficiently. It is duty of managers that they

assess performance of employees and making them successful. Management has functions which

includes planning, organising, analysing, coordinating, directing, budgeting etc. These functions

helps management for assessing organisational activities in order to accomplish organisations

objectives. Management accounting helps in overview of company finance and resource flow for

decision making. It helps in arranging resources of production, assembles and organizes,

integrates resources in effective manner in order to accomplish objectives (Bromwich and

Scapens, 2016). The company which is selected for this report is MSD Lighting Ltd. It is light

manufacturing company, headquarter situated UK. This report covers topics such as management

accounting system and essential requirements of this, methods of management accounting

reports, marginal and absorption costing in order to cost analysis. Apart from this it also covers

topics such as disadvantages and advantages of different types of planning tools and how

organisation adapting management accounting system in respond to financial problems.

TASK 1

P1: Different types of management accounting system and their essential requirements:

Management accounting is the process of providing information to the higher authorities

for short term and long term decision making (Cooper, Ezzamel and Qu, 2017). In management

accounting there are various systems which includes cost accounting system, inventory

management system, job costing system, price optimisation system. These systems are

mentioned below:

Cost accounting system: This system helps managers for tracking costs involves in its

production process. It is using for known costs of each activity which indicates which

resource is beneficial and which is not MSD Lighting Ltd. as manufacturing company it

is important to know the costs involves in its production process and helps in identify

excessive costs so that they can take decisions regarding reducing the costs.

Management is the process of preparing reports and managing things for the organisation

which helps managers for making firms short term and long term decisions. It helps business for

identifying, measuring, analysing, interpreting, budgeting, communicating organisations

information to managers. Management helps firms to organise its resources in such way so that

firm can accomplish its objectives effectively and efficiently. It is duty of managers that they

assess performance of employees and making them successful. Management has functions which

includes planning, organising, analysing, coordinating, directing, budgeting etc. These functions

helps management for assessing organisational activities in order to accomplish organisations

objectives. Management accounting helps in overview of company finance and resource flow for

decision making. It helps in arranging resources of production, assembles and organizes,

integrates resources in effective manner in order to accomplish objectives (Bromwich and

Scapens, 2016). The company which is selected for this report is MSD Lighting Ltd. It is light

manufacturing company, headquarter situated UK. This report covers topics such as management

accounting system and essential requirements of this, methods of management accounting

reports, marginal and absorption costing in order to cost analysis. Apart from this it also covers

topics such as disadvantages and advantages of different types of planning tools and how

organisation adapting management accounting system in respond to financial problems.

TASK 1

P1: Different types of management accounting system and their essential requirements:

Management accounting is the process of providing information to the higher authorities

for short term and long term decision making (Cooper, Ezzamel and Qu, 2017). In management

accounting there are various systems which includes cost accounting system, inventory

management system, job costing system, price optimisation system. These systems are

mentioned below:

Cost accounting system: This system helps managers for tracking costs involves in its

production process. It is using for known costs of each activity which indicates which

resource is beneficial and which is not MSD Lighting Ltd. as manufacturing company it

is important to know the costs involves in its production process and helps in identify

excessive costs so that they can take decisions regarding reducing the costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Essential requirements:

It is important for the eliminating excessive expenses so that it can generate higher

probability.

This helps organisation for identifying different types of costs so that it can find out the

problems and solutions for these (Drury, 2018).

Inventory accounting system: In this system, it helps managers for identifying

inventory and tracking inventory management how the company manages its stock

orders. How the company manages its outward and inwards by movement of stock

orders. It also considers its storage, ordering costs whether it is managed in proper way or

not. By assessing inventory management firm using various approaches so that it can

manage it effectively and efficiently (Langfield-Smith, Thorne and Hilton, 2018).

In this system, organisations using different methods for assessing inventory management

. These techniques includes LIFO, FIFO, Weighted average costs etc. it is important so

that level of inventory can be assessed effectively and efficiently (Lavia López and Hiebl,

2016).

This is used for reduction of unnecessary things and inefficiency in wastage of resources

and helps In enhancement of overall level of profits.

Job accounting system: This is related to tracking of costs associated with specific

production and services. This information is required in order to track the information to

the customers which are under contract where the costs are reimbursed. This helps

management for tracking costs involved in every process of goods and services which

gives it profitability.

Essential requirements:

In this techniques is using for identifying job costing. It should be update the frequent and

latest changes in job costing. It is essentially required for accurate profitability reports

about the individuals operations.

It is required for knowing employment performance, indirect costs measurement, costs

monitoring by the manufacturing process (Malina, 2017).

Price optimisation system: This management accounting system is used for tracking

demand variations at different levels and collect the data for costs affection. It is about

costs should be set according to customers satisfaction which can provide probability to

It is important for the eliminating excessive expenses so that it can generate higher

probability.

This helps organisation for identifying different types of costs so that it can find out the

problems and solutions for these (Drury, 2018).

Inventory accounting system: In this system, it helps managers for identifying

inventory and tracking inventory management how the company manages its stock

orders. How the company manages its outward and inwards by movement of stock

orders. It also considers its storage, ordering costs whether it is managed in proper way or

not. By assessing inventory management firm using various approaches so that it can

manage it effectively and efficiently (Langfield-Smith, Thorne and Hilton, 2018).

In this system, organisations using different methods for assessing inventory management

. These techniques includes LIFO, FIFO, Weighted average costs etc. it is important so

that level of inventory can be assessed effectively and efficiently (Lavia López and Hiebl,

2016).

This is used for reduction of unnecessary things and inefficiency in wastage of resources

and helps In enhancement of overall level of profits.

Job accounting system: This is related to tracking of costs associated with specific

production and services. This information is required in order to track the information to

the customers which are under contract where the costs are reimbursed. This helps

management for tracking costs involved in every process of goods and services which

gives it profitability.

Essential requirements:

In this techniques is using for identifying job costing. It should be update the frequent and

latest changes in job costing. It is essentially required for accurate profitability reports

about the individuals operations.

It is required for knowing employment performance, indirect costs measurement, costs

monitoring by the manufacturing process (Malina, 2017).

Price optimisation system: This management accounting system is used for tracking

demand variations at different levels and collect the data for costs affection. It is about

costs should be set according to customers satisfaction which can provide probability to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company. In context to MSD Lighting Ltd. It is about how the change in demand and

prices leads to improve profits. It is company assess for how the customers respond to its

different prices for the goods and services.

Essential requirements:

The essential requirements for this it provides opportunities to the company for focusing

on various goals including margin of sales and the number of conversions (Ostaev And

et. al., 2019).

This is require for better and quick decisions and maintaining consistency for the

company. It helps organisation for meet customers needs and maintain firms probability.

P2: Different methods for management accounting reporting:

Management accounting reporting: It is different from financial accounting which

helps in produces reports for the company's internal shareholders for opposed to its external

shareholders. It is about providing information related to the firms different activities so that it

can provide to the external parties such as shareholders so that they can investment in the

company. By this various departments of the firm collects data from tracking key performance

indicators.

Performance reports: It is the report which indicates performance bout the something. It

is about collecting information about the firm for the proper utilisation of resources and

provide this information to the stake holders which is including in performance report. It

report considers information related to the activities of employees conducting in

manufacturing process (Schaltegger, 2018). This is about clear picture of the organisation

that can be find firms weaknesses and works on it. In context to MSD Lighting Ltd. it is

beneficial for the company as it provides the performance data and achieved goals by

employees, this will increase morale of the employees and increase the productivity of

the company which leads to higher profitability.

Budget reports: Every company makes budget for assessing its actual performance with

expected performance. It is helps in assessing which activity gives higher expenditure

and how can control it according to expected budget level. In context to MSD Lighting

Ltd. The budget report helps firm to manage its activities expenses and income so that

actual performance of the company can be measured by expected results.

prices leads to improve profits. It is company assess for how the customers respond to its

different prices for the goods and services.

Essential requirements:

The essential requirements for this it provides opportunities to the company for focusing

on various goals including margin of sales and the number of conversions (Ostaev And

et. al., 2019).

This is require for better and quick decisions and maintaining consistency for the

company. It helps organisation for meet customers needs and maintain firms probability.

P2: Different methods for management accounting reporting:

Management accounting reporting: It is different from financial accounting which

helps in produces reports for the company's internal shareholders for opposed to its external

shareholders. It is about providing information related to the firms different activities so that it

can provide to the external parties such as shareholders so that they can investment in the

company. By this various departments of the firm collects data from tracking key performance

indicators.

Performance reports: It is the report which indicates performance bout the something. It

is about collecting information about the firm for the proper utilisation of resources and

provide this information to the stake holders which is including in performance report. It

report considers information related to the activities of employees conducting in

manufacturing process (Schaltegger, 2018). This is about clear picture of the organisation

that can be find firms weaknesses and works on it. In context to MSD Lighting Ltd. it is

beneficial for the company as it provides the performance data and achieved goals by

employees, this will increase morale of the employees and increase the productivity of

the company which leads to higher profitability.

Budget reports: Every company makes budget for assessing its actual performance with

expected performance. It is helps in assessing which activity gives higher expenditure

and how can control it according to expected budget level. In context to MSD Lighting

Ltd. The budget report helps firm to manage its activities expenses and income so that

actual performance of the company can be measured by expected results.

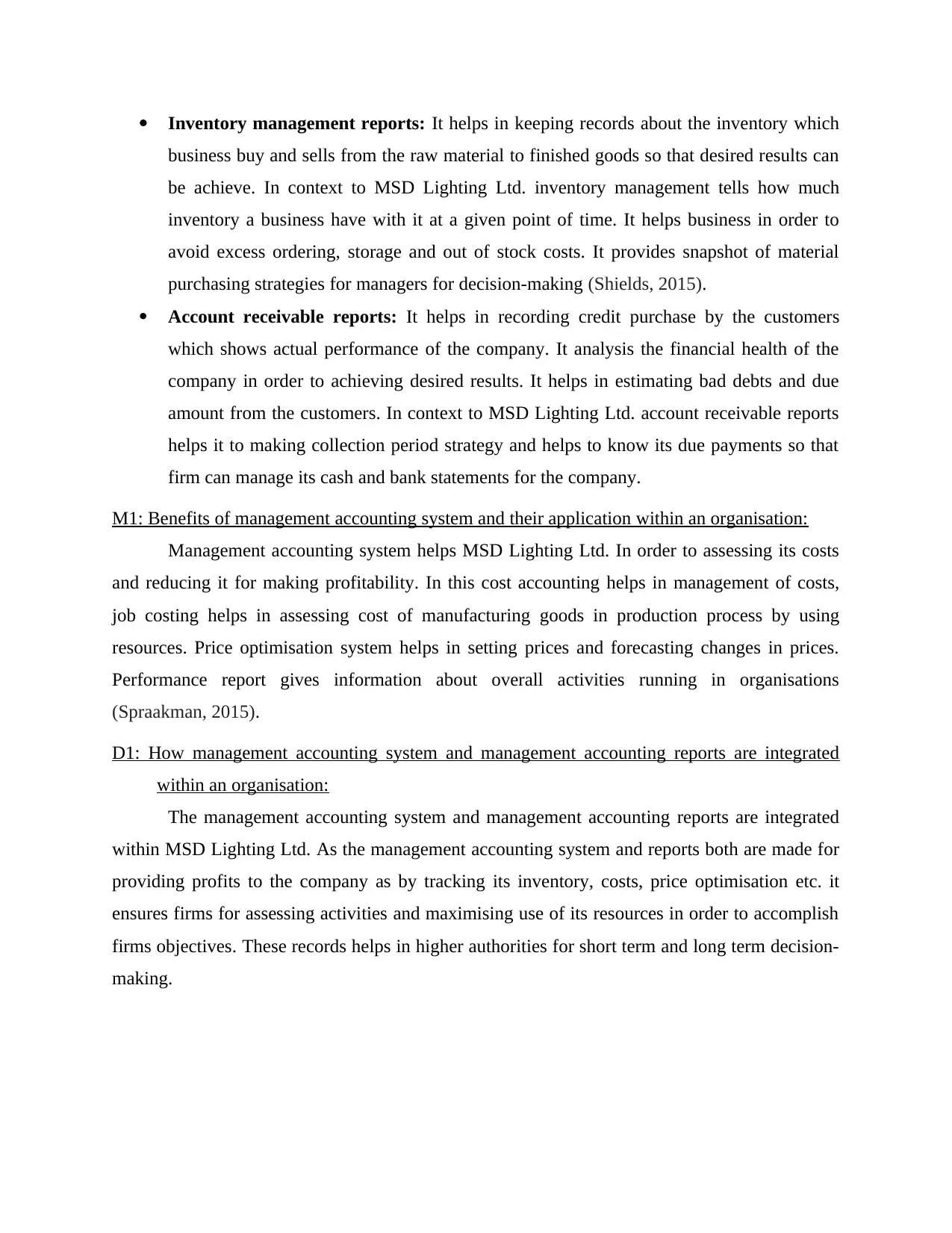

Inventory management reports: It helps in keeping records about the inventory which

business buy and sells from the raw material to finished goods so that desired results can

be achieve. In context to MSD Lighting Ltd. inventory management tells how much

inventory a business have with it at a given point of time. It helps business in order to

avoid excess ordering, storage and out of stock costs. It provides snapshot of material

purchasing strategies for managers for decision-making (Shields, 2015).

Account receivable reports: It helps in recording credit purchase by the customers

which shows actual performance of the company. It analysis the financial health of the

company in order to achieving desired results. It helps in estimating bad debts and due

amount from the customers. In context to MSD Lighting Ltd. account receivable reports

helps it to making collection period strategy and helps to know its due payments so that

firm can manage its cash and bank statements for the company.

M1: Benefits of management accounting system and their application within an organisation:

Management accounting system helps MSD Lighting Ltd. In order to assessing its costs

and reducing it for making profitability. In this cost accounting helps in management of costs,

job costing helps in assessing cost of manufacturing goods in production process by using

resources. Price optimisation system helps in setting prices and forecasting changes in prices.

Performance report gives information about overall activities running in organisations

(Spraakman, 2015).

D1: How management accounting system and management accounting reports are integrated

within an organisation:

The management accounting system and management accounting reports are integrated

within MSD Lighting Ltd. As the management accounting system and reports both are made for

providing profits to the company as by tracking its inventory, costs, price optimisation etc. it

ensures firms for assessing activities and maximising use of its resources in order to accomplish

firms objectives. These records helps in higher authorities for short term and long term decision-

making.

business buy and sells from the raw material to finished goods so that desired results can

be achieve. In context to MSD Lighting Ltd. inventory management tells how much

inventory a business have with it at a given point of time. It helps business in order to

avoid excess ordering, storage and out of stock costs. It provides snapshot of material

purchasing strategies for managers for decision-making (Shields, 2015).

Account receivable reports: It helps in recording credit purchase by the customers

which shows actual performance of the company. It analysis the financial health of the

company in order to achieving desired results. It helps in estimating bad debts and due

amount from the customers. In context to MSD Lighting Ltd. account receivable reports

helps it to making collection period strategy and helps to know its due payments so that

firm can manage its cash and bank statements for the company.

M1: Benefits of management accounting system and their application within an organisation:

Management accounting system helps MSD Lighting Ltd. In order to assessing its costs

and reducing it for making profitability. In this cost accounting helps in management of costs,

job costing helps in assessing cost of manufacturing goods in production process by using

resources. Price optimisation system helps in setting prices and forecasting changes in prices.

Performance report gives information about overall activities running in organisations

(Spraakman, 2015).

D1: How management accounting system and management accounting reports are integrated

within an organisation:

The management accounting system and management accounting reports are integrated

within MSD Lighting Ltd. As the management accounting system and reports both are made for

providing profits to the company as by tracking its inventory, costs, price optimisation etc. it

ensures firms for assessing activities and maximising use of its resources in order to accomplish

firms objectives. These records helps in higher authorities for short term and long term decision-

making.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

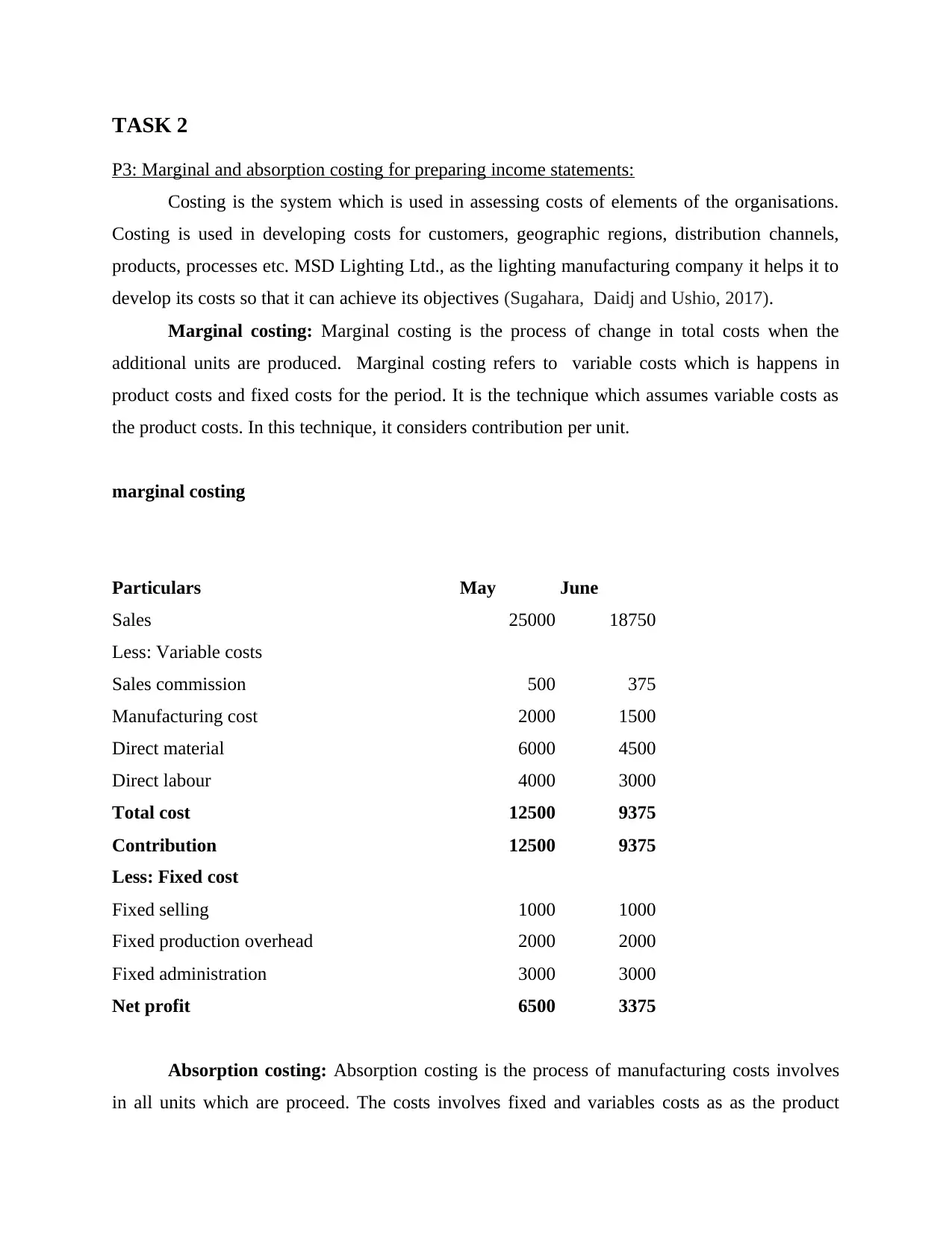

TASK 2

P3: Marginal and absorption costing for preparing income statements:

Costing is the system which is used in assessing costs of elements of the organisations.

Costing is used in developing costs for customers, geographic regions, distribution channels,

products, processes etc. MSD Lighting Ltd., as the lighting manufacturing company it helps it to

develop its costs so that it can achieve its objectives (Sugahara, Daidj and Ushio, 2017).

Marginal costing: Marginal costing is the process of change in total costs when the

additional units are produced. Marginal costing refers to variable costs which is happens in

product costs and fixed costs for the period. It is the technique which assumes variable costs as

the product costs. In this technique, it considers contribution per unit.

marginal costing

Particulars May June

Sales 25000 18750

Less: Variable costs

Sales commission 500 375

Manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Total cost 12500 9375

Contribution 12500 9375

Less: Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 6500 3375

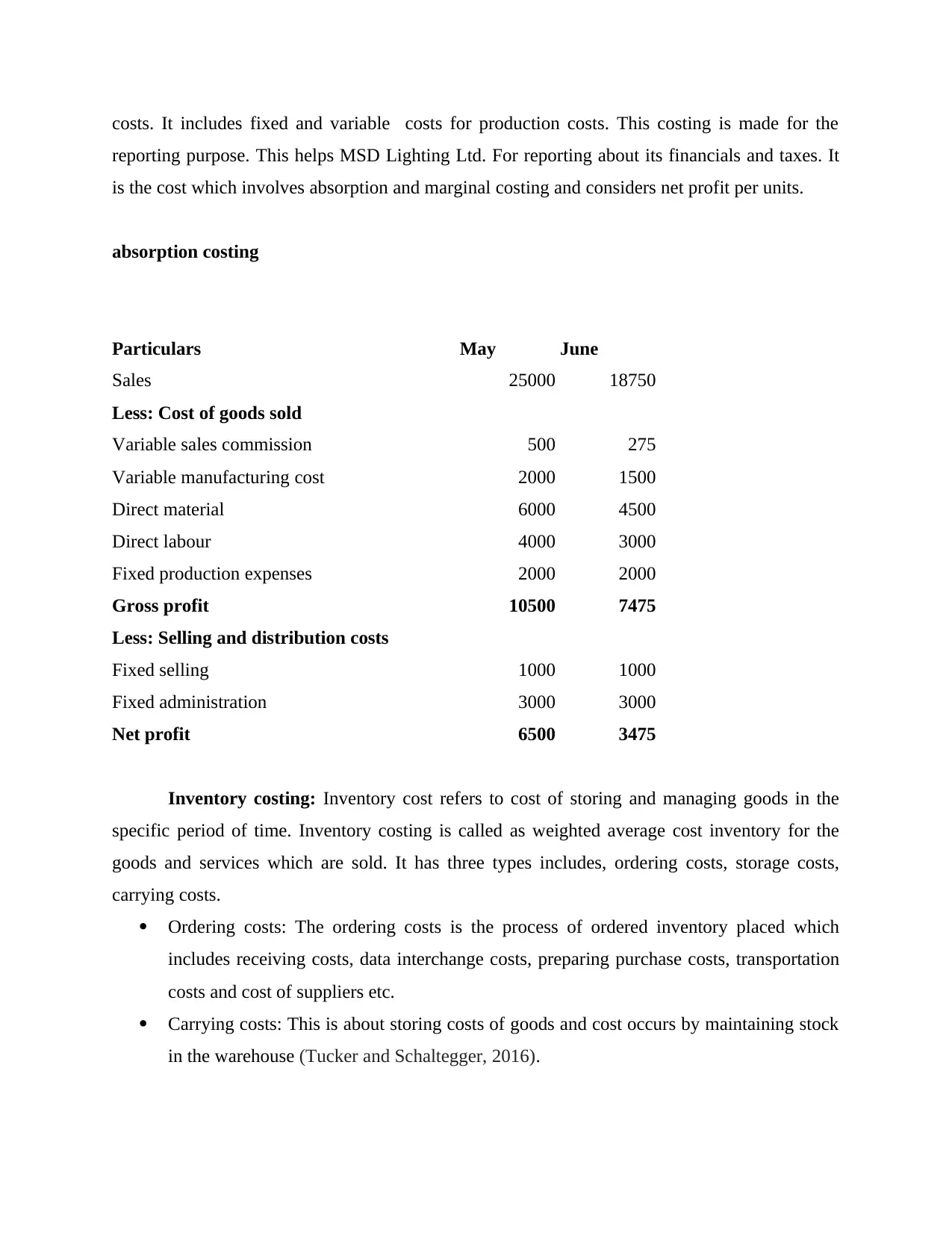

Absorption costing: Absorption costing is the process of manufacturing costs involves

in all units which are proceed. The costs involves fixed and variables costs as as the product

P3: Marginal and absorption costing for preparing income statements:

Costing is the system which is used in assessing costs of elements of the organisations.

Costing is used in developing costs for customers, geographic regions, distribution channels,

products, processes etc. MSD Lighting Ltd., as the lighting manufacturing company it helps it to

develop its costs so that it can achieve its objectives (Sugahara, Daidj and Ushio, 2017).

Marginal costing: Marginal costing is the process of change in total costs when the

additional units are produced. Marginal costing refers to variable costs which is happens in

product costs and fixed costs for the period. It is the technique which assumes variable costs as

the product costs. In this technique, it considers contribution per unit.

marginal costing

Particulars May June

Sales 25000 18750

Less: Variable costs

Sales commission 500 375

Manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Total cost 12500 9375

Contribution 12500 9375

Less: Fixed cost

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 6500 3375

Absorption costing: Absorption costing is the process of manufacturing costs involves

in all units which are proceed. The costs involves fixed and variables costs as as the product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costs. It includes fixed and variable costs for production costs. This costing is made for the

reporting purpose. This helps MSD Lighting Ltd. For reporting about its financials and taxes. It

is the cost which involves absorption and marginal costing and considers net profit per units.

absorption costing

Particulars May June

Sales 25000 18750

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Inventory costing: Inventory cost refers to cost of storing and managing goods in the

specific period of time. Inventory costing is called as weighted average cost inventory for the

goods and services which are sold. It has three types includes, ordering costs, storage costs,

carrying costs.

Ordering costs: The ordering costs is the process of ordered inventory placed which

includes receiving costs, data interchange costs, preparing purchase costs, transportation

costs and cost of suppliers etc.

Carrying costs: This is about storing costs of goods and cost occurs by maintaining stock

in the warehouse (Tucker and Schaltegger, 2016).

reporting purpose. This helps MSD Lighting Ltd. For reporting about its financials and taxes. It

is the cost which involves absorption and marginal costing and considers net profit per units.

absorption costing

Particulars May June

Sales 25000 18750

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Inventory costing: Inventory cost refers to cost of storing and managing goods in the

specific period of time. Inventory costing is called as weighted average cost inventory for the

goods and services which are sold. It has three types includes, ordering costs, storage costs,

carrying costs.

Ordering costs: The ordering costs is the process of ordered inventory placed which

includes receiving costs, data interchange costs, preparing purchase costs, transportation

costs and cost of suppliers etc.

Carrying costs: This is about storing costs of goods and cost occurs by maintaining stock

in the warehouse (Tucker and Schaltegger, 2016).

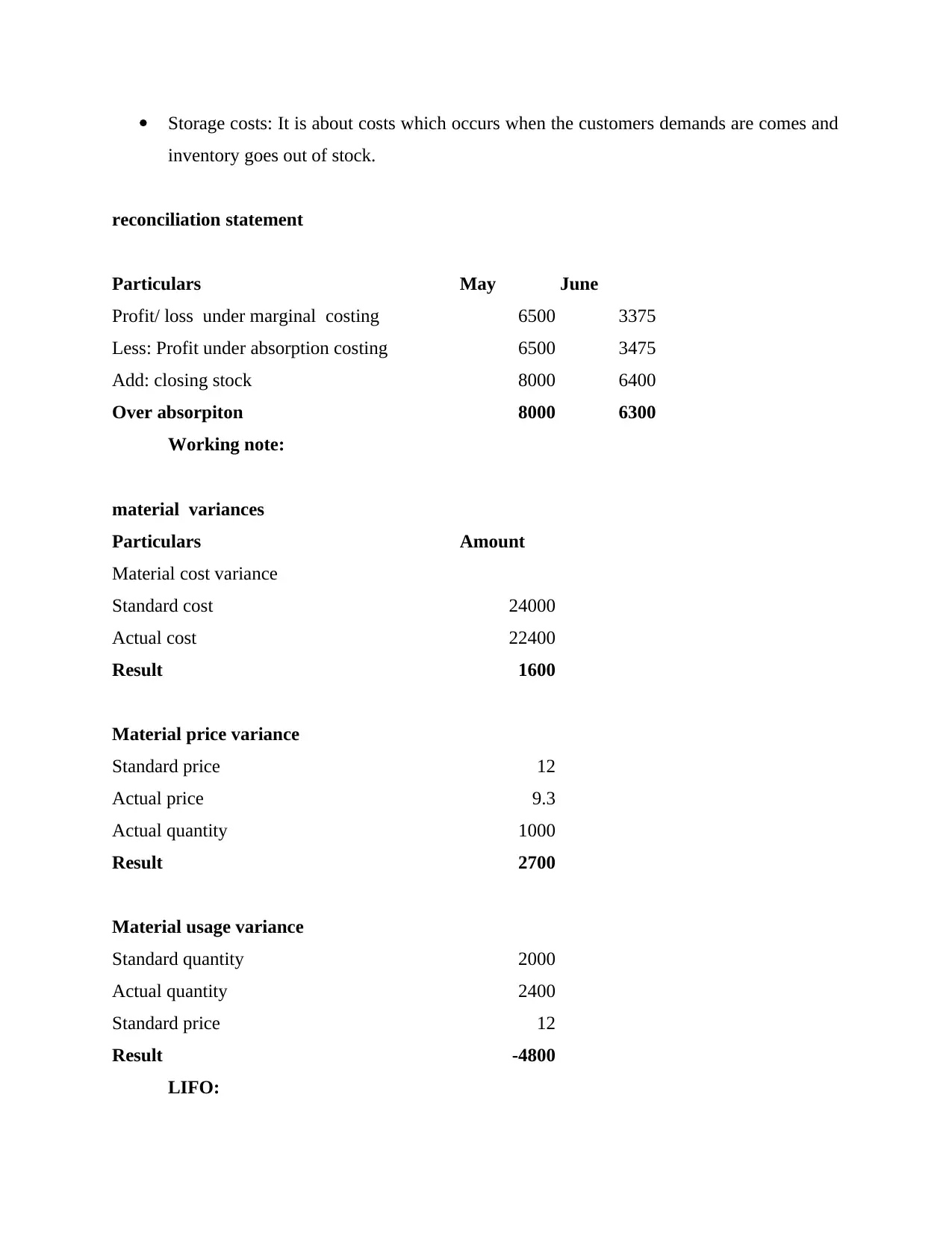

Storage costs: It is about costs which occurs when the customers demands are comes and

inventory goes out of stock.

reconciliation statement

Particulars May June

Profit/ loss under marginal costing 6500 3375

Less: Profit under absorption costing 6500 3475

Add: closing stock 8000 6400

Over absorpiton 8000 6300

Working note:

material variances

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

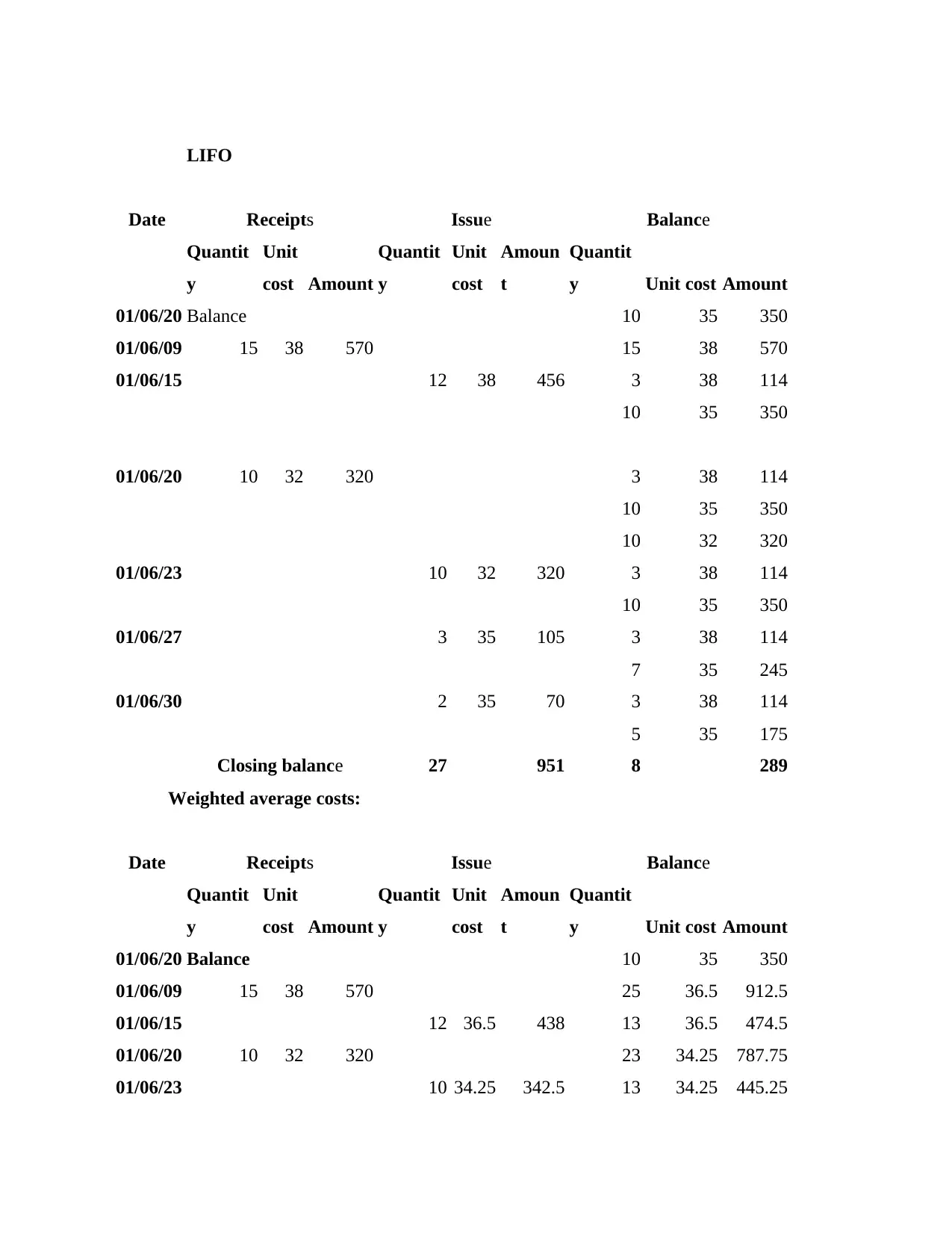

LIFO:

inventory goes out of stock.

reconciliation statement

Particulars May June

Profit/ loss under marginal costing 6500 3375

Less: Profit under absorption costing 6500 3475

Add: closing stock 8000 6400

Over absorpiton 8000 6300

Working note:

material variances

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

Result 2700

Material usage variance

Standard quantity 2000

Actual quantity 2400

Standard price 12

Result -4800

LIFO:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LIFO

Date Receipts Issue Balance

Quantit

y

Unit

cost Amount

Quantit

y

Unit

cost

Amoun

t

Quantit

y Unit cost Amount

01/06/20 Balance 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

Closing balance 27 951 8 289

Weighted average costs:

Date Receipts Issue Balance

Quantit

y

Unit

cost Amount

Quantit

y

Unit

cost

Amoun

t

Quantit

y Unit cost Amount

01/06/20 Balance 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

Date Receipts Issue Balance

Quantit

y

Unit

cost Amount

Quantit

y

Unit

cost

Amoun

t

Quantit

y Unit cost Amount

01/06/20 Balance 10 35 350

01/06/09 15 38 570 15 38 570

01/06/15 12 38 456 3 38 114

10 35 350

01/06/20 10 32 320 3 38 114

10 35 350

10 32 320

01/06/23 10 32 320 3 38 114

10 35 350

01/06/27 3 35 105 3 38 114

7 35 245

01/06/30 2 35 70 3 38 114

5 35 175

Closing balance 27 951 8 289

Weighted average costs:

Date Receipts Issue Balance

Quantit

y

Unit

cost Amount

Quantit

y

Unit

cost

Amoun

t

Quantit

y Unit cost Amount

01/06/20 Balance 10 35 350

01/06/09 15 38 570 25 36.5 912.5

01/06/15 12 36.5 438 13 36.5 474.5

01/06/20 10 32 320 23 34.25 787.75

01/06/23 10 34.25 342.5 13 34.25 445.25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

01/06/27 3 34.25 102.75 10 34.25 342.5

01/06/30 Closing balance 2 34.25 68.5 8 34.25 274

M2: Range of management accounting techniques for financial reporting:

Costing is essential requirement for any organisation as it provides costing of production

goods and services. Costs plays vital role in profitability of the firms. It helps firm in order to

know its productivity and profitability by the better use of its resources. Costing has two types

absorption costing and marginal costing. Absorption costing is refers to cost of all produced

goods and services in the organisation. Marginal costing refers to costs of each extra units which

is produced by the company.

D2: Explanation of financial reports in range of business activities:

As per the above data it shows all costs involved in manufacturing process such as

absorption cost, marginal costs, inventory costs etc. According to this, in absorption costing net

profits shows 6500 in may and 3475 in June. Marginal costing, it shows in may 6500 and 3375 in

June. As per its bank reconciliation it shows over absorption in may as 8000 and June as 6300.

As per LIFO method of inventory valuation it shows balance of 289 while weighted average

method shows 274 in its balance.

TASK 3

P4: Planning tools and their advantages and disadvantages:

Budgeting is the process of making plans about the firms spendings. It is the pre

estimation of expenses and income which are occurs from firms activities. It helps in comparing

actual performance with expected performance of the company. In context to, MSD Lighting

Ltd., firms financials department makes budget for their activities which are running in

organisation. It is made for achieving goals by strategic plans (Van der Stede, 2015). Budget

involves sales, operating expenses, income for the company which occurred by its manufacturing

activities. It provides roadmap to the employees so that they can manage activities by efficient

utilisation of resources. It helps managers for fund management and arrangement of money for

running business activities. It helps in forecasting how much money firm has to manage in the

future. In context to MSD lighting Ltd. Firm makes budget for forecasting firms performance so

that it ensures that firm has enough money for the activities.

01/06/30 Closing balance 2 34.25 68.5 8 34.25 274

M2: Range of management accounting techniques for financial reporting:

Costing is essential requirement for any organisation as it provides costing of production

goods and services. Costs plays vital role in profitability of the firms. It helps firm in order to

know its productivity and profitability by the better use of its resources. Costing has two types

absorption costing and marginal costing. Absorption costing is refers to cost of all produced

goods and services in the organisation. Marginal costing refers to costs of each extra units which

is produced by the company.

D2: Explanation of financial reports in range of business activities:

As per the above data it shows all costs involved in manufacturing process such as

absorption cost, marginal costs, inventory costs etc. According to this, in absorption costing net

profits shows 6500 in may and 3475 in June. Marginal costing, it shows in may 6500 and 3375 in

June. As per its bank reconciliation it shows over absorption in may as 8000 and June as 6300.

As per LIFO method of inventory valuation it shows balance of 289 while weighted average

method shows 274 in its balance.

TASK 3

P4: Planning tools and their advantages and disadvantages:

Budgeting is the process of making plans about the firms spendings. It is the pre

estimation of expenses and income which are occurs from firms activities. It helps in comparing

actual performance with expected performance of the company. In context to, MSD Lighting

Ltd., firms financials department makes budget for their activities which are running in

organisation. It is made for achieving goals by strategic plans (Van der Stede, 2015). Budget

involves sales, operating expenses, income for the company which occurred by its manufacturing

activities. It provides roadmap to the employees so that they can manage activities by efficient

utilisation of resources. It helps managers for fund management and arrangement of money for

running business activities. It helps in forecasting how much money firm has to manage in the

future. In context to MSD lighting Ltd. Firm makes budget for forecasting firms performance so

that it ensures that firm has enough money for the activities.

It estimates expenditures, revenues which helps company bin its manufacturing process,

inventory details, fund arrangement, pricing, managing activities. From this managers can review

performance of the employees if there are any problem than they can takes actions towards them.

Budgeting ensures that money is allocated in those resources which are comes under in firms

strategic objectives.

Cash budget: Cash budget is the planning of expected cash receipts and payments during

the specific period of time. Cash outflows and inflows includes revenues, expenses,

loans receipts and payments. It is the pre estimation of firms position in the future. It

ensures firm that it has enough cash for running its activities.

Advantages Disadvantages

Cash budget is helpful in avoiding debts,

regulate expenses, it use to show deficits and

surplus etc.

Cash budget is not prefer by them those deals

with flexibility. In context to MSD lighting ltd.

It creates disadvantage of the for the managers

as it provides only cash related informations.

Capital budget: It is the process of which business use to assess fixed assets

investments. It is used to evaluating potential major investments which company makes

for future growth. Example of this, as construction of new building, machinery purchase,

new product line which gives future benefits to the company. It has various techniques

for knowing which investment option is better which provides higher return in the future

to the MSD lighting ltd.

Advantages Disadvantages

Capital budget helps in understanding risks and

returns involved in investments. It helps in

increase shareholders wealth and advantages in

the market.

This helps in long term decisions, in this

techniques are assumed.

Production budget: It is about calculating number of units of the goods that business

must be manufactured and derived from the sales. In context to MSD lighting ltd., it

inventory details, fund arrangement, pricing, managing activities. From this managers can review

performance of the employees if there are any problem than they can takes actions towards them.

Budgeting ensures that money is allocated in those resources which are comes under in firms

strategic objectives.

Cash budget: Cash budget is the planning of expected cash receipts and payments during

the specific period of time. Cash outflows and inflows includes revenues, expenses,

loans receipts and payments. It is the pre estimation of firms position in the future. It

ensures firm that it has enough cash for running its activities.

Advantages Disadvantages

Cash budget is helpful in avoiding debts,

regulate expenses, it use to show deficits and

surplus etc.

Cash budget is not prefer by them those deals

with flexibility. In context to MSD lighting ltd.

It creates disadvantage of the for the managers

as it provides only cash related informations.

Capital budget: It is the process of which business use to assess fixed assets

investments. It is used to evaluating potential major investments which company makes

for future growth. Example of this, as construction of new building, machinery purchase,

new product line which gives future benefits to the company. It has various techniques

for knowing which investment option is better which provides higher return in the future

to the MSD lighting ltd.

Advantages Disadvantages

Capital budget helps in understanding risks and

returns involved in investments. It helps in

increase shareholders wealth and advantages in

the market.

This helps in long term decisions, in this

techniques are assumed.

Production budget: It is about calculating number of units of the goods that business

must be manufactured and derived from the sales. In context to MSD lighting ltd., it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.