Unit 5 Management Accounting Report: Creams Ltd Analysis

VerifiedAdded on 2023/01/11

|21

|5930

|54

Report

AI Summary

This report delves into the core concepts and practical applications of management accounting within the context of Creams Ltd, a UK-based company. It initiates with an introduction to management accounting, emphasizing its significance in strategic planning and decision-making. The report then explores various management accounting systems, including cost accounting, price optimization, and inventory management, evaluating their benefits and essential requirements. Different management accounting reporting methods, such as performance reports, budget reports, and cost managerial accounting reports, are examined. Furthermore, the report analyzes the integration of management accounting systems and reporting within organizational processes. It also discusses cost calculation techniques and the role of financial reports in interpreting business activities. The report further assesses planning tools for budgetary control, comparing their advantages and disadvantages, and examines how organizations apply management accounting to address financial challenges. The report concludes by summarizing the key findings and implications of management accounting practices for businesses like Creams Ltd.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting and different types of system........................................................3

P2: Different method for management accounting reporting. ...................................................5

M1. Evaluation of benefits of various management accounting systems...................................6

D1 Management accounting system and management accounting reporting are integrated

with organisation process. ..........................................................................................................7

TASK 2............................................................................................................................................7

P3: Calculation of costs by using appropriate techniques...........................................................7

M2: Management accounting techniques and financial reporting documents..........................10

D2. Financial reports which applies to interpret many business activities...............................11

TASK 3..........................................................................................................................................11

P4. Advantages and disadvantages of different types of planning tools of budgetary control. 11

M3. Usage of different planning tools for preparing and forecasting budgets.........................14

TASK 4..........................................................................................................................................15

P5. Management accounting systems for responding to financial problems............................15

M4. Management accounting in response to financial problems..............................................17

D3 Various planning tools to resolve financial problems.........................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting and different types of system........................................................3

P2: Different method for management accounting reporting. ...................................................5

M1. Evaluation of benefits of various management accounting systems...................................6

D1 Management accounting system and management accounting reporting are integrated

with organisation process. ..........................................................................................................7

TASK 2............................................................................................................................................7

P3: Calculation of costs by using appropriate techniques...........................................................7

M2: Management accounting techniques and financial reporting documents..........................10

D2. Financial reports which applies to interpret many business activities...............................11

TASK 3..........................................................................................................................................11

P4. Advantages and disadvantages of different types of planning tools of budgetary control. 11

M3. Usage of different planning tools for preparing and forecasting budgets.........................14

TASK 4..........................................................................................................................................15

P5. Management accounting systems for responding to financial problems............................15

M4. Management accounting in response to financial problems..............................................17

D3 Various planning tools to resolve financial problems.........................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

2

INTRODUCTION

Management accounting is a very crucial component for an organisation in developing plans

and strategies for accomplishing their desired goals. Through this component, firms develop their

reports for taking effective decisions in order to ensure the successful implementation of

strategies and plans. Accounting managers has the roles and responsibilities for managing the

accounting activities so that organisational operations can run smoothly without any issues. It

helps an organisation to maintain their strong financial stability in competitive market

environment by preparing financial accounts such as profit and loss a/cs, balance sheet, and cash

flow statement. The taken firm for this assessment is Creams Ltd which is providing ice creams,

doughnuts, waffles etc. to their customers across UK. This report will discuss the management

accounting systems along with the methods used for management accounting reporting. Along

with this, essential requirements of management accounting systems are also discussed under

this report. The report also explains the different costing methods such as absorption and

marginal costing methods so that the management of Creams Ltd. can decide the selection of

method according to their business objectives. Further, the advantages and disadvantages for

different type of planning tool will be discussed used for budgetary control. This report will also

discuss the comparison of how organisations are adopting management accounting systems for

responding to their financial problems.

TASK 1

P1: Management accounting and different types of system.

Management accounting is the procedure of managing the different aspects of an

organisation by developing the reports. This concept is very beneficial for the business

organisations in developing effective strategies and plans through which objectives can be

achieved in future time of period. This method is not compulsory for the organisation but it can

be used in needy times for enhancing the efficiency and reducing the errors. There are various

types of management accounting systems which can be used by the firms as discussed below:

Cost accounting system: This system is beneficial for the organisations in determining their

various costs such as fixed, variable cost etc. The determination of these costs for their products

and services assist the firms in determining their profit and loss as they can keep an eye on the

expected and obtained results for determining the performance of their offerings. Creams ltd. Is a

3

Management accounting is a very crucial component for an organisation in developing plans

and strategies for accomplishing their desired goals. Through this component, firms develop their

reports for taking effective decisions in order to ensure the successful implementation of

strategies and plans. Accounting managers has the roles and responsibilities for managing the

accounting activities so that organisational operations can run smoothly without any issues. It

helps an organisation to maintain their strong financial stability in competitive market

environment by preparing financial accounts such as profit and loss a/cs, balance sheet, and cash

flow statement. The taken firm for this assessment is Creams Ltd which is providing ice creams,

doughnuts, waffles etc. to their customers across UK. This report will discuss the management

accounting systems along with the methods used for management accounting reporting. Along

with this, essential requirements of management accounting systems are also discussed under

this report. The report also explains the different costing methods such as absorption and

marginal costing methods so that the management of Creams Ltd. can decide the selection of

method according to their business objectives. Further, the advantages and disadvantages for

different type of planning tool will be discussed used for budgetary control. This report will also

discuss the comparison of how organisations are adopting management accounting systems for

responding to their financial problems.

TASK 1

P1: Management accounting and different types of system.

Management accounting is the procedure of managing the different aspects of an

organisation by developing the reports. This concept is very beneficial for the business

organisations in developing effective strategies and plans through which objectives can be

achieved in future time of period. This method is not compulsory for the organisation but it can

be used in needy times for enhancing the efficiency and reducing the errors. There are various

types of management accounting systems which can be used by the firms as discussed below:

Cost accounting system: This system is beneficial for the organisations in determining their

various costs such as fixed, variable cost etc. The determination of these costs for their products

and services assist the firms in determining their profit and loss as they can keep an eye on the

expected and obtained results for determining the performance of their offerings. Creams ltd. Is a

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

small firm due to which it is using this system for checking the costs and other financial data of

their products. Through this, the company is ensuring that focus is given to those products which

are serving the customer needs and proved beneficial for the organisation.

Essential requirements-

Cost Accounting System should be able to provide the organizations with an input

measurement basis. By doing so it will ensure that it is able to identify the right way

through which the measurement of costs can be done. This can help the managers of

Creams Ltd. And the managers are required to ensure this. In a Cost Accounting System there should be the use of techniques through which the

costs can be reduced effectively in the organization. For Creams Ltd. This can be helpful

and the managers must ensure this.

Price optimisation system: This is another system which is used by the business firms for setting

the process of their products and services. This system provides the factors which can impact the

price of the offerings of company. Through this system, companies can analyse the reviews and

feedbacks of the customers regarding the price range so that better decisions can be taken for

ensuring customer satisfaction which will enhance the brand image too. Creams ltd. is also using

this system for setting their prices. This ensures that the prices set by the Creams ltd. will ensure

customer satisfaction and trust as products are provided to them at affordable prices which are

also value based. Along with this, it also helps company to acquiring information about the

actual thoughts of their targeted customers towards their old pricing strategies and make changes

accordingly so as to retain them with company for longer duration.

Essential requirements-

In a price optimization system there should be a systematic use of right methods for

collection of historical data regarding the prices. Therefore this will ensure that Creams

Ltd.'s managers are able to make the correct use of this data. In a price optimization system, there must be a use of varied techniques of setting up

price according to a change in demand level. In this way the management of Creams Ltd.

will be able to identify the right price to be set according to a change in demand level.

Inventory management system: This system is used for managing and tracking the inventories

for an organisation such as products and services. This system is also beneficial for tracking the

status of the offerings provided by company to its customers. Through this system, firms can

4

their products. Through this, the company is ensuring that focus is given to those products which

are serving the customer needs and proved beneficial for the organisation.

Essential requirements-

Cost Accounting System should be able to provide the organizations with an input

measurement basis. By doing so it will ensure that it is able to identify the right way

through which the measurement of costs can be done. This can help the managers of

Creams Ltd. And the managers are required to ensure this. In a Cost Accounting System there should be the use of techniques through which the

costs can be reduced effectively in the organization. For Creams Ltd. This can be helpful

and the managers must ensure this.

Price optimisation system: This is another system which is used by the business firms for setting

the process of their products and services. This system provides the factors which can impact the

price of the offerings of company. Through this system, companies can analyse the reviews and

feedbacks of the customers regarding the price range so that better decisions can be taken for

ensuring customer satisfaction which will enhance the brand image too. Creams ltd. is also using

this system for setting their prices. This ensures that the prices set by the Creams ltd. will ensure

customer satisfaction and trust as products are provided to them at affordable prices which are

also value based. Along with this, it also helps company to acquiring information about the

actual thoughts of their targeted customers towards their old pricing strategies and make changes

accordingly so as to retain them with company for longer duration.

Essential requirements-

In a price optimization system there should be a systematic use of right methods for

collection of historical data regarding the prices. Therefore this will ensure that Creams

Ltd.'s managers are able to make the correct use of this data. In a price optimization system, there must be a use of varied techniques of setting up

price according to a change in demand level. In this way the management of Creams Ltd.

will be able to identify the right price to be set according to a change in demand level.

Inventory management system: This system is used for managing and tracking the inventories

for an organisation such as products and services. This system is also beneficial for tracking the

status of the offerings provided by company to its customers. Through this system, firms can

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

improve their supply chain management. Creams ltd is providing ice cream products to their

customers due to which it is essential for Cream ltd. to streamline their inventory for providing

products in an effective manner. This tool has been proved beneficially for the firm in improving

the gap between supply and demand. Adoption of such kind of system helps Creams Ltd. to

minimise business cost by controlling over storage cost of inventory by ordering whenever

required. This makes easy for company to meet the demands of their loyal clients on due date

which indirectly increases their brand image and reputations in rivalry market.

Essential requirements-

In an Inventory Management System, there should be a use of Inventory Management

Software which manages and tracks the inflows as well as outflows of the stock items

and therefore is able to manage them in a highly effective manner.

Inventory Management System must ensure that the methods like LIFO, FIFO, Weighted

Average Cost etc. can be used so that stock level can be monitored and if there are any

variances and deviations then they can be rectified effectively.

While considering various management accounting system the managers need to take

into consideration various essential requirements such as :

Management style: The organisation follows different styles of management with the

help of which they can define to whom and how to inform and get the results. The

Creams ltd has been taking into consideration the democratic style due to which they

easily adopt different management accounting system.

Organisation structure: It defines the roles and responsibilities of different persona and

the structure in which the people has to work. Creams ltd has been considering

functional structure within their organisation.

P2: Different method for management accounting reporting.

Management accounting of reports is very important for an organisation as these helps in

decision making process. Management accounting is also essential for the business organisations

in taking the decisions regarding the internal information and parts of business. Through these

reports, the business managers can take suitable and effective decisions for implementing the

business strategies so that better output can be obtained (Adler, 2013). The management

accounting reports consist of both monetary and non monetary information. Cream ltd is using

different types of reports which are discussed below:

5

customers due to which it is essential for Cream ltd. to streamline their inventory for providing

products in an effective manner. This tool has been proved beneficially for the firm in improving

the gap between supply and demand. Adoption of such kind of system helps Creams Ltd. to

minimise business cost by controlling over storage cost of inventory by ordering whenever

required. This makes easy for company to meet the demands of their loyal clients on due date

which indirectly increases their brand image and reputations in rivalry market.

Essential requirements-

In an Inventory Management System, there should be a use of Inventory Management

Software which manages and tracks the inflows as well as outflows of the stock items

and therefore is able to manage them in a highly effective manner.

Inventory Management System must ensure that the methods like LIFO, FIFO, Weighted

Average Cost etc. can be used so that stock level can be monitored and if there are any

variances and deviations then they can be rectified effectively.

While considering various management accounting system the managers need to take

into consideration various essential requirements such as :

Management style: The organisation follows different styles of management with the

help of which they can define to whom and how to inform and get the results. The

Creams ltd has been taking into consideration the democratic style due to which they

easily adopt different management accounting system.

Organisation structure: It defines the roles and responsibilities of different persona and

the structure in which the people has to work. Creams ltd has been considering

functional structure within their organisation.

P2: Different method for management accounting reporting.

Management accounting of reports is very important for an organisation as these helps in

decision making process. Management accounting is also essential for the business organisations

in taking the decisions regarding the internal information and parts of business. Through these

reports, the business managers can take suitable and effective decisions for implementing the

business strategies so that better output can be obtained (Adler, 2013). The management

accounting reports consist of both monetary and non monetary information. Cream ltd is using

different types of reports which are discussed below:

5

Performance reports: These reports are developed for measuring and evaluating the

performance of business functions. Performance reports play an essential role in

determining the performance of employees and the business activities so that proper

rewards can be provided to them accordingly. Cream ltd is using the performance reports

for determining the efficiency and performance of their employees. Through this

determination, the company is providing enumeration to the employees so that they can

accomplish their goals in a more effective manner. Budget report: This report is used by the organisation for determining the variation in

expected and obtained performance. Through this, managers can develop better policies

and strategies based on the output obtained through report. This report also estimates the

expenses of the firm for a future time period which will be followed by the departments

and firm. Cream ltd is using this type of report for comparing their obtained financial

efficiency with the targeted goals in order to determine the errors and flaws in strategies.

This is beneficial in improving and implementing the future policies if the current

strategies are giving less output than expected. Accounts receivable ageing report: such type of reports contain the data associated with

the credit transactions of the company. This report is mostly used by the firms which are

making their transactions in credit form. This is beneficial for the firms in determining

the pending amount of customers in the marketplace (Arroyo, 2012). Also these reports

provide the date and time of the credit transactions for quick calculations. Cream ltd is

using this type of reports for determining the amount credited by the customers to the

company for their products.

Cost managerial accounting report: This is also an essential type of report which is used

by companies for tracking the profit and loss from the different organisational functions.

This report is useful in calculating the expenses of products before selling and then

compares these expenses with the total amount of money received from selling of

products. When the total expenses are high then selling amount then the company is

facing loss whereas if the expenses are low then it is profit for the firm. Cream ltd uses

this report for determining their profit and loss and if losses occurs then strategies and

policies are developed accordingly.

6

performance of business functions. Performance reports play an essential role in

determining the performance of employees and the business activities so that proper

rewards can be provided to them accordingly. Cream ltd is using the performance reports

for determining the efficiency and performance of their employees. Through this

determination, the company is providing enumeration to the employees so that they can

accomplish their goals in a more effective manner. Budget report: This report is used by the organisation for determining the variation in

expected and obtained performance. Through this, managers can develop better policies

and strategies based on the output obtained through report. This report also estimates the

expenses of the firm for a future time period which will be followed by the departments

and firm. Cream ltd is using this type of report for comparing their obtained financial

efficiency with the targeted goals in order to determine the errors and flaws in strategies.

This is beneficial in improving and implementing the future policies if the current

strategies are giving less output than expected. Accounts receivable ageing report: such type of reports contain the data associated with

the credit transactions of the company. This report is mostly used by the firms which are

making their transactions in credit form. This is beneficial for the firms in determining

the pending amount of customers in the marketplace (Arroyo, 2012). Also these reports

provide the date and time of the credit transactions for quick calculations. Cream ltd is

using this type of reports for determining the amount credited by the customers to the

company for their products.

Cost managerial accounting report: This is also an essential type of report which is used

by companies for tracking the profit and loss from the different organisational functions.

This report is useful in calculating the expenses of products before selling and then

compares these expenses with the total amount of money received from selling of

products. When the total expenses are high then selling amount then the company is

facing loss whereas if the expenses are low then it is profit for the firm. Cream ltd uses

this report for determining their profit and loss and if losses occurs then strategies and

policies are developed accordingly.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1. Evaluation of benefits of various management accounting systems.

Advantage of cost accounting system:

This is advantageous in determining the costs of the products and services through

which high margin of profit can be achieved.

Also advantageous for Creams ltd in determining the issues and errors which are

enhancing the operating costs of the company.

Advantage of inventory management system:

Advantageous for Creams ltd in tracking the supply and demand of products and

services provided by the company.

Reduces the time required for tracking inventory which will also saves the costs

for Creams ltd.

Advantages of price optimisation system:

Prices of the products can be set appropriately based on the reviews and feedback

from customers.

Provides a tool to Creams ltd for determining the prices of products based on

analysis of customer behaviour.

D1 Management accounting system and management accounting reporting are integrated with

organisation process.

Both management accounting system and reporting system are very much interrelated with

each other which increases the contribution towards achievement of organisational goals and

objectives. It can be understood by the following example, cost accounting system and budget

report both are interrelate with each other in such a way that cost accounting system helps in

identifying the total cost incurred in manufacturing activities and on the basis of which pricing

strategies will be framed. This helps in preparing budget report containing all details regarding

the total funds that an organisation have. Another instance of interrelationship, inventory

management system and report are interrelate with each other as inventory management system

assist in maintaining sufficient amount of inventory which makes easy for accounting manager to

record documents containing the details of level of stock which brings motivation among

employees to perform its roles and responsibilities.

7

Advantage of cost accounting system:

This is advantageous in determining the costs of the products and services through

which high margin of profit can be achieved.

Also advantageous for Creams ltd in determining the issues and errors which are

enhancing the operating costs of the company.

Advantage of inventory management system:

Advantageous for Creams ltd in tracking the supply and demand of products and

services provided by the company.

Reduces the time required for tracking inventory which will also saves the costs

for Creams ltd.

Advantages of price optimisation system:

Prices of the products can be set appropriately based on the reviews and feedback

from customers.

Provides a tool to Creams ltd for determining the prices of products based on

analysis of customer behaviour.

D1 Management accounting system and management accounting reporting are integrated with

organisation process.

Both management accounting system and reporting system are very much interrelated with

each other which increases the contribution towards achievement of organisational goals and

objectives. It can be understood by the following example, cost accounting system and budget

report both are interrelate with each other in such a way that cost accounting system helps in

identifying the total cost incurred in manufacturing activities and on the basis of which pricing

strategies will be framed. This helps in preparing budget report containing all details regarding

the total funds that an organisation have. Another instance of interrelationship, inventory

management system and report are interrelate with each other as inventory management system

assist in maintaining sufficient amount of inventory which makes easy for accounting manager to

record documents containing the details of level of stock which brings motivation among

employees to perform its roles and responsibilities.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

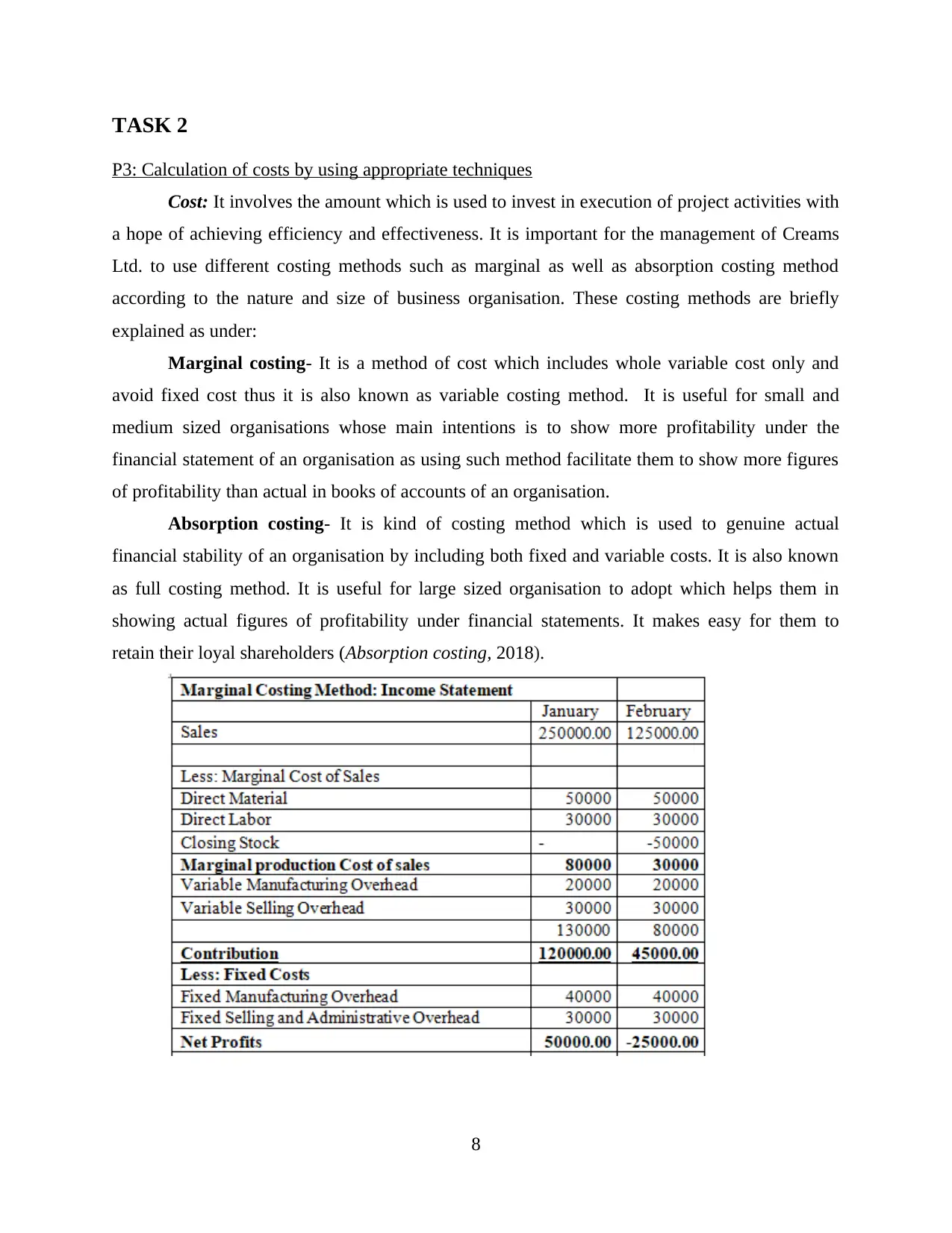

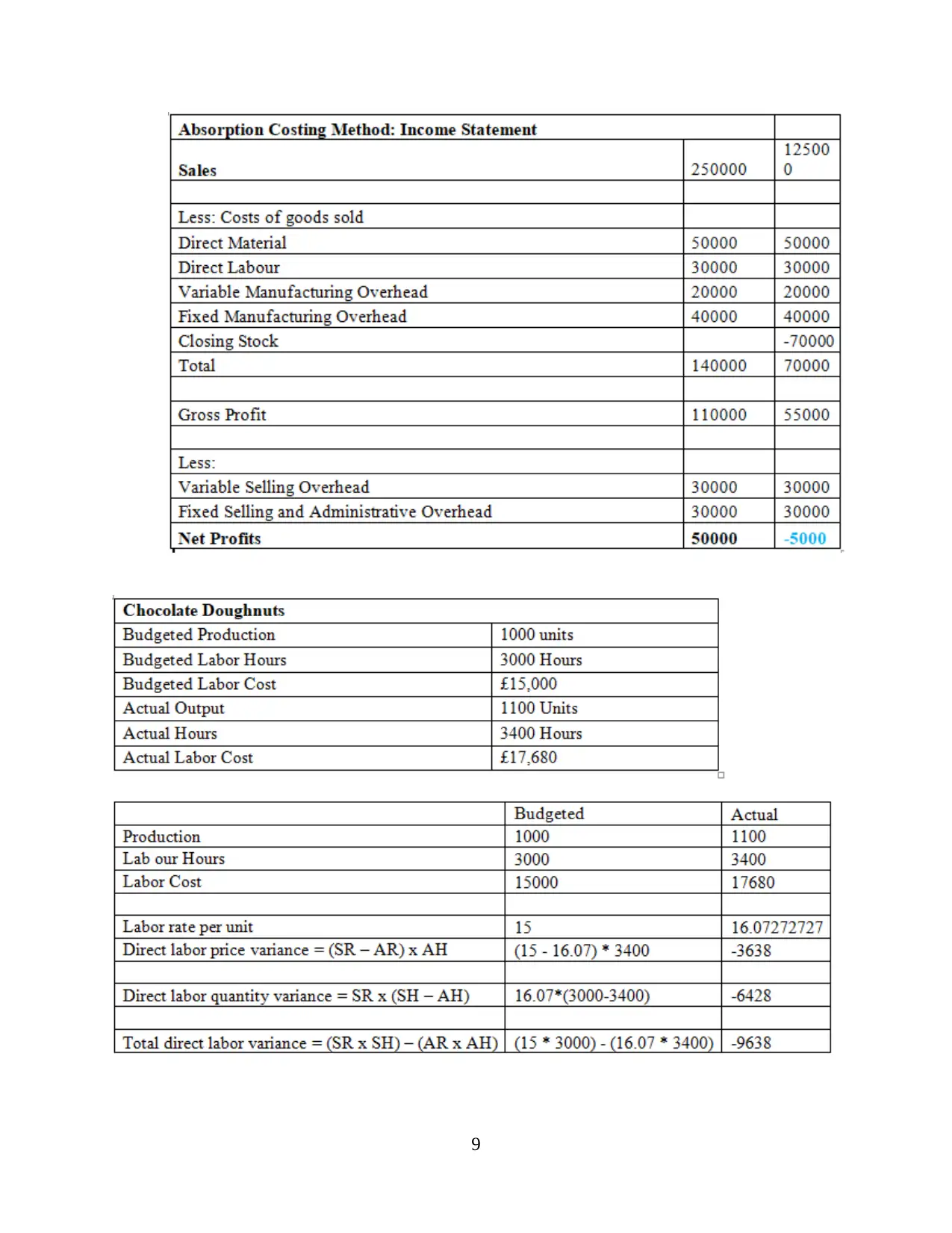

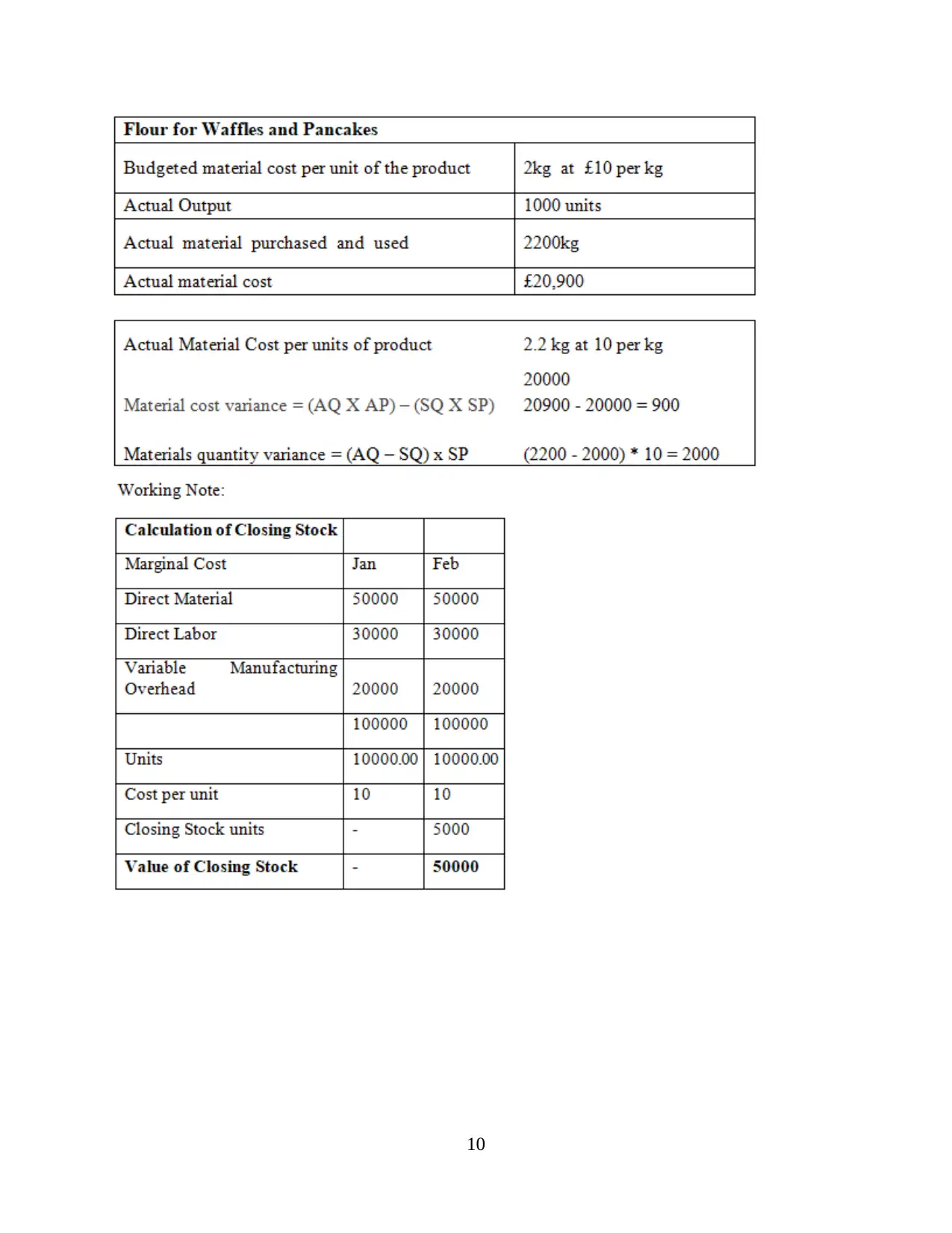

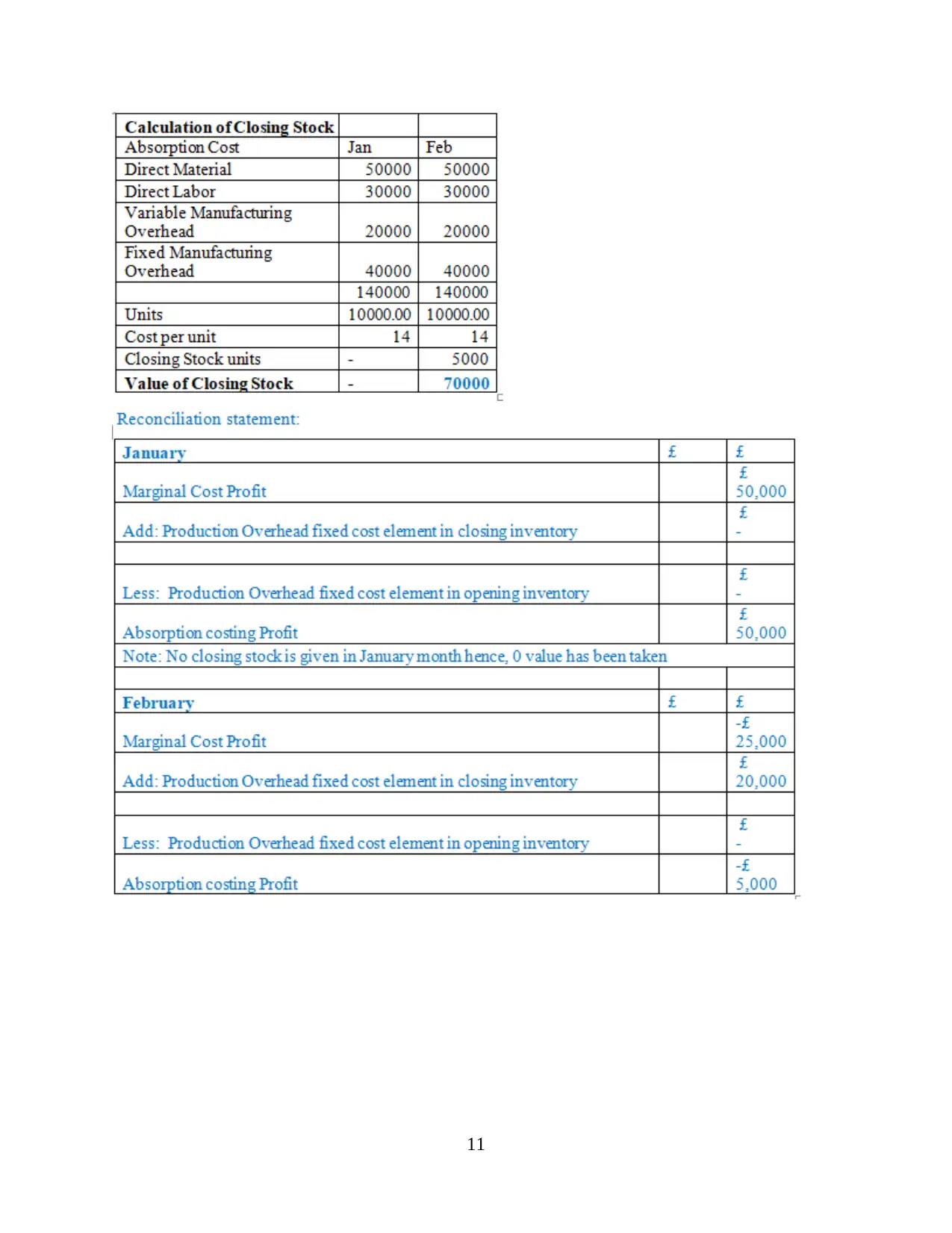

P3: Calculation of costs by using appropriate techniques

Cost: It involves the amount which is used to invest in execution of project activities with

a hope of achieving efficiency and effectiveness. It is important for the management of Creams

Ltd. to use different costing methods such as marginal as well as absorption costing method

according to the nature and size of business organisation. These costing methods are briefly

explained as under:

Marginal costing- It is a method of cost which includes whole variable cost only and

avoid fixed cost thus it is also known as variable costing method. It is useful for small and

medium sized organisations whose main intentions is to show more profitability under the

financial statement of an organisation as using such method facilitate them to show more figures

of profitability than actual in books of accounts of an organisation.

Absorption costing- It is kind of costing method which is used to genuine actual

financial stability of an organisation by including both fixed and variable costs. It is also known

as full costing method. It is useful for large sized organisation to adopt which helps them in

showing actual figures of profitability under financial statements. It makes easy for them to

retain their loyal shareholders (Absorption costing, 2018).

8

P3: Calculation of costs by using appropriate techniques

Cost: It involves the amount which is used to invest in execution of project activities with

a hope of achieving efficiency and effectiveness. It is important for the management of Creams

Ltd. to use different costing methods such as marginal as well as absorption costing method

according to the nature and size of business organisation. These costing methods are briefly

explained as under:

Marginal costing- It is a method of cost which includes whole variable cost only and

avoid fixed cost thus it is also known as variable costing method. It is useful for small and

medium sized organisations whose main intentions is to show more profitability under the

financial statement of an organisation as using such method facilitate them to show more figures

of profitability than actual in books of accounts of an organisation.

Absorption costing- It is kind of costing method which is used to genuine actual

financial stability of an organisation by including both fixed and variable costs. It is also known

as full costing method. It is useful for large sized organisation to adopt which helps them in

showing actual figures of profitability under financial statements. It makes easy for them to

retain their loyal shareholders (Absorption costing, 2018).

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

M2: Management accounting techniques and financial reporting documents

Management accounting and financial reporting techniques both are important to identify

the actual financial position of an organisation. In the context of Cream Ltd., it is important to

use management accounting techniques to maintain financial reporting documents such as final

accounts including profit and loss a/c, balance sheet etc. This will help in analysing the actual

financial stability of company which makes easy for an organisation to retain their loyal

shareholders.

D2. Financial reports which applies to interpret many business activities

It is important for the management of Cream Ltd. to interpret the information given under

the financial statements into understandable manner which makes easy to make an effective

decision and plans for the achievement of desired goals and objectives within limited time frame.

For this, there are various financial statement which includes profit and loss a/c, balance sheet

and cash flow statement thus it is important to analyse the information so as to identify the actual

financial position of an organisation.

TASK 3

P4. Advantages and disadvantages of different types of planning tools of budgetary control.

Budgetary control refers to the technique of developing future strategies and policies for

better financial performance by analysing the performance from past budgets. This tool is widely

used by the managers of firms for monitoring and controlling the financials objectives as well as

for managing the costs of a specific accounting period (Bennett and James, 2017). The

budgetary controls are essential component for an organisation as these help in managing the

performance of organisational activities through which organisational productivity can be

enhanced. These tools are useful in estimating the expenses of organisations for future activities

and operations. Managers of Cream ltd are setting several targets for controlling and monitoring

the financial activities of organisation. The advantages and disadvantages of these tools are

discussed below:

12

Management accounting and financial reporting techniques both are important to identify

the actual financial position of an organisation. In the context of Cream Ltd., it is important to

use management accounting techniques to maintain financial reporting documents such as final

accounts including profit and loss a/c, balance sheet etc. This will help in analysing the actual

financial stability of company which makes easy for an organisation to retain their loyal

shareholders.

D2. Financial reports which applies to interpret many business activities

It is important for the management of Cream Ltd. to interpret the information given under

the financial statements into understandable manner which makes easy to make an effective

decision and plans for the achievement of desired goals and objectives within limited time frame.

For this, there are various financial statement which includes profit and loss a/c, balance sheet

and cash flow statement thus it is important to analyse the information so as to identify the actual

financial position of an organisation.

TASK 3

P4. Advantages and disadvantages of different types of planning tools of budgetary control.

Budgetary control refers to the technique of developing future strategies and policies for

better financial performance by analysing the performance from past budgets. This tool is widely

used by the managers of firms for monitoring and controlling the financials objectives as well as

for managing the costs of a specific accounting period (Bennett and James, 2017). The

budgetary controls are essential component for an organisation as these help in managing the

performance of organisational activities through which organisational productivity can be

enhanced. These tools are useful in estimating the expenses of organisations for future activities

and operations. Managers of Cream ltd are setting several targets for controlling and monitoring

the financial activities of organisation. The advantages and disadvantages of these tools are

discussed below:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.