Evaluating Management Accounting Systems and Reports for IKEA

VerifiedAdded on 2023/01/10

|23

|6656

|44

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within IKEA, a multinational furniture retailer. It begins by defining management accounting and its key roles, differentiating it from financial accounting. The report then delves into specific management accounting systems employed by IKEA, including cost accounting, inventory management, price optimization, and job costing systems. It explores various management accounting reports, such as performance reports, inventory reports, accounts receivable aging reports, and cost accounting reports. The report evaluates the benefits of these systems and reports, offering insights into their impact on IKEA's operations. Furthermore, it examines cost computation methods, specifically marginal and absorption costing, and their application in formulating income statements. The report also discusses the advantages and disadvantages of planning tools used for budgetary control and analyzes how IKEA adapts management accounting systems to address financial challenges and achieve sustainable success. The content demonstrates how management accounting can be used to make informed decisions and improve business operations, covering critical aspects of financial management.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting Systems:........................................................................................3

P2 Management Accounting Reports:.........................................................................................5

M1 Evaluating benefits of discussed MA systems:.....................................................................6

D1 Evaluating how MA-systems and MA-reporting are integrated within organisational

processes:....................................................................................................................................7

P3. Computing costs through applying suitable methods of cost-analysis to formulatye income

statements:...................................................................................................................................7

M2. Accurately apply the range of management accounting techniques and produce

appropriate financial report.......................................................................................................13

D2. Produce financial report which accurately apply and interpret the business activities ...13

P4: Explaining major advantages & disadvantages of different types of planning tools used for

budgetary control:.....................................................................................................................13

M3: Analysing uses of different planning tools/methods and their application for preparing

and forecasting budgets:............................................................................................................15

P5 Comparing as to how corporations are effectively adapting MA systems for responding to

multiple financial problems:.....................................................................................................15

M4 Analysing about how as to respond financial problems, MA can lead entities towards

sustainable successes:................................................................................................................17

D3 Evaluating as to how discussed planning tools can respond effectively to resolving such

financial problems to lead organisations to sustainable success:..............................................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting Systems:........................................................................................3

P2 Management Accounting Reports:.........................................................................................5

M1 Evaluating benefits of discussed MA systems:.....................................................................6

D1 Evaluating how MA-systems and MA-reporting are integrated within organisational

processes:....................................................................................................................................7

P3. Computing costs through applying suitable methods of cost-analysis to formulatye income

statements:...................................................................................................................................7

M2. Accurately apply the range of management accounting techniques and produce

appropriate financial report.......................................................................................................13

D2. Produce financial report which accurately apply and interpret the business activities ...13

P4: Explaining major advantages & disadvantages of different types of planning tools used for

budgetary control:.....................................................................................................................13

M3: Analysing uses of different planning tools/methods and their application for preparing

and forecasting budgets:............................................................................................................15

P5 Comparing as to how corporations are effectively adapting MA systems for responding to

multiple financial problems:.....................................................................................................15

M4 Analysing about how as to respond financial problems, MA can lead entities towards

sustainable successes:................................................................................................................17

D3 Evaluating as to how discussed planning tools can respond effectively to resolving such

financial problems to lead organisations to sustainable success:..............................................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

INTRODUCTION

Management accounting simply corresponds to process of identifying, analyzing,

evaluating, interpreting and expressing information to company's upper managers for the purpose

of achieving the objectives. This is also referred to cost accounting as well as information that

helps to make better company-related decisions. Management accounting framework is distinct

from any other method of accounting framework as it provides in-depth information concerning

financial and non-financial transactions (Monden, 2019).

The assignment is focused on IKEA. The corporation is big multinational corporation of

Swedish origin, have headquarters in Netherlands, founded in year 1943, which designs and sells

entirely designed and furnished furniture. It also deals in kitchen appliances, household

furniture items and other customized furniture as per client requirements. The report will analyse

the different forms of managerial accounting systems. The different approaches used for

handling accounting reporting also will be discussed here. Along with the benefits and

drawbacks of the planning mechanism being used budgetary controlling. The final cost should be

determined using the correct method for readying income statements considering both marginal

and absorption methods.

TASK 1

P1 Management Accounting Systems:

According to CIMA, MA is "the practise of defining, assessing, storing, examining,

planning, presenting and transmitting the critical information that management personnel uses to

plan, analyse and coordinate within an organisation and to ensure that organisation's all

key resources are properly deployed and accountable. In this regard following are certain key

roles of management accounting, as follows:

1. Effective planning: MA plays a critical role in creating efficient plan that ensures that

includes the details required. Management accountants offer details for drawing up plans

for capital budget, revenue schedule, cost-volumes-profit review.

2. Increasing Business Operations Efficiency: MA also performs a considerable role in

raising business operations performance by financial planning, ratio analysis, process

costing etc.

3. Effective Controlling: Through JIT theory and absolute quality management framework,

MA holds pan inefficient controlling.

3

Management accounting simply corresponds to process of identifying, analyzing,

evaluating, interpreting and expressing information to company's upper managers for the purpose

of achieving the objectives. This is also referred to cost accounting as well as information that

helps to make better company-related decisions. Management accounting framework is distinct

from any other method of accounting framework as it provides in-depth information concerning

financial and non-financial transactions (Monden, 2019).

The assignment is focused on IKEA. The corporation is big multinational corporation of

Swedish origin, have headquarters in Netherlands, founded in year 1943, which designs and sells

entirely designed and furnished furniture. It also deals in kitchen appliances, household

furniture items and other customized furniture as per client requirements. The report will analyse

the different forms of managerial accounting systems. The different approaches used for

handling accounting reporting also will be discussed here. Along with the benefits and

drawbacks of the planning mechanism being used budgetary controlling. The final cost should be

determined using the correct method for readying income statements considering both marginal

and absorption methods.

TASK 1

P1 Management Accounting Systems:

According to CIMA, MA is "the practise of defining, assessing, storing, examining,

planning, presenting and transmitting the critical information that management personnel uses to

plan, analyse and coordinate within an organisation and to ensure that organisation's all

key resources are properly deployed and accountable. In this regard following are certain key

roles of management accounting, as follows:

1. Effective planning: MA plays a critical role in creating efficient plan that ensures that

includes the details required. Management accountants offer details for drawing up plans

for capital budget, revenue schedule, cost-volumes-profit review.

2. Increasing Business Operations Efficiency: MA also performs a considerable role in

raising business operations performance by financial planning, ratio analysis, process

costing etc.

3. Effective Controlling: Through JIT theory and absolute quality management framework,

MA holds pan inefficient controlling.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Improve labour productivity: MA aims to increase labour production by connecting

bonus to competitiveness and budgeting by standard wage costs.

5. Achieve management performance: MA leads a great deal to improving the organisation's

management quality by supplying the right knowledge to management.

6. Help managerial functions: All know that arranging, coordinating, directing and

managing are key roles of MA that help management staff to execute the tasks correctly,

including the required accounting details.

Difference between MA and Financial Accounting:

There are 2 key distinctions among FA and MA. The first distinction is that MA is being

presented to internal stakeholders of a corporation, whereas financial accounting is being done

for external stakeholders. Although FA is of considerable interest to existing and prospective

owners, MA is important for management personnel to render their business' existing and

prospective financial decisions. The secondary distinction is that FA is reliable and must conform

to accounting standards and guidelines, whereas MA can be dependent on a assumption or

estimation as most managing officials don't have enough time to collect precise figures as soon

as decision is taken.

Management accounting systems are presenting of accounting information for development

of strategies implemented by mangers and also for the support of day-to-day operations. Simply

put, it allows management to conduct all tasks, along with planning, scheduling, hiring,

managing and regulating. Management accounting includes a particular form of accounting

method that plays a significant role in various types of business establishments (Meidell and

Kaarbøe, 2017). There are also several key accounting systems that can be used by IKEA are

explained below:

Cost accounting system – This form of MA system is often referred to as costing system

for products. This is the method used by businesses to measure cost of their goods for

inventory/stock valuation, cost benefit analysis and cost management purposes. The cost

accounting method helps to measure the cost of goods that are essential to the

organization of sustainable operations. This allow businesses like IKEA to monitor their

cost of manufacturing activities. The said system require detailed, proper and

comprehensive details of all the costs and expenses along with adequate explanation

about the classification of different costs within entity. The cost

accounting system implemented in a specific company must balance the scope and scale

of the enterprise and information requirements of the company. This system should be

4

bonus to competitiveness and budgeting by standard wage costs.

5. Achieve management performance: MA leads a great deal to improving the organisation's

management quality by supplying the right knowledge to management.

6. Help managerial functions: All know that arranging, coordinating, directing and

managing are key roles of MA that help management staff to execute the tasks correctly,

including the required accounting details.

Difference between MA and Financial Accounting:

There are 2 key distinctions among FA and MA. The first distinction is that MA is being

presented to internal stakeholders of a corporation, whereas financial accounting is being done

for external stakeholders. Although FA is of considerable interest to existing and prospective

owners, MA is important for management personnel to render their business' existing and

prospective financial decisions. The secondary distinction is that FA is reliable and must conform

to accounting standards and guidelines, whereas MA can be dependent on a assumption or

estimation as most managing officials don't have enough time to collect precise figures as soon

as decision is taken.

Management accounting systems are presenting of accounting information for development

of strategies implemented by mangers and also for the support of day-to-day operations. Simply

put, it allows management to conduct all tasks, along with planning, scheduling, hiring,

managing and regulating. Management accounting includes a particular form of accounting

method that plays a significant role in various types of business establishments (Meidell and

Kaarbøe, 2017). There are also several key accounting systems that can be used by IKEA are

explained below:

Cost accounting system – This form of MA system is often referred to as costing system

for products. This is the method used by businesses to measure cost of their goods for

inventory/stock valuation, cost benefit analysis and cost management purposes. The cost

accounting method helps to measure the cost of goods that are essential to the

organization of sustainable operations. This allow businesses like IKEA to monitor their

cost of manufacturing activities. The said system require detailed, proper and

comprehensive details of all the costs and expenses along with adequate explanation

about the classification of different costs within entity. The cost

accounting system implemented in a specific company must balance the scope and scale

of the enterprise and information requirements of the company. This system should be

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost-effective for the company and the system's advantages should be greater than its

implementation and maintenance costs. IKEA should incorporate this accounting method

in their practice as it helps to track the expense of manufacturing operations.

Inventory management system – This is the form of accounting framework that relates

to the effective management of company's inventories or stocks, like raw materials,

finished products and so forth within the organisation. With assistance of inventory

management systems, the organization will take decisions concerning the procurement of

raw materials and production capacity. Since it helps to recognize the quality of inventory

in stores (Liff and Wahlstrom, 2018). The correct accounting system will assist the

company in determining the supply of raw materials, finished products and other

inventories decisions. As in IKEA company, inventory accounting system could be used

in their function to determine the quality of materials and also finished products within

the organization. This system generally require preparation of inventories sheet and

register which cleanly shows the place, nature and value of inventories. This system also

require a proper basis for classification of different kind of inventories and proper

physical handling as well as storage.

Price optimisation system – It is kind of accounting mechanism that helps to assess the

price of goods and services at an efficient level. The price management method can help

to assess consumer responses at various price rates (Dyckman and Zeff, 2015). In fact,

because there is no price management program inside IKEA, this is hard to determine the

correct prices of the products. The corresponding accounting method is therefore

essential for the company to find the correct price for its products and services. Thus,

IKEA 's implementation of the price optimization system helps to allocate effective

products' prices within the corporation. Effective analysis and evaluation of price and

demand relationship and other related factors are key requirement of this system.

Job costing system – It is the form of MA system that helps to assess separate job costs

for various operations. job costing framework is useful in providing accurate details on

the costs of jobs, and also in the capacity of business companies to make sensible

decisions about different jobs. Generally, this accounting system plays an important role

in controlling job costs. Simply put, the method of labour costing uses within the business

sector and it uses to evaluate that the productions cost surpasses the overheads and the

price of materials in order to offer profits for the entire process. In general, therefore, the

method of costing jobs is implemented by IKEA Ltd for purpose of determining costs of

5

implementation and maintenance costs. IKEA should incorporate this accounting method

in their practice as it helps to track the expense of manufacturing operations.

Inventory management system – This is the form of accounting framework that relates

to the effective management of company's inventories or stocks, like raw materials,

finished products and so forth within the organisation. With assistance of inventory

management systems, the organization will take decisions concerning the procurement of

raw materials and production capacity. Since it helps to recognize the quality of inventory

in stores (Liff and Wahlstrom, 2018). The correct accounting system will assist the

company in determining the supply of raw materials, finished products and other

inventories decisions. As in IKEA company, inventory accounting system could be used

in their function to determine the quality of materials and also finished products within

the organization. This system generally require preparation of inventories sheet and

register which cleanly shows the place, nature and value of inventories. This system also

require a proper basis for classification of different kind of inventories and proper

physical handling as well as storage.

Price optimisation system – It is kind of accounting mechanism that helps to assess the

price of goods and services at an efficient level. The price management method can help

to assess consumer responses at various price rates (Dyckman and Zeff, 2015). In fact,

because there is no price management program inside IKEA, this is hard to determine the

correct prices of the products. The corresponding accounting method is therefore

essential for the company to find the correct price for its products and services. Thus,

IKEA 's implementation of the price optimization system helps to allocate effective

products' prices within the corporation. Effective analysis and evaluation of price and

demand relationship and other related factors are key requirement of this system.

Job costing system – It is the form of MA system that helps to assess separate job costs

for various operations. job costing framework is useful in providing accurate details on

the costs of jobs, and also in the capacity of business companies to make sensible

decisions about different jobs. Generally, this accounting system plays an important role

in controlling job costs. Simply put, the method of labour costing uses within the business

sector and it uses to evaluate that the productions cost surpasses the overheads and the

price of materials in order to offer profits for the entire process. In general, therefore, the

method of costing jobs is implemented by IKEA Ltd for purpose of determining costs of

5

jobs assigned to various business operations (Kure, Nørreklit and Raffnsøe-Møller,

2017). This system require proper categorisation of different jobs and allocation basis of

various costs to such defined jobs.

P2 Management Accounting Reports:

There are many approaches used to prepare a management accounting reporting for a

company to monitor both its financial and non-financial results. IKEA will also prepare its

various accounting reports with the support of distinct-distinct accounting systems. The summary

of the different reports or reporting methods are given below: -

Performance report - This form of report depicts actual performance of various aspects

that occur within the company or in some kind of research carried out by the employee.

The report contains the effects of the outcomes resulting from a comparison of the real

with budgeted/standard. This could serve to assess the difference between the two

statistics and between outputs of employees, along with justification and further that can

be used by management of the company for the implementation of strategies that will

eventually help to resolve these differences and assist to achieve the goals set. IKEA

is small company selling furniture (Kerr, Rouse and de Villiers, 2015). This

is manufacturing organization that utilizes such report for 2 main reasons, like monitoring

of performance of employees and quality assurance of the products. The overall benefit

of this study is seen in manner with which it works, which enables employees to make

effective use of terms that contribute to the production of better products.

Inventory report – It is the method for collecting information and report it which

provides information on the quantities of raw materials as well as the finished products

located in the IKEA warehouses. With the aid of inventories report business organization

obtain information about how much inventories are currently available so about if there is

a need to buy IKEA can buy. The respective organization shall therefore make

preparations of an inventory reports for the management of its raw materials and product.

In addition, implementation of inventories reports provides assistance in obtaining data

on a range of types of overheads in inventory storage procedure. This same as in IKEA

may also compile a report on the management of raw materials and also ready furniture.

Account receivable ageing report – It is the form of MA report which relates to the

provision of detailed information, and to the organization's data on overall market debts

including defaulted debtors. In fact, most businesses are provided with information

6

2017). This system require proper categorisation of different jobs and allocation basis of

various costs to such defined jobs.

P2 Management Accounting Reports:

There are many approaches used to prepare a management accounting reporting for a

company to monitor both its financial and non-financial results. IKEA will also prepare its

various accounting reports with the support of distinct-distinct accounting systems. The summary

of the different reports or reporting methods are given below: -

Performance report - This form of report depicts actual performance of various aspects

that occur within the company or in some kind of research carried out by the employee.

The report contains the effects of the outcomes resulting from a comparison of the real

with budgeted/standard. This could serve to assess the difference between the two

statistics and between outputs of employees, along with justification and further that can

be used by management of the company for the implementation of strategies that will

eventually help to resolve these differences and assist to achieve the goals set. IKEA

is small company selling furniture (Kerr, Rouse and de Villiers, 2015). This

is manufacturing organization that utilizes such report for 2 main reasons, like monitoring

of performance of employees and quality assurance of the products. The overall benefit

of this study is seen in manner with which it works, which enables employees to make

effective use of terms that contribute to the production of better products.

Inventory report – It is the method for collecting information and report it which

provides information on the quantities of raw materials as well as the finished products

located in the IKEA warehouses. With the aid of inventories report business organization

obtain information about how much inventories are currently available so about if there is

a need to buy IKEA can buy. The respective organization shall therefore make

preparations of an inventory reports for the management of its raw materials and product.

In addition, implementation of inventories reports provides assistance in obtaining data

on a range of types of overheads in inventory storage procedure. This same as in IKEA

may also compile a report on the management of raw materials and also ready furniture.

Account receivable ageing report – It is the form of MA report which relates to the

provision of detailed information, and to the organization's data on overall market debts

including defaulted debtors. In fact, most businesses are provided with information

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

about dates on which payments has been made. The main purpose of the respective study

is therefore to assist the company in the recovery of the sum from the debtors. Business

company shall prepare an account receivable aging report to collect details on the overall

amount owed on the market from specific debtors (Kenyon and Kenyon, 2016).

Cost accounting report - This report covers costs of all activities carried out by the

corporation in the production of a particular product. etIn the scenario of

IKEA, management team of this corporation utilizes this accounting report to capture

all costs incurred in production of its furniture items. This study assists an enterprise to

evaluate its potential costs and profits. The cost accounting reports can be formed

applying two methods, i.e. job-orders costing and process-costing.

In the context of costs of a specific job orders, all costs charged while performing a job

shall be regarded. For instance, Management personnel in IKEA utilizes such report to record all

costs accrued while conducting a specific job of manufacturing of furniture for a specific type of

customer. In process costing, IKEA must transfer all the costs incurred when performing a

process that can be used to manufacture a specific portion of furniture. The main objective

behind the development of such reports is assist organizations recognize the overall costs

recouped so that they can be even farther monitored and assessed (Hoque, Parker, Covaleski and

Haynes, 2017).

M1 Evaluating benefits of discussed MA systems:

As described above, there's certain different types of accounting systems within MA.

These accounting system have several benefits of as described below:-

Type of management

accounting system

Benefits of management accounting system

Cost accounting system It is useful accounting system that helps to provide extensive

information on the costs of different operations. An organization can

therefore manage the costs of its various activities or

operations through cost accounting system.

Inventory management

system

Such management accounting framework is advantageous to the

management of the stocks and by helping the company to take

decisions on both the purchase and manufacturing of finished goods.

This also help to effectively optimizing inventory costs like storing

7

is therefore to assist the company in the recovery of the sum from the debtors. Business

company shall prepare an account receivable aging report to collect details on the overall

amount owed on the market from specific debtors (Kenyon and Kenyon, 2016).

Cost accounting report - This report covers costs of all activities carried out by the

corporation in the production of a particular product. etIn the scenario of

IKEA, management team of this corporation utilizes this accounting report to capture

all costs incurred in production of its furniture items. This study assists an enterprise to

evaluate its potential costs and profits. The cost accounting reports can be formed

applying two methods, i.e. job-orders costing and process-costing.

In the context of costs of a specific job orders, all costs charged while performing a job

shall be regarded. For instance, Management personnel in IKEA utilizes such report to record all

costs accrued while conducting a specific job of manufacturing of furniture for a specific type of

customer. In process costing, IKEA must transfer all the costs incurred when performing a

process that can be used to manufacture a specific portion of furniture. The main objective

behind the development of such reports is assist organizations recognize the overall costs

recouped so that they can be even farther monitored and assessed (Hoque, Parker, Covaleski and

Haynes, 2017).

M1 Evaluating benefits of discussed MA systems:

As described above, there's certain different types of accounting systems within MA.

These accounting system have several benefits of as described below:-

Type of management

accounting system

Benefits of management accounting system

Cost accounting system It is useful accounting system that helps to provide extensive

information on the costs of different operations. An organization can

therefore manage the costs of its various activities or

operations through cost accounting system.

Inventory management

system

Such management accounting framework is advantageous to the

management of the stocks and by helping the company to take

decisions on both the purchase and manufacturing of finished goods.

This also help to effectively optimizing inventory costs like storing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and handling of stocks.

Price optimisation system It is an accounting system that helps IKEA to set an accurate

prices for furniture. In addition to this, the price optimization system

helps to recognise customer behaviours at the differential level

offered by the respective organization (Harrison and Lock, 2017).

Job costing system job costing framework is advantageous to the organization in the

calculation of job costs on its own. In addition, the costing system

help to records costs in a more acceptable way and enables cost

containment by contrasting actual costs and forecasts costs.

D1 Evaluating how MA-systems and MA-reporting are integrated within organisational

processes:

The managerial accounting systems as well as managerial accounting reports are blended

together because, with assistance of such integration firms, they can compile management

accounting reports Thus, IKEA can form accounting reports such as stock and cost reports with

the aid of costs and inventory system. This also demonstrates that both the management

accounting frameworks and the reporting systems are linked to the corporation's processes (Gray,

2015).

P3. Computing costs through applying suitable methods of cost-analysis to formulate income

statements:

Marginal Costing: Under marginal method contribution is assessed as in this method costs all are

classified separately as variable costs and fixed costs.

Absorption Costing: Under absorption costing productions overheads whether fixed or variable

are regarded as absorption costs to derive gross profit figure.

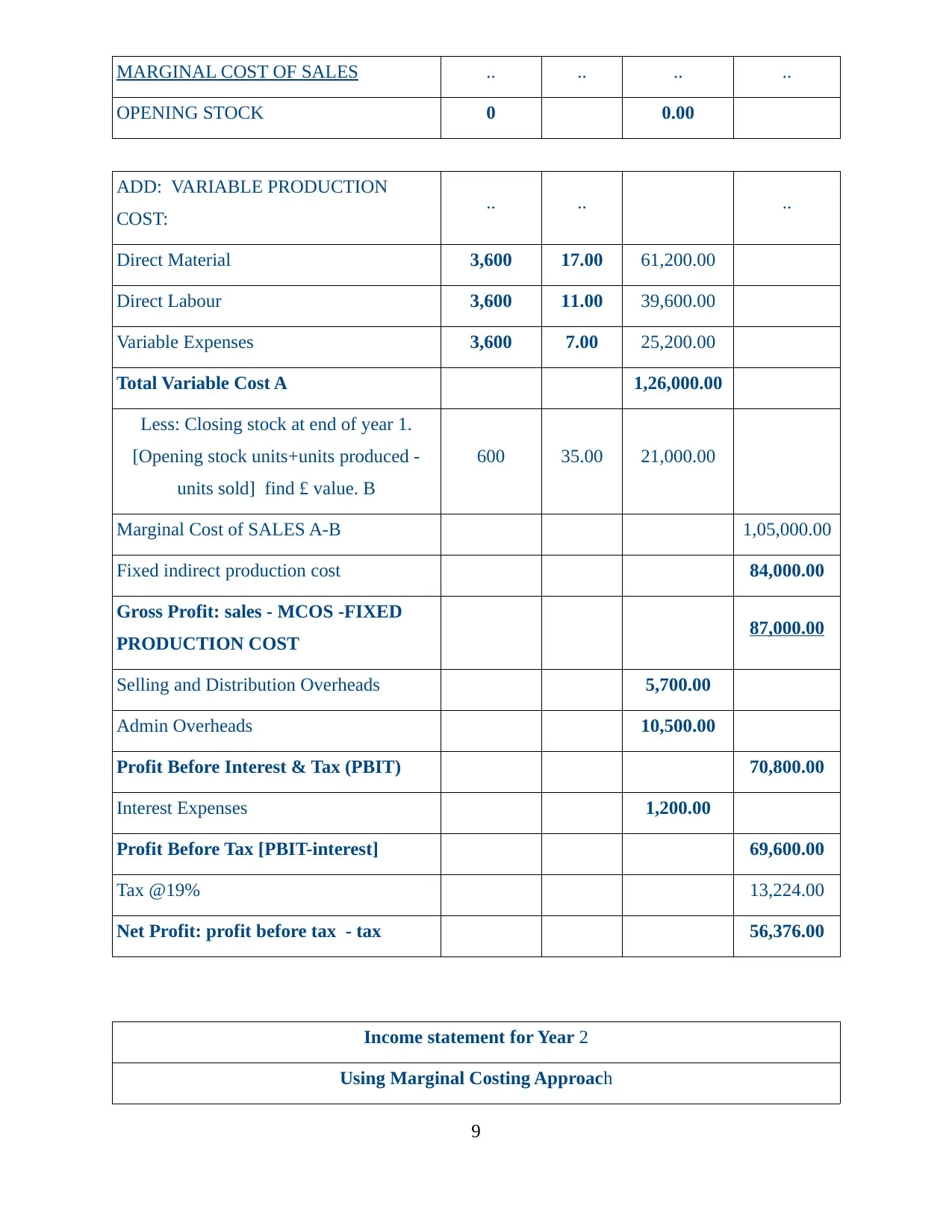

Marwa Limited:

Income statement for Year 1

Using Marginal Costing Approach

ITEM Number of

units £ P.U. AMOUNT £ AMOUNT

£

SALES 3,000 92.00 2,76,000.00

8

Price optimisation system It is an accounting system that helps IKEA to set an accurate

prices for furniture. In addition to this, the price optimization system

helps to recognise customer behaviours at the differential level

offered by the respective organization (Harrison and Lock, 2017).

Job costing system job costing framework is advantageous to the organization in the

calculation of job costs on its own. In addition, the costing system

help to records costs in a more acceptable way and enables cost

containment by contrasting actual costs and forecasts costs.

D1 Evaluating how MA-systems and MA-reporting are integrated within organisational

processes:

The managerial accounting systems as well as managerial accounting reports are blended

together because, with assistance of such integration firms, they can compile management

accounting reports Thus, IKEA can form accounting reports such as stock and cost reports with

the aid of costs and inventory system. This also demonstrates that both the management

accounting frameworks and the reporting systems are linked to the corporation's processes (Gray,

2015).

P3. Computing costs through applying suitable methods of cost-analysis to formulate income

statements:

Marginal Costing: Under marginal method contribution is assessed as in this method costs all are

classified separately as variable costs and fixed costs.

Absorption Costing: Under absorption costing productions overheads whether fixed or variable

are regarded as absorption costs to derive gross profit figure.

Marwa Limited:

Income statement for Year 1

Using Marginal Costing Approach

ITEM Number of

units £ P.U. AMOUNT £ AMOUNT

£

SALES 3,000 92.00 2,76,000.00

8

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 0 0.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,600 17.00 61,200.00

Direct Labour 3,600 11.00 39,600.00

Variable Expenses 3,600 7.00 25,200.00

Total Variable Cost A 1,26,000.00

Less: Closing stock at end of year 1.

[Opening stock units+units produced -

units sold] find £ value. B

600 35.00 21,000.00

Marginal Cost of SALES A-B 1,05,000.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 87,000.00

Selling and Distribution Overheads 5,700.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 70,800.00

Interest Expenses 1,200.00

Profit Before Tax [PBIT-interest] 69,600.00

Tax @19% 13,224.00

Net Profit: profit before tax - tax 56,376.00

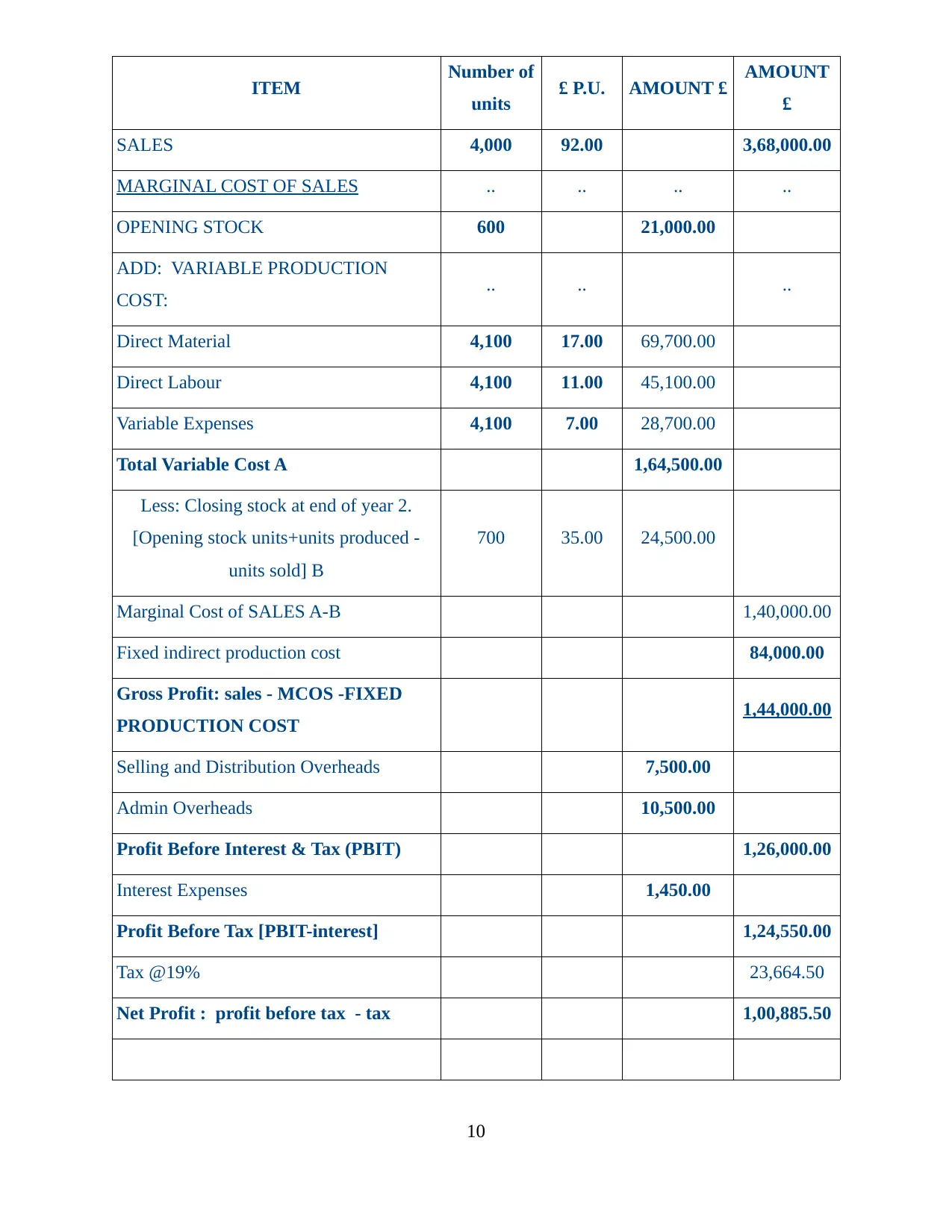

Income statement for Year 2

Using Marginal Costing Approach

9

OPENING STOCK 0 0.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,600 17.00 61,200.00

Direct Labour 3,600 11.00 39,600.00

Variable Expenses 3,600 7.00 25,200.00

Total Variable Cost A 1,26,000.00

Less: Closing stock at end of year 1.

[Opening stock units+units produced -

units sold] find £ value. B

600 35.00 21,000.00

Marginal Cost of SALES A-B 1,05,000.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 87,000.00

Selling and Distribution Overheads 5,700.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 70,800.00

Interest Expenses 1,200.00

Profit Before Tax [PBIT-interest] 69,600.00

Tax @19% 13,224.00

Net Profit: profit before tax - tax 56,376.00

Income statement for Year 2

Using Marginal Costing Approach

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ITEM Number of

units £ P.U. AMOUNT £ AMOUNT

£

SALES 4,000 92.00 3,68,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 600 21,000.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 4,100 17.00 69,700.00

Direct Labour 4,100 11.00 45,100.00

Variable Expenses 4,100 7.00 28,700.00

Total Variable Cost A 1,64,500.00

Less: Closing stock at end of year 2.

[Opening stock units+units produced -

units sold] B

700 35.00 24,500.00

Marginal Cost of SALES A-B 1,40,000.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 1,44,000.00

Selling and Distribution Overheads 7,500.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 1,26,000.00

Interest Expenses 1,450.00

Profit Before Tax [PBIT-interest] 1,24,550.00

Tax @19% 23,664.50

Net Profit : profit before tax - tax 1,00,885.50

10

units £ P.U. AMOUNT £ AMOUNT

£

SALES 4,000 92.00 3,68,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 600 21,000.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 4,100 17.00 69,700.00

Direct Labour 4,100 11.00 45,100.00

Variable Expenses 4,100 7.00 28,700.00

Total Variable Cost A 1,64,500.00

Less: Closing stock at end of year 2.

[Opening stock units+units produced -

units sold] B

700 35.00 24,500.00

Marginal Cost of SALES A-B 1,40,000.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 1,44,000.00

Selling and Distribution Overheads 7,500.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 1,26,000.00

Interest Expenses 1,450.00

Profit Before Tax [PBIT-interest] 1,24,550.00

Tax @19% 23,664.50

Net Profit : profit before tax - tax 1,00,885.50

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement for Year 3

Using Marginal Costing Approach

ITEM Number of

units £ P.U. AMOUNT £ AMOUNT £

SALES 3,500 92.00 3,22,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 700 24,500.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,400 17.00 57,800.00

Direct Labour 3,400 11.00 37,400.00

Variable Expenses 3,400 7.00 23,800.00

Total Variable Cost A 1,43,500.00

Less: Closing stock at end of year 2.

[Opening stock units+units produced -

units sold] B

600 35.00 21,000.00

Marginal Cost of SALES A-B 1,22,500.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 1,15,500.00

Selling and Distribution Overheads 7,100.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 97,900.00

Interest Expenses 1,700.00

Profit Before Tax [PBIT-interest] 96,200.00

Tax @19% 18,278.00

Net Profit : profit before tax - tax 77,922.00

Year 1 Year 2 Year 3

Total fixed indirect production cost 84,000.00 84,000.00 84,000.00 [£]

11

Using Marginal Costing Approach

ITEM Number of

units £ P.U. AMOUNT £ AMOUNT £

SALES 3,500 92.00 3,22,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 700 24,500.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,400 17.00 57,800.00

Direct Labour 3,400 11.00 37,400.00

Variable Expenses 3,400 7.00 23,800.00

Total Variable Cost A 1,43,500.00

Less: Closing stock at end of year 2.

[Opening stock units+units produced -

units sold] B

600 35.00 21,000.00

Marginal Cost of SALES A-B 1,22,500.00

Fixed indirect production cost 84,000.00

Gross Profit: sales - MCOS -FIXED

PRODUCTION COST 1,15,500.00

Selling and Distribution Overheads 7,100.00

Admin Overheads 10,500.00

Profit Before Interest & Tax (PBIT) 97,900.00

Interest Expenses 1,700.00

Profit Before Tax [PBIT-interest] 96,200.00

Tax @19% 18,278.00

Net Profit : profit before tax - tax 77,922.00

Year 1 Year 2 Year 3

Total fixed indirect production cost 84,000.00 84,000.00 84,000.00 [£]

11

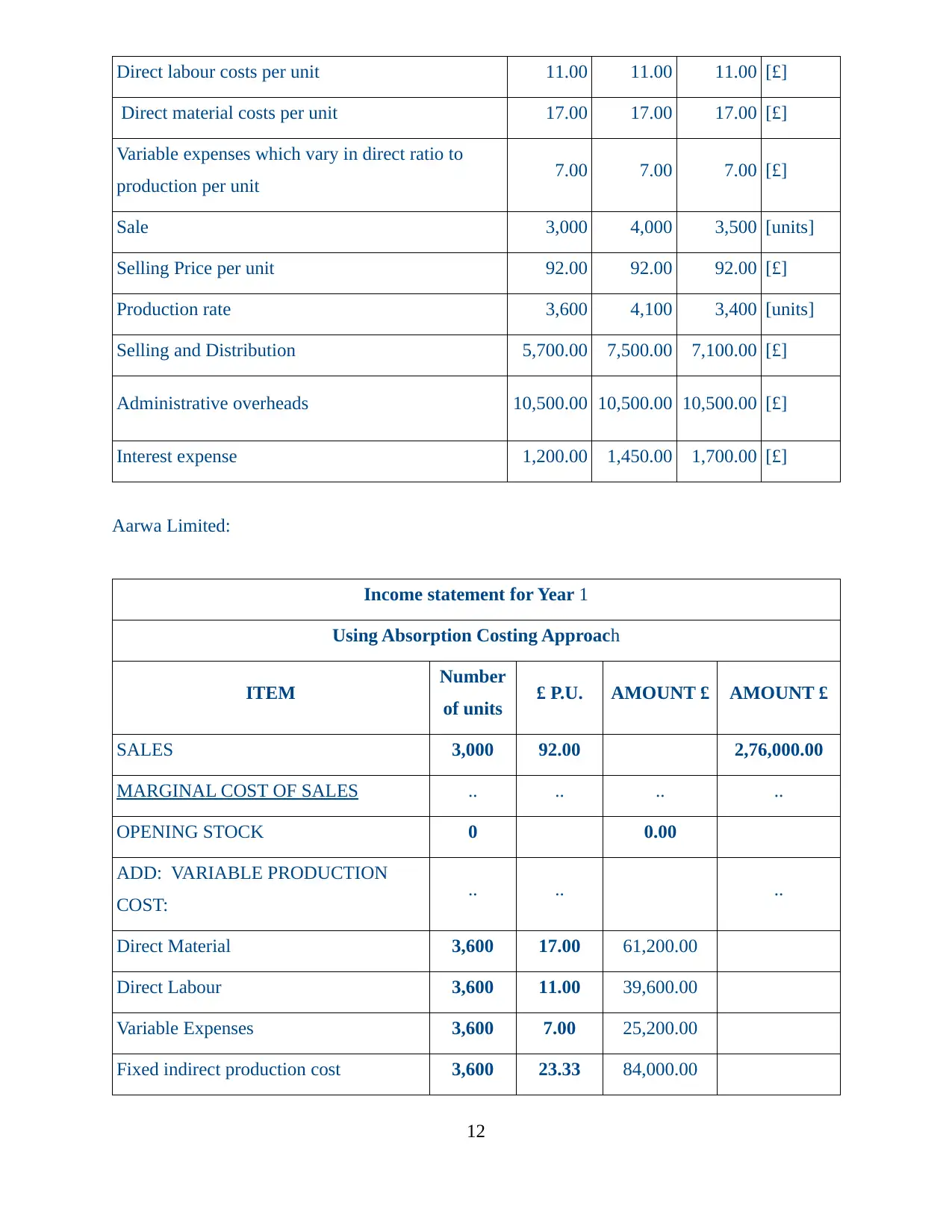

Direct labour costs per unit 11.00 11.00 11.00 [£]

Direct material costs per unit 17.00 17.00 17.00 [£]

Variable expenses which vary in direct ratio to

production per unit 7.00 7.00 7.00 [£]

Sale 3,000 4,000 3,500 [units]

Selling Price per unit 92.00 92.00 92.00 [£]

Production rate 3,600 4,100 3,400 [units]

Selling and Distribution 5,700.00 7,500.00 7,100.00 [£]

Administrative overheads 10,500.00 10,500.00 10,500.00 [£]

Interest expense 1,200.00 1,450.00 1,700.00 [£]

Aarwa Limited:

Income statement for Year 1

Using Absorption Costing Approach

ITEM Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 3,000 92.00 2,76,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 0 0.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,600 17.00 61,200.00

Direct Labour 3,600 11.00 39,600.00

Variable Expenses 3,600 7.00 25,200.00

Fixed indirect production cost 3,600 23.33 84,000.00

12

Direct material costs per unit 17.00 17.00 17.00 [£]

Variable expenses which vary in direct ratio to

production per unit 7.00 7.00 7.00 [£]

Sale 3,000 4,000 3,500 [units]

Selling Price per unit 92.00 92.00 92.00 [£]

Production rate 3,600 4,100 3,400 [units]

Selling and Distribution 5,700.00 7,500.00 7,100.00 [£]

Administrative overheads 10,500.00 10,500.00 10,500.00 [£]

Interest expense 1,200.00 1,450.00 1,700.00 [£]

Aarwa Limited:

Income statement for Year 1

Using Absorption Costing Approach

ITEM Number

of units £ P.U. AMOUNT £ AMOUNT £

SALES 3,000 92.00 2,76,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 0 0.00

ADD: VARIABLE PRODUCTION

COST: .. .. ..

Direct Material 3,600 17.00 61,200.00

Direct Labour 3,600 11.00 39,600.00

Variable Expenses 3,600 7.00 25,200.00

Fixed indirect production cost 3,600 23.33 84,000.00

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.