Management Accounting Report: Evaluation of Alpha Limited's Finances

VerifiedAdded on 2023/01/17

|22

|4689

|61

Report

AI Summary

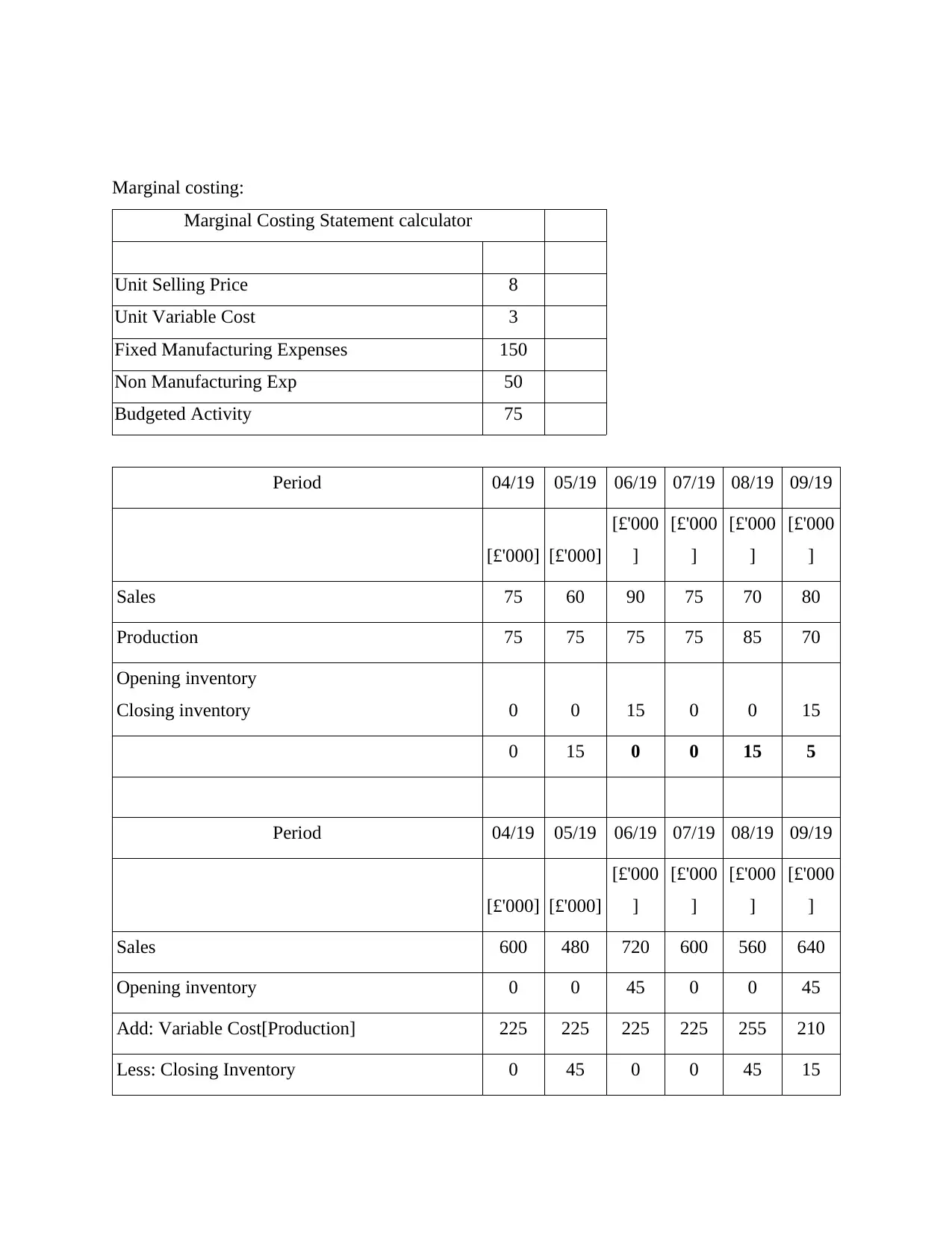

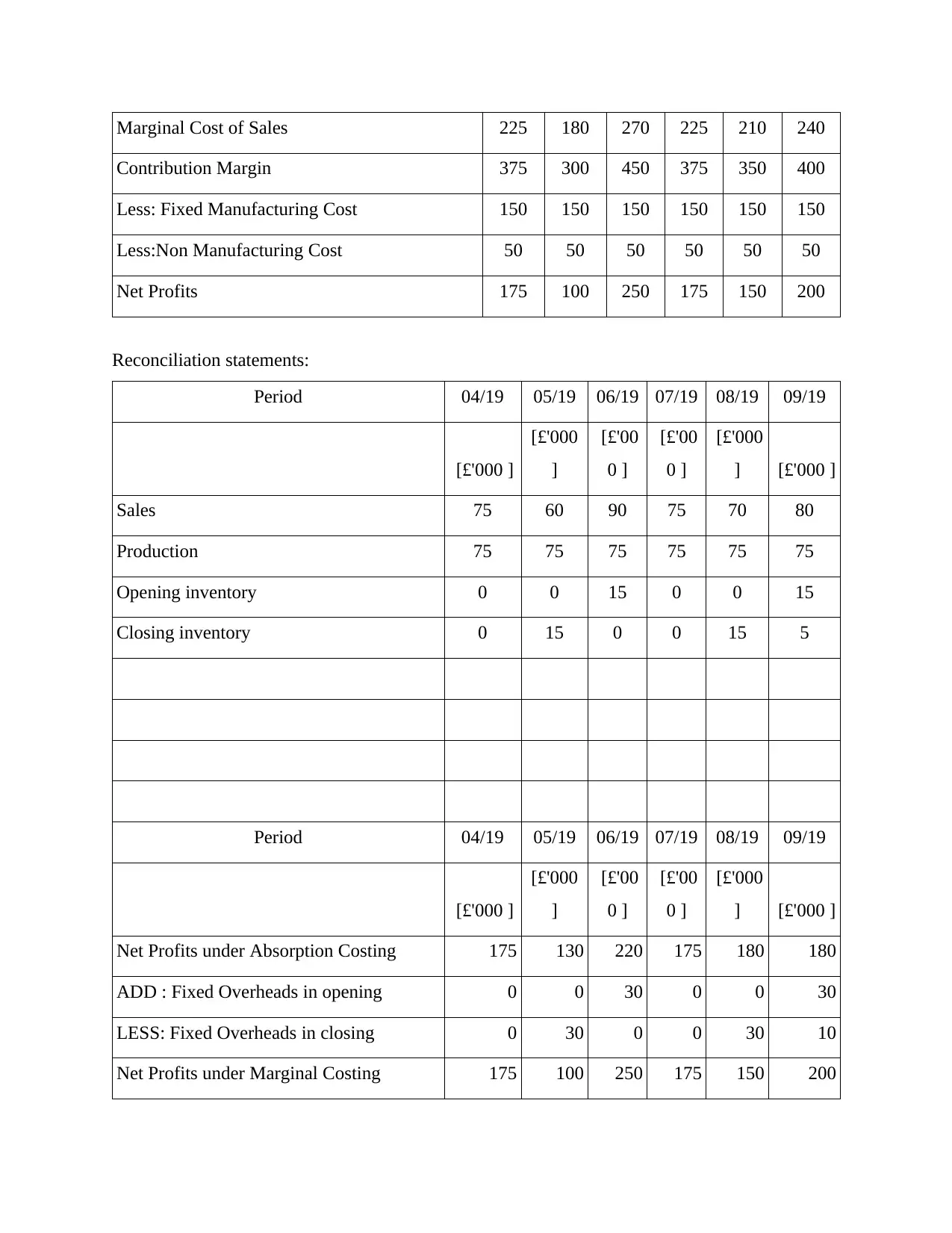

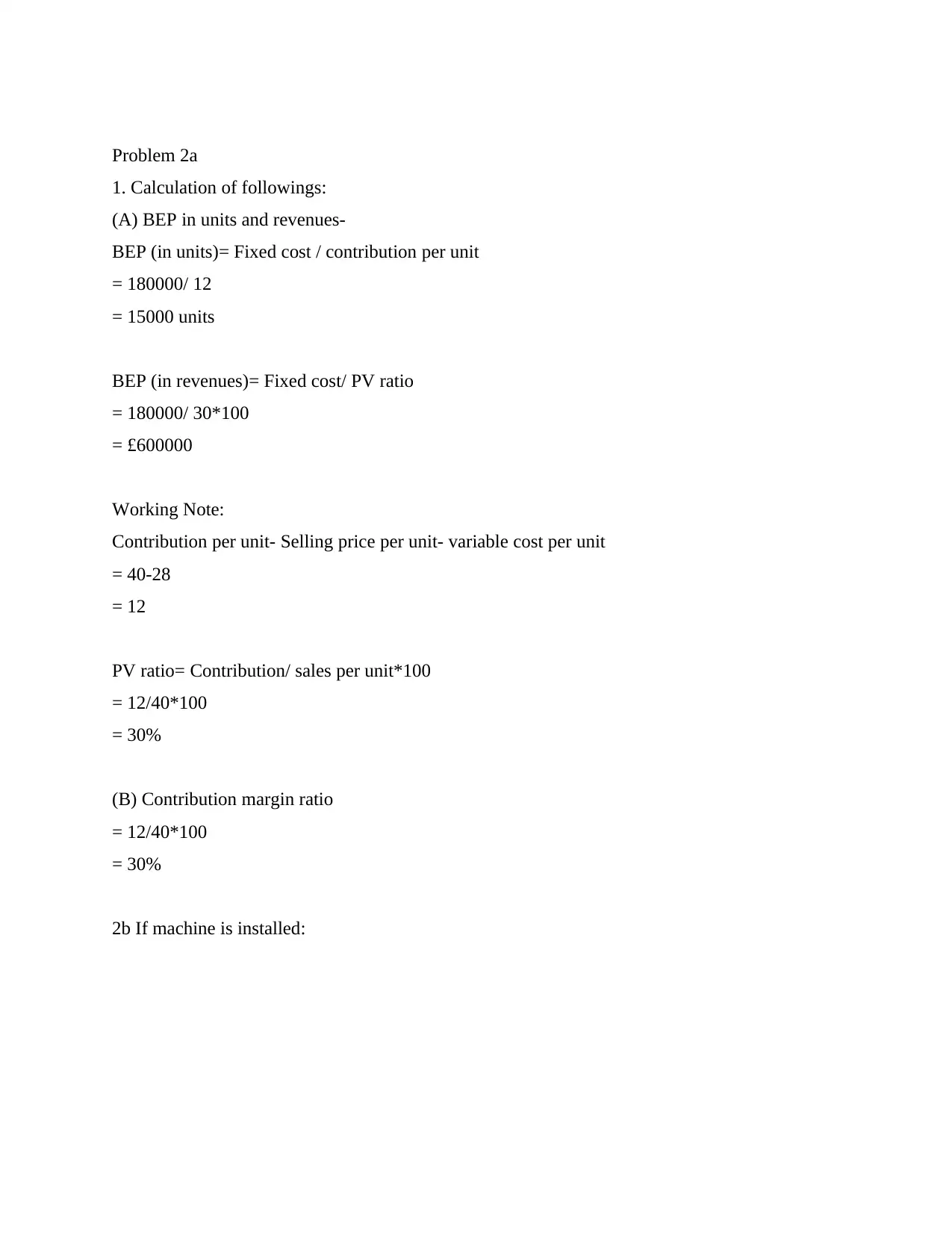

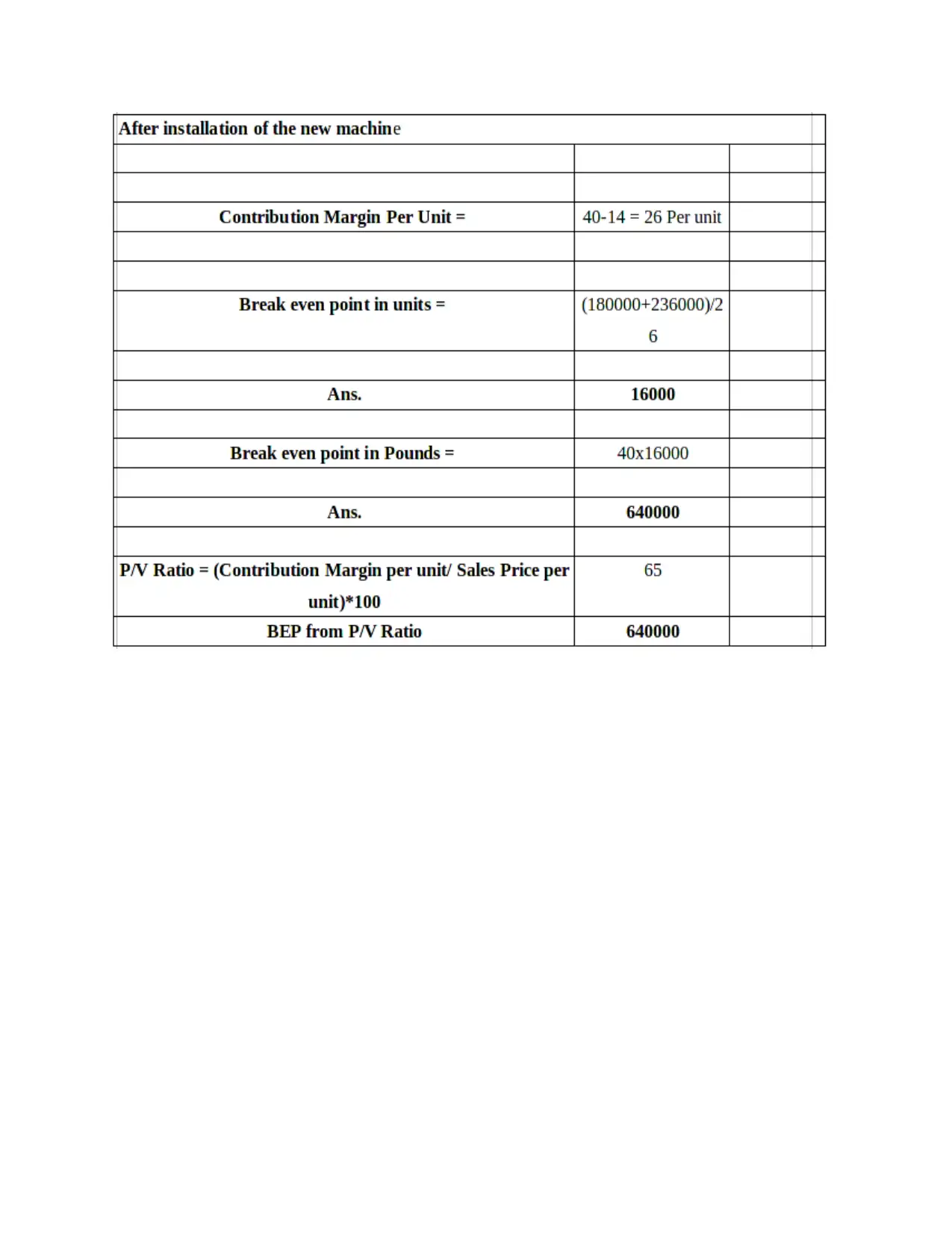

This report provides a comprehensive overview of management accounting principles, using Alpha Limited as a case study. It explores various management accounting systems, including cost accounting, price optimization, inventory management, and job order costing, highlighting their importance in business operations. The report details different methods used for management accounting reporting, such as inventory management reports, performance reports, budget reports, and accounts receivable reports, along with their benefits. Furthermore, it differentiates between management accounting and financial accounting, illustrating the integration of management accounting systems with organizational processes. The report includes the preparation of income statements using both absorption and marginal costing methods, providing a detailed analysis of financial performance under each costing technique. The analysis covers key financial periods, offering insights into sales, production costs, and profitability, making it a valuable resource for understanding management accounting in practice.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.