Management Accounting Report: Systems, Analysis, and Control

VerifiedAdded on 2022/12/12

|14

|4183

|458

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing its core principles and essential requirements for various systems like job costing and inventory management. It delves into different methods used for management accounting reporting, including budget reports, account receivable aging reports, and performance reports. The report also explores cost analysis techniques, specifically marginal and absorption costing, and demonstrates their application in preparing an income statement. Furthermore, it examines the advantages and disadvantages of various planning tools used for budgetary control, and concludes by analyzing how organizations adapt management accounting systems to address financial problems. The report uses Eastern Engineering Co. Ltd. as a case study to illustrate the practical application of these concepts.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................7

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................7

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction

Management accounting is the process of identifying the problem, analysing, interpret the

situations which is helpful of managers to take any decision related to their business profit. It

helps in providing that useful information to managers which is required by them to take major

decisions for business for the growth (Syarif and Novita, 2019). The following report covers

explanation of management accounting and essential requirements of different types of

management accounting systems, different methods used for management accounting reporting,

techniques of cost analysis, advantages and disadvantages of different types of planning tools

used for budgetary control and how organisations are adapting management accounting systems

to respond to financial problems.

Main Body

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting is the process of collecting, analysing and interpreting data which

is essential for managers to take decisions for company’s benefit. It is a wide concept which

cover forecasting and planning, measuring employee’s performance, monitoring cost control

over business, making budgets for other departments and many others. It consists of taking

decisions related to monetary system as well as non monetary system. For example if company

are spending more money than they earn then management accountant checks the financial

documents and take decision to cut down unwanted expenses of business. On the other hand to

increase the employees performance by providing them training is also the work of management

accountant (Ratnadi, Ariyanto and Putra, 2020).

Different types of management accounting systems are explained below-

Job costing system- It is the process of assigning the cost to a particular job role which is

most important job role of the organisation. This is mostly used in construction companies where

each project is assigned with specific cost under which they have to complete their task. Eastern

Engineering Co. Ltd. is a construction company which uses job costing system to analyse the

cost of each project.

Management accounting is the process of identifying the problem, analysing, interpret the

situations which is helpful of managers to take any decision related to their business profit. It

helps in providing that useful information to managers which is required by them to take major

decisions for business for the growth (Syarif and Novita, 2019). The following report covers

explanation of management accounting and essential requirements of different types of

management accounting systems, different methods used for management accounting reporting,

techniques of cost analysis, advantages and disadvantages of different types of planning tools

used for budgetary control and how organisations are adapting management accounting systems

to respond to financial problems.

Main Body

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting is the process of collecting, analysing and interpreting data which

is essential for managers to take decisions for company’s benefit. It is a wide concept which

cover forecasting and planning, measuring employee’s performance, monitoring cost control

over business, making budgets for other departments and many others. It consists of taking

decisions related to monetary system as well as non monetary system. For example if company

are spending more money than they earn then management accountant checks the financial

documents and take decision to cut down unwanted expenses of business. On the other hand to

increase the employees performance by providing them training is also the work of management

accountant (Ratnadi, Ariyanto and Putra, 2020).

Different types of management accounting systems are explained below-

Job costing system- It is the process of assigning the cost to a particular job role which is

most important job role of the organisation. This is mostly used in construction companies where

each project is assigned with specific cost under which they have to complete their task. Eastern

Engineering Co. Ltd. is a construction company which uses job costing system to analyse the

cost of each project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system- This is used to manage inventory of a particular business.

In involves the management of manufactured goods, management of warehouses, management

of supply chain and many others. This management system is required for manufacturing

industries that manufacture goods in bulk and store them in warehouses for future use. It

involves that how manufactured products can be arranged in warehouses that which product and

in how much amount will be kept in which section of warehouse. A proper inventory

management system plays an important role in managing supply chain of a company.

Price optimization system- It is the managerial accounting system where company

decrease and increases the prices of their product according to the situation in market (Mariina

and Tjahjadi, 2020). The main aim of this system is to enhance the quick selling of products at

right places which makes profit for the company. Here, companies up and down the supply chain

for business to business and for business to customer settings.

Cost accounting system- This is the managerial accounting system which is mostly used

by manufacturing industry to record the production activities of their company. This system

records all activities of production like purchasing of raw material, converting the raw material

to finished goods and many others. It tracks the flow of inventory through the various stages of

production.

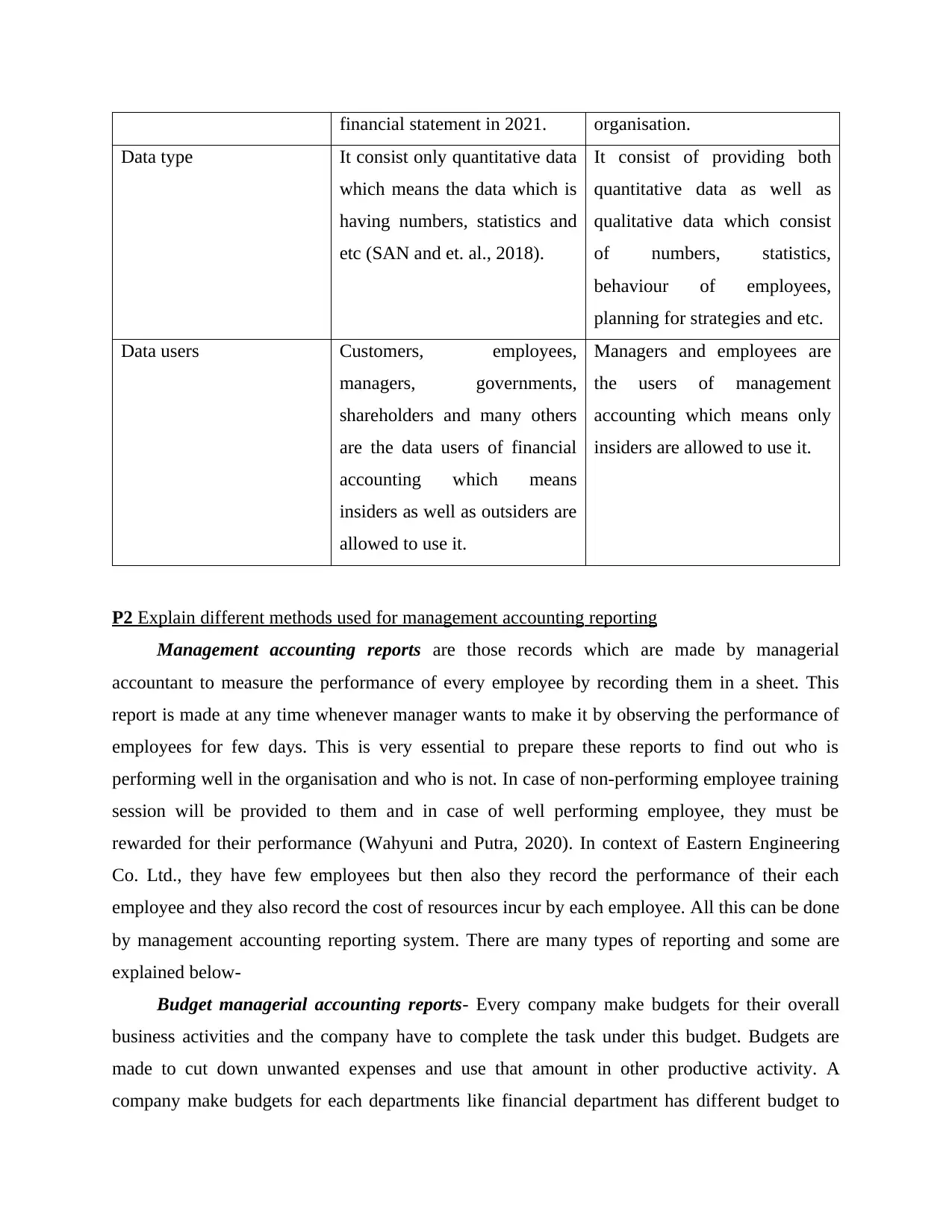

The difference between financial accounting and managerial accounting are explained below-

Basis of Difference Financial Accounting Management Accounting

Main aim The main aim of financial

accounting is to provide

information related to finance

to interested parties like

customers, employers,

stakeholders and many others.

The main aim of management

accounting is to provide useful

decision which is helpful in

taking business decisions for

the benefit of company.

Time period It can be made at the end of

financial year and it involve the

past 1 year of expenses and

revenues. For example 2019

financial statement will be

shown in 2020 and 2020

There is no fix time to use

management accounting. It’s

upon the will of managers that

anytime anywhere they can

prepare reports. It’s basically

focuses on future activities of

In involves the management of manufactured goods, management of warehouses, management

of supply chain and many others. This management system is required for manufacturing

industries that manufacture goods in bulk and store them in warehouses for future use. It

involves that how manufactured products can be arranged in warehouses that which product and

in how much amount will be kept in which section of warehouse. A proper inventory

management system plays an important role in managing supply chain of a company.

Price optimization system- It is the managerial accounting system where company

decrease and increases the prices of their product according to the situation in market (Mariina

and Tjahjadi, 2020). The main aim of this system is to enhance the quick selling of products at

right places which makes profit for the company. Here, companies up and down the supply chain

for business to business and for business to customer settings.

Cost accounting system- This is the managerial accounting system which is mostly used

by manufacturing industry to record the production activities of their company. This system

records all activities of production like purchasing of raw material, converting the raw material

to finished goods and many others. It tracks the flow of inventory through the various stages of

production.

The difference between financial accounting and managerial accounting are explained below-

Basis of Difference Financial Accounting Management Accounting

Main aim The main aim of financial

accounting is to provide

information related to finance

to interested parties like

customers, employers,

stakeholders and many others.

The main aim of management

accounting is to provide useful

decision which is helpful in

taking business decisions for

the benefit of company.

Time period It can be made at the end of

financial year and it involve the

past 1 year of expenses and

revenues. For example 2019

financial statement will be

shown in 2020 and 2020

There is no fix time to use

management accounting. It’s

upon the will of managers that

anytime anywhere they can

prepare reports. It’s basically

focuses on future activities of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statement in 2021. organisation.

Data type It consist only quantitative data

which means the data which is

having numbers, statistics and

etc (SAN and et. al., 2018).

It consist of providing both

quantitative data as well as

qualitative data which consist

of numbers, statistics,

behaviour of employees,

planning for strategies and etc.

Data users Customers, employees,

managers, governments,

shareholders and many others

are the data users of financial

accounting which means

insiders as well as outsiders are

allowed to use it.

Managers and employees are

the users of management

accounting which means only

insiders are allowed to use it.

P2 Explain different methods used for management accounting reporting

Management accounting reports are those records which are made by managerial

accountant to measure the performance of every employee by recording them in a sheet. This

report is made at any time whenever manager wants to make it by observing the performance of

employees for few days. This is very essential to prepare these reports to find out who is

performing well in the organisation and who is not. In case of non-performing employee training

session will be provided to them and in case of well performing employee, they must be

rewarded for their performance (Wahyuni and Putra, 2020). In context of Eastern Engineering

Co. Ltd., they have few employees but then also they record the performance of their each

employee and they also record the cost of resources incur by each employee. All this can be done

by management accounting reporting system. There are many types of reporting and some are

explained below-

Budget managerial accounting reports- Every company make budgets for their overall

business activities and the company have to complete the task under this budget. Budgets are

made to cut down unwanted expenses and use that amount in other productive activity. A

company make budgets for each departments like financial department has different budget to

Data type It consist only quantitative data

which means the data which is

having numbers, statistics and

etc (SAN and et. al., 2018).

It consist of providing both

quantitative data as well as

qualitative data which consist

of numbers, statistics,

behaviour of employees,

planning for strategies and etc.

Data users Customers, employees,

managers, governments,

shareholders and many others

are the data users of financial

accounting which means

insiders as well as outsiders are

allowed to use it.

Managers and employees are

the users of management

accounting which means only

insiders are allowed to use it.

P2 Explain different methods used for management accounting reporting

Management accounting reports are those records which are made by managerial

accountant to measure the performance of every employee by recording them in a sheet. This

report is made at any time whenever manager wants to make it by observing the performance of

employees for few days. This is very essential to prepare these reports to find out who is

performing well in the organisation and who is not. In case of non-performing employee training

session will be provided to them and in case of well performing employee, they must be

rewarded for their performance (Wahyuni and Putra, 2020). In context of Eastern Engineering

Co. Ltd., they have few employees but then also they record the performance of their each

employee and they also record the cost of resources incur by each employee. All this can be done

by management accounting reporting system. There are many types of reporting and some are

explained below-

Budget managerial accounting reports- Every company make budgets for their overall

business activities and the company have to complete the task under this budget. Budgets are

made to cut down unwanted expenses and use that amount in other productive activity. A

company make budgets for each departments like financial department has different budget to

work, marketing department has different budget, and production department is assigned with

other budget and many more. All these departments have to work under their budget. In case any

department cross the budget line then there is some kind of unproductive activity in that

department which means that department is not performing well. On the other who work under

fixed budget is well perform department. Eastern Engineering Co. Ltd makes budgets for their

each department so that they can work separately with full flexibility. This also helps Eastern

Engineering to eliminate their unwanted expenses on unproductive activities in some

departments which can be identified only by using budgets.

Account Receivable Aging Reports- This report is made in the case of business relies on

extending credits most of the time. Hence, to identify the reason of delay in payments to clients

and paying back the credit loans this reporting system is used (Kurniati, Haji and Renaningtyas,

2019). Basically, manager breakdown the amount of client and also breakdown the time period

to measure defaulters of business who acts as obstacles for paying back the credits of business.

In case of many defaulters then manager must change whole credit policy of company and in

case only few members is found as defaulters then manager must give them warning for such

irresponsibility in organisation. Bad debts must be written off as soon as possible. Making it a

habit of paying delay of all credits is not a good thing for business. This report is made by

Eastern Engineering to check whether there are any credits on them or not and in case of late

payment of bad debts then it uses to identify that what is the reason of late payment of bad debts.

Performance Reports- Performance report is made to check the overall performance of

whole organisation as well as to check the performance of each employee within an organisation.

These reports are made to identify which employee is performing well and which is not

(KARSHALOVA and et. al., 2018). This is also done by department wise. Manager observe

everything from employees activity at workplace to financial reports and background of that

employee then manager record the performance in their sheets and at the end of every month

they conduct a meeting to discuss what’s going on in organisation that who is performing well

and who is not and what are the reasons of not performing well. This records are also helpful to

motivate workforce by providing rewards to well performed employees and providing training

sessions for non-performing employees. This performance reports are also considered as helpful

for employers to identify where they are lacking behind and what measures can be done to

improve their performance. In context of Eastern Engineering company, they are dealing under

other budget and many more. All these departments have to work under their budget. In case any

department cross the budget line then there is some kind of unproductive activity in that

department which means that department is not performing well. On the other who work under

fixed budget is well perform department. Eastern Engineering Co. Ltd makes budgets for their

each department so that they can work separately with full flexibility. This also helps Eastern

Engineering to eliminate their unwanted expenses on unproductive activities in some

departments which can be identified only by using budgets.

Account Receivable Aging Reports- This report is made in the case of business relies on

extending credits most of the time. Hence, to identify the reason of delay in payments to clients

and paying back the credit loans this reporting system is used (Kurniati, Haji and Renaningtyas,

2019). Basically, manager breakdown the amount of client and also breakdown the time period

to measure defaulters of business who acts as obstacles for paying back the credits of business.

In case of many defaulters then manager must change whole credit policy of company and in

case only few members is found as defaulters then manager must give them warning for such

irresponsibility in organisation. Bad debts must be written off as soon as possible. Making it a

habit of paying delay of all credits is not a good thing for business. This report is made by

Eastern Engineering to check whether there are any credits on them or not and in case of late

payment of bad debts then it uses to identify that what is the reason of late payment of bad debts.

Performance Reports- Performance report is made to check the overall performance of

whole organisation as well as to check the performance of each employee within an organisation.

These reports are made to identify which employee is performing well and which is not

(KARSHALOVA and et. al., 2018). This is also done by department wise. Manager observe

everything from employees activity at workplace to financial reports and background of that

employee then manager record the performance in their sheets and at the end of every month

they conduct a meeting to discuss what’s going on in organisation that who is performing well

and who is not and what are the reasons of not performing well. This records are also helpful to

motivate workforce by providing rewards to well performed employees and providing training

sessions for non-performing employees. This performance reports are also considered as helpful

for employers to identify where they are lacking behind and what measures can be done to

improve their performance. In context of Eastern Engineering company, they are dealing under

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

construction industry where the performance of every employee is based upon the effectiveness

of their projects under low cost as much as possible. Hence, their performance reports are made

upon success of their projects on construction sites.

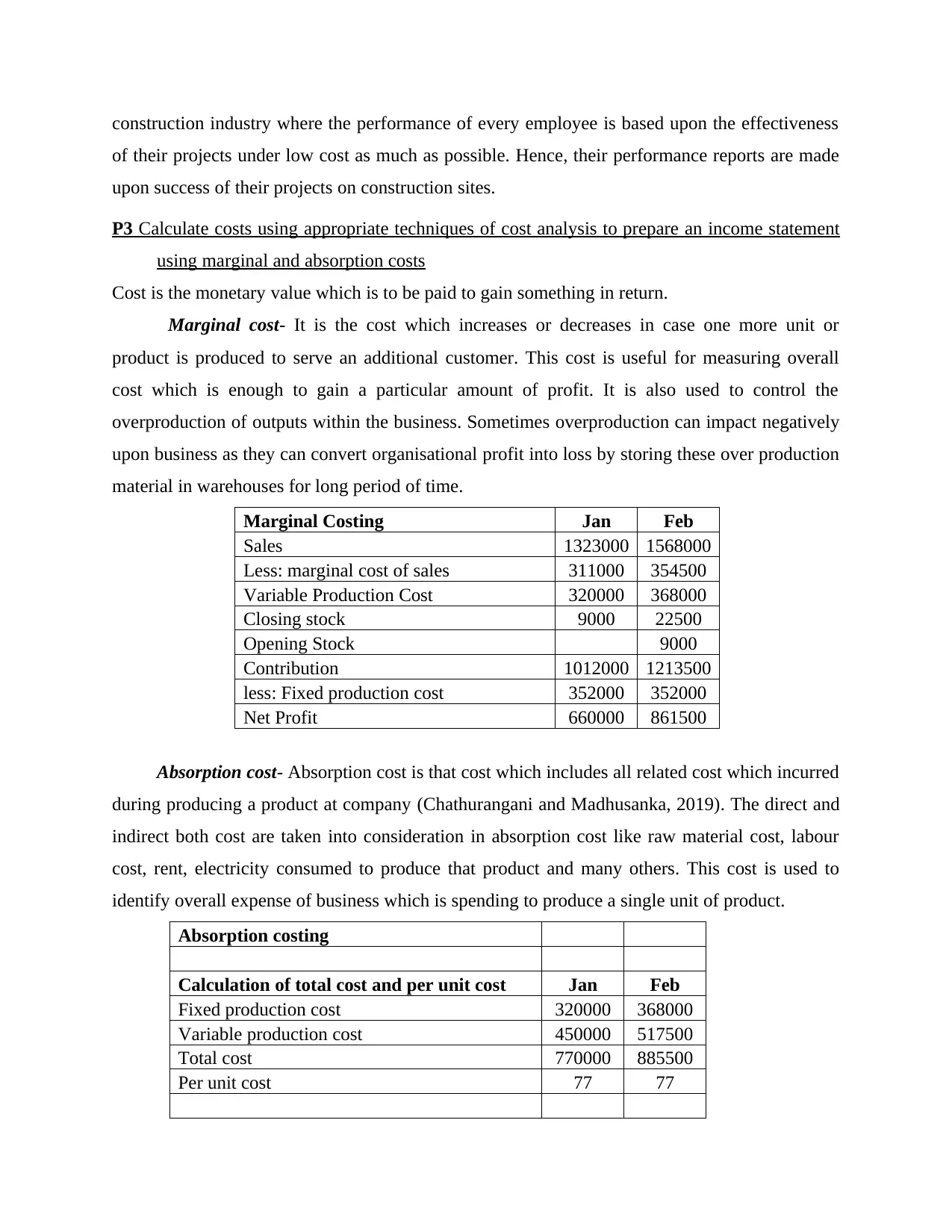

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Cost is the monetary value which is to be paid to gain something in return.

Marginal cost- It is the cost which increases or decreases in case one more unit or

product is produced to serve an additional customer. This cost is useful for measuring overall

cost which is enough to gain a particular amount of profit. It is also used to control the

overproduction of outputs within the business. Sometimes overproduction can impact negatively

upon business as they can convert organisational profit into loss by storing these over production

material in warehouses for long period of time.

Marginal Costing Jan Feb

Sales 1323000 1568000

Less: marginal cost of sales 311000 354500

Variable Production Cost 320000 368000

Closing stock 9000 22500

Opening Stock 9000

Contribution 1012000 1213500

less: Fixed production cost 352000 352000

Net Profit 660000 861500

Absorption cost- Absorption cost is that cost which includes all related cost which incurred

during producing a product at company (Chathurangani and Madhusanka, 2019). The direct and

indirect both cost are taken into consideration in absorption cost like raw material cost, labour

cost, rent, electricity consumed to produce that product and many others. This cost is used to

identify overall expense of business which is spending to produce a single unit of product.

Absorption costing

Calculation of total cost and per unit cost Jan Feb

Fixed production cost 320000 368000

Variable production cost 450000 517500

Total cost 770000 885500

Per unit cost 77 77

of their projects under low cost as much as possible. Hence, their performance reports are made

upon success of their projects on construction sites.

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Cost is the monetary value which is to be paid to gain something in return.

Marginal cost- It is the cost which increases or decreases in case one more unit or

product is produced to serve an additional customer. This cost is useful for measuring overall

cost which is enough to gain a particular amount of profit. It is also used to control the

overproduction of outputs within the business. Sometimes overproduction can impact negatively

upon business as they can convert organisational profit into loss by storing these over production

material in warehouses for long period of time.

Marginal Costing Jan Feb

Sales 1323000 1568000

Less: marginal cost of sales 311000 354500

Variable Production Cost 320000 368000

Closing stock 9000 22500

Opening Stock 9000

Contribution 1012000 1213500

less: Fixed production cost 352000 352000

Net Profit 660000 861500

Absorption cost- Absorption cost is that cost which includes all related cost which incurred

during producing a product at company (Chathurangani and Madhusanka, 2019). The direct and

indirect both cost are taken into consideration in absorption cost like raw material cost, labour

cost, rent, electricity consumed to produce that product and many others. This cost is used to

identify overall expense of business which is spending to produce a single unit of product.

Absorption costing

Calculation of total cost and per unit cost Jan Feb

Fixed production cost 320000 368000

Variable production cost 450000 517500

Total cost 770000 885500

Per unit cost 77 77

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

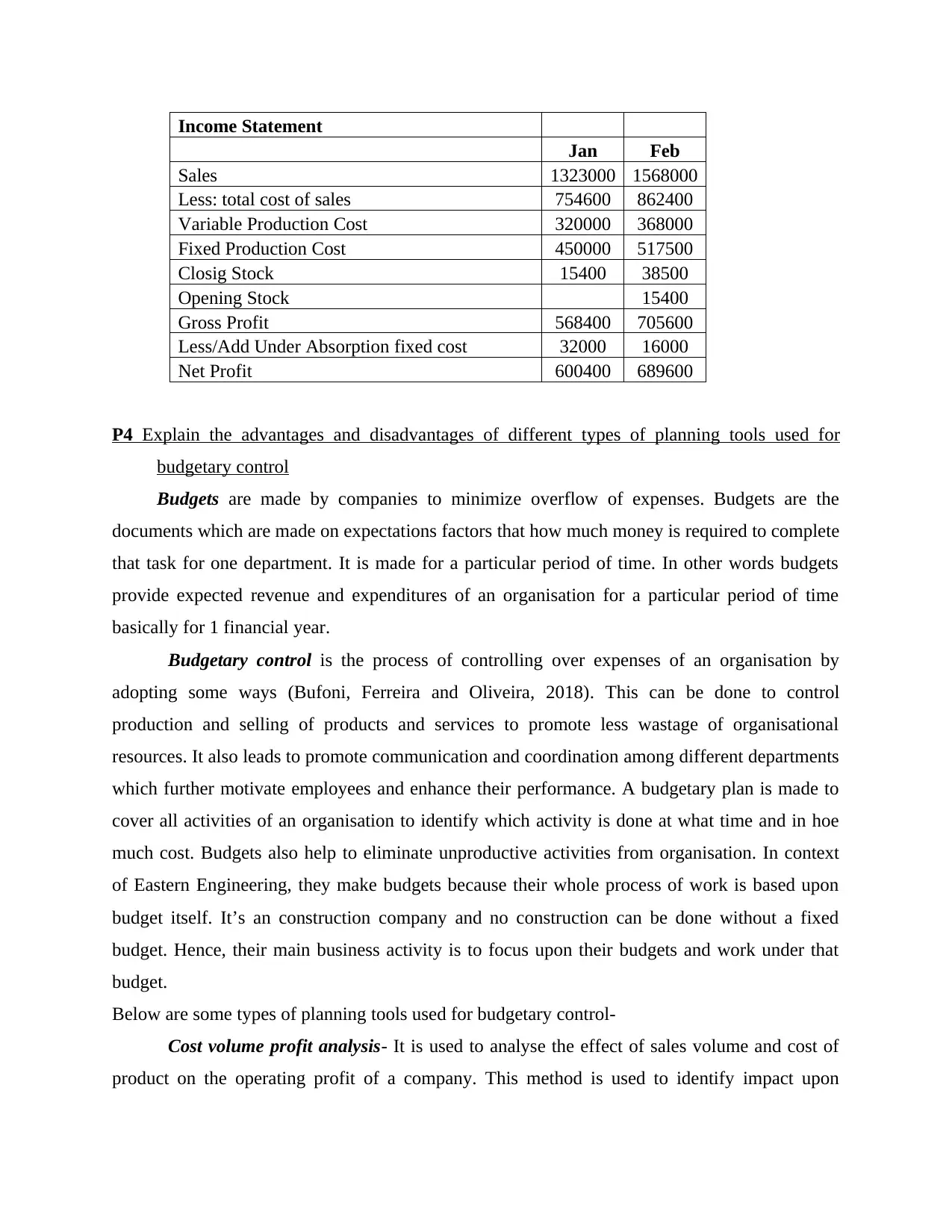

Income Statement

Jan Feb

Sales 1323000 1568000

Less: total cost of sales 754600 862400

Variable Production Cost 320000 368000

Fixed Production Cost 450000 517500

Closig Stock 15400 38500

Opening Stock 15400

Gross Profit 568400 705600

Less/Add Under Absorption fixed cost 32000 16000

Net Profit 600400 689600

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budgets are made by companies to minimize overflow of expenses. Budgets are the

documents which are made on expectations factors that how much money is required to complete

that task for one department. It is made for a particular period of time. In other words budgets

provide expected revenue and expenditures of an organisation for a particular period of time

basically for 1 financial year.

Budgetary control is the process of controlling over expenses of an organisation by

adopting some ways (Bufoni, Ferreira and Oliveira, 2018). This can be done to control

production and selling of products and services to promote less wastage of organisational

resources. It also leads to promote communication and coordination among different departments

which further motivate employees and enhance their performance. A budgetary plan is made to

cover all activities of an organisation to identify which activity is done at what time and in hoe

much cost. Budgets also help to eliminate unproductive activities from organisation. In context

of Eastern Engineering, they make budgets because their whole process of work is based upon

budget itself. It’s an construction company and no construction can be done without a fixed

budget. Hence, their main business activity is to focus upon their budgets and work under that

budget.

Below are some types of planning tools used for budgetary control-

Cost volume profit analysis- It is used to analyse the effect of sales volume and cost of

product on the operating profit of a company. This method is used to identify impact upon

Jan Feb

Sales 1323000 1568000

Less: total cost of sales 754600 862400

Variable Production Cost 320000 368000

Fixed Production Cost 450000 517500

Closig Stock 15400 38500

Opening Stock 15400

Gross Profit 568400 705600

Less/Add Under Absorption fixed cost 32000 16000

Net Profit 600400 689600

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budgets are made by companies to minimize overflow of expenses. Budgets are the

documents which are made on expectations factors that how much money is required to complete

that task for one department. It is made for a particular period of time. In other words budgets

provide expected revenue and expenditures of an organisation for a particular period of time

basically for 1 financial year.

Budgetary control is the process of controlling over expenses of an organisation by

adopting some ways (Bufoni, Ferreira and Oliveira, 2018). This can be done to control

production and selling of products and services to promote less wastage of organisational

resources. It also leads to promote communication and coordination among different departments

which further motivate employees and enhance their performance. A budgetary plan is made to

cover all activities of an organisation to identify which activity is done at what time and in hoe

much cost. Budgets also help to eliminate unproductive activities from organisation. In context

of Eastern Engineering, they make budgets because their whole process of work is based upon

budget itself. It’s an construction company and no construction can be done without a fixed

budget. Hence, their main business activity is to focus upon their budgets and work under that

budget.

Below are some types of planning tools used for budgetary control-

Cost volume profit analysis- It is used to analyse the effect of sales volume and cost of

product on the operating profit of a company. This method is used to identify impact upon

operating profit by changing in variable cost, fixed cost, selling price per unit and many more

expenses related to sale and production of product. Cost volume profit analysis is a planning tool

which is used by companies to estimate their revenue and expenses from sales, production (Boyd

and Pitre, 2020). This method further help to analyse by a mathematical formula that how change

to cost and sales volume will affect future profit generation for a particular period of time. This

method is also used by manages to identify the breakeven point of product which further means

the case of no profit and no loss.

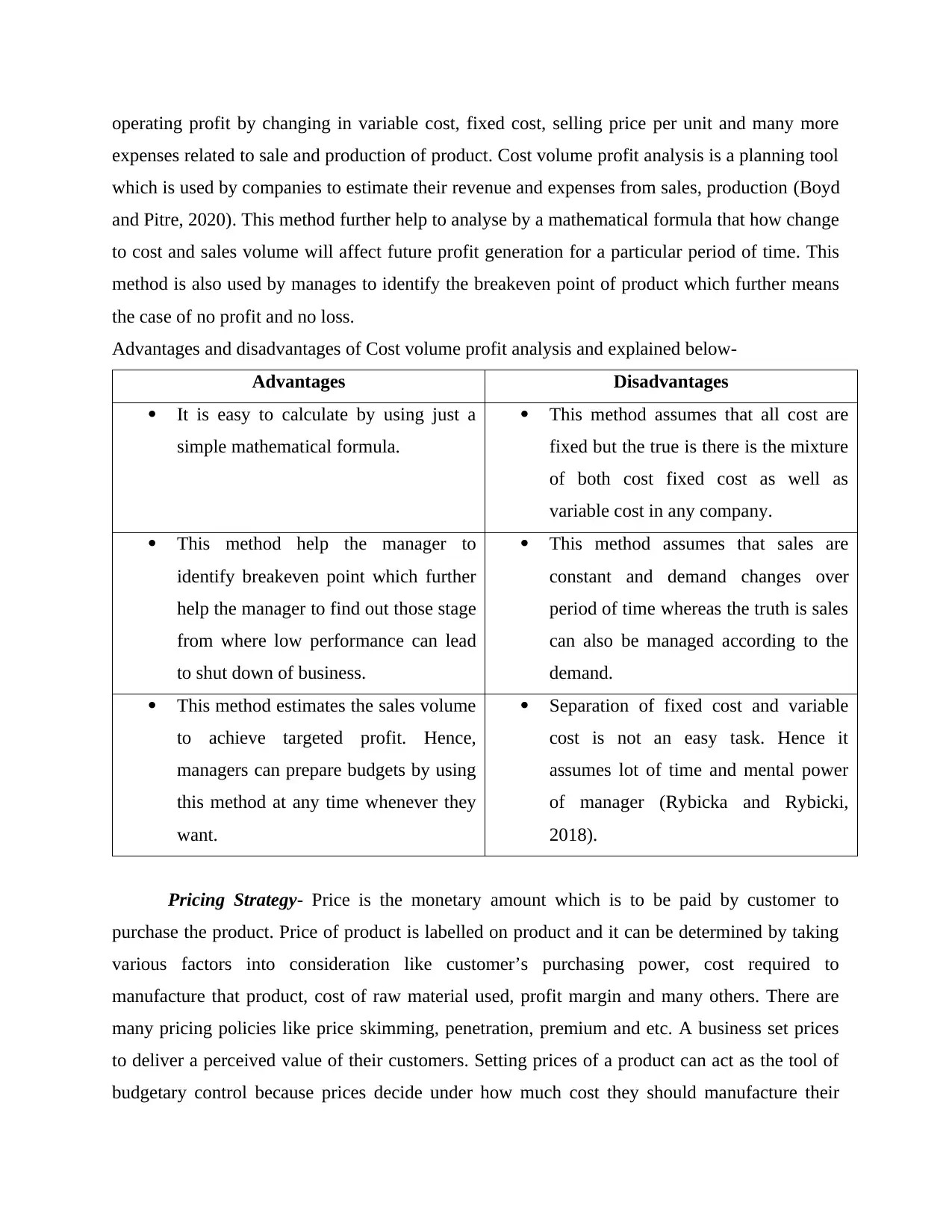

Advantages and disadvantages of Cost volume profit analysis and explained below-

Advantages Disadvantages

It is easy to calculate by using just a

simple mathematical formula.

This method assumes that all cost are

fixed but the true is there is the mixture

of both cost fixed cost as well as

variable cost in any company.

This method help the manager to

identify breakeven point which further

help the manager to find out those stage

from where low performance can lead

to shut down of business.

This method assumes that sales are

constant and demand changes over

period of time whereas the truth is sales

can also be managed according to the

demand.

This method estimates the sales volume

to achieve targeted profit. Hence,

managers can prepare budgets by using

this method at any time whenever they

want.

Separation of fixed cost and variable

cost is not an easy task. Hence it

assumes lot of time and mental power

of manager (Rybicka and Rybicki,

2018).

Pricing Strategy- Price is the monetary amount which is to be paid by customer to

purchase the product. Price of product is labelled on product and it can be determined by taking

various factors into consideration like customer’s purchasing power, cost required to

manufacture that product, cost of raw material used, profit margin and many others. There are

many pricing policies like price skimming, penetration, premium and etc. A business set prices

to deliver a perceived value of their customers. Setting prices of a product can act as the tool of

budgetary control because prices decide under how much cost they should manufacture their

expenses related to sale and production of product. Cost volume profit analysis is a planning tool

which is used by companies to estimate their revenue and expenses from sales, production (Boyd

and Pitre, 2020). This method further help to analyse by a mathematical formula that how change

to cost and sales volume will affect future profit generation for a particular period of time. This

method is also used by manages to identify the breakeven point of product which further means

the case of no profit and no loss.

Advantages and disadvantages of Cost volume profit analysis and explained below-

Advantages Disadvantages

It is easy to calculate by using just a

simple mathematical formula.

This method assumes that all cost are

fixed but the true is there is the mixture

of both cost fixed cost as well as

variable cost in any company.

This method help the manager to

identify breakeven point which further

help the manager to find out those stage

from where low performance can lead

to shut down of business.

This method assumes that sales are

constant and demand changes over

period of time whereas the truth is sales

can also be managed according to the

demand.

This method estimates the sales volume

to achieve targeted profit. Hence,

managers can prepare budgets by using

this method at any time whenever they

want.

Separation of fixed cost and variable

cost is not an easy task. Hence it

assumes lot of time and mental power

of manager (Rybicka and Rybicki,

2018).

Pricing Strategy- Price is the monetary amount which is to be paid by customer to

purchase the product. Price of product is labelled on product and it can be determined by taking

various factors into consideration like customer’s purchasing power, cost required to

manufacture that product, cost of raw material used, profit margin and many others. There are

many pricing policies like price skimming, penetration, premium and etc. A business set prices

to deliver a perceived value of their customers. Setting prices of a product can act as the tool of

budgetary control because prices decide under how much cost they should manufacture their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products (Ostaev and et. al., 2019). For example the price of a product is $8 then it is compulsory

to produce that product under the cost of $8 only. In case cost exceed the price then company

have to face loss. Hence, pricing strategy is also a good tool for budgetary control.

Advantages and disadvantages of pricing strategies and explained below-

Advantages Disadvantages

Pricing strategy is not only used to

control the budgets but it also used to

attract more customers.

Most of the time companies set prices

according to cost incurred to

manufacture that product and they did

not consider that factor of willingness

to pay by customers which further

results in declining in overall sales.

It helps in determining all factors which

is used for setting prices which help the

company to know what will impact

upon these factors and what are not.

Calculating price of a product is very

complicated. Hence it includes lot of

time and mind power to decide actual

price of product (Balios, 2021).

Using low pricing helps to attract more

customers and using high prices help to

make standard and it implies good

quality of product.

Using low prices may put question on

quality of product and using high prices

can lead to switch customers perception

toward other brand.

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems are the problem which take place due to lack of adequate finance within an

organisation, inefficient use of business finance, spending too much money upon unproductive

activities, not paying credit loans on time and many others. Finance is the backbone of every

company because all activities are depends on it from purchasing raw material to delivering

finished goods to customers (Shalaeva, 2018). It is compulsory to overcome with financial issues

as soon as possible for effective working of each department. Comparison of Eastern

Engineering Company with Sigma Constructions in context of their different financial problems

and different ways to overcome with their financial issues are explained below-

to produce that product under the cost of $8 only. In case cost exceed the price then company

have to face loss. Hence, pricing strategy is also a good tool for budgetary control.

Advantages and disadvantages of pricing strategies and explained below-

Advantages Disadvantages

Pricing strategy is not only used to

control the budgets but it also used to

attract more customers.

Most of the time companies set prices

according to cost incurred to

manufacture that product and they did

not consider that factor of willingness

to pay by customers which further

results in declining in overall sales.

It helps in determining all factors which

is used for setting prices which help the

company to know what will impact

upon these factors and what are not.

Calculating price of a product is very

complicated. Hence it includes lot of

time and mind power to decide actual

price of product (Balios, 2021).

Using low pricing helps to attract more

customers and using high prices help to

make standard and it implies good

quality of product.

Using low prices may put question on

quality of product and using high prices

can lead to switch customers perception

toward other brand.

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems are the problem which take place due to lack of adequate finance within an

organisation, inefficient use of business finance, spending too much money upon unproductive

activities, not paying credit loans on time and many others. Finance is the backbone of every

company because all activities are depends on it from purchasing raw material to delivering

finished goods to customers (Shalaeva, 2018). It is compulsory to overcome with financial issues

as soon as possible for effective working of each department. Comparison of Eastern

Engineering Company with Sigma Constructions in context of their different financial problems

and different ways to overcome with their financial issues are explained below-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

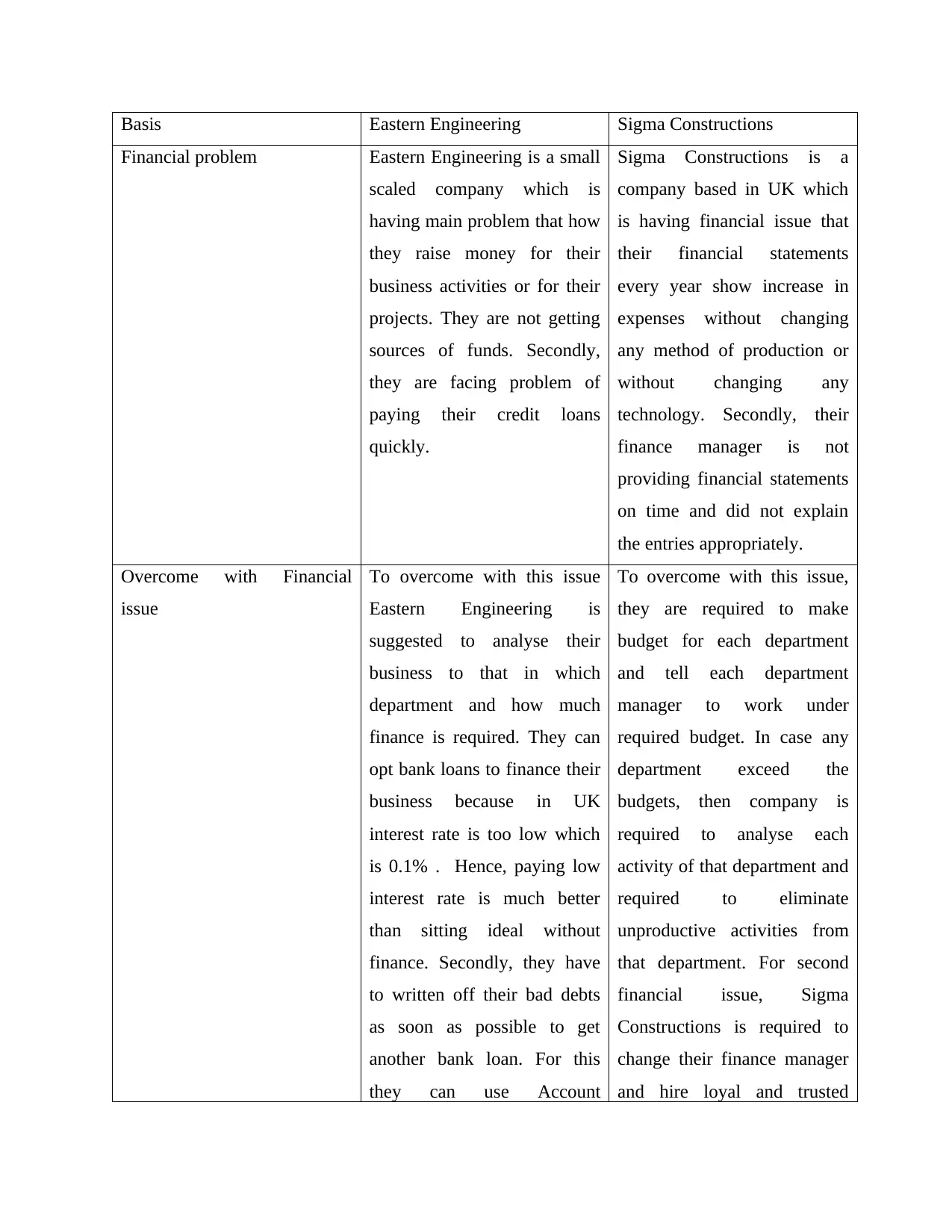

Basis Eastern Engineering Sigma Constructions

Financial problem Eastern Engineering is a small

scaled company which is

having main problem that how

they raise money for their

business activities or for their

projects. They are not getting

sources of funds. Secondly,

they are facing problem of

paying their credit loans

quickly.

Sigma Constructions is a

company based in UK which

is having financial issue that

their financial statements

every year show increase in

expenses without changing

any method of production or

without changing any

technology. Secondly, their

finance manager is not

providing financial statements

on time and did not explain

the entries appropriately.

Overcome with Financial

issue

To overcome with this issue

Eastern Engineering is

suggested to analyse their

business to that in which

department and how much

finance is required. They can

opt bank loans to finance their

business because in UK

interest rate is too low which

is 0.1% . Hence, paying low

interest rate is much better

than sitting ideal without

finance. Secondly, they have

to written off their bad debts

as soon as possible to get

another bank loan. For this

they can use Account

To overcome with this issue,

they are required to make

budget for each department

and tell each department

manager to work under

required budget. In case any

department exceed the

budgets, then company is

required to analyse each

activity of that department and

required to eliminate

unproductive activities from

that department. For second

financial issue, Sigma

Constructions is required to

change their finance manager

and hire loyal and trusted

Financial problem Eastern Engineering is a small

scaled company which is

having main problem that how

they raise money for their

business activities or for their

projects. They are not getting

sources of funds. Secondly,

they are facing problem of

paying their credit loans

quickly.

Sigma Constructions is a

company based in UK which

is having financial issue that

their financial statements

every year show increase in

expenses without changing

any method of production or

without changing any

technology. Secondly, their

finance manager is not

providing financial statements

on time and did not explain

the entries appropriately.

Overcome with Financial

issue

To overcome with this issue

Eastern Engineering is

suggested to analyse their

business to that in which

department and how much

finance is required. They can

opt bank loans to finance their

business because in UK

interest rate is too low which

is 0.1% . Hence, paying low

interest rate is much better

than sitting ideal without

finance. Secondly, they have

to written off their bad debts

as soon as possible to get

another bank loan. For this

they can use Account

To overcome with this issue,

they are required to make

budget for each department

and tell each department

manager to work under

required budget. In case any

department exceed the

budgets, then company is

required to analyse each

activity of that department and

required to eliminate

unproductive activities from

that department. For second

financial issue, Sigma

Constructions is required to

change their finance manager

and hire loyal and trusted

Receivable Aging Reports

method which identify who

are defaulters for not paying

the credit loans on time

(Abugalia and Mehafdi,

2018).

financial manager who make

time to time financial

statement for company at the

end of every financial year

and willing to describe it to

managerial accountant if

required. Hence, hiring

experience good reputed

financial manager is

important.

Conclusion

From the above information it is concluded that management accounting is used to gather those

useful data which is used to take essential business decisions. Reporting is the process of

measuring performance and take corrective measures to overcome the issues and problems and

there are many methods of management accounting like Budget managerial accounting reports,

account Receivable Aging Reports and many others. Cost is the value of producing the product.

Budgets are made to control the unwanted expenses and enhance the performance of employees

to achieve organisational goal on time. Financial problems are those problems which are related

to finance like lack of funds, improper use of funds, delay in paying credit loans and many

others. It is compulsory to overcome with financial issues as soon as possible for the profit of

company. Finance must be managed properly.

method which identify who

are defaulters for not paying

the credit loans on time

(Abugalia and Mehafdi,

2018).

financial manager who make

time to time financial

statement for company at the

end of every financial year

and willing to describe it to

managerial accountant if

required. Hence, hiring

experience good reputed

financial manager is

important.

Conclusion

From the above information it is concluded that management accounting is used to gather those

useful data which is used to take essential business decisions. Reporting is the process of

measuring performance and take corrective measures to overcome the issues and problems and

there are many methods of management accounting like Budget managerial accounting reports,

account Receivable Aging Reports and many others. Cost is the value of producing the product.

Budgets are made to control the unwanted expenses and enhance the performance of employees

to achieve organisational goal on time. Financial problems are those problems which are related

to finance like lack of funds, improper use of funds, delay in paying credit loans and many

others. It is compulsory to overcome with financial issues as soon as possible for the profit of

company. Finance must be managed properly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.