Management Accounting Report: Ikea Inventory and Financial Data

VerifiedAdded on 2023/01/13

|20

|4609

|24

Report

AI Summary

This management accounting report provides a comprehensive overview of the subject, beginning with a definition of management accounting and its functions within an organization. It differentiates between financial and management accounting, highlighting their distinct purposes and requirements. The report delves into various management accounting systems, including cost accounting, inventory management, and job costing systems, along with their applications and benefits. It includes an analysis of financial data, comparing absorption and marginal costing methods, and presents different types of management accounting reports, such as inventory and accounts receivable aging reports, along with budgeting techniques. The report also examines the integration of different management accounting systems and explores various budgeting methods like zero-based budgeting. Furthermore, it provides insights into measuring tools and the characteristics of effective management accountants, including a case study on Ikea's inventory management system. The report concludes by summarizing key findings and offering recommendations for effective management accounting practices.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

MA Definition........................................................................................................................1

Function of MA......................................................................................................................1

Difference between Financial and MA...................................................................................2

Requirement of MA................................................................................................................2

MA System, application and benefits.....................................................................................3

Financial Data of Company....................................................................................................5

Different type of MA report...................................................................................................8

Different type of Budgeting..................................................................................................10

Different type of measuring tool..........................................................................................12

Characteristic of effective management Accountant............................................................13

Difference between adoption of MA system in organization...............................................13

Ikea inventory management system.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

MA Definition........................................................................................................................1

Function of MA......................................................................................................................1

Difference between Financial and MA...................................................................................2

Requirement of MA................................................................................................................2

MA System, application and benefits.....................................................................................3

Financial Data of Company....................................................................................................5

Different type of MA report...................................................................................................8

Different type of Budgeting..................................................................................................10

Different type of measuring tool..........................................................................................12

Characteristic of effective management Accountant............................................................13

Difference between adoption of MA system in organization...............................................13

Ikea inventory management system.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is the process in which organization uses different report in the

organization to improve the performance of the business. Katie walker Furniture, is the

organization who has to consider dealt in the retail sector of the nation. This report explain the

critical evaluation of MA and system in the firm. After that the report explain the various type of

Management accounting report and budgetary tool. In the end the report explain the different

measuring tool in real and how different organization has to consider adopt MA system in an

organization. Report also explain the calculation of different financial data.

MAIN BODY

MA Definition

As per Institute of MA (IMA), MA is define as a profession which has to consider provide their

support in management decision making of an organization. This eventually prove crucial for

organization in planning different operation in an organization and provides a good hand of

support to financial reporting and implementing various policy in an organization (Otley, 2016).

Institute of cost and management accounting, defines management accounting as application of

different professional skill in the preparation of report in the various which provides good

support in formulation policy and considering different alternative.

Function of MA

Function of MA are as follows:

Planing: MA has to consider provide the contrastive information about the situation of

the business and on the consideration of same different policy and strategy are being planned in

an organization (Cooper, Ezzamel and Qu, 2017).

Organising: MA help manager in organizing different activity, as this helps Management

accounting manager is able to regulate, adjust and coordinate various activity at workplace.

Controlling: MA provides the organization in controlling various activity in the

organization. As MA help organization in understanding variance between actual and expected

performance.

Margin Analysis: management accounting is has to consider determine the different

amount of profit or flow of cash which is generated in the firm, due to product, customer and

region.

1

Management accounting is the process in which organization uses different report in the

organization to improve the performance of the business. Katie walker Furniture, is the

organization who has to consider dealt in the retail sector of the nation. This report explain the

critical evaluation of MA and system in the firm. After that the report explain the various type of

Management accounting report and budgetary tool. In the end the report explain the different

measuring tool in real and how different organization has to consider adopt MA system in an

organization. Report also explain the calculation of different financial data.

MAIN BODY

MA Definition

As per Institute of MA (IMA), MA is define as a profession which has to consider provide their

support in management decision making of an organization. This eventually prove crucial for

organization in planning different operation in an organization and provides a good hand of

support to financial reporting and implementing various policy in an organization (Otley, 2016).

Institute of cost and management accounting, defines management accounting as application of

different professional skill in the preparation of report in the various which provides good

support in formulation policy and considering different alternative.

Function of MA

Function of MA are as follows:

Planing: MA has to consider provide the contrastive information about the situation of

the business and on the consideration of same different policy and strategy are being planned in

an organization (Cooper, Ezzamel and Qu, 2017).

Organising: MA help manager in organizing different activity, as this helps Management

accounting manager is able to regulate, adjust and coordinate various activity at workplace.

Controlling: MA provides the organization in controlling various activity in the

organization. As MA help organization in understanding variance between actual and expected

performance.

Margin Analysis: management accounting is has to consider determine the different

amount of profit or flow of cash which is generated in the firm, due to product, customer and

region.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost setting: MA also provide very crucial support the company in ascertaining different

cost which will be require by a company in manufacturing process.

Inventory valuation: MA provides good hand of support to company in determining

variety of different direct and indirect cost and inventory item in an organization (Maas,

Schaltegger and Crutzen, 2016).

Difference between Financial and MA

Basis MA Financial Accounting

Aggregation MA in the firm looks at

detailed level to enhance the

performance. Such as profit by

product, product line, customer

and geographic region

Financial Accounting at the

same time has to consider look

at enhancing the result of

entire business.

Standard Management accounting did

not need to compile with any

of the standard to present the

result (Hopper and Bui, 2016).

Financial accounting has to

compile the out come of the

report with variety of different

standard.

Time Period This is generally prepare on

the frequent basis in the

organization.

Financial accounting is

generally drawn once or twice

the year only.

Requirement of MA

Forecasting cash flow: MA is require in the firm to forecast different cash flow of the

organization. As MA has to consider make various forecasting decision on the basis of budget

and different financial report.

Analyzing ROI: management accounting is require in the organization to analyze ROI of

the business. As with MA is required in the firm to select the best opportunity available at market

place (Bromwich and Scapens, 2016).

Strategic management: MA is also required at the workplace for the purpose of

Strategic management. As MA help organization in forming different strategy.

2

cost which will be require by a company in manufacturing process.

Inventory valuation: MA provides good hand of support to company in determining

variety of different direct and indirect cost and inventory item in an organization (Maas,

Schaltegger and Crutzen, 2016).

Difference between Financial and MA

Basis MA Financial Accounting

Aggregation MA in the firm looks at

detailed level to enhance the

performance. Such as profit by

product, product line, customer

and geographic region

Financial Accounting at the

same time has to consider look

at enhancing the result of

entire business.

Standard Management accounting did

not need to compile with any

of the standard to present the

result (Hopper and Bui, 2016).

Financial accounting has to

compile the out come of the

report with variety of different

standard.

Time Period This is generally prepare on

the frequent basis in the

organization.

Financial accounting is

generally drawn once or twice

the year only.

Requirement of MA

Forecasting cash flow: MA is require in the firm to forecast different cash flow of the

organization. As MA has to consider make various forecasting decision on the basis of budget

and different financial report.

Analyzing ROI: management accounting is require in the organization to analyze ROI of

the business. As with MA is required in the firm to select the best opportunity available at market

place (Bromwich and Scapens, 2016).

Strategic management: MA is also required at the workplace for the purpose of

Strategic management. As MA help organization in forming different strategy.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Decision making: MA is also required in the firm to make or take various type of

decision in the firm. As this framework provide a good basis of information to make different

decision in an organization.

MA System, application and benefits

Cost Accounting System: Cost accounting system is the system which is used in the MA

to estimate different sort of cost of the product to determine cost of the product, inventory

valuation and control.

Requirement and Benefit

Cost Accounting system is required in the organization to determine the variety of fixed

and variable cost incurred in the company. This help the firm in optimizing the budget

and resource allocation in the organization.

It provides company in offering product at reasonable price, as it eliminates unnecessary

item in production (Quattrone, 2016).

Inventory management system: It is the accounting system in the firm which prove

crucial for organization in tracking the different level of inventory in the firm.

Requirement and Benefit

Inventory management system is required to forecasting the different need of company

product at market place. This help in planning the different manufacturing activity in a

way that it help company in achieving the goal efficiently.

provides organization in keeping the warehouse of the company well organized.

Job costing System: This is the system which looks at determining the contrastive cost

which has been incurred for a specific production or service in an organization.

Requirement and Benefit

Job costing system is generally required to estimate similar or different type of job which

can be undertaken.

provides organization in understanding the variety of pros and cons of job in an

organization (Ax and Greve, 2017).

Price-optimizing System: This is the system which has to consider consider the change

in demand due to change in the pricing structure in an organization.

Requirement and Benefit

3

decision in the firm. As this framework provide a good basis of information to make different

decision in an organization.

MA System, application and benefits

Cost Accounting System: Cost accounting system is the system which is used in the MA

to estimate different sort of cost of the product to determine cost of the product, inventory

valuation and control.

Requirement and Benefit

Cost Accounting system is required in the organization to determine the variety of fixed

and variable cost incurred in the company. This help the firm in optimizing the budget

and resource allocation in the organization.

It provides company in offering product at reasonable price, as it eliminates unnecessary

item in production (Quattrone, 2016).

Inventory management system: It is the accounting system in the firm which prove

crucial for organization in tracking the different level of inventory in the firm.

Requirement and Benefit

Inventory management system is required to forecasting the different need of company

product at market place. This help in planning the different manufacturing activity in a

way that it help company in achieving the goal efficiently.

provides organization in keeping the warehouse of the company well organized.

Job costing System: This is the system which looks at determining the contrastive cost

which has been incurred for a specific production or service in an organization.

Requirement and Benefit

Job costing system is generally required to estimate similar or different type of job which

can be undertaken.

provides organization in understanding the variety of pros and cons of job in an

organization (Ax and Greve, 2017).

Price-optimizing System: This is the system which has to consider consider the change

in demand due to change in the pricing structure in an organization.

Requirement and Benefit

3

This is required in the business to drive the focus of organization toward different value

added activities in an organization.

Also it helps the organization in promoting automation of task in the company and helped

in making quick decision in an organization.

Information should be relevant, accurate and reliable

There is very much need of providing the contrastive information in a relevant and

accurate way to contrastive interested party. Reason behind the same is identified that it will help

the manager in making more relevant decision as manager will be having accurate data . It is also

very crucial for the organization to have reliable information, otherwise it may impact the

efficiency of the business in long run.

4

added activities in an organization.

Also it helps the organization in promoting automation of task in the company and helped

in making quick decision in an organization.

Information should be relevant, accurate and reliable

There is very much need of providing the contrastive information in a relevant and

accurate way to contrastive interested party. Reason behind the same is identified that it will help

the manager in making more relevant decision as manager will be having accurate data . It is also

very crucial for the organization to have reliable information, otherwise it may impact the

efficiency of the business in long run.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

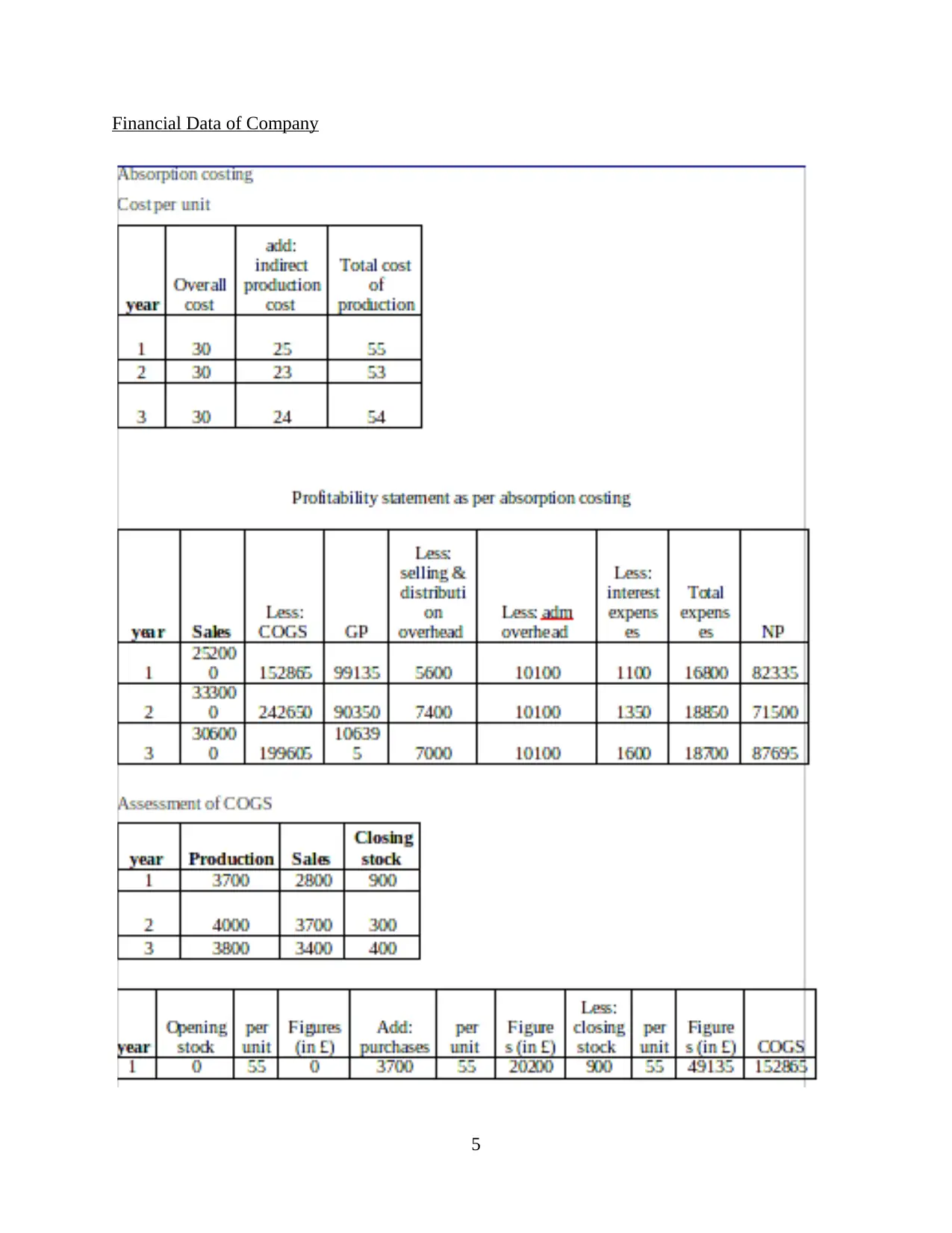

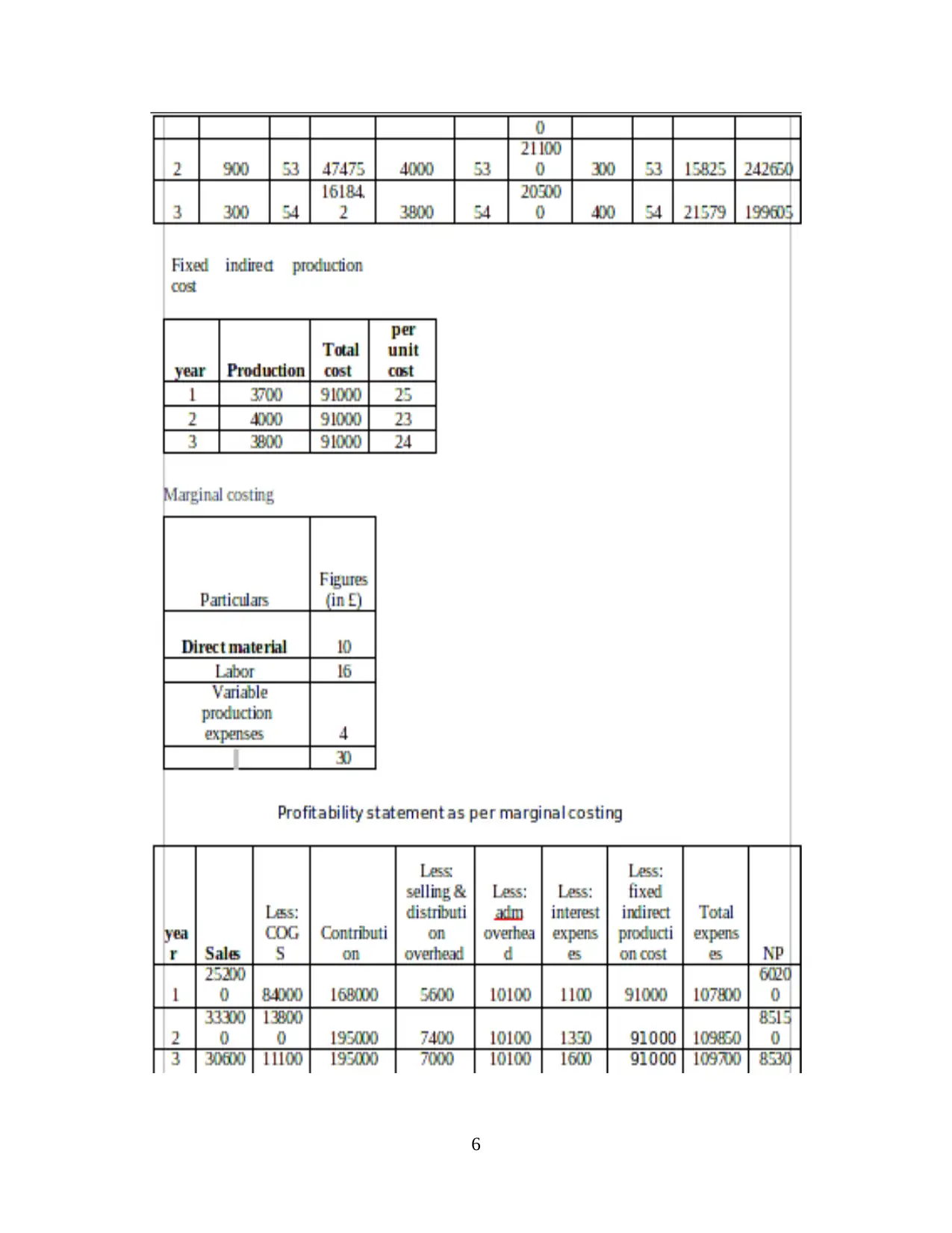

Financial Data of Company

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

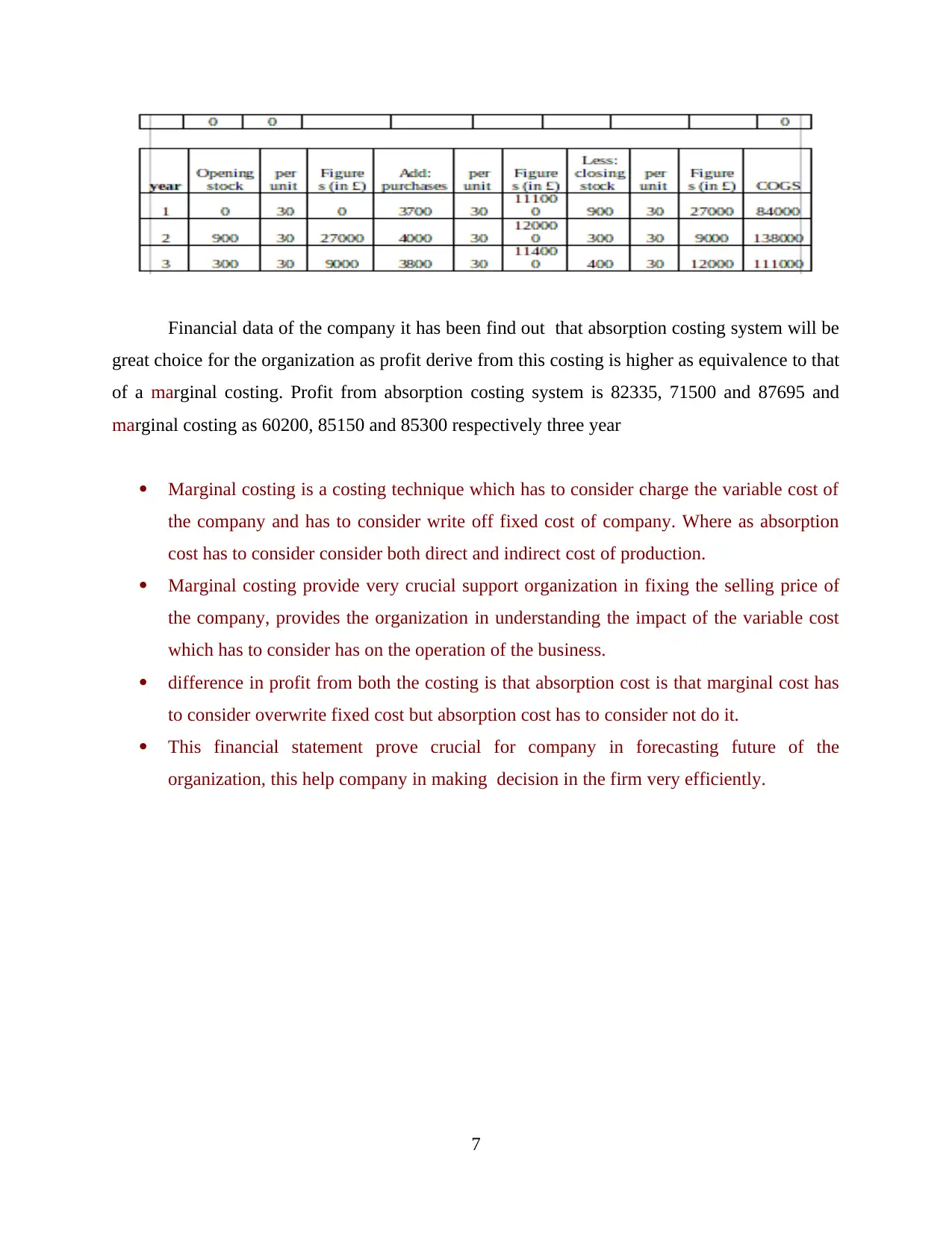

Financial data of the company it has been find out that absorption costing system will be

great choice for the organization as profit derive from this costing is higher as equivalence to that

of a marginal costing. Profit from absorption costing system is 82335, 71500 and 87695 and

marginal costing as 60200, 85150 and 85300 respectively three year

Marginal costing is a costing technique which has to consider charge the variable cost of

the company and has to consider write off fixed cost of company. Where as absorption

cost has to consider consider both direct and indirect cost of production.

Marginal costing provide very crucial support organization in fixing the selling price of

the company, provides the organization in understanding the impact of the variable cost

which has to consider has on the operation of the business.

difference in profit from both the costing is that absorption cost is that marginal cost has

to consider overwrite fixed cost but absorption cost has to consider not do it.

This financial statement prove crucial for company in forecasting future of the

organization, this help company in making decision in the firm very efficiently.

7

great choice for the organization as profit derive from this costing is higher as equivalence to that

of a marginal costing. Profit from absorption costing system is 82335, 71500 and 87695 and

marginal costing as 60200, 85150 and 85300 respectively three year

Marginal costing is a costing technique which has to consider charge the variable cost of

the company and has to consider write off fixed cost of company. Where as absorption

cost has to consider consider both direct and indirect cost of production.

Marginal costing provide very crucial support organization in fixing the selling price of

the company, provides the organization in understanding the impact of the variable cost

which has to consider has on the operation of the business.

difference in profit from both the costing is that absorption cost is that marginal cost has

to consider overwrite fixed cost but absorption cost has to consider not do it.

This financial statement prove crucial for company in forecasting future of the

organization, this help company in making decision in the firm very efficiently.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Different type of MA report

Inventory Report: Inventory report is the report which has to consider show the

summarized version of the various type of the inventory present in firm and the stage at through

which that inventory is going on (Granlund and Lukka, 2017). This shows the comprehensive

accounts related to the stock and supply of different item in an organization.

Benefit of inventory report

Inventory report help organization in making different management strategy in the

organization. As at the time of making contrastive strategy related to production of inventory,

inventory report provide the basis of current situation of inventory in the company. This helps

the organization in overcoming the issue of duplicate of work at the workplace. Also, saving the

cost of the production in an organization. Also inventory report help organization in preventing

the situation of product shortage and allowing you to keep good amount of product in the

organization.

Account Receivable aging report: Account Receivable aging report which has to

consider shows the list of the various sort of debtor of firm with the date on which they are liable

to pay debt. This report has to consider record the date of the occurrence of the debt as well.

Benefit of Account receivable aging report

This eventually prove crucial for company in managing the debt of the company in more

efficient way in the organization. As with the help of Accounts receivable aging report

organization is able to identify the customer which has to consider fall behind on their payment

and can memorized them on time to pay contrastive debt in an organization. This prove crucial

for organization in seeing the greater amount of financial availability in the company

(Soderstrom, Soderstrom and Stewart, 2017). This eventually prove crucial for company in

planning different activity very efficiently.

Budget Report: Budget Report has to consider show the actual result of the outcome of

the budget with the per-established budget of an organization. They generally has to consider

show the variance in the budget formation.

Benefit of Budget Report

Budget report generally help the management of the organization in knowing the

contrastive expenditure level in the organization is too high for the organization. Organization

can take different action to lower down the same in the organization. This report also has to

8

Inventory Report: Inventory report is the report which has to consider show the

summarized version of the various type of the inventory present in firm and the stage at through

which that inventory is going on (Granlund and Lukka, 2017). This shows the comprehensive

accounts related to the stock and supply of different item in an organization.

Benefit of inventory report

Inventory report help organization in making different management strategy in the

organization. As at the time of making contrastive strategy related to production of inventory,

inventory report provide the basis of current situation of inventory in the company. This helps

the organization in overcoming the issue of duplicate of work at the workplace. Also, saving the

cost of the production in an organization. Also inventory report help organization in preventing

the situation of product shortage and allowing you to keep good amount of product in the

organization.

Account Receivable aging report: Account Receivable aging report which has to

consider shows the list of the various sort of debtor of firm with the date on which they are liable

to pay debt. This report has to consider record the date of the occurrence of the debt as well.

Benefit of Account receivable aging report

This eventually prove crucial for company in managing the debt of the company in more

efficient way in the organization. As with the help of Accounts receivable aging report

organization is able to identify the customer which has to consider fall behind on their payment

and can memorized them on time to pay contrastive debt in an organization. This prove crucial

for organization in seeing the greater amount of financial availability in the company

(Soderstrom, Soderstrom and Stewart, 2017). This eventually prove crucial for company in

planning different activity very efficiently.

Budget Report: Budget Report has to consider show the actual result of the outcome of

the budget with the per-established budget of an organization. They generally has to consider

show the variance in the budget formation.

Benefit of Budget Report

Budget report generally help the management of the organization in knowing the

contrastive expenditure level in the organization is too high for the organization. Organization

can take different action to lower down the same in the organization. This report also has to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consider show the different revenue option available in front of the organization. This help the

management of the organization in overcoming the issue related to the profit margin in the

organization.

Integration of Different MA system

MA system in the organization is linked with the variety of the various reports in the

firm. As it has seen that MA system in the firm shows the result qualitative form. Whereas MA

report in the firm has to consider show the different result in quantitative form. So manager in

the organization has to consider check out the result of both reporting as well as system and has

to consider make different managerial decision in the firm.

For Example: Inventory management system or job costing system has to consider

create the environment in company which prove crucial for company in analysis how

organization can manage the inventory in the firm or maintain good cost structure in an

organization (Dekker, 2016). At the same time MA report in the firm has to consider provide the

current situation of the cost in the organization or inventory in the company. On the basis of the

integrating the strategy to maintain the inventory or cost and actual position, manager in the firm

has to consider take various type of management action in an organization.

9

management of the organization in overcoming the issue related to the profit margin in the

organization.

Integration of Different MA system

MA system in the organization is linked with the variety of the various reports in the

firm. As it has seen that MA system in the firm shows the result qualitative form. Whereas MA

report in the firm has to consider show the different result in quantitative form. So manager in

the organization has to consider check out the result of both reporting as well as system and has

to consider make different managerial decision in the firm.

For Example: Inventory management system or job costing system has to consider

create the environment in company which prove crucial for company in analysis how

organization can manage the inventory in the firm or maintain good cost structure in an

organization (Dekker, 2016). At the same time MA report in the firm has to consider provide the

current situation of the cost in the organization or inventory in the company. On the basis of the

integrating the strategy to maintain the inventory or cost and actual position, manager in the firm

has to consider take various type of management action in an organization.

9

Different type of Budgeting

Zero Based Budgeting: Zero Based Budgeting is budgeting which looks at justifying all

the different expenses for new period. This process of budgeting has to consider starts from the

scrap and has to consider take every budget as a zero and all the function in the organization are

also analyzed for the purpose of needs and cost (Nitzl, 2016).

Advantage of Zero based budgeting

Zero based budgeting in the organization help the manager in justifying all type of the

expenses in cited firm. Not only that it provide the help to the organization in justifying

the various operating expenses in the organization as well.

Zero based budgeting is also recognized as the efficient budgeting tool as this tool has to

consider focus on the current situation of the business as compare to the previous or past

budget of an organization.

It provides the organization in removing the redundant spending of the company as it has

to consider re-assist unnecessary expenditure in cited firm.

Disadvantage

Zero based budgeting consume good amount of time and efforts in company, this

eventually has to consider impact efficiency of the business. As they have to start from scrap

from starting.

Also it has been Analyzed that ZBB is the technique which increases the chances of the

corruption in the organization as compare to the other budgeting tool.

Purchasing Budget: It is the type of the budget which has to consider determine the

amount of the resources or the inventory which will be require by the organization in coming

period to carry out the various operation. Also this budgetary tool has to consider define the

amount of the money which will be require to procure the same in the organization (Budgeting

Tool, 2016).

Advantage

This budgetary tool in the organization provide very crucial support the organization in

optimum utilization of the resources. As there is good amount of the clarity, which

reduces the amount of wastage.

10

Zero Based Budgeting: Zero Based Budgeting is budgeting which looks at justifying all

the different expenses for new period. This process of budgeting has to consider starts from the

scrap and has to consider take every budget as a zero and all the function in the organization are

also analyzed for the purpose of needs and cost (Nitzl, 2016).

Advantage of Zero based budgeting

Zero based budgeting in the organization help the manager in justifying all type of the

expenses in cited firm. Not only that it provide the help to the organization in justifying

the various operating expenses in the organization as well.

Zero based budgeting is also recognized as the efficient budgeting tool as this tool has to

consider focus on the current situation of the business as compare to the previous or past

budget of an organization.

It provides the organization in removing the redundant spending of the company as it has

to consider re-assist unnecessary expenditure in cited firm.

Disadvantage

Zero based budgeting consume good amount of time and efforts in company, this

eventually has to consider impact efficiency of the business. As they have to start from scrap

from starting.

Also it has been Analyzed that ZBB is the technique which increases the chances of the

corruption in the organization as compare to the other budgeting tool.

Purchasing Budget: It is the type of the budget which has to consider determine the

amount of the resources or the inventory which will be require by the organization in coming

period to carry out the various operation. Also this budgetary tool has to consider define the

amount of the money which will be require to procure the same in the organization (Budgeting

Tool, 2016).

Advantage

This budgetary tool in the organization provide very crucial support the organization in

optimum utilization of the resources. As there is good amount of the clarity, which

reduces the amount of wastage.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.