Analysis of Management Accounting Practices and Reporting for ABC Ltd

VerifiedAdded on 2023/01/18

|18

|4525

|86

Report

AI Summary

This report delves into the realm of management accounting, focusing on the internal information processes that drive strategic decision-making within ABC Ltd. The analysis encompasses various aspects, including the definition and evolution of management accounting, its distinction from financial accounting, and the diverse systems employed, such as cost accounting, inventory management, and price optimization. The report explores different reporting methods, including performance, budget, and accounts receivable reports, and their integration into organizational processes. Furthermore, it examines costing techniques like direct and indirect costs, cost analysis, cost-volume-profit analysis, flexible budgeting, and various costing methods such as marginal costing, absorption costing, and activity-based costing. The role of costing in setting selling prices and managing inventory costs is also discussed. The report then explores budgetary control, outlining its advantages and disadvantages, and concludes with a comparison of different management accounting systems adopted by organizations.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.....................................................................................................................................3

TASK 1.......................................................................................................................................................3

P1 Define management accounting along with its essential requirements.........................................3

P2 Various methods for management accounting reporting..............................................................5

TASK 2.......................................................................................................................................................7

P3 Different techniques of costing that are used by cost calculation.................................................7

TASK 3.....................................................................................................................................................12

P4 Different planning tool of budgetary control along with its advantages and disadvantages........12

TASK 4.....................................................................................................................................................15

P5 Comparison of the ways in that organization adopts management accounting system...............15

CONCLUSION.........................................................................................................................................17

REFERENCES........................................................................................................................................18

INTRODUCTION.....................................................................................................................................3

TASK 1.......................................................................................................................................................3

P1 Define management accounting along with its essential requirements.........................................3

P2 Various methods for management accounting reporting..............................................................5

TASK 2.......................................................................................................................................................7

P3 Different techniques of costing that are used by cost calculation.................................................7

TASK 3.....................................................................................................................................................12

P4 Different planning tool of budgetary control along with its advantages and disadvantages........12

TASK 4.....................................................................................................................................................15

P5 Comparison of the ways in that organization adopts management accounting system...............15

CONCLUSION.........................................................................................................................................17

REFERENCES........................................................................................................................................18

INTRODUCTION

Management accounting refers to the process of recording internal information in order to

make and implement strategic decisions for the benefits of organization (Liff and Wahlstrom,

2018). In order to examine the business performance in the external marketplace, internal

stakeholders like employees and managers plays an important role. This will also help external

stakeholders for identify the present status of a company. In this report ABC Ltd. Is taken which

is a manufacturing company. Under this report discussed about the management accounting,

reporting, accounting systems, costing methods, planning tool for budgetary control and its

advantages and disadvantages etc. In addition, study about the effectiveness and implications,

financial challenges as well as ways to solve those challenges.

TASK 1

P1 Define management accounting along with its essential requirements.

Management accounting: It refers to the process of examining and communicating

information with the manager in order to observe the performance of ABC ltd. And design

strategies as per the requirement (Fleischman and Parker, 2017).

Origin and evolution of management accounting: It was originated after the financial

accounting that can trace its origin into stewardship character in various trading ventures. Mainly

two major industries such as textile and railroad played a significant role in its evolution.

Management accounting system: This is used by the manager of ABC limited in order to

keep suggested records of operational and functional departments of a company. ABC used

many systems for the purpose of determine the actual sales of business.

Explanation of management accounting: It defined as a process of creating various

management accounts and reports for the purpose of identifying actual sales through which a

manager of ABC limited formulate appropriate strategies for operating regular activities and

functions (Kerr, Rouse and de Villiers, 2015).

Difference between management as well as financial accounting:

Management accounting Financial accounting

It facilitates the whole information of a In this, external stakeholders get information

Management accounting refers to the process of recording internal information in order to

make and implement strategic decisions for the benefits of organization (Liff and Wahlstrom,

2018). In order to examine the business performance in the external marketplace, internal

stakeholders like employees and managers plays an important role. This will also help external

stakeholders for identify the present status of a company. In this report ABC Ltd. Is taken which

is a manufacturing company. Under this report discussed about the management accounting,

reporting, accounting systems, costing methods, planning tool for budgetary control and its

advantages and disadvantages etc. In addition, study about the effectiveness and implications,

financial challenges as well as ways to solve those challenges.

TASK 1

P1 Define management accounting along with its essential requirements.

Management accounting: It refers to the process of examining and communicating

information with the manager in order to observe the performance of ABC ltd. And design

strategies as per the requirement (Fleischman and Parker, 2017).

Origin and evolution of management accounting: It was originated after the financial

accounting that can trace its origin into stewardship character in various trading ventures. Mainly

two major industries such as textile and railroad played a significant role in its evolution.

Management accounting system: This is used by the manager of ABC limited in order to

keep suggested records of operational and functional departments of a company. ABC used

many systems for the purpose of determine the actual sales of business.

Explanation of management accounting: It defined as a process of creating various

management accounts and reports for the purpose of identifying actual sales through which a

manager of ABC limited formulate appropriate strategies for operating regular activities and

functions (Kerr, Rouse and de Villiers, 2015).

Difference between management as well as financial accounting:

Management accounting Financial accounting

It facilitates the whole information of a In this, external stakeholders get information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company to its internal stakeholders such as

manager, employees etc.

regarding the financial performance of ABC

limited.

To do a management accounting there is no

specific principles as well as standards

(Cooper, 2017).

Financial accounting conducted by using

specific measures, principles as well as

standard of accounting.

Different systems of management accounting: Cost accounting system: This system is used by the financial advisor of ABC limited for

the purpose of recording all information of an organizational expenditure either direct or

indirect that are related to the manufacturing industry (Morillo and Montesinos, 2015). Inventory management system: This is basically related to the manufacturing industry as

to manage the inventory for preparation of final goods. Three techniques are mainly used

in as an inventory management system like LIFO, FIFO, AVCO for maintaining stock

according to the requirements. Price optimization system: It is used by the ABC limited in order to sets optimum prices

of their products for constructing is able to fulfil customer’s expectations or not.

Job order costing system: It is used to allocate and gather cost of each activities or

manufacturing unit of an ABC limited. As this helps in analyzing the entire cost of each

activity that are manufactured or offered as per the customer specification (Monden,

2019).

Benefits of management accounting system:

Management accounting

system

Benefits

Cost accounting system This is used by ABC limited for keeping a record of all cost

which are involved in business activities.

Inventory management

system

It is applied in ABC ltd. Through which manager of the company

able to know about the requirement of inventory in order to

perform activities.

manager, employees etc.

regarding the financial performance of ABC

limited.

To do a management accounting there is no

specific principles as well as standards

(Cooper, 2017).

Financial accounting conducted by using

specific measures, principles as well as

standard of accounting.

Different systems of management accounting: Cost accounting system: This system is used by the financial advisor of ABC limited for

the purpose of recording all information of an organizational expenditure either direct or

indirect that are related to the manufacturing industry (Morillo and Montesinos, 2015). Inventory management system: This is basically related to the manufacturing industry as

to manage the inventory for preparation of final goods. Three techniques are mainly used

in as an inventory management system like LIFO, FIFO, AVCO for maintaining stock

according to the requirements. Price optimization system: It is used by the ABC limited in order to sets optimum prices

of their products for constructing is able to fulfil customer’s expectations or not.

Job order costing system: It is used to allocate and gather cost of each activities or

manufacturing unit of an ABC limited. As this helps in analyzing the entire cost of each

activity that are manufactured or offered as per the customer specification (Monden,

2019).

Benefits of management accounting system:

Management accounting

system

Benefits

Cost accounting system This is used by ABC limited for keeping a record of all cost

which are involved in business activities.

Inventory management

system

It is applied in ABC ltd. Through which manager of the company

able to know about the requirement of inventory in order to

perform activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system In this, manager sets specific prices of products that are required

to meet the customer’s expectations (Brustbauer, 2016).

Job order costing system This system is used by ABC limited for identifying the several

activities which are performed according to the clients’

requirement or specification.

P2 Various methods for management accounting reporting.

Management accounting reporting: It refers to the procedure of making several

management accountings reports that includes many information regarding the company’s

performance.

Features of good information system: Accuracy: Good information system helps in gathering accurate informations towards the

performance of a company that can direct stakeholders for making strategic decisions.

Reliability: This facilitates reliable informations to its users that assists them to know and

examine the actual status of company (Meidell and Kaarbøe, 2017).

Reasons behind understanding and comprehensive of report:

It is crucial that management accounting systems must be comprehensive as well as

understandable because through this a manager can measure actual status or performance of

ABC limited.

As management accounting reports direct managers in order to plan innovative as well as

strategic strategies for the improvement ABC limited but if there are not clear understandability

the it is not thinkable for manager to complete the activities (Tucker and Leach, 2017).

Different methods of management accounting report: Performance report: This can basically base on the purpose of keeping performance

records related to all operations of ABC limited. This is used by the company for

gathering and recording informations regarding employees as well as business

to meet the customer’s expectations (Brustbauer, 2016).

Job order costing system This system is used by ABC limited for identifying the several

activities which are performed according to the clients’

requirement or specification.

P2 Various methods for management accounting reporting.

Management accounting reporting: It refers to the procedure of making several

management accountings reports that includes many information regarding the company’s

performance.

Features of good information system: Accuracy: Good information system helps in gathering accurate informations towards the

performance of a company that can direct stakeholders for making strategic decisions.

Reliability: This facilitates reliable informations to its users that assists them to know and

examine the actual status of company (Meidell and Kaarbøe, 2017).

Reasons behind understanding and comprehensive of report:

It is crucial that management accounting systems must be comprehensive as well as

understandable because through this a manager can measure actual status or performance of

ABC limited.

As management accounting reports direct managers in order to plan innovative as well as

strategic strategies for the improvement ABC limited but if there are not clear understandability

the it is not thinkable for manager to complete the activities (Tucker and Leach, 2017).

Different methods of management accounting report: Performance report: This can basically base on the purpose of keeping performance

records related to all operations of ABC limited. This is used by the company for

gathering and recording informations regarding employees as well as business

performance. As it helps in facilitating incentives and bonus to employees according to

their efforts for attaining the tasks which are assigned to them. Budget report: It is considered as a internal report that can applied by ABC limited in

order to estimate budget for different operational and functional department. It is used for

understanding the gap between actual and standard spending to measure the performance

and execute all functions in estimated budget (Cowton, 2018). Account receivable report: This is formed to list owned of many customers and this can

used while a company ABC limited provides goods and services to their clients on credit

basis. This helps in determining the unpaid amount which are due by clients as well as

overcome from the late payment issue of company.

Inventory management report: This report can be used to keep the records regarding the

inventories that is kept by the ABC limited. It is benefited for a business organization as

it helps in checking the status of inventory that is delivered to its customers (Mahmoudi,

Jodeiri and Fatehifar, 2017).

Integration of management accounting systems and report in organization process:

There are several management accountings reports and systems which are integrates with

the organizational procedure. Mainly price optimization is used by ABC limited in order to set

specific prices for goods and services. Whereas, accounting receivable reports are used to

constrict credit policies by examining the total preserved expanse of many customers.

TASK 2

P3 Different techniques of costing that are used by cost calculation.

Cost: It is the amount which is needed to be paid by a buyer to seller for a particular

products and services.

Type of cost: Direct cost: This is related to that which are directly related to the organizational

activities such as depreciation, salary, insurance etc.

their efforts for attaining the tasks which are assigned to them. Budget report: It is considered as a internal report that can applied by ABC limited in

order to estimate budget for different operational and functional department. It is used for

understanding the gap between actual and standard spending to measure the performance

and execute all functions in estimated budget (Cowton, 2018). Account receivable report: This is formed to list owned of many customers and this can

used while a company ABC limited provides goods and services to their clients on credit

basis. This helps in determining the unpaid amount which are due by clients as well as

overcome from the late payment issue of company.

Inventory management report: This report can be used to keep the records regarding the

inventories that is kept by the ABC limited. It is benefited for a business organization as

it helps in checking the status of inventory that is delivered to its customers (Mahmoudi,

Jodeiri and Fatehifar, 2017).

Integration of management accounting systems and report in organization process:

There are several management accountings reports and systems which are integrates with

the organizational procedure. Mainly price optimization is used by ABC limited in order to set

specific prices for goods and services. Whereas, accounting receivable reports are used to

constrict credit policies by examining the total preserved expanse of many customers.

TASK 2

P3 Different techniques of costing that are used by cost calculation.

Cost: It is the amount which is needed to be paid by a buyer to seller for a particular

products and services.

Type of cost: Direct cost: This is related to that which are directly related to the organizational

activities such as depreciation, salary, insurance etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Indirect cost: These expenses are not directly related to the accountable activities for

ABC limited such as rent, office utilities (Brewer, Garrison and Noreen, 2015).

Cost analysis: This can be referred as a procedure which is in used to analysis the

importance of several actions which are taken by ABC limited for earning profits. This will help

in analyzing the decisions which were formulated by company in order to accomplish long term

objectives.

Cost volume profit: This is related to the cost accounting method that is implemented by

manager of ABC limited for identifying effects of alterations in cost as well as volume on the

profits of business organization.

Flexible budgeting: It is defining as a method of framing budgets in that alterations could be

complete according to variations in an activity. It is in used by ABC limited for making changes in budget

as per the varying cost.

Cost variance: This is used by ABC limited to analyse the gap between actual and budgeted

cost of manufacturing.

Marginal costing: In this, the cost of per unit remains same and based on the fixed and

variable terms as it helps in resolving the problem of over and under absorption. It is used by the

management of ABC limited in order to sets, price, profit, BEP calculation and decisions.

Absorption costing: This refers to the use for recording a financial performance of a

company as it provides a clear view about gross and net profit of ABC limited that helps in

assigning fixed overheads expenses for specific departments.

Fixed cost: It refers to that cost which is remain constant whether the production quantity

fluctuate either increase or decrease ( Kenyon and Kenyon, 2016).

Variable cost: This is the opposite of fixed cost which is fluctuated according to the changes

in the level of production.

Cost allocation: It can be referred as a type of systematic procedure which is related to the

process of finding, aggregating as well as allocating the cost to specific objectives.

ABC limited such as rent, office utilities (Brewer, Garrison and Noreen, 2015).

Cost analysis: This can be referred as a procedure which is in used to analysis the

importance of several actions which are taken by ABC limited for earning profits. This will help

in analyzing the decisions which were formulated by company in order to accomplish long term

objectives.

Cost volume profit: This is related to the cost accounting method that is implemented by

manager of ABC limited for identifying effects of alterations in cost as well as volume on the

profits of business organization.

Flexible budgeting: It is defining as a method of framing budgets in that alterations could be

complete according to variations in an activity. It is in used by ABC limited for making changes in budget

as per the varying cost.

Cost variance: This is used by ABC limited to analyse the gap between actual and budgeted

cost of manufacturing.

Marginal costing: In this, the cost of per unit remains same and based on the fixed and

variable terms as it helps in resolving the problem of over and under absorption. It is used by the

management of ABC limited in order to sets, price, profit, BEP calculation and decisions.

Absorption costing: This refers to the use for recording a financial performance of a

company as it provides a clear view about gross and net profit of ABC limited that helps in

assigning fixed overheads expenses for specific departments.

Fixed cost: It refers to that cost which is remain constant whether the production quantity

fluctuate either increase or decrease ( Kenyon and Kenyon, 2016).

Variable cost: This is the opposite of fixed cost which is fluctuated according to the changes

in the level of production.

Cost allocation: It can be referred as a type of systematic procedure which is related to the

process of finding, aggregating as well as allocating the cost to specific objectives.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing: It refers to the cost which is approximated not actually occurred and it is

based on the past year information of accounting.

Normal costing: It refers to that type of cost which is incurred actually in order to complete

the operational activities.

Activity based costing: It is related to the several activities that are analyzed to allocate cost

for each single activities with regards to the production as well as services.

Role of costing in selling price: Costing plays an important role in setting the prices of

products and services because price includes the profit margin in their total cost of production.

For example, in the context of ABC limited company the cost of a particular unit is £20 then

price will be £25 and prices set by adding £5 in their actual production cost (Gray and Alles,

2015).

Inventory cost: It is related to that type of expenses which includes ordering, holding and

purchasing cost. These costs are considered as follows: Ordering cost: It is that type of cost which are occurred during the procedure of creating

suppliers orders towards the purchasing of goods. For example: The cost of invoice that

are required for producing a supplier order. Carrying cost: It also known as a holding cost that occurs in ABC limited while the

company holding inventory in stock.

Shortage cost: ABC limited face this cost when they do not have material in stock (Ruch

and Taylor, 2015).

Benefits of reducing inventory cost:

Decrease in inventory cost, increases the profit of company as it saved some amount that

are used for reinvestment.

Decrease inventory cost results in setting competitive prices in competitive era that

attracts large customers.

Valuation method: LIFO: In this method, last received material is used first for producing goods.

based on the past year information of accounting.

Normal costing: It refers to that type of cost which is incurred actually in order to complete

the operational activities.

Activity based costing: It is related to the several activities that are analyzed to allocate cost

for each single activities with regards to the production as well as services.

Role of costing in selling price: Costing plays an important role in setting the prices of

products and services because price includes the profit margin in their total cost of production.

For example, in the context of ABC limited company the cost of a particular unit is £20 then

price will be £25 and prices set by adding £5 in their actual production cost (Gray and Alles,

2015).

Inventory cost: It is related to that type of expenses which includes ordering, holding and

purchasing cost. These costs are considered as follows: Ordering cost: It is that type of cost which are occurred during the procedure of creating

suppliers orders towards the purchasing of goods. For example: The cost of invoice that

are required for producing a supplier order. Carrying cost: It also known as a holding cost that occurs in ABC limited while the

company holding inventory in stock.

Shortage cost: ABC limited face this cost when they do not have material in stock (Ruch

and Taylor, 2015).

Benefits of reducing inventory cost:

Decrease in inventory cost, increases the profit of company as it saved some amount that

are used for reinvestment.

Decrease inventory cost results in setting competitive prices in competitive era that

attracts large customers.

Valuation method: LIFO: In this method, last received material is used first for producing goods.

FIFO: In this, first received material is used for conducting operational activity.

Cost variance: For understanding the gap between actual and budgeted cost many kinds of

variances are in used such as cost, usage and price variance. ABC limited examine the gap

between budgeted and actual cost, usage and price factors.

Overhead costs: It includes all expenses that are occur while ABC manufactured goods such

as depreciation, taxation as well as insurance charges.

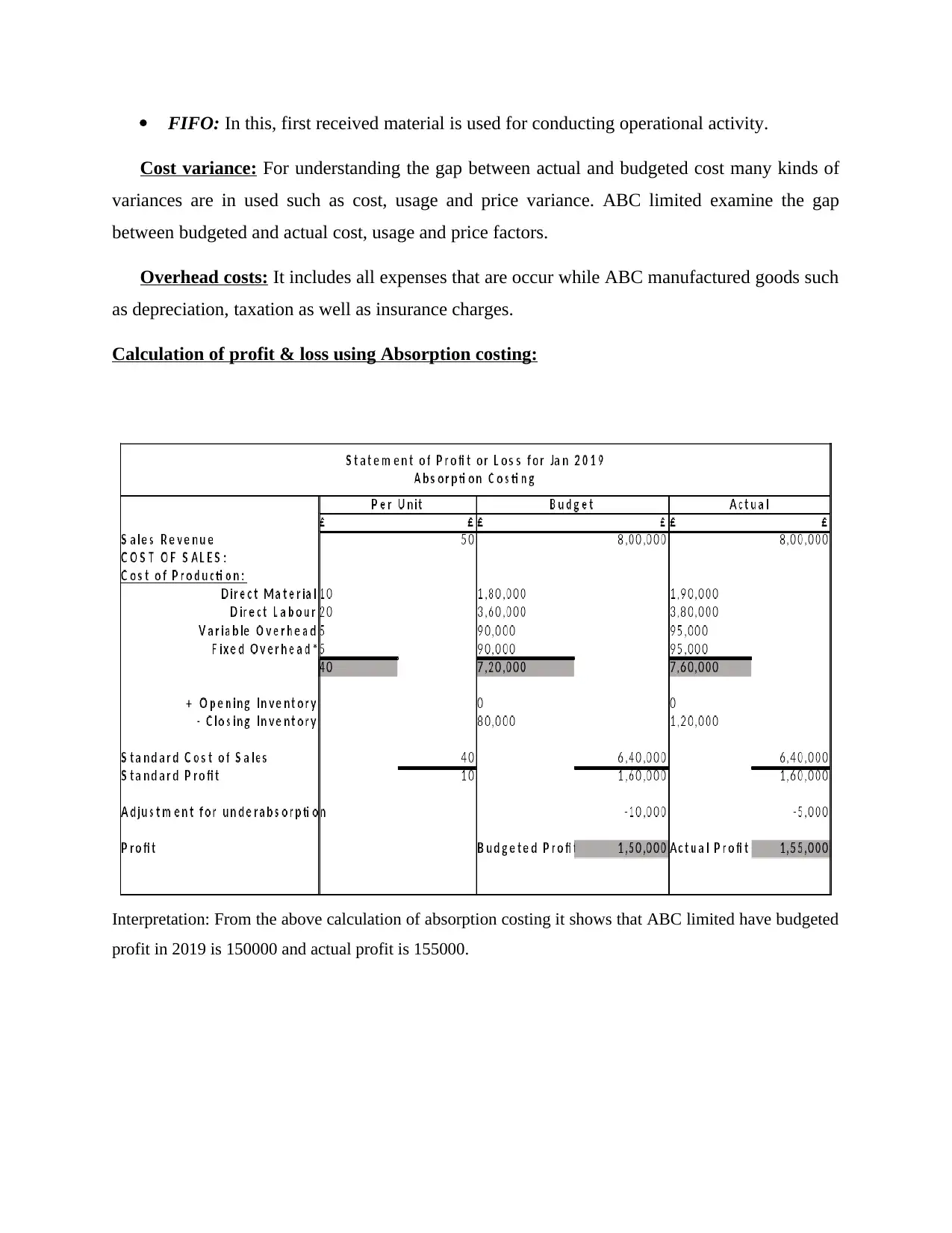

Calculation of profit & loss using Absorption costing:

Interpretation: From the above calculation of absorption costing it shows that ABC limited have budgeted

profit in 2019 is 150000 and actual profit is 155000.

Cost variance: For understanding the gap between actual and budgeted cost many kinds of

variances are in used such as cost, usage and price variance. ABC limited examine the gap

between budgeted and actual cost, usage and price factors.

Overhead costs: It includes all expenses that are occur while ABC manufactured goods such

as depreciation, taxation as well as insurance charges.

Calculation of profit & loss using Absorption costing:

Interpretation: From the above calculation of absorption costing it shows that ABC limited have budgeted

profit in 2019 is 150000 and actual profit is 155000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

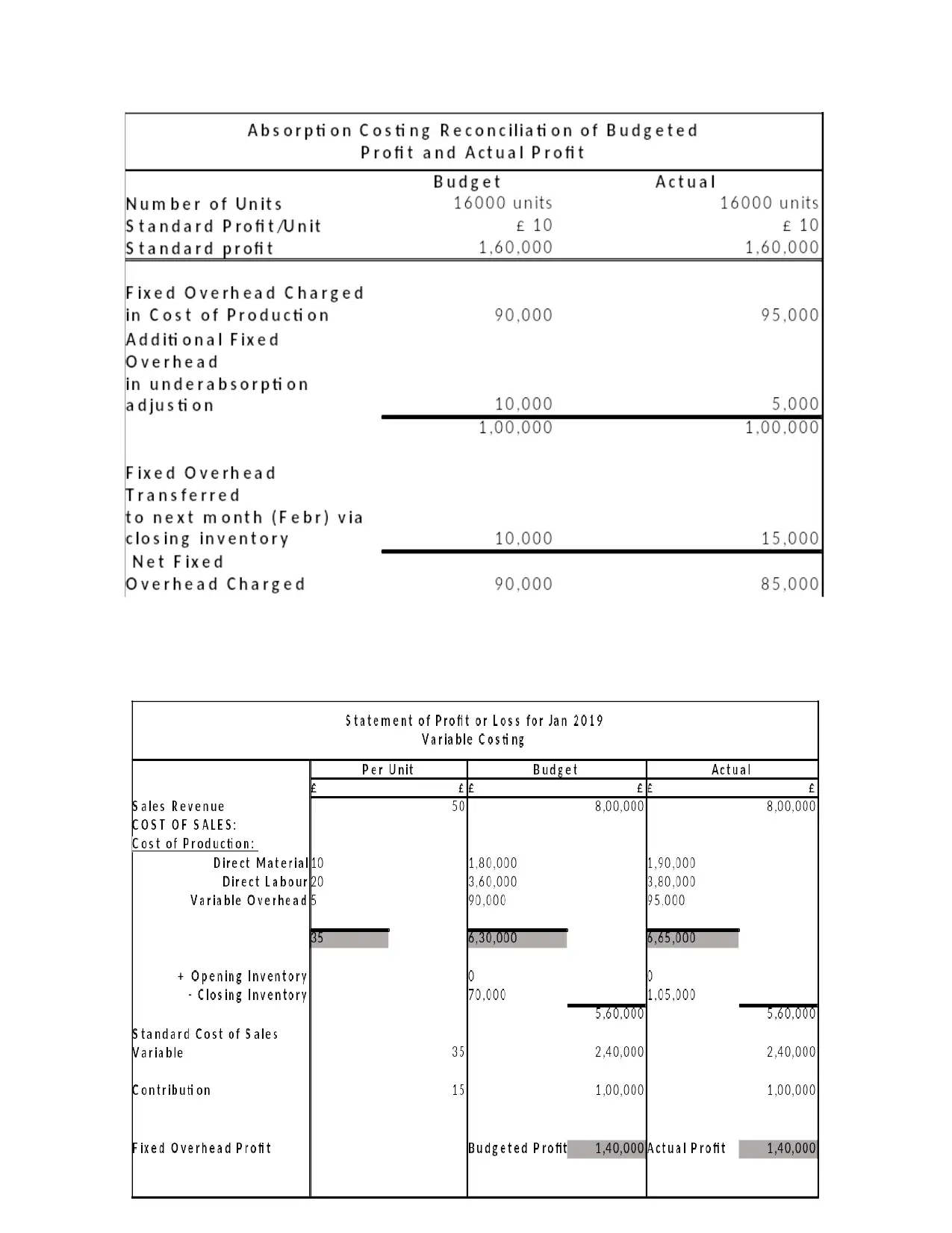

Interpretation: It has been considered from the above calculation of variable costing that

ABC limited has equal profit of actual and budgeted in 2019 that is 140000.

TASK 3

P4 Different planning tool of budgetary control along with its advantages and disadvantages.

Budget: It refers to the estimating tool that is in use to examine the future expenses and

incomes related to the specific period of time. As ABC limited use different budgets as per their

requirements.

Preparing a budget: At the time of budget formulation many steps are takes place that are

required to be followed by the manager of ABC limited in order to analyse the present position

of the company as well as available resources. After that formulate several plans that are

approved by manager in the betterment of an organization (Hoque, 2018).

Different type of budget:

Capital budget: In this, ABC limited is used to record all information that is related to the

various activities and functions in which a large capital investment is also considered.

ABC limited used this budget for analyzing financial performance and make plans for a

specific duration of time.

Advantages Disadvantages

Capital budget records all the activity of all

projects where the company invested large

amount of financial resources.

Lack of specificity is a demerit of this budget

as it includes the collective information

records of all departments of company.

Operating budget: It is related to that kind of budget in which overall expenses and

income of all projects are estimated that is totally based on the predicted sales as well as

revenue of ABC limited (Albanese, Andersen and Iabichino, 2015).

Advantages Disadvantages

It shows a clear view to the company’s

manager that monetary resources are properly

in used or not.

In this manipulation of figures could be done

simply so it is a disadvantage of operating

budget.

ABC limited has equal profit of actual and budgeted in 2019 that is 140000.

TASK 3

P4 Different planning tool of budgetary control along with its advantages and disadvantages.

Budget: It refers to the estimating tool that is in use to examine the future expenses and

incomes related to the specific period of time. As ABC limited use different budgets as per their

requirements.

Preparing a budget: At the time of budget formulation many steps are takes place that are

required to be followed by the manager of ABC limited in order to analyse the present position

of the company as well as available resources. After that formulate several plans that are

approved by manager in the betterment of an organization (Hoque, 2018).

Different type of budget:

Capital budget: In this, ABC limited is used to record all information that is related to the

various activities and functions in which a large capital investment is also considered.

ABC limited used this budget for analyzing financial performance and make plans for a

specific duration of time.

Advantages Disadvantages

Capital budget records all the activity of all

projects where the company invested large

amount of financial resources.

Lack of specificity is a demerit of this budget

as it includes the collective information

records of all departments of company.

Operating budget: It is related to that kind of budget in which overall expenses and

income of all projects are estimated that is totally based on the predicted sales as well as

revenue of ABC limited (Albanese, Andersen and Iabichino, 2015).

Advantages Disadvantages

It shows a clear view to the company’s

manager that monetary resources are properly

in used or not.

In this manipulation of figures could be done

simply so it is a disadvantage of operating

budget.

Alternative method of budgeting:

Zero based budgeting: This kind of budget is origin with the zero amount and used for

justifying the all expenses for every new period of time. It is mainly used by ABC limited

for minimizing the operational cost of company.

Advantages Disadvantages

It is accurate in nature as it is formulated for

each new accounting year with a zero base.

This is not suitable for short period of time

planning as it can be biases by the company

manager.

Traditional budgeting: It is related to the cash inflows and outflows of each income and

expenditure for a time period. It is expected to be followed by ABC limited monthly and

quarterly in order to keep the track record of financial resources.

Advantages Disadvantages

It helps in analysing company’s loss easily in

their financial statement.

It restricts the organizational ability to deal in

credit transactions.

Behavioral implication of budget:

Budget helps in developing the interaction and coordination among the company’s

employees.

It will result in efficient resource allocation that referred actual data rather then budgeted.

Process of budget preparation is complex in nature as it requires a high amount of

financial investment.

Pricing strategies: Penetration: In this a company ABC limited can initially sets low prices for their

offerings which are offered to the customers for selling purpose.

Zero based budgeting: This kind of budget is origin with the zero amount and used for

justifying the all expenses for every new period of time. It is mainly used by ABC limited

for minimizing the operational cost of company.

Advantages Disadvantages

It is accurate in nature as it is formulated for

each new accounting year with a zero base.

This is not suitable for short period of time

planning as it can be biases by the company

manager.

Traditional budgeting: It is related to the cash inflows and outflows of each income and

expenditure for a time period. It is expected to be followed by ABC limited monthly and

quarterly in order to keep the track record of financial resources.

Advantages Disadvantages

It helps in analysing company’s loss easily in

their financial statement.

It restricts the organizational ability to deal in

credit transactions.

Behavioral implication of budget:

Budget helps in developing the interaction and coordination among the company’s

employees.

It will result in efficient resource allocation that referred actual data rather then budgeted.

Process of budget preparation is complex in nature as it requires a high amount of

financial investment.

Pricing strategies: Penetration: In this a company ABC limited can initially sets low prices for their

offerings which are offered to the customers for selling purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.