HND Business: Management Accounting Report for Ever Joy Enterprises

VerifiedAdded on 2023/02/02

|24

|4702

|93

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Ever Joy Enterprises (UK), a company in the leisure and entertainment industry. It begins by defining management accounting and its objectives, differentiating it from financial accounting. The report explores cost accounting systems, including direct costing and standard costing, along with inventory management systems and job costing systems. It also discusses various management accounting reports and the importance of a sound accounting system. The report then delves into break-even analysis, calculating the number of tickets needed to break even and achieve a specific profit target. Furthermore, it evaluates the use of budgeting as a planning and problem-solving tool and assesses the role of strong financial governance. The report concludes with recommendations for Ever Joy Enterprises to improve its financial management and achieve sustainable success.

Management Accounting report for Ever Joy

Enterprises (UK)

1

Enterprises (UK)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Management Accounting.............................................................................................................4

a. Differences between Management Accounting and Financial Accounting.............................6

b. Cost accounting systems (Direct Costs and Standard Costing)...............................................8

c. Inventory Management Systems..............................................................................................9

d. Job costing systems................................................................................................................10

e. Different types management accounting reports....................................................................11

f. The need for a sound accounting system and the importance of the department producing

timely, accurate and relevant information..................................................................................13

Task 2............................................................................................................................................14

a. The number of tickets that must be sold to break even (i.e. the point at which there is neither

profit nor loss)............................................................................................................................14

b. If we want to make a profit of £30,000.00, how many tickets should be sold?.....................15

c. What profit would result if 8,000 tickets were sold?.............................................................16

Task 3............................................................................................................................................17

a. You are to evaluate how budgeting can be used by Ever Joy Enterprises as a planning and

problem-solving tool in dealing with financial problems, but also for leading the organization

to sustainable success.................................................................................................................17

b. You are to also evaluate how strong financial governance can help to pre-empt or prevent

financial problems for Ever Joy Enterprises and the means by which management accounting

systems can contribute...............................................................................................................19

Conclusion....................................................................................................................................22

References.....................................................................................................................................23

2

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

Management Accounting.............................................................................................................4

a. Differences between Management Accounting and Financial Accounting.............................6

b. Cost accounting systems (Direct Costs and Standard Costing)...............................................8

c. Inventory Management Systems..............................................................................................9

d. Job costing systems................................................................................................................10

e. Different types management accounting reports....................................................................11

f. The need for a sound accounting system and the importance of the department producing

timely, accurate and relevant information..................................................................................13

Task 2............................................................................................................................................14

a. The number of tickets that must be sold to break even (i.e. the point at which there is neither

profit nor loss)............................................................................................................................14

b. If we want to make a profit of £30,000.00, how many tickets should be sold?.....................15

c. What profit would result if 8,000 tickets were sold?.............................................................16

Task 3............................................................................................................................................17

a. You are to evaluate how budgeting can be used by Ever Joy Enterprises as a planning and

problem-solving tool in dealing with financial problems, but also for leading the organization

to sustainable success.................................................................................................................17

b. You are to also evaluate how strong financial governance can help to pre-empt or prevent

financial problems for Ever Joy Enterprises and the means by which management accounting

systems can contribute...............................................................................................................19

Conclusion....................................................................................................................................22

References.....................................................................................................................................23

2

Introduction

Management accounting is an integral part of the enterprises which helps them to achieve their

goals and objectives in an effective and efficient manner. This report will be prepared to reflect

and discuss the concept of managerial or management accounting and write a reference in the

context for EVER JOY ENTERPRISES (UK) that operates its business operations in leisure and

entertainment industry in the UK. This report defines the concept of job costing systems, cost

accounting systems and inventory management systems and its usage in the enterprises. This

report will also solve the given problems to assist the Ever Joy Enterprise reviewing its

performance in Manchester region to determine its feasibility by using the break-event point

formulae and which present the profits and BEP at which enterprises in the position of no profit

and no loss. This report also gives suitable advice to Ever Joy Enterprises on utilizing the

budgets as planning and problem-solving tools which solve the financial problems of the

enterprises.

3

Management accounting is an integral part of the enterprises which helps them to achieve their

goals and objectives in an effective and efficient manner. This report will be prepared to reflect

and discuss the concept of managerial or management accounting and write a reference in the

context for EVER JOY ENTERPRISES (UK) that operates its business operations in leisure and

entertainment industry in the UK. This report defines the concept of job costing systems, cost

accounting systems and inventory management systems and its usage in the enterprises. This

report will also solve the given problems to assist the Ever Joy Enterprise reviewing its

performance in Manchester region to determine its feasibility by using the break-event point

formulae and which present the profits and BEP at which enterprises in the position of no profit

and no loss. This report also gives suitable advice to Ever Joy Enterprises on utilizing the

budgets as planning and problem-solving tools which solve the financial problems of the

enterprises.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Management Accounting

Management Accounting is the accounting branch which basically deals with providing and

presenting accounting information to the manager in such an organized manner so that it can do

its managerial functions of planning, controlling and decision- making in an efficient and

effective manner. Management accounting acts as a decision-making support system to the

manager of an enterprises (Kaplan and Atkinson, 2015).

As per Certified Institute of Management Accountants (CIMA), United Kingdom,

“Management Accounting is an essential part of the company’s management concerned with

classifying, offering, and understanding information which is utilized for framing planning,

strategy and monitoring and governing activities or events, decision- making, optimal usage of

resources of an enterprise, disclosure to stakeholders and other external to the enterprises,

disclosure to workers or employees and assets safeguarding.

Objectives of Management Accounting

The main objective of management accounting is to offer important information to the

management for an efficient and effective execution of managerial functions. Various objectives

of management accounting are enumerated as follows:

1. Planning and policy- making: Management Accounting provides or offers important and

accurate information to the management in the process of its policy- making and planning to

attain goals and objectives.

2. Controlling: Management: Accounting applies various essential techniques or methods such

as Budgetary control, Management Audit, Standard Costing, and Responsibility Accounting to

ensure an effective management control over the resources use of the enterprise.

3. Communicating: Appropriate communication of the performance of many departments of an

enterprise to different administration levels is necessary required for planning, decision- making

and controlling.

4

Management Accounting

Management Accounting is the accounting branch which basically deals with providing and

presenting accounting information to the manager in such an organized manner so that it can do

its managerial functions of planning, controlling and decision- making in an efficient and

effective manner. Management accounting acts as a decision-making support system to the

manager of an enterprises (Kaplan and Atkinson, 2015).

As per Certified Institute of Management Accountants (CIMA), United Kingdom,

“Management Accounting is an essential part of the company’s management concerned with

classifying, offering, and understanding information which is utilized for framing planning,

strategy and monitoring and governing activities or events, decision- making, optimal usage of

resources of an enterprise, disclosure to stakeholders and other external to the enterprises,

disclosure to workers or employees and assets safeguarding.

Objectives of Management Accounting

The main objective of management accounting is to offer important information to the

management for an efficient and effective execution of managerial functions. Various objectives

of management accounting are enumerated as follows:

1. Planning and policy- making: Management Accounting provides or offers important and

accurate information to the management in the process of its policy- making and planning to

attain goals and objectives.

2. Controlling: Management: Accounting applies various essential techniques or methods such

as Budgetary control, Management Audit, Standard Costing, and Responsibility Accounting to

ensure an effective management control over the resources use of the enterprise.

3. Communicating: Appropriate communication of the performance of many departments of an

enterprise to different administration levels is necessary required for planning, decision- making

and controlling.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Analysis and interpretation of financial statements: Management Accounting gathers,

analyses and understands the important data from the results shown by the cost and financial

accounting system, and also offers important and appropriate information to the management in a

useful and systematic manner.

5. Decision- making: Management accounting offers important and accurate information to the

management in the process of its decision- making. The growth and success of management

highly and mostly depends upon a perfect decision- making.

6. Tax planning: Management accounting assists to the management in the process of tax

planning by availing various tax rebates and reliefs and, thus, minimizes the tax burden of the

enterprise on the whole.

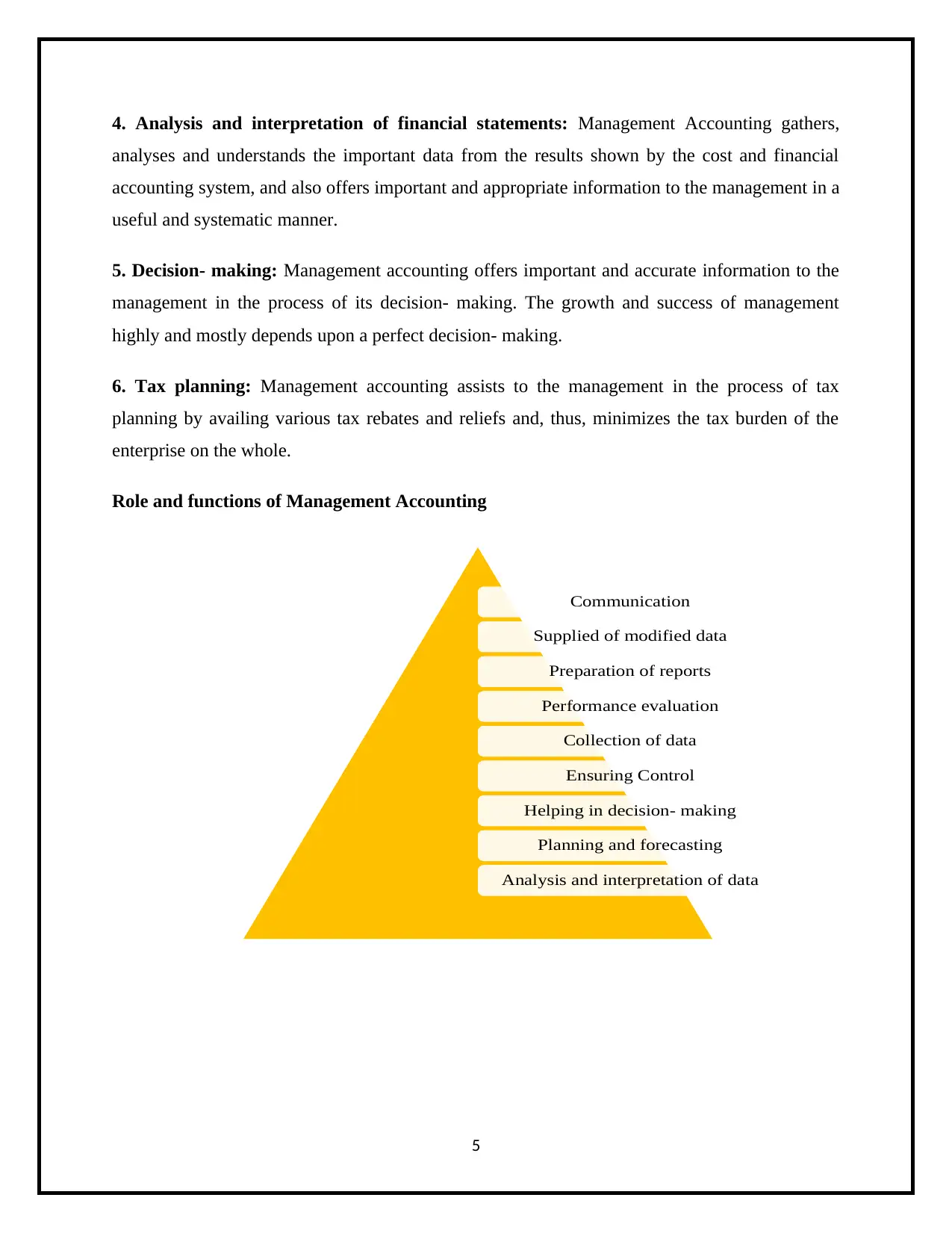

Role and functions of Management Accounting

5

Communication

Supplied of modified data

Preparation of reports

Performance evaluation

Collection of data

Ensuring Control

Helping in decision- making

Planning and forecasting

Analysis and interpretation of data

analyses and understands the important data from the results shown by the cost and financial

accounting system, and also offers important and appropriate information to the management in a

useful and systematic manner.

5. Decision- making: Management accounting offers important and accurate information to the

management in the process of its decision- making. The growth and success of management

highly and mostly depends upon a perfect decision- making.

6. Tax planning: Management accounting assists to the management in the process of tax

planning by availing various tax rebates and reliefs and, thus, minimizes the tax burden of the

enterprise on the whole.

Role and functions of Management Accounting

5

Communication

Supplied of modified data

Preparation of reports

Performance evaluation

Collection of data

Ensuring Control

Helping in decision- making

Planning and forecasting

Analysis and interpretation of data

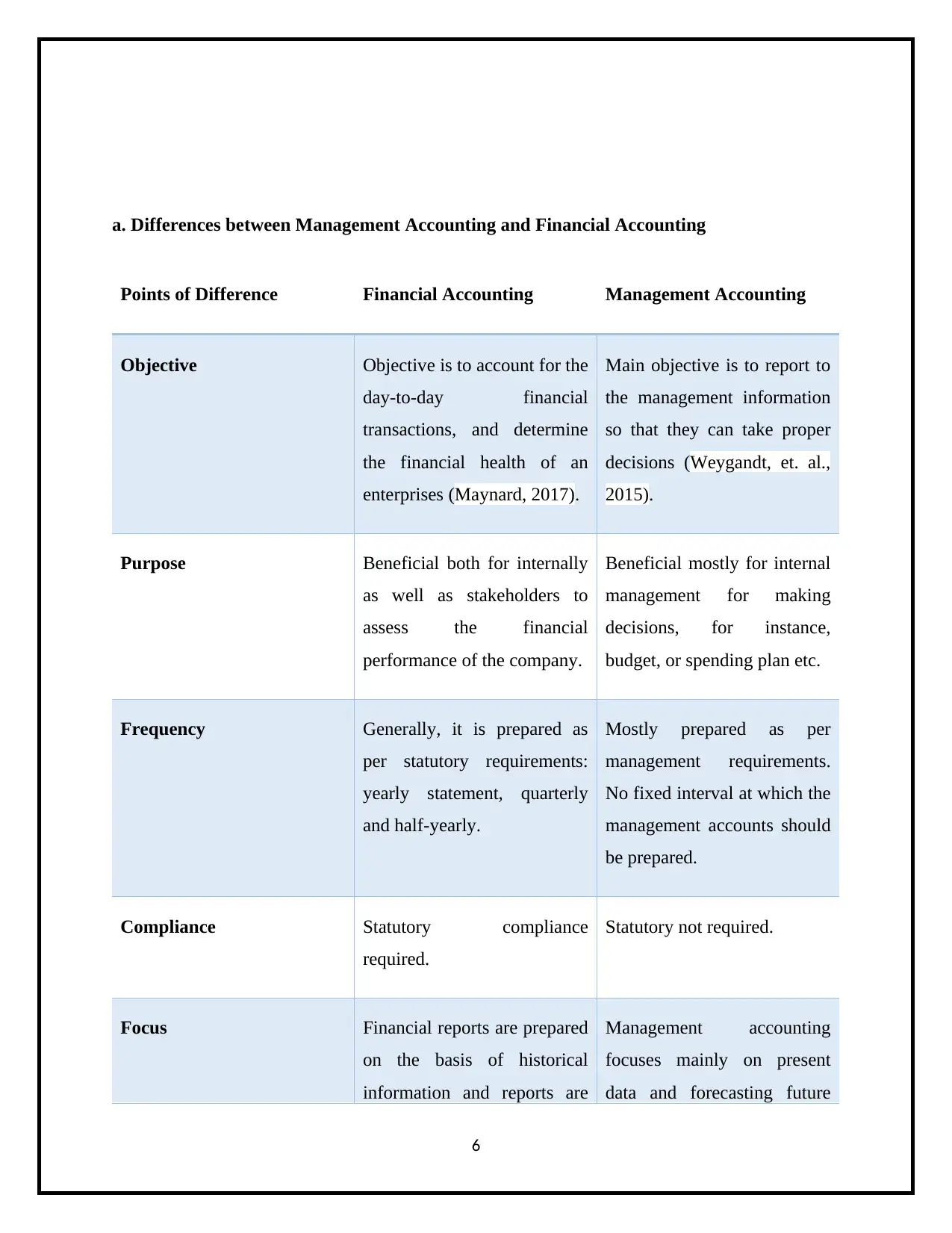

a. Differences between Management Accounting and Financial Accounting

Points of Difference Financial Accounting Management Accounting

Objective Objective is to account for the

day-to-day financial

transactions, and determine

the financial health of an

enterprises (Maynard, 2017).

Main objective is to report to

the management information

so that they can take proper

decisions (Weygandt, et. al.,

2015).

Purpose Beneficial both for internally

as well as stakeholders to

assess the financial

performance of the company.

Beneficial mostly for internal

management for making

decisions, for instance,

budget, or spending plan etc.

Frequency Generally, it is prepared as

per statutory requirements:

yearly statement, quarterly

and half-yearly.

Mostly prepared as per

management requirements.

No fixed interval at which the

management accounts should

be prepared.

Compliance Statutory compliance

required.

Statutory not required.

Focus Financial reports are prepared

on the basis of historical

information and reports are

Management accounting

focuses mainly on present

data and forecasting future

6

Points of Difference Financial Accounting Management Accounting

Objective Objective is to account for the

day-to-day financial

transactions, and determine

the financial health of an

enterprises (Maynard, 2017).

Main objective is to report to

the management information

so that they can take proper

decisions (Weygandt, et. al.,

2015).

Purpose Beneficial both for internally

as well as stakeholders to

assess the financial

performance of the company.

Beneficial mostly for internal

management for making

decisions, for instance,

budget, or spending plan etc.

Frequency Generally, it is prepared as

per statutory requirements:

yearly statement, quarterly

and half-yearly.

Mostly prepared as per

management requirements.

No fixed interval at which the

management accounts should

be prepared.

Compliance Statutory compliance

required.

Statutory not required.

Focus Financial reports are prepared

on the basis of historical

information and reports are

Management accounting

focuses mainly on present

data and forecasting future

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prepared for a fixed period of

time.

reports.

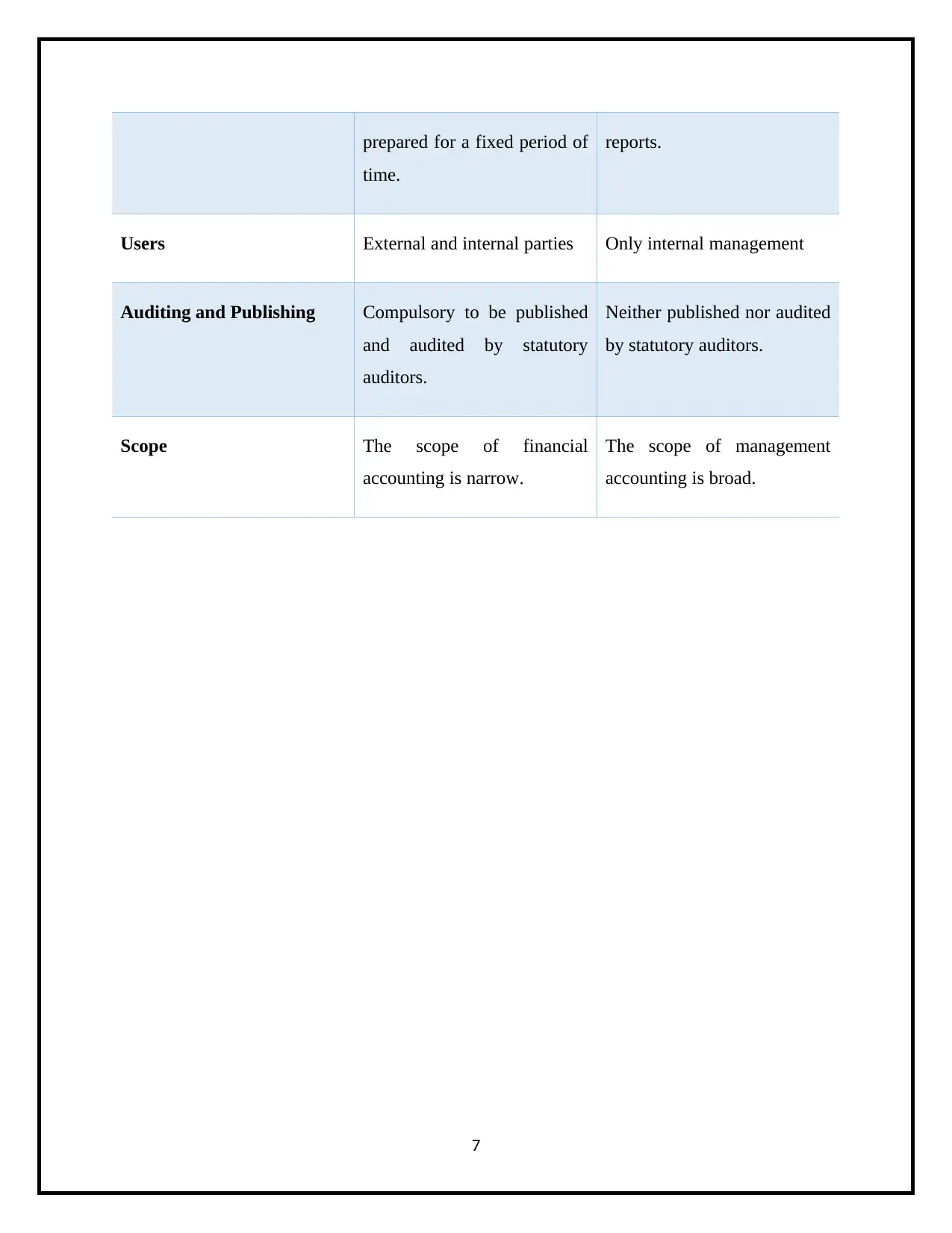

Users External and internal parties Only internal management

Auditing and Publishing Compulsory to be published

and audited by statutory

auditors.

Neither published nor audited

by statutory auditors.

Scope The scope of financial

accounting is narrow.

The scope of management

accounting is broad.

7

time.

reports.

Users External and internal parties Only internal management

Auditing and Publishing Compulsory to be published

and audited by statutory

auditors.

Neither published nor audited

by statutory auditors.

Scope The scope of financial

accounting is narrow.

The scope of management

accounting is broad.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Cost accounting systems (Direct Costs and Standard Costing)

The cost accounting systems can assist the company in so many ways. It provides an exact

product cost, delivers valuable operational and financial information, and also evaluates the

performance. The cost accounting includes measuring, recording, and reporting of product costs.

This system assists to the Ever Joy Enterprises to estimate the cost of their products for

profitability analysis, valuation of inventory, and control the cost. The Ever Joy Enterprises can

utilize this framework to assess the productivity in the procedures and this framework likewise

helps in making the upgrades in the up and coming procedures of the enterprises. It will likewise

help the enterprises in value obsession of the item and limits the wastages in the assembling

procedure (DRURY, 2013). It additionally gives helpful data to the administration bookkeeper

for the further arranging of the items.

Types of costs

Direct Costing: It is a type of costing method which uses only variable manufacturing costs are

allocated to cost of goods sold and inventory. This method can be used internally and not for

external purpose. While preparing the financial statements both fixed cost and variable cost are

considered and assigned to the products (Weygandt, et. al., 2015).

Standard Costing: In standard costing some standards are fixed by the manufacturer regarding

product or service. The manufacturers identify the variances in between actual and standard

costs. If the enterprises had incurred more than the standard costs, then the enterprises will not

meet its projected or estimated net income (Maynard, 2017).

8

The cost accounting systems can assist the company in so many ways. It provides an exact

product cost, delivers valuable operational and financial information, and also evaluates the

performance. The cost accounting includes measuring, recording, and reporting of product costs.

This system assists to the Ever Joy Enterprises to estimate the cost of their products for

profitability analysis, valuation of inventory, and control the cost. The Ever Joy Enterprises can

utilize this framework to assess the productivity in the procedures and this framework likewise

helps in making the upgrades in the up and coming procedures of the enterprises. It will likewise

help the enterprises in value obsession of the item and limits the wastages in the assembling

procedure (DRURY, 2013). It additionally gives helpful data to the administration bookkeeper

for the further arranging of the items.

Types of costs

Direct Costing: It is a type of costing method which uses only variable manufacturing costs are

allocated to cost of goods sold and inventory. This method can be used internally and not for

external purpose. While preparing the financial statements both fixed cost and variable cost are

considered and assigned to the products (Weygandt, et. al., 2015).

Standard Costing: In standard costing some standards are fixed by the manufacturer regarding

product or service. The manufacturers identify the variances in between actual and standard

costs. If the enterprises had incurred more than the standard costs, then the enterprises will not

meet its projected or estimated net income (Maynard, 2017).

8

c. Inventory Management Systems

The stock administration frameworks will allude to the way toward bookkeeping in which

inventories including the completed merchandise and work in advancement will be overseen and

revealed properly and convenient for making progress in the creation limits. The stock

administration will be vital for the venture with the end goal to accomplish the ideal dimension

of stock to be held in the organization which will result in opportune accessibility of stock and

will likewise help with accomplishing least expense of stock held in the organization (Holm,

2018). The essential points of executing stock administration framework in the enterprise are:

Attaining an ideal stock level of stock that must be kept up in the enterprise with the goal that no

requests are postponed and the expense of support is least for the enterprises.

Identifying the ideal level of placing the orders for buying of different materials and building the

concept of just in time inventory.

The inventory management system will use different kinds of methods which are summarized as

below:

First in first out method

Last in first out method

Just in time method

Weighted average method

9

The stock administration frameworks will allude to the way toward bookkeeping in which

inventories including the completed merchandise and work in advancement will be overseen and

revealed properly and convenient for making progress in the creation limits. The stock

administration will be vital for the venture with the end goal to accomplish the ideal dimension

of stock to be held in the organization which will result in opportune accessibility of stock and

will likewise help with accomplishing least expense of stock held in the organization (Holm,

2018). The essential points of executing stock administration framework in the enterprise are:

Attaining an ideal stock level of stock that must be kept up in the enterprise with the goal that no

requests are postponed and the expense of support is least for the enterprises.

Identifying the ideal level of placing the orders for buying of different materials and building the

concept of just in time inventory.

The inventory management system will use different kinds of methods which are summarized as

below:

First in first out method

Last in first out method

Just in time method

Weighted average method

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

d. Job costing systems

Job costing systems is a system for assigning the production or manufacturing costs to a specific

batches or products. Basically, this costing system is utilized only when the products produced

are different from each other. Job costing includes the accumulation materials, labor and

overhead costs for a particular job. For instance, a job costing is useful in the designing a

software program, manufacturing a small batch of products, constructing a custom machine

(DRURY, 2013).

In a job costing it includes the following activities which are listed below:

Materials

Labor

Overhead

Job costing assists to the Ever Joy Enterprises by providing useful information regarding

particular job in an accurate manner. The management easily accumulated the price of job and

estimated how much cost involved in this job. The whole data are stored in the database of the

company which provides relevant information to the management and its customers.

10

Job costing systems is a system for assigning the production or manufacturing costs to a specific

batches or products. Basically, this costing system is utilized only when the products produced

are different from each other. Job costing includes the accumulation materials, labor and

overhead costs for a particular job. For instance, a job costing is useful in the designing a

software program, manufacturing a small batch of products, constructing a custom machine

(DRURY, 2013).

In a job costing it includes the following activities which are listed below:

Materials

Labor

Overhead

Job costing assists to the Ever Joy Enterprises by providing useful information regarding

particular job in an accurate manner. The management easily accumulated the price of job and

estimated how much cost involved in this job. The whole data are stored in the database of the

company which provides relevant information to the management and its customers.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e. Different types management accounting reports

Reports Description Use in Ever Joy Enterprise

Cost and revenue reports The cost and revenue reports

give data with respect to cost

engaged with different

procedures and income

created there from. It

empowers the administration

to dissect the operational

productivity of the business

(DRURY, 2013).

It will empower the

administration of Ever Joy

Enterprises (UK) to plan

future business

methodologies and

furthermore follow if there is

any wasteful procedure.

Performance reports Performance report is an

explanation that evaluates the

result of an action over a

predefined time allotment. It

is set up to survey the

execution (Kaplan and

Atkinson, 2015).

Performance report can be

instrumental in Ever Joy

Enterprises (UK) to evaluate

its arrangements dependent

on their execution/result and

it can outline the future

systems appropriately.

Inventory reports Inventory report condenses

different things having a

place with a business,

industry, association. It gives

a record of inventory level in

an organization including raw

material, finished goods, etc.

Inventory reports can be

utilized in Ever Joy

Enterprises (UK) to monitor

stock and different things.

11

Reports Description Use in Ever Joy Enterprise

Cost and revenue reports The cost and revenue reports

give data with respect to cost

engaged with different

procedures and income

created there from. It

empowers the administration

to dissect the operational

productivity of the business

(DRURY, 2013).

It will empower the

administration of Ever Joy

Enterprises (UK) to plan

future business

methodologies and

furthermore follow if there is

any wasteful procedure.

Performance reports Performance report is an

explanation that evaluates the

result of an action over a

predefined time allotment. It

is set up to survey the

execution (Kaplan and

Atkinson, 2015).

Performance report can be

instrumental in Ever Joy

Enterprises (UK) to evaluate

its arrangements dependent

on their execution/result and

it can outline the future

systems appropriately.

Inventory reports Inventory report condenses

different things having a

place with a business,

industry, association. It gives

a record of inventory level in

an organization including raw

material, finished goods, etc.

Inventory reports can be

utilized in Ever Joy

Enterprises (UK) to monitor

stock and different things.

11

(Holm, 2018).

Budgetary reports Budgetary report is a report

that empowers the

administrator to think about

the projections made toward

the start of the year with real

execution. It is intended to

decide concerning how close

be the real execution with the

planned execution (Maynard,

2017).

Ever Joy Enterprises (UK)

can utilize Budgetary report

to dissect the productivity of

the business. In the event that

there is any deviation

between the genuine

execution and planned

execution it can discover the

purpose behind a similar

which will empower it to

frame better business

methodologies in future.

12

Budgetary reports Budgetary report is a report

that empowers the

administrator to think about

the projections made toward

the start of the year with real

execution. It is intended to

decide concerning how close

be the real execution with the

planned execution (Maynard,

2017).

Ever Joy Enterprises (UK)

can utilize Budgetary report

to dissect the productivity of

the business. In the event that

there is any deviation

between the genuine

execution and planned

execution it can discover the

purpose behind a similar

which will empower it to

frame better business

methodologies in future.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.