Management Accounting: Evaluating Systems, Techniques, and Budgeting

VerifiedAdded on 2022/11/30

|17

|4442

|112

Report

AI Summary

This report on management accounting delves into various aspects of the discipline, including its role in decision-making, performance evaluation, and financial reporting. It discusses management accounting systems like inventory management, price optimization, cost accounting, and job costing, evaluating their benefits and applications within a business context. The report further explores different types of management accounting reporting such as inventory management, performance, and accounts receivable reports. It also covers cost calculation techniques, including marginal and absorption costing, and examines a range of management accounting techniques used to produce financial accounting documents. Additionally, the report analyzes planning tools like cash budgets, outlining their advantages and disadvantages. Finally, it assesses how businesses adapt management accounting systems to address financial challenges, emphasizing the role of management accounting in achieving sustainable success and resolving financial problems.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Discussion of management accounting and requirements of its systems.........................................3

P2. Different types of management accounting reporting......................................................................4

M1. Evaluate the benefits of management accounting systems along with its applications...................6

TASK 2..........................................................................................................................................................7

P3 Calculate cost by using appropriate techniques.................................................................................7

M2. Range of management accounting techniques which used to produce financial accounting

documents...............................................................................................................................................8

TASK 3..........................................................................................................................................................9

P4. Advantage & disadvantage of various planning tools which used for budgetary control..................9

M3. Evaluate different planning tools which required for forecasting budget......................................11

TASK 4........................................................................................................................................................11

P5. Compare how business adapting management accounting system to respond their financial

problems...............................................................................................................................................11

M4. Evaluate that how organization lead sustainable success by using management accounting and

resolve financial problems.....................................................................................................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Discussion of management accounting and requirements of its systems.........................................3

P2. Different types of management accounting reporting......................................................................4

M1. Evaluate the benefits of management accounting systems along with its applications...................6

TASK 2..........................................................................................................................................................7

P3 Calculate cost by using appropriate techniques.................................................................................7

M2. Range of management accounting techniques which used to produce financial accounting

documents...............................................................................................................................................8

TASK 3..........................................................................................................................................................9

P4. Advantage & disadvantage of various planning tools which used for budgetary control..................9

M3. Evaluate different planning tools which required for forecasting budget......................................11

TASK 4........................................................................................................................................................11

P5. Compare how business adapting management accounting system to respond their financial

problems...............................................................................................................................................11

M4. Evaluate that how organization lead sustainable success by using management accounting and

resolve financial problems.....................................................................................................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a discipline that requires involvement in decision-making

procedures, the development of performance appraisal and monitoring systems, and the

provision of financial reporting and monitoring resources to traditional authorities in designing

and executing the corporate objectives. Numerous management accounting principles are used

by the enterprise to aid managers' judgment processes in meeting organizational objectives (Shen

and et.al, 2020). It is the method of assessing company expenses and expenditures in order to

create appropriate financial reports, databases, and accounts. This report addresses a variety of

subjects, including the use of management accounting schemes, reports, incentives, and cost

estimation using multiple costing strategies. As well as this, the business employs a variety of

strategy methods. This report further compares the aspects wherein management accounting aids

in the resolution of financial difficulties.

TASK 1

P1. Discussion of management accounting and requirements of its systems

Management accounting: Management accounting may be described as a general

framework for communicating and presenting account records or critical details to management

staff in order to assist them in decision-making tasks. Furthermore, this term will be used by the

entity's local employees in order to achieve operational mission and targets.

Inventory management system: This method focuses on the efficient control of

inventories and associated products. This method enables efficient leverage of all activities that

are attributable to handling and using stocks in industry. This is a method for companies like

EECL to monitor all of their inventories, such as products used to manufacture smoothies,

packaging products, finished goods, and so on, via the entity's distribution chain. It produces the

entire collection, from making orders with various wholesalers to ensuring the satisfaction of its

consumer spending, showing the complete approach of making finished products. Entities will

reduce duplication by closely analyzing items, sorting situations, and settling on more brilliant

choices dependent (Amadi and Ejiogu, 2021). This method necessitates the tracking of any

transfer of stock/inventory in or out at various levels, as well as the fair identification of stocks

inside an organizational sense.

Management accounting is a discipline that requires involvement in decision-making

procedures, the development of performance appraisal and monitoring systems, and the

provision of financial reporting and monitoring resources to traditional authorities in designing

and executing the corporate objectives. Numerous management accounting principles are used

by the enterprise to aid managers' judgment processes in meeting organizational objectives (Shen

and et.al, 2020). It is the method of assessing company expenses and expenditures in order to

create appropriate financial reports, databases, and accounts. This report addresses a variety of

subjects, including the use of management accounting schemes, reports, incentives, and cost

estimation using multiple costing strategies. As well as this, the business employs a variety of

strategy methods. This report further compares the aspects wherein management accounting aids

in the resolution of financial difficulties.

TASK 1

P1. Discussion of management accounting and requirements of its systems

Management accounting: Management accounting may be described as a general

framework for communicating and presenting account records or critical details to management

staff in order to assist them in decision-making tasks. Furthermore, this term will be used by the

entity's local employees in order to achieve operational mission and targets.

Inventory management system: This method focuses on the efficient control of

inventories and associated products. This method enables efficient leverage of all activities that

are attributable to handling and using stocks in industry. This is a method for companies like

EECL to monitor all of their inventories, such as products used to manufacture smoothies,

packaging products, finished goods, and so on, via the entity's distribution chain. It produces the

entire collection, from making orders with various wholesalers to ensuring the satisfaction of its

consumer spending, showing the complete approach of making finished products. Entities will

reduce duplication by closely analyzing items, sorting situations, and settling on more brilliant

choices dependent (Amadi and Ejiogu, 2021). This method necessitates the tracking of any

transfer of stock/inventory in or out at various levels, as well as the fair identification of stocks

inside an organizational sense.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system: It is the most important accounting mechanism because it

enables the company to change the price of a commodity based on customer motivation, thus

achieving the company's mission. They want to relate their annual income to profits for EECL,

which means that optimal retail prices are required, particularly unless the corporation's target is

to maximize profits while maintaining the same level of customer retention. This has become

increasingly important as actual business selling price trends become highly profitable. A variety

of companies, even those in business market segments, are now looking to release creative

products. In that way, having the right price becomes more and more essential, or a company

could end up losing a significant portion of its client base to competitors (Zou, 2019).

Cost accounting system: Manufacturing firms use costing methods to actively monitor the

movement of items via the various stages of processing and measure each manufacturer's

expense at specific points. The overall cost of the items in the employment and finished state

must be calculated. Furthermore, EECL executives should devise strategies to minimize or

control costs in the production process.

Job costing system: This method was used to calculate the performance of based products

in the organisation. It is a term used to define audit criteria on a closed economy used in a

production facility. The director of Alpha Ltd will use this mechanism to optimize their

corporate efficiency with the assistance of the job order costing method. This accounting system

was predominantly often used evaluate the purchasing costing of every other functional member.

This system was being used whenever things are segregated into diverse communities and are

vastly different from the others in relation to price.

The accounting systems listed above are used by EECL administrators to increase overall

organizational performance and efficacy. Companies maintain their stock levels, monitor their

costs, and identify the necessary price for goods that fulfill the needs of their consumers and

corporate goals (Qasim and Kharbat, 2020).

P2. Different types of management accounting reporting

Management accounting reporting is a set of accounting records that analyze what's

really moving on in the company. Those other reports are prepared for a range of functions, like

taxation or management. It aids in the collection of data and provides valuable knowledge about

enables the company to change the price of a commodity based on customer motivation, thus

achieving the company's mission. They want to relate their annual income to profits for EECL,

which means that optimal retail prices are required, particularly unless the corporation's target is

to maximize profits while maintaining the same level of customer retention. This has become

increasingly important as actual business selling price trends become highly profitable. A variety

of companies, even those in business market segments, are now looking to release creative

products. In that way, having the right price becomes more and more essential, or a company

could end up losing a significant portion of its client base to competitors (Zou, 2019).

Cost accounting system: Manufacturing firms use costing methods to actively monitor the

movement of items via the various stages of processing and measure each manufacturer's

expense at specific points. The overall cost of the items in the employment and finished state

must be calculated. Furthermore, EECL executives should devise strategies to minimize or

control costs in the production process.

Job costing system: This method was used to calculate the performance of based products

in the organisation. It is a term used to define audit criteria on a closed economy used in a

production facility. The director of Alpha Ltd will use this mechanism to optimize their

corporate efficiency with the assistance of the job order costing method. This accounting system

was predominantly often used evaluate the purchasing costing of every other functional member.

This system was being used whenever things are segregated into diverse communities and are

vastly different from the others in relation to price.

The accounting systems listed above are used by EECL administrators to increase overall

organizational performance and efficacy. Companies maintain their stock levels, monitor their

costs, and identify the necessary price for goods that fulfill the needs of their consumers and

corporate goals (Qasim and Kharbat, 2020).

P2. Different types of management accounting reporting

Management accounting reporting is a set of accounting records that analyze what's

really moving on in the company. Those other reports are prepared for a range of functions, like

taxation or management. It aids in the collection of data and provides valuable knowledge about

activities. There are several categories of management accounting records, some of which are

mentioned elsewhere here:

Inventory management report: It is one of the best or most appropriate reports for the

automotive industry. The corporation then managed their inventory volume for manufacturing

purposes. In the framework of EECL, managers use this monitoring method to analyze supply

requirements at the development stage. Managers may use this report to determine the amount of

stock required for the production. For instance, if a company orders more raw materials than it

needs, there is a high risk of losing stock that raises manufacturing costs and reduces profit

margins. In the other hand, if the ordered quantity is poor in comparison to the demand, the

business will face a supply issue, which would have a significant effect on both production and

profitability (Sangster, Stoner and Flood, 2020).

Performance report: It is a systematic study of all actions taken by workers as well as

corporate roles. As an example: Annual review reports are created by every individual and assist

the company with analyzing performance levels. It is therefore advantageous for the boss to

include benefits and other resources to inspire workers in recognition of their positive

contributions. This study is used by EECL's managers to assess or devise policy depending on

the conditions. Businesses may also determine whether or not further improvements are

expected. If this is the case, the manager may implement a variety of programs to develop

particular talents and competencies.

Accounts receivable report: This report, also known as trade receivables repayment,

includes the balance held by the client. Organizations can detect debtors and create additional

techniques to reduce their safety. Through its assistance, EECL's administrator generates an

account receivable report, which aids in the creation of a credit policy that includes a variety of

strict user agreement. Both activities would lower the quantity of defaulters while still assisting

the manager in determining the unpaid figure.

The accounting reports listed above assist the manager in evaluating all of the details that

is useful to the company. It also aids managers in their decision-making processes, where

different techniques are developed based on the knowledge gathered. These reports aid in the

comparison of facts and the formulation of strategies to improve organizational performance or

mentioned elsewhere here:

Inventory management report: It is one of the best or most appropriate reports for the

automotive industry. The corporation then managed their inventory volume for manufacturing

purposes. In the framework of EECL, managers use this monitoring method to analyze supply

requirements at the development stage. Managers may use this report to determine the amount of

stock required for the production. For instance, if a company orders more raw materials than it

needs, there is a high risk of losing stock that raises manufacturing costs and reduces profit

margins. In the other hand, if the ordered quantity is poor in comparison to the demand, the

business will face a supply issue, which would have a significant effect on both production and

profitability (Sangster, Stoner and Flood, 2020).

Performance report: It is a systematic study of all actions taken by workers as well as

corporate roles. As an example: Annual review reports are created by every individual and assist

the company with analyzing performance levels. It is therefore advantageous for the boss to

include benefits and other resources to inspire workers in recognition of their positive

contributions. This study is used by EECL's managers to assess or devise policy depending on

the conditions. Businesses may also determine whether or not further improvements are

expected. If this is the case, the manager may implement a variety of programs to develop

particular talents and competencies.

Accounts receivable report: This report, also known as trade receivables repayment,

includes the balance held by the client. Organizations can detect debtors and create additional

techniques to reduce their safety. Through its assistance, EECL's administrator generates an

account receivable report, which aids in the creation of a credit policy that includes a variety of

strict user agreement. Both activities would lower the quantity of defaulters while still assisting

the manager in determining the unpaid figure.

The accounting reports listed above assist the manager in evaluating all of the details that

is useful to the company. It also aids managers in their decision-making processes, where

different techniques are developed based on the knowledge gathered. These reports aid in the

comparison of facts and the formulation of strategies to improve organizational performance or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

efficacy. It raises product efficiency, which increases demand and, as a result, competitiveness or

competitiveness (Moll and Yigitbasioglu, 2019).

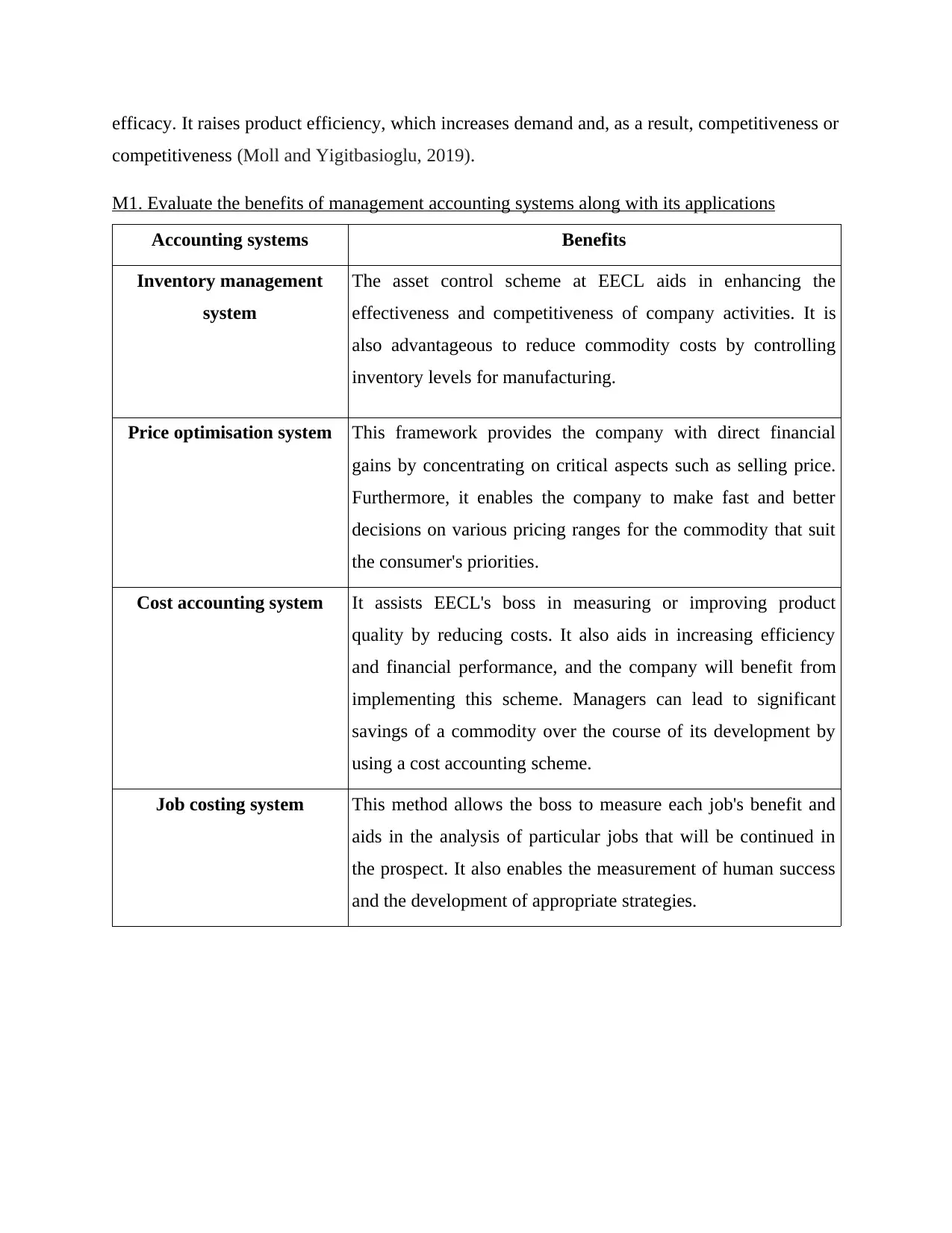

M1. Evaluate the benefits of management accounting systems along with its applications

Accounting systems Benefits

Inventory management

system

The asset control scheme at EECL aids in enhancing the

effectiveness and competitiveness of company activities. It is

also advantageous to reduce commodity costs by controlling

inventory levels for manufacturing.

Price optimisation system This framework provides the company with direct financial

gains by concentrating on critical aspects such as selling price.

Furthermore, it enables the company to make fast and better

decisions on various pricing ranges for the commodity that suit

the consumer's priorities.

Cost accounting system It assists EECL's boss in measuring or improving product

quality by reducing costs. It also aids in increasing efficiency

and financial performance, and the company will benefit from

implementing this scheme. Managers can lead to significant

savings of a commodity over the course of its development by

using a cost accounting scheme.

Job costing system This method allows the boss to measure each job's benefit and

aids in the analysis of particular jobs that will be continued in

the prospect. It also enables the measurement of human success

and the development of appropriate strategies.

competitiveness (Moll and Yigitbasioglu, 2019).

M1. Evaluate the benefits of management accounting systems along with its applications

Accounting systems Benefits

Inventory management

system

The asset control scheme at EECL aids in enhancing the

effectiveness and competitiveness of company activities. It is

also advantageous to reduce commodity costs by controlling

inventory levels for manufacturing.

Price optimisation system This framework provides the company with direct financial

gains by concentrating on critical aspects such as selling price.

Furthermore, it enables the company to make fast and better

decisions on various pricing ranges for the commodity that suit

the consumer's priorities.

Cost accounting system It assists EECL's boss in measuring or improving product

quality by reducing costs. It also aids in increasing efficiency

and financial performance, and the company will benefit from

implementing this scheme. Managers can lead to significant

savings of a commodity over the course of its development by

using a cost accounting scheme.

Job costing system This method allows the boss to measure each job's benefit and

aids in the analysis of particular jobs that will be continued in

the prospect. It also enables the measurement of human success

and the development of appropriate strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

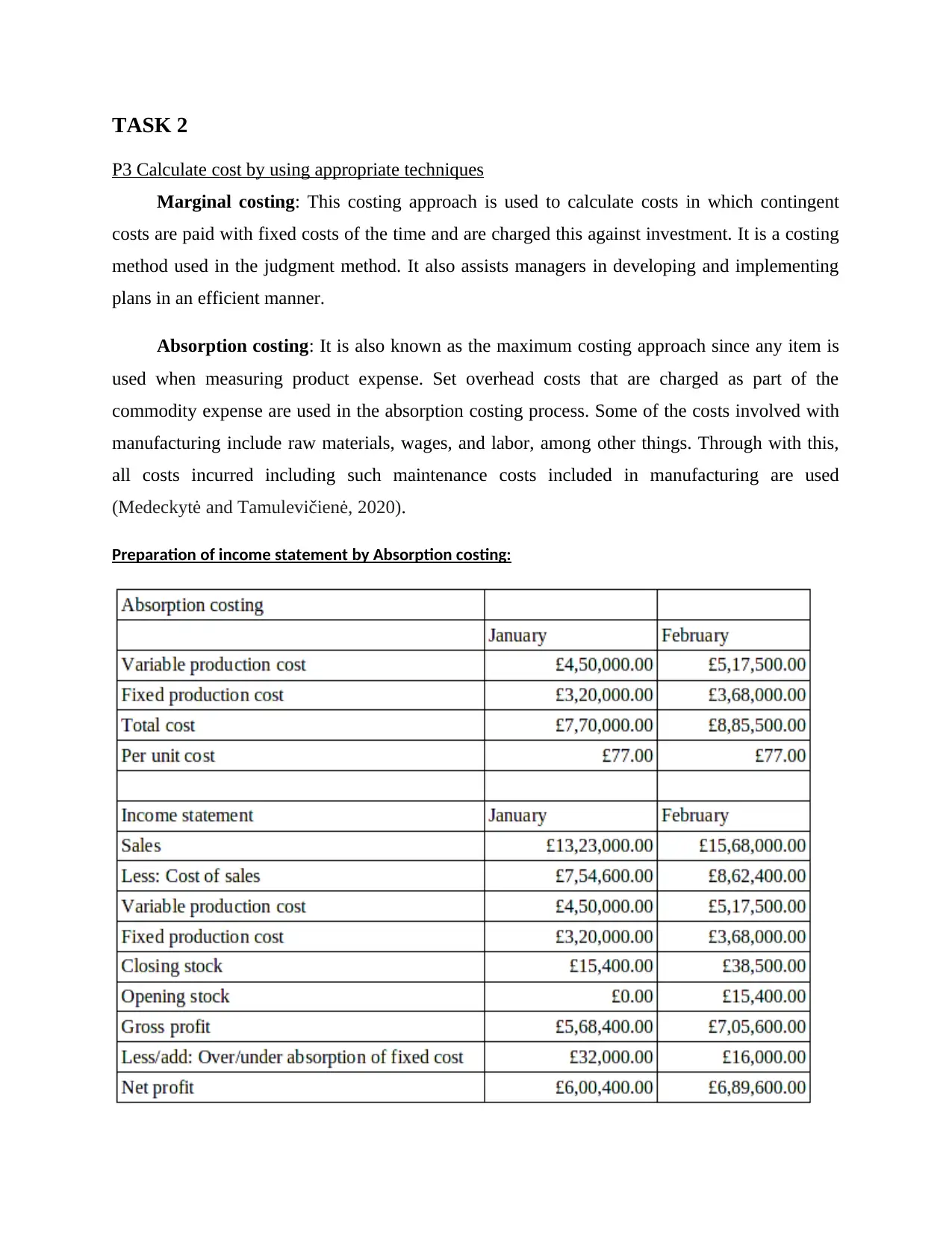

P3 Calculate cost by using appropriate techniques

Marginal costing: This costing approach is used to calculate costs in which contingent

costs are paid with fixed costs of the time and are charged this against investment. It is a costing

method used in the judgment method. It also assists managers in developing and implementing

plans in an efficient manner.

Absorption costing: It is also known as the maximum costing approach since any item is

used when measuring product expense. Set overhead costs that are charged as part of the

commodity expense are used in the absorption costing process. Some of the costs involved with

manufacturing include raw materials, wages, and labor, among other things. Through with this,

all costs incurred including such maintenance costs included in manufacturing are used

(Medeckytė and Tamulevičienė, 2020).

Preparation of income statement by Absorption costing:

P3 Calculate cost by using appropriate techniques

Marginal costing: This costing approach is used to calculate costs in which contingent

costs are paid with fixed costs of the time and are charged this against investment. It is a costing

method used in the judgment method. It also assists managers in developing and implementing

plans in an efficient manner.

Absorption costing: It is also known as the maximum costing approach since any item is

used when measuring product expense. Set overhead costs that are charged as part of the

commodity expense are used in the absorption costing process. Some of the costs involved with

manufacturing include raw materials, wages, and labor, among other things. Through with this,

all costs incurred including such maintenance costs included in manufacturing are used

(Medeckytė and Tamulevičienė, 2020).

Preparation of income statement by Absorption costing:

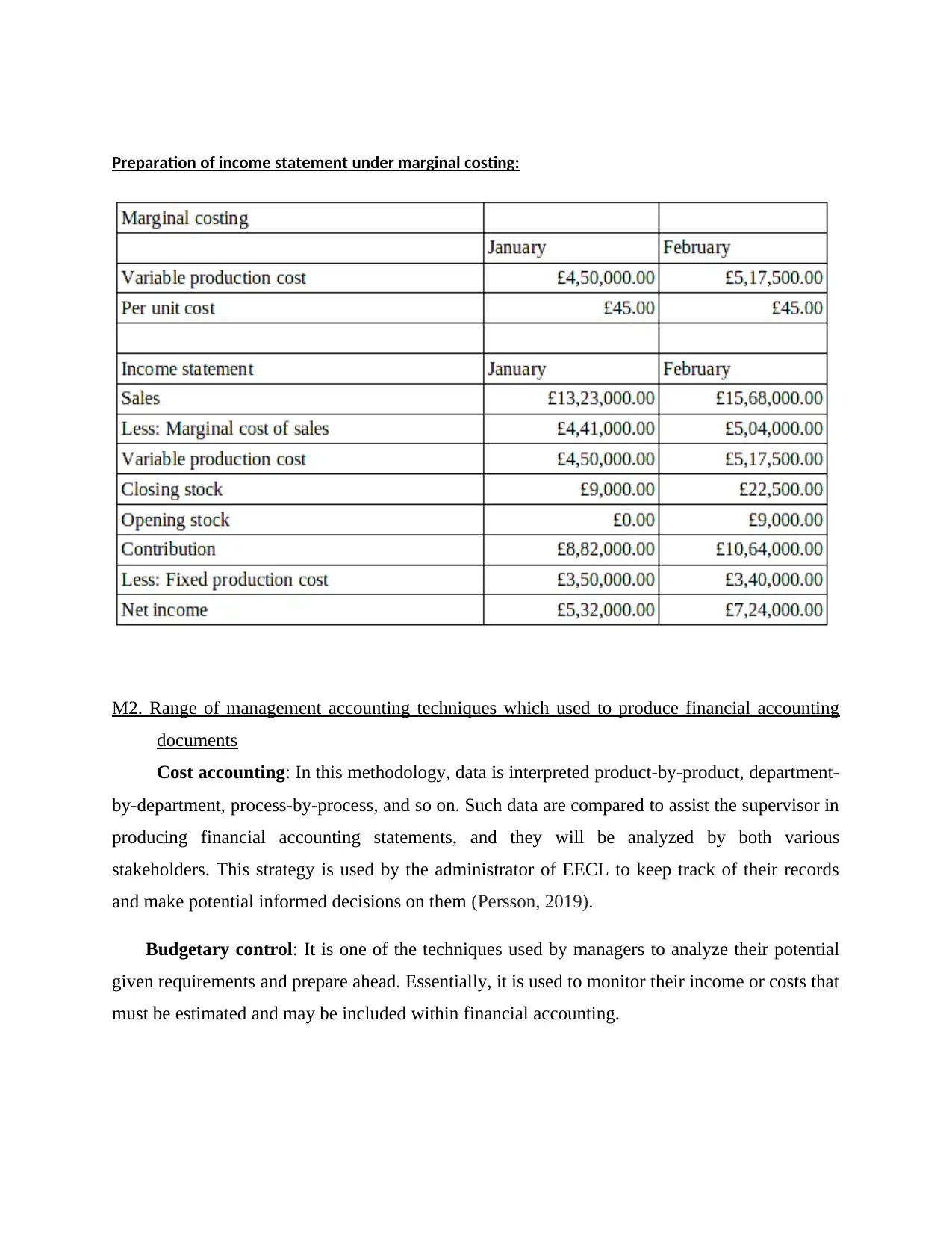

Preparation of income statement under marginal costing:

M2. Range of management accounting techniques which used to produce financial accounting

documents

Cost accounting: In this methodology, data is interpreted product-by-product, department-

by-department, process-by-process, and so on. Such data are compared to assist the supervisor in

producing financial accounting statements, and they will be analyzed by both various

stakeholders. This strategy is used by the administrator of EECL to keep track of their records

and make potential informed decisions on them (Persson, 2019).

Budgetary control: It is one of the techniques used by managers to analyze their potential

given requirements and prepare ahead. Essentially, it is used to monitor their income or costs that

must be estimated and may be included within financial accounting.

M2. Range of management accounting techniques which used to produce financial accounting

documents

Cost accounting: In this methodology, data is interpreted product-by-product, department-

by-department, process-by-process, and so on. Such data are compared to assist the supervisor in

producing financial accounting statements, and they will be analyzed by both various

stakeholders. This strategy is used by the administrator of EECL to keep track of their records

and make potential informed decisions on them (Persson, 2019).

Budgetary control: It is one of the techniques used by managers to analyze their potential

given requirements and prepare ahead. Essentially, it is used to monitor their income or costs that

must be estimated and may be included within financial accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4. Advantage & disadvantage of various planning tools which used for budgetary control

Budget: It is a budgetary forecast that is prepared for a particular time span that includes

the sales value, income, or capital needed for product development. It contains a short

description of specific perspectives, including the costs of manufacturing products. EECL creates

a schedule for future operations, which assists managers in categorizing their budgets based on

events.

Budgetary control: It is a mechanism for monitoring an applicant's finances or results,

and it also assists the planner in developing a budget based on previous estimates. Most budgets

in organizations are developed with the aid of previous knowledge, which produces inaccurate

outcomes. There are a variety of strategy resources ready to help the management of EECL in

doing well or meeting corporate priorities and objectives (Gerdin, 2020). Any preparation

method has some advantages and disadvantages that are mentioned further below:

Different types of planning tools:

Cash budget: This budget includes the anticipated cash receipts and disbursements for the

fiscal year. The budget includes the input and output of funds, and these transactions have

included money collected from different operations, the cost of each operation, and indeed the

debt sum that must be paid. EECL need to use a cash fund for financial oversight, where they

oversee all operating operations (Gonzalez and Mendoza, 2021). This budget has some benefits

and drawbacks that are listed underneath:

Advantage: This budget avoids borrowing, allowing the planner to provide reliable

results on cash inflows and outflows from operating operations. It assists the manager in

being grounded in practice, as actual cost data aids in the development of potential

strategies.

Disadvantage: One drawback is that This provide inflexible judgment and mandated

adequate opportunity to build budget so that each really have to examine since it only

have included the money activities. This budget stipulate the restriction that also going to

prevent career pathway.

P4. Advantage & disadvantage of various planning tools which used for budgetary control

Budget: It is a budgetary forecast that is prepared for a particular time span that includes

the sales value, income, or capital needed for product development. It contains a short

description of specific perspectives, including the costs of manufacturing products. EECL creates

a schedule for future operations, which assists managers in categorizing their budgets based on

events.

Budgetary control: It is a mechanism for monitoring an applicant's finances or results,

and it also assists the planner in developing a budget based on previous estimates. Most budgets

in organizations are developed with the aid of previous knowledge, which produces inaccurate

outcomes. There are a variety of strategy resources ready to help the management of EECL in

doing well or meeting corporate priorities and objectives (Gerdin, 2020). Any preparation

method has some advantages and disadvantages that are mentioned further below:

Different types of planning tools:

Cash budget: This budget includes the anticipated cash receipts and disbursements for the

fiscal year. The budget includes the input and output of funds, and these transactions have

included money collected from different operations, the cost of each operation, and indeed the

debt sum that must be paid. EECL need to use a cash fund for financial oversight, where they

oversee all operating operations (Gonzalez and Mendoza, 2021). This budget has some benefits

and drawbacks that are listed underneath:

Advantage: This budget avoids borrowing, allowing the planner to provide reliable

results on cash inflows and outflows from operating operations. It assists the manager in

being grounded in practice, as actual cost data aids in the development of potential

strategies.

Disadvantage: One drawback is that This provide inflexible judgment and mandated

adequate opportunity to build budget so that each really have to examine since it only

have included the money activities. This budget stipulate the restriction that also going to

prevent career pathway.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based budget: This strategy is also used by different organizations for budgetary

management, in which the budgets of each object are justified for each new fiscal year.

Essentially, this expenditure is not dependent on previous projections. It is prepared from the

ground up, with the planner having to predict all of the details from the beginning

(Vangermeersch, 2020). It will take a significant amount of time to plan zero - based budgeting,

but it can be useful for financial management in the sense of EECL any benefits and drawbacks

are addressed elsewhere here:

Advantage: This budget is used to measure the effective assessment of the organizational

bioavailability. It also assists management in developing plans to have accurate

outcomes. It also contributes to increased productivity or efficacy.

Disadvantage: This approach is very time intensive and also expensive, which includes

the calculation along with training time. In addition, managers must check this

expenditure on a daily basis to ensure its efficacy.

Master budget: It is a conglomeration of various organizations in which the management

creates a budget for every one of them and expects them to execute or accomplish their tasks

appropriately. For a more efficient or reliable budget, EECL manager should follow this budget

or attempt to increase operating performance or usefulness. It will be prepared on a quarterly and

annual basis and will necessitate financial preparation and comfortable dealing. This budget still

has some benefits and drawbacks, which are listed underneath:

Advantage: It allows the boss and owner to analyze independent agency budgets that aids

in performance analysis. The budget for all cognitive activities is located in a single

report that the management can easily analyze for future operations.

Disadvantage: The master budget is a time-consuming system because each division

needs time for calculation. Furthermore, it became a very expensive method since it

necessitated substantial amounts of money and resources for expenditure calculation (De

Silva Lokuwaduge and De Silva, 2020).

The above-mentioned planning method is used by EECL's administrator since it provides a

reliable estimate of each item's expense. It assists the supervisor in evaluating the success of each

organization and developing appropriate strategies.

management, in which the budgets of each object are justified for each new fiscal year.

Essentially, this expenditure is not dependent on previous projections. It is prepared from the

ground up, with the planner having to predict all of the details from the beginning

(Vangermeersch, 2020). It will take a significant amount of time to plan zero - based budgeting,

but it can be useful for financial management in the sense of EECL any benefits and drawbacks

are addressed elsewhere here:

Advantage: This budget is used to measure the effective assessment of the organizational

bioavailability. It also assists management in developing plans to have accurate

outcomes. It also contributes to increased productivity or efficacy.

Disadvantage: This approach is very time intensive and also expensive, which includes

the calculation along with training time. In addition, managers must check this

expenditure on a daily basis to ensure its efficacy.

Master budget: It is a conglomeration of various organizations in which the management

creates a budget for every one of them and expects them to execute or accomplish their tasks

appropriately. For a more efficient or reliable budget, EECL manager should follow this budget

or attempt to increase operating performance or usefulness. It will be prepared on a quarterly and

annual basis and will necessitate financial preparation and comfortable dealing. This budget still

has some benefits and drawbacks, which are listed underneath:

Advantage: It allows the boss and owner to analyze independent agency budgets that aids

in performance analysis. The budget for all cognitive activities is located in a single

report that the management can easily analyze for future operations.

Disadvantage: The master budget is a time-consuming system because each division

needs time for calculation. Furthermore, it became a very expensive method since it

necessitated substantial amounts of money and resources for expenditure calculation (De

Silva Lokuwaduge and De Silva, 2020).

The above-mentioned planning method is used by EECL's administrator since it provides a

reliable estimate of each item's expense. It assists the supervisor in evaluating the success of each

organization and developing appropriate strategies.

M3. Evaluate different planning tools which required for forecasting budget

Any organisation employs a financial forecasting method to assist managers in estimating

both expenditures and projected sales. In the framework of EECL, managers use master budgets

to assess individual organization success and analyze the outcomes to ensure that it is able to

attain desired outcomes and priorities under a restricted budget. When any operating operation

exceeds their budgeted number, the company will investigate the cause, and if any segment does

exceedingly well within the budgeted amount, this method would be used in the potential too

though.

TASK 4

P5. Compare how business adapting management accounting system to respond their financial

problems

Financial problem: Almost every company faces this dilemma, in which businesses

struggle due to a shortage of funds. Certain challenges are extremely difficult to solve, although

some of them can be avoided by utilizing an accounting scheme that improves company

operating practices. Managers at EECL are under scrutiny as a result of their organizational

operations, which have an effect on the bank's earnings (Spanò and et.al, 2020). A few issues are

listed elsewhere here:

Excessive spending: Companies experience difficulties as a result of extravagant

spending while making products. That will raise the price of the product, which again

will inevitably raise the cost of the item, lowering prices. This factor has an effect on

efficiency and performance, so managers can take proactive action to address these

issues.

Lack of cash flow: EECL's management needed enough money to cover their monthly

bills. With capital, they are unable to complete their tasks or pay their rent, since they

need adequate funding to do so.

Techniques to solve financial problems:

Key Performance Indicator (KPI): It is a quantitative metric that assists the

organisation in determining how well it achieves its aims and objectives. KPIs are used at

various levels to assess the performance of each stage. High-level KPIs are used to assess general

Any organisation employs a financial forecasting method to assist managers in estimating

both expenditures and projected sales. In the framework of EECL, managers use master budgets

to assess individual organization success and analyze the outcomes to ensure that it is able to

attain desired outcomes and priorities under a restricted budget. When any operating operation

exceeds their budgeted number, the company will investigate the cause, and if any segment does

exceedingly well within the budgeted amount, this method would be used in the potential too

though.

TASK 4

P5. Compare how business adapting management accounting system to respond their financial

problems

Financial problem: Almost every company faces this dilemma, in which businesses

struggle due to a shortage of funds. Certain challenges are extremely difficult to solve, although

some of them can be avoided by utilizing an accounting scheme that improves company

operating practices. Managers at EECL are under scrutiny as a result of their organizational

operations, which have an effect on the bank's earnings (Spanò and et.al, 2020). A few issues are

listed elsewhere here:

Excessive spending: Companies experience difficulties as a result of extravagant

spending while making products. That will raise the price of the product, which again

will inevitably raise the cost of the item, lowering prices. This factor has an effect on

efficiency and performance, so managers can take proactive action to address these

issues.

Lack of cash flow: EECL's management needed enough money to cover their monthly

bills. With capital, they are unable to complete their tasks or pay their rent, since they

need adequate funding to do so.

Techniques to solve financial problems:

Key Performance Indicator (KPI): It is a quantitative metric that assists the

organisation in determining how well it achieves its aims and objectives. KPIs are used at

various levels to assess the performance of each stage. High-level KPIs are used to assess general

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.