Management Accounting System and Its Application for KEF Ltd Report

VerifiedAdded on 2021/02/21

|15

|4294

|24

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their application within a manufacturing context, specifically referencing KEF Ltd. It explores various management accounting systems like inventory management, price optimization, and job costing, highlighting their importance in strategic decision-making. The report details different reporting methods, including budgeting and cost accounting reports. It includes practical cost analysis using absorption and marginal costing techniques, demonstrating the computation of production costs, cost of sales, and profit and loss statements. Furthermore, the report examines the advantages and disadvantages of planning tools used in budgetary control and discusses how organizations adapt management accounting systems to address financial problems. The report concludes by emphasizing the role of management accounting in providing accurate, reliable, and timely information for managerial personnel.

Management

Accounting System

and its Application

Accounting System

and its Application

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. - Management accounting and essential requirement of various type of management

accounting systems:................................................................................................................3

P2. - Different kind of methods used in respect of management accounting reporting:........5

TASK 2............................................................................................................................................6

P3. - Computation of costs applying appropriate cost analysis techniques to formulate income

statement applying absorption and marginal costing:............................................................6

TASK 3............................................................................................................................................9

P4. - Disadvantages and advantages of different planning tools applied in budgetary control:. 9

TASK 4..........................................................................................................................................11

P5. - In which manner organisation are adapting management accounting systems to respond

to different financial problems:............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. - Management accounting and essential requirement of various type of management

accounting systems:................................................................................................................3

P2. - Different kind of methods used in respect of management accounting reporting:........5

TASK 2............................................................................................................................................6

P3. - Computation of costs applying appropriate cost analysis techniques to formulate income

statement applying absorption and marginal costing:............................................................6

TASK 3............................................................................................................................................9

P4. - Disadvantages and advantages of different planning tools applied in budgetary control:. 9

TASK 4..........................................................................................................................................11

P5. - In which manner organisation are adapting management accounting systems to respond

to different financial problems:............................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is popular field of accounting which deals with preparation of

various accounts and reports and main motive is to provide accurate, reliable and timely

information for managerial personnels to take major strategic decisions. Planning tool and

methods help managers to identify and solve financial and monetary problems on early basis

(Stechemesser and Guenther, 2012). This report mainly try to emphasises on various aspects of

management accounting system and essential requirement of various management accounting

systems, methods of management accounting systems and planning tool along with benefits and

disadvantages of different planning tools in the context of KEF Ltd, a medium sized

manufacturing company. This report also contains practical calculation of costs using absorption

and marginal costing, and manner in which management accounting system assist in responding

to financial problems.

TASK 1

P1. - Management accounting and essential requirement of various type of management

accounting systems:

Management Accounting denotes to a organised and managed process of producing

relevant financial information and reports for managerial use. Moreover, top management by

applying such report and information formulates effective strategies in order to attain

organisation's targets and objectives. The management accounting considers different types of

accounting system like cost accounting system. Price optimisation system and inventory

management system. Information generated by management accounting systems are key

financial and accounting data that is directly or indirectly provide assistance to managerial

personnels in strategic planning and actions (Cazier and et.al., 2015). As KEF Ltd is

manufacturing company so different production managers provide relevant information

generated through systems of management accounting to top management for business decision-

making. Following are the main management accounting systems, as follows:

Inventory management system: It is a system which emphasises on managing and

maintaining inventories within a business organisation to optimise the cost of inventories.

This system is used by management to enhance accountability and efficiency in

management of inventories (Burritt and Tingey-Holyoak, 2012). As KEF Ltd is a

Management accounting is popular field of accounting which deals with preparation of

various accounts and reports and main motive is to provide accurate, reliable and timely

information for managerial personnels to take major strategic decisions. Planning tool and

methods help managers to identify and solve financial and monetary problems on early basis

(Stechemesser and Guenther, 2012). This report mainly try to emphasises on various aspects of

management accounting system and essential requirement of various management accounting

systems, methods of management accounting systems and planning tool along with benefits and

disadvantages of different planning tools in the context of KEF Ltd, a medium sized

manufacturing company. This report also contains practical calculation of costs using absorption

and marginal costing, and manner in which management accounting system assist in responding

to financial problems.

TASK 1

P1. - Management accounting and essential requirement of various type of management

accounting systems:

Management Accounting denotes to a organised and managed process of producing

relevant financial information and reports for managerial use. Moreover, top management by

applying such report and information formulates effective strategies in order to attain

organisation's targets and objectives. The management accounting considers different types of

accounting system like cost accounting system. Price optimisation system and inventory

management system. Information generated by management accounting systems are key

financial and accounting data that is directly or indirectly provide assistance to managerial

personnels in strategic planning and actions (Cazier and et.al., 2015). As KEF Ltd is

manufacturing company so different production managers provide relevant information

generated through systems of management accounting to top management for business decision-

making. Following are the main management accounting systems, as follows:

Inventory management system: It is a system which emphasises on managing and

maintaining inventories within a business organisation to optimise the cost of inventories.

This system is used by management to enhance accountability and efficiency in

management of inventories (Burritt and Tingey-Holyoak, 2012). As KEF Ltd is a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manufacturing company, so here inventories includes WIP, raw materials, processed

goods, spare tools and finished goods. In order to manage all kind of inventories within

company heads of different production and manufacturing depart applying inventory

management system. inventory management system help to maintain the records of

inventory that solve financial problems. If KEF Ltd uses inventory accounting system

that can get the information of products and services and what need to be place order for

purchasing the goods. Under this system managers put their efforts identification,

classification, recording and monitoring of inventories to assess the actual cost

inventories in production and manufacturing activities. This system help managers to

asses the excessive inventories cost and minimise such cost to increaser probability

margin.

Price Optimisation System: It is a systematic set of activities related to determining

most considerable and appropriate price of product and services. In this system of

management accounting a unique relationship between price of product or service and

demand is analysed by business organisation to set a effective price at which demand of

product is high. Price optimisation system help to utilize the prices of products and

services that leads to maintain the profits. Production and division managers in KEF Ltd

analyse the response of customer and market by setting different price of products during

a specific period of time. Here main motive is to reduce price while retaining same profit

margin.

Job Costing System: This system is adopted by organisation which produce product on

specific customer order. Under this system each specific product is considered as job. In

this system is cost is assigned or allocated to each particular task or job. In KEF Ltd this

system is used for products which are totally different from production line. Manager first

classifies such product as task or job, thereafter they allocate different cost to this

participate task or job. Main purpose or objectives of this system is to increase

accountability within company (Marr and Gray, 2012). Following are the key information

that is required for job costing system:

Direct Material: In KEF Ltd, managers first classifies the cost of direct material involved in

production of different products as its is required to allocate cost of direct material to particular

task or job.

goods, spare tools and finished goods. In order to manage all kind of inventories within

company heads of different production and manufacturing depart applying inventory

management system. inventory management system help to maintain the records of

inventory that solve financial problems. If KEF Ltd uses inventory accounting system

that can get the information of products and services and what need to be place order for

purchasing the goods. Under this system managers put their efforts identification,

classification, recording and monitoring of inventories to assess the actual cost

inventories in production and manufacturing activities. This system help managers to

asses the excessive inventories cost and minimise such cost to increaser probability

margin.

Price Optimisation System: It is a systematic set of activities related to determining

most considerable and appropriate price of product and services. In this system of

management accounting a unique relationship between price of product or service and

demand is analysed by business organisation to set a effective price at which demand of

product is high. Price optimisation system help to utilize the prices of products and

services that leads to maintain the profits. Production and division managers in KEF Ltd

analyse the response of customer and market by setting different price of products during

a specific period of time. Here main motive is to reduce price while retaining same profit

margin.

Job Costing System: This system is adopted by organisation which produce product on

specific customer order. Under this system each specific product is considered as job. In

this system is cost is assigned or allocated to each particular task or job. In KEF Ltd this

system is used for products which are totally different from production line. Manager first

classifies such product as task or job, thereafter they allocate different cost to this

participate task or job. Main purpose or objectives of this system is to increase

accountability within company (Marr and Gray, 2012). Following are the key information

that is required for job costing system:

Direct Material: In KEF Ltd, managers first classifies the cost of direct material involved in

production of different products as its is required to allocate cost of direct material to particular

task or job.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct Labour: This is also significant information that is used by production managers to asses

the total direct labour cost associated with particular job or task.

Cost Accounting System: This system mainly focus on profitability analysis by

estimating and projecting cost of particular product or services. This system includes

activities like recording , summarizing, classifying and analysing various costs and

expenses related to production and manufacturing to control cost. Under this system

managers put their efforts towards controlling costs in order to maximise profitability. In

KEF Ltd cost accountants and production managers with help of this system try to

optimise cost of products to increase their profit margin. Here main objectives is effective

management and monitoring of costs to achieve organisation objectives and goals. These

system help to solve financial problem within organisation that also help to maintain the

profitability.

P2. - Different kind of methods used in respect of management accounting reporting:

Reporting is systematic process under which information is transferred from lower or

middle managers to top management through various formal reports. In Management accounting

reporting various reports are prepared by managers to report vital matter to top management in

order to assist them in managerial decision making process. By using these reports management

frames new strategies and plan to attain predetermined objectives. In KEF Ltd, following

management accounting reporting are used by managerial personnels, as follows:

Budgeting or Budget Reports: Budgeting refers to making projection of cost and

expenses for assessment of future performance of business organisation. Various budget

reports are prepared by managers as per organisation's specific requirement. Budget

report help top managers to analyse the various financial aspects and performance

(Mook, 2013). In KEF Ltd, various budget reports are prepared by managers like sales

budget, purchase budget, cash budget etc. In Company management use this report to

identify and asses the issues and problems related to manufacturing of products, which

ultimately leads to increase in productivity. This process help to save the cost of

organisation and increase the productivity and profitability by using this system.

Cost accounting reports- These reports provide a detailed assessment of cost of various

products produced and manufactured by business organisation. This report also provides

the total direct labour cost associated with particular job or task.

Cost Accounting System: This system mainly focus on profitability analysis by

estimating and projecting cost of particular product or services. This system includes

activities like recording , summarizing, classifying and analysing various costs and

expenses related to production and manufacturing to control cost. Under this system

managers put their efforts towards controlling costs in order to maximise profitability. In

KEF Ltd cost accountants and production managers with help of this system try to

optimise cost of products to increase their profit margin. Here main objectives is effective

management and monitoring of costs to achieve organisation objectives and goals. These

system help to solve financial problem within organisation that also help to maintain the

profitability.

P2. - Different kind of methods used in respect of management accounting reporting:

Reporting is systematic process under which information is transferred from lower or

middle managers to top management through various formal reports. In Management accounting

reporting various reports are prepared by managers to report vital matter to top management in

order to assist them in managerial decision making process. By using these reports management

frames new strategies and plan to attain predetermined objectives. In KEF Ltd, following

management accounting reporting are used by managerial personnels, as follows:

Budgeting or Budget Reports: Budgeting refers to making projection of cost and

expenses for assessment of future performance of business organisation. Various budget

reports are prepared by managers as per organisation's specific requirement. Budget

report help top managers to analyse the various financial aspects and performance

(Mook, 2013). In KEF Ltd, various budget reports are prepared by managers like sales

budget, purchase budget, cash budget etc. In Company management use this report to

identify and asses the issues and problems related to manufacturing of products, which

ultimately leads to increase in productivity. This process help to save the cost of

organisation and increase the productivity and profitability by using this system.

Cost accounting reports- These reports provide a detailed assessment of cost of various

products produced and manufactured by business organisation. This report also provides

information of costs related to different activities and functions. Main motive of this

reporting system is to asses the cost of each product and identification of any

unproductive cost. In KEF Ltd, cost accountant prepare cost reports to provide a setailed

assessment of cost which ultimately used by management and production department to

take decision regarding manufacturing and production. These reports are also used by

management for optimisation of various costs.

Inventory reports- Inventory reports are prepared by business organisation to track the

actual fluctuation in inventories in terms of value and number of item. This report is used

by business organisations to monitor various inventories like raw material, finished

goods, work in progress, spare tools etc (Hoque, Covaleski and Gooneratne, 2013). In

KEF Ltd these reports are prepared by production managers to monitor the movement of

various inventories within business organisation. It also assist management in effective

management of inventories to enhance accountability. In KEF, managers using inventory

report also identifies and eliminates inventory costs like storage costs, inventories

handling costs etc.

TASK 2

P3. - Computation of costs applying appropriate cost analysis techniques to formulate income

statement applying absorption and marginal costing:

(i) Production cost per unit:

Particulars Amount (in £)

Direct Expenses:

Material 12

Labour 20

Other variable production overheads 8

Total fixed production overhead cost =

£120000 (120000/20000) = 6

Use standard volume of 20000 units to absorb

the fixed production overhead cost

Selling price per unit: £60

Absorption Costing = £46/unit

Thus production cost per unit is £ 46.

reporting system is to asses the cost of each product and identification of any

unproductive cost. In KEF Ltd, cost accountant prepare cost reports to provide a setailed

assessment of cost which ultimately used by management and production department to

take decision regarding manufacturing and production. These reports are also used by

management for optimisation of various costs.

Inventory reports- Inventory reports are prepared by business organisation to track the

actual fluctuation in inventories in terms of value and number of item. This report is used

by business organisations to monitor various inventories like raw material, finished

goods, work in progress, spare tools etc (Hoque, Covaleski and Gooneratne, 2013). In

KEF Ltd these reports are prepared by production managers to monitor the movement of

various inventories within business organisation. It also assist management in effective

management of inventories to enhance accountability. In KEF, managers using inventory

report also identifies and eliminates inventory costs like storage costs, inventories

handling costs etc.

TASK 2

P3. - Computation of costs applying appropriate cost analysis techniques to formulate income

statement applying absorption and marginal costing:

(i) Production cost per unit:

Particulars Amount (in £)

Direct Expenses:

Material 12

Labour 20

Other variable production overheads 8

Total fixed production overhead cost =

£120000 (120000/20000) = 6

Use standard volume of 20000 units to absorb

the fixed production overhead cost

Selling price per unit: £60

Absorption Costing = £46/unit

Thus production cost per unit is £ 46.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

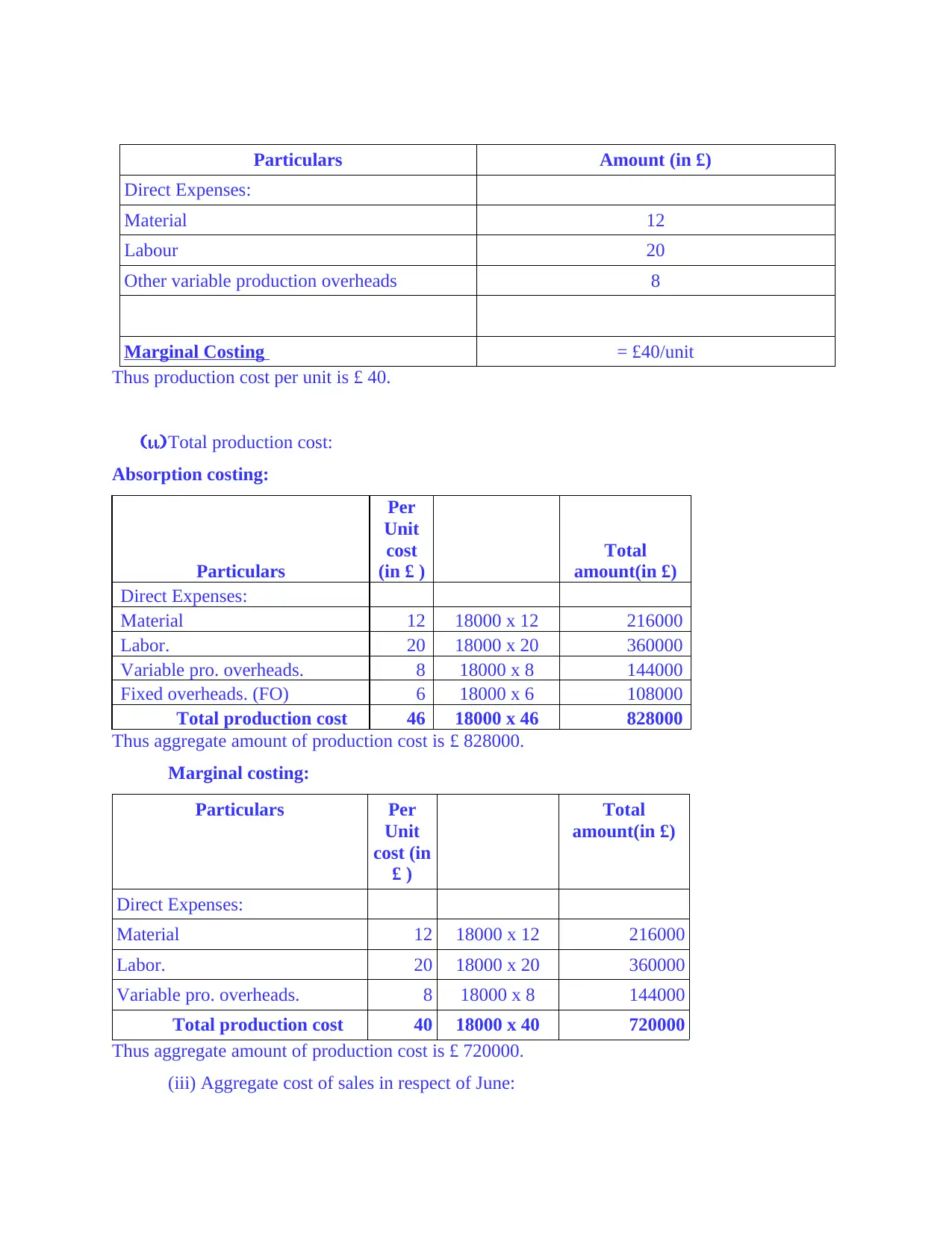

Particulars Amount (in £)

Direct Expenses:

Material 12

Labour 20

Other variable production overheads 8

Marginal Costing = £40/unit

Thus production cost per unit is £ 40.

(ii)Total production cost:

Absorption costing:

Particulars

Per

Unit

cost

(in £ )

Total

amount(in £)

Direct Expenses:

Material 12 18000 x 12 216000

Labor. 20 18000 x 20 360000

Variable pro. overheads. 8 18000 x 8 144000

Fixed overheads. (FO) 6 18000 x 6 108000

Total production cost 46 18000 x 46 828000

Thus aggregate amount of production cost is £ 828000.

Marginal costing:

Particulars Per

Unit

cost (in

£ )

Total

amount(in £)

Direct Expenses:

Material 12 18000 x 12 216000

Labor. 20 18000 x 20 360000

Variable pro. overheads. 8 18000 x 8 144000

Total production cost 40 18000 x 40 720000

Thus aggregate amount of production cost is £ 720000.

(iii) Aggregate cost of sales in respect of June:

Direct Expenses:

Material 12

Labour 20

Other variable production overheads 8

Marginal Costing = £40/unit

Thus production cost per unit is £ 40.

(ii)Total production cost:

Absorption costing:

Particulars

Per

Unit

cost

(in £ )

Total

amount(in £)

Direct Expenses:

Material 12 18000 x 12 216000

Labor. 20 18000 x 20 360000

Variable pro. overheads. 8 18000 x 8 144000

Fixed overheads. (FO) 6 18000 x 6 108000

Total production cost 46 18000 x 46 828000

Thus aggregate amount of production cost is £ 828000.

Marginal costing:

Particulars Per

Unit

cost (in

£ )

Total

amount(in £)

Direct Expenses:

Material 12 18000 x 12 216000

Labor. 20 18000 x 20 360000

Variable pro. overheads. 8 18000 x 8 144000

Total production cost 40 18000 x 40 720000

Thus aggregate amount of production cost is £ 720000.

(iii) Aggregate cost of sales in respect of June:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

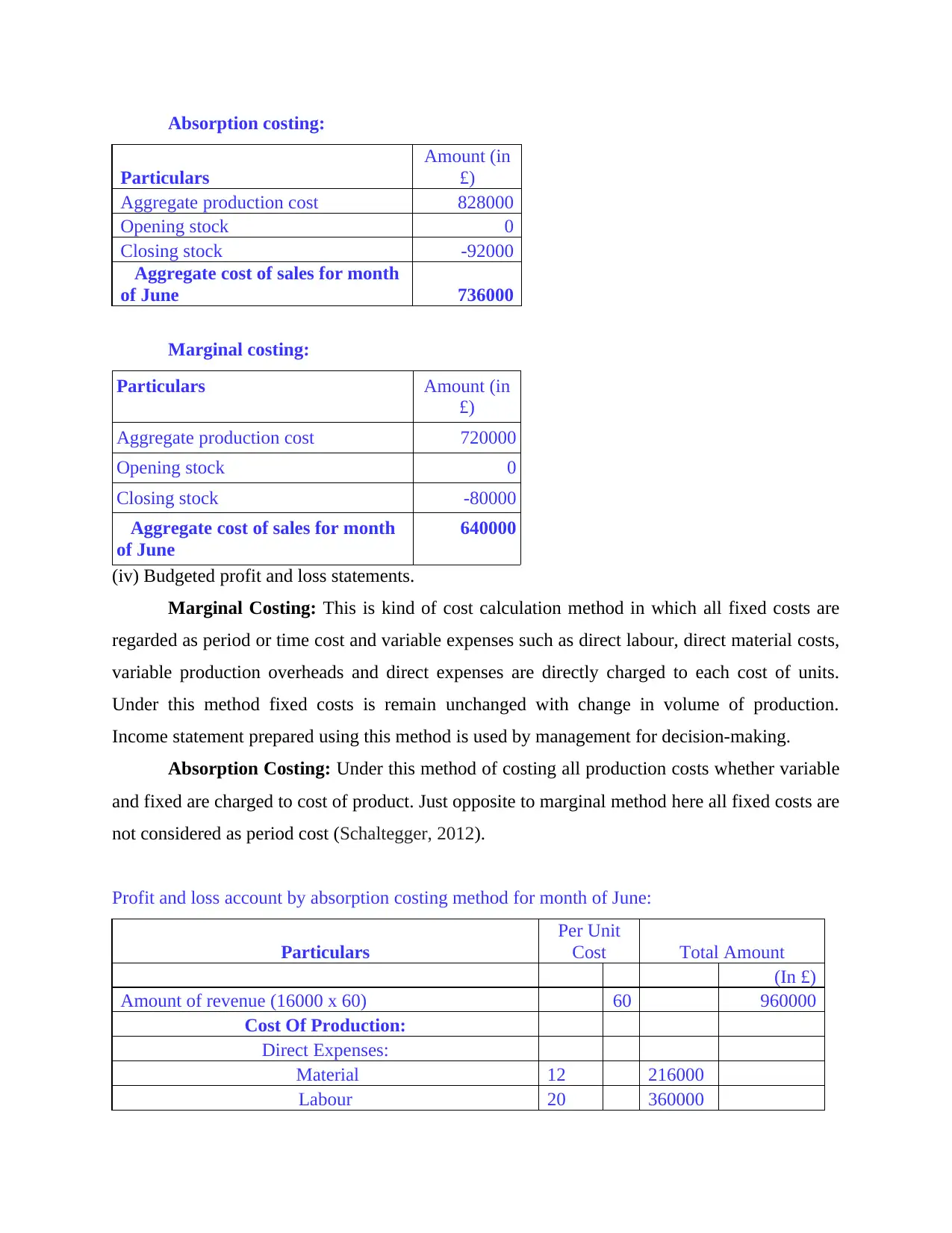

Absorption costing:

Particulars

Amount (in

£)

Aggregate production cost 828000

Opening stock 0

Closing stock -92000

Aggregate cost of sales for month

of June 736000

Marginal costing:

Particulars Amount (in

£)

Aggregate production cost 720000

Opening stock 0

Closing stock -80000

Aggregate cost of sales for month

of June

640000

(iv) Budgeted profit and loss statements.

Marginal Costing: This is kind of cost calculation method in which all fixed costs are

regarded as period or time cost and variable expenses such as direct labour, direct material costs,

variable production overheads and direct expenses are directly charged to each cost of units.

Under this method fixed costs is remain unchanged with change in volume of production.

Income statement prepared using this method is used by management for decision-making.

Absorption Costing: Under this method of costing all production costs whether variable

and fixed are charged to cost of product. Just opposite to marginal method here all fixed costs are

not considered as period cost (Schaltegger, 2012).

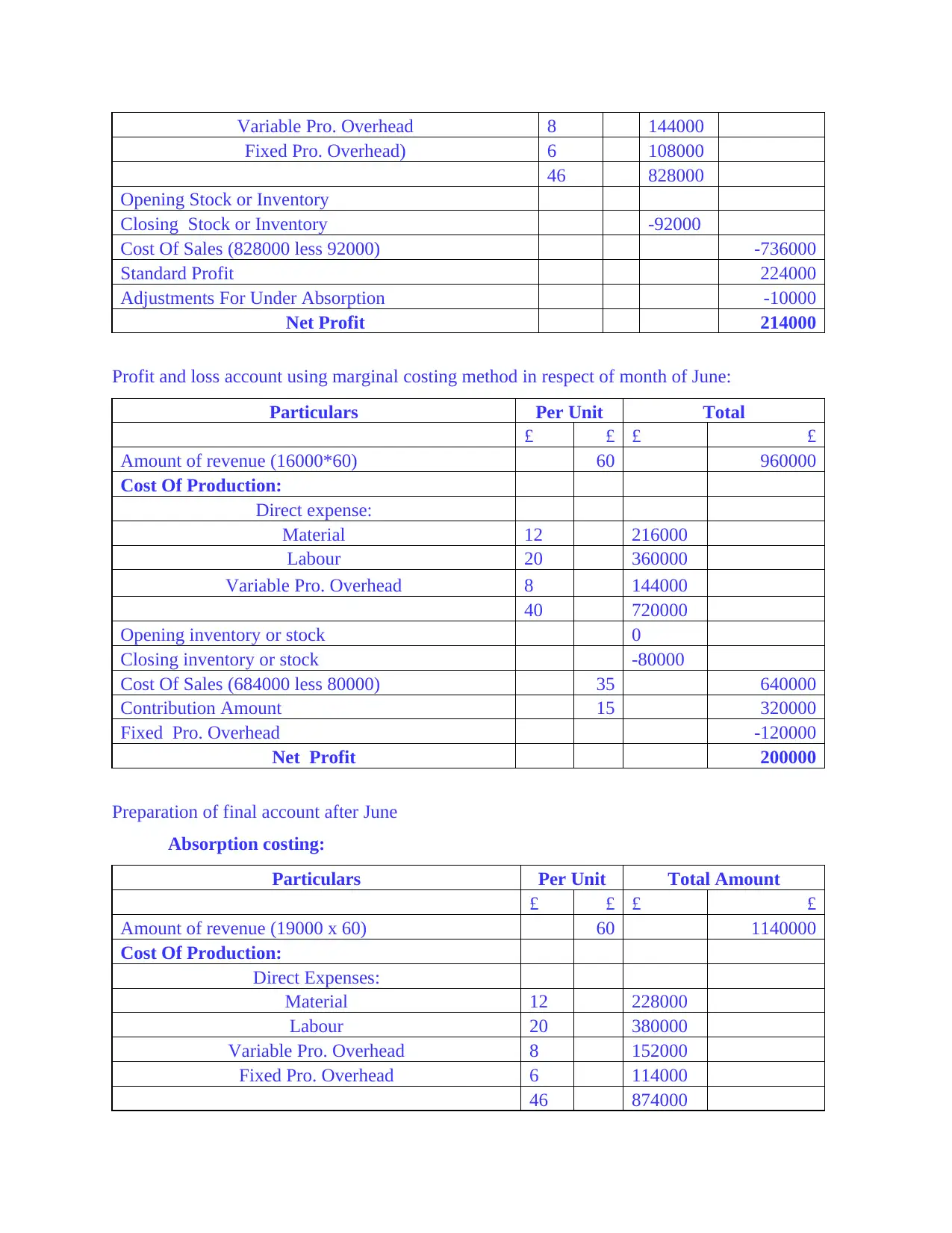

Profit and loss account by absorption costing method for month of June:

Particulars

Per Unit

Cost Total Amount

(In £)

Amount of revenue (16000 x 60) 60 960000

Cost Of Production:

Direct Expenses:

Material 12 216000

Labour 20 360000

Particulars

Amount (in

£)

Aggregate production cost 828000

Opening stock 0

Closing stock -92000

Aggregate cost of sales for month

of June 736000

Marginal costing:

Particulars Amount (in

£)

Aggregate production cost 720000

Opening stock 0

Closing stock -80000

Aggregate cost of sales for month

of June

640000

(iv) Budgeted profit and loss statements.

Marginal Costing: This is kind of cost calculation method in which all fixed costs are

regarded as period or time cost and variable expenses such as direct labour, direct material costs,

variable production overheads and direct expenses are directly charged to each cost of units.

Under this method fixed costs is remain unchanged with change in volume of production.

Income statement prepared using this method is used by management for decision-making.

Absorption Costing: Under this method of costing all production costs whether variable

and fixed are charged to cost of product. Just opposite to marginal method here all fixed costs are

not considered as period cost (Schaltegger, 2012).

Profit and loss account by absorption costing method for month of June:

Particulars

Per Unit

Cost Total Amount

(In £)

Amount of revenue (16000 x 60) 60 960000

Cost Of Production:

Direct Expenses:

Material 12 216000

Labour 20 360000

Variable Pro. Overhead 8 144000

Fixed Pro. Overhead) 6 108000

46 828000

Opening Stock or Inventory

Closing Stock or Inventory -92000

Cost Of Sales (828000 less 92000) -736000

Standard Profit 224000

Adjustments For Under Absorption -10000

Net Profit 214000

Profit and loss account using marginal costing method in respect of month of June:

Particulars Per Unit Total

£ £ £ £

Amount of revenue (16000*60) 60 960000

Cost Of Production:

Direct expense:

Material 12 216000

Labour 20 360000

Variable Pro. Overhead 8 144000

40 720000

Opening inventory or stock 0

Closing inventory or stock -80000

Cost Of Sales (684000 less 80000) 35 640000

Contribution Amount 15 320000

Fixed Pro. Overhead -120000

Net Profit 200000

Preparation of final account after June

Absorption costing:

Particulars Per Unit Total Amount

£ £ £ £

Amount of revenue (19000 x 60) 60 1140000

Cost Of Production:

Direct Expenses:

Material 12 228000

Labour 20 380000

Variable Pro. Overhead 8 152000

Fixed Pro. Overhead 6 114000

46 874000

Fixed Pro. Overhead) 6 108000

46 828000

Opening Stock or Inventory

Closing Stock or Inventory -92000

Cost Of Sales (828000 less 92000) -736000

Standard Profit 224000

Adjustments For Under Absorption -10000

Net Profit 214000

Profit and loss account using marginal costing method in respect of month of June:

Particulars Per Unit Total

£ £ £ £

Amount of revenue (16000*60) 60 960000

Cost Of Production:

Direct expense:

Material 12 216000

Labour 20 360000

Variable Pro. Overhead 8 144000

40 720000

Opening inventory or stock 0

Closing inventory or stock -80000

Cost Of Sales (684000 less 80000) 35 640000

Contribution Amount 15 320000

Fixed Pro. Overhead -120000

Net Profit 200000

Preparation of final account after June

Absorption costing:

Particulars Per Unit Total Amount

£ £ £ £

Amount of revenue (19000 x 60) 60 1140000

Cost Of Production:

Direct Expenses:

Material 12 228000

Labour 20 380000

Variable Pro. Overhead 8 152000

Fixed Pro. Overhead 6 114000

46 874000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

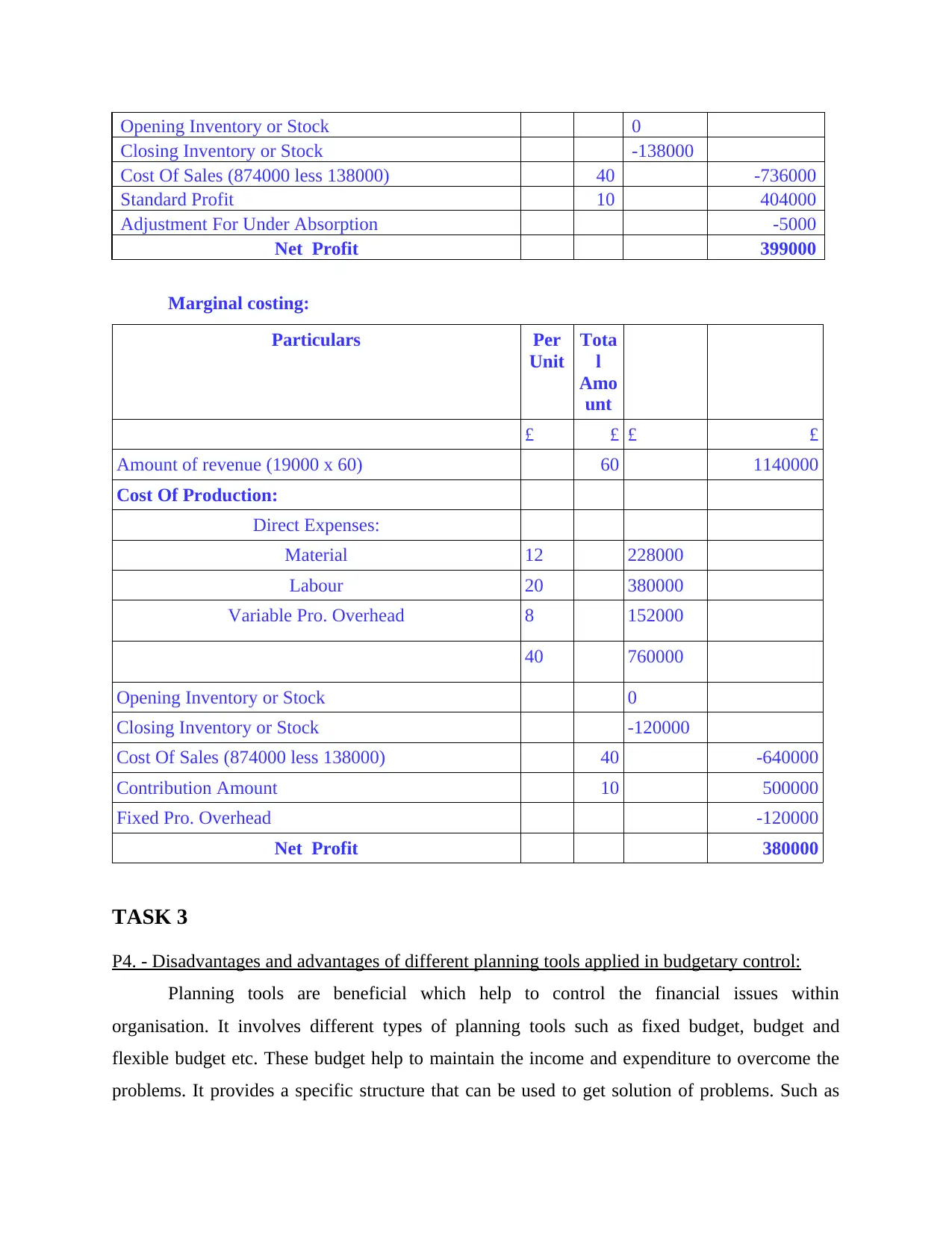

Opening Inventory or Stock 0

Closing Inventory or Stock -138000

Cost Of Sales (874000 less 138000) 40 -736000

Standard Profit 10 404000

Adjustment For Under Absorption -5000

Net Profit 399000

Marginal costing:

Particulars Per

Unit

Tota

l

Amo

unt

£ £ £ £

Amount of revenue (19000 x 60) 60 1140000

Cost Of Production:

Direct Expenses:

Material 12 228000

Labour 20 380000

Variable Pro. Overhead 8 152000

40 760000

Opening Inventory or Stock 0

Closing Inventory or Stock -120000

Cost Of Sales (874000 less 138000) 40 -640000

Contribution Amount 10 500000

Fixed Pro. Overhead -120000

Net Profit 380000

TASK 3

P4. - Disadvantages and advantages of different planning tools applied in budgetary control:

Planning tools are beneficial which help to control the financial issues within

organisation. It involves different types of planning tools such as fixed budget, budget and

flexible budget etc. These budget help to maintain the income and expenditure to overcome the

problems. It provides a specific structure that can be used to get solution of problems. Such as

Closing Inventory or Stock -138000

Cost Of Sales (874000 less 138000) 40 -736000

Standard Profit 10 404000

Adjustment For Under Absorption -5000

Net Profit 399000

Marginal costing:

Particulars Per

Unit

Tota

l

Amo

unt

£ £ £ £

Amount of revenue (19000 x 60) 60 1140000

Cost Of Production:

Direct Expenses:

Material 12 228000

Labour 20 380000

Variable Pro. Overhead 8 152000

40 760000

Opening Inventory or Stock 0

Closing Inventory or Stock -120000

Cost Of Sales (874000 less 138000) 40 -640000

Contribution Amount 10 500000

Fixed Pro. Overhead -120000

Net Profit 380000

TASK 3

P4. - Disadvantages and advantages of different planning tools applied in budgetary control:

Planning tools are beneficial which help to control the financial issues within

organisation. It involves different types of planning tools such as fixed budget, budget and

flexible budget etc. These budget help to maintain the income and expenditure to overcome the

problems. It provides a specific structure that can be used to get solution of problems. Such as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

KEF Ltd are using fixed and flexible budget to solve the financial problems that leads to

organisational success.

Budgetary control- The budgetary control can be defined as a kind of controlling technique

which is related with the management of actual performance. In this, manager of companies

assign the monetary and non monetary goals. On the basis of it, organisations compares the

actual performance (McVay, Kennedy and Fullerton, 2016). So overall, the budgetary control is

useful in managing the financial and non financial performance of organisations. Herein, below

some planning tools of budgetary control are mentioned below:

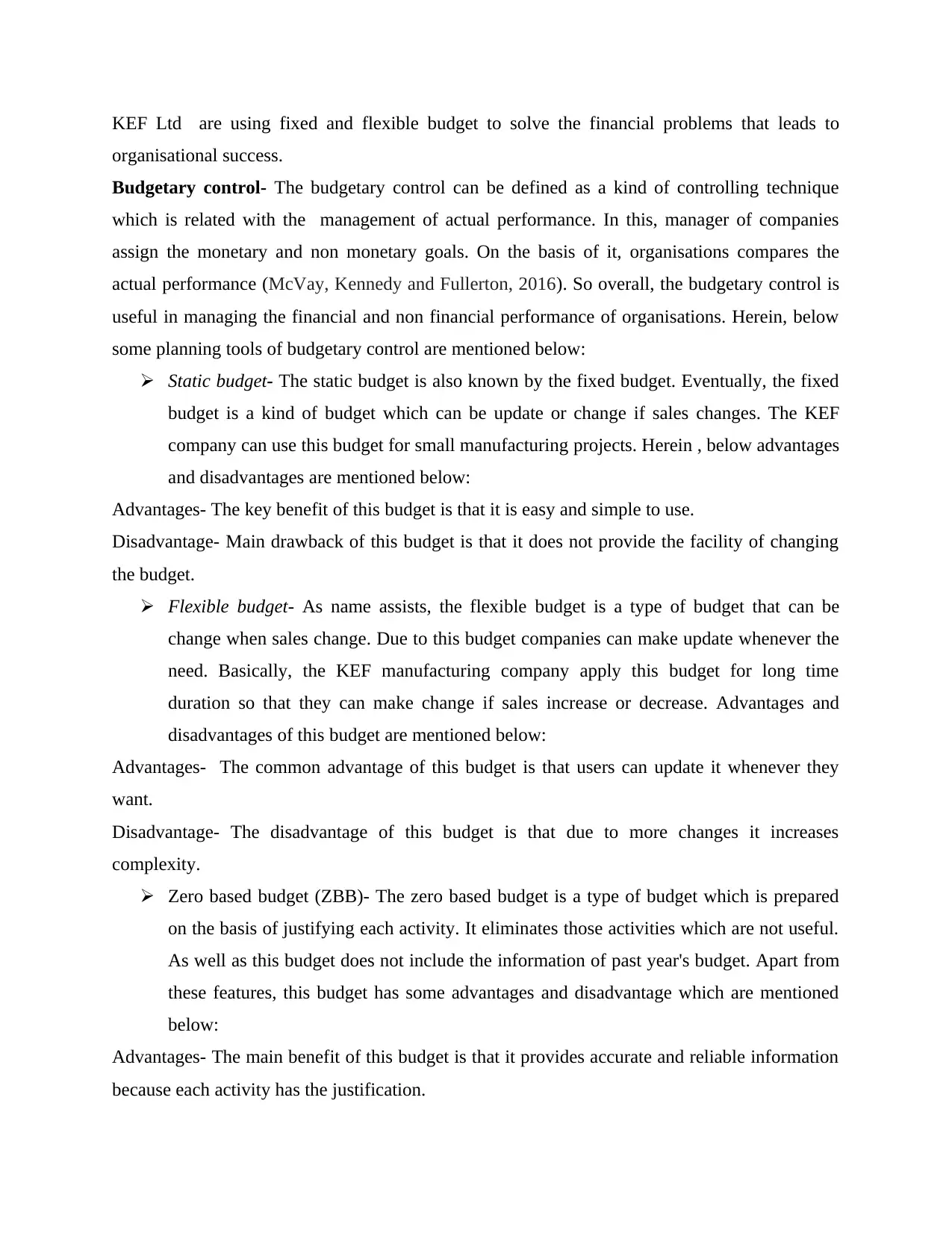

Static budget- The static budget is also known by the fixed budget. Eventually, the fixed

budget is a kind of budget which can be update or change if sales changes. The KEF

company can use this budget for small manufacturing projects. Herein , below advantages

and disadvantages are mentioned below:

Advantages- The key benefit of this budget is that it is easy and simple to use.

Disadvantage- Main drawback of this budget is that it does not provide the facility of changing

the budget.

Flexible budget- As name assists, the flexible budget is a type of budget that can be

change when sales change. Due to this budget companies can make update whenever the

need. Basically, the KEF manufacturing company apply this budget for long time

duration so that they can make change if sales increase or decrease. Advantages and

disadvantages of this budget are mentioned below:

Advantages- The common advantage of this budget is that users can update it whenever they

want.

Disadvantage- The disadvantage of this budget is that due to more changes it increases

complexity.

Zero based budget (ZBB)- The zero based budget is a type of budget which is prepared

on the basis of justifying each activity. It eliminates those activities which are not useful.

As well as this budget does not include the information of past year's budget. Apart from

these features, this budget has some advantages and disadvantage which are mentioned

below:

Advantages- The main benefit of this budget is that it provides accurate and reliable information

because each activity has the justification.

organisational success.

Budgetary control- The budgetary control can be defined as a kind of controlling technique

which is related with the management of actual performance. In this, manager of companies

assign the monetary and non monetary goals. On the basis of it, organisations compares the

actual performance (McVay, Kennedy and Fullerton, 2016). So overall, the budgetary control is

useful in managing the financial and non financial performance of organisations. Herein, below

some planning tools of budgetary control are mentioned below:

Static budget- The static budget is also known by the fixed budget. Eventually, the fixed

budget is a kind of budget which can be update or change if sales changes. The KEF

company can use this budget for small manufacturing projects. Herein , below advantages

and disadvantages are mentioned below:

Advantages- The key benefit of this budget is that it is easy and simple to use.

Disadvantage- Main drawback of this budget is that it does not provide the facility of changing

the budget.

Flexible budget- As name assists, the flexible budget is a type of budget that can be

change when sales change. Due to this budget companies can make update whenever the

need. Basically, the KEF manufacturing company apply this budget for long time

duration so that they can make change if sales increase or decrease. Advantages and

disadvantages of this budget are mentioned below:

Advantages- The common advantage of this budget is that users can update it whenever they

want.

Disadvantage- The disadvantage of this budget is that due to more changes it increases

complexity.

Zero based budget (ZBB)- The zero based budget is a type of budget which is prepared

on the basis of justifying each activity. It eliminates those activities which are not useful.

As well as this budget does not include the information of past year's budget. Apart from

these features, this budget has some advantages and disadvantage which are mentioned

below:

Advantages- The main benefit of this budget is that it provides accurate and reliable information

because each activity has the justification.

Disadvantage- The main disadvantage of the zero based budget is that it takes too much time and

cost. As well as it is not affordable for small companies.

Budget- This is the estimation of income and expenditures for a particular time period.

Under this, manager of company compares their actual result with the budgeted

performance (Myers, 2013). It has some advantages and disadvantages which are as

follows:

Advantage- The main advantage of this budget is that company can measure their actual

performance.

Disadvantage- The drawback of the budget is that estimation of income and expenditure can be

wrong.

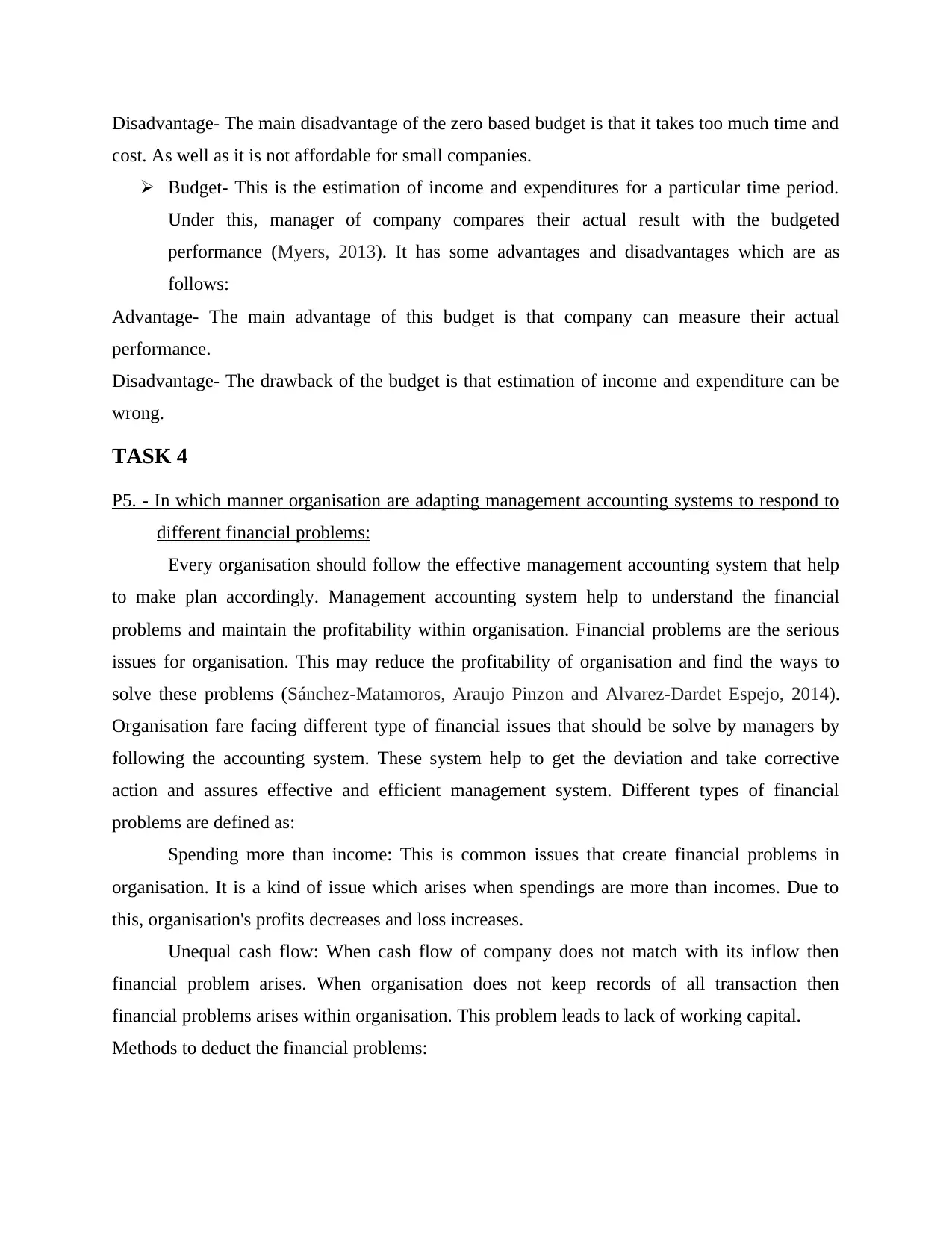

TASK 4

P5. - In which manner organisation are adapting management accounting systems to respond to

different financial problems:

Every organisation should follow the effective management accounting system that help

to make plan accordingly. Management accounting system help to understand the financial

problems and maintain the profitability within organisation. Financial problems are the serious

issues for organisation. This may reduce the profitability of organisation and find the ways to

solve these problems (Sánchez-Matamoros, Araujo Pinzon and Alvarez-Dardet Espejo, 2014).

Organisation fare facing different type of financial issues that should be solve by managers by

following the accounting system. These system help to get the deviation and take corrective

action and assures effective and efficient management system. Different types of financial

problems are defined as:

Spending more than income: This is common issues that create financial problems in

organisation. It is a kind of issue which arises when spendings are more than incomes. Due to

this, organisation's profits decreases and loss increases.

Unequal cash flow: When cash flow of company does not match with its inflow then

financial problem arises. When organisation does not keep records of all transaction then

financial problems arises within organisation. This problem leads to lack of working capital.

Methods to deduct the financial problems:

cost. As well as it is not affordable for small companies.

Budget- This is the estimation of income and expenditures for a particular time period.

Under this, manager of company compares their actual result with the budgeted

performance (Myers, 2013). It has some advantages and disadvantages which are as

follows:

Advantage- The main advantage of this budget is that company can measure their actual

performance.

Disadvantage- The drawback of the budget is that estimation of income and expenditure can be

wrong.

TASK 4

P5. - In which manner organisation are adapting management accounting systems to respond to

different financial problems:

Every organisation should follow the effective management accounting system that help

to make plan accordingly. Management accounting system help to understand the financial

problems and maintain the profitability within organisation. Financial problems are the serious

issues for organisation. This may reduce the profitability of organisation and find the ways to

solve these problems (Sánchez-Matamoros, Araujo Pinzon and Alvarez-Dardet Espejo, 2014).

Organisation fare facing different type of financial issues that should be solve by managers by

following the accounting system. These system help to get the deviation and take corrective

action and assures effective and efficient management system. Different types of financial

problems are defined as:

Spending more than income: This is common issues that create financial problems in

organisation. It is a kind of issue which arises when spendings are more than incomes. Due to

this, organisation's profits decreases and loss increases.

Unequal cash flow: When cash flow of company does not match with its inflow then

financial problem arises. When organisation does not keep records of all transaction then

financial problems arises within organisation. This problem leads to lack of working capital.

Methods to deduct the financial problems:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.