Management Accounting Report: Toshiba's Planning and Analysis

VerifiedAdded on 2023/01/19

|13

|3621

|56

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Toshiba. It explores various planning tools, including cash flow, capital, zero-based, rolling, and operational budgets, outlining their advantages and disadvantages. The report examines how management accountants utilize these tools, such as cost accounting, budgetary control, pricing strategies, and financial statement analysis, to predict costs, revenues, and make informed decisions. It also analyzes the use of Key Performance Indicators (KPIs) in internal processes, highlighting their role in measuring performance. Furthermore, the report concludes with an analysis of the role of management accounting in the Patisserie Valerie scandal, providing a comprehensive understanding of the subject matter.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

ASSESSMENT TWO......................................................................................................................3

Planning tools used in management accounting..........................................................................3

Using different planning tools.....................................................................................................6

Use of Key Performance indicator in internal process................................................................7

Patisserie Valerie scandal............................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

ASSESSMENT TWO......................................................................................................................3

Planning tools used in management accounting..........................................................................3

Using different planning tools.....................................................................................................6

Use of Key Performance indicator in internal process................................................................7

Patisserie Valerie scandal............................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is the internal accounting tool which provides manager with the

different information about the position of the company in the market. Manager used to take this

accounting as the basic to take decision in the organization (Quattrone, 2016). Toshiba is the

Japanese multination company headquartered in Tokyo, Japan. Toshiba was founded in the year

1939 by the founder Tokyo Shibaura Denki K.K. through the merger of Shibaura Seisaku-sho

and Tokyo Denki. This report highlights the purpose of budgetary control and different form of

budgetary control which include advantage and disadvantage of different budgetary control tool

in the organization. After that the report highlights ways in which management accountants use

different planning tools and then the report goes on to explain the way management accountant

used to keep the KPI in company internal process with the help of different advantage and

disadvantage of KPI system. In the end the report highlights analyses role of management

accounting profession with reference to Patisserie Valerie scandal.

MAIN BODY

ASSESSMENT TWO

Planning tools used in management accounting

There are a variety of planning tools that can be used by the managers of the company in

order to ensure that the business i.e. the entire organization runs smoothly and is able to allocate

funds in an appropriate manner. One such planning tool is budget. Budgetary Control can be

defined as the formulation of a financial statement where the managers of the company identify

the sources of fund and its allocation to different expenditures of the company where the exact

amount is specified (Yermack, 2017). Further, tools like budget also helps in regularly evaluating

the financial performance of the company and therefore, it gets easier for managerial accountants

to track the performance of the organization and compare it with their past performance or the

competitor’s performance. At Toshiba, some major types of budgets that assist in financial

planning of an organization are:

Cash Flow Budget: Cash Flow Budget can be defined as that budget that is used to prepare to

ascertain all those sources through which there is inflow of cash and determine the expenditure

modes i.e. the venue at which there is expenditure of funds in the form of cash. They identify all

those sources and then allocate and estimate the funds which can be generated and the probable

amount of expenditure that can be incurred. There are various advantages as well as

Management accounting is the internal accounting tool which provides manager with the

different information about the position of the company in the market. Manager used to take this

accounting as the basic to take decision in the organization (Quattrone, 2016). Toshiba is the

Japanese multination company headquartered in Tokyo, Japan. Toshiba was founded in the year

1939 by the founder Tokyo Shibaura Denki K.K. through the merger of Shibaura Seisaku-sho

and Tokyo Denki. This report highlights the purpose of budgetary control and different form of

budgetary control which include advantage and disadvantage of different budgetary control tool

in the organization. After that the report highlights ways in which management accountants use

different planning tools and then the report goes on to explain the way management accountant

used to keep the KPI in company internal process with the help of different advantage and

disadvantage of KPI system. In the end the report highlights analyses role of management

accounting profession with reference to Patisserie Valerie scandal.

MAIN BODY

ASSESSMENT TWO

Planning tools used in management accounting

There are a variety of planning tools that can be used by the managers of the company in

order to ensure that the business i.e. the entire organization runs smoothly and is able to allocate

funds in an appropriate manner. One such planning tool is budget. Budgetary Control can be

defined as the formulation of a financial statement where the managers of the company identify

the sources of fund and its allocation to different expenditures of the company where the exact

amount is specified (Yermack, 2017). Further, tools like budget also helps in regularly evaluating

the financial performance of the company and therefore, it gets easier for managerial accountants

to track the performance of the organization and compare it with their past performance or the

competitor’s performance. At Toshiba, some major types of budgets that assist in financial

planning of an organization are:

Cash Flow Budget: Cash Flow Budget can be defined as that budget that is used to prepare to

ascertain all those sources through which there is inflow of cash and determine the expenditure

modes i.e. the venue at which there is expenditure of funds in the form of cash. They identify all

those sources and then allocate and estimate the funds which can be generated and the probable

amount of expenditure that can be incurred. There are various advantages as well as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

disadvantages of the preparation of cash budget and therefore the mangers should take this into

account before implementing it (Zietlow and et.al., 2018).

Advantages Disadvantages

When the funds are allocated in an

appropriate manner, it gets easier to ascertain

the financial position and therefore control

any unnecessary expenditure that might be

incurred otherwise. It also helps in

determining the liquidity of the company and

therefore ascertains the financial position of

the company easily ensuring that company

does not go into debts.

However the disadvantages of the preparation

of cash budgets can be categorized that

preparation of these such budgets is an

extremely lengthy and complicated process

and therefore, it might get difficult for the

managers to identify every single source and

then included in the preparation of budget is

an extremely tedious process.

Capital Budget: Capital Budget is another type of budget categorised as the one which accounts

for these assets that are usually long term in nature and cannot be reversed. It needs to be taken

for long term and therefore, the managers of the company need to formulate this type of budget

extremely carefully because it is not easy to incorporate changes in the budget if necessary,

easily (Kaplan and Atkinson, 2015). Although, it is of extreme assistance to the managers

intending to implement a long term project, yet there are various disadvantages as well

associated to it.

Advantages Disadvantages

Capital budget involves selection of the

various avenues through which funds can be

raised and therefore it helps in correct

estimation of the cost required an arranging

funds accordingly so that costs can be

predetermined and therefore it gets easier to

arrange funds beforehand so that

underutilisation or overutilization can be

avoided and the entire project can be

completed on time.

Once this budget has be formulated, it is not

easy to deviate from this budget and therefore,

the entire process needs to be repeated which

is an extremely tedious task. In order to

complete this process of budget formulation,

an extensive study needs to be taken and

therefore, this is an extremely time consuming

process.

account before implementing it (Zietlow and et.al., 2018).

Advantages Disadvantages

When the funds are allocated in an

appropriate manner, it gets easier to ascertain

the financial position and therefore control

any unnecessary expenditure that might be

incurred otherwise. It also helps in

determining the liquidity of the company and

therefore ascertains the financial position of

the company easily ensuring that company

does not go into debts.

However the disadvantages of the preparation

of cash budgets can be categorized that

preparation of these such budgets is an

extremely lengthy and complicated process

and therefore, it might get difficult for the

managers to identify every single source and

then included in the preparation of budget is

an extremely tedious process.

Capital Budget: Capital Budget is another type of budget categorised as the one which accounts

for these assets that are usually long term in nature and cannot be reversed. It needs to be taken

for long term and therefore, the managers of the company need to formulate this type of budget

extremely carefully because it is not easy to incorporate changes in the budget if necessary,

easily (Kaplan and Atkinson, 2015). Although, it is of extreme assistance to the managers

intending to implement a long term project, yet there are various disadvantages as well

associated to it.

Advantages Disadvantages

Capital budget involves selection of the

various avenues through which funds can be

raised and therefore it helps in correct

estimation of the cost required an arranging

funds accordingly so that costs can be

predetermined and therefore it gets easier to

arrange funds beforehand so that

underutilisation or overutilization can be

avoided and the entire project can be

completed on time.

Once this budget has be formulated, it is not

easy to deviate from this budget and therefore,

the entire process needs to be repeated which

is an extremely tedious task. In order to

complete this process of budget formulation,

an extensive study needs to be taken and

therefore, this is an extremely time consuming

process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

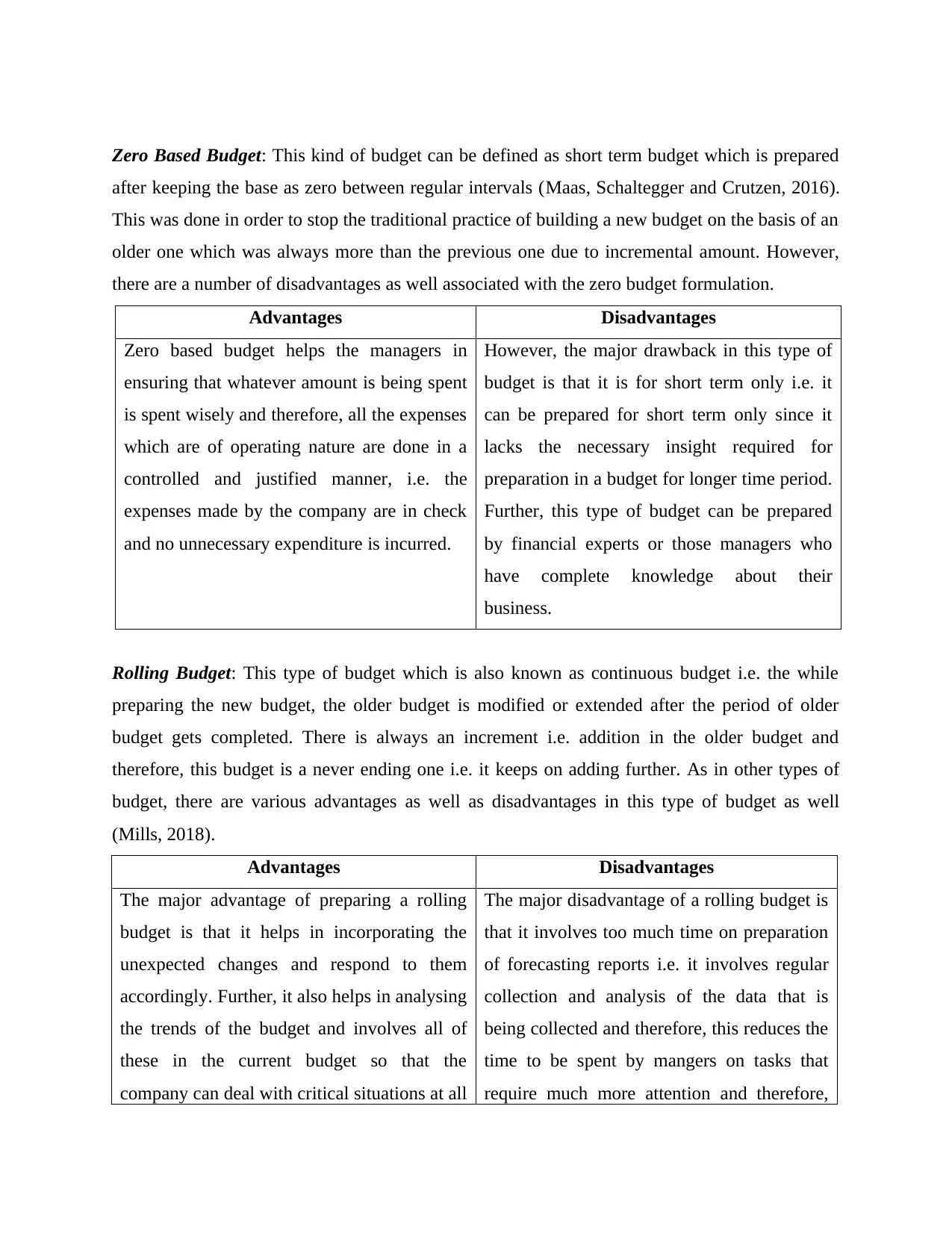

Zero Based Budget: This kind of budget can be defined as short term budget which is prepared

after keeping the base as zero between regular intervals (Maas, Schaltegger and Crutzen, 2016).

This was done in order to stop the traditional practice of building a new budget on the basis of an

older one which was always more than the previous one due to incremental amount. However,

there are a number of disadvantages as well associated with the zero budget formulation.

Advantages Disadvantages

Zero based budget helps the managers in

ensuring that whatever amount is being spent

is spent wisely and therefore, all the expenses

which are of operating nature are done in a

controlled and justified manner, i.e. the

expenses made by the company are in check

and no unnecessary expenditure is incurred.

However, the major drawback in this type of

budget is that it is for short term only i.e. it

can be prepared for short term only since it

lacks the necessary insight required for

preparation in a budget for longer time period.

Further, this type of budget can be prepared

by financial experts or those managers who

have complete knowledge about their

business.

Rolling Budget: This type of budget which is also known as continuous budget i.e. the while

preparing the new budget, the older budget is modified or extended after the period of older

budget gets completed. There is always an increment i.e. addition in the older budget and

therefore, this budget is a never ending one i.e. it keeps on adding further. As in other types of

budget, there are various advantages as well as disadvantages in this type of budget as well

(Mills, 2018).

Advantages Disadvantages

The major advantage of preparing a rolling

budget is that it helps in incorporating the

unexpected changes and respond to them

accordingly. Further, it also helps in analysing

the trends of the budget and involves all of

these in the current budget so that the

company can deal with critical situations at all

The major disadvantage of a rolling budget is

that it involves too much time on preparation

of forecasting reports i.e. it involves regular

collection and analysis of the data that is

being collected and therefore, this reduces the

time to be spent by mangers on tasks that

require much more attention and therefore,

after keeping the base as zero between regular intervals (Maas, Schaltegger and Crutzen, 2016).

This was done in order to stop the traditional practice of building a new budget on the basis of an

older one which was always more than the previous one due to incremental amount. However,

there are a number of disadvantages as well associated with the zero budget formulation.

Advantages Disadvantages

Zero based budget helps the managers in

ensuring that whatever amount is being spent

is spent wisely and therefore, all the expenses

which are of operating nature are done in a

controlled and justified manner, i.e. the

expenses made by the company are in check

and no unnecessary expenditure is incurred.

However, the major drawback in this type of

budget is that it is for short term only i.e. it

can be prepared for short term only since it

lacks the necessary insight required for

preparation in a budget for longer time period.

Further, this type of budget can be prepared

by financial experts or those managers who

have complete knowledge about their

business.

Rolling Budget: This type of budget which is also known as continuous budget i.e. the while

preparing the new budget, the older budget is modified or extended after the period of older

budget gets completed. There is always an increment i.e. addition in the older budget and

therefore, this budget is a never ending one i.e. it keeps on adding further. As in other types of

budget, there are various advantages as well as disadvantages in this type of budget as well

(Mills, 2018).

Advantages Disadvantages

The major advantage of preparing a rolling

budget is that it helps in incorporating the

unexpected changes and respond to them

accordingly. Further, it also helps in analysing

the trends of the budget and involves all of

these in the current budget so that the

company can deal with critical situations at all

The major disadvantage of a rolling budget is

that it involves too much time on preparation

of forecasting reports i.e. it involves regular

collection and analysis of the data that is

being collected and therefore, this reduces the

time to be spent by mangers on tasks that

require much more attention and therefore,

times. this budget is resented by managers.

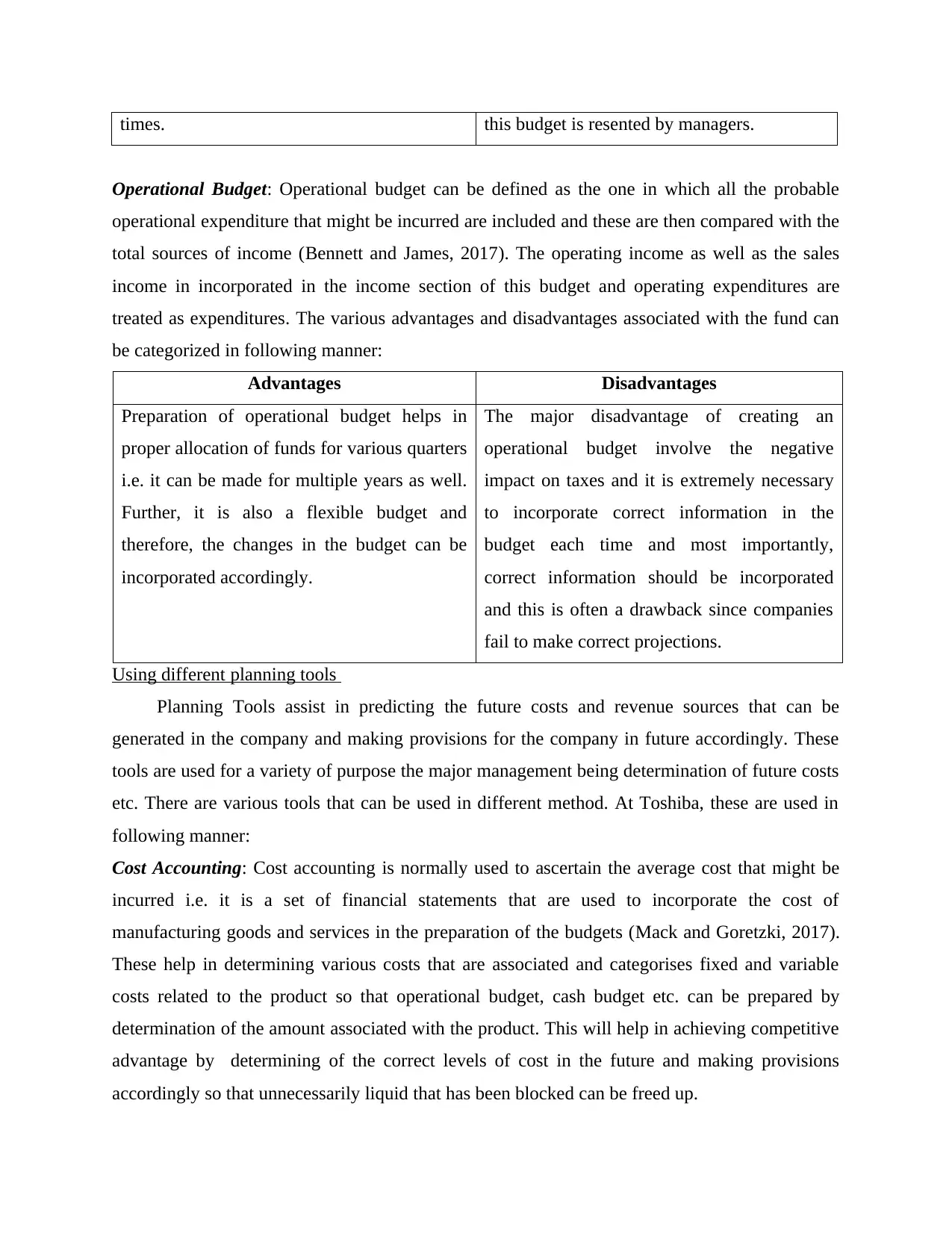

Operational Budget: Operational budget can be defined as the one in which all the probable

operational expenditure that might be incurred are included and these are then compared with the

total sources of income (Bennett and James, 2017). The operating income as well as the sales

income in incorporated in the income section of this budget and operating expenditures are

treated as expenditures. The various advantages and disadvantages associated with the fund can

be categorized in following manner:

Advantages Disadvantages

Preparation of operational budget helps in

proper allocation of funds for various quarters

i.e. it can be made for multiple years as well.

Further, it is also a flexible budget and

therefore, the changes in the budget can be

incorporated accordingly.

The major disadvantage of creating an

operational budget involve the negative

impact on taxes and it is extremely necessary

to incorporate correct information in the

budget each time and most importantly,

correct information should be incorporated

and this is often a drawback since companies

fail to make correct projections.

Using different planning tools

Planning Tools assist in predicting the future costs and revenue sources that can be

generated in the company and making provisions for the company in future accordingly. These

tools are used for a variety of purpose the major management being determination of future costs

etc. There are various tools that can be used in different method. At Toshiba, these are used in

following manner:

Cost Accounting: Cost accounting is normally used to ascertain the average cost that might be

incurred i.e. it is a set of financial statements that are used to incorporate the cost of

manufacturing goods and services in the preparation of the budgets (Mack and Goretzki, 2017).

These help in determining various costs that are associated and categorises fixed and variable

costs related to the product so that operational budget, cash budget etc. can be prepared by

determination of the amount associated with the product. This will help in achieving competitive

advantage by determining of the correct levels of cost in the future and making provisions

accordingly so that unnecessarily liquid that has been blocked can be freed up.

Operational Budget: Operational budget can be defined as the one in which all the probable

operational expenditure that might be incurred are included and these are then compared with the

total sources of income (Bennett and James, 2017). The operating income as well as the sales

income in incorporated in the income section of this budget and operating expenditures are

treated as expenditures. The various advantages and disadvantages associated with the fund can

be categorized in following manner:

Advantages Disadvantages

Preparation of operational budget helps in

proper allocation of funds for various quarters

i.e. it can be made for multiple years as well.

Further, it is also a flexible budget and

therefore, the changes in the budget can be

incorporated accordingly.

The major disadvantage of creating an

operational budget involve the negative

impact on taxes and it is extremely necessary

to incorporate correct information in the

budget each time and most importantly,

correct information should be incorporated

and this is often a drawback since companies

fail to make correct projections.

Using different planning tools

Planning Tools assist in predicting the future costs and revenue sources that can be

generated in the company and making provisions for the company in future accordingly. These

tools are used for a variety of purpose the major management being determination of future costs

etc. There are various tools that can be used in different method. At Toshiba, these are used in

following manner:

Cost Accounting: Cost accounting is normally used to ascertain the average cost that might be

incurred i.e. it is a set of financial statements that are used to incorporate the cost of

manufacturing goods and services in the preparation of the budgets (Mack and Goretzki, 2017).

These help in determining various costs that are associated and categorises fixed and variable

costs related to the product so that operational budget, cash budget etc. can be prepared by

determination of the amount associated with the product. This will help in achieving competitive

advantage by determining of the correct levels of cost in the future and making provisions

accordingly so that unnecessarily liquid that has been blocked can be freed up.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

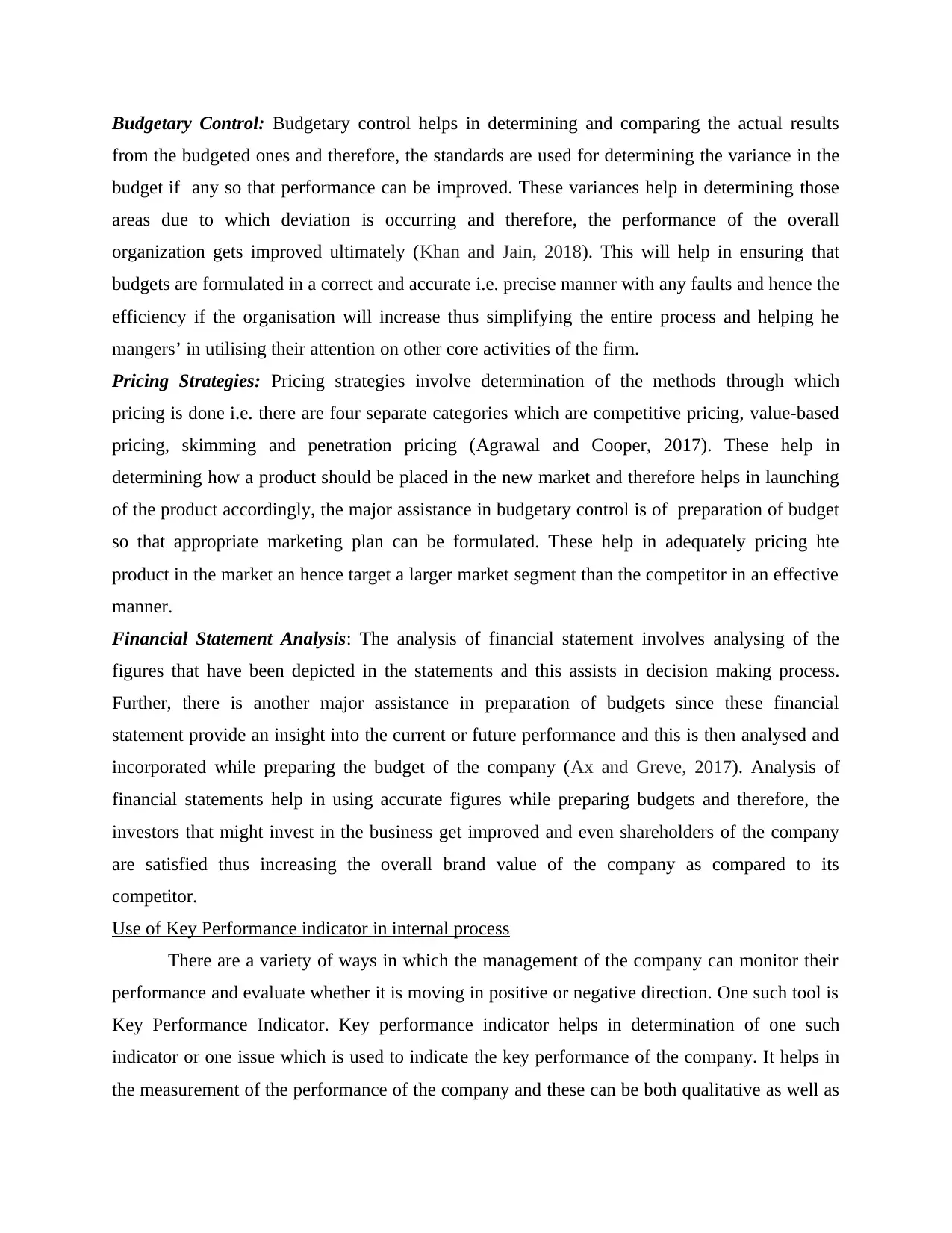

Budgetary Control: Budgetary control helps in determining and comparing the actual results

from the budgeted ones and therefore, the standards are used for determining the variance in the

budget if any so that performance can be improved. These variances help in determining those

areas due to which deviation is occurring and therefore, the performance of the overall

organization gets improved ultimately (Khan and Jain, 2018). This will help in ensuring that

budgets are formulated in a correct and accurate i.e. precise manner with any faults and hence the

efficiency if the organisation will increase thus simplifying the entire process and helping he

mangers’ in utilising their attention on other core activities of the firm.

Pricing Strategies: Pricing strategies involve determination of the methods through which

pricing is done i.e. there are four separate categories which are competitive pricing, value-based

pricing, skimming and penetration pricing (Agrawal and Cooper, 2017). These help in

determining how a product should be placed in the new market and therefore helps in launching

of the product accordingly, the major assistance in budgetary control is of preparation of budget

so that appropriate marketing plan can be formulated. These help in adequately pricing hte

product in the market an hence target a larger market segment than the competitor in an effective

manner.

Financial Statement Analysis: The analysis of financial statement involves analysing of the

figures that have been depicted in the statements and this assists in decision making process.

Further, there is another major assistance in preparation of budgets since these financial

statement provide an insight into the current or future performance and this is then analysed and

incorporated while preparing the budget of the company (Ax and Greve, 2017). Analysis of

financial statements help in using accurate figures while preparing budgets and therefore, the

investors that might invest in the business get improved and even shareholders of the company

are satisfied thus increasing the overall brand value of the company as compared to its

competitor.

Use of Key Performance indicator in internal process

There are a variety of ways in which the management of the company can monitor their

performance and evaluate whether it is moving in positive or negative direction. One such tool is

Key Performance Indicator. Key performance indicator helps in determination of one such

indicator or one issue which is used to indicate the key performance of the company. It helps in

the measurement of the performance of the company and these can be both qualitative as well as

from the budgeted ones and therefore, the standards are used for determining the variance in the

budget if any so that performance can be improved. These variances help in determining those

areas due to which deviation is occurring and therefore, the performance of the overall

organization gets improved ultimately (Khan and Jain, 2018). This will help in ensuring that

budgets are formulated in a correct and accurate i.e. precise manner with any faults and hence the

efficiency if the organisation will increase thus simplifying the entire process and helping he

mangers’ in utilising their attention on other core activities of the firm.

Pricing Strategies: Pricing strategies involve determination of the methods through which

pricing is done i.e. there are four separate categories which are competitive pricing, value-based

pricing, skimming and penetration pricing (Agrawal and Cooper, 2017). These help in

determining how a product should be placed in the new market and therefore helps in launching

of the product accordingly, the major assistance in budgetary control is of preparation of budget

so that appropriate marketing plan can be formulated. These help in adequately pricing hte

product in the market an hence target a larger market segment than the competitor in an effective

manner.

Financial Statement Analysis: The analysis of financial statement involves analysing of the

figures that have been depicted in the statements and this assists in decision making process.

Further, there is another major assistance in preparation of budgets since these financial

statement provide an insight into the current or future performance and this is then analysed and

incorporated while preparing the budget of the company (Ax and Greve, 2017). Analysis of

financial statements help in using accurate figures while preparing budgets and therefore, the

investors that might invest in the business get improved and even shareholders of the company

are satisfied thus increasing the overall brand value of the company as compared to its

competitor.

Use of Key Performance indicator in internal process

There are a variety of ways in which the management of the company can monitor their

performance and evaluate whether it is moving in positive or negative direction. One such tool is

Key Performance Indicator. Key performance indicator helps in determination of one such

indicator or one issue which is used to indicate the key performance of the company. It helps in

the measurement of the performance of the company and these can be both qualitative as well as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

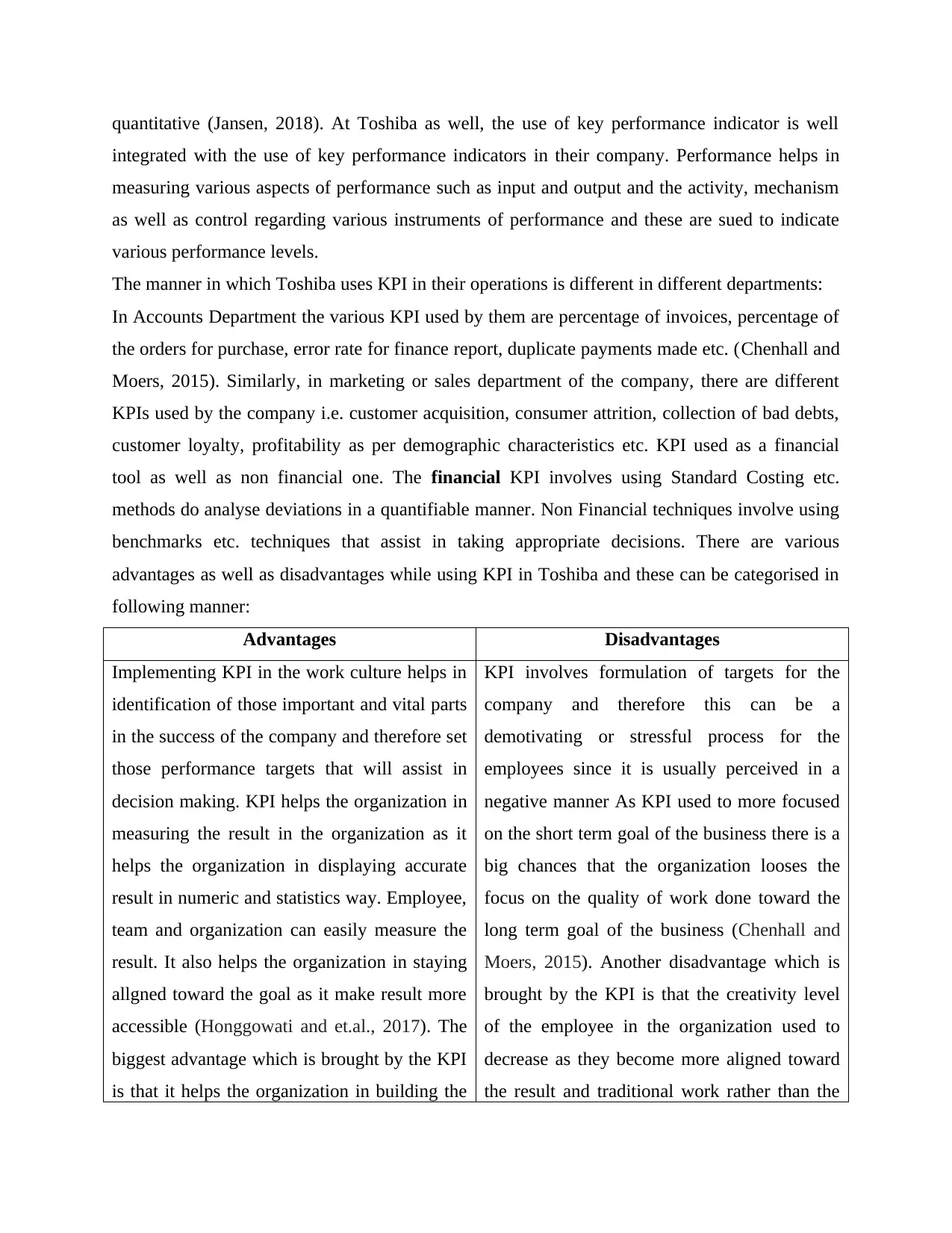

quantitative (Jansen, 2018). At Toshiba as well, the use of key performance indicator is well

integrated with the use of key performance indicators in their company. Performance helps in

measuring various aspects of performance such as input and output and the activity, mechanism

as well as control regarding various instruments of performance and these are sued to indicate

various performance levels.

The manner in which Toshiba uses KPI in their operations is different in different departments:

In Accounts Department the various KPI used by them are percentage of invoices, percentage of

the orders for purchase, error rate for finance report, duplicate payments made etc. (Chenhall and

Moers, 2015). Similarly, in marketing or sales department of the company, there are different

KPIs used by the company i.e. customer acquisition, consumer attrition, collection of bad debts,

customer loyalty, profitability as per demographic characteristics etc. KPI used as a financial

tool as well as non financial one. The financial KPI involves using Standard Costing etc.

methods do analyse deviations in a quantifiable manner. Non Financial techniques involve using

benchmarks etc. techniques that assist in taking appropriate decisions. There are various

advantages as well as disadvantages while using KPI in Toshiba and these can be categorised in

following manner:

Advantages Disadvantages

Implementing KPI in the work culture helps in

identification of those important and vital parts

in the success of the company and therefore set

those performance targets that will assist in

decision making. KPI helps the organization in

measuring the result in the organization as it

helps the organization in displaying accurate

result in numeric and statistics way. Employee,

team and organization can easily measure the

result. It also helps the organization in staying

allgned toward the goal as it make result more

accessible (Honggowati and et.al., 2017). The

biggest advantage which is brought by the KPI

is that it helps the organization in building the

KPI involves formulation of targets for the

company and therefore this can be a

demotivating or stressful process for the

employees since it is usually perceived in a

negative manner As KPI used to more focused

on the short term goal of the business there is a

big chances that the organization looses the

focus on the quality of work done toward the

long term goal of the business (Chenhall and

Moers, 2015). Another disadvantage which is

brought by the KPI is that the creativity level

of the employee in the organization used to

decrease as they become more aligned toward

the result and traditional work rather than the

integrated with the use of key performance indicators in their company. Performance helps in

measuring various aspects of performance such as input and output and the activity, mechanism

as well as control regarding various instruments of performance and these are sued to indicate

various performance levels.

The manner in which Toshiba uses KPI in their operations is different in different departments:

In Accounts Department the various KPI used by them are percentage of invoices, percentage of

the orders for purchase, error rate for finance report, duplicate payments made etc. (Chenhall and

Moers, 2015). Similarly, in marketing or sales department of the company, there are different

KPIs used by the company i.e. customer acquisition, consumer attrition, collection of bad debts,

customer loyalty, profitability as per demographic characteristics etc. KPI used as a financial

tool as well as non financial one. The financial KPI involves using Standard Costing etc.

methods do analyse deviations in a quantifiable manner. Non Financial techniques involve using

benchmarks etc. techniques that assist in taking appropriate decisions. There are various

advantages as well as disadvantages while using KPI in Toshiba and these can be categorised in

following manner:

Advantages Disadvantages

Implementing KPI in the work culture helps in

identification of those important and vital parts

in the success of the company and therefore set

those performance targets that will assist in

decision making. KPI helps the organization in

measuring the result in the organization as it

helps the organization in displaying accurate

result in numeric and statistics way. Employee,

team and organization can easily measure the

result. It also helps the organization in staying

allgned toward the goal as it make result more

accessible (Honggowati and et.al., 2017). The

biggest advantage which is brought by the KPI

is that it helps the organization in building the

KPI involves formulation of targets for the

company and therefore this can be a

demotivating or stressful process for the

employees since it is usually perceived in a

negative manner As KPI used to more focused

on the short term goal of the business there is a

big chances that the organization looses the

focus on the quality of work done toward the

long term goal of the business (Chenhall and

Moers, 2015). Another disadvantage which is

brought by the KPI is that the creativity level

of the employee in the organization used to

decrease as they become more aligned toward

the result and traditional work rather than the

future strategy as organization used to make

the different policy and rules in the

organization on the basis of result measure by

KPI.

process of doing it. Also sometime it get

difficult for the company to track quality of

work as KPI just shows the progress level of

organization.

Patisserie Valerie scandal

Patisserie Valerie which was a company operating in UK is a chain of cafes and in the

year 2018 it was found that the company had committed major frauds by making numerous false

entries which the company has made in previous years thus depicting false profits and position of

the company. The financial auditor of the company was to be blamed for the fraudulent entries.

The management accountant or the internal auditor of the company could have pointed out the

fraudulent activities that were going on to the owner or the top management (Bui and De

Villiers, 2017). Even if they had not taken any decision, they could have gone further and

complained to regulatory or legal bodies stating that the practices carried out at the company are

fraudulent. If they had taken an active role in avoiding frauds within the company it could have

been avoided ultimately. The management of the company can adopt a zero tolerance approach

for fraud management and for this purpose, the management accounting can assist in formulation

of proper budgets, cost sheets etc. that ascertain the exact amount that might be incurred and the

comparison between actual and budgeted expenses is done minutely so that the fake transactions

that were depicted in the books could be removed immediately. Further, the management

accountant should have immediately reported the incidents of fake transactions taking place in

the company to higher authorities (Patisserie Valerie: It’s Not The Accountants Responsibility To

Spot Fraud, 2017). This might had prevented the wide scale failure that the company is now

experiencing.

CONCLUSION

After going through the above report it has been summarized that budgetary control used

to play a very crucial in the organization to help them in getting the success. After that the report

summarized that there are many benefits and dis benefits of budgetary tool which are used by the

accountant. Most commonly used budgetary tools are Cash flow budgeting, Capital budgeting,

Zero Based Budget, Rolling Budget, Operational Budge. After that the report summarized the

way in which management accounting is used by the management accountant. After that the

the different policy and rules in the

organization on the basis of result measure by

KPI.

process of doing it. Also sometime it get

difficult for the company to track quality of

work as KPI just shows the progress level of

organization.

Patisserie Valerie scandal

Patisserie Valerie which was a company operating in UK is a chain of cafes and in the

year 2018 it was found that the company had committed major frauds by making numerous false

entries which the company has made in previous years thus depicting false profits and position of

the company. The financial auditor of the company was to be blamed for the fraudulent entries.

The management accountant or the internal auditor of the company could have pointed out the

fraudulent activities that were going on to the owner or the top management (Bui and De

Villiers, 2017). Even if they had not taken any decision, they could have gone further and

complained to regulatory or legal bodies stating that the practices carried out at the company are

fraudulent. If they had taken an active role in avoiding frauds within the company it could have

been avoided ultimately. The management of the company can adopt a zero tolerance approach

for fraud management and for this purpose, the management accounting can assist in formulation

of proper budgets, cost sheets etc. that ascertain the exact amount that might be incurred and the

comparison between actual and budgeted expenses is done minutely so that the fake transactions

that were depicted in the books could be removed immediately. Further, the management

accountant should have immediately reported the incidents of fake transactions taking place in

the company to higher authorities (Patisserie Valerie: It’s Not The Accountants Responsibility To

Spot Fraud, 2017). This might had prevented the wide scale failure that the company is now

experiencing.

CONCLUSION

After going through the above report it has been summarized that budgetary control used

to play a very crucial in the organization to help them in getting the success. After that the report

summarized that there are many benefits and dis benefits of budgetary tool which are used by the

accountant. Most commonly used budgetary tools are Cash flow budgeting, Capital budgeting,

Zero Based Budget, Rolling Budget, Operational Budge. After that the report summarized the

way in which management accounting is used by the management accountant. After that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report summarized that KPI used to help the company in looking at the performance of the

company on the regular basis that’s the reason accountant used to keep KPI in an internal

process. In the end the report summarized that the management accounting profession has played

a crucial role in identifying and preventing the financial irregularities that were seen.

company on the regular basis that’s the reason accountant used to keep KPI in an internal

process. In the end the report summarized that the management accounting profession has played

a crucial role in identifying and preventing the financial irregularities that were seen.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance, 7(01). p.1650014.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting

Review, 49(1).

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.]

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society, 47. pp.1-13.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1). pp.23-

30.

Jansen, E. P., 2018. Bridging the gap between theory and practice in management accounting:

Reviewing the literature to shape interventions. Accounting, Auditing & Accountability

Journal. 31(5). pp.1486-1509.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Khan, M.Y. and Jain, P.K., 2018. Financial Management: Text, Problems and Cases, 8e.

McGraw-Hill Education.

1

Books and journals

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of

Finance, 7(01). p.1650014.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting

Review, 49(1).

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.]

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society, 47. pp.1-13.

Honggowati, S. and et.al., 2017. Corporate governance and strategic management accounting

disclosure. Indonesian Journal of Sustainability Accounting and Management. 1(1). pp.23-

30.

Jansen, E. P., 2018. Bridging the gap between theory and practice in management accounting:

Reviewing the literature to shape interventions. Accounting, Auditing & Accountability

Journal. 31(5). pp.1486-1509.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Khan, M.Y. and Jain, P.K., 2018. Financial Management: Text, Problems and Cases, 8e.

McGraw-Hill Education.

1

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136.

pp.237-248.

Mack, S. and Goretzki, L., 2017. How management accountants exert influence on managers–a

micro-level analysis of management accountants’ influence tactics in budgetary control

meetings. Qualitative Research in Accounting & Management.14(3). pp.328-362.

Mills, D., 2018. Financial Reporting: A Case Study Analysis (Doctoral dissertation, The

University of Mississippi).

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research. 31. pp.118-122.

Yermack, D., 2017. Donor governance and financial management in prominent US art museums.

Journal of Cultural Economics. 41(3). pp.215-235.

Zietlow, J. and et.al., 2018. Financial management for nonprofit organizations: policies and

practices. John Wiley & Sons.

Online

Patisserie Valerie: It’s Not The Accountants Responsibility To Spot Fraud. 2017.[Online].

Available through: <https://www.lawyer-monthly.com/2019/02/patisserie-valerie-its-

not-the-accountants-responsibility-to-spot-fraud/>

2

management accounting, control, and reporting. Journal of Cleaner Production, 136.

pp.237-248.

Mack, S. and Goretzki, L., 2017. How management accountants exert influence on managers–a

micro-level analysis of management accountants’ influence tactics in budgetary control

meetings. Qualitative Research in Accounting & Management.14(3). pp.328-362.

Mills, D., 2018. Financial Reporting: A Case Study Analysis (Doctoral dissertation, The

University of Mississippi).

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research. 31. pp.118-122.

Yermack, D., 2017. Donor governance and financial management in prominent US art museums.

Journal of Cultural Economics. 41(3). pp.215-235.

Zietlow, J. and et.al., 2018. Financial management for nonprofit organizations: policies and

practices. John Wiley & Sons.

Online

Patisserie Valerie: It’s Not The Accountants Responsibility To Spot Fraud. 2017.[Online].

Available through: <https://www.lawyer-monthly.com/2019/02/patisserie-valerie-its-

not-the-accountants-responsibility-to-spot-fraud/>

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.