Management Accounting: Concepts and Techniques for Decision Makers

VerifiedAdded on 2022/12/26

|17

|4763

|88

Report

AI Summary

This report delves into the core concepts of management accounting, offering a detailed analysis of various techniques and their applications. It begins with an introduction to management accounting and the necessity of different systems, followed by a discussion of management reporting methods. Task 1 examines the benefits of management accounting systems and their practical applications, critically evaluating their integration within an organization. Task 2 focuses on the preparation of marginal costing and absorption costing income statements, alongside an analysis of management accounting techniques and financial reporting documents. Task 3 explores the advantages and disadvantages of planning tools used for budgetary control, while analyzing their application in budget and forecast preparation. Task 4 compares firms to identify their adaptation to management accounting systems and their response to management accounting problems. The report also includes financial reports and reconciliation statements. The report concludes with a summary of the key findings and insights.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and requirement of various management accounting systems......3

P2 Different methods used in management reporting.................................................................4

M1 Benefits of management accounting system with their respective application ...................5

D1 Critically examine integration of management accounting systems and management

accounting in an organisation .....................................................................................................6

TASK 2............................................................................................................................................6

P3 Preparation of marginal costing and absorption costing income statements ........................6

M2 Application of management accounting techniques and appropriate financial reporting

documents...................................................................................................................................9

D2 Financial reports which interpret wide range of business operations.................................11

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of various planning tools used for budgetary control........11

M3 Analysis of planning tools and their respective application for budgets and forecasts......12

TASK 4..........................................................................................................................................13

P5 Comparison of firms in order to identify their adaptation to management accounting

system .......................................................................................................................................13

M4 Response to management accounting problems leading to sustainable success................14

D3 Planning tools responsible for financial problem solving in order to attain organisational

success.......................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and requirement of various management accounting systems......3

P2 Different methods used in management reporting.................................................................4

M1 Benefits of management accounting system with their respective application ...................5

D1 Critically examine integration of management accounting systems and management

accounting in an organisation .....................................................................................................6

TASK 2............................................................................................................................................6

P3 Preparation of marginal costing and absorption costing income statements ........................6

M2 Application of management accounting techniques and appropriate financial reporting

documents...................................................................................................................................9

D2 Financial reports which interpret wide range of business operations.................................11

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of various planning tools used for budgetary control........11

M3 Analysis of planning tools and their respective application for budgets and forecasts......12

TASK 4..........................................................................................................................................13

P5 Comparison of firms in order to identify their adaptation to management accounting

system .......................................................................................................................................13

M4 Response to management accounting problems leading to sustainable success................14

D3 Planning tools responsible for financial problem solving in order to attain organisational

success.......................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is considered as mostly used technique which helps managers to

use certain statements for the sake of decision making. This technique aid in proper evaluation of

performance of the company. Decision-making includes financial as well as non financial

decision making in order to regulate business based operations in the long term. This is guidance

which is being provided by management to the superiors to reflect appropriate and efficient

decision making as per the condition. This report comprises of various tools of management

accounting which will ultimately be responsible for decision-making. These tools and techniques

will include marginal costing, absorption costing and various variance analysis. This will

ultimately be helpful in efficient decision making on behalf of manager of a company. Also it

include interpretation and evaluation of different above stated systems of management

accounting as well as planning tools in relation to a company in specific time period.

TASK 1

P1 Management accounting and requirement of various management accounting systems

Management accounting is defined as a broad branch of finance where various significant

techniques are used in order to assist in ultimate decision-making by manager on behalf of

organisation (Hogle, 2019). This is used by finance department in order to promote healthy

business operations by rectification of any errors in them. Connect Catering Services has adopted

this technique to enhance company's overall productivity in relations to its operations in the long

term.

Various management accounting systems have established strong roots over company's

decision making by making them much effective and reliable. Adoption of such systems promote

growth and sustainability of its relevant operations. Connect catering services enables its

superiors to use various management accounts and statements in order to produce appropriate

decisions which will ultimately define company's progress. There are various management

accounting practices which can be discussed as follows:

Price-optimization: It refers to effective mathematical tools which signifies how demand

of a particular changes due to the variation in customer's behaviour. Through this approach,

customer's willingness to pay will be highlighted so that is will become easier for a company to

modify its policies as per customer's preferences in order to maintain profit-margins and costs so

Management accounting is considered as mostly used technique which helps managers to

use certain statements for the sake of decision making. This technique aid in proper evaluation of

performance of the company. Decision-making includes financial as well as non financial

decision making in order to regulate business based operations in the long term. This is guidance

which is being provided by management to the superiors to reflect appropriate and efficient

decision making as per the condition. This report comprises of various tools of management

accounting which will ultimately be responsible for decision-making. These tools and techniques

will include marginal costing, absorption costing and various variance analysis. This will

ultimately be helpful in efficient decision making on behalf of manager of a company. Also it

include interpretation and evaluation of different above stated systems of management

accounting as well as planning tools in relation to a company in specific time period.

TASK 1

P1 Management accounting and requirement of various management accounting systems

Management accounting is defined as a broad branch of finance where various significant

techniques are used in order to assist in ultimate decision-making by manager on behalf of

organisation (Hogle, 2019). This is used by finance department in order to promote healthy

business operations by rectification of any errors in them. Connect Catering Services has adopted

this technique to enhance company's overall productivity in relations to its operations in the long

term.

Various management accounting systems have established strong roots over company's

decision making by making them much effective and reliable. Adoption of such systems promote

growth and sustainability of its relevant operations. Connect catering services enables its

superiors to use various management accounts and statements in order to produce appropriate

decisions which will ultimately define company's progress. There are various management

accounting practices which can be discussed as follows:

Price-optimization: It refers to effective mathematical tools which signifies how demand

of a particular changes due to the variation in customer's behaviour. Through this approach,

customer's willingness to pay will be highlighted so that is will become easier for a company to

modify its policies as per customer's preferences in order to maintain profit-margins and costs so

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that company's performance will not be harmed (Christ and Burritt, 2017). By analysing

consumer's behaviour, company can build strategic policies, forecasts demand, pricing policies

and so on in order to manage profitability level. Connect catering services have adopted this

system in order to enhance its production levels to avoid any extra costs which will reflect

sufficient profit-margin.

Inventory management system: Stock is said to be most important factor for company's

revenue earning capacity. It is something on which company's profitability is dependent through

effective sales turnover (Ylä-Kujala and et. al., 2018). In this regard inventory management

system has been adopted by Connect catering services as company is implementing effective

tools of management accounting in order to eliminate complexities in the respective supply chain

systems and processes of the company. It is necessary for a company to manage inventory

related shortcoming and errors so that appropriate productivity could be achieved by the

company. Basic functioning of inventory management system is suggested as forecast

anticipated demand in respect of goods being produced by the company as well as determine

level of operational efficiency and so on.

Cost accounting system: This system refers to accounting which has been introduced for

sake of manufacturers in order to trace flow of inventory as per the relevant stage of production

system (Stockenstrand and Nilsson, 2017). It is basically evaluation of material in raw form till

its conversion into finished products through various production stages. This is mostly

implemented by manufacturing houses in order to identify their actual performance of production

department. Connect catering services has implemented this technique to track record of its

significant activities in reference to production of goods as well as its transformation process in

order to maintain profitability by eliminating any sort of wastages.

P2 Different methods used in management reporting

Budget report: It is established in order to meet future based contingencies in reference

to expenses of an organisation. It is considered as a valuable practice which needs to be adopted

by organisations in order to eliminate unnecessary occurrence of cost in business operations. It is

also stated as identification of deviation in actual performance as compared to forecasted

performance. Factors responsible for such factors could be high prices of raw materials, extra

cost for operations, reduced market share, etc. Connect catering services has enabled usage of

consumer's behaviour, company can build strategic policies, forecasts demand, pricing policies

and so on in order to manage profitability level. Connect catering services have adopted this

system in order to enhance its production levels to avoid any extra costs which will reflect

sufficient profit-margin.

Inventory management system: Stock is said to be most important factor for company's

revenue earning capacity. It is something on which company's profitability is dependent through

effective sales turnover (Ylä-Kujala and et. al., 2018). In this regard inventory management

system has been adopted by Connect catering services as company is implementing effective

tools of management accounting in order to eliminate complexities in the respective supply chain

systems and processes of the company. It is necessary for a company to manage inventory

related shortcoming and errors so that appropriate productivity could be achieved by the

company. Basic functioning of inventory management system is suggested as forecast

anticipated demand in respect of goods being produced by the company as well as determine

level of operational efficiency and so on.

Cost accounting system: This system refers to accounting which has been introduced for

sake of manufacturers in order to trace flow of inventory as per the relevant stage of production

system (Stockenstrand and Nilsson, 2017). It is basically evaluation of material in raw form till

its conversion into finished products through various production stages. This is mostly

implemented by manufacturing houses in order to identify their actual performance of production

department. Connect catering services has implemented this technique to track record of its

significant activities in reference to production of goods as well as its transformation process in

order to maintain profitability by eliminating any sort of wastages.

P2 Different methods used in management reporting

Budget report: It is established in order to meet future based contingencies in reference

to expenses of an organisation. It is considered as a valuable practice which needs to be adopted

by organisations in order to eliminate unnecessary occurrence of cost in business operations. It is

also stated as identification of deviation in actual performance as compared to forecasted

performance. Factors responsible for such factors could be high prices of raw materials, extra

cost for operations, reduced market share, etc. Connect catering services has enabled usage of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this report as it is beneficial for an organisation in the long term as well as shatter extra cost

which is being affecting company's overall efficiency.

Performance report: It is somewhat similar to budget report, but its actual emphasizes is

over company's performance irrespective of budget is made or not. It is necessary for an

organisation to eliminate any kind of deviations in its performance as compared to set standards

by it (Hörisch and et. al., 2020). In this regard, Connect catering services is focusing over its

operations to increase its overall efficiency in the long term in order to survive in marketplace.

This is important for superiors to analyse its business from every aspect to eliminate any factor

which may affect profit generation capacity of a company.

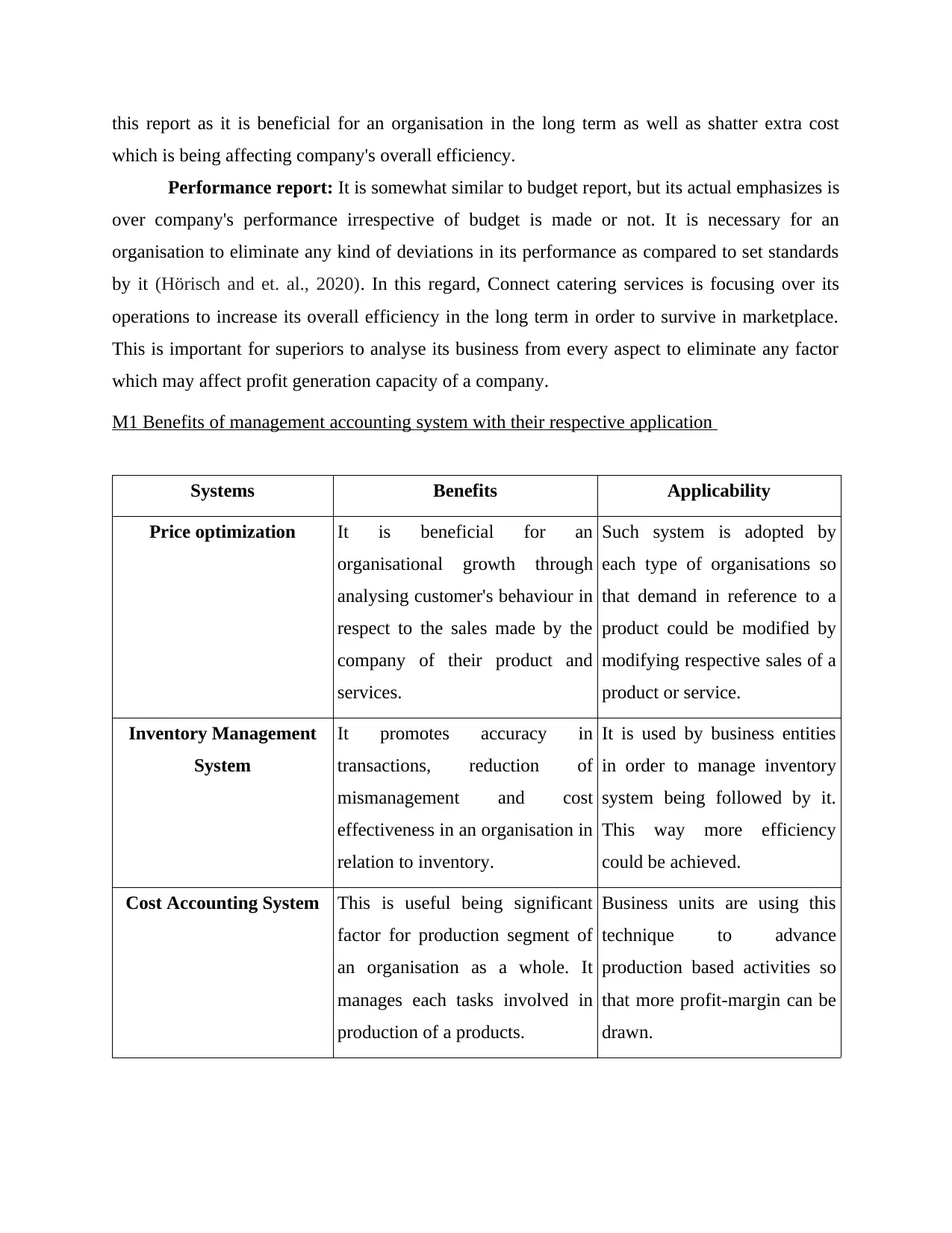

M1 Benefits of management accounting system with their respective application

Systems Benefits Applicability

Price optimization It is beneficial for an

organisational growth through

analysing customer's behaviour in

respect to the sales made by the

company of their product and

services.

Such system is adopted by

each type of organisations so

that demand in reference to a

product could be modified by

modifying respective sales of a

product or service.

Inventory Management

System

It promotes accuracy in

transactions, reduction of

mismanagement and cost

effectiveness in an organisation in

relation to inventory.

It is used by business entities

in order to manage inventory

system being followed by it.

This way more efficiency

could be achieved.

Cost Accounting System This is useful being significant

factor for production segment of

an organisation as a whole. It

manages each tasks involved in

production of a products.

Business units are using this

technique to advance

production based activities so

that more profit-margin can be

drawn.

which is being affecting company's overall efficiency.

Performance report: It is somewhat similar to budget report, but its actual emphasizes is

over company's performance irrespective of budget is made or not. It is necessary for an

organisation to eliminate any kind of deviations in its performance as compared to set standards

by it (Hörisch and et. al., 2020). In this regard, Connect catering services is focusing over its

operations to increase its overall efficiency in the long term in order to survive in marketplace.

This is important for superiors to analyse its business from every aspect to eliminate any factor

which may affect profit generation capacity of a company.

M1 Benefits of management accounting system with their respective application

Systems Benefits Applicability

Price optimization It is beneficial for an

organisational growth through

analysing customer's behaviour in

respect to the sales made by the

company of their product and

services.

Such system is adopted by

each type of organisations so

that demand in reference to a

product could be modified by

modifying respective sales of a

product or service.

Inventory Management

System

It promotes accuracy in

transactions, reduction of

mismanagement and cost

effectiveness in an organisation in

relation to inventory.

It is used by business entities

in order to manage inventory

system being followed by it.

This way more efficiency

could be achieved.

Cost Accounting System This is useful being significant

factor for production segment of

an organisation as a whole. It

manages each tasks involved in

production of a products.

Business units are using this

technique to advance

production based activities so

that more profit-margin can be

drawn.

D1 Critically examine integration of management accounting systems and management

accounting in an organisation

Management accounting is a wide activity which is being adopted by various

organisations through implementation of effective management accounting systems.

Management accounting systems are integrated with management accounting being its ultimate

essence (Malik and et. al., 2021). Connect catering services have selected such techniques of

inventory management, cost management and so on in order to facilitate managers in production

of most efficient and effective decision-making in regard to company's ultimate success. As per

suitability of a company, its choose relevant management accounting systems which will be

helpful in progress and success of an organisation. Being a catering company, it must ensure

adoption of management accounting techniques which can produce most effective services and

products to its clients to survive in the market.

TASK 2

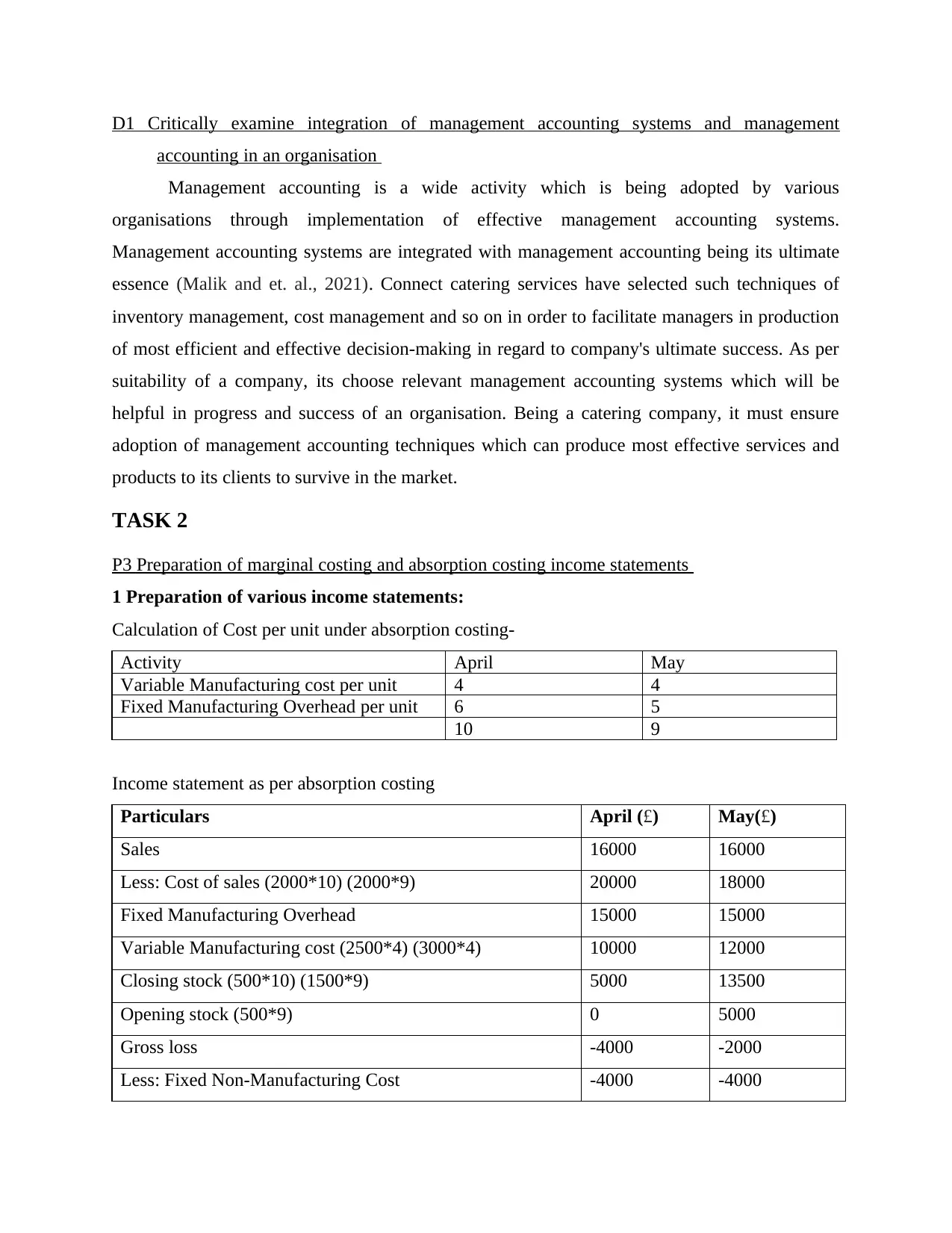

P3 Preparation of marginal costing and absorption costing income statements

1 Preparation of various income statements:

Calculation of Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement as per absorption costing

Particulars April (£) May(£)

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

accounting in an organisation

Management accounting is a wide activity which is being adopted by various

organisations through implementation of effective management accounting systems.

Management accounting systems are integrated with management accounting being its ultimate

essence (Malik and et. al., 2021). Connect catering services have selected such techniques of

inventory management, cost management and so on in order to facilitate managers in production

of most efficient and effective decision-making in regard to company's ultimate success. As per

suitability of a company, its choose relevant management accounting systems which will be

helpful in progress and success of an organisation. Being a catering company, it must ensure

adoption of management accounting techniques which can produce most effective services and

products to its clients to survive in the market.

TASK 2

P3 Preparation of marginal costing and absorption costing income statements

1 Preparation of various income statements:

Calculation of Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement as per absorption costing

Particulars April (£) May(£)

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

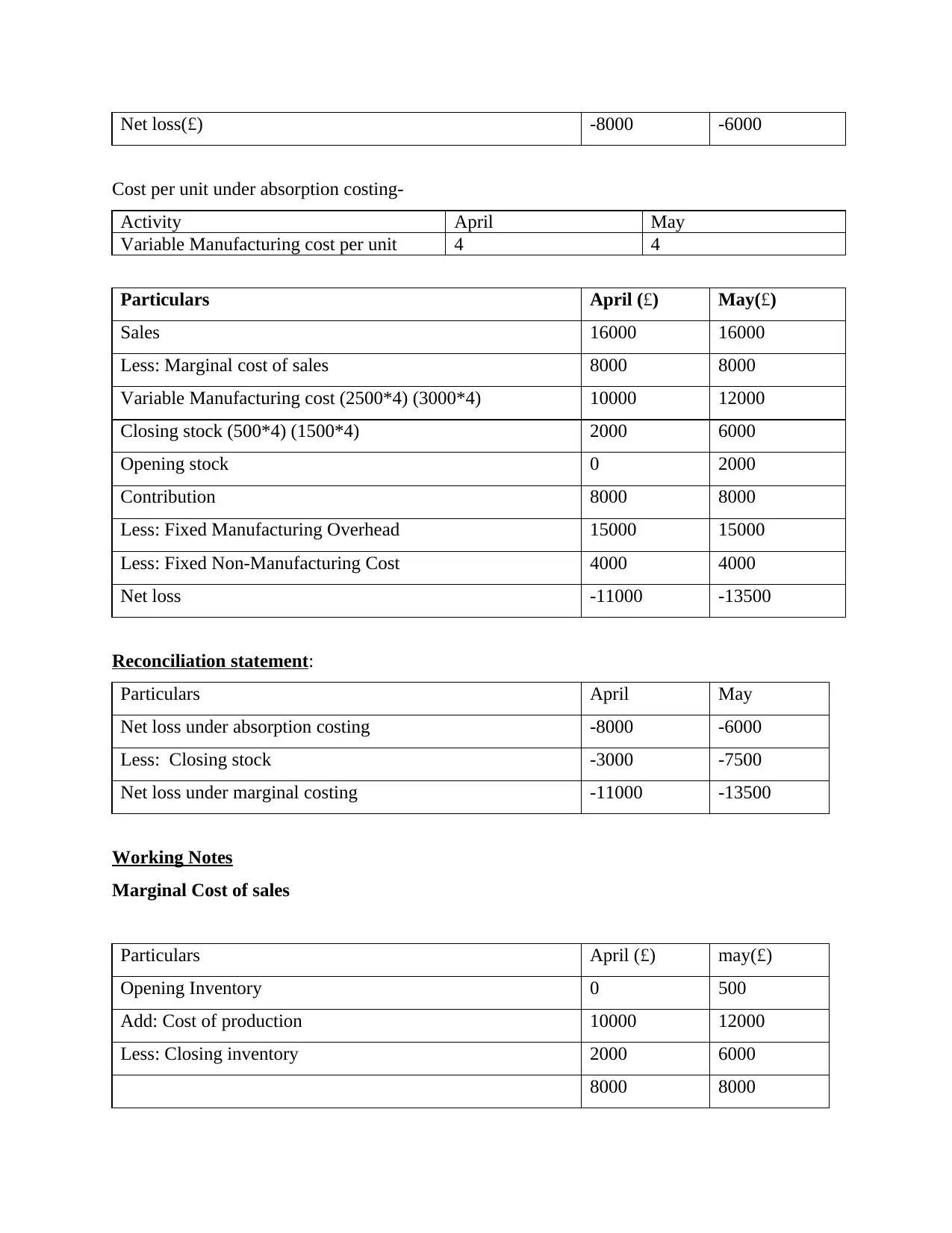

Net loss(£) -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April (£) May(£)

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Net loss -11000 -13500

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April (£) may(£)

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April (£) May(£)

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Net loss -11000 -13500

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April (£) may(£)

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

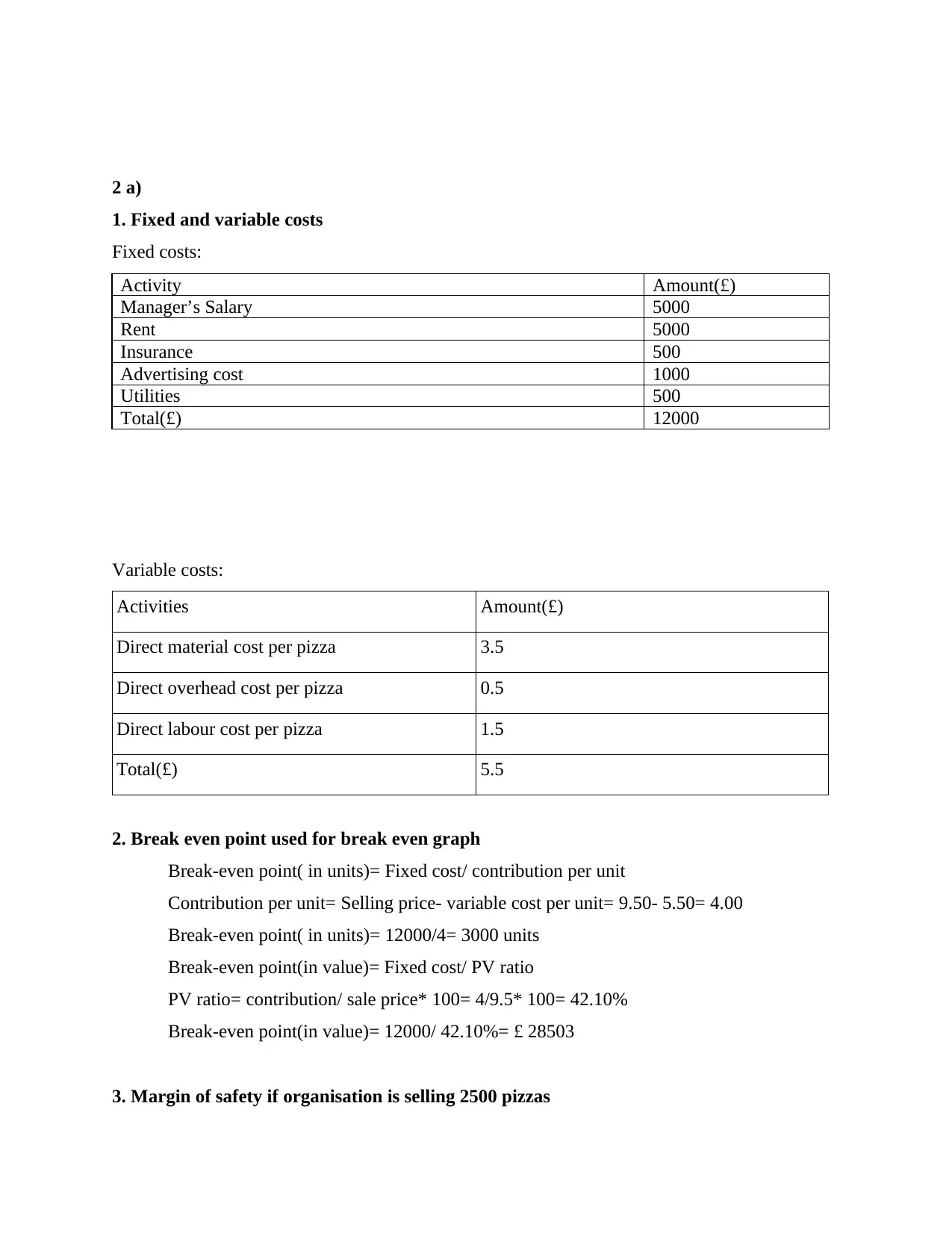

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount(£)

Manager’s Salary 5000

Rent 5000

Insurance 500

Advertising cost 1000

Utilities 500

Total(£) 12000

Variable costs:

Activities Amount(£)

Direct material cost per pizza 3.5

Direct overhead cost per pizza 0.5

Direct labour cost per pizza 1.5

Total(£) 5.5

2. Break even point used for break even graph

Break-even point( in units)= Fixed cost/ contribution per unit

Contribution per unit= Selling price- variable cost per unit= 9.50- 5.50= 4.00

Break-even point( in units)= 12000/4= 3000 units

Break-even point(in value)= Fixed cost/ PV ratio

PV ratio= contribution/ sale price* 100= 4/9.5* 100= 42.10%

Break-even point(in value)= 12000/ 42.10%= £ 28503

3. Margin of safety if organisation is selling 2500 pizzas

1. Fixed and variable costs

Fixed costs:

Activity Amount(£)

Manager’s Salary 5000

Rent 5000

Insurance 500

Advertising cost 1000

Utilities 500

Total(£) 12000

Variable costs:

Activities Amount(£)

Direct material cost per pizza 3.5

Direct overhead cost per pizza 0.5

Direct labour cost per pizza 1.5

Total(£) 5.5

2. Break even point used for break even graph

Break-even point( in units)= Fixed cost/ contribution per unit

Contribution per unit= Selling price- variable cost per unit= 9.50- 5.50= 4.00

Break-even point( in units)= 12000/4= 3000 units

Break-even point(in value)= Fixed cost/ PV ratio

PV ratio= contribution/ sale price* 100= 4/9.5* 100= 42.10%

Break-even point(in value)= 12000/ 42.10%= £ 28503

3. Margin of safety if organisation is selling 2500 pizzas

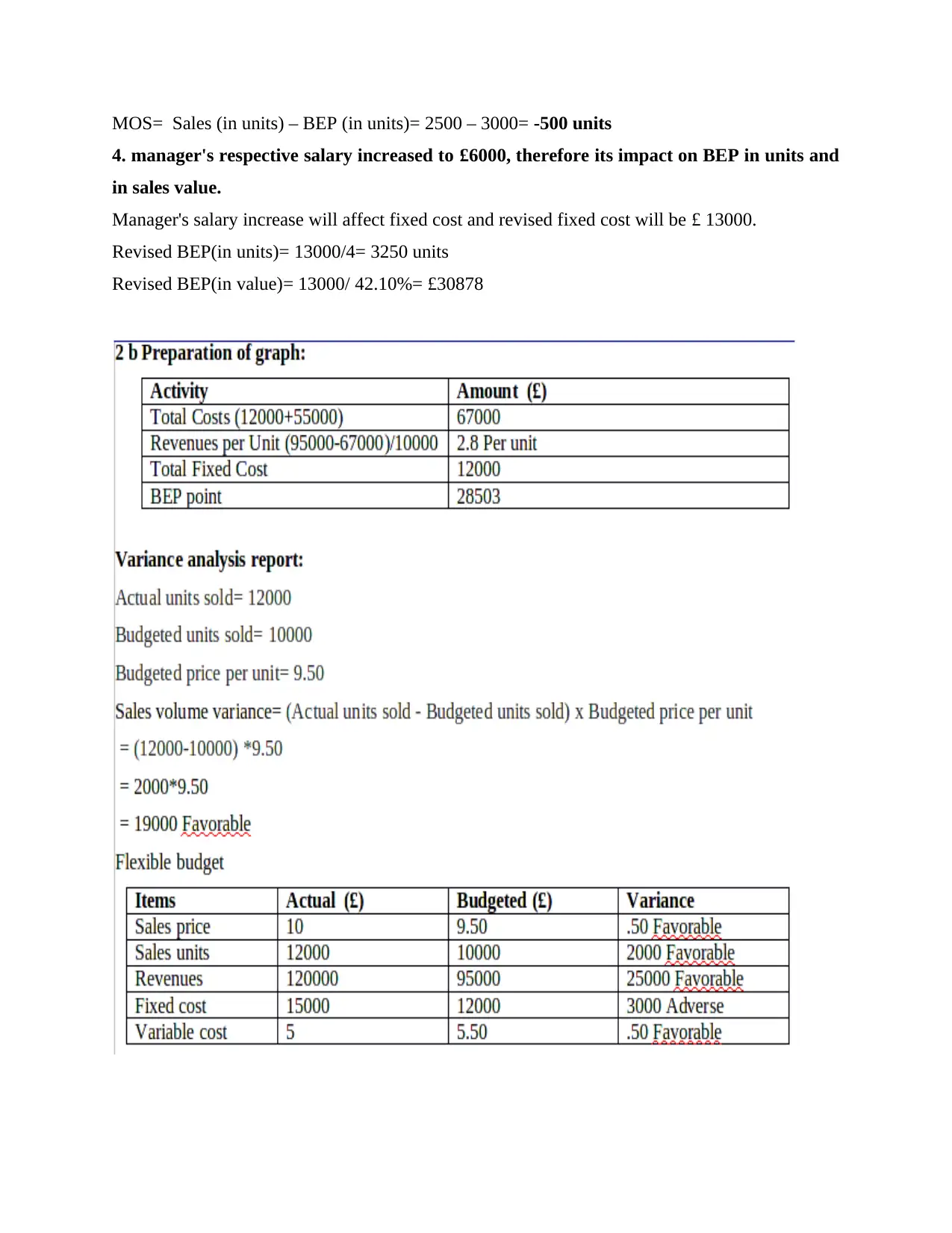

MOS= Sales (in units) – BEP (in units)= 2500 – 3000= -500 units

4. manager's respective salary increased to £6000, therefore its impact on BEP in units and

in sales value.

Manager's salary increase will affect fixed cost and revised fixed cost will be £ 13000.

Revised BEP(in units)= 13000/4= 3250 units

Revised BEP(in value)= 13000/ 42.10%= £30878

4. manager's respective salary increased to £6000, therefore its impact on BEP in units and

in sales value.

Manager's salary increase will affect fixed cost and revised fixed cost will be £ 13000.

Revised BEP(in units)= 13000/4= 3250 units

Revised BEP(in value)= 13000/ 42.10%= £30878

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Application of management accounting techniques and appropriate financial reporting

documents

There are considerably wide variety of management accounting techniques as well as

financial reporting statements which are said to be very important for company's overall

productivity and profitability in connection to its growth. Its techniques have been used by

Connect catering services in order to manage its events and services in appropriate manner. It is

important to adopt appropriate techniques which can be illustrated as follows:

Marginal costing: In marginal costing, the effect of variable costs has been evaluated in

reference to production capacity of a company (Chiou and et. al., 2020). It is very

effective technique helpful in evaluation of performance of a company in its progress.

Connect catering services have been implementing such strategy in its competent

business in order to maintain reliable procedures for long lasting term. This is mostly

used for developing understanding of performance of a company.

Variance analysis: It is a study of any kind of deviation between actual performance as

compared to forecasted estimates. Connect catering is devoted towards analysing its

operations to reflect utmost accuracy and reliable data in order to survive through the

competitive environment. It is considered as a most effective technique which is used by

each size of organisation across the globe.

Management reporting: This is very effective approach towards assisting managers

through decision-making process. Management must prepare set of statements which are

responsible for companies performance evaluation, efficiency maintenance and cost

effective techniques. Connect catering services being serving in UK has to maintain

appropriate combination of management reporting structure in order to motivate its

workforce for production of effective results which will be responsible for managerial

decision-making.

Budget Preparation: Budget is a sort of estimate of revenue as well as expenditure over

a given period of time on future grounds. A budget is also known as financial plan which

is used to attain maximum profit-margins through elimination of unnecessary costs in the

operations of a company (Lennon, 2020). Such practice helps in achieving optimum level

of profitability by organisation in order to expand over a large platform. Connect catering

services in this context has applied techniques like budget forecasts and planning in order

documents

There are considerably wide variety of management accounting techniques as well as

financial reporting statements which are said to be very important for company's overall

productivity and profitability in connection to its growth. Its techniques have been used by

Connect catering services in order to manage its events and services in appropriate manner. It is

important to adopt appropriate techniques which can be illustrated as follows:

Marginal costing: In marginal costing, the effect of variable costs has been evaluated in

reference to production capacity of a company (Chiou and et. al., 2020). It is very

effective technique helpful in evaluation of performance of a company in its progress.

Connect catering services have been implementing such strategy in its competent

business in order to maintain reliable procedures for long lasting term. This is mostly

used for developing understanding of performance of a company.

Variance analysis: It is a study of any kind of deviation between actual performance as

compared to forecasted estimates. Connect catering is devoted towards analysing its

operations to reflect utmost accuracy and reliable data in order to survive through the

competitive environment. It is considered as a most effective technique which is used by

each size of organisation across the globe.

Management reporting: This is very effective approach towards assisting managers

through decision-making process. Management must prepare set of statements which are

responsible for companies performance evaluation, efficiency maintenance and cost

effective techniques. Connect catering services being serving in UK has to maintain

appropriate combination of management reporting structure in order to motivate its

workforce for production of effective results which will be responsible for managerial

decision-making.

Budget Preparation: Budget is a sort of estimate of revenue as well as expenditure over

a given period of time on future grounds. A budget is also known as financial plan which

is used to attain maximum profit-margins through elimination of unnecessary costs in the

operations of a company (Lennon, 2020). Such practice helps in achieving optimum level

of profitability by organisation in order to expand over a large platform. Connect catering

services in this context has applied techniques like budget forecasts and planning in order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to manage its prevailing cost expectations to survive the competitive environment.

Budget is ultimately helpful for company's growth and success as well as survival by

elimination of losses.

D2 Financial reports which interpret wide range of business operations

Financial reporting has a huge impact over company's decision-making which hamper its

performance adversely or positively. Such reporting formats includes cash flow statements,

balance sheet, income statements and so on. Connect catering services has used wide range of

financial reporting which includes cash flow statements, income statements, etc. As such

reporting techniques aid in effective decision-making to an organisation for long term

sustainability. A company must adopt appropriate reporting strategy in order to perform easy

flow of operations.

TASK 3

P4 Advantages and disadvantages of various planning tools used for budgetary control

Planning tools are said to be important for company's overall success. These planning

tools are used in context to budgetary control technique so that adequate maintenance of cost will

be done (Rashid, 2020). These planning techniques are very much required for company's overall

growth and development of cost effectiveness. In reference to Connect catering services,

following given planning tools have been used:

Variance analysis: It deals with inherent deviation between forecasted as well as actual

performance of an organisation (Adler, 2018). Such deviations are reflected in order to identify

respective areas of improvisation within a company. Variance can be optimistic as well as

pessimistic which needs to be identified by organisation so that proper actions can be made in

such reference. Connect catering has adopted this technique in order to evaluate variables in

operations of a company as well corrective actions could be taken.

Advantages: Various advantages of this technique is that it indicates adjustments which

needs to be made in budget forecasts, examine performance, controls expenditure and so on.

Disadvantages: It requires participation of experts as it is regarded as a complex and time

consuming procedure which requires optimum contribution of specialised personnel.

Balanced scorecard: It is considered as strategic tool which is regarded as planning for a

set target which company is willing to achieve. It required day to day operations management,

Budget is ultimately helpful for company's growth and success as well as survival by

elimination of losses.

D2 Financial reports which interpret wide range of business operations

Financial reporting has a huge impact over company's decision-making which hamper its

performance adversely or positively. Such reporting formats includes cash flow statements,

balance sheet, income statements and so on. Connect catering services has used wide range of

financial reporting which includes cash flow statements, income statements, etc. As such

reporting techniques aid in effective decision-making to an organisation for long term

sustainability. A company must adopt appropriate reporting strategy in order to perform easy

flow of operations.

TASK 3

P4 Advantages and disadvantages of various planning tools used for budgetary control

Planning tools are said to be important for company's overall success. These planning

tools are used in context to budgetary control technique so that adequate maintenance of cost will

be done (Rashid, 2020). These planning techniques are very much required for company's overall

growth and development of cost effectiveness. In reference to Connect catering services,

following given planning tools have been used:

Variance analysis: It deals with inherent deviation between forecasted as well as actual

performance of an organisation (Adler, 2018). Such deviations are reflected in order to identify

respective areas of improvisation within a company. Variance can be optimistic as well as

pessimistic which needs to be identified by organisation so that proper actions can be made in

such reference. Connect catering has adopted this technique in order to evaluate variables in

operations of a company as well corrective actions could be taken.

Advantages: Various advantages of this technique is that it indicates adjustments which

needs to be made in budget forecasts, examine performance, controls expenditure and so on.

Disadvantages: It requires participation of experts as it is regarded as a complex and time

consuming procedure which requires optimum contribution of specialised personnel.

Balanced scorecard: It is considered as strategic tool which is regarded as planning for a

set target which company is willing to achieve. It required day to day operations management,

prioritizing events, evaluate and monitor further progress of the target goals (Jiang and Chen,

2019). Key factor of using this technique is that it enables organisation to connect the puzzle in

the right manner. Connect catering services is using such tool in order to formulate beneficial

strategic policies for welfare of its organisation.

Advantages: This has wide range of benefits which includes facilitating activities in

aligned manner, effortless communication system, better format to business based strategy and

so on.

Disadvantages: Such technique required tons of data in order to conduct smoother flow of

activities which makes it complicated for companies to implement in appropriate manner.

Responsibility accounting: It is a system which includes determination of responsibility

units or centres for their respective jobs or objectives as well as development of performance in

reference to respective job centre (Mawejje and Odhiambo, 2020). It considers assembling and

reporting revenues as well as cost in respect of specific area. Its inherent advantages and

disadvantages can be given as follows:

Advantages: this approach delegates authority from top to down that means from

managers to lower divisional employees. It is also considered as technique of performance

evaluation which helps in identification of companies actual financial position.

Disadvantages: In this system, sometimes it become challenging to meet essentials of a

successful unit which could be harmful for company's image and profitability.

M3 Analysis of planning tools and their respective application for budgets and forecasts

Planning tools are concluded to be effective technique which helps in managing

company's tasks and operations in much efficient way (KUTSURI and et. al., 2018). Such

techniques are used for budget control which facilitate with appropriate planning and forecast

factors in long term growth of a company. Connect catering services has enabled this technique

which provides appropriate planning structure and forecasts in order to interpret future demands

and fluctuation which may incur at future date. Therefore, it must use effective techniques of

budgeting and forecasts so that healthy financial conditions could be maintained in an

organisation for the long term.

2019). Key factor of using this technique is that it enables organisation to connect the puzzle in

the right manner. Connect catering services is using such tool in order to formulate beneficial

strategic policies for welfare of its organisation.

Advantages: This has wide range of benefits which includes facilitating activities in

aligned manner, effortless communication system, better format to business based strategy and

so on.

Disadvantages: Such technique required tons of data in order to conduct smoother flow of

activities which makes it complicated for companies to implement in appropriate manner.

Responsibility accounting: It is a system which includes determination of responsibility

units or centres for their respective jobs or objectives as well as development of performance in

reference to respective job centre (Mawejje and Odhiambo, 2020). It considers assembling and

reporting revenues as well as cost in respect of specific area. Its inherent advantages and

disadvantages can be given as follows:

Advantages: this approach delegates authority from top to down that means from

managers to lower divisional employees. It is also considered as technique of performance

evaluation which helps in identification of companies actual financial position.

Disadvantages: In this system, sometimes it become challenging to meet essentials of a

successful unit which could be harmful for company's image and profitability.

M3 Analysis of planning tools and their respective application for budgets and forecasts

Planning tools are concluded to be effective technique which helps in managing

company's tasks and operations in much efficient way (KUTSURI and et. al., 2018). Such

techniques are used for budget control which facilitate with appropriate planning and forecast

factors in long term growth of a company. Connect catering services has enabled this technique

which provides appropriate planning structure and forecasts in order to interpret future demands

and fluctuation which may incur at future date. Therefore, it must use effective techniques of

budgeting and forecasts so that healthy financial conditions could be maintained in an

organisation for the long term.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.