Management Accounting Report: Financial Problem Solving Strategies

VerifiedAdded on 2021/01/02

|17

|4860

|166

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its significance in organizational management and financial decision-making. It delves into the core concepts, including the meaning and requirements of various types of management accounting, such as cost accounting, inventory management, job costing, price optimization, and process costing. The report outlines different methods of management accounting reporting, including financial reports, pro forma cash flow statements, and sales reports, highlighting their utility in evaluating financial performance and making strategic decisions. It also discusses the benefits of management accounting systems in terms of cost control, profitability enhancement, and business expansion. Furthermore, the report explores the integration of management accounting systems with organizational structures and processes, emphasizing the role of reports like cash flow statements and income statements in financial analysis. The report also covers marginal and absorption costing methods, providing detailed examples and interpretations of their application in profit and loss statements. Finally, it examines the advantages and disadvantages of different planning tools used in budgetary control, evaluating their role in addressing financial problems and contributing to sustainable success. The report concludes with a discussion on how organizations adapt management accounting systems to respond to financial challenges and achieve long-term financial stability.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning and requirement of types of management accounting..................................................1

Different methods of management accounting reporting............................................................2

Benefits of management accounting systems..............................................................................3

System and reports of management accounting integrated with organization............................3

TASK 2............................................................................................................................................3

Marginal and absorption costing..................................................................................................3

TASK 3...........................................................................................................................................6

1. Advantages and disadvantages of different types of planning tools used in Budgetary

Control.........................................................................................................................................6

2. Use of different planning tools and their application for preparing and forecasting budgets..8

3. Evaluate how planning tools for accounting respond appropriately for solving Financial

problems.....................................................................................................................................10

TASK 4..........................................................................................................................................10

1. Organizations are adapting management accounting systems to respond financial problems

....................................................................................................................................................10

2. Management Accounting can lead organizations to sustainable success by responding to

financial problems......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Meaning and requirement of types of management accounting..................................................1

Different methods of management accounting reporting............................................................2

Benefits of management accounting systems..............................................................................3

System and reports of management accounting integrated with organization............................3

TASK 2............................................................................................................................................3

Marginal and absorption costing..................................................................................................3

TASK 3...........................................................................................................................................6

1. Advantages and disadvantages of different types of planning tools used in Budgetary

Control.........................................................................................................................................6

2. Use of different planning tools and their application for preparing and forecasting budgets..8

3. Evaluate how planning tools for accounting respond appropriately for solving Financial

problems.....................................................................................................................................10

TASK 4..........................................................................................................................................10

1. Organizations are adapting management accounting systems to respond financial problems

....................................................................................................................................................10

2. Management Accounting can lead organizations to sustainable success by responding to

financial problems......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a internal accounting that use by managers for

manage and maintain organization through evolution. Managers of organization

evaluate and analyze books and accounts that helps in make planning, organizing,

directing and controlling. On the bases of financial performance they make effective

strategies for development and increase efficiency (Chenhall and Moers, 2015). It is

very important and it makes by management for short term and long term that helpful in

get quick information for decision making. This report will be cover that requirement of

management accounting, methods use in it, planning tools of this accounting, helps of

these tools for solve financial problems.

TASK 1

Meaning and requirement of types of management accounting.

Management accounting is very helpful in make financial report by managers

that useful for decision making because ABC ltd. Evaluate and analyze all report and

books than take decision for meet objective. Data of books and statement that is

prepared so all these documenting s evaluate by managers regarding cost, profit and

saving. So it is very important for ABC ltd for manage all works and activities and

increase profit. Following requirements of management accounting :-

Cost accounting systems :- this system of accounting is very useful for make

estimate of cost. Through this ABC ltd evaluate gap between cost and profit because

organization do all works for earn profit and increase revenue. It is a technique and tool

of reduce production cost of products and fix selling price. Cost accounting system of

past present and future evaluate by managers for making decision about budget,

investment and expand business so that is important for all types of organization.

Inventory management system :- this system of accounting majorly use by

manufacturing organization for trace all activities about stock. Management of ABC ltd

get all information about inventory and movement of stock and products. It includes

product from manufacturing to warehouse and warehouse to shipping. These things

make easy to management of inventory and making decision for increase profitability.

Through this system organization easily track whole supply chain and analyze quantity

of products running in work in progress (Bromwich and Scapens, 2016).

Management accounting is a internal accounting that use by managers for

manage and maintain organization through evolution. Managers of organization

evaluate and analyze books and accounts that helps in make planning, organizing,

directing and controlling. On the bases of financial performance they make effective

strategies for development and increase efficiency (Chenhall and Moers, 2015). It is

very important and it makes by management for short term and long term that helpful in

get quick information for decision making. This report will be cover that requirement of

management accounting, methods use in it, planning tools of this accounting, helps of

these tools for solve financial problems.

TASK 1

Meaning and requirement of types of management accounting.

Management accounting is very helpful in make financial report by managers

that useful for decision making because ABC ltd. Evaluate and analyze all report and

books than take decision for meet objective. Data of books and statement that is

prepared so all these documenting s evaluate by managers regarding cost, profit and

saving. So it is very important for ABC ltd for manage all works and activities and

increase profit. Following requirements of management accounting :-

Cost accounting systems :- this system of accounting is very useful for make

estimate of cost. Through this ABC ltd evaluate gap between cost and profit because

organization do all works for earn profit and increase revenue. It is a technique and tool

of reduce production cost of products and fix selling price. Cost accounting system of

past present and future evaluate by managers for making decision about budget,

investment and expand business so that is important for all types of organization.

Inventory management system :- this system of accounting majorly use by

manufacturing organization for trace all activities about stock. Management of ABC ltd

get all information about inventory and movement of stock and products. It includes

product from manufacturing to warehouse and warehouse to shipping. These things

make easy to management of inventory and making decision for increase profitability.

Through this system organization easily track whole supply chain and analyze quantity

of products running in work in progress (Bromwich and Scapens, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system :- it is very important for those organizations that produce

products according to demand of customers. Different types of peoples demand different

product design and quality so organization face difficulty in costing because it creates

difficulties for organization. So through this system it easily calculates all cost and

revenue of products according to per item. ABC ltd evaluate revenue on per product

because it main purpose is increase revenue and profit always earn more than it cost. On

the bases of this system management of organization take decision easily and make

strategy.

Price optimizing system :- this system of accounting is use by all types of

organization and through this it evaluates that customer reaction according to price of

products. So ABC ltd easily make decision about price and cost of products. Customers

always wants to quality products at low price and if price of product decrease so their

demand increase and organization attract customer through this easily. So management

of organization easily evaluate all things about customers and then provide according to

their choice and demand at reasonable price.

Process costing method :- this costing method use by organization that produce

mass products and organization face difficulties to calculate per unit cost. Products pass

from many process during production so each process contain cost separately. This

method make easy to calculate cost of process.

Different methods of management accounting reporting.

Management accounting is a technique of evaluation of all financial reports and take

decision for expand business and increase investment. Through this it makes budget on

the bases of tax, revenue and expenses. Following are different methods:-

Financial report :- this report includes many types of books and records that

keep by ABC ltd of whole financial year. It includes balance sheet, cash flow statement

and profit and loss account and income statement as well. Management of organization

use this account for evaluation and knows about all operation.

Pro forms cash flow :- this statement helps in keep all data and information

about flow of cash in ABC ltd as per financial year. Cash flow statement includes all

transaction that related to cash. Cash inflow and outflow is two part of this statement if

cash comes organization through sales of products and return on investment that it

products according to demand of customers. Different types of peoples demand different

product design and quality so organization face difficulty in costing because it creates

difficulties for organization. So through this system it easily calculates all cost and

revenue of products according to per item. ABC ltd evaluate revenue on per product

because it main purpose is increase revenue and profit always earn more than it cost. On

the bases of this system management of organization take decision easily and make

strategy.

Price optimizing system :- this system of accounting is use by all types of

organization and through this it evaluates that customer reaction according to price of

products. So ABC ltd easily make decision about price and cost of products. Customers

always wants to quality products at low price and if price of product decrease so their

demand increase and organization attract customer through this easily. So management

of organization easily evaluate all things about customers and then provide according to

their choice and demand at reasonable price.

Process costing method :- this costing method use by organization that produce

mass products and organization face difficulties to calculate per unit cost. Products pass

from many process during production so each process contain cost separately. This

method make easy to calculate cost of process.

Different methods of management accounting reporting.

Management accounting is a technique of evaluation of all financial reports and take

decision for expand business and increase investment. Through this it makes budget on

the bases of tax, revenue and expenses. Following are different methods:-

Financial report :- this report includes many types of books and records that

keep by ABC ltd of whole financial year. It includes balance sheet, cash flow statement

and profit and loss account and income statement as well. Management of organization

use this account for evaluation and knows about all operation.

Pro forms cash flow :- this statement helps in keep all data and information

about flow of cash in ABC ltd as per financial year. Cash flow statement includes all

transaction that related to cash. Cash inflow and outflow is two part of this statement if

cash comes organization through sales of products and return on investment that it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

includes cash inflow and if cash goes out from organization through give dividend and

purchase of raw material so it includes in cash outflow so management of organization

easily evaluate and make decision about invest (Bobryshev, 2015).

Sales report :- this report is very useful for all ABC ltd because this report

includes all data about sales of products. Through this it evaluates that sales increase

sources that helps in increase source and also analyze whole seller and retailer.

Management accounting make decision about efficient source of sales. It also motivates

through provide incentives and bonus to different sellers. That helps in motivate to

them.

Benefits of management accounting systems.

Management accounting is very important for organization because through this

it easily evaluates all cost and financial activities for making effective and efficient

decision about increase profit and expand business. Job costing system helps in

calculates easily cost of different products because without this system it is very lengthy

process. Cost accounting system helpful for evaluate cost and reduce cost that helps in

increase profit. Price optimization system is important for evaluate customers reaction

and know about their interest with price of products. All things are important for

management accounting because management of ABC ltd compare easily profit is more

than cost or not. It also makes decision according to situation for investment and expand

business (Nielsen, Mitchell and Nørreklit, 2015).

System and reports of management accounting integrated with organization.

Management accounting system is tool of control on cost and effectively manage

all activities that increase profit and revenue of organization. Through systems of this

accounting managers making effective decision for profitability. So they make decisions

after comparison of past present and future estimates of cost reports. Overall it useful for

making decision.

Management accounting reports use by organization and through reports like

cash flow statements, financial reports and income statement they compare all cost.

Through this it easily evaluates that profit earn by organization proper or not according

to cost incur in production and shipping.

purchase of raw material so it includes in cash outflow so management of organization

easily evaluate and make decision about invest (Bobryshev, 2015).

Sales report :- this report is very useful for all ABC ltd because this report

includes all data about sales of products. Through this it evaluates that sales increase

sources that helps in increase source and also analyze whole seller and retailer.

Management accounting make decision about efficient source of sales. It also motivates

through provide incentives and bonus to different sellers. That helps in motivate to

them.

Benefits of management accounting systems.

Management accounting is very important for organization because through this

it easily evaluates all cost and financial activities for making effective and efficient

decision about increase profit and expand business. Job costing system helps in

calculates easily cost of different products because without this system it is very lengthy

process. Cost accounting system helpful for evaluate cost and reduce cost that helps in

increase profit. Price optimization system is important for evaluate customers reaction

and know about their interest with price of products. All things are important for

management accounting because management of ABC ltd compare easily profit is more

than cost or not. It also makes decision according to situation for investment and expand

business (Nielsen, Mitchell and Nørreklit, 2015).

System and reports of management accounting integrated with organization.

Management accounting system is tool of control on cost and effectively manage

all activities that increase profit and revenue of organization. Through systems of this

accounting managers making effective decision for profitability. So they make decisions

after comparison of past present and future estimates of cost reports. Overall it useful for

making decision.

Management accounting reports use by organization and through reports like

cash flow statements, financial reports and income statement they compare all cost.

Through this it easily evaluates that profit earn by organization proper or not according

to cost incur in production and shipping.

TASK 2

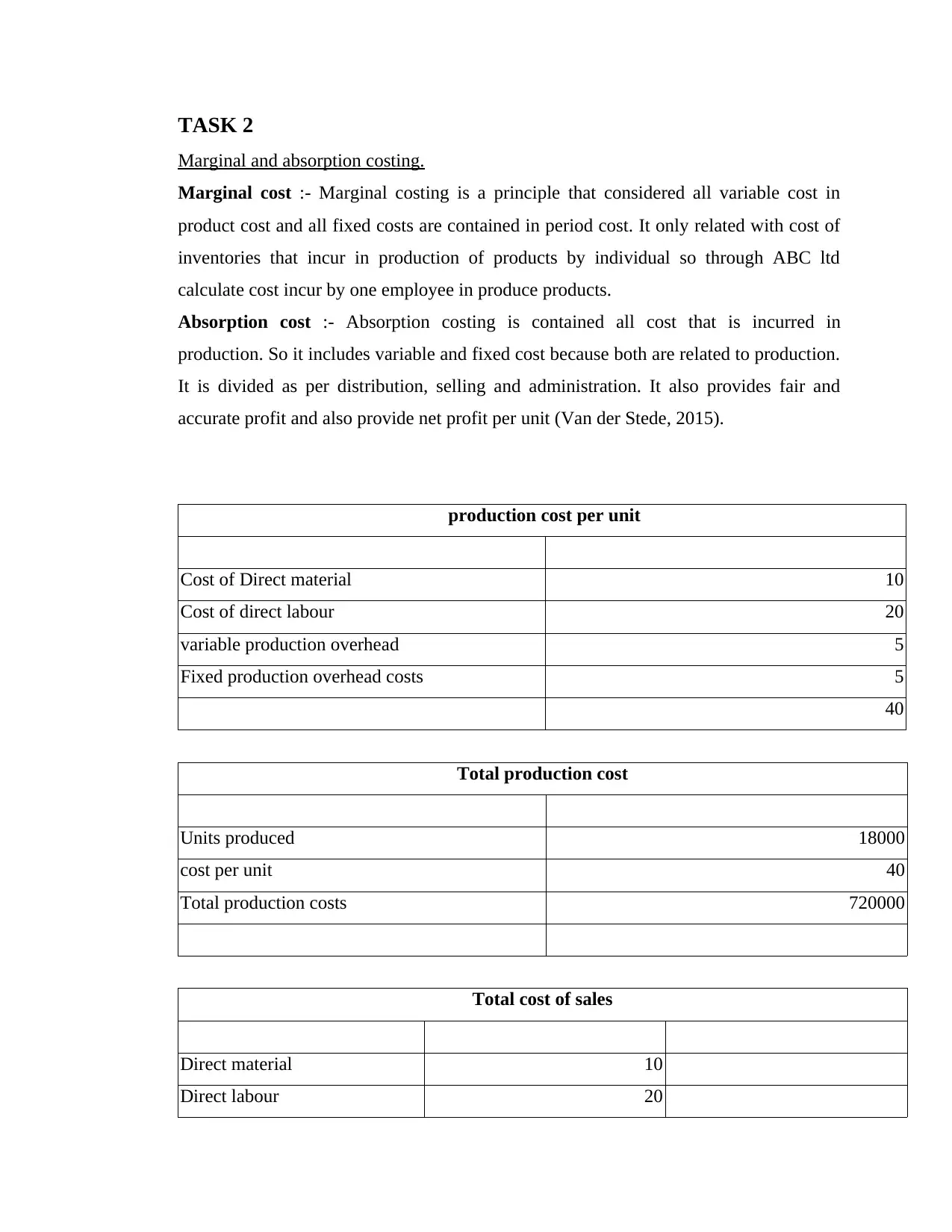

Marginal and absorption costing.

Marginal cost :- Marginal costing is a principle that considered all variable cost in

product cost and all fixed costs are contained in period cost. It only related with cost of

inventories that incur in production of products by individual so through ABC ltd

calculate cost incur by one employee in produce products.

Absorption cost :- Absorption costing is contained all cost that is incurred in

production. So it includes variable and fixed cost because both are related to production.

It is divided as per distribution, selling and administration. It also provides fair and

accurate profit and also provide net profit per unit (Van der Stede, 2015).

production cost per unit

Cost of Direct material 10

Cost of direct labour 20

variable production overhead 5

Fixed production overhead costs 5

40

Total production cost

Units produced 18000

cost per unit 40

Total production costs 720000

Total cost of sales

Direct material 10

Direct labour 20

Marginal and absorption costing.

Marginal cost :- Marginal costing is a principle that considered all variable cost in

product cost and all fixed costs are contained in period cost. It only related with cost of

inventories that incur in production of products by individual so through ABC ltd

calculate cost incur by one employee in produce products.

Absorption cost :- Absorption costing is contained all cost that is incurred in

production. So it includes variable and fixed cost because both are related to production.

It is divided as per distribution, selling and administration. It also provides fair and

accurate profit and also provide net profit per unit (Van der Stede, 2015).

production cost per unit

Cost of Direct material 10

Cost of direct labour 20

variable production overhead 5

Fixed production overhead costs 5

40

Total production cost

Units produced 18000

cost per unit 40

Total production costs 720000

Total cost of sales

Direct material 10

Direct labour 20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

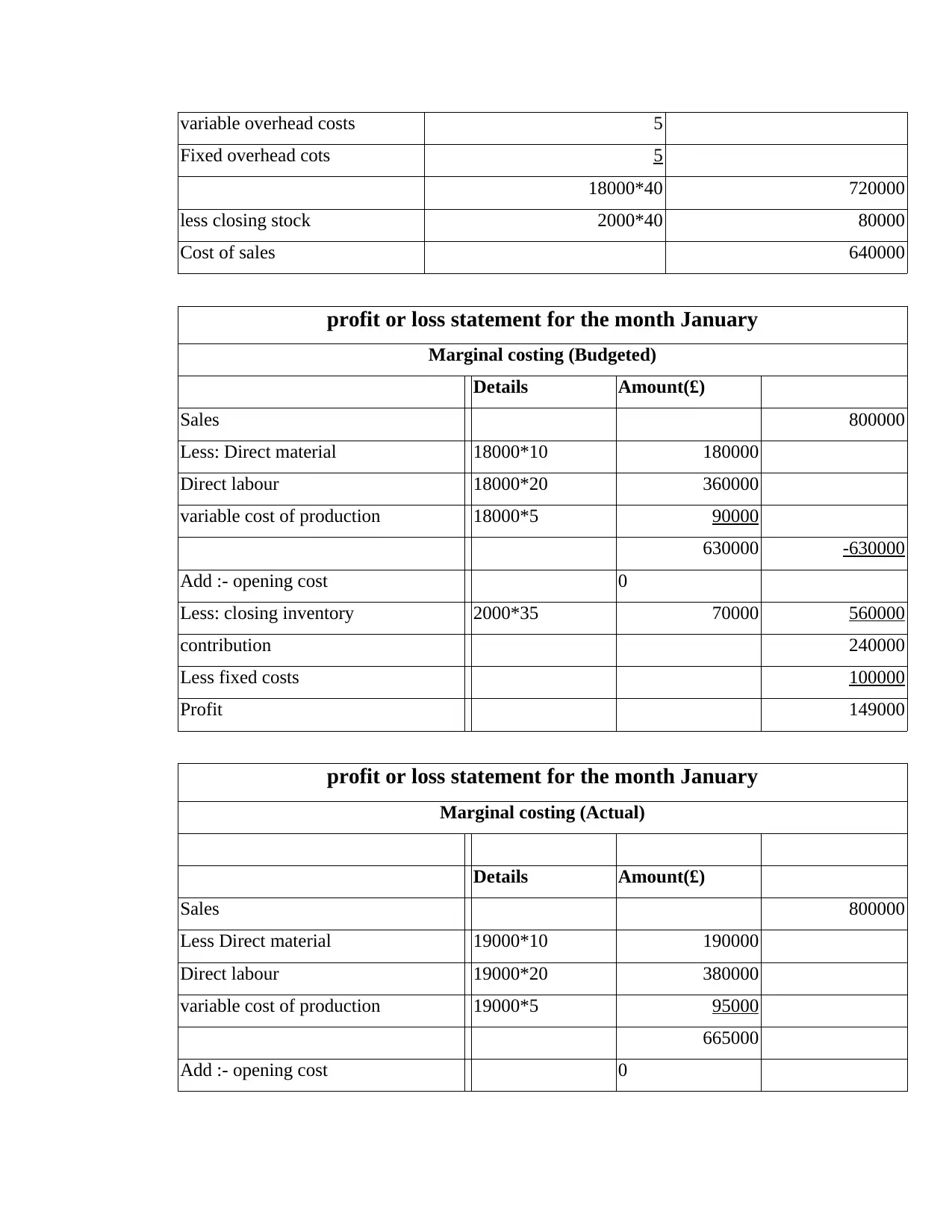

variable overhead costs 5

Fixed overhead cots 5

18000*40 720000

less closing stock 2000*40 80000

Cost of sales 640000

profit or loss statement for the month January

Marginal costing (Budgeted)

Details Amount(£)

Sales 800000

Less: Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of production 18000*5 90000

630000 -630000

Add :- opening cost 0

Less: closing inventory 2000*35 70000 560000

contribution 240000

Less fixed costs 100000

Profit 149000

profit or loss statement for the month January

Marginal costing (Actual)

Details Amount(£)

Sales 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of production 19000*5 95000

665000

Add :- opening cost 0

Fixed overhead cots 5

18000*40 720000

less closing stock 2000*40 80000

Cost of sales 640000

profit or loss statement for the month January

Marginal costing (Budgeted)

Details Amount(£)

Sales 800000

Less: Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of production 18000*5 90000

630000 -630000

Add :- opening cost 0

Less: closing inventory 2000*35 70000 560000

contribution 240000

Less fixed costs 100000

Profit 149000

profit or loss statement for the month January

Marginal costing (Actual)

Details Amount(£)

Sales 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of production 19000*5 95000

665000

Add :- opening cost 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: closing inventory 3000*35 105000 560000

contribution 24000

Less fixed cost of production 100000

Profit . 140000

Interpretation:- from the above table I interpreted that actual profit is less than

expected profit because organization has budget and plan for produce 18000 units of

products and it produces 19000 units of products that these things direct effect it profits

and overall cost of production increase that net profit decrease. So budget is very

important accurately that helps in manage all cost and profit of organization.

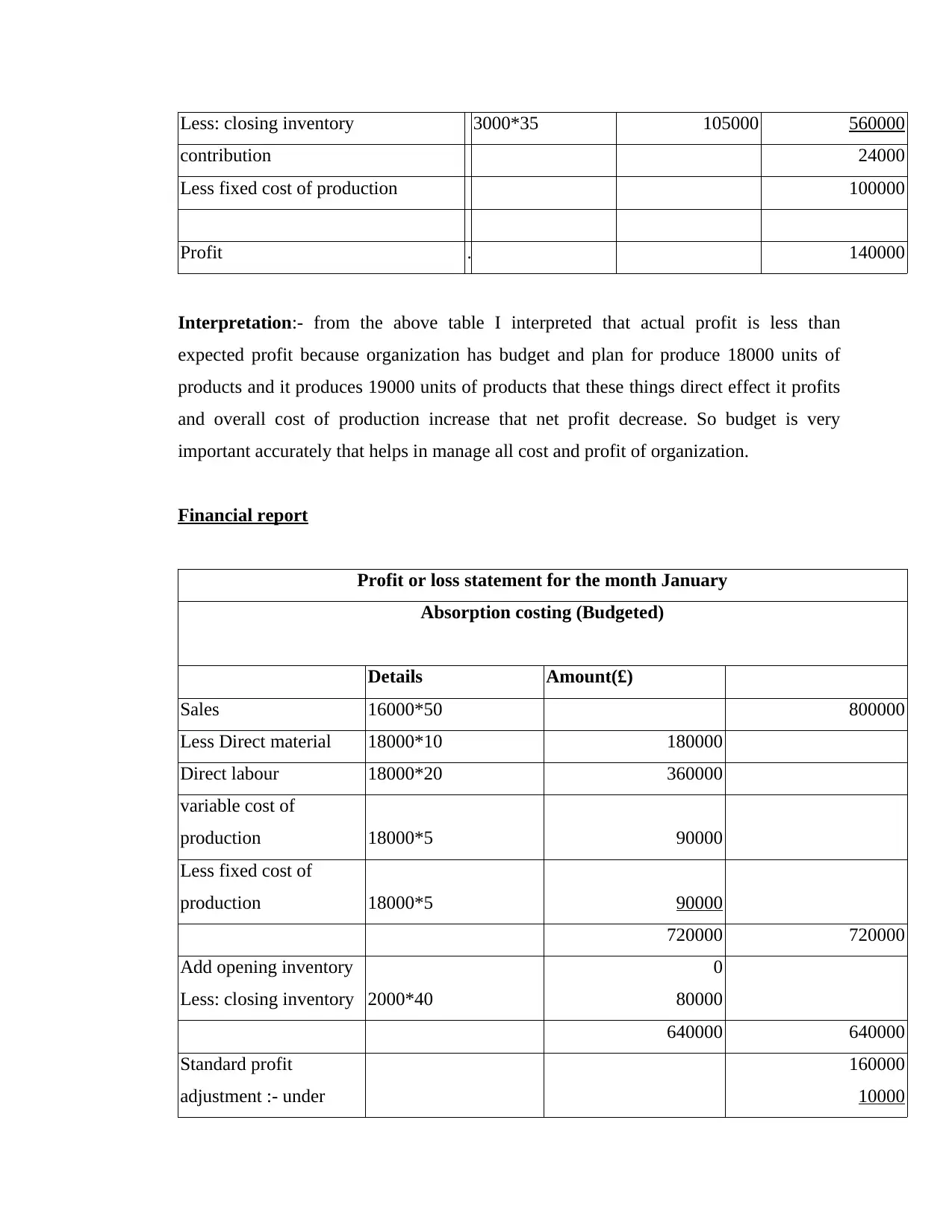

Financial report

Profit or loss statement for the month January

Absorption costing (Budgeted)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of

production 18000*5 90000

Less fixed cost of

production 18000*5 90000

720000 720000

Add opening inventory

Less: closing inventory 2000*40

0

80000

640000 640000

Standard profit

adjustment :- under

160000

10000

contribution 24000

Less fixed cost of production 100000

Profit . 140000

Interpretation:- from the above table I interpreted that actual profit is less than

expected profit because organization has budget and plan for produce 18000 units of

products and it produces 19000 units of products that these things direct effect it profits

and overall cost of production increase that net profit decrease. So budget is very

important accurately that helps in manage all cost and profit of organization.

Financial report

Profit or loss statement for the month January

Absorption costing (Budgeted)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 18000*10 180000

Direct labour 18000*20 360000

variable cost of

production 18000*5 90000

Less fixed cost of

production 18000*5 90000

720000 720000

Add opening inventory

Less: closing inventory 2000*40

0

80000

640000 640000

Standard profit

adjustment :- under

160000

10000

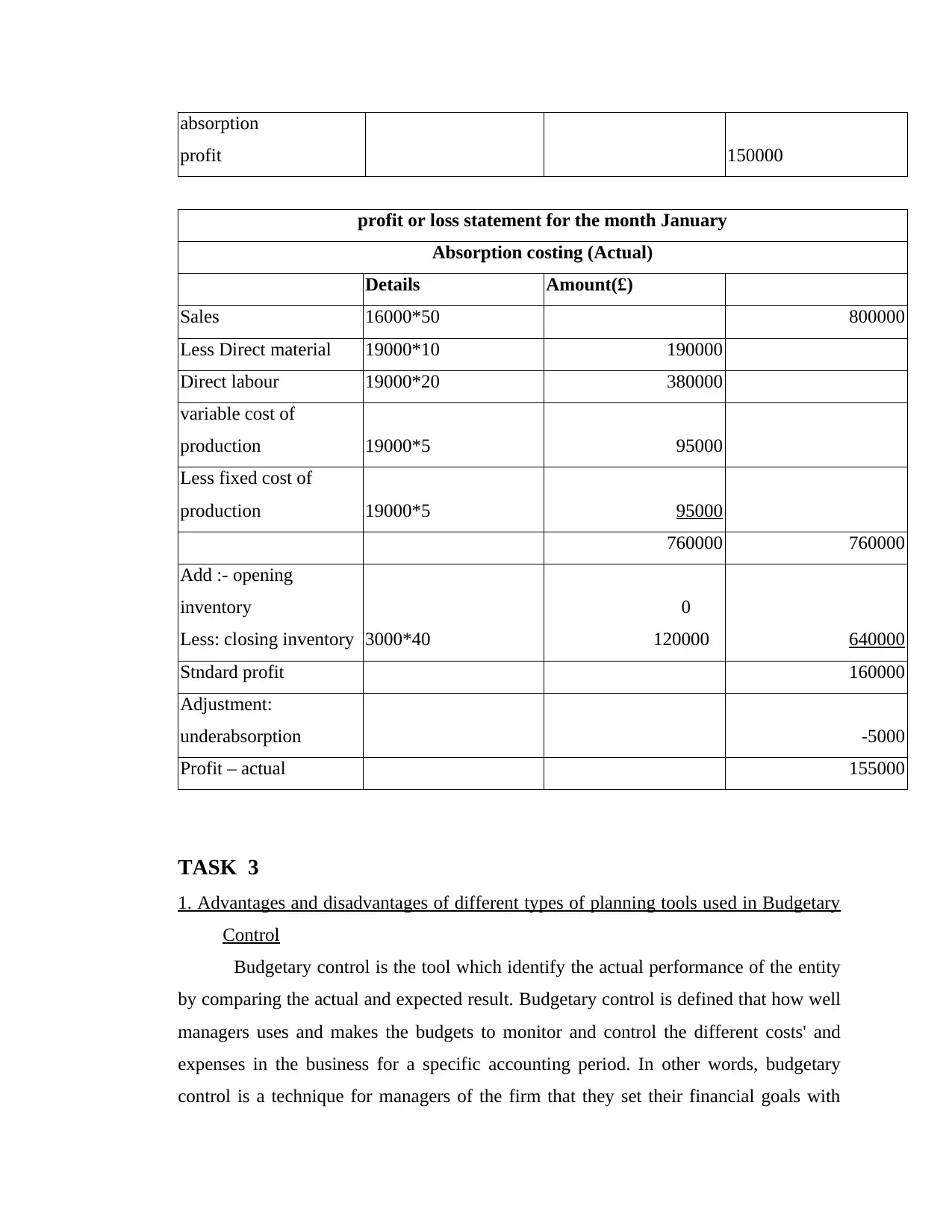

absorption

profit 150000

profit or loss statement for the month January

Absorption costing (Actual)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of

production 19000*5 95000

Less fixed cost of

production 19000*5 95000

760000 760000

Add :- opening

inventory

Less: closing inventory 3000*40

0

120000 640000

Stndard profit 160000

Adjustment:

underabsorption -5000

Profit – actual 155000

TASK 3

1. Advantages and disadvantages of different types of planning tools used in Budgetary

Control

Budgetary control is the tool which identify the actual performance of the entity

by comparing the actual and expected result. Budgetary control is defined that how well

managers uses and makes the budgets to monitor and control the different costs' and

expenses in the business for a specific accounting period. In other words, budgetary

control is a technique for managers of the firm that they set their financial goals with

profit 150000

profit or loss statement for the month January

Absorption costing (Actual)

Details Amount(£)

Sales 16000*50 800000

Less Direct material 19000*10 190000

Direct labour 19000*20 380000

variable cost of

production 19000*5 95000

Less fixed cost of

production 19000*5 95000

760000 760000

Add :- opening

inventory

Less: closing inventory 3000*40

0

120000 640000

Stndard profit 160000

Adjustment:

underabsorption -5000

Profit – actual 155000

TASK 3

1. Advantages and disadvantages of different types of planning tools used in Budgetary

Control

Budgetary control is the tool which identify the actual performance of the entity

by comparing the actual and expected result. Budgetary control is defined that how well

managers uses and makes the budgets to monitor and control the different costs' and

expenses in the business for a specific accounting period. In other words, budgetary

control is a technique for managers of the firm that they set their financial goals with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budgets, managers can compare the actual performance with expected performance and

adjust budget accordingly as it is needed.

Activity based budgeting

Activity based is the budgeting method firms can use this method to prepared

their budget. Activity Based Budgeting method define the overall cost of business

activity it is also included the overhead activities of the business and also contains the

associated costs of the business. It is a tool which maintain all the financial records and

analyses the activities that increase the costs of the business. Each department of the

business has incurred the costs of different activities by measuring the number of units

of cost driver for the expected activity level. Budgets are prepared by the manager of the

firm they make the budget on the basis of results.

Advantages

It provides real value of costs for the manufacturing of the particular products.

Activity-based budget focuses on managing activities of the firm to reduce costs.

This technique identifying a business indirect cost activities.

It helps to identify the profits margins of the particular product.

It discovers the processes that are unnecessary and have wasted costed.

It provides accurate value of costing and this method is easy for applying

It helps to Identify the activities and their cost drivers.

It helps to forecast the number of sales and number of unit orders for the budget

period

Disadvantages

This process is costly as well as time-consuming it includes the more time for

collection of date and take time for preparation of data.

The collection of data is sometimes is accurate it leads the cost.

The collection and sources of data is not suddenly available from accounting

reports. This requires more research in order to collection the data.

Sometimes this not be important for small organization because the overhead is

small in ratio to total operating costs

Zero based budgeting

adjust budget accordingly as it is needed.

Activity based budgeting

Activity based is the budgeting method firms can use this method to prepared

their budget. Activity Based Budgeting method define the overall cost of business

activity it is also included the overhead activities of the business and also contains the

associated costs of the business. It is a tool which maintain all the financial records and

analyses the activities that increase the costs of the business. Each department of the

business has incurred the costs of different activities by measuring the number of units

of cost driver for the expected activity level. Budgets are prepared by the manager of the

firm they make the budget on the basis of results.

Advantages

It provides real value of costs for the manufacturing of the particular products.

Activity-based budget focuses on managing activities of the firm to reduce costs.

This technique identifying a business indirect cost activities.

It helps to identify the profits margins of the particular product.

It discovers the processes that are unnecessary and have wasted costed.

It provides accurate value of costing and this method is easy for applying

It helps to Identify the activities and their cost drivers.

It helps to forecast the number of sales and number of unit orders for the budget

period

Disadvantages

This process is costly as well as time-consuming it includes the more time for

collection of date and take time for preparation of data.

The collection of data is sometimes is accurate it leads the cost.

The collection and sources of data is not suddenly available from accounting

reports. This requires more research in order to collection the data.

Sometimes this not be important for small organization because the overhead is

small in ratio to total operating costs

Zero based budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based budgeting is another tool of budgeting which describe that the budget

is starts from the zero base which means the budget of all expenses and cost are

Equitable individually in each period (What is Zero Based Budgeting (ZBB)?, 2018 ). In

other words, the zero based budget is starts form the Zero base and each activity within

an organization is analyzed ad identify for its needs and costs.

Advantages

This process helps to identify the decision units.

This process is determining and allocate available resources. This process

focuses on uses of resources.

helps to eliminating the waste.

it leads to employee involvements so it helps to collect more information.

Disadvantages

This process is costly because it leads paper work

Its only focus on short term planning not focus on long term planning

Small business cannot use this method because it costly and time-consuming

Incremental Budgeting

incremental budgeting is also another way of making the budget. It is a budget

which is based on the preceding period's. This budget compare the expected budget to

actual budget to identify the cost of activity. It is most common approach that every firm

can use this approach to identify the overall cost activity of the business. Furthermore,

where businesses are not spent too much amount for formulating budgets. So firms

commonly use this method in their business to generate the profits.

Advantages

This method is very easy to adopt and also this is the easiest method as compare

to other methods.

Funding will continue in this method because it requires the limit fluctuations in

allocation of funds

Disadvantages

This budgeting method does not encourage innovation because it only considers

the previous year data.

This method is not identified the real expenses.

is starts from the zero base which means the budget of all expenses and cost are

Equitable individually in each period (What is Zero Based Budgeting (ZBB)?, 2018 ). In

other words, the zero based budget is starts form the Zero base and each activity within

an organization is analyzed ad identify for its needs and costs.

Advantages

This process helps to identify the decision units.

This process is determining and allocate available resources. This process

focuses on uses of resources.

helps to eliminating the waste.

it leads to employee involvements so it helps to collect more information.

Disadvantages

This process is costly because it leads paper work

Its only focus on short term planning not focus on long term planning

Small business cannot use this method because it costly and time-consuming

Incremental Budgeting

incremental budgeting is also another way of making the budget. It is a budget

which is based on the preceding period's. This budget compare the expected budget to

actual budget to identify the cost of activity. It is most common approach that every firm

can use this approach to identify the overall cost activity of the business. Furthermore,

where businesses are not spent too much amount for formulating budgets. So firms

commonly use this method in their business to generate the profits.

Advantages

This method is very easy to adopt and also this is the easiest method as compare

to other methods.

Funding will continue in this method because it requires the limit fluctuations in

allocation of funds

Disadvantages

This budgeting method does not encourage innovation because it only considers

the previous year data.

This method is not identified the real expenses.

The previous problem in budget is build the problem in current year budget.

2. Use of different planning tools and their application for preparing and forecasting

budgets.

Cash Budgeting

Cash budgeting is a budget which identify the income and cash expenditure that

is includes revenue and capital items. Cash Flow Budget should be prepared on the

basis of cash inflow and cash outflow. When cash is high which means the inflow of

cash is also high and in other side the cash flow is low so the outflow of cash is high. So

mainly cash budgeting is focuses on inflows and outflows of cash. It shows that the high

cash flows arising of the operational budgets. Furthermore, The main motive of any

entity is to maximize profits and generate high profit margin so firm makes proper

financial planning to achieve the objective and goal. Cash budget is effectively managed

Working Capital in the financial report of the firm also it is effectively managed by

preparation of cash budget. There are three types of cash budgeting.

Adjusted income method

Adjusted cash budget is calculated for managing the sales and revenue.

managers adjust the annual cash in flow and outflow by calculating the receipts and

payments. This method helps to identify the sales revenues and cost figures. So firm

can use this method to maintain their cash flows also eliminating non-cash items like

depreciation.

Adjusted balance sheet method

Adjusted balance sheet is calculate liabilities and assets of the firm. Company

makes the balance sheet to identify the weight of assets and liabilities. Increase in

liabilities and assets is affect the performance of business. Also, affect the owner's

equity and can be foretasted by the adjusted balance sheet method.

Receipts and payments

Receipts and payments it describes that high cash inflow is included in Receipts

and high cash outflow is contains in payments.

Sales budget.

Sales Budgeting is identified the sale of particular product it refers to a primary

forecast of sales. When sales is high its generate the high income and when sales Is low

2. Use of different planning tools and their application for preparing and forecasting

budgets.

Cash Budgeting

Cash budgeting is a budget which identify the income and cash expenditure that

is includes revenue and capital items. Cash Flow Budget should be prepared on the

basis of cash inflow and cash outflow. When cash is high which means the inflow of

cash is also high and in other side the cash flow is low so the outflow of cash is high. So

mainly cash budgeting is focuses on inflows and outflows of cash. It shows that the high

cash flows arising of the operational budgets. Furthermore, The main motive of any

entity is to maximize profits and generate high profit margin so firm makes proper

financial planning to achieve the objective and goal. Cash budget is effectively managed

Working Capital in the financial report of the firm also it is effectively managed by

preparation of cash budget. There are three types of cash budgeting.

Adjusted income method

Adjusted cash budget is calculated for managing the sales and revenue.

managers adjust the annual cash in flow and outflow by calculating the receipts and

payments. This method helps to identify the sales revenues and cost figures. So firm

can use this method to maintain their cash flows also eliminating non-cash items like

depreciation.

Adjusted balance sheet method

Adjusted balance sheet is calculate liabilities and assets of the firm. Company

makes the balance sheet to identify the weight of assets and liabilities. Increase in

liabilities and assets is affect the performance of business. Also, affect the owner's

equity and can be foretasted by the adjusted balance sheet method.

Receipts and payments

Receipts and payments it describes that high cash inflow is included in Receipts

and high cash outflow is contains in payments.

Sales budget.

Sales Budgeting is identified the sale of particular product it refers to a primary

forecast of sales. When sales is high its generate the high income and when sales Is low

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.