Management Accounting Principles Report for Business Students

VerifiedAdded on 2023/01/10

|15

|1088

|49

Report

AI Summary

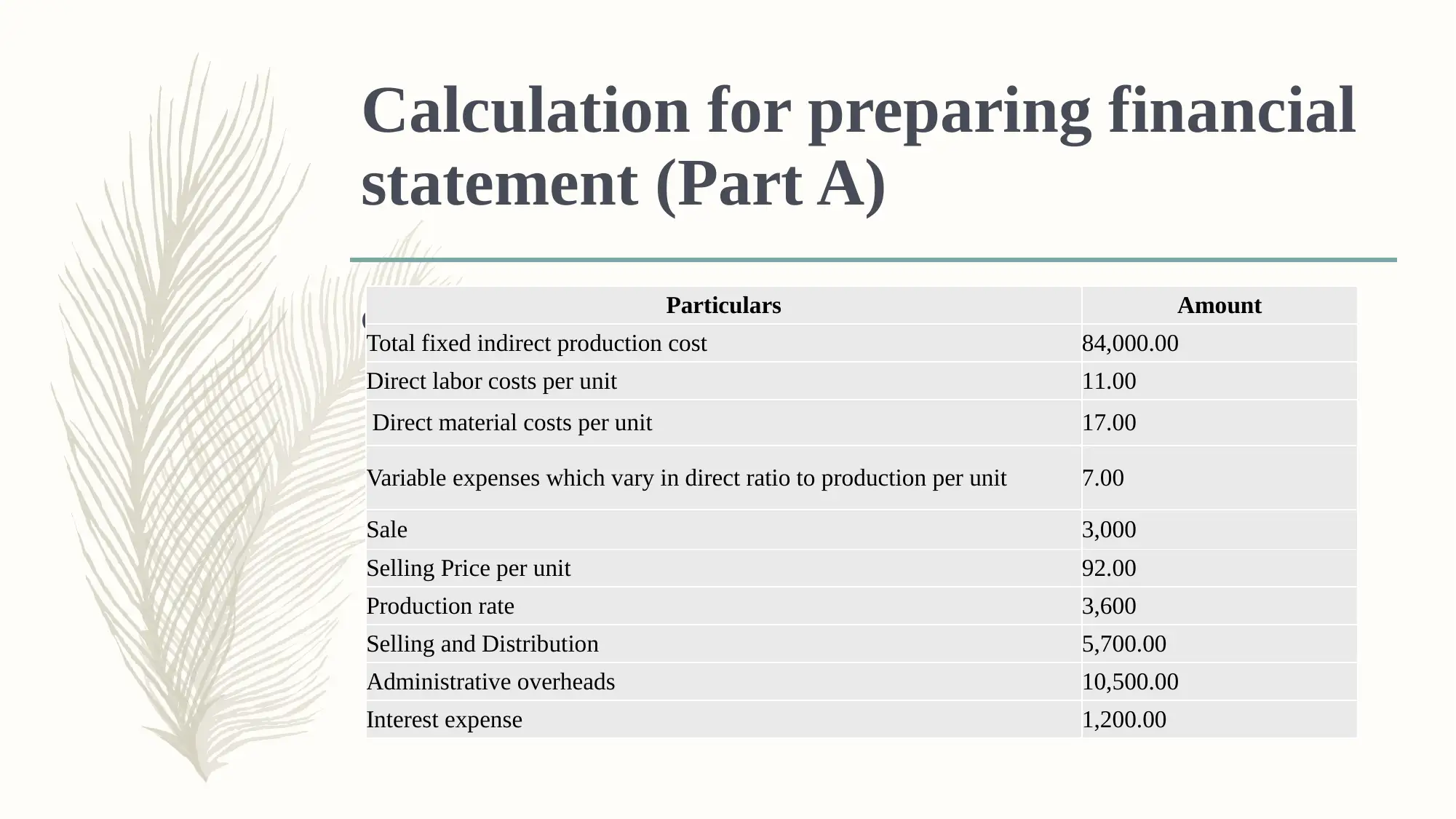

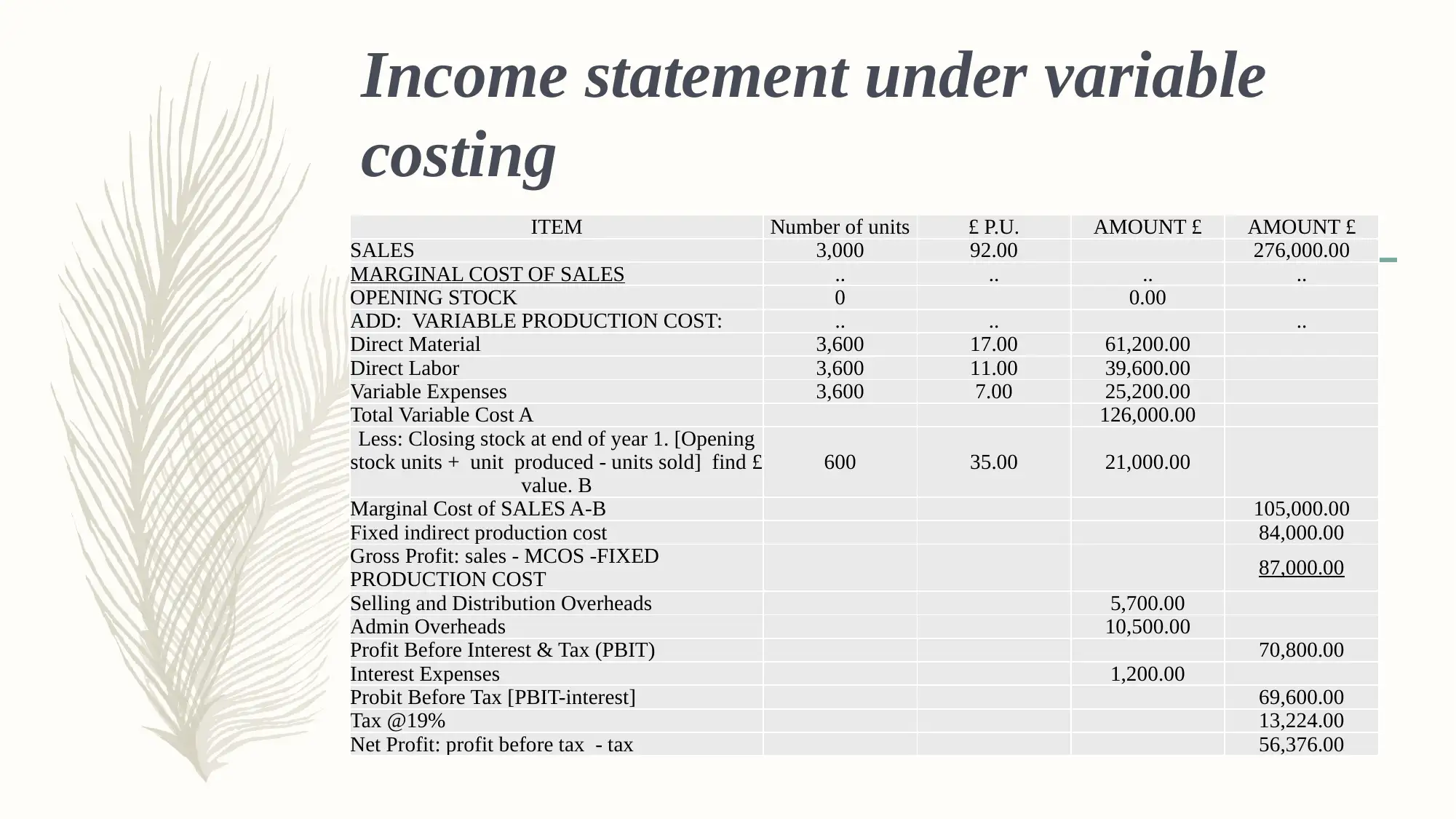

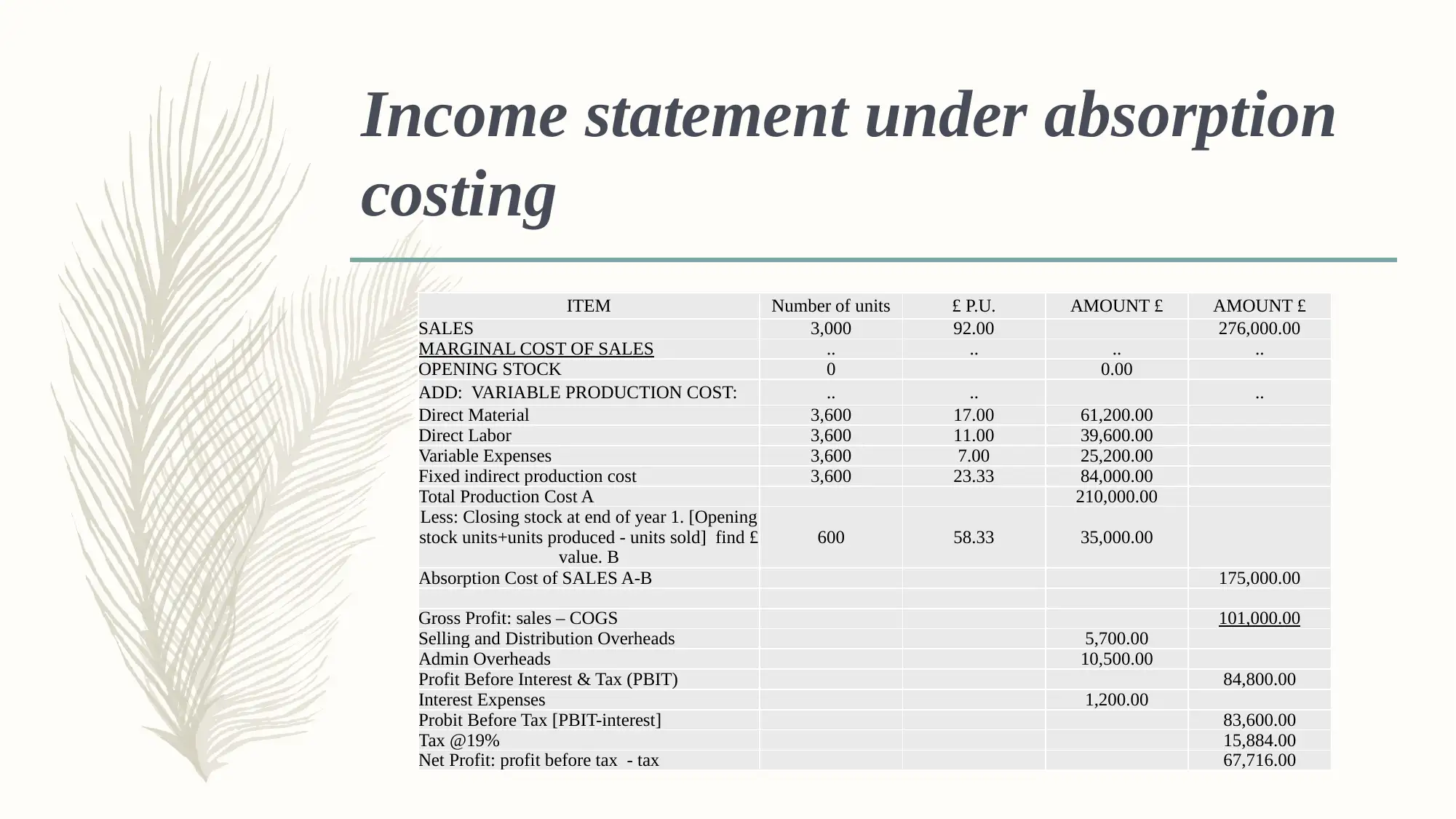

This report delves into the core principles of management accounting, providing a detailed analysis of financial statements and costing methods. It begins with an introduction to management accounting, emphasizing its role in decision-making and its integration within organizations. The report then presents calculations for preparing financial statements, including income statements under both variable and absorption costing methods. It outlines the principles of management accounting, discussing key concepts such as influence, relevance, value, and credibility. The report also explores the roles of management accounting and management accounting systems, including cost accounting, inventory management, price optimization, and job costing systems. Various management accounting reports are examined, along with the methods employed in preparing income statements. The benefits of key functions within these systems are discussed, and the report concludes by highlighting the significance of managerial accounting for corporate business enterprises. The report is based on the assignment brief for BTEC Higher National Certificate in Business and includes references to support the analysis. The report is contributed by a student to be published on the website Desklib.

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.