Management Accounting Systems and Techniques Report, BTEC - Unit 5

VerifiedAdded on 2023/01/03

|16

|3982

|97

Report

AI Summary

This report delves into the core concepts of management accounting, exploring its role in facilitating critical business decision-making. The report uses Capital Joinery Ltd as a case study, examining various management accounting systems, including cost accounting, stock management, job costing, and price optimization. It differentiates between absorption and marginal costing methods, providing income statements and reconciliation statements. The report also analyzes different types of budgets, such as sales budgets, cash budgets, and zero-based budgets, and their advantages and disadvantages. Furthermore, it covers material variance calculations and inventory valuation methods like LIFO and average cost methods. The report highlights the significance of management accounting reports, including account receivable reports, budgetary reports, and performance reports, for effective financial control and strategic planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1...........................................................................................................................................3

P1.................................................................................................................................................3

P2.................................................................................................................................................5

Task 2...........................................................................................................................................6

P3.................................................................................................................................................6

Task 3...........................................................................................................................................9

P4.................................................................................................................................................9

Task 4.........................................................................................................................................12

P5...............................................................................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1...........................................................................................................................................3

P1.................................................................................................................................................3

P2.................................................................................................................................................5

Task 2...........................................................................................................................................6

P3.................................................................................................................................................6

Task 3...........................................................................................................................................9

P4.................................................................................................................................................9

Task 4.........................................................................................................................................12

P5...............................................................................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INTRODUCTION

Management accounting is a term that defines a systematic system for systematically reporting

the collection of financial statistical analysis and justification to facilitate critical business

decision-making for the internal position (Cooper, Ezzamel and Qu, 2017). The value of

Accounting Systems has been introduced to explain the need for assistance. Capital Joinery Ltd.,

it manufactures a wide range of joinery, helped make gates, frames, etc., is the business chosen

for the project. The study established the significance of the MAS and the application of steps for

the estimation or quantification of benefit prices, which also include the criteria for the

forecasting method for a theoretical framework to this judgement, as well as the preparation of

budget managers in the use of performance testing as well as other accounting practices to deal

with the fiscal challenge.

MAIN BODY

Task 1

P1

MA is a fusion of 2 concepts that describe management as a process for business activities to be

coordinated, organised, managed and supervised. Accounting, on the other hand, is regarded as a

systematic method of records management for collecting and recording accounting documents.

MA is a structured term used to present accounting information regularly to achieve the aims of

multinational organisations (Malmi, 2016). This is designed to resolve the problem of cost

increases, non-specific accounting records, the determination of the right approach, the

judgement process and the optimal utilisation of projects and providing pertaining to the

accounting industry. Often highlighted as an essential part of reporting, cost reporting is only

essential for economic transfers.

Cost accounting system- For marketing products, the overall accounting management technique

is taken into account to identify expenses incurred for running business activities, earning profit.

In order to calculate costs, the boss will use many methods: marginal, accumulation, dependent,

and standard costing. Capital Joinery Ltd uses nominal and even standard costing methods in

calculating benefit and understanding the influence of per provides expert change on profit. This

Management accounting is a term that defines a systematic system for systematically reporting

the collection of financial statistical analysis and justification to facilitate critical business

decision-making for the internal position (Cooper, Ezzamel and Qu, 2017). The value of

Accounting Systems has been introduced to explain the need for assistance. Capital Joinery Ltd.,

it manufactures a wide range of joinery, helped make gates, frames, etc., is the business chosen

for the project. The study established the significance of the MAS and the application of steps for

the estimation or quantification of benefit prices, which also include the criteria for the

forecasting method for a theoretical framework to this judgement, as well as the preparation of

budget managers in the use of performance testing as well as other accounting practices to deal

with the fiscal challenge.

MAIN BODY

Task 1

P1

MA is a fusion of 2 concepts that describe management as a process for business activities to be

coordinated, organised, managed and supervised. Accounting, on the other hand, is regarded as a

systematic method of records management for collecting and recording accounting documents.

MA is a structured term used to present accounting information regularly to achieve the aims of

multinational organisations (Malmi, 2016). This is designed to resolve the problem of cost

increases, non-specific accounting records, the determination of the right approach, the

judgement process and the optimal utilisation of projects and providing pertaining to the

accounting industry. Often highlighted as an essential part of reporting, cost reporting is only

essential for economic transfers.

Cost accounting system- For marketing products, the overall accounting management technique

is taken into account to identify expenses incurred for running business activities, earning profit.

In order to calculate costs, the boss will use many methods: marginal, accumulation, dependent,

and standard costing. Capital Joinery Ltd uses nominal and even standard costing methods in

calculating benefit and understanding the influence of per provides expert change on profit. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting method can be extended and important to them in the sense of limited capital joinery.

This is so they can categorise the costs of fixing door etc. with the aid of such a method. They

will categorise the cost of raw materials, the cost of work in progress and much more. Via this

they would be able to grasp the expense of absorbing larger costs.

Stock management system- Indeed, inventory is an important organisational product, stock

management helps expected returns misuse and reduces the cost of these stocks being controlled.

Through the use of these MAS, like EOQ, JIT, companies may manage the inventory ratio,

helping to determine the optimum amount of inventory required for storage (Otley, 2016). With

LIFO, FIFO methodology is applied in Capital Joinery Ltd., the selling stock rate can be

calculated. It also is helpful for the estimation of the average, maximum and safe framework of

the stock. In the case of the above-mentioned business, the need for additional raw materials to

manufacture more furniture pieces may be calculated on the basis of such an accounting method.

They will become informed about what types of goods are kept in warehouses and what types of

products are expected to be manufactured to fulfil consumer needs.

Job costing system- Usually, this MAS approach is used to describe the unit cost necessary for

goods that process ore. It helps to identify the necessity of customer order, log, quantity of orders

received, expense, scheduling needed for the production of goods. This methodology is used by

the applicable chosen business to calculate market demand. This accounting is important for

small capital joinery above to monitor the costs of operation that is used over a period or

reporting period of their activities to manufacture doors as well as other soft furnishings.

Price optimization system- After incorporating this structure within the enterprise, administrators

are able to select the best pricing strategy for their products. Price skimming, penetration, and

discounting are also used as a tool for determining the importance of a single well's price.

Competitive nature of the firm applies to the organisation policy they adopt, the business model

that is successful in assessing better profit margins and obtaining a reasonable price edge. Capital

Joinery Ltd uses to control its share of the market. Thus, as per the target requirement, they

decide the price of each good. Consumers are grouped into discrete units, loyal, prospective, nice

standard consumers. They use diffusion pricing strategies for the new goods and other services

This is so they can categorise the costs of fixing door etc. with the aid of such a method. They

will categorise the cost of raw materials, the cost of work in progress and much more. Via this

they would be able to grasp the expense of absorbing larger costs.

Stock management system- Indeed, inventory is an important organisational product, stock

management helps expected returns misuse and reduces the cost of these stocks being controlled.

Through the use of these MAS, like EOQ, JIT, companies may manage the inventory ratio,

helping to determine the optimum amount of inventory required for storage (Otley, 2016). With

LIFO, FIFO methodology is applied in Capital Joinery Ltd., the selling stock rate can be

calculated. It also is helpful for the estimation of the average, maximum and safe framework of

the stock. In the case of the above-mentioned business, the need for additional raw materials to

manufacture more furniture pieces may be calculated on the basis of such an accounting method.

They will become informed about what types of goods are kept in warehouses and what types of

products are expected to be manufactured to fulfil consumer needs.

Job costing system- Usually, this MAS approach is used to describe the unit cost necessary for

goods that process ore. It helps to identify the necessity of customer order, log, quantity of orders

received, expense, scheduling needed for the production of goods. This methodology is used by

the applicable chosen business to calculate market demand. This accounting is important for

small capital joinery above to monitor the costs of operation that is used over a period or

reporting period of their activities to manufacture doors as well as other soft furnishings.

Price optimization system- After incorporating this structure within the enterprise, administrators

are able to select the best pricing strategy for their products. Price skimming, penetration, and

discounting are also used as a tool for determining the importance of a single well's price.

Competitive nature of the firm applies to the organisation policy they adopt, the business model

that is successful in assessing better profit margins and obtaining a reasonable price edge. Capital

Joinery Ltd uses to control its share of the market. Thus, as per the target requirement, they

decide the price of each good. Consumers are grouped into discrete units, loyal, prospective, nice

standard consumers. They use diffusion pricing strategies for the new goods and other services

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

only as they switch into different target markets. They fixed prices for their various types of

furniture pieces as per the results received from markets and customer request in the sense of the

above business.

P2

Management accounting reports- Such reports are essential components of the management

accounting practices in which strategic actions are made by managers. Along with these records,

the monetary and non activities of the companies are generated by means of assistance (Hopper

and Bui, 2016). Like the company Capital Joinery Ltd, they compile various kinds of papers,

which are listed underneath:

Account receivable report: Receivable accounts log is a significant report and was known to be

among the most personal data of such an account business if creditor data gathering reports is

expected. This analysis was used to identify restructuring debt holders that converted the

business's poor credit reserves.

Budgetary report: It is structured to provide a structure for the development of the budget.

Managers draught this study by collecting data from all the documents they have generated. The

financial statements help include guidance for evaluating the competitive situation and strategies

of the company. With the ever retail sector, the manager of Capital Journey Ltd used the budget

document to identify future growth opportunities.

Inventory management report: This paper is written on the basis of data gathered from inventory

control. The key reason for the introduction of this study helps to determine the total required

stock production, maintenance expenses and judgement of future stock supply.

Performance report: This paper is the most critical aspect that each company needs for

formulations. It is also helpful for providing details regarding each firm's outcomes. Often on the

framework of identifying and measuring performance, managers will devise compensation

strategies and take action on organizational rewards on the basis of reviewing this paper. Capital

Journey Ltd has more than 500 employees and is a multinational company. For the chief

executive, the report card is largely focused on something that can track the level of

accomplishment within each section of employees and formulate policies for their planning and

development.

furniture pieces as per the results received from markets and customer request in the sense of the

above business.

P2

Management accounting reports- Such reports are essential components of the management

accounting practices in which strategic actions are made by managers. Along with these records,

the monetary and non activities of the companies are generated by means of assistance (Hopper

and Bui, 2016). Like the company Capital Joinery Ltd, they compile various kinds of papers,

which are listed underneath:

Account receivable report: Receivable accounts log is a significant report and was known to be

among the most personal data of such an account business if creditor data gathering reports is

expected. This analysis was used to identify restructuring debt holders that converted the

business's poor credit reserves.

Budgetary report: It is structured to provide a structure for the development of the budget.

Managers draught this study by collecting data from all the documents they have generated. The

financial statements help include guidance for evaluating the competitive situation and strategies

of the company. With the ever retail sector, the manager of Capital Journey Ltd used the budget

document to identify future growth opportunities.

Inventory management report: This paper is written on the basis of data gathered from inventory

control. The key reason for the introduction of this study helps to determine the total required

stock production, maintenance expenses and judgement of future stock supply.

Performance report: This paper is the most critical aspect that each company needs for

formulations. It is also helpful for providing details regarding each firm's outcomes. Often on the

framework of identifying and measuring performance, managers will devise compensation

strategies and take action on organizational rewards on the basis of reviewing this paper. Capital

Journey Ltd has more than 500 employees and is a multinational company. For the chief

executive, the report card is largely focused on something that can track the level of

accomplishment within each section of employees and formulate policies for their planning and

development.

Task 2

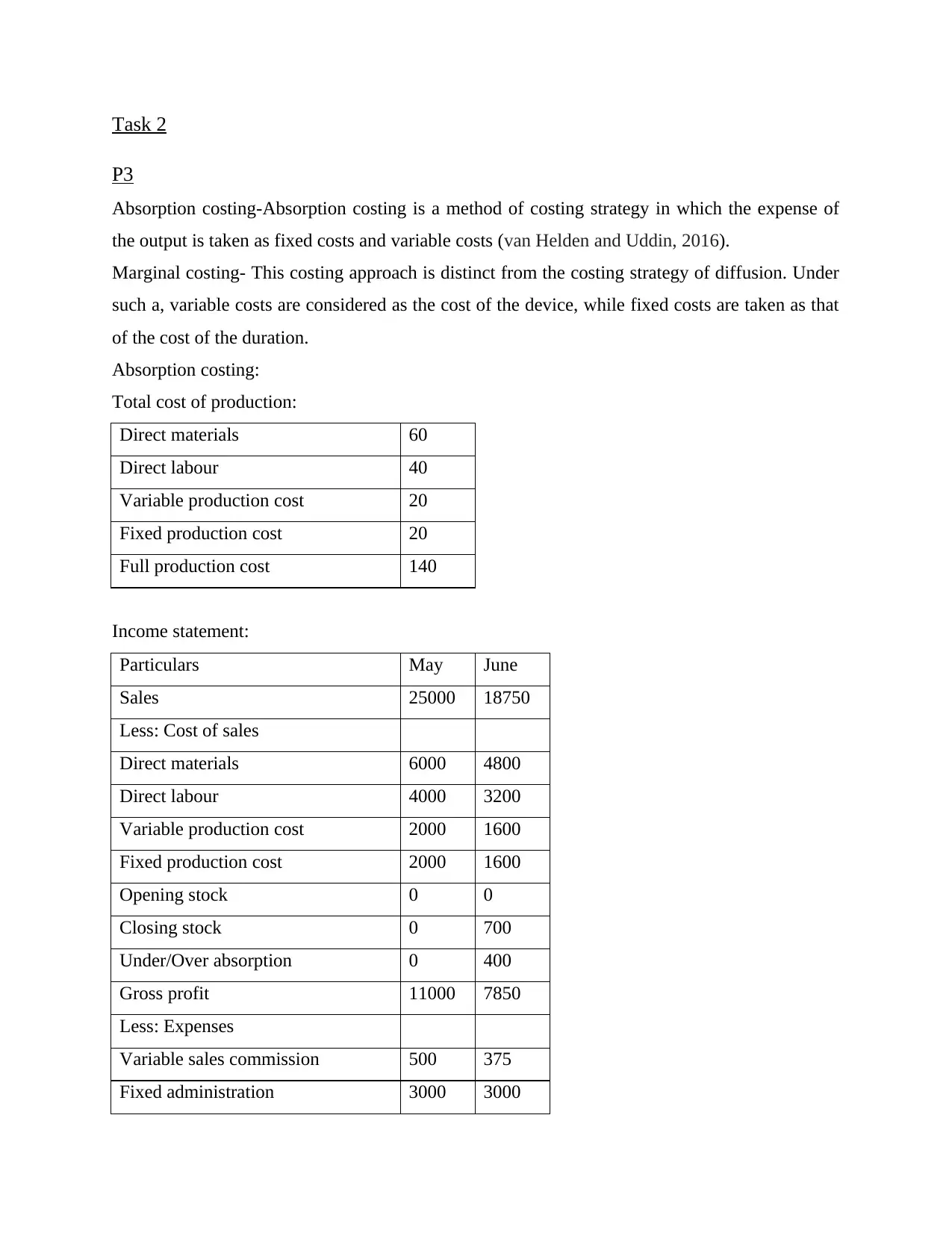

P3

Absorption costing-Absorption costing is a method of costing strategy in which the expense of

the output is taken as fixed costs and variable costs (van Helden and Uddin, 2016).

Marginal costing- This costing approach is distinct from the costing strategy of diffusion. Under

such a, variable costs are considered as the cost of the device, while fixed costs are taken as that

of the cost of the duration.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

P3

Absorption costing-Absorption costing is a method of costing strategy in which the expense of

the output is taken as fixed costs and variable costs (van Helden and Uddin, 2016).

Marginal costing- This costing approach is distinct from the costing strategy of diffusion. Under

such a, variable costs are considered as the cost of the device, while fixed costs are taken as that

of the cost of the duration.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

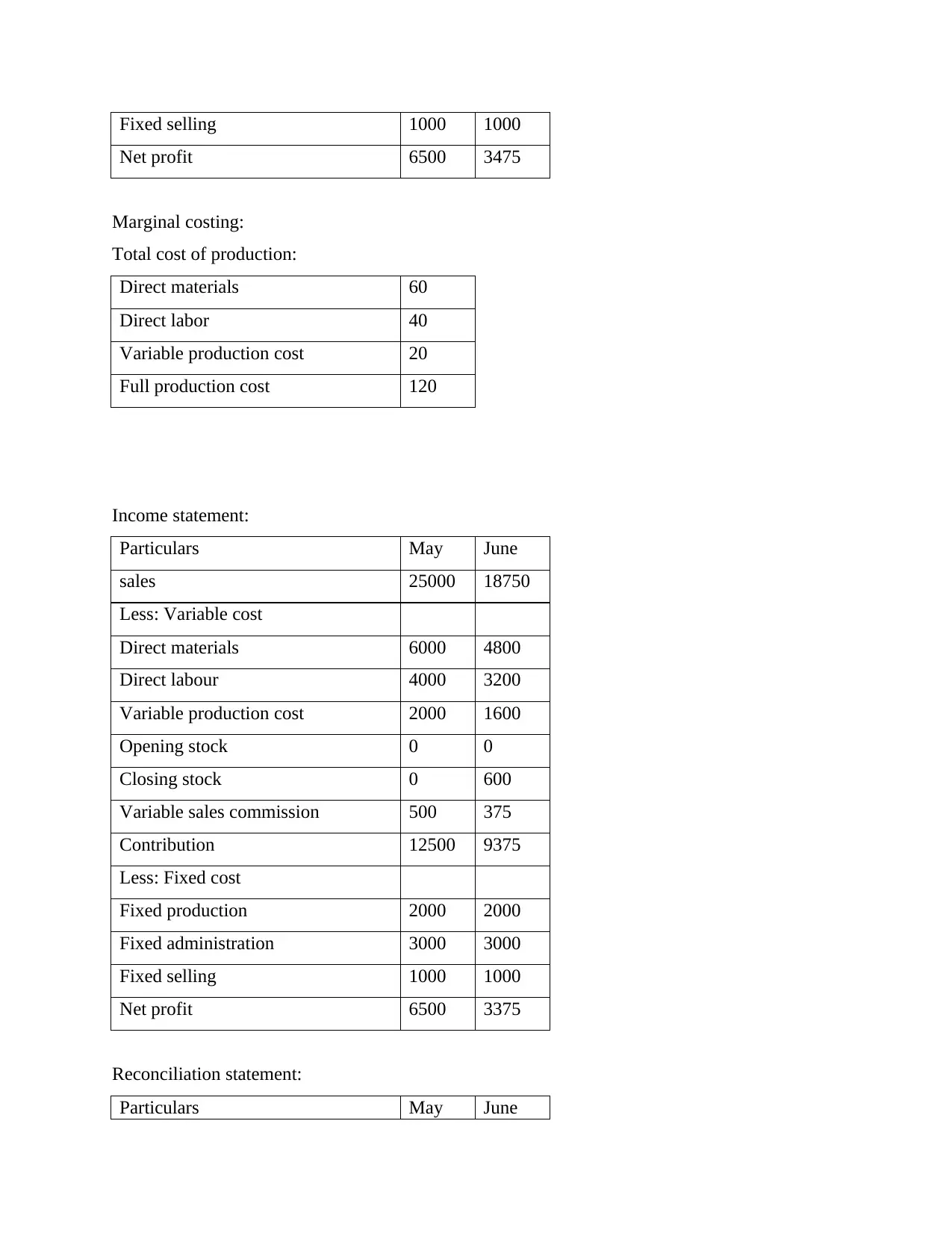

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

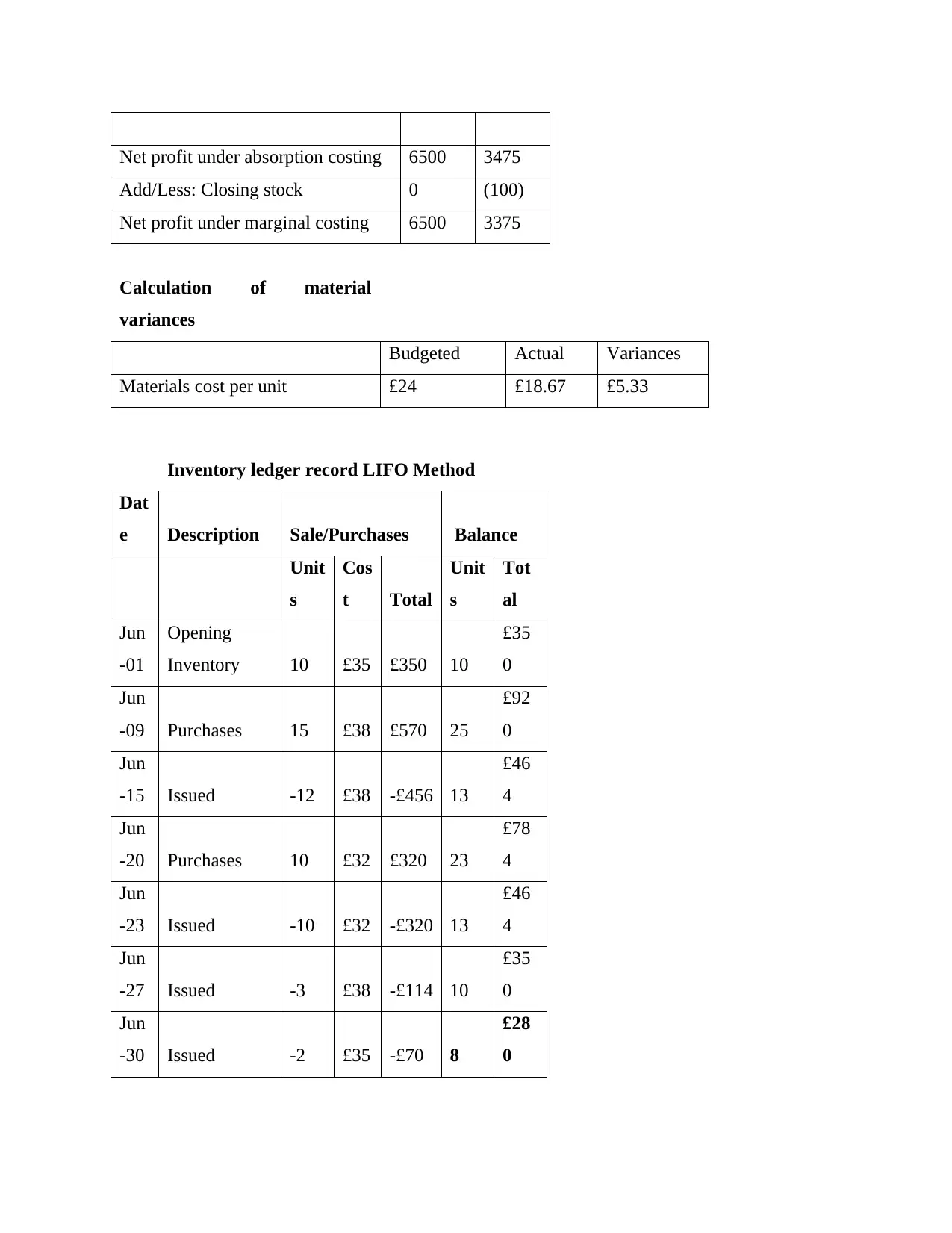

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat

e Description Sale/Purchases Balance

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

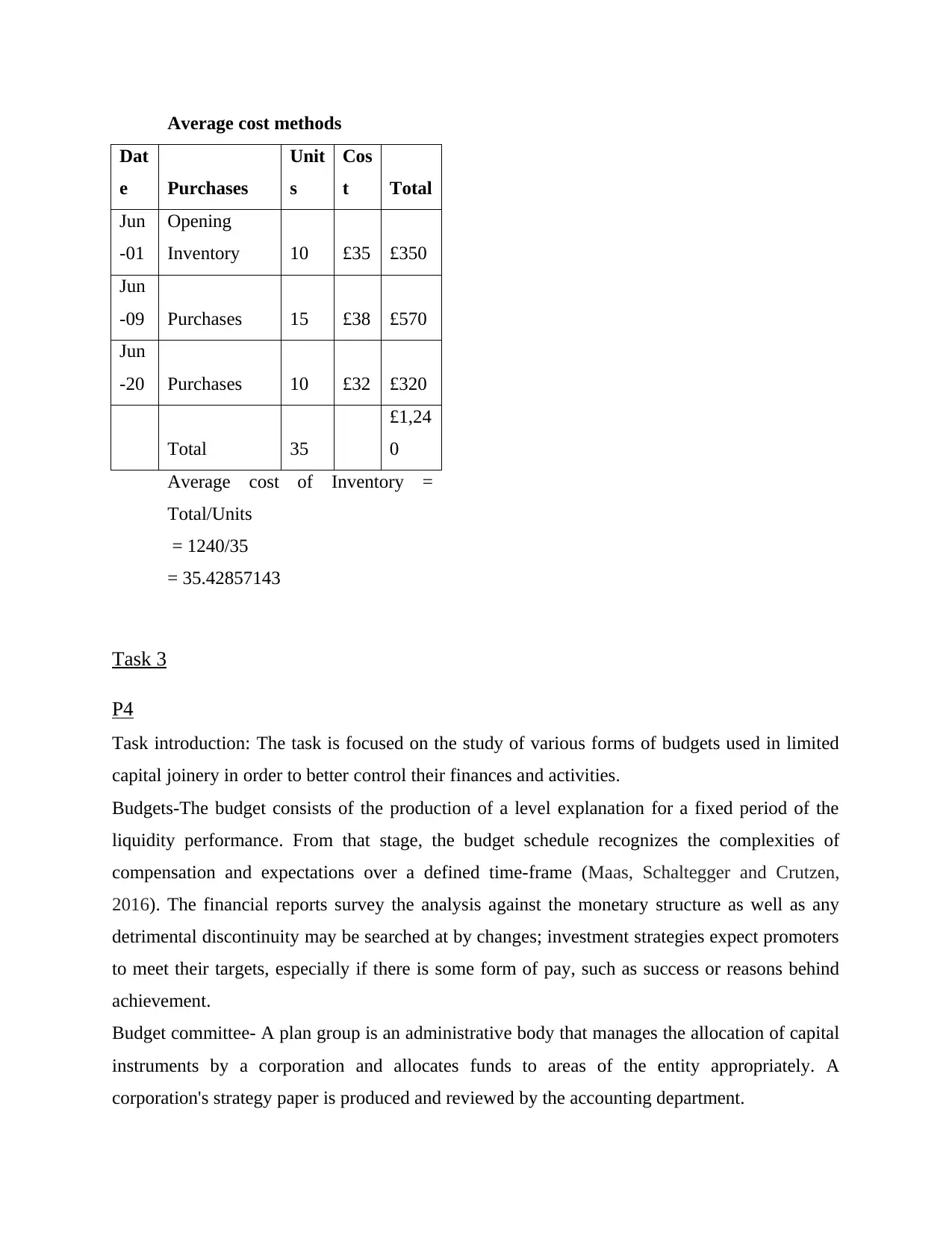

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

Task 3

P4

Task introduction: The task is focused on the study of various forms of budgets used in limited

capital joinery in order to better control their finances and activities.

Budgets-The budget consists of the production of a level explanation for a fixed period of the

liquidity performance. From that stage, the budget schedule recognizes the complexities of

compensation and expectations over a defined time-frame (Maas, Schaltegger and Crutzen,

2016). The financial reports survey the analysis against the monetary structure as well as any

detrimental discontinuity may be searched at by changes; investment strategies expect promoters

to meet their targets, especially if there is some form of pay, such as success or reasons behind

achievement.

Budget committee- A plan group is an administrative body that manages the allocation of capital

instruments by a corporation and allocates funds to areas of the entity appropriately. A

corporation's strategy paper is produced and reviewed by the accounting department.

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

= 1240/35

= 35.42857143

Task 3

P4

Task introduction: The task is focused on the study of various forms of budgets used in limited

capital joinery in order to better control their finances and activities.

Budgets-The budget consists of the production of a level explanation for a fixed period of the

liquidity performance. From that stage, the budget schedule recognizes the complexities of

compensation and expectations over a defined time-frame (Maas, Schaltegger and Crutzen,

2016). The financial reports survey the analysis against the monetary structure as well as any

detrimental discontinuity may be searched at by changes; investment strategies expect promoters

to meet their targets, especially if there is some form of pay, such as success or reasons behind

achievement.

Budget committee- A plan group is an administrative body that manages the allocation of capital

instruments by a corporation and allocates funds to areas of the entity appropriately. A

corporation's strategy paper is produced and reviewed by the accounting department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

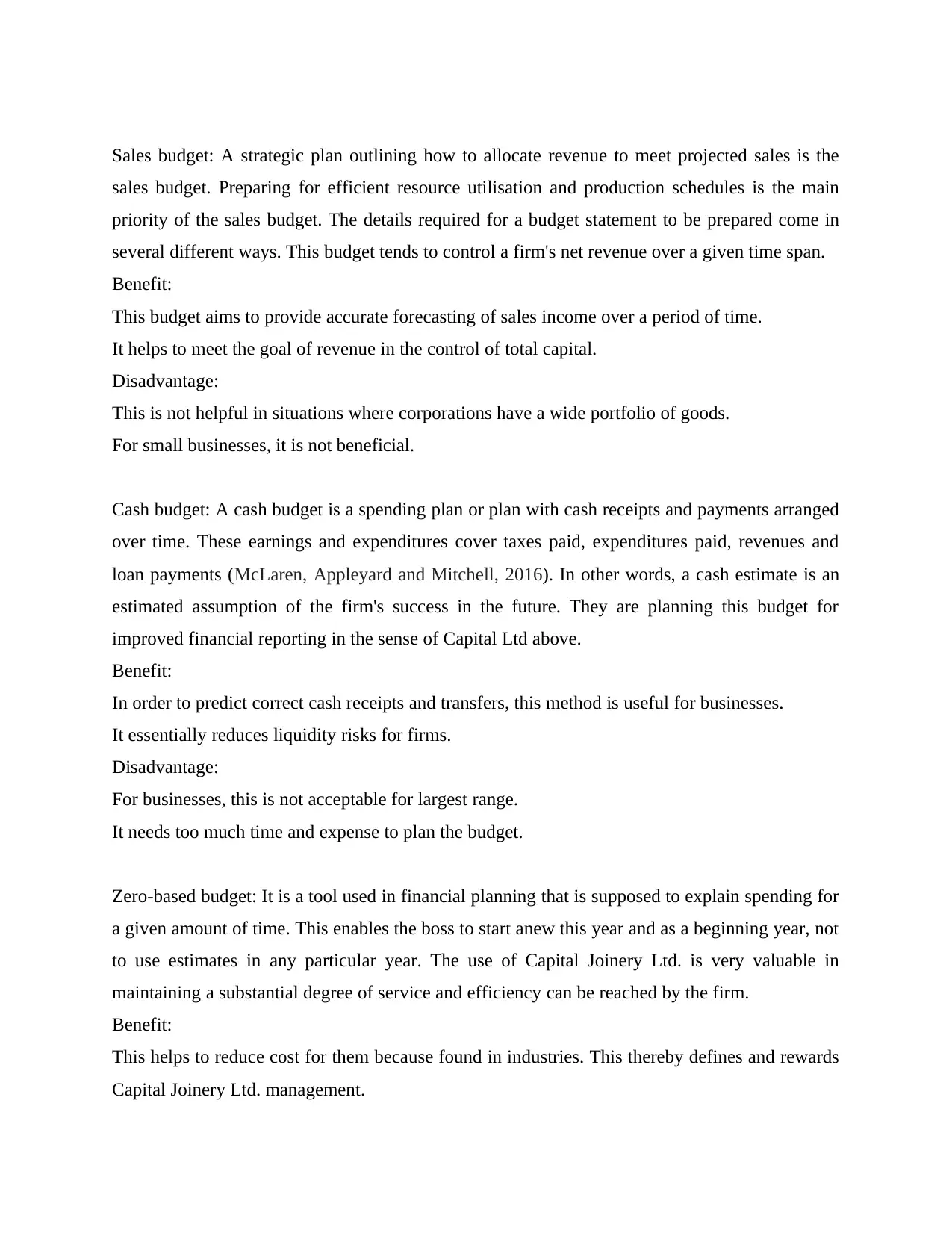

Sales budget: A strategic plan outlining how to allocate revenue to meet projected sales is the

sales budget. Preparing for efficient resource utilisation and production schedules is the main

priority of the sales budget. The details required for a budget statement to be prepared come in

several different ways. This budget tends to control a firm's net revenue over a given time span.

Benefit:

This budget aims to provide accurate forecasting of sales income over a period of time.

It helps to meet the goal of revenue in the control of total capital.

Disadvantage:

This is not helpful in situations where corporations have a wide portfolio of goods.

For small businesses, it is not beneficial.

Cash budget: A cash budget is a spending plan or plan with cash receipts and payments arranged

over time. These earnings and expenditures cover taxes paid, expenditures paid, revenues and

loan payments (McLaren, Appleyard and Mitchell, 2016). In other words, a cash estimate is an

estimated assumption of the firm's success in the future. They are planning this budget for

improved financial reporting in the sense of Capital Ltd above.

Benefit:

In order to predict correct cash receipts and transfers, this method is useful for businesses.

It essentially reduces liquidity risks for firms.

Disadvantage:

For businesses, this is not acceptable for largest range.

It needs too much time and expense to plan the budget.

Zero-based budget: It is a tool used in financial planning that is supposed to explain spending for

a given amount of time. This enables the boss to start anew this year and as a beginning year, not

to use estimates in any particular year. The use of Capital Joinery Ltd. is very valuable in

maintaining a substantial degree of service and efficiency can be reached by the firm.

Benefit:

This helps to reduce cost for them because found in industries. This thereby defines and rewards

Capital Joinery Ltd. management.

sales budget. Preparing for efficient resource utilisation and production schedules is the main

priority of the sales budget. The details required for a budget statement to be prepared come in

several different ways. This budget tends to control a firm's net revenue over a given time span.

Benefit:

This budget aims to provide accurate forecasting of sales income over a period of time.

It helps to meet the goal of revenue in the control of total capital.

Disadvantage:

This is not helpful in situations where corporations have a wide portfolio of goods.

For small businesses, it is not beneficial.

Cash budget: A cash budget is a spending plan or plan with cash receipts and payments arranged

over time. These earnings and expenditures cover taxes paid, expenditures paid, revenues and

loan payments (McLaren, Appleyard and Mitchell, 2016). In other words, a cash estimate is an

estimated assumption of the firm's success in the future. They are planning this budget for

improved financial reporting in the sense of Capital Ltd above.

Benefit:

In order to predict correct cash receipts and transfers, this method is useful for businesses.

It essentially reduces liquidity risks for firms.

Disadvantage:

For businesses, this is not acceptable for largest range.

It needs too much time and expense to plan the budget.

Zero-based budget: It is a tool used in financial planning that is supposed to explain spending for

a given amount of time. This enables the boss to start anew this year and as a beginning year, not

to use estimates in any particular year. The use of Capital Joinery Ltd. is very valuable in

maintaining a substantial degree of service and efficiency can be reached by the firm.

Benefit:

This helps to reduce cost for them because found in industries. This thereby defines and rewards

Capital Joinery Ltd. management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Its use will ensure proper preparation within companies is taken out. In this way, the

management of Capital Joinery Ltd. may also be supported with a return.

Disadvantage:

Scheduling a Zero-Based Budget requires a lot of operational time. A drawback can also be

developed for the administration of Capital Joinery Ltd in this manner.

Implementing a zero-based budget will create a lot of challenges and complications with

operational strategy and teamwork.

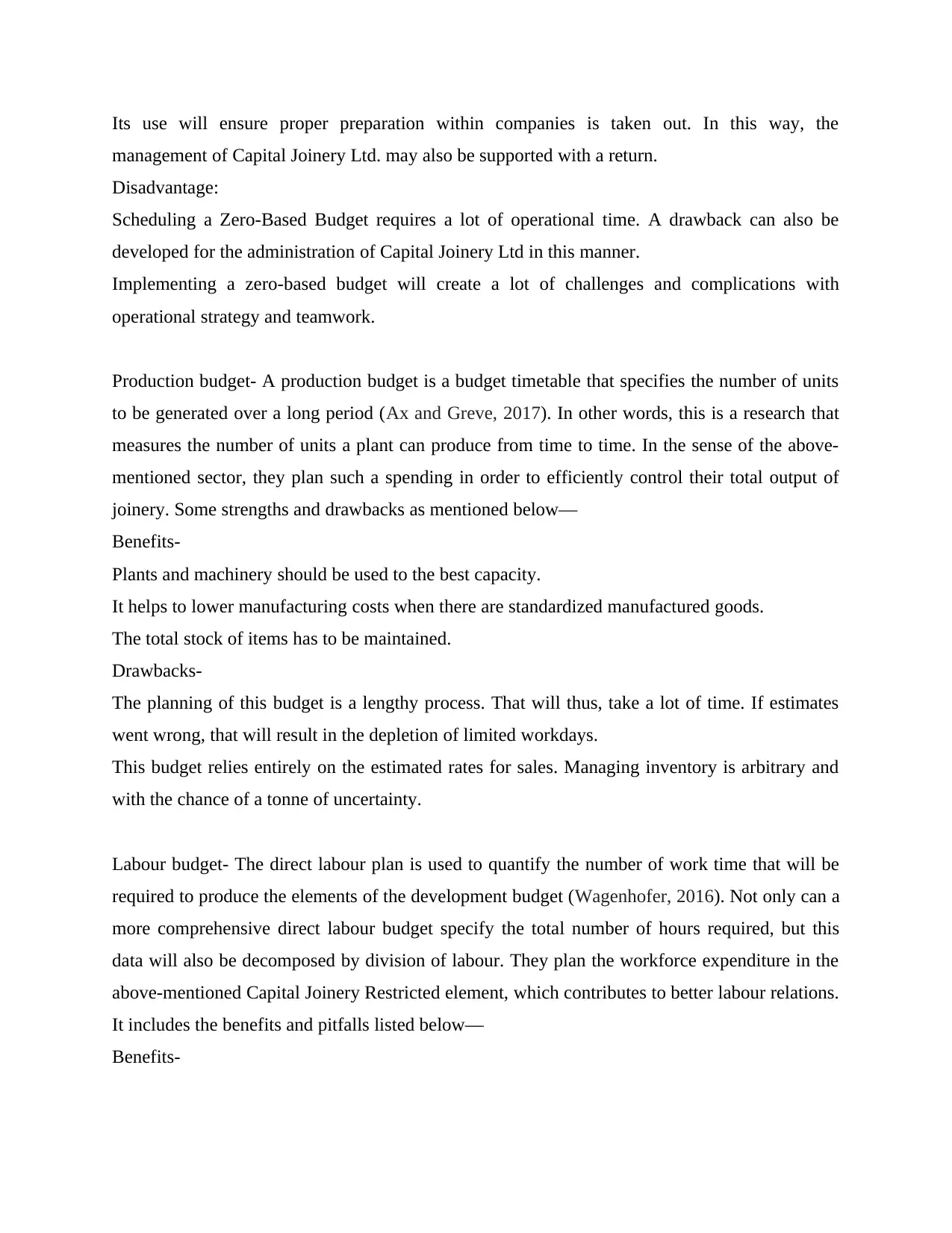

Production budget- A production budget is a budget timetable that specifies the number of units

to be generated over a long period (Ax and Greve, 2017). In other words, this is a research that

measures the number of units a plant can produce from time to time. In the sense of the above-

mentioned sector, they plan such a spending in order to efficiently control their total output of

joinery. Some strengths and drawbacks as mentioned below—

Benefits-

Plants and machinery should be used to the best capacity.

It helps to lower manufacturing costs when there are standardized manufactured goods.

The total stock of items has to be maintained.

Drawbacks-

The planning of this budget is a lengthy process. That will thus, take a lot of time. If estimates

went wrong, that will result in the depletion of limited workdays.

This budget relies entirely on the estimated rates for sales. Managing inventory is arbitrary and

with the chance of a tonne of uncertainty.

Labour budget- The direct labour plan is used to quantify the number of work time that will be

required to produce the elements of the development budget (Wagenhofer, 2016). Not only can a

more comprehensive direct labour budget specify the total number of hours required, but this

data will also be decomposed by division of labour. They plan the workforce expenditure in the

above-mentioned Capital Joinery Restricted element, which contributes to better labour relations.

It includes the benefits and pitfalls listed below—

Benefits-

management of Capital Joinery Ltd. may also be supported with a return.

Disadvantage:

Scheduling a Zero-Based Budget requires a lot of operational time. A drawback can also be

developed for the administration of Capital Joinery Ltd in this manner.

Implementing a zero-based budget will create a lot of challenges and complications with

operational strategy and teamwork.

Production budget- A production budget is a budget timetable that specifies the number of units

to be generated over a long period (Ax and Greve, 2017). In other words, this is a research that

measures the number of units a plant can produce from time to time. In the sense of the above-

mentioned sector, they plan such a spending in order to efficiently control their total output of

joinery. Some strengths and drawbacks as mentioned below—

Benefits-

Plants and machinery should be used to the best capacity.

It helps to lower manufacturing costs when there are standardized manufactured goods.

The total stock of items has to be maintained.

Drawbacks-

The planning of this budget is a lengthy process. That will thus, take a lot of time. If estimates

went wrong, that will result in the depletion of limited workdays.

This budget relies entirely on the estimated rates for sales. Managing inventory is arbitrary and

with the chance of a tonne of uncertainty.

Labour budget- The direct labour plan is used to quantify the number of work time that will be

required to produce the elements of the development budget (Wagenhofer, 2016). Not only can a

more comprehensive direct labour budget specify the total number of hours required, but this

data will also be decomposed by division of labour. They plan the workforce expenditure in the

above-mentioned Capital Joinery Restricted element, which contributes to better labour relations.

It includes the benefits and pitfalls listed below—

Benefits-

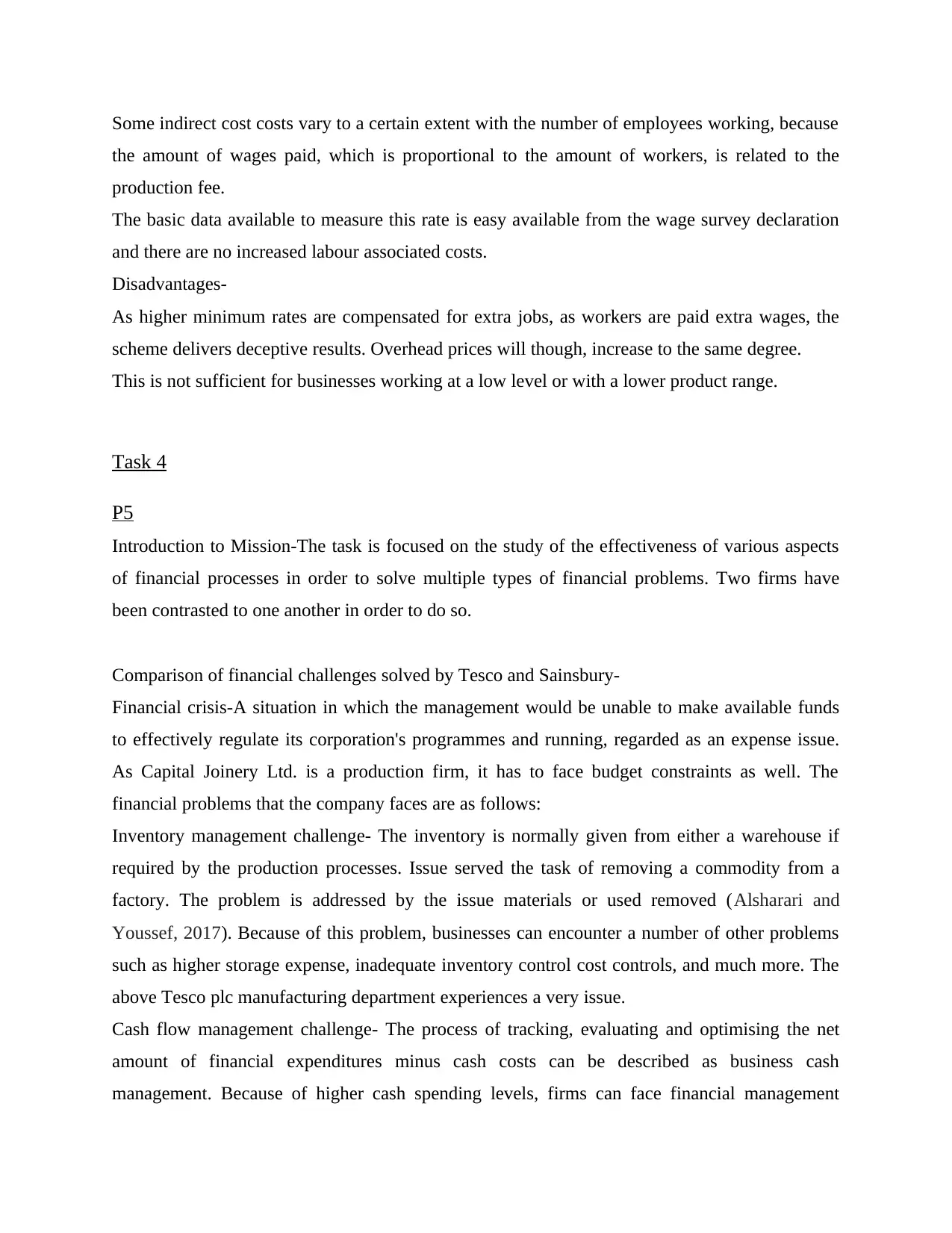

Some indirect cost costs vary to a certain extent with the number of employees working, because

the amount of wages paid, which is proportional to the amount of workers, is related to the

production fee.

The basic data available to measure this rate is easy available from the wage survey declaration

and there are no increased labour associated costs.

Disadvantages-

As higher minimum rates are compensated for extra jobs, as workers are paid extra wages, the

scheme delivers deceptive results. Overhead prices will though, increase to the same degree.

This is not sufficient for businesses working at a low level or with a lower product range.

Task 4

P5

Introduction to Mission-The task is focused on the study of the effectiveness of various aspects

of financial processes in order to solve multiple types of financial problems. Two firms have

been contrasted to one another in order to do so.

Comparison of financial challenges solved by Tesco and Sainsbury-

Financial crisis-A situation in which the management would be unable to make available funds

to effectively regulate its corporation's programmes and running, regarded as an expense issue.

As Capital Joinery Ltd. is a production firm, it has to face budget constraints as well. The

financial problems that the company faces are as follows:

Inventory management challenge- The inventory is normally given from either a warehouse if

required by the production processes. Issue served the task of removing a commodity from a

factory. The problem is addressed by the issue materials or used removed (Alsharari and

Youssef, 2017). Because of this problem, businesses can encounter a number of other problems

such as higher storage expense, inadequate inventory control cost controls, and much more. The

above Tesco plc manufacturing department experiences a very issue.

Cash flow management challenge- The process of tracking, evaluating and optimising the net

amount of financial expenditures minus cash costs can be described as business cash

management. Because of higher cash spending levels, firms can face financial management

the amount of wages paid, which is proportional to the amount of workers, is related to the

production fee.

The basic data available to measure this rate is easy available from the wage survey declaration

and there are no increased labour associated costs.

Disadvantages-

As higher minimum rates are compensated for extra jobs, as workers are paid extra wages, the

scheme delivers deceptive results. Overhead prices will though, increase to the same degree.

This is not sufficient for businesses working at a low level or with a lower product range.

Task 4

P5

Introduction to Mission-The task is focused on the study of the effectiveness of various aspects

of financial processes in order to solve multiple types of financial problems. Two firms have

been contrasted to one another in order to do so.

Comparison of financial challenges solved by Tesco and Sainsbury-

Financial crisis-A situation in which the management would be unable to make available funds

to effectively regulate its corporation's programmes and running, regarded as an expense issue.

As Capital Joinery Ltd. is a production firm, it has to face budget constraints as well. The

financial problems that the company faces are as follows:

Inventory management challenge- The inventory is normally given from either a warehouse if

required by the production processes. Issue served the task of removing a commodity from a

factory. The problem is addressed by the issue materials or used removed (Alsharari and

Youssef, 2017). Because of this problem, businesses can encounter a number of other problems

such as higher storage expense, inadequate inventory control cost controls, and much more. The

above Tesco plc manufacturing department experiences a very issue.

Cash flow management challenge- The process of tracking, evaluating and optimising the net

amount of financial expenditures minus cash costs can be described as business cash

management. Because of higher cash spending levels, firms can face financial management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.