Comprehensive Management Accounting Analysis and Financial Forecasting

VerifiedAdded on 2023/01/11

|12

|3672

|56

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of Lets Grow Ltd. It begins with an introduction to management accounting and its role in internal financial reporting, planning, controlling, and performance enhancement. The report then delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, outlining their requirements, benefits, and applications. It also explores the use of management accounting systems and reports, such as cost reports, inventory reports, budget reports, and performance reports, in effective decision-making. A cash budget for Lets Grow Ltd is presented and analyzed, along with its role in financial forecasting. The report further discusses adapting management accounting techniques to address financial problems and provides a critical evaluation of Lets Grow Ltd's financial position based on forecasted projects. The report concludes with a summary of findings and provides references.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

SCENARIO.....................................................................................................................................1

a) Requirements and benefits of different management accounting systems..............................1

b) Management accounting systems and reports in effective decision making...........................4

c) Cash budget of Lets Grow for six months for year ending August, 2020...............................5

d) Use of cash budget and its application for the preparation and forecasting the financial

position of the organisation.........................................................................................................6

e) Adapting management accounting techniques for dealing with the financial problems.........7

f) Critical evaluation of the financial position of Lets Grow based on forecasted projects........8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

SCENARIO.....................................................................................................................................1

a) Requirements and benefits of different management accounting systems..............................1

b) Management accounting systems and reports in effective decision making...........................4

c) Cash budget of Lets Grow for six months for year ending August, 2020...............................5

d) Use of cash budget and its application for the preparation and forecasting the financial

position of the organisation.........................................................................................................6

e) Adapting management accounting techniques for dealing with the financial problems.........7

f) Critical evaluation of the financial position of Lets Grow based on forecasted projects........8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUTION

Management accounting refers to the process that is used by the company in preparing its

internal financial reports. It involves the process of planning, controlling, monitoring and

enhancing the performance of the business. It provides the concept and techniques that are used

by the organisation for managing the operation and activities efficiently. It enables the company

in achieving its desired goals and objectives by effectively utilising the available resources of

company. Report is based on Lets Grow Ltd that is a manufacturing concern. Study will reveal

about the different management accounting systems and reporting methods used by business. it

will address about the different planning tools that are used by the business and ways of

responding to the financial problems using management accounting.

SCENARIO

a) Requirements and benefits of different management accounting systems

Management accounting

Management accounting refers to provision of the financial as well as non financial decision

making to the managers. In management accounting financial information that is essential for

decision making for the organisation. Management accounting techniques provides the managers

in effectively managing and performing the control functions (Otley, 2016). It allows the

managers to identify, accumulate, measure, prepare, analysis and interpretation of the

information assisting executives for fulfilling the organisational objectives.

Management Accounting Systems

Management accountings systems allow the managers to manage the operation and activities of

business. There are various management accounting systems such as inventory management,

cost accounting, job costing and price optimisation system.

Cost Accounting

Cost accounting is management accounting system that is used by the management for

approximation of product cost for the valuation of inventory, profitability and the cost control.

Cost accounting provides different methods that could be used for allocation of the costs over

products manufactured using cost accounting traditional methods or activity based costing. One

of the important tasks of the cost accounting is to ascertain the actual cost of the products or

goods manufactured during the year. Costing method record all the costs of producing the

products and weighs input cost including both variable and fixed costs such as depreciation of

1

Management accounting refers to the process that is used by the company in preparing its

internal financial reports. It involves the process of planning, controlling, monitoring and

enhancing the performance of the business. It provides the concept and techniques that are used

by the organisation for managing the operation and activities efficiently. It enables the company

in achieving its desired goals and objectives by effectively utilising the available resources of

company. Report is based on Lets Grow Ltd that is a manufacturing concern. Study will reveal

about the different management accounting systems and reporting methods used by business. it

will address about the different planning tools that are used by the business and ways of

responding to the financial problems using management accounting.

SCENARIO

a) Requirements and benefits of different management accounting systems

Management accounting

Management accounting refers to provision of the financial as well as non financial decision

making to the managers. In management accounting financial information that is essential for

decision making for the organisation. Management accounting techniques provides the managers

in effectively managing and performing the control functions (Otley, 2016). It allows the

managers to identify, accumulate, measure, prepare, analysis and interpretation of the

information assisting executives for fulfilling the organisational objectives.

Management Accounting Systems

Management accountings systems allow the managers to manage the operation and activities of

business. There are various management accounting systems such as inventory management,

cost accounting, job costing and price optimisation system.

Cost Accounting

Cost accounting is management accounting system that is used by the management for

approximation of product cost for the valuation of inventory, profitability and the cost control.

Cost accounting provides different methods that could be used for allocation of the costs over

products manufactured using cost accounting traditional methods or activity based costing. One

of the important tasks of the cost accounting is to ascertain the actual cost of the products or

goods manufactured during the year. Costing method record all the costs of producing the

products and weighs input cost including both variable and fixed costs such as depreciation of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capital assets. It allows the managers to compare the actual outcomes with the estimated inputs

for assessing the performance of the managers. On the basis of these information strategies for

making the process cost efficient are made by company.

Benefits and Application

Cost accounting is used by company for evaluating the cost of manufacturing a product.

It provides all the cost information that is used by the management in decision making. They can

identify per unit cost for evaluating the prices earning reasonable rate of return. Using the cost

accounting methods managers can more accurately records the cost information for driving

towards the desired goals and objectives.

Inventory management systems

Inventory management provides all the information required for effectively management

of the various inventories. The inventory systems allow the company to control and monitor the

operations related with inventory such as ordering, use and storage of different raw materials or

components used in the production of products or services. Inventory management enables the

company to understand the present level of inventory and ensuring that situation of over stock

and under stock to minimum (Maas, Schaltegger and Crutzen, 2016). This has enables the

organisation and management in effectively managing their inventory and taking more informed

decisions. The software used in inventory management allows the company in centrally

managing the inventory levels of its branches. Orders for the inventory are placed on reaching

the requirement. Inventory management is one of the important aspect in management

accounting that plays an effective role in achieving the growth and sustainability

Benefits and Application

There are various benefits of the inventory management to the Lets Grow ltd. Inventory

management enables to keep record of all the inventory movements. They provide the

management to be updated with inventory levels of each day. System allows for inventory

counts, physical counts, bar codes and such other software and techniques for keeping proper

track of all inventories. It is applied in the organisation for making decision related with ordering

purchasing and for making technical decisions. this avoids the company to overstock that

increases the carrying cost of inventory.

Job Costing Method

2

for assessing the performance of the managers. On the basis of these information strategies for

making the process cost efficient are made by company.

Benefits and Application

Cost accounting is used by company for evaluating the cost of manufacturing a product.

It provides all the cost information that is used by the management in decision making. They can

identify per unit cost for evaluating the prices earning reasonable rate of return. Using the cost

accounting methods managers can more accurately records the cost information for driving

towards the desired goals and objectives.

Inventory management systems

Inventory management provides all the information required for effectively management

of the various inventories. The inventory systems allow the company to control and monitor the

operations related with inventory such as ordering, use and storage of different raw materials or

components used in the production of products or services. Inventory management enables the

company to understand the present level of inventory and ensuring that situation of over stock

and under stock to minimum (Maas, Schaltegger and Crutzen, 2016). This has enables the

organisation and management in effectively managing their inventory and taking more informed

decisions. The software used in inventory management allows the company in centrally

managing the inventory levels of its branches. Orders for the inventory are placed on reaching

the requirement. Inventory management is one of the important aspect in management

accounting that plays an effective role in achieving the growth and sustainability

Benefits and Application

There are various benefits of the inventory management to the Lets Grow ltd. Inventory

management enables to keep record of all the inventory movements. They provide the

management to be updated with inventory levels of each day. System allows for inventory

counts, physical counts, bar codes and such other software and techniques for keeping proper

track of all inventories. It is applied in the organisation for making decision related with ordering

purchasing and for making technical decisions. this avoids the company to overstock that

increases the carrying cost of inventory.

Job Costing Method

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing method is management accounting system that is used for describing the

allocation of production costs the products or items separately. System is used in the organisation

in which production process is different from each other. job costing measures the cost of

producing a job separately using the job costing system managers identify all the costs such as

raw materials, labour and the overhead cost for producing a particular job. Companies

accumulate the data related to the processes involved in the specified job. It enables the company

in effective decision making for the costs related to job.

Benefits and Application

It is useful for making accurate estimates about the cost involved in production of job from

the previous estimates. Using the cost information they could more accurately quote prices for

earning reasonable profits over the job. This information is also used for allocating inventory

cost to processed goods. Lets Grow ltd uses the job costing for estimating the cost of producing a

job for dealing with special orders (Bromwich. and Scapens, 2016). It enables the management

with essential information for the job so that customers could be given the estimates for which

costs will be refunded by the customers. It allows the managers in earning reasonable profit

margins.

Price Optimisation

Price Optimisation system involves application of mathematical concept and techniques

to determine the response of customers over different levels of prices that are determined by

management for goods and services. Demand at every price levels is different and therefore the

managers evaluate the different price levels that will enable the company to reach its break-even

point and reasonable profit (Christ and Burritt, 2017). Price optimisation method involves the

application of different concepts and techniques that gives more reliable estimates of the price

levels. Using the price optimisation system ascertain the prices that will be optimum for products

and services.

Benefits and Application

Price Optimisation provides the management in deciding the most optimum prices for

goods and services to be set by Lets Grow ltd. it is useful in decision making process and making

pricing strategies for products by analysing the sales required for achieving the goals and

objectives. This is applied for making effective pricing strategies for the products where

company achieves the target revenues. Deciding the prices of goods is a crucial decision of the

3

allocation of production costs the products or items separately. System is used in the organisation

in which production process is different from each other. job costing measures the cost of

producing a job separately using the job costing system managers identify all the costs such as

raw materials, labour and the overhead cost for producing a particular job. Companies

accumulate the data related to the processes involved in the specified job. It enables the company

in effective decision making for the costs related to job.

Benefits and Application

It is useful for making accurate estimates about the cost involved in production of job from

the previous estimates. Using the cost information they could more accurately quote prices for

earning reasonable profits over the job. This information is also used for allocating inventory

cost to processed goods. Lets Grow ltd uses the job costing for estimating the cost of producing a

job for dealing with special orders (Bromwich. and Scapens, 2016). It enables the management

with essential information for the job so that customers could be given the estimates for which

costs will be refunded by the customers. It allows the managers in earning reasonable profit

margins.

Price Optimisation

Price Optimisation system involves application of mathematical concept and techniques

to determine the response of customers over different levels of prices that are determined by

management for goods and services. Demand at every price levels is different and therefore the

managers evaluate the different price levels that will enable the company to reach its break-even

point and reasonable profit (Christ and Burritt, 2017). Price optimisation method involves the

application of different concepts and techniques that gives more reliable estimates of the price

levels. Using the price optimisation system ascertain the prices that will be optimum for products

and services.

Benefits and Application

Price Optimisation provides the management in deciding the most optimum prices for

goods and services to be set by Lets Grow ltd. it is useful in decision making process and making

pricing strategies for products by analysing the sales required for achieving the goals and

objectives. This is applied for making effective pricing strategies for the products where

company achieves the target revenues. Deciding the prices of goods is a crucial decision of the

3

management which is required to be taken after analysing all the factors associated with the

products and services.

b) Management accounting systems and reports in effective decision making.

MA pays attention towards the internal information reflected in the financial accounting.

MA is used for effective plans, controls and for sound decision making. It also considers

financial statements such as income statement and cash flow statement. Internal MA reports are

used by the management for effectively managing the resources and to evaluate the corporate

performance from the information. Different cost reports are used for framing strategies for

improving the internal performance of business such as cost reports, budget reports and

performance reports.

Cost Reports

MA accounting is concerned with measuring cost for making or producing the goods or

services. Cost accountants in calculating the cost includes raw material, labour cost, overheads

and any extra costs for manufacturing the products and items. Cost per unit is ascertained by

dividing the aggregate costs with units produced. Cost report contains all the information related

to the costs from raw materials to all the costs that are incurred for preparing the finished goods.

Managers use this information to evaluate the different costs and for determining the price levels

earning reasonable rate of returns (Ameen, Ahmed and Abd Hafez, 2018). It enables the

managers to identify whether the selling prices and products will be able to cover the production

cost. This information is used by the managers for dealing effectively with the operations and

activity by planning and controlling. Managers evaluate the sales level using break even analysis

where the costs and revenues are equal. It must earn the break even sales for covering the costs.

cost information provides the managers to analyse the variances between the actual and budgeted

figures.

Inventory Reports

Inventory reports contain the information about all the inventories of the organisation. it

contains the quantity of inventory purchased, inventory in work in progress and the finished

goods produced. It keeps all the records of inventory wasted or damaged. This enables the

management to take decision about the inventory related with their procurement, consumption

and storage. Also the estimates about the future orders are made by the management analysing

the frequency with which movements are made in inventory of company. This enables the

4

products and services.

b) Management accounting systems and reports in effective decision making.

MA pays attention towards the internal information reflected in the financial accounting.

MA is used for effective plans, controls and for sound decision making. It also considers

financial statements such as income statement and cash flow statement. Internal MA reports are

used by the management for effectively managing the resources and to evaluate the corporate

performance from the information. Different cost reports are used for framing strategies for

improving the internal performance of business such as cost reports, budget reports and

performance reports.

Cost Reports

MA accounting is concerned with measuring cost for making or producing the goods or

services. Cost accountants in calculating the cost includes raw material, labour cost, overheads

and any extra costs for manufacturing the products and items. Cost per unit is ascertained by

dividing the aggregate costs with units produced. Cost report contains all the information related

to the costs from raw materials to all the costs that are incurred for preparing the finished goods.

Managers use this information to evaluate the different costs and for determining the price levels

earning reasonable rate of returns (Ameen, Ahmed and Abd Hafez, 2018). It enables the

managers to identify whether the selling prices and products will be able to cover the production

cost. This information is used by the managers for dealing effectively with the operations and

activity by planning and controlling. Managers evaluate the sales level using break even analysis

where the costs and revenues are equal. It must earn the break even sales for covering the costs.

cost information provides the managers to analyse the variances between the actual and budgeted

figures.

Inventory Reports

Inventory reports contain the information about all the inventories of the organisation. it

contains the quantity of inventory purchased, inventory in work in progress and the finished

goods produced. It keeps all the records of inventory wasted or damaged. This enables the

management to take decision about the inventory related with their procurement, consumption

and storage. Also the estimates about the future orders are made by the management analysing

the frequency with which movements are made in inventory of company. This enables the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company to decide about the peak months in which inventory consumption is higher and

similarly in down months which is essential for managing the costs.

Budget Reports

Budgeting is one of the important part in planning process. Budgets are prepared using the

budgets of previous. Managers make adjustment to the budget for current year after analysing the

influencing factors related with the budget. These adjustments are made related to inflations,

market conditions, economic conditions, demand and supply and such other factors. it involves

projecting the future sales and expenditures from previous trends. These projections are made on

the basis of previous budgets for current year (Hopper and Bui, 2016). Managers evaluate

different factors that are associated with the budget. It lists all the expenses and incomes to be

incurred during the year. Focus of the managers is at attaining the goals and objectives by

staying in the budgets. Budget reports help the company in keeping the costs and expenses under

control by implementation of effective cost effective strategies.

Performance Reports

Performance reports are prepared by the management to analyse the performance of various

operations and employees during the specified period or related with specified project.

Performance reports consist of information on the difference between actual and budgeted

figures. Managers analyse whether the department have been able to achieve their targets with

the available resources. They identify the reasons lacking them from achieving the defined goals

and objectives for which strategies are framed by the organisation to improve the performance.

Performance reports are essential for assessing the performance of departments and employees to

enhance efficiency & productivity.

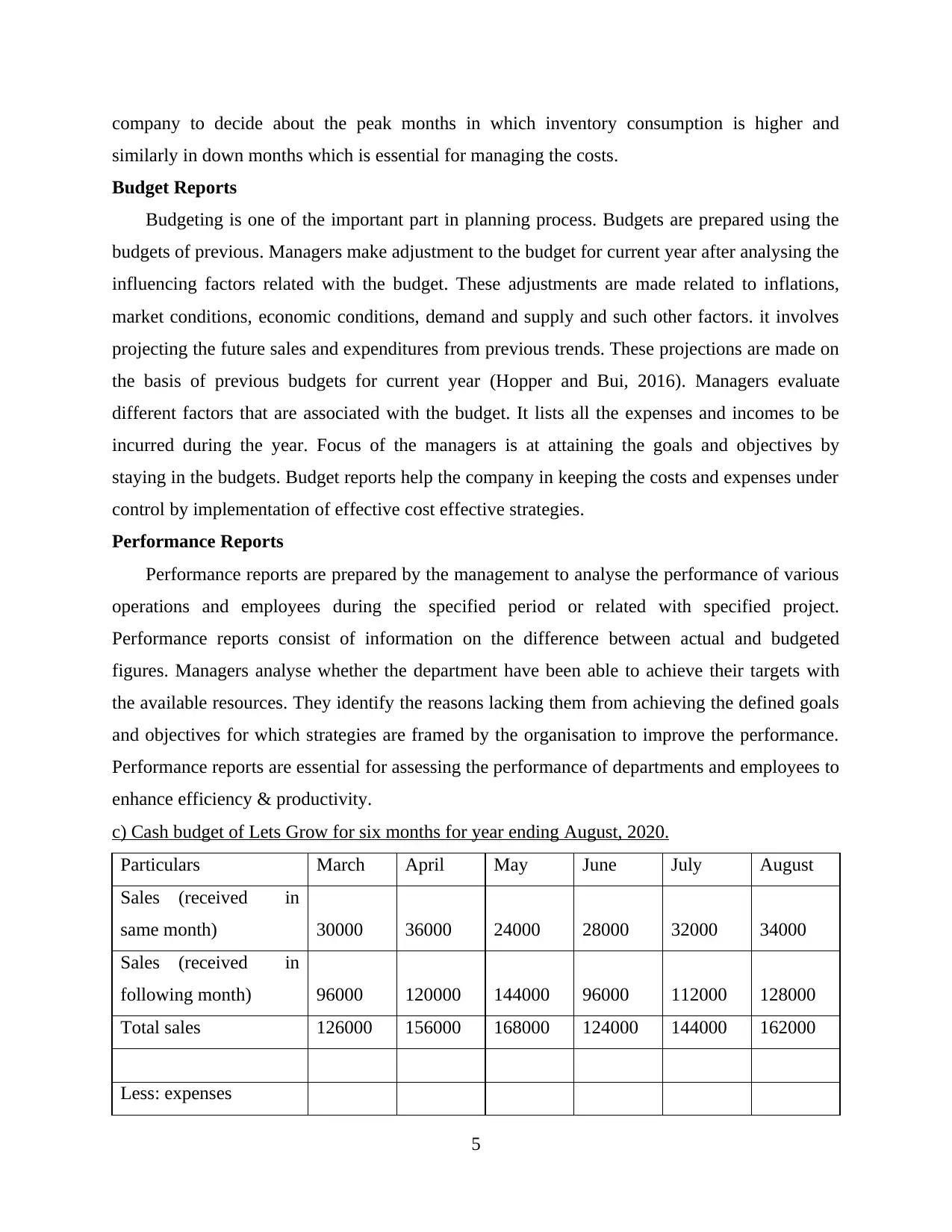

c) Cash budget of Lets Grow for six months for year ending August, 2020.

Particulars March April May June July August

Sales (received in

same month) 30000 36000 24000 28000 32000 34000

Sales (received in

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Less: expenses

5

similarly in down months which is essential for managing the costs.

Budget Reports

Budgeting is one of the important part in planning process. Budgets are prepared using the

budgets of previous. Managers make adjustment to the budget for current year after analysing the

influencing factors related with the budget. These adjustments are made related to inflations,

market conditions, economic conditions, demand and supply and such other factors. it involves

projecting the future sales and expenditures from previous trends. These projections are made on

the basis of previous budgets for current year (Hopper and Bui, 2016). Managers evaluate

different factors that are associated with the budget. It lists all the expenses and incomes to be

incurred during the year. Focus of the managers is at attaining the goals and objectives by

staying in the budgets. Budget reports help the company in keeping the costs and expenses under

control by implementation of effective cost effective strategies.

Performance Reports

Performance reports are prepared by the management to analyse the performance of various

operations and employees during the specified period or related with specified project.

Performance reports consist of information on the difference between actual and budgeted

figures. Managers analyse whether the department have been able to achieve their targets with

the available resources. They identify the reasons lacking them from achieving the defined goals

and objectives for which strategies are framed by the organisation to improve the performance.

Performance reports are essential for assessing the performance of departments and employees to

enhance efficiency & productivity.

c) Cash budget of Lets Grow for six months for year ending August, 2020.

Particulars March April May June July August

Sales (received in

same month) 30000 36000 24000 28000 32000 34000

Sales (received in

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Less: expenses

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchases 50000 50000 70000 80000 90000 100000

wages 30000 30000 30000 30000 30000 30000

Rent (paid quarterly) 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus / deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

d) Use of cash budget and its application for the preparation and forecasting the financial

position of the organisation.

Cash Budget

Cash budget is defined as the plan or budget of the expected receipts and expenses to be

incurred during the year. Cash budgets includes inflows and outflows includes the revenues,

incomes where the outflows contain expenses, purchases, payments and other operational

expenses. Cash budget is the estimated projection of future revenues and expenditures reflecting

the cash position of company at the end of the period. Cash budgets are usually developed by the

organisation after the purchase, sales and expenses budgets are already prepared by the

organisation. It is essential to prepare the cash budget after these budgets have been prepared for

accurately estimating the cash flows affected during the given period.

Use of Cash budget for forecasting financial position

Cash budget is used by the management for adequately managing the cash flows of

company. Cash management records the cash inflows and outflows from different sources. Cash

budgets budget is prepared using the previous budgets and making estimates about future

expenses based on previous trends. It is used by the organisation adequately allocating the funds

into different departments. Cash budgets are prepared analysing the requirement for ever

department of company and resources are allocated for carrying out their operations

(Rikhardsson and Yigitbasioglu, 2018). It enables the managers to keep control over the business

operations by defining the fixed budget for each department. Cash budgets are the spending plan

6

wages 30000 30000 30000 30000 30000 30000

Rent (paid quarterly) 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus / deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

d) Use of cash budget and its application for the preparation and forecasting the financial

position of the organisation.

Cash Budget

Cash budget is defined as the plan or budget of the expected receipts and expenses to be

incurred during the year. Cash budgets includes inflows and outflows includes the revenues,

incomes where the outflows contain expenses, purchases, payments and other operational

expenses. Cash budget is the estimated projection of future revenues and expenditures reflecting

the cash position of company at the end of the period. Cash budgets are usually developed by the

organisation after the purchase, sales and expenses budgets are already prepared by the

organisation. It is essential to prepare the cash budget after these budgets have been prepared for

accurately estimating the cash flows affected during the given period.

Use of Cash budget for forecasting financial position

Cash budget is used by the management for adequately managing the cash flows of

company. Cash management records the cash inflows and outflows from different sources. Cash

budgets budget is prepared using the previous budgets and making estimates about future

expenses based on previous trends. It is used by the organisation adequately allocating the funds

into different departments. Cash budgets are prepared analysing the requirement for ever

department of company and resources are allocated for carrying out their operations

(Rikhardsson and Yigitbasioglu, 2018). It enables the managers to keep control over the business

operations by defining the fixed budget for each department. Cash budgets are the spending plan

6

of the company that reflects the budgeted for every department. This enables management to

keep the costs and expenses under control by making most effective use of the available

resources. It is used for preventing overspendings and increasing the costs and expenses. Cash

budget enable the company to move towards a well defined direction for achieving the goals and

objectives of the business by staying in the limited budgeted funds.

It is used by the management for analysing the year end cash position of company. it is

assessed for ensuring that the company is available with enough monetary funds for meeting the

cash expenses and payments. It represents the financial position of the company at the end of the

year. Cash budgets are prepared by the organisation to enable the management to take required

decision for improving the cash position of company. Companies take steps for making effective

utilisation of the resources and managing the inflows and outflows so that company do not goes

out of cash during the period. Negative cash position reflects that management is not having

enough funds for meeting the expenses. Negative cash position impacts the operations and

functioning of the organisation. Non availability of funds puts stop to production process.

Therefore it is essential for the managers to make necessary arrangements for meeting the

operations of funds in advance so that operations of company are not affected.

e) Adapting management accounting techniques for dealing with the financial problems

Corporation are encountering questions about how the business models are adapting to

strategies business models and the procedures for responding to the environmental & social

challenges by establishing value for the stakeholders and achieving financial success (Messner,

2016). Many organisations miss out the advantages of the management accounting taking

insights and valuables for resolving the financial issues.

Identifying the financial issues - Lets Grow ltd uses budgetary target, financial and non

financial key performance indicators and benchmarks for identifying the variances and problems

for addressing them on time

Financial Governance – Company should efficiently define the financial governance as well as

understand how it could be applied for preventing or pre-empting the financial issues. Financial

governance could be used by Lets Grow for monitoring the strategy.

Managerial accounting skills – Lets Grow ltd must have knowledge about the features of

effective and efficient managerial accountant. They should understand how skills are applied for

7

keep the costs and expenses under control by making most effective use of the available

resources. It is used for preventing overspendings and increasing the costs and expenses. Cash

budget enable the company to move towards a well defined direction for achieving the goals and

objectives of the business by staying in the limited budgeted funds.

It is used by the management for analysing the year end cash position of company. it is

assessed for ensuring that the company is available with enough monetary funds for meeting the

cash expenses and payments. It represents the financial position of the company at the end of the

year. Cash budgets are prepared by the organisation to enable the management to take required

decision for improving the cash position of company. Companies take steps for making effective

utilisation of the resources and managing the inflows and outflows so that company do not goes

out of cash during the period. Negative cash position reflects that management is not having

enough funds for meeting the expenses. Negative cash position impacts the operations and

functioning of the organisation. Non availability of funds puts stop to production process.

Therefore it is essential for the managers to make necessary arrangements for meeting the

operations of funds in advance so that operations of company are not affected.

e) Adapting management accounting techniques for dealing with the financial problems

Corporation are encountering questions about how the business models are adapting to

strategies business models and the procedures for responding to the environmental & social

challenges by establishing value for the stakeholders and achieving financial success (Messner,

2016). Many organisations miss out the advantages of the management accounting taking

insights and valuables for resolving the financial issues.

Identifying the financial issues - Lets Grow ltd uses budgetary target, financial and non

financial key performance indicators and benchmarks for identifying the variances and problems

for addressing them on time

Financial Governance – Company should efficiently define the financial governance as well as

understand how it could be applied for preventing or pre-empting the financial issues. Financial

governance could be used by Lets Grow for monitoring the strategy.

Managerial accounting skills – Lets Grow ltd must have knowledge about the features of

effective and efficient managerial accountant. They should understand how skills are applied for

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

dealing and preventing such problems like misappropriation of the resources that are used for

growing the business.

Effective systems and strategies – Company for dealing with these financial issues is requires

development of efficient and effective strategies and systems which requires timely reporting. it

requires full disclosure of the financial statement that are responsibly owned and governed by

the organisation.

There are different ways in which accounting can help the management in effectively managing

the financial issues and leading the company towards sustainable success.

Management accounting involves identifying the environment and social trends that are

impacting the capability of company to build value over time.

It could describe impacts of sustainability issues in the strong business terms containing

how it will be impacting the performance of company and its operations.

Management accounting tools and techniques such natural resources, scenario planning,

lifecycle costing and carbon foot printing for assisting the managers to incorporate the

sustainability issues in the decision making process.

Generating reports that include the information over the sustainability effects for

informing pricing & budgeting decisions, investment appraisals and strategic planning

(Weetman, 2019). It established the reporting strategies incorporating sustainability

matters for ensuring relevant financial information is revealed.

Different management accounting systems could be used in managing the internal

process and operations on time. It includes processing the goods and services at time

reducing the wastage of materials in the production process.

f) Critical evaluation of the financial position of Lets Grow based on forecasted projects.

Cash budget of the company could be used for analysing the financial position of company.

Cash budget for the six months reflect that sales and revenues of the company have increased

continuously till April. Month of June and Jul could be seen as months with low sales level.

Months with peak sales are May and August. Purchases have increased continuously over the 6

months. There is stead increase in the expenses of company but the inflows are not increased in

the same proportion to that of the outflows (Quattrone, 2016). Company has shown a cash deficit

in month July and August. This reflects that company has gone out of cash in last months of the

8

growing the business.

Effective systems and strategies – Company for dealing with these financial issues is requires

development of efficient and effective strategies and systems which requires timely reporting. it

requires full disclosure of the financial statement that are responsibly owned and governed by

the organisation.

There are different ways in which accounting can help the management in effectively managing

the financial issues and leading the company towards sustainable success.

Management accounting involves identifying the environment and social trends that are

impacting the capability of company to build value over time.

It could describe impacts of sustainability issues in the strong business terms containing

how it will be impacting the performance of company and its operations.

Management accounting tools and techniques such natural resources, scenario planning,

lifecycle costing and carbon foot printing for assisting the managers to incorporate the

sustainability issues in the decision making process.

Generating reports that include the information over the sustainability effects for

informing pricing & budgeting decisions, investment appraisals and strategic planning

(Weetman, 2019). It established the reporting strategies incorporating sustainability

matters for ensuring relevant financial information is revealed.

Different management accounting systems could be used in managing the internal

process and operations on time. It includes processing the goods and services at time

reducing the wastage of materials in the production process.

f) Critical evaluation of the financial position of Lets Grow based on forecasted projects.

Cash budget of the company could be used for analysing the financial position of company.

Cash budget for the six months reflect that sales and revenues of the company have increased

continuously till April. Month of June and Jul could be seen as months with low sales level.

Months with peak sales are May and August. Purchases have increased continuously over the 6

months. There is stead increase in the expenses of company but the inflows are not increased in

the same proportion to that of the outflows (Quattrone, 2016). Company has shown a cash deficit

in month July and August. This reflects that company has gone out of cash in last months of the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash budget. Inflows and outflows are not managed efficiently that leads to negative cash

balance. It has negative cash position that is required to be improved using effective strategies.

CONCLUSION

Organisation using right managerial accounting systems is able to achieve their goals and

objectives in the desired manner. Managerial accounting is required to provide the management

with accurate and reliable information for ensuring that effective cost structures are appointed by

the company. it enables the management to implement right model for the business. study of

management accounting enhance the understanding about the concepts and techniques for

managing the business operations. MA is considered as the cornerstone and therefore it requires

providing accurate and reliable information. Lets Grow using the management accounting

system could effectively manage the internal operations of business ensuring that company

achieves maximum profits at minimal cost. Management accounting reports provide the

management with all the information that is essential for decision making. Efficient use of the

planning tools enables the company to achieve growth and sustainable success.

9

balance. It has negative cash position that is required to be improved using effective strategies.

CONCLUSION

Organisation using right managerial accounting systems is able to achieve their goals and

objectives in the desired manner. Managerial accounting is required to provide the management

with accurate and reliable information for ensuring that effective cost structures are appointed by

the company. it enables the management to implement right model for the business. study of

management accounting enhance the understanding about the concepts and techniques for

managing the business operations. MA is considered as the cornerstone and therefore it requires

providing accurate and reliable information. Lets Grow using the management accounting

system could effectively manage the internal operations of business ensuring that company

achieves maximum profits at minimal cost. Management accounting reports provide the

management with all the information that is essential for decision making. Efficient use of the

planning tools enables the company to achieve growth and sustainable success.

9

REFERENCES

Books and Journals

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31.pp.45-62.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner

Production.136.pp.237-248.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31. pp.10-30.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems.29.pp.37-58.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Christ, K.L. and Burritt, R.L., 2017. Water management accounting: A framework for corporate

practice. Journal of cleaner production.152. pp.379-386.

10

Books and Journals

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31.pp.45-62.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner

Production.136.pp.237-248.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research, 31, pp.1-9.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research.31. pp.10-30.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems.29.pp.37-58.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Christ, K.L. and Burritt, R.L., 2017. Water management accounting: A framework for corporate

practice. Journal of cleaner production.152. pp.379-386.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.