Management Accounting Report for Prime Furniture Limited

VerifiedAdded on 2023/01/12

|14

|3389

|46

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on cost calculation, financial statement preparation using marginal and absorption costing methods, and interpretation of financial statements. It delves into budgetary control, exploring its benefits, limitations, and various planning tools like operational, cash, and capital budgets. The report also examines pricing strategies, competitor analysis, and the impact of supply and demand. Furthermore, it analyzes the role of management accounting methods in addressing financial problems and achieving sustainable success, including the application of SWOT analysis. The case study focuses on Prime Furniture Limited, offering practical insights into real-world applications of these concepts. The report concludes with a discussion on the importance of financial planning for managing monetary resources and overcoming financial challenges.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

TASK 2...................................................................................................................................................3

P3. Calculation of costs and preparation of financial statements under marginal and absorption costing

method.....................................................................................................................................................3

M2. Accounting techniques to produce financial statements...................................................................6

D2. Interpretation of prepared financial statements.................................................................................6

TASK 3...................................................................................................................................................6

P4. Limitations and benefits of planning tools of budgetary control........................................................6

M3. Use of different planning tools and their application for preparing and forecasting budgets............7

TASK 4...................................................................................................................................................8

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success..............................................................................8

M4. MAS to solve financial issue............................................................................................................9

D3. Importance of financial plans for planning and managing monetary sources which can contribute in

overcoming problems regards to finance...............................................................................................10

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

TASK 2...................................................................................................................................................3

P3. Calculation of costs and preparation of financial statements under marginal and absorption costing

method.....................................................................................................................................................3

M2. Accounting techniques to produce financial statements...................................................................6

D2. Interpretation of prepared financial statements.................................................................................6

TASK 3...................................................................................................................................................6

P4. Limitations and benefits of planning tools of budgetary control........................................................6

M3. Use of different planning tools and their application for preparing and forecasting budgets............7

TASK 4...................................................................................................................................................8

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success..............................................................................8

M4. MAS to solve financial issue............................................................................................................9

D3. Importance of financial plans for planning and managing monetary sources which can contribute in

overcoming problems regards to finance...............................................................................................10

CONCLUSION.........................................................................................................................................10

REFERENCES..........................................................................................................................................11

INTRODUCTION

The term MA is defined as a way of making internal reports by help of financial and non

financial information. There are a wide range of techniques such as absorption, marginal in order

to make financial statements (Arroyo, 2012). The report covers detailed information related to

various accounting techniques, planning tools and use of management accounting systems in

order to solve monetary issues. The company selected for this report is Prime furniture limited.

MAIN BODY

TASK 2

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method.

Micro economic techniques:

Cost- This can be defined as total amount of expenses that occur in order to complete different

types of operations and activities. There are different types of costs such as fixed cost, variable

cost, direct cost, indirect cost and many more.

Cost volume analysis- The cost-benefit analysis is a strategic approach to the model of

weaknesses and strengths of choices used for determining the best method to gain advantages

while maintaining costs, also termed the cost / benefit study or benefit cost analysis.

Cost variance- This can be defined as a process of calculating difference between actual cost and

estimated cost. It is presented in adverse and favorable aspects.

There are a vital number of approaches such as absorption and marginal methods in the field

of planning financial reports. They are used to preparation of financial statements for companies.

Herein, below description of these costing techniques is mentioned in such manner:

Absorption costing method- This is a form of technique of costing that defines and

widely allocates the expense of various activities and operations. The expense of the item

is considered as fixed and non-fixed costs (Chenhall and Moers, 2015).

The term MA is defined as a way of making internal reports by help of financial and non

financial information. There are a wide range of techniques such as absorption, marginal in order

to make financial statements (Arroyo, 2012). The report covers detailed information related to

various accounting techniques, planning tools and use of management accounting systems in

order to solve monetary issues. The company selected for this report is Prime furniture limited.

MAIN BODY

TASK 2

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method.

Micro economic techniques:

Cost- This can be defined as total amount of expenses that occur in order to complete different

types of operations and activities. There are different types of costs such as fixed cost, variable

cost, direct cost, indirect cost and many more.

Cost volume analysis- The cost-benefit analysis is a strategic approach to the model of

weaknesses and strengths of choices used for determining the best method to gain advantages

while maintaining costs, also termed the cost / benefit study or benefit cost analysis.

Cost variance- This can be defined as a process of calculating difference between actual cost and

estimated cost. It is presented in adverse and favorable aspects.

There are a vital number of approaches such as absorption and marginal methods in the field

of planning financial reports. They are used to preparation of financial statements for companies.

Herein, below description of these costing techniques is mentioned in such manner:

Absorption costing method- This is a form of technique of costing that defines and

widely allocates the expense of various activities and operations. The expense of the item

is considered as fixed and non-fixed costs (Chenhall and Moers, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing method- It can be understood as a way of identifying the expenses

involved with different activities. The fixed costs are considered time cost and unit costs

are considered variable costs.

Product costing:

Fixed cost- It is a type of cost that cannot be changed or not affected due to change in production

volume.

Variable cost- It is a type of cost that can be changed or affected due to change in production

volume.

Standard costing- Standard costing combines the expected expense in the accounting records

with the actual cost. Thereafter, the variations between the planned and the actual costs are

reported as indicated

Activity based costing- Activity costing is a costing method, which defines operational tasks and

calculates costs for each operation according to the real use of each product and service. The

approach allocates more direct costs than traditional costs to indirect costs.

Role of costing in setting prices- Costing plays a key role for setting prices because on the basis

of it companies set prices. This is so because if cost is higher than expectation than companies

set price higher, vice versa.

Cost of inventory:

Inventory cost- Inventory costs are the expenses of acquisition, transportation and better

management of cost. There are different types of inventory cost which are as follows:

Ordering cost

Carrying cost

Purchasing cost

Hiring cost

Valuation methods:

involved with different activities. The fixed costs are considered time cost and unit costs

are considered variable costs.

Product costing:

Fixed cost- It is a type of cost that cannot be changed or not affected due to change in production

volume.

Variable cost- It is a type of cost that can be changed or affected due to change in production

volume.

Standard costing- Standard costing combines the expected expense in the accounting records

with the actual cost. Thereafter, the variations between the planned and the actual costs are

reported as indicated

Activity based costing- Activity costing is a costing method, which defines operational tasks and

calculates costs for each operation according to the real use of each product and service. The

approach allocates more direct costs than traditional costs to indirect costs.

Role of costing in setting prices- Costing plays a key role for setting prices because on the basis

of it companies set prices. This is so because if cost is higher than expectation than companies

set price higher, vice versa.

Cost of inventory:

Inventory cost- Inventory costs are the expenses of acquisition, transportation and better

management of cost. There are different types of inventory cost which are as follows:

Ordering cost

Carrying cost

Purchasing cost

Hiring cost

Valuation methods:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

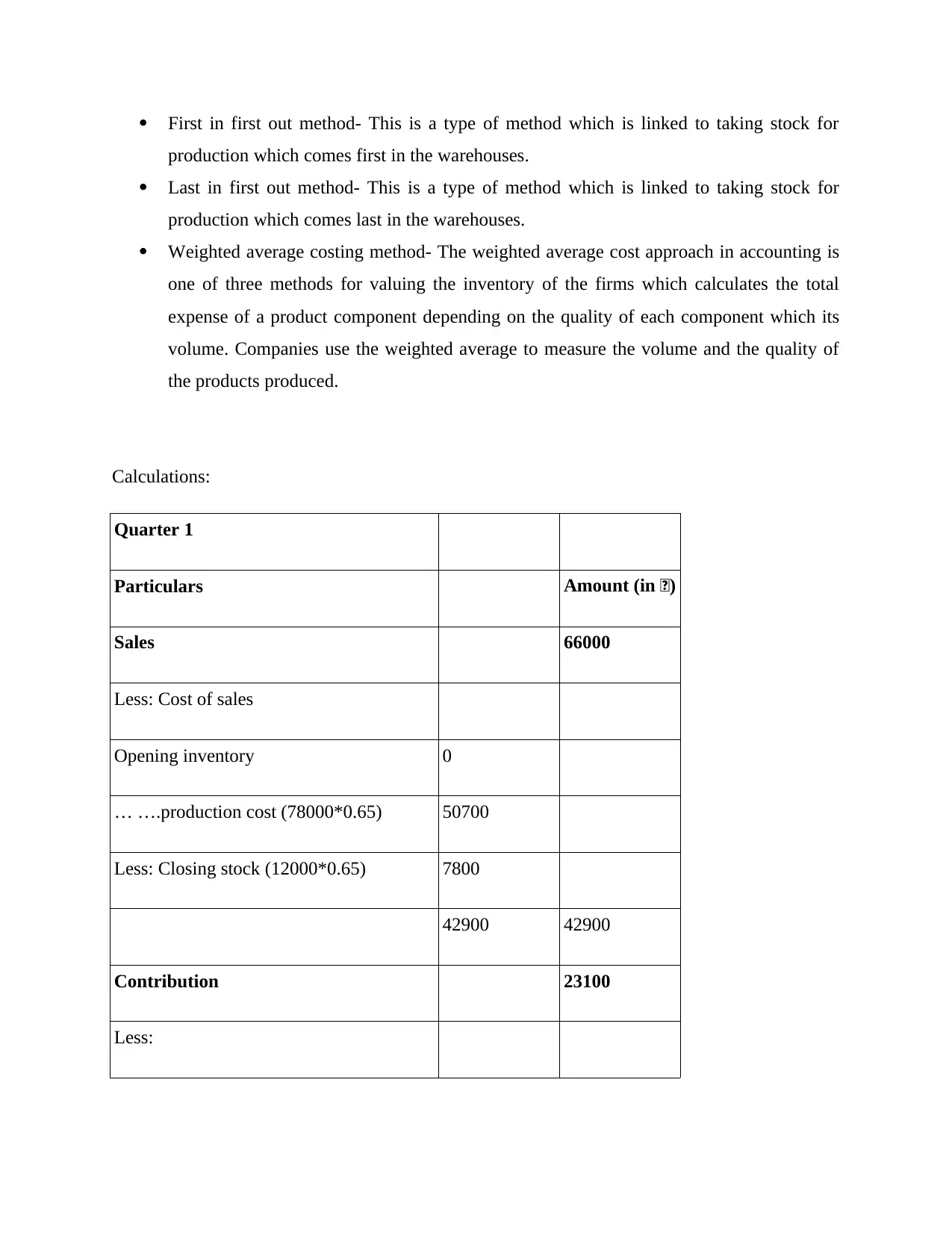

First in first out method- This is a type of method which is linked to taking stock for

production which comes first in the warehouses.

Last in first out method- This is a type of method which is linked to taking stock for

production which comes last in the warehouses.

Weighted average costing method- The weighted average cost approach in accounting is

one of three methods for valuing the inventory of the firms which calculates the total

expense of a product component depending on the quality of each component which its

volume. Companies use the weighted average to measure the volume and the quality of

the products produced.

Calculations:

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

… ….production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

production which comes first in the warehouses.

Last in first out method- This is a type of method which is linked to taking stock for

production which comes last in the warehouses.

Weighted average costing method- The weighted average cost approach in accounting is

one of three methods for valuing the inventory of the firms which calculates the total

expense of a product component depending on the quality of each component which its

volume. Companies use the weighted average to measure the volume and the quality of

the products produced.

Calculations:

Quarter 1

Particulars Amount (in £)

Sales 66000

Less: Cost of sales

Opening inventory 0

… ….production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

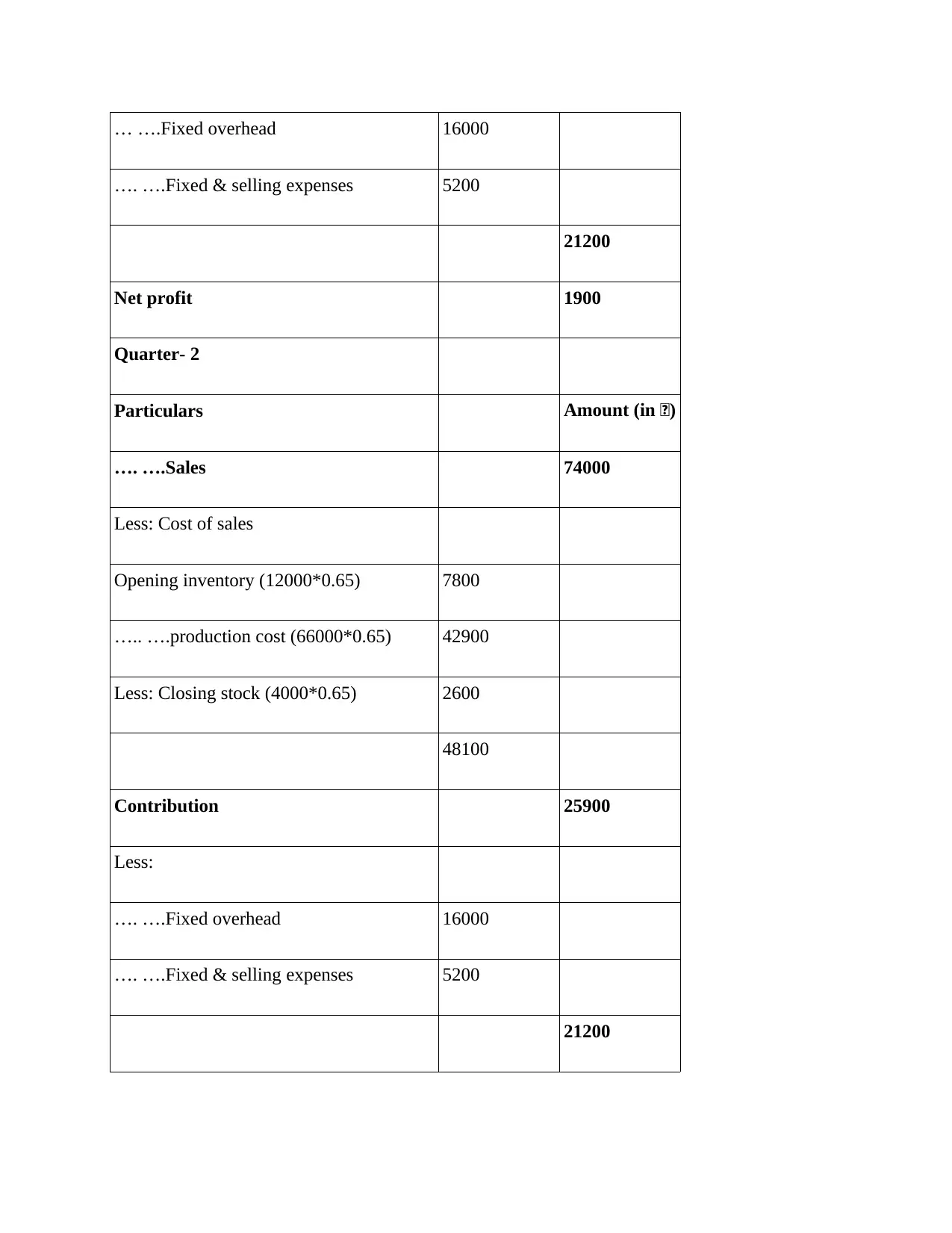

… ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

…. ….Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

…. ….Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars Amount (in £)

…. ….Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

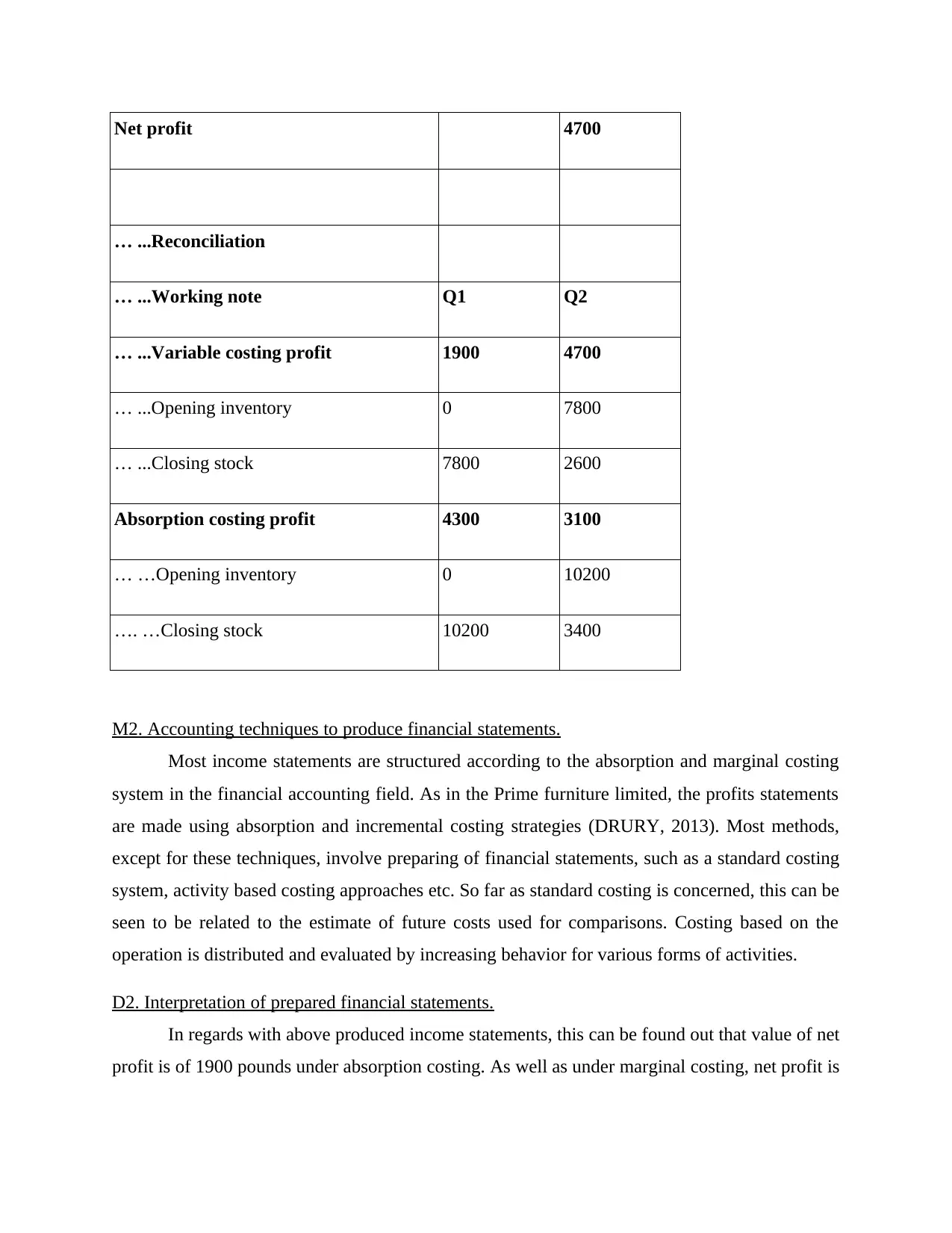

Net profit 4700

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

M2. Accounting techniques to produce financial statements.

Most income statements are structured according to the absorption and marginal costing

system in the financial accounting field. As in the Prime furniture limited, the profits statements

are made using absorption and incremental costing strategies (DRURY, 2013). Most methods,

except for these techniques, involve preparing of financial statements, such as a standard costing

system, activity based costing approaches etc. So far as standard costing is concerned, this can be

seen to be related to the estimate of future costs used for comparisons. Costing based on the

operation is distributed and evaluated by increasing behavior for various forms of activities.

D2. Interpretation of prepared financial statements.

In regards with above produced income statements, this can be found out that value of net

profit is of 1900 pounds under absorption costing. As well as under marginal costing, net profit is

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

M2. Accounting techniques to produce financial statements.

Most income statements are structured according to the absorption and marginal costing

system in the financial accounting field. As in the Prime furniture limited, the profits statements

are made using absorption and incremental costing strategies (DRURY, 2013). Most methods,

except for these techniques, involve preparing of financial statements, such as a standard costing

system, activity based costing approaches etc. So far as standard costing is concerned, this can be

seen to be related to the estimate of future costs used for comparisons. Costing based on the

operation is distributed and evaluated by increasing behavior for various forms of activities.

D2. Interpretation of prepared financial statements.

In regards with above produced income statements, this can be found out that value of net

profit is of 1900 pounds under absorption costing. As well as under marginal costing, net profit is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of 4700 pounds. The cause of variation in profit is consideration of cost in different manner

under both of methods.

TASK 3.

P4. Limitations and benefits of planning tools of budgetary control.

Budgetary control- This may be comprehended as a types of approach and try to regulating of

monetary and anti-financial results by help of lots of different types of budget. In this facet of

position of budgets is important because by aid of these financial strategies management of

organizations take corrective actions for setting more outcomes. A number of budgets are

required and these are as follows:

Operational budget- It is a form of budget which makes it possible for management to

estimate the quantity of material necessary for the completion of various operations for a

certain period of time (Tucker and Lowe, 2014). The accountants plan this estimate for

their managers in the sense Prime furniture limited. With this program, the administrators

take corrective measures with respect to the administration of various operations.

Benefits- This budget is helpful for companies in order to track usage of different types

of resources available in a business entity.

Drawbacks- The key issues under this budget are that it consumes too much time as well

as cost for allocation of expenses.

Cash budget- It is a statement that defined regarding the all cash sales and expenses and

is focused on expectations for particular accounting period of time. The actual budget has

been generated after planning of all budgets such as revenue budget, master budget,

capital budget and purchasing budget (Hiebl, 2014). Financial products and expenditures

and transfers are recoded. It is a document that is mainly prepared for external actors and

cannot be changed easily after publication. In the aspect of above company this budget is

prepared which has some benefits and drawbacks such as:

Benefits- This is beneficial for companies in order to manage daily basis of cash expenses

and income.

under both of methods.

TASK 3.

P4. Limitations and benefits of planning tools of budgetary control.

Budgetary control- This may be comprehended as a types of approach and try to regulating of

monetary and anti-financial results by help of lots of different types of budget. In this facet of

position of budgets is important because by aid of these financial strategies management of

organizations take corrective actions for setting more outcomes. A number of budgets are

required and these are as follows:

Operational budget- It is a form of budget which makes it possible for management to

estimate the quantity of material necessary for the completion of various operations for a

certain period of time (Tucker and Lowe, 2014). The accountants plan this estimate for

their managers in the sense Prime furniture limited. With this program, the administrators

take corrective measures with respect to the administration of various operations.

Benefits- This budget is helpful for companies in order to track usage of different types

of resources available in a business entity.

Drawbacks- The key issues under this budget are that it consumes too much time as well

as cost for allocation of expenses.

Cash budget- It is a statement that defined regarding the all cash sales and expenses and

is focused on expectations for particular accounting period of time. The actual budget has

been generated after planning of all budgets such as revenue budget, master budget,

capital budget and purchasing budget (Hiebl, 2014). Financial products and expenditures

and transfers are recoded. It is a document that is mainly prepared for external actors and

cannot be changed easily after publication. In the aspect of above company this budget is

prepared which has some benefits and drawbacks such as:

Benefits- This is beneficial for companies in order to manage daily basis of cash expenses

and income.

Drawbacks- This budget is based on assumptions so companies cannot rely on it

completely for further financial plans.

Capital budget- Any divisions or lower budgets provide a complete budget of a company.

It finds that the recording of potential sales, production levels, expenditure in resources

and even tons to be gained and repayable is a costly corporate strategy. In accordance

with Prime furniture limited, the balance sheet as well as the income statement is

determined according to the schedule.

Benefits- With a detailed budgeted review summary of Prime furniture limited’s financial

situation is analyzed (Kokubu and Kitada, 2015).

Drawback- The main issue of this budget is that it is difficult to make modifications

under it.

Pricing:

Pricing strategies:

Penetration pricing strategy- The penetration pricing strategy initially reduces the price of

a product to reach a large portion of the market rapidly. The approach works for

consumers moving to the new company because of the cheaper price

Skimming pricing strategy- Price skimming is a pricing tactic whereby a marketer

initially sets a relatively high initial price for an item or service and then lowers the price

over time. There was a misunderstanding. The organization lowers the price to draw

another market-sensitive group, when competition from the first customers is satisfied.

How competitors determine prices- Companies set prices in accordance of market trends and

activities of competitors. They assess key activities which are being performed and on the basis

of it they set prices.

Supply-demand consideration: Supply and demand is a price-determination economic concept on

a sector. It states that the price of the unit of a specific product or other exchanged item, such as

labor or liquid financial assets, shall differ until the quantity required (on current prices) is settled

in a situation where it is equal to that provided (on current prices) which leads to a balanced

economic demand and supply.

completely for further financial plans.

Capital budget- Any divisions or lower budgets provide a complete budget of a company.

It finds that the recording of potential sales, production levels, expenditure in resources

and even tons to be gained and repayable is a costly corporate strategy. In accordance

with Prime furniture limited, the balance sheet as well as the income statement is

determined according to the schedule.

Benefits- With a detailed budgeted review summary of Prime furniture limited’s financial

situation is analyzed (Kokubu and Kitada, 2015).

Drawback- The main issue of this budget is that it is difficult to make modifications

under it.

Pricing:

Pricing strategies:

Penetration pricing strategy- The penetration pricing strategy initially reduces the price of

a product to reach a large portion of the market rapidly. The approach works for

consumers moving to the new company because of the cheaper price

Skimming pricing strategy- Price skimming is a pricing tactic whereby a marketer

initially sets a relatively high initial price for an item or service and then lowers the price

over time. There was a misunderstanding. The organization lowers the price to draw

another market-sensitive group, when competition from the first customers is satisfied.

How competitors determine prices- Companies set prices in accordance of market trends and

activities of competitors. They assess key activities which are being performed and on the basis

of it they set prices.

Supply-demand consideration: Supply and demand is a price-determination economic concept on

a sector. It states that the price of the unit of a specific product or other exchanged item, such as

labor or liquid financial assets, shall differ until the quantity required (on current prices) is settled

in a situation where it is equal to that provided (on current prices) which leads to a balanced

economic demand and supply.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic planning:

SWOT Analysis- This is a type of technique which is related to assessing companies’ strength,

weakness, opportunities and threats for a particular time period. This technique has below

mentioned benefits and drawbacks such as:

Benefits: SWOT analysis may be extended to an organization, organizational unit, person or

team. In fact, the research will endorse a variety of project goals. The SWOT approach can, for

example, be used for assessing a commodity or brand, a purchase or partnership, or for

externalizing a functioning business. Therefore, SWOT analysis can help to determine a

particular source of supply, business cycle, and product demand or technology implementation.

Drawbacks: SWOT analysis refers to four sets of strong points, vulnerabilities, possibilities and

risks in individual countries. But the method does not provide a system to list the value of one

element over another. It is however difficult to evaluate the true effect of any aspect on the

target.

M3. Use of different planning tools and their application for preparing and forecasting budgets.

There are various types of budgets used by companies for better financial decision-

making. Their reports include a number of budgets such as the Cash budget, the operational

budget and capital budget in the form of above Prime furniture. All of these forecasts can be used

in an effective management of their money assets and to reliable planning of various operations.

In the precise calculation of income and spending, all these expenditures play a major part

(Kotas, 2014). This is likely as management of this organization analyzes details calculated in

previous years in order to predict new operations. It can therefore be said that budgetary

management forecasting devices are too important to reliably project various types of financial

operations.

SWOT Analysis- This is a type of technique which is related to assessing companies’ strength,

weakness, opportunities and threats for a particular time period. This technique has below

mentioned benefits and drawbacks such as:

Benefits: SWOT analysis may be extended to an organization, organizational unit, person or

team. In fact, the research will endorse a variety of project goals. The SWOT approach can, for

example, be used for assessing a commodity or brand, a purchase or partnership, or for

externalizing a functioning business. Therefore, SWOT analysis can help to determine a

particular source of supply, business cycle, and product demand or technology implementation.

Drawbacks: SWOT analysis refers to four sets of strong points, vulnerabilities, possibilities and

risks in individual countries. But the method does not provide a system to list the value of one

element over another. It is however difficult to evaluate the true effect of any aspect on the

target.

M3. Use of different planning tools and their application for preparing and forecasting budgets.

There are various types of budgets used by companies for better financial decision-

making. Their reports include a number of budgets such as the Cash budget, the operational

budget and capital budget in the form of above Prime furniture. All of these forecasts can be used

in an effective management of their money assets and to reliable planning of various operations.

In the precise calculation of income and spending, all these expenditures play a major part

(Kotas, 2014). This is likely as management of this organization analyzes details calculated in

previous years in order to predict new operations. It can therefore be said that budgetary

management forecasting devices are too important to reliably project various types of financial

operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success.

Monetary issues- The rivalry in today's business scenario is increasing which is leading to

monetary problems. The inadequate preparation and execution of a policy establish such issues.

In general, financial difficulties emerge from the shortage of revenue outlets, through which

businesses struggle to carry out different functions (Otley and Emmanuel, 2013). Here are some

specific financial challenges that most of the businesses face in this way:

Errors in accounting records- This can be described as a form of financial problem linked

to the deliberate or accidental distortion of figures, which contributes to the incorrect

preparing of accounts. As a consequence, businesses cannot find actual revenues,

acquisitions and so much more owing to this financial problem. In the above Prime

furniture limited, they face this problem that affects the financial statements they have

prepared (Suomala and Lyly-Yrjänäinen, 2012).

Inadequate protection of financial assets- The risk of losing investments is a kind of

investment issue. This dilemma exists because of a loss of management of fixed and

unfixed assets. As a result, businesses experience other problems, including resources

absence and much more.

MA methods to respond financial problems:

Benchmarking- This strategy relates financial aspects of an organization to competing

businesses with the goal of identifying adverse variances (Sánchez-Rodríguez and

Spraakman, 2012). As a consequence, the business can figure out the factors which lead

to the financial problem. They use this method in the above business to assess their

particular monetary problem. The financial aspects are compared to the rest of the firms.

Key performance indicator- It can be described as a methodology linked to the correct

assessment of financial and non-financial aspects. The financial dimension covers the

productivity of the company, the costs etc. whereas the stress level of employees, relation

etc., is included in the non-financial aspect.

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success.

Monetary issues- The rivalry in today's business scenario is increasing which is leading to

monetary problems. The inadequate preparation and execution of a policy establish such issues.

In general, financial difficulties emerge from the shortage of revenue outlets, through which

businesses struggle to carry out different functions (Otley and Emmanuel, 2013). Here are some

specific financial challenges that most of the businesses face in this way:

Errors in accounting records- This can be described as a form of financial problem linked

to the deliberate or accidental distortion of figures, which contributes to the incorrect

preparing of accounts. As a consequence, businesses cannot find actual revenues,

acquisitions and so much more owing to this financial problem. In the above Prime

furniture limited, they face this problem that affects the financial statements they have

prepared (Suomala and Lyly-Yrjänäinen, 2012).

Inadequate protection of financial assets- The risk of losing investments is a kind of

investment issue. This dilemma exists because of a loss of management of fixed and

unfixed assets. As a result, businesses experience other problems, including resources

absence and much more.

MA methods to respond financial problems:

Benchmarking- This strategy relates financial aspects of an organization to competing

businesses with the goal of identifying adverse variances (Sánchez-Rodríguez and

Spraakman, 2012). As a consequence, the business can figure out the factors which lead

to the financial problem. They use this method in the above business to assess their

particular monetary problem. The financial aspects are compared to the rest of the firms.

Key performance indicator- It can be described as a methodology linked to the correct

assessment of financial and non-financial aspects. The financial dimension covers the

productivity of the company, the costs etc. whereas the stress level of employees, relation

etc., is included in the non-financial aspect.

Financial governance- It can be recognized as a strategy in which a corporate entity's

entire financial activity is reported accurately for a specific period of time (Schaltegger,

S. and Burritt, R., 2017). Using this method, real monetary challenges are defined and

theoretical solutions are used to solve the problem.

Management accountant skills:

Better communication skills- Effective accountant should have better communication

skills so that financial information can be shared inside company.

Effective knowledge of accounting concepts- As well as accounts must have complete

knowledge of accounting so that financial statements can be produced.

These accounting skills can be used to overcome financial issues. This is so because on the basis

of it, companies can overcome from any type of issue and can guide to manager of companies to

solve issues.

Comparison of companies in order to solve financial issues by help of MAS:

Basis of

difference

London beer factory Orbit beers

Monetary issue Their financial issue is related to

accounting errors in this business. It

prohibits them from learning actual

business details.

The issue confronting the organization

is the absence of asset protection. As a

result, the valuation of properties

cannot be monitored and assessed.

Techniques to

solve issues

This organization used benchmarking

technology to solve the financial

problem. They contrasted their

financial statements with another

organization using this method in order

to discover mistakes and thus solved

their problem.

They also used key indicator

technology for results. They evaluated

the financial implications of this

method and addressed their issue. It

was made possible by measuring the

true worth of properties and by

matching them with the normal value.

entire financial activity is reported accurately for a specific period of time (Schaltegger,

S. and Burritt, R., 2017). Using this method, real monetary challenges are defined and

theoretical solutions are used to solve the problem.

Management accountant skills:

Better communication skills- Effective accountant should have better communication

skills so that financial information can be shared inside company.

Effective knowledge of accounting concepts- As well as accounts must have complete

knowledge of accounting so that financial statements can be produced.

These accounting skills can be used to overcome financial issues. This is so because on the basis

of it, companies can overcome from any type of issue and can guide to manager of companies to

solve issues.

Comparison of companies in order to solve financial issues by help of MAS:

Basis of

difference

London beer factory Orbit beers

Monetary issue Their financial issue is related to

accounting errors in this business. It

prohibits them from learning actual

business details.

The issue confronting the organization

is the absence of asset protection. As a

result, the valuation of properties

cannot be monitored and assessed.

Techniques to

solve issues

This organization used benchmarking

technology to solve the financial

problem. They contrasted their

financial statements with another

organization using this method in order

to discover mistakes and thus solved

their problem.

They also used key indicator

technology for results. They evaluated

the financial implications of this

method and addressed their issue. It

was made possible by measuring the

true worth of properties and by

matching them with the normal value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.