Management Accounting Report: Costing and Reporting for J. Rotherham

VerifiedAdded on 2023/01/12

|11

|2316

|40

Report

AI Summary

This report delves into the realm of management accounting, offering a comprehensive analysis of its principles and applications within the context of the UK-based stone manufacturing company, J Rotherham. The report begins by defining management accounting and highlighting its significance in decision-making, planning, and performance management, crucial for any business. It then explores the various management accounting systems utilized by J Rotherham, including inventory management, price optimization, and cost accounting systems. Furthermore, the report examines different types of management accounting reports, such as accounts receivable, performance, and inventory management reports. A significant portion of the report is dedicated to cost calculation techniques, including manufacturing, product and period, variable and fixed, direct and indirect, differential, opportunity, and sunk costs. The report also discusses specific costing techniques like marginal and absorption costing, along with their advantages and disadvantages. The conclusion emphasizes the value of management accounting in aiding managerial decisions and achieving organizational goals. References to relevant academic sources are provided to support the analysis.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Activity 2......................................................................................................................................................3

Calculation of costs using appropriate techniques..................................................................................3

Activity 3: Covered in PPT............................................................................................................................5

Activity 4: Covered in PPT............................................................................................................................5

CONCLUSION...............................................................................................................................................5

REFERENCES................................................................................................................................................7

Activity 2......................................................................................................................................................3

Calculation of costs using appropriate techniques..................................................................................3

Activity 3: Covered in PPT............................................................................................................................5

Activity 4: Covered in PPT............................................................................................................................5

CONCLUSION...............................................................................................................................................5

REFERENCES................................................................................................................................................7

INTRODUCTION

Management accounting is a profession in which consist of partnering in management

decision making, devising panning and performance management system (Askarany, 2016).

Along with offering professional advising in financial activities and control to analysis of

administration in order to execution and implication of effective business strategy. This term has

been applied in broadly in business environment and all the activities are conducted according to

atmosphere. In any business sector, it is required to understand how this term utilized for

financial data aid planning decision and the observing and control of finance with an

organisation Managers use the provisions of accounting information in order to better inform

themselves before understand all the matters in regard of business that aids their management as

well as performance of control functions. For understanding this select J Rotherham which is a

UK based organization. It was introduced in 1930 to manufacturer stone and also does

architectural work on stone. This report comprises of various topics like requirement if different

systems and usage of managing reports. Along with use costing technique to set up cost for

business to generate more profitability and take different planning tools that is utilized for

budgetary control. To sort out financial problems by accounting system within industry.

PART A

Activity 1

Management accounting along with important requirements of different

systems

Management accounting is described as the pathway of tracking, managing as well as

measuring the effectiveness of an organisation over a given period of time (Banker and et.al.,

2018). It is quite useful for administrative interested parties as it can assist them assess the

organization's current status. The accounting systems are part of internal system which is applied

by management to conduct daily routing activities. J Rotherham Limited is a hand carved stone

manufacturing business that currently operates in Yorkshire UK. It is utilized by all

organizations to maintain track of all transactions and improve corporate productivity.

Management accounting is a profession in which consist of partnering in management

decision making, devising panning and performance management system (Askarany, 2016).

Along with offering professional advising in financial activities and control to analysis of

administration in order to execution and implication of effective business strategy. This term has

been applied in broadly in business environment and all the activities are conducted according to

atmosphere. In any business sector, it is required to understand how this term utilized for

financial data aid planning decision and the observing and control of finance with an

organisation Managers use the provisions of accounting information in order to better inform

themselves before understand all the matters in regard of business that aids their management as

well as performance of control functions. For understanding this select J Rotherham which is a

UK based organization. It was introduced in 1930 to manufacturer stone and also does

architectural work on stone. This report comprises of various topics like requirement if different

systems and usage of managing reports. Along with use costing technique to set up cost for

business to generate more profitability and take different planning tools that is utilized for

budgetary control. To sort out financial problems by accounting system within industry.

PART A

Activity 1

Management accounting along with important requirements of different

systems

Management accounting is described as the pathway of tracking, managing as well as

measuring the effectiveness of an organisation over a given period of time (Banker and et.al.,

2018). It is quite useful for administrative interested parties as it can assist them assess the

organization's current status. The accounting systems are part of internal system which is applied

by management to conduct daily routing activities. J Rotherham Limited is a hand carved stone

manufacturing business that currently operates in Yorkshire UK. It is utilized by all

organizations to maintain track of all transactions and improve corporate productivity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management relates to the scheduling, coordination, resources, and monitoring of company

knowledge and operations. This helps to better manage the records and growing organization's

functioning efficiency. Management accounting's key target is quick payment and company

decision taking. There are mentioned some management accounting system are:

Inventory management system: This is an effective system that can enable enterprise

company to keep stock details and to position next orders appropriately (Dierynck and Labro,

2018). This is mainly included and is used routinely in resource management. Managers at J

Rotherham use this method to monitor and maintain the product or stock inside a company. It is

necessary for management in this business to monitor the raw ingredients and handle it to

enhance the competitiveness. This is handled through a program to analyze the data and produce

documents. The manager of J Rotherham uses different method that is described as:

FIFO: This implies first of all that the business of states will market the commodity that

first came.

LIFO: In these method materials come is last that was selling will first.

AVOC: Organization sells products and services throughout this system that help

determine average growth costs.

Price optimization system: This is the framework that completes a company's quantitative

order to determine and consumers focus on goods and services for various prices (Feng and Ho,

2016). Executives are using it to adjust commodity costs and control the consumer. J Rotherham

is a maker that operates as a builder on marble and modernist work that affects clients. This uses

the tools to set market prices and preserve organizational profit margins. Such as J Rotherham

manager incur all costs and expenditures when making the goods, and establish the fair price.

This method allows companies to achieve targets such as income maximization in a business.

Cost accounting system: This is an innovative method that uses a functional inventory

system to monitor manufacturing practices by producers and other business concerns. Managing

the expenses and the reports in addition to making money is necessary in all organizations.

Basically, this method works by monitoring raw resources as J Rotherham's supervisors get by

the manufacturing process and gradually convert in to final products in actual period of time. It

lets managers concentrate on cost and enhance the manufacturing process which helps to

knowledge and operations. This helps to better manage the records and growing organization's

functioning efficiency. Management accounting's key target is quick payment and company

decision taking. There are mentioned some management accounting system are:

Inventory management system: This is an effective system that can enable enterprise

company to keep stock details and to position next orders appropriately (Dierynck and Labro,

2018). This is mainly included and is used routinely in resource management. Managers at J

Rotherham use this method to monitor and maintain the product or stock inside a company. It is

necessary for management in this business to monitor the raw ingredients and handle it to

enhance the competitiveness. This is handled through a program to analyze the data and produce

documents. The manager of J Rotherham uses different method that is described as:

FIFO: This implies first of all that the business of states will market the commodity that

first came.

LIFO: In these method materials come is last that was selling will first.

AVOC: Organization sells products and services throughout this system that help

determine average growth costs.

Price optimization system: This is the framework that completes a company's quantitative

order to determine and consumers focus on goods and services for various prices (Feng and Ho,

2016). Executives are using it to adjust commodity costs and control the consumer. J Rotherham

is a maker that operates as a builder on marble and modernist work that affects clients. This uses

the tools to set market prices and preserve organizational profit margins. Such as J Rotherham

manager incur all costs and expenditures when making the goods, and establish the fair price.

This method allows companies to achieve targets such as income maximization in a business.

Cost accounting system: This is an innovative method that uses a functional inventory

system to monitor manufacturing practices by producers and other business concerns. Managing

the expenses and the reports in addition to making money is necessary in all organizations.

Basically, this method works by monitoring raw resources as J Rotherham's supervisors get by

the manufacturing process and gradually convert in to final products in actual period of time. It

lets managers concentrate on cost and enhance the manufacturing process which helps to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintain productivity. Giving correct costs is needed by using tools that help to keep the

profitability.

Different methods used by industry for reporting

Management accounting reporting is method which is applied by different organisation to

produce reports in monthly as well as yearly bass (Maziriri and Mapuranga, 2017). Such as J.

Rotherham used this strategy to make effective decisions for the betterment of a business entity.

There are discussed various kinds of reports that produced by company such as:

Accounts receivable report: It is the collecting method which ensures customers are

paying their receipts. Effective control of liabilities tends to prevent late payment or failure to

pay. It's a fast and efficient way to improve the monetary or leverage status of the business. The

report is also used by management of J Rotherham Limited to determine the effectiveness of the

credit and collection functions of the company. It is beneficial for the company as it may help to

strengthen the credit policy.

Performance report: Performance Report assessed the outcome of an operation that an

person conducts. This study compares the real end outcome with the typical output of a given

operation and identifies variability. For instance, Annual financial report review for every worker

that in the measurement concept what they related to an organization. J Rotherham compares the

different factors surrounding the worker's current capacity with their real quality, which will help

to boost quality and profitability.

Inventory management report: This is a study that demonstrates the understanding of

stock turnover in actual time across a reporting term (Nørreklit, Raffnsøe-Møller and Mitchell,

2016). This report is developed by the producing businesses to keep track of the stock. In J

Rotherham the administrators are expected to hold accurate product details that the organization

uses to carry out its operational tasks. It helps to monitor the statement that can effectively treat

inventories and control stocks in real time.

Activity 2

Calculation of costs using appropriate techniques

Types of costs in management accounting-

profitability.

Different methods used by industry for reporting

Management accounting reporting is method which is applied by different organisation to

produce reports in monthly as well as yearly bass (Maziriri and Mapuranga, 2017). Such as J.

Rotherham used this strategy to make effective decisions for the betterment of a business entity.

There are discussed various kinds of reports that produced by company such as:

Accounts receivable report: It is the collecting method which ensures customers are

paying their receipts. Effective control of liabilities tends to prevent late payment or failure to

pay. It's a fast and efficient way to improve the monetary or leverage status of the business. The

report is also used by management of J Rotherham Limited to determine the effectiveness of the

credit and collection functions of the company. It is beneficial for the company as it may help to

strengthen the credit policy.

Performance report: Performance Report assessed the outcome of an operation that an

person conducts. This study compares the real end outcome with the typical output of a given

operation and identifies variability. For instance, Annual financial report review for every worker

that in the measurement concept what they related to an organization. J Rotherham compares the

different factors surrounding the worker's current capacity with their real quality, which will help

to boost quality and profitability.

Inventory management report: This is a study that demonstrates the understanding of

stock turnover in actual time across a reporting term (Nørreklit, Raffnsøe-Møller and Mitchell,

2016). This report is developed by the producing businesses to keep track of the stock. In J

Rotherham the administrators are expected to hold accurate product details that the organization

uses to carry out its operational tasks. It helps to monitor the statement that can effectively treat

inventories and control stocks in real time.

Activity 2

Calculation of costs using appropriate techniques

Types of costs in management accounting-

Manufacturing costs- These types of costs can be broken up into three categories- direct

materials, direct labor and manufacturing overhead (Endenich, Trapp and Brandau, 2017). Direct

material costs are incurred on production of products, labor costs are incurred on payment of

wages to workers and manufacturing overheads are incurred on expenses other than material and

labor on the production process. In J Rotherham Limited these types of costs are incurred.

Product and period costs- Product and period costs are those expenses which are

incurred in a business other than manufacturing costs (Fleischman, Johnson and Walker, 2017).

In J Rotherham Limited which is a manufacturing company these types of costs are incurred in

processes other than production.

Variable and fixed costs- Variable costs are associated with the units of output produced

and change according to it. Fixed costs are not associated with the units of output produced and

are constant in nature. Both these types of costs are incurred in J Rotherham Limited.

Direct and indirect costs- Direct costs are associated directly with the products and

services of the enterprise. Indirect costs are associated with the indirect expenses which are

incurred in business having no relation with the production of goods. In Rotherham Limited both

these types of costs are incurred.

Differential costs- In management accounting, manager sometimes has to decide

between two options. Both of them are reviewed and after that a decision is taken to select the

best one according to the needs and requirements of the organization. Thus in doing so costs are

incurred which are termed as differential costs. In J Rotherham Limited, sometimes these types

of decisions need to be taken and thus differential costs are incurred.

Opportunity costs- These are costs which cannot be valued in terms of money but are

present in terms of an available opportunity for a business from where it can profit. J Rotherham

Limited also has many opportunities which are reflected in terms of opportunity cost.

Sunk cost- Sometimes costs are incurred in enterprises in form of assets which were once

useful but are not useful currently. It is so because these assets do not have a scrap value which

can be realized. As J Rotherham is a manufacturing company it has various assets which are

discarded without realizing scrap value and thus sunk cost is incurred.

Techniques used for calculation of costs in management accounting-

Following techniques can be used for calculation of costs in management accounting in J

Rotherham Limited-

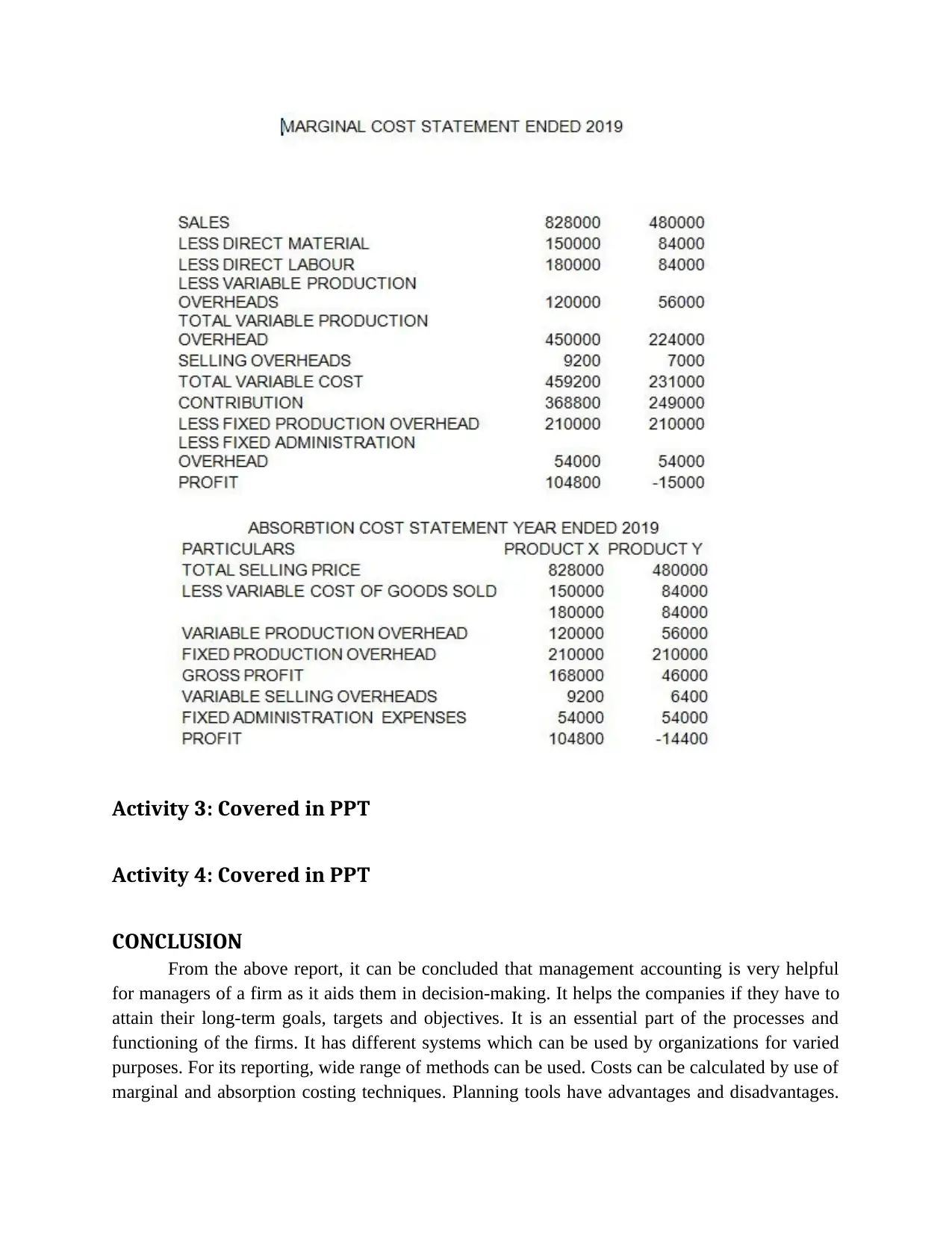

Marginal costing- In this technique, variable cost is charged to the units of output while

fixed cost is written off against the contribution (Gomez-Conde, Lunkes and Rosa, 2019). J

Rotherham Limited can use it effectively to calculate its costs.

materials, direct labor and manufacturing overhead (Endenich, Trapp and Brandau, 2017). Direct

material costs are incurred on production of products, labor costs are incurred on payment of

wages to workers and manufacturing overheads are incurred on expenses other than material and

labor on the production process. In J Rotherham Limited these types of costs are incurred.

Product and period costs- Product and period costs are those expenses which are

incurred in a business other than manufacturing costs (Fleischman, Johnson and Walker, 2017).

In J Rotherham Limited which is a manufacturing company these types of costs are incurred in

processes other than production.

Variable and fixed costs- Variable costs are associated with the units of output produced

and change according to it. Fixed costs are not associated with the units of output produced and

are constant in nature. Both these types of costs are incurred in J Rotherham Limited.

Direct and indirect costs- Direct costs are associated directly with the products and

services of the enterprise. Indirect costs are associated with the indirect expenses which are

incurred in business having no relation with the production of goods. In Rotherham Limited both

these types of costs are incurred.

Differential costs- In management accounting, manager sometimes has to decide

between two options. Both of them are reviewed and after that a decision is taken to select the

best one according to the needs and requirements of the organization. Thus in doing so costs are

incurred which are termed as differential costs. In J Rotherham Limited, sometimes these types

of decisions need to be taken and thus differential costs are incurred.

Opportunity costs- These are costs which cannot be valued in terms of money but are

present in terms of an available opportunity for a business from where it can profit. J Rotherham

Limited also has many opportunities which are reflected in terms of opportunity cost.

Sunk cost- Sometimes costs are incurred in enterprises in form of assets which were once

useful but are not useful currently. It is so because these assets do not have a scrap value which

can be realized. As J Rotherham is a manufacturing company it has various assets which are

discarded without realizing scrap value and thus sunk cost is incurred.

Techniques used for calculation of costs in management accounting-

Following techniques can be used for calculation of costs in management accounting in J

Rotherham Limited-

Marginal costing- In this technique, variable cost is charged to the units of output while

fixed cost is written off against the contribution (Gomez-Conde, Lunkes and Rosa, 2019). J

Rotherham Limited can use it effectively to calculate its costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages-

Marginal costing is an approach which is constant in nature and delivers results

consistently for a business.

Marginal costing effectively helps a business in controlling its costs.

Disadvantages-

The use of marginal costing technique makes it quite difficult to analyze the overheads.

Sometimes this technique involves assumptions which are quite unrealistic.

Absorption costing- In this technique, the full cost associated with manufacturing of a

product is taken into consideration including overheads (Lowe, 2019). Thus it is useful

for manufacturing firms like J Rotherham Limited.

Advantages-

Its usage is compliant with the Generally Accepted Accounting Principles (GAAP).

It takes into account all the costs associated with the production process.

Disadvantages-

The use of this technique can result in skewing of profit or loss which can mislead the

stakeholders of a business enterprise.

Its usage doesn’t help in improving the overall operational efficiency and therefore it is

not useful in this part.

Marginal costing is an approach which is constant in nature and delivers results

consistently for a business.

Marginal costing effectively helps a business in controlling its costs.

Disadvantages-

The use of marginal costing technique makes it quite difficult to analyze the overheads.

Sometimes this technique involves assumptions which are quite unrealistic.

Absorption costing- In this technique, the full cost associated with manufacturing of a

product is taken into consideration including overheads (Lowe, 2019). Thus it is useful

for manufacturing firms like J Rotherham Limited.

Advantages-

Its usage is compliant with the Generally Accepted Accounting Principles (GAAP).

It takes into account all the costs associated with the production process.

Disadvantages-

The use of this technique can result in skewing of profit or loss which can mislead the

stakeholders of a business enterprise.

Its usage doesn’t help in improving the overall operational efficiency and therefore it is

not useful in this part.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity 3: Covered in PPT

Activity 4: Covered in PPT

CONCLUSION

From the above report, it can be concluded that management accounting is very helpful

for managers of a firm as it aids them in decision-making. It helps the companies if they have to

attain their long-term goals, targets and objectives. It is an essential part of the processes and

functioning of the firms. It has different systems which can be used by organizations for varied

purposes. For its reporting, wide range of methods can be used. Costs can be calculated by use of

marginal and absorption costing techniques. Planning tools have advantages and disadvantages.

Activity 4: Covered in PPT

CONCLUSION

From the above report, it can be concluded that management accounting is very helpful

for managers of a firm as it aids them in decision-making. It helps the companies if they have to

attain their long-term goals, targets and objectives. It is an essential part of the processes and

functioning of the firms. It has different systems which can be used by organizations for varied

purposes. For its reporting, wide range of methods can be used. Costs can be calculated by use of

marginal and absorption costing techniques. Planning tools have advantages and disadvantages.

Organizations can use different systems of management accounting to solve their various

financial problems.

financial problems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Askarany, D., 2016. Attributes of innovation and management accounting

changes. Contemporary Management Research, pp.455-466.

Banker, R. D. and et.al., 2018. Cost management research. Journal of Management Accounting

Research. 30(3). pp.187-209.

Dierynck, B. and Labro, E., 2018. Management accounting information properties and

operations management. Foundations and Trends® in Technology, Information and Operations

Management. 12(1). pp.1-114.

Endenich, C., Trapp, R. and Brandau, M., 2017. Management accounting networks in corporate

processes–a cross-national study. Journal of Accounting & Organizational Change.

Feng, S. and Ho, C. Y., 2016. The real option approach to adoption or discontinuation of a

management accounting innovation: the case of activity-based costing. Review of Quantitative

Finance and Accounting. 47(3). pp.835-856.

Fleischman, G. M., Johnson, E. N. and Walker, K. B., 2017. An exploratory examination of

management accounting service and information quality. Journal of Management Accounting

Research. 29(2). pp.11-31.

Gomez-Conde, J., Lunkes, R. J. and Rosa, F. S., 2019. Environmental innovation practices and

operational performance. The joint effects of management accounting and control systems and

environmental training. Accounting, Auditing & Accountability Journal.

Lowe, E. A., 2019. On the idea of a management control system: integrating accounting and

management control. Management Control Theory. p.63.

Maziriri, E. T. and Mapuranga, M., 2017. The impact of management accounting practices

(maps) on the business performance of small and medium enterprises within the Gauteng

Province of South Africa. The Journal of Accounting and Management. 7(2).

Books and Journals:

Askarany, D., 2016. Attributes of innovation and management accounting

changes. Contemporary Management Research, pp.455-466.

Banker, R. D. and et.al., 2018. Cost management research. Journal of Management Accounting

Research. 30(3). pp.187-209.

Dierynck, B. and Labro, E., 2018. Management accounting information properties and

operations management. Foundations and Trends® in Technology, Information and Operations

Management. 12(1). pp.1-114.

Endenich, C., Trapp, R. and Brandau, M., 2017. Management accounting networks in corporate

processes–a cross-national study. Journal of Accounting & Organizational Change.

Feng, S. and Ho, C. Y., 2016. The real option approach to adoption or discontinuation of a

management accounting innovation: the case of activity-based costing. Review of Quantitative

Finance and Accounting. 47(3). pp.835-856.

Fleischman, G. M., Johnson, E. N. and Walker, K. B., 2017. An exploratory examination of

management accounting service and information quality. Journal of Management Accounting

Research. 29(2). pp.11-31.

Gomez-Conde, J., Lunkes, R. J. and Rosa, F. S., 2019. Environmental innovation practices and

operational performance. The joint effects of management accounting and control systems and

environmental training. Accounting, Auditing & Accountability Journal.

Lowe, E. A., 2019. On the idea of a management control system: integrating accounting and

management control. Management Control Theory. p.63.

Maziriri, E. T. and Mapuranga, M., 2017. The impact of management accounting practices

(maps) on the business performance of small and medium enterprises within the Gauteng

Province of South Africa. The Journal of Accounting and Management. 7(2).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nørreklit, H., Raffnsøe-Møller, M. and Mitchell, F., 2016. A pragmatic constructivist approach

to accounting practice and research. Qualitative Research in Accounting & Management.

to accounting practice and research. Qualitative Research in Accounting & Management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.