Nelson College HND Business: Management Accounting Report and Analysis

VerifiedAdded on 2023/01/12

|13

|2934

|24

Report

AI Summary

This report delves into the core concepts of management accounting, examining its significance in modern business operations. It analyzes various management accounting systems, including cost accounting, inventory management, and job costing, highlighting their roles in decision-making and strategic planning. The report explores tools used for management accounting and reporting, such as cost reports, budgets, and performance reports. It also compares marginal and absorption costing techniques, illustrating their application through income statement preparation. Furthermore, the report evaluates the merits and demerits of budgetary control tools and examines how companies employ management accounting systems to address financial challenges, providing insights into effective financial management practices and the importance of adapting to evolving business trends.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SUMMARY

In the following report, a detailed deliberation regarding the management accounting

concepts and merits and demerits of tools that are in use for management accounting systems is

done. During the course of this project report, it has been analysed that with the growing

business trend and increasing competency of the firms in every industry, application of

management accounting principles is extremely important to furnish useful information helpful

in decision-making and strategic policy formulation regarding business operations.

In the following report, a detailed deliberation regarding the management accounting

concepts and merits and demerits of tools that are in use for management accounting systems is

done. During the course of this project report, it has been analysed that with the growing

business trend and increasing competency of the firms in every industry, application of

management accounting principles is extremely important to furnish useful information helpful

in decision-making and strategic policy formulation regarding business operations.

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Management accounting system and paramount requirements of multiple types of

management accounting systems...........................................................................................4

P2 Tools used for management accounting & reporting.......................................................5

TASK 2............................................................................................................................................6

P3 Calculation of total costs using different techniques of allocation of cost to prepare income

statement.................................................................................................................................6

TASK 3............................................................................................................................................8

P4 Merits and demerits of various types of planning tools used for budgetary control.........8

TASK 4..........................................................................................................................................10

P5 Comparison of how different companies are using management accounting systems to

counter financial problems...................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1 Management accounting system and paramount requirements of multiple types of

management accounting systems...........................................................................................4

P2 Tools used for management accounting & reporting.......................................................5

TASK 2............................................................................................................................................6

P3 Calculation of total costs using different techniques of allocation of cost to prepare income

statement.................................................................................................................................6

TASK 3............................................................................................................................................8

P4 Merits and demerits of various types of planning tools used for budgetary control.........8

TASK 4..........................................................................................................................................10

P5 Comparison of how different companies are using management accounting systems to

counter financial problems...................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the concept of analysis and reporting income and

expenditures which an organisation earns and expends while operating in macro-environment.

The main objective of this report is to develop an understanding about the concepts of

management accounting (Kaplan and Atkinson, 2015). For this purpose, two companies are

consulted in this report which are Cooke Optics Ltd (Camera lens manufacturer) and Bulldog

Tools Ltd. (Gardening tools manufacturer). In this report, the concepts of management

accounting, necessary requirements of various types of management accounting systems,

different costing techniques, tools of budgetary control and adaption of management accounting

in countering financial problems are discussed.

TASK 1

P1 Management accounting system and paramount requirements of multiple types of

management accounting systems.

Management accounting is the process of application of professional skill and expertise in

using financial information in a way to assist the management in policy formulation and decision

making. Management accounting has the objective of using financial information and data for

taking a better and accurate decision related to the key operational areas of the organisation.

There exist many kinds of management accounting systems that are essential for any

organisation. Some of them are:

Cost accounting systems:

Cost accounting system is a tool which is used by the management to find the

approximate cost of its products for making decisions related to stock valuation, profit-analysis

and cost control (Obigbemi, 2013). Allocation of cost under cost accounting is either done on the

basis of activity-based costing or traditional methods of costing. Cost accounting helps the

management to determine the exact reason behind any unusual change in the profit which may

be due to a change in the cost of producing the goods.

Inventory management:

Inventory management is defined as the method of controlling the ordering, storage and

consumption of materials which are used by the organisation in the production of its goods.

Inventory management aims at providing the right stock, at the right time, at the right place

Management accounting is the concept of analysis and reporting income and

expenditures which an organisation earns and expends while operating in macro-environment.

The main objective of this report is to develop an understanding about the concepts of

management accounting (Kaplan and Atkinson, 2015). For this purpose, two companies are

consulted in this report which are Cooke Optics Ltd (Camera lens manufacturer) and Bulldog

Tools Ltd. (Gardening tools manufacturer). In this report, the concepts of management

accounting, necessary requirements of various types of management accounting systems,

different costing techniques, tools of budgetary control and adaption of management accounting

in countering financial problems are discussed.

TASK 1

P1 Management accounting system and paramount requirements of multiple types of

management accounting systems.

Management accounting is the process of application of professional skill and expertise in

using financial information in a way to assist the management in policy formulation and decision

making. Management accounting has the objective of using financial information and data for

taking a better and accurate decision related to the key operational areas of the organisation.

There exist many kinds of management accounting systems that are essential for any

organisation. Some of them are:

Cost accounting systems:

Cost accounting system is a tool which is used by the management to find the

approximate cost of its products for making decisions related to stock valuation, profit-analysis

and cost control (Obigbemi, 2013). Allocation of cost under cost accounting is either done on the

basis of activity-based costing or traditional methods of costing. Cost accounting helps the

management to determine the exact reason behind any unusual change in the profit which may

be due to a change in the cost of producing the goods.

Inventory management:

Inventory management is defined as the method of controlling the ordering, storage and

consumption of materials which are used by the organisation in the production of its goods.

Inventory management aims at providing the right stock, at the right time, at the right place

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

procured at the right cost (Parker, 2012). It aims to avoid overstock and understock situations.

Management of inventory helps the organisation in decreasing various costs associated to

inventory such as storage costs, cost of ordering and carrying cost.

Job costing system:

The process of allocation of manufacturing costs of an organisation to individual jobs of

production or batches of items is termed as job costing system. Generally, it is applied if the

manufactured goods are distinct from each other. Information derived out of job costing system

have multiple uses (Langevin and Mendoza, 2013). It may be used by the management for

estimating cost to quote prices for any particular order or the figures may be used to provide the

data related to costs to a customer for any contract under which costs are to be refunded.

Price optimisation systems:

Price optimisation models are mathematical tools used to determine the reaction of

customers at different price levels. It measures the effective demand in response to any change in

the prices by the organisation. Price optimisation is all about determining the perfect balance

between value and profit and since relative prices of goods and services keep changing, it is a

perpetual task for the management. It helps the management to determine the level of price at

which the organisation is able to fulfil its goals like maximising the revenue or profits.

P2 Tools used for management accounting & reporting.

Management accounting uses financial reports prepared by the accounts department as

well as other accounting reports that are furnished by the accountants for the internal use of

management for making decisions and policy formulation. Some of the reports are:

Cost reports:

Cost of the items that are manufactured is calculated under management accounting. All

the elements of cost like prices of raw material, direct wages, overheads related to production,

selling and administration costs, variable selling and fixed costs etcetera are taken into

consideration for the preparation of cost reports (Fullerton, Kennedy and Widener, 2014). It

assists the management to view the total cost incurred on production and selling of the product

and the selling price of the product. It helps in making decisions related to profit margins and

cost control.

Budgets:

Management of inventory helps the organisation in decreasing various costs associated to

inventory such as storage costs, cost of ordering and carrying cost.

Job costing system:

The process of allocation of manufacturing costs of an organisation to individual jobs of

production or batches of items is termed as job costing system. Generally, it is applied if the

manufactured goods are distinct from each other. Information derived out of job costing system

have multiple uses (Langevin and Mendoza, 2013). It may be used by the management for

estimating cost to quote prices for any particular order or the figures may be used to provide the

data related to costs to a customer for any contract under which costs are to be refunded.

Price optimisation systems:

Price optimisation models are mathematical tools used to determine the reaction of

customers at different price levels. It measures the effective demand in response to any change in

the prices by the organisation. Price optimisation is all about determining the perfect balance

between value and profit and since relative prices of goods and services keep changing, it is a

perpetual task for the management. It helps the management to determine the level of price at

which the organisation is able to fulfil its goals like maximising the revenue or profits.

P2 Tools used for management accounting & reporting.

Management accounting uses financial reports prepared by the accounts department as

well as other accounting reports that are furnished by the accountants for the internal use of

management for making decisions and policy formulation. Some of the reports are:

Cost reports:

Cost of the items that are manufactured is calculated under management accounting. All

the elements of cost like prices of raw material, direct wages, overheads related to production,

selling and administration costs, variable selling and fixed costs etcetera are taken into

consideration for the preparation of cost reports (Fullerton, Kennedy and Widener, 2014). It

assists the management to view the total cost incurred on production and selling of the product

and the selling price of the product. It helps in making decisions related to profit margins and

cost control.

Budgets:

Budget reports prepared under management accounting are very useful in measuring the

performance of the organisation. These budget reports act as standards or benchmarks against

which the actual performance of the company is evaluated and any discrepancies found therein

are analysed. Budget reports have the element of flexibility to change them in future as per the

changes in business environment of the organisation. Generally, each department prepares its

own budget and a master budget is prepared for the whole organisation keeping in mind the goals

and targets of the organisation (Datar and Rajan, 2018). These are prepared on the basis of

budgeted and actual reports of previous years and some changes are made accordingly. Budget

reports assist the management to evaluate the work of the employees and providing incentives.

Accounts receivable aging reports:

It is a critical tool for determining flow of cash in the business if the organisation is

involved extensively in granting credit purchases to its customers. Classification of customer

balances on the basis of the time period for which they have been due is made under this report.

It aids the management of the firm to evaluate the collection process of the organisation.

Performance reports:

Performance reports are prepared for each employee and every department and sub-

department that exist in the organisation for evaluation of actual performances against budgeted

standards. These reports are used by the management to make key strategic with respect to

operations of the organisation. Performance reports are also used as tool for self-evaluation.

TASK 2

P3 Calculation of total costs using different techniques of allocation of cost to prepare income

statement.

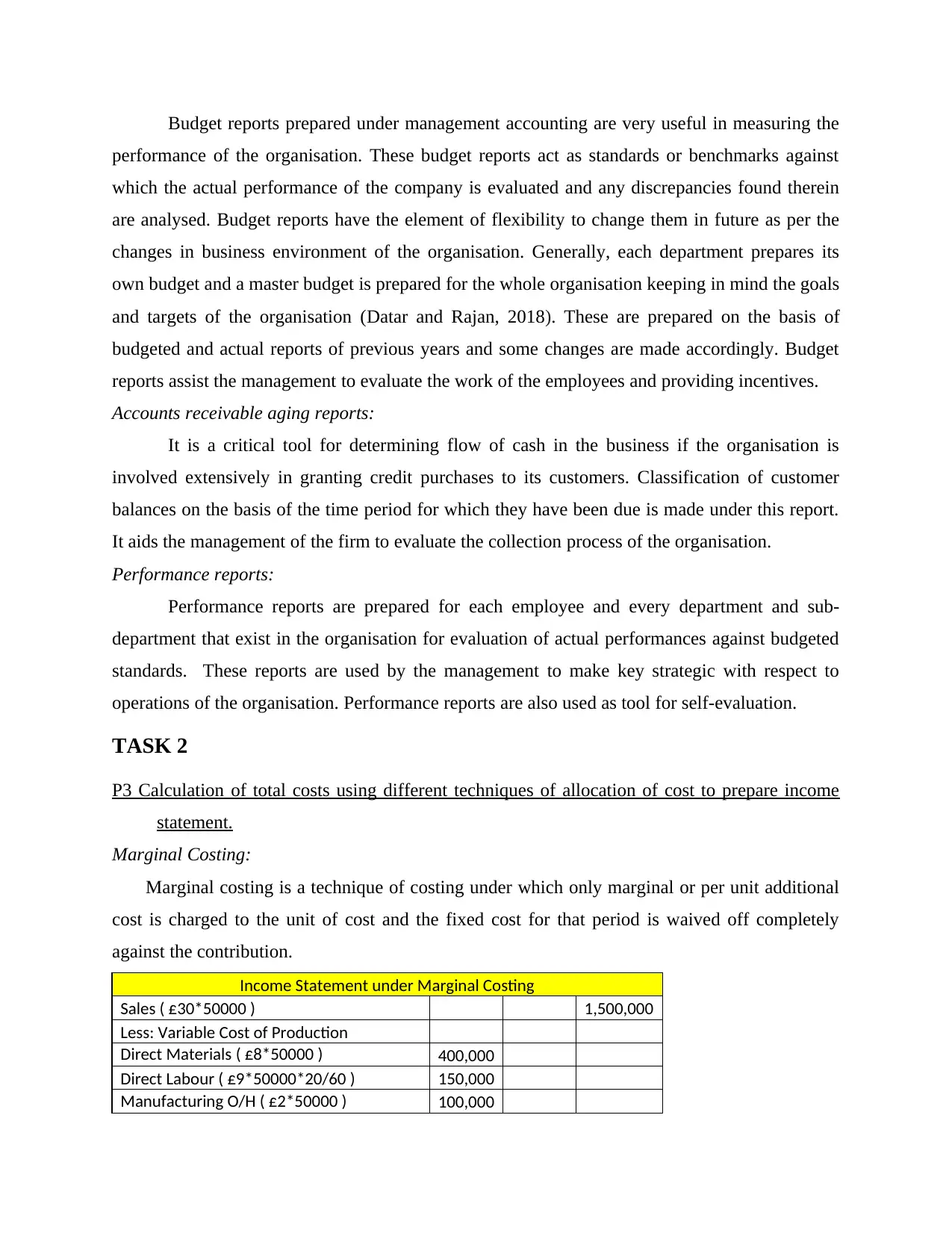

Marginal Costing:

Marginal costing is a technique of costing under which only marginal or per unit additional

cost is charged to the unit of cost and the fixed cost for that period is waived off completely

against the contribution.

Income Statement under Marginal Costing

Sales ( £30*50000 ) 1,500,000

Less: Variable Cost of Production

Direct Materials ( £8*50000 ) 400,000

Direct Labour ( £9*50000*20/60 ) 150,000

Manufacturing O/H ( £2*50000 ) 100,000

performance of the organisation. These budget reports act as standards or benchmarks against

which the actual performance of the company is evaluated and any discrepancies found therein

are analysed. Budget reports have the element of flexibility to change them in future as per the

changes in business environment of the organisation. Generally, each department prepares its

own budget and a master budget is prepared for the whole organisation keeping in mind the goals

and targets of the organisation (Datar and Rajan, 2018). These are prepared on the basis of

budgeted and actual reports of previous years and some changes are made accordingly. Budget

reports assist the management to evaluate the work of the employees and providing incentives.

Accounts receivable aging reports:

It is a critical tool for determining flow of cash in the business if the organisation is

involved extensively in granting credit purchases to its customers. Classification of customer

balances on the basis of the time period for which they have been due is made under this report.

It aids the management of the firm to evaluate the collection process of the organisation.

Performance reports:

Performance reports are prepared for each employee and every department and sub-

department that exist in the organisation for evaluation of actual performances against budgeted

standards. These reports are used by the management to make key strategic with respect to

operations of the organisation. Performance reports are also used as tool for self-evaluation.

TASK 2

P3 Calculation of total costs using different techniques of allocation of cost to prepare income

statement.

Marginal Costing:

Marginal costing is a technique of costing under which only marginal or per unit additional

cost is charged to the unit of cost and the fixed cost for that period is waived off completely

against the contribution.

Income Statement under Marginal Costing

Sales ( £30*50000 ) 1,500,000

Less: Variable Cost of Production

Direct Materials ( £8*50000 ) 400,000

Direct Labour ( £9*50000*20/60 ) 150,000

Manufacturing O/H ( £2*50000 ) 100,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

650,000

850,000

Less: Variable Selling Cost

Variable Sales O/H ( £4*50000 ) 200000 200000

Contribution : 650,000

Less: Fixed Production Costs 160,000

Less: Fixed Selling Costs 60000

Net Profit: 430,000

Total cost = Sales - Profit

= 1500000-430000 1070000

Cost per unit = 1070000/50000 21.4

Working Note:

Direct Manufacturing labour p/u: 20 mins

Units produced: 50000

Total labour mins: 50000*20 1000000

Total labour hours: 100000/60 1666.666667

Absorption costing:

Absorption costing is a technique of costing under which both marginal or per unit

additional cost and fixed costs of manufacturing a product is charged to the units of cost.

Income Statement under Absorption Costing

Sales ( £30*50000 ) 1,500,000

Less: Cost of Production

Variable Production Cost:

Direct Materials ( £8*50000 ) 400000

Direct Labour ( £9*50000*20/60 ) 150000

Manufacturing O/H ( £2*50000 ) 100,000

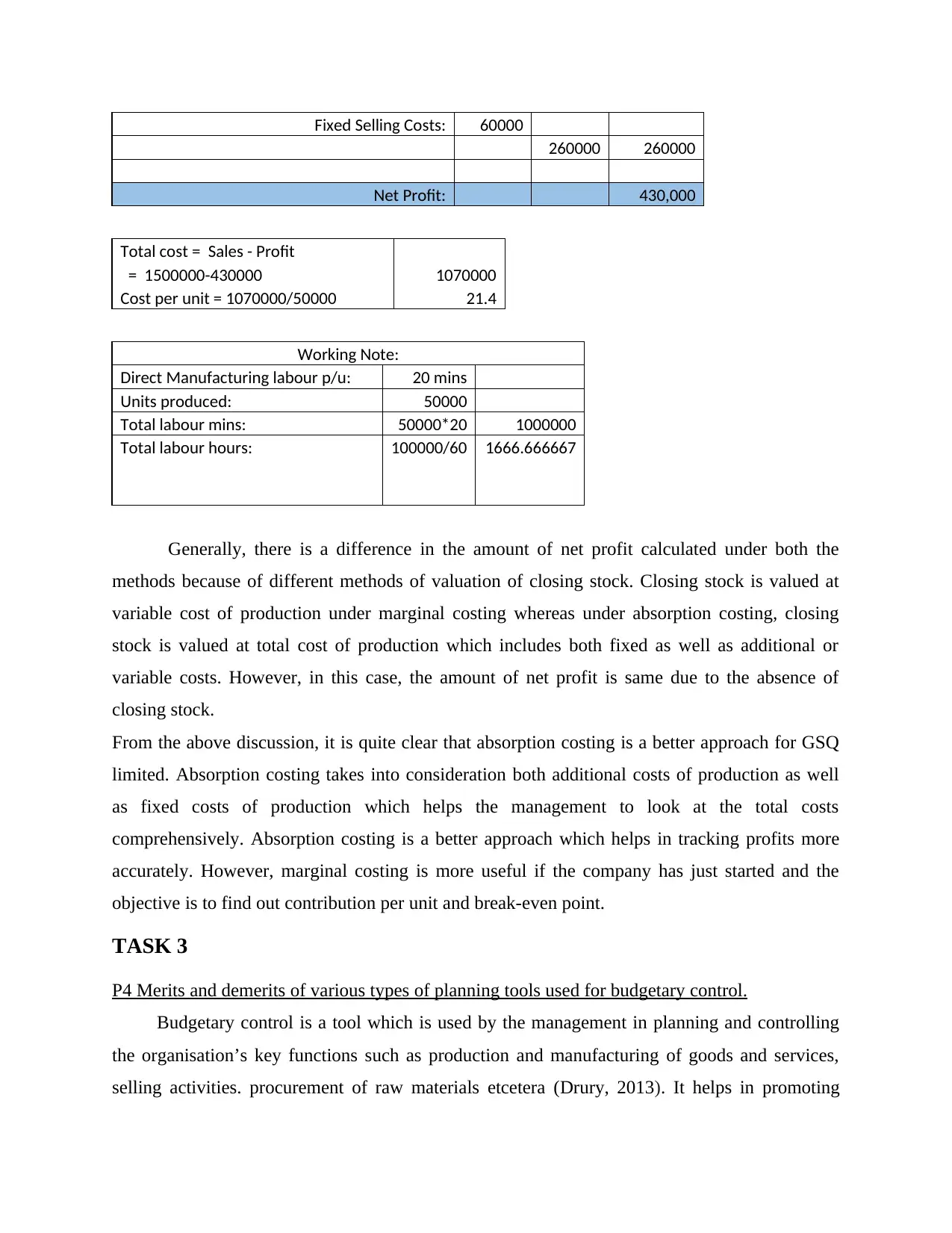

650,000

Fixed Production Costs: 160,000

810,000

Gross Profit: 690,000

Less: Selling and Administration Costs

Variable Sales O/H ( £4*50000 ) 200000

850,000

Less: Variable Selling Cost

Variable Sales O/H ( £4*50000 ) 200000 200000

Contribution : 650,000

Less: Fixed Production Costs 160,000

Less: Fixed Selling Costs 60000

Net Profit: 430,000

Total cost = Sales - Profit

= 1500000-430000 1070000

Cost per unit = 1070000/50000 21.4

Working Note:

Direct Manufacturing labour p/u: 20 mins

Units produced: 50000

Total labour mins: 50000*20 1000000

Total labour hours: 100000/60 1666.666667

Absorption costing:

Absorption costing is a technique of costing under which both marginal or per unit

additional cost and fixed costs of manufacturing a product is charged to the units of cost.

Income Statement under Absorption Costing

Sales ( £30*50000 ) 1,500,000

Less: Cost of Production

Variable Production Cost:

Direct Materials ( £8*50000 ) 400000

Direct Labour ( £9*50000*20/60 ) 150000

Manufacturing O/H ( £2*50000 ) 100,000

650,000

Fixed Production Costs: 160,000

810,000

Gross Profit: 690,000

Less: Selling and Administration Costs

Variable Sales O/H ( £4*50000 ) 200000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Selling Costs: 60000

260000 260000

Net Profit: 430,000

Total cost = Sales - Profit

= 1500000-430000 1070000

Cost per unit = 1070000/50000 21.4

Working Note:

Direct Manufacturing labour p/u: 20 mins

Units produced: 50000

Total labour mins: 50000*20 1000000

Total labour hours: 100000/60 1666.666667

Generally, there is a difference in the amount of net profit calculated under both the

methods because of different methods of valuation of closing stock. Closing stock is valued at

variable cost of production under marginal costing whereas under absorption costing, closing

stock is valued at total cost of production which includes both fixed as well as additional or

variable costs. However, in this case, the amount of net profit is same due to the absence of

closing stock.

From the above discussion, it is quite clear that absorption costing is a better approach for GSQ

limited. Absorption costing takes into consideration both additional costs of production as well

as fixed costs of production which helps the management to look at the total costs

comprehensively. Absorption costing is a better approach which helps in tracking profits more

accurately. However, marginal costing is more useful if the company has just started and the

objective is to find out contribution per unit and break-even point.

TASK 3

P4 Merits and demerits of various types of planning tools used for budgetary control.

Budgetary control is a tool which is used by the management in planning and controlling

the organisation’s key functions such as production and manufacturing of goods and services,

selling activities. procurement of raw materials etcetera (Drury, 2013). It helps in promoting

260000 260000

Net Profit: 430,000

Total cost = Sales - Profit

= 1500000-430000 1070000

Cost per unit = 1070000/50000 21.4

Working Note:

Direct Manufacturing labour p/u: 20 mins

Units produced: 50000

Total labour mins: 50000*20 1000000

Total labour hours: 100000/60 1666.666667

Generally, there is a difference in the amount of net profit calculated under both the

methods because of different methods of valuation of closing stock. Closing stock is valued at

variable cost of production under marginal costing whereas under absorption costing, closing

stock is valued at total cost of production which includes both fixed as well as additional or

variable costs. However, in this case, the amount of net profit is same due to the absence of

closing stock.

From the above discussion, it is quite clear that absorption costing is a better approach for GSQ

limited. Absorption costing takes into consideration both additional costs of production as well

as fixed costs of production which helps the management to look at the total costs

comprehensively. Absorption costing is a better approach which helps in tracking profits more

accurately. However, marginal costing is more useful if the company has just started and the

objective is to find out contribution per unit and break-even point.

TASK 3

P4 Merits and demerits of various types of planning tools used for budgetary control.

Budgetary control is a tool which is used by the management in planning and controlling

the organisation’s key functions such as production and manufacturing of goods and services,

selling activities. procurement of raw materials etcetera (Drury, 2013). It helps in promoting

coordination and communication between departments, evaluation of performances, motivating

employees with the main objective of achieving the goals and targets of the organisation. Some

of the tools used for budgetary control are:

Financial budgets:

Financial budgets such as cash budget, budgets for asset-acquisition and statement of

financial position budgets are used by the management to forecast and determine the sources

from where it expects to meet its requirement of funds.

Advantages:

It provides vital help to the management in decision-making related to capital expenditure

projects and ascertaining that the firm is able to meet its working capital requirements.

Preparation of financial budgets ensure optimal allocation of scarce financial resources.

Disadvantages:

Financial budgets create an upper limit on every transaction that happens within an

organisation. These budgets are often perceived as tools of restriction used by the management to

control expenditure and resource allocation (Yalcin, 2012). Element of flexibility must be

included while preparation of these budgets.

Operating budgets:

Operating budgets are budgets that are prepared for carrying out the operations of

business such as manufacturing goods, selling activities and procurement of materials. It

showcases an organisation's expected revenue and expenditure for a certain period of time.

Advantages:

Operating budget act as a tool for the management to measure the performance of various

departments. It makes possible the comparison between the standard performance and the actual

performance.

Disadvantages:

Operating budgets are based on the forecasts made by the management after taking into

consideration the budgets for previous year. Thus, it is very difficult to trust the accuracy of these

budgets. Operating budget formulation increases the chances of inter-departmental conflicts

since the budget of each department is inter-connected.

employees with the main objective of achieving the goals and targets of the organisation. Some

of the tools used for budgetary control are:

Financial budgets:

Financial budgets such as cash budget, budgets for asset-acquisition and statement of

financial position budgets are used by the management to forecast and determine the sources

from where it expects to meet its requirement of funds.

Advantages:

It provides vital help to the management in decision-making related to capital expenditure

projects and ascertaining that the firm is able to meet its working capital requirements.

Preparation of financial budgets ensure optimal allocation of scarce financial resources.

Disadvantages:

Financial budgets create an upper limit on every transaction that happens within an

organisation. These budgets are often perceived as tools of restriction used by the management to

control expenditure and resource allocation (Yalcin, 2012). Element of flexibility must be

included while preparation of these budgets.

Operating budgets:

Operating budgets are budgets that are prepared for carrying out the operations of

business such as manufacturing goods, selling activities and procurement of materials. It

showcases an organisation's expected revenue and expenditure for a certain period of time.

Advantages:

Operating budget act as a tool for the management to measure the performance of various

departments. It makes possible the comparison between the standard performance and the actual

performance.

Disadvantages:

Operating budgets are based on the forecasts made by the management after taking into

consideration the budgets for previous year. Thus, it is very difficult to trust the accuracy of these

budgets. Operating budget formulation increases the chances of inter-departmental conflicts

since the budget of each department is inter-connected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 4

P5 Comparison of how different companies are using management accounting systems to

counter financial problems.

Each organisation faces a lot of difficulties related to finance such as lack of funds,

increasing cost of production etcetera. The management of the company needs to find solutions

to these problems as soon as possible to sustain in the market and protect the organisation form

any negative impact of these problems. The role of management accounting is increasing in

responding to these financial problems (Marginson, 2013). Some of the tools of management

accounting that are being used to solve financial problems are:

Cost accounting and cost sheets:

Cost accounting provides vital information to the management with respect to the various

costs that are being incurred in the production, manufacturing and selling activities of the

business. This information facilitates decision-making and policy formulation by the

management.

Variance analysis:

Variance analysis refers to the process of investigating the deviations between the actual

performance and the budgeted or standard performance (Banerjee, 2012). It helps the

management to find out whether the activities of the organisation are directed towards achieving

the targets or goals that were set during the initial planning process.

Here is a comparison that shows how organisations implement the same management accounting

tool to counter to different financial problems:

Tool Cooke Optics Ltd. Bulldog Tools Ltd.

Cost accounting The company was recently

facing a financial problem of

reduced profit margins due to

increase in cost of production.

Company made use of cost

sheets to find the reason

behind the increasing cost.

After a brief analysis of the

Due to an intense competition,

the sales of the company were

on a declining rally. This lead

to a decrease in the profits and

scarcity of funds. Management

of the Bulldog Tools Ltd.

analysed the cost sheets to

calculate the current profit

P5 Comparison of how different companies are using management accounting systems to

counter financial problems.

Each organisation faces a lot of difficulties related to finance such as lack of funds,

increasing cost of production etcetera. The management of the company needs to find solutions

to these problems as soon as possible to sustain in the market and protect the organisation form

any negative impact of these problems. The role of management accounting is increasing in

responding to these financial problems (Marginson, 2013). Some of the tools of management

accounting that are being used to solve financial problems are:

Cost accounting and cost sheets:

Cost accounting provides vital information to the management with respect to the various

costs that are being incurred in the production, manufacturing and selling activities of the

business. This information facilitates decision-making and policy formulation by the

management.

Variance analysis:

Variance analysis refers to the process of investigating the deviations between the actual

performance and the budgeted or standard performance (Banerjee, 2012). It helps the

management to find out whether the activities of the organisation are directed towards achieving

the targets or goals that were set during the initial planning process.

Here is a comparison that shows how organisations implement the same management accounting

tool to counter to different financial problems:

Tool Cooke Optics Ltd. Bulldog Tools Ltd.

Cost accounting The company was recently

facing a financial problem of

reduced profit margins due to

increase in cost of production.

Company made use of cost

sheets to find the reason

behind the increasing cost.

After a brief analysis of the

Due to an intense competition,

the sales of the company were

on a declining rally. This lead

to a decrease in the profits and

scarcity of funds. Management

of the Bulldog Tools Ltd.

analysed the cost sheets to

calculate the current profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost sheet for different

periods, the management of

Cooke Optics Ltd. was able to

figure out that the reason

behind increasing total cost

was increased cost of raw

materials by the supplier and

started looking for alternate

options.

margin and offer a price lesser

than the competitor's price to

increase the sales.

Variance analysis The company uses the model

of variance analysis to make

sure that the products which

are being manufactured match

the standards of quality.

Quality of products has

proved to be the main reason

behind the increasing sales of

the company.

Bulldog Tools Ltd. implements

the model of variance analysis

for setting profit-targets. Any

differences between the actual

and the standard profit are

thoroughly analysed by the

management.

CONCLUSION

After going through the report, it has been inferred that management accounting is a very

important process of providing information related with the operations of the company to the

management for more informed decisions and policy formulation. Management accounting and

financial accounting are very different from each other. It can be concluded that while financial

accounting methods are used to ascertain the financial position of the organisation, management

accounting aims at providing aid to the management in managing and controlling the operations

of the organisation.

periods, the management of

Cooke Optics Ltd. was able to

figure out that the reason

behind increasing total cost

was increased cost of raw

materials by the supplier and

started looking for alternate

options.

margin and offer a price lesser

than the competitor's price to

increase the sales.

Variance analysis The company uses the model

of variance analysis to make

sure that the products which

are being manufactured match

the standards of quality.

Quality of products has

proved to be the main reason

behind the increasing sales of

the company.

Bulldog Tools Ltd. implements

the model of variance analysis

for setting profit-targets. Any

differences between the actual

and the standard profit are

thoroughly analysed by the

management.

CONCLUSION

After going through the report, it has been inferred that management accounting is a very

important process of providing information related with the operations of the company to the

management for more informed decisions and policy formulation. Management accounting and

financial accounting are very different from each other. It can be concluded that while financial

accounting methods are used to ascertain the financial position of the organisation, management

accounting aims at providing aid to the management in managing and controlling the operations

of the organisation.

REFERENCES

Books & Journals

Banerjee, B., 2012. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Datar, S.M. and Rajan, M., 2018. Horngren's Cost Accounting: A Managerial Emphasis.

Drury, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Langevin, P. and Mendoza, C., 2013. How can management control system fairness reduce

managers’ unethical behaviours?. European Management Journal. 31(3). pp.209-222.

Marginson, D., 2013. Budgetary control: what’s been happening?. In The Routledge Companion

to Cost Management (pp. 21-43). Routledge.

Obigbemi, I.F., 2013. Employee Participation in Budgeting and Effective Budgetary Control a

Tool for Enhancing Organizational Performance. Tactful Management Research

Journal, 1.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe. 9(1). pp.95-110.

Books & Journals

Banerjee, B., 2012. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Datar, S.M. and Rajan, M., 2018. Horngren's Cost Accounting: A Managerial Emphasis.

Drury, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Langevin, P. and Mendoza, C., 2013. How can management control system fairness reduce

managers’ unethical behaviours?. European Management Journal. 31(3). pp.209-222.

Marginson, D., 2013. Budgetary control: what’s been happening?. In The Routledge Companion

to Cost Management (pp. 21-43). Routledge.

Obigbemi, I.F., 2013. Employee Participation in Budgeting and Effective Budgetary Control a

Tool for Enhancing Organizational Performance. Tactful Management Research

Journal, 1.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Yalcin, S., 2012. Adoption and benefits of management accounting practices: an inter-country

comparison. Accounting in Europe. 9(1). pp.95-110.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.