Management Accounting: Systems, Methods, and Reporting in Business

VerifiedAdded on 2023/02/02

|8

|848

|81

Report

AI Summary

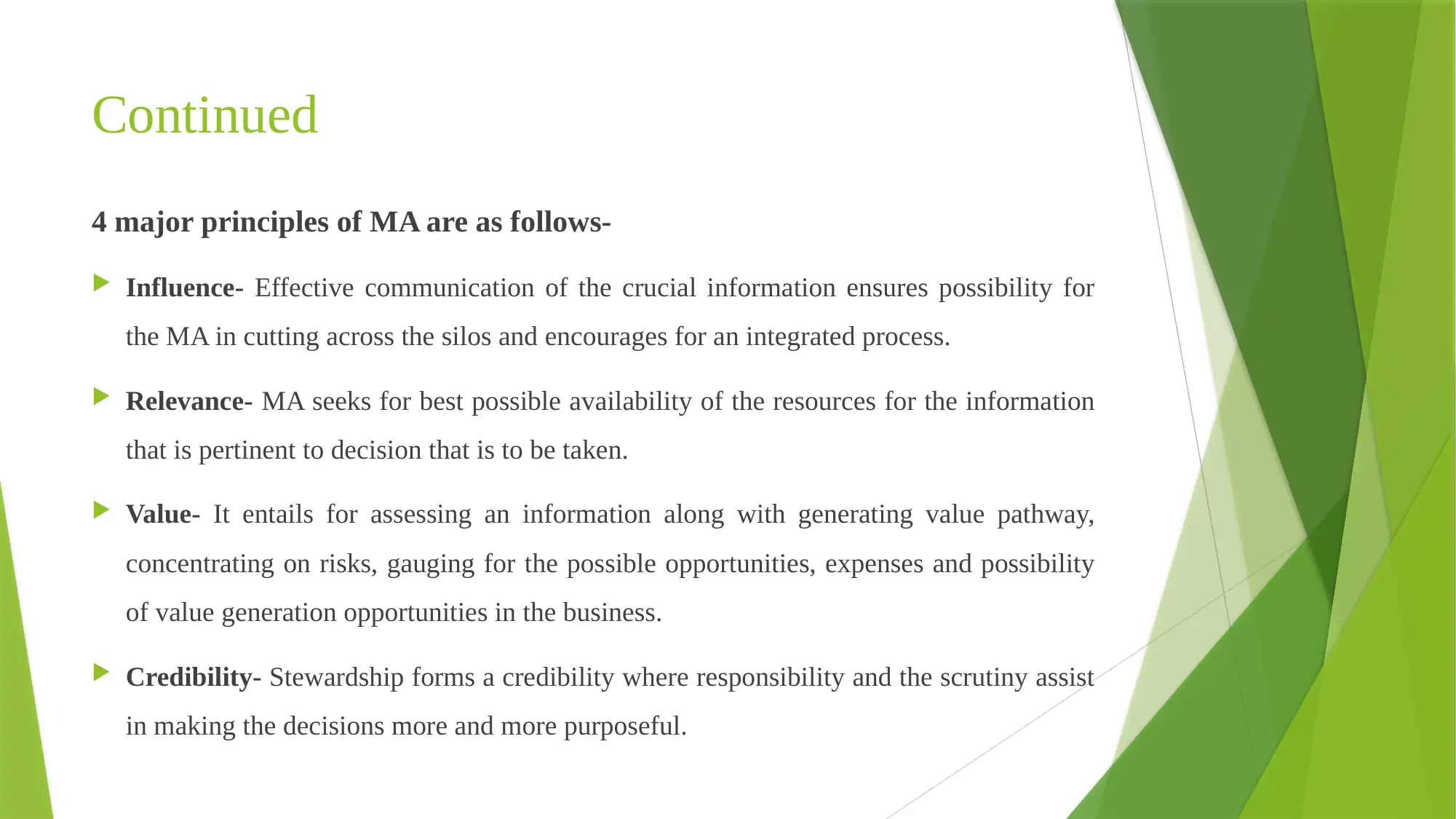

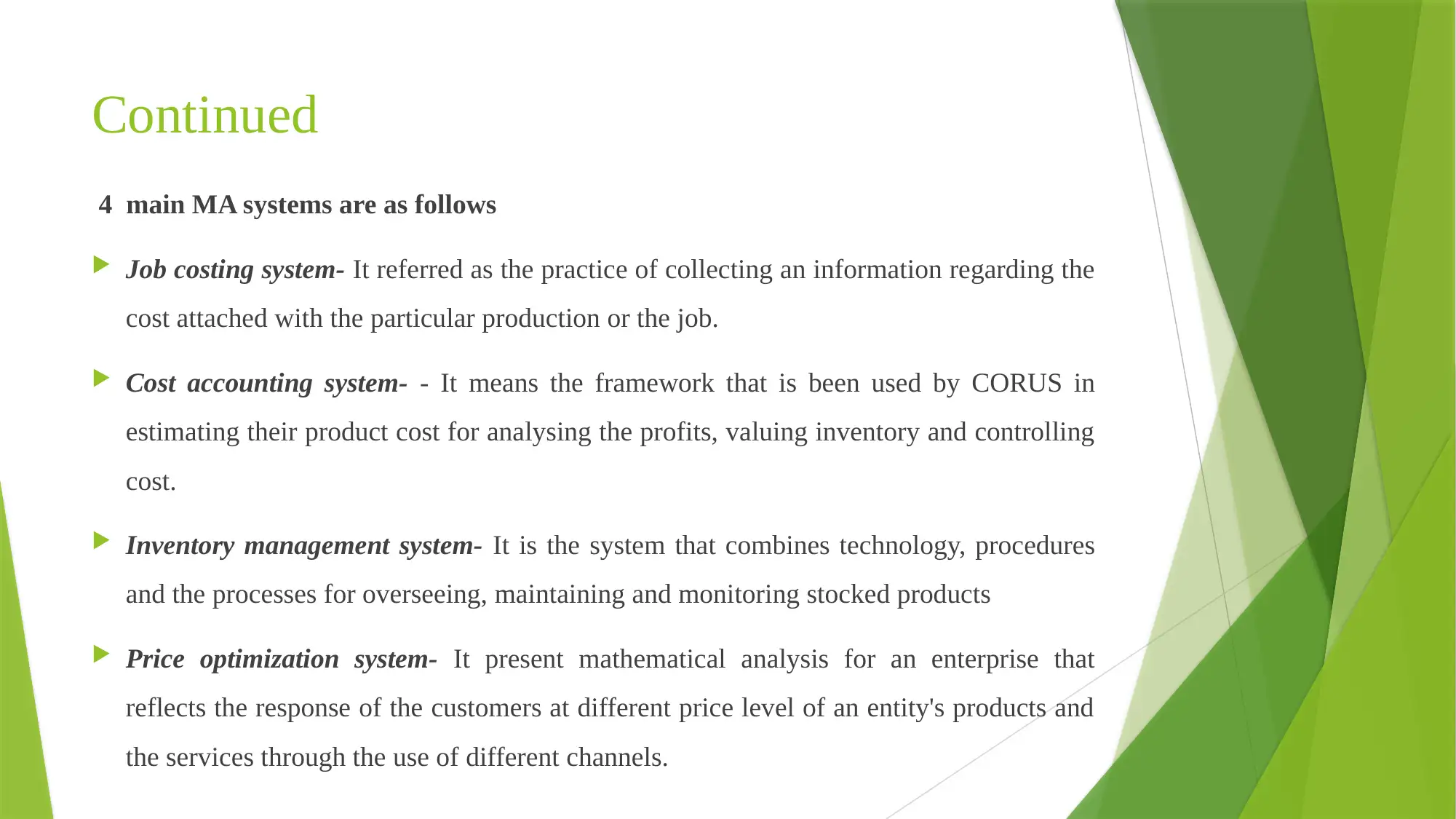

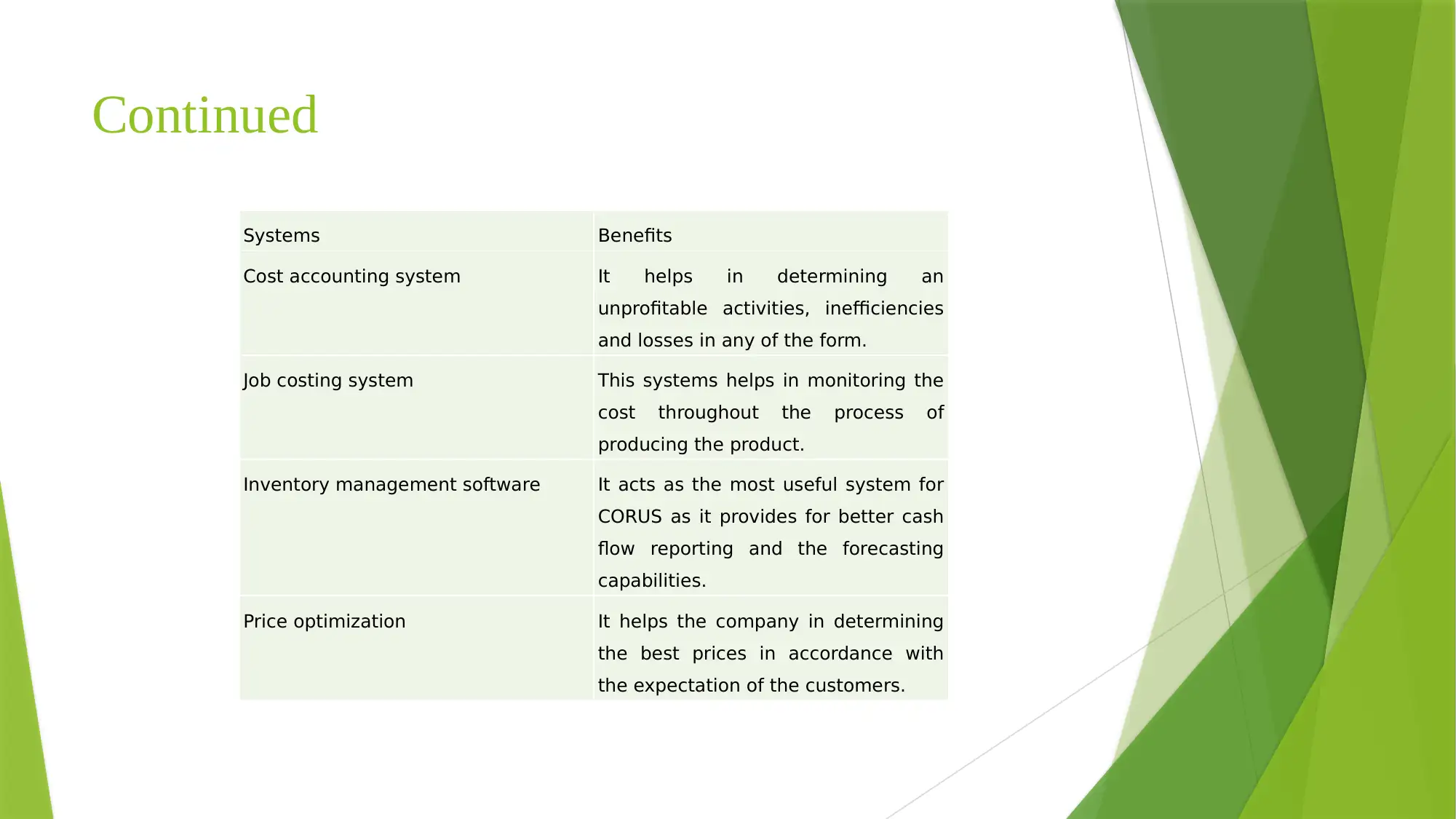

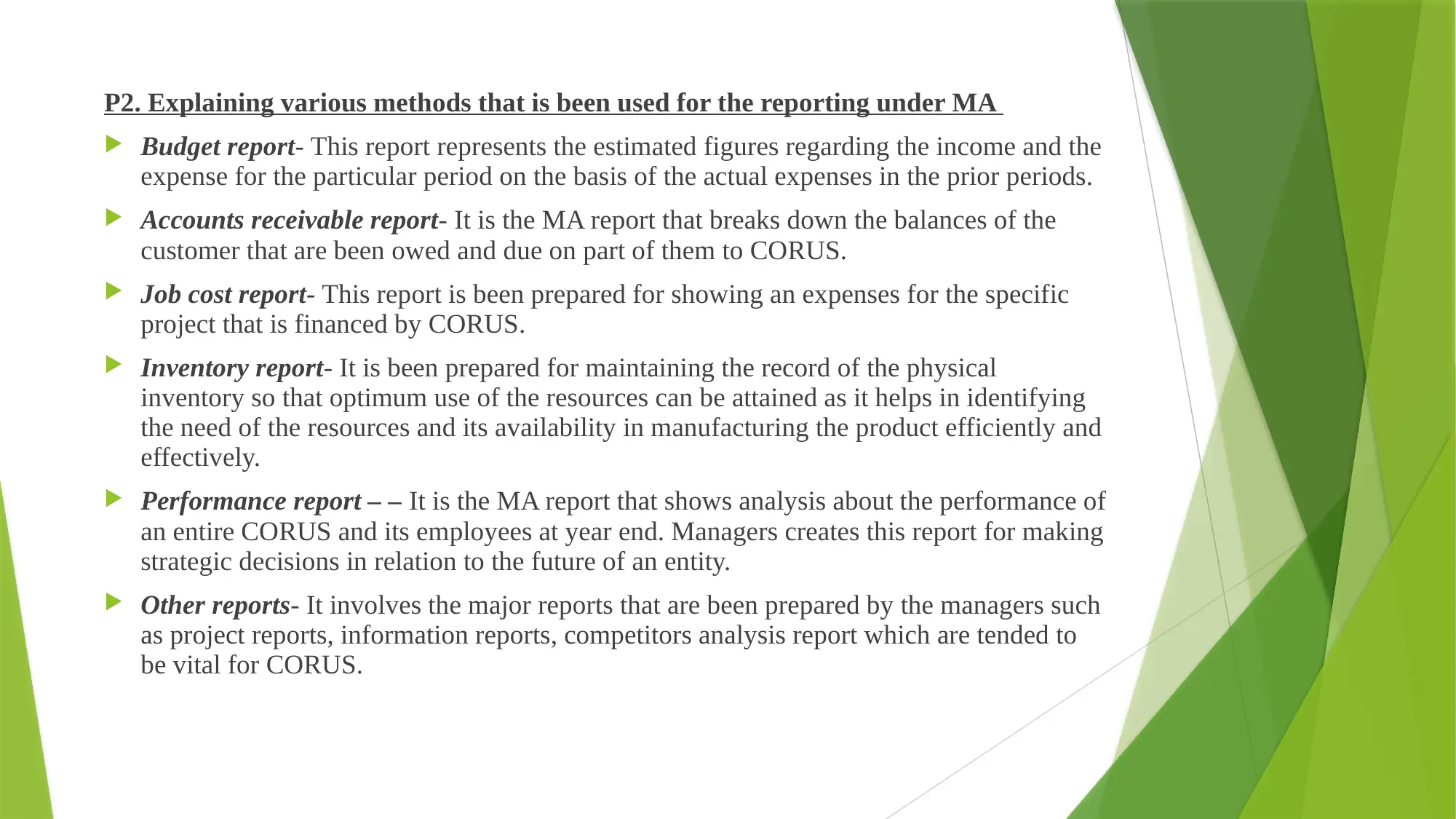

This report delves into the core concepts of management accounting, elucidating its significance in decision-making, planning, and performance management. It outlines four key principles: influence, relevance, value, and credibility, which underpin effective management accounting practices. The report then explores four main management accounting systems: job costing, cost accounting, inventory management, and price optimization, highlighting their benefits for businesses like CORUS. Furthermore, it details various reporting methods used in management accounting, including budget reports, accounts receivable reports, job cost reports, inventory reports, and performance reports, providing insights into their applications and importance for strategic decision-making. The report concludes with a list of references, including books and journals, to support the information presented.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.