Management Accounting Concepts and Techniques Report

VerifiedAdded on 2023/01/09

|18

|4445

|53

Report

AI Summary

This report delves into the realm of management accounting, exploring its core concepts, techniques, and applications for effective decision-making. It begins by defining management accounting (MA) and emphasizing its significance in providing financial information to managers. The report then explains various MA reporting methods, including job costing, performance reports, inventory reports, and debtors aging reports. It evaluates the merits of different MA systems like inventory, costing, job cost, and price optimization systems. The report further examines the application of MA techniques, such as marginal costing, absorption costing, and cost-volume-profit analysis, providing illustrative income statements and break-even analysis. It also explores different types of planning tools used to construct budgets and highlights how management accounting aids in resolving financial issues within an organization. Finally, the report provides a comparative analysis of MA techniques, including marginal and absorption costing, and concludes by summarizing key findings.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Declaration

I certify that the work submitted for this unit is my own and the research sources are fully

acknowledged.

Learners Name: Date:

I certify that the work submitted for this unit is my own and the research sources are fully

acknowledged.

Learners Name: Date:

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

Part 1..........................................................................................................................................3

LO1............................................................................................................................................3

P1. Describing the meaning of MA and importance of its systems.......................................3

P2. Explaining different methods used for reporting under MA...........................................4

M1. Evaluating merits of different MA systems....................................................................5

Part 2..........................................................................................................................................6

Application of different types of MA techniques..................................................................6

Part 3........................................................................................................................................10

Different type of planning tool to construct budget in organization....................................10

Management accounting for resolving the financial issues.................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................3

Part 1..........................................................................................................................................3

LO1............................................................................................................................................3

P1. Describing the meaning of MA and importance of its systems.......................................3

P2. Explaining different methods used for reporting under MA...........................................4

M1. Evaluating merits of different MA systems....................................................................5

Part 2..........................................................................................................................................6

Application of different types of MA techniques..................................................................6

Part 3........................................................................................................................................10

Different type of planning tool to construct budget in organization....................................10

Management accounting for resolving the financial issues.................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting (MA) is the procedure which is utilized with the aim of meeting

with the changing requirements of the business. This report provides an insight about eth

different types of MA techniques and reporting system along with the costing techniques for

cost analysis. It also includes various types of budgetary control tools which can be

implemented for exercising control over cost and at last a comparative analysis among two

companies is carried out in regard to MA techniques used by it for resolving tehri problems.

Part 1

LO1.

P1. Describing the meaning of MA and importance of its systems

MA refers to practice of assessing & communicating the financial information to the

managers who makes use of such information in making suitable business decisions. The

main purpose or objective of MA is to help the management of an entity in performing their

business operations in efficient manner. It helps in getting out maximum results through

minimum efforts by making optimum use of available resources within the work

environment. Moreover, it enables in providing improved & better services to the customers

that is been assured by such accounting systems. It helps in maintaining the higher degree of

the morale among employees which in turn helps in improving the productivity and financial

state of Tesco.

MA differs from financial accounting ion several different bases that are as follows-

Basis MA FA

Meaning It means as providing relevant

information to managers in

making strategies, plans and

policies for running the

enterprise in an effective way.

It refers to system that

emphasize on framing final

report of an entity in facilitating

financial information to

interested users.

Information It includes both types of

information that is monetary &

non-monetary.

However, it involves only the

monetary information which is

expressed in numbers.

Users It is been mainly used by

internal management.

It is used by internal as well as

external parties.

Management accounting (MA) is the procedure which is utilized with the aim of meeting

with the changing requirements of the business. This report provides an insight about eth

different types of MA techniques and reporting system along with the costing techniques for

cost analysis. It also includes various types of budgetary control tools which can be

implemented for exercising control over cost and at last a comparative analysis among two

companies is carried out in regard to MA techniques used by it for resolving tehri problems.

Part 1

LO1.

P1. Describing the meaning of MA and importance of its systems

MA refers to practice of assessing & communicating the financial information to the

managers who makes use of such information in making suitable business decisions. The

main purpose or objective of MA is to help the management of an entity in performing their

business operations in efficient manner. It helps in getting out maximum results through

minimum efforts by making optimum use of available resources within the work

environment. Moreover, it enables in providing improved & better services to the customers

that is been assured by such accounting systems. It helps in maintaining the higher degree of

the morale among employees which in turn helps in improving the productivity and financial

state of Tesco.

MA differs from financial accounting ion several different bases that are as follows-

Basis MA FA

Meaning It means as providing relevant

information to managers in

making strategies, plans and

policies for running the

enterprise in an effective way.

It refers to system that

emphasize on framing final

report of an entity in facilitating

financial information to

interested users.

Information It includes both types of

information that is monetary &

non-monetary.

However, it involves only the

monetary information which is

expressed in numbers.

Users It is been mainly used by

internal management.

It is used by internal as well as

external parties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Essentials of MA systems

Cost accounting system- It referred as the framework that is been used by an

enterprise for estimating cost of its product for the profitability assessment, controlling cost

and valuing inventory (Zarzycka and et.al., 2017). This system is considered as critical as it

allows the management in checking raw material at every production stage and helps the

managers in controlling cost within the operations.

Price optimization system- It means as the mathematical program that compute the

way in which demand varies at various price levels, then combining data with an information

on the inventory levels and the costs for recommending the prices that would improve profits.

This system plays a vital role in an entity in terms of setting most suitable price that would be

providing large amount of profits and is affordable to customers.

Inventory management system- This MA system is indicated as combination of the

technology and the procedures which oversees maintenance & monitoring of the products

that are stocked and the assets which is to be sent to ultimate consumers & vendors (Joshi and

Li, 2016). It plays an essential role in improving the management of warehouse through

providing efficiency and transparency to the complex system.

Job costing system- It includes procedure of accumulating information regarding the

costs attached with particular production or the job service. Such type of information is

needed for the purpose of submitting cost related information to customer under the contract

where the costs are been reimbursed. This information is found as useful in identifying

accuracy in estimating system of firm that must be able in quoting suitable or optimal price

which allows for the reasonable amount of profit. It could also be utilized for assigning

inventory cost towards manufacturing the goods.

P2. Explaining different methods used for reporting under MA

There are several MA reports that helps in formulation of adequate management

reports that counts on forecasts in order to make critical or crucial decision making. They

facilitate with reliable & accurate financial relation data. The different types of the reports are

as follows-

Job costing report- This report is concerned with determining cost, disbursements and

the profitability of every specific job. With the help of this report, an evaluation could be

Cost accounting system- It referred as the framework that is been used by an

enterprise for estimating cost of its product for the profitability assessment, controlling cost

and valuing inventory (Zarzycka and et.al., 2017). This system is considered as critical as it

allows the management in checking raw material at every production stage and helps the

managers in controlling cost within the operations.

Price optimization system- It means as the mathematical program that compute the

way in which demand varies at various price levels, then combining data with an information

on the inventory levels and the costs for recommending the prices that would improve profits.

This system plays a vital role in an entity in terms of setting most suitable price that would be

providing large amount of profits and is affordable to customers.

Inventory management system- This MA system is indicated as combination of the

technology and the procedures which oversees maintenance & monitoring of the products

that are stocked and the assets which is to be sent to ultimate consumers & vendors (Joshi and

Li, 2016). It plays an essential role in improving the management of warehouse through

providing efficiency and transparency to the complex system.

Job costing system- It includes procedure of accumulating information regarding the

costs attached with particular production or the job service. Such type of information is

needed for the purpose of submitting cost related information to customer under the contract

where the costs are been reimbursed. This information is found as useful in identifying

accuracy in estimating system of firm that must be able in quoting suitable or optimal price

which allows for the reasonable amount of profit. It could also be utilized for assigning

inventory cost towards manufacturing the goods.

P2. Explaining different methods used for reporting under MA

There are several MA reports that helps in formulation of adequate management

reports that counts on forecasts in order to make critical or crucial decision making. They

facilitate with reliable & accurate financial relation data. The different types of the reports are

as follows-

Job costing report- This report is concerned with determining cost, disbursements and

the profitability of every specific job. With the help of this report, an evaluation could be

made relating to earning aspect of projects so that the firm could introduce an effort on such

concerned at the time of reducing their efforts on the business activities that is less profitable

(Hasyim and Jabid, 2019). It enables in evaluation of cost during the period in which the

project is in the progress so that the wastage areas could be taken care and proposals could be

made as workable & profitable.

Performance report- It is prepared for comparing budgeted with that of actual

performance are assessed & information relating to this is been presented in the performance

reports. It is been framed on annual basis, however they could be prepared on quarterly and

monthly basis. This reports helps tin reviewing entire performance of both employees and

Tesco so that appropriate measures can be executed for filling the gap.

Inventory report- This MA report is prepared for maintaining the data relating to

inventory or stock item in the organization. It comprises of labor cost, wages, per unit cost of

overhead with the inventory that provides the managers for making comparison between the

different assembly lines & in seeing for improvement opportunities that could be exploited

through several departments and their respective staff.

Debtors aging report- It relates to managing the receivables for the firm that

facilitates credit to its customers. It helps in tracing remaining balances of the debtors that are

due for the Tesco to collect (Soderstrom, Soderstrom and Stewart, 2017). It points out any

kind of problem in association with collection process of an enterprise. An assessment could

be made regarding the credit policy and the requirement for tightening the policy which helps

in reducing debt and enhancing liquidity of an entity.

M1. Evaluating merits of different MA systems

systems Benefits

Inventory system This system helps in tracking the flow of

inventory in overall supply chain starting from

transit to delivering for end consumers.

Costing system It is the system helps in insurance affective

control on the cost of manufacturing the product.

It helps in computing closing value of an

inventory which in turn act as the basis for

preparing final statements of an enterprise.

concerned at the time of reducing their efforts on the business activities that is less profitable

(Hasyim and Jabid, 2019). It enables in evaluation of cost during the period in which the

project is in the progress so that the wastage areas could be taken care and proposals could be

made as workable & profitable.

Performance report- It is prepared for comparing budgeted with that of actual

performance are assessed & information relating to this is been presented in the performance

reports. It is been framed on annual basis, however they could be prepared on quarterly and

monthly basis. This reports helps tin reviewing entire performance of both employees and

Tesco so that appropriate measures can be executed for filling the gap.

Inventory report- This MA report is prepared for maintaining the data relating to

inventory or stock item in the organization. It comprises of labor cost, wages, per unit cost of

overhead with the inventory that provides the managers for making comparison between the

different assembly lines & in seeing for improvement opportunities that could be exploited

through several departments and their respective staff.

Debtors aging report- It relates to managing the receivables for the firm that

facilitates credit to its customers. It helps in tracing remaining balances of the debtors that are

due for the Tesco to collect (Soderstrom, Soderstrom and Stewart, 2017). It points out any

kind of problem in association with collection process of an enterprise. An assessment could

be made regarding the credit policy and the requirement for tightening the policy which helps

in reducing debt and enhancing liquidity of an entity.

M1. Evaluating merits of different MA systems

systems Benefits

Inventory system This system helps in tracking the flow of

inventory in overall supply chain starting from

transit to delivering for end consumers.

Costing system It is the system helps in insurance affective

control on the cost of manufacturing the product.

It helps in computing closing value of an

inventory which in turn act as the basis for

preparing final statements of an enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost system This system allows the Tesco in assigning the

cost on separate basis towards performance of an

individual and in calculating the return that will

be generated on every job.

It also enables the firm in accessing performance

of its employees with regard to productivity, cost

and efficiency.

Price optimization This tool provides an opportunity to emphasize

on several goals like sells margin & no of

conversations. It in turn could make the finance

related benefit for the business that adds to

expansion and growth.

It helps an entity in understanding buying

behavior of customer and their need for pricing.

This could further assist in taking quick decisions

relating to pricing of the product.

Part 2

Application of different types of MA techniques

The implication of various MA techniques helps in effectively carrying out the cost

analysis process which assist in adequately assessing the cost involved in the activity which

supports in exercising cost saving initiative. Few of the techniques are explained below.

Marginal costing

It is the powerful tool which provides assistance in decision making process. It establishes the

true relation among the cost, volume and profit which provides support in effectively planning the

profit and selling price along with determining the level of production (Taschner and Charifzadeh,

2016). It mainly puts focus on the variability in respect to the cost and ignores the overhead

expenditure.

Absorption costing

It is mainly the practice under which all the cost is charged to the production cost of the

product. It is most widely used technique for the purpose of ascertaining the cost (Kalkhouran,

cost on separate basis towards performance of an

individual and in calculating the return that will

be generated on every job.

It also enables the firm in accessing performance

of its employees with regard to productivity, cost

and efficiency.

Price optimization This tool provides an opportunity to emphasize

on several goals like sells margin & no of

conversations. It in turn could make the finance

related benefit for the business that adds to

expansion and growth.

It helps an entity in understanding buying

behavior of customer and their need for pricing.

This could further assist in taking quick decisions

relating to pricing of the product.

Part 2

Application of different types of MA techniques

The implication of various MA techniques helps in effectively carrying out the cost

analysis process which assist in adequately assessing the cost involved in the activity which

supports in exercising cost saving initiative. Few of the techniques are explained below.

Marginal costing

It is the powerful tool which provides assistance in decision making process. It establishes the

true relation among the cost, volume and profit which provides support in effectively planning the

profit and selling price along with determining the level of production (Taschner and Charifzadeh,

2016). It mainly puts focus on the variability in respect to the cost and ignores the overhead

expenditure.

Absorption costing

It is mainly the practice under which all the cost is charged to the production cost of the

product. It is most widely used technique for the purpose of ascertaining the cost (Kalkhouran,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

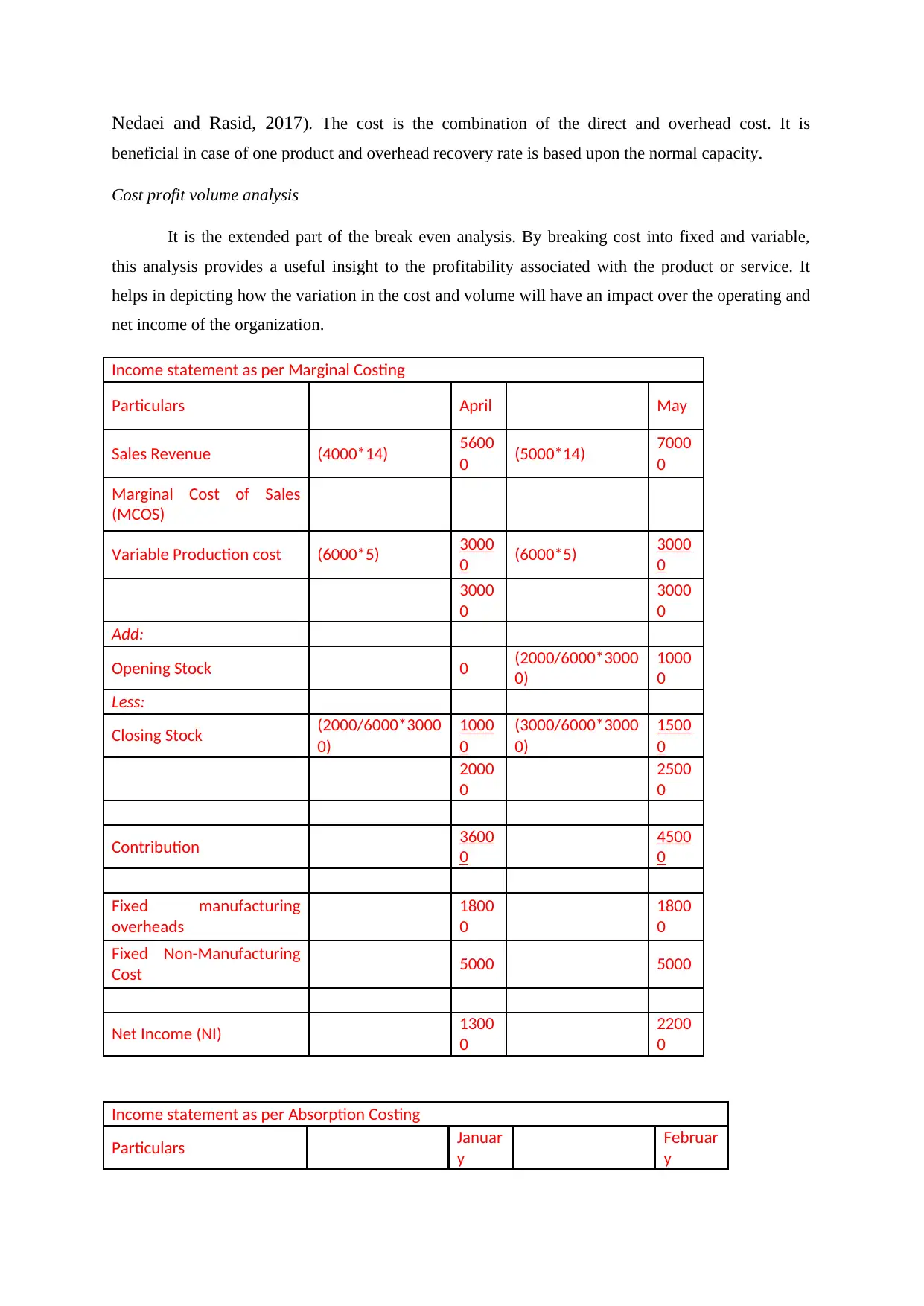

Nedaei and Rasid, 2017). The cost is the combination of the direct and overhead cost. It is

beneficial in case of one product and overhead recovery rate is based upon the normal capacity.

Cost profit volume analysis

It is the extended part of the break even analysis. By breaking cost into fixed and variable,

this analysis provides a useful insight to the profitability associated with the product or service. It

helps in depicting how the variation in the cost and volume will have an impact over the operating and

net income of the organization.

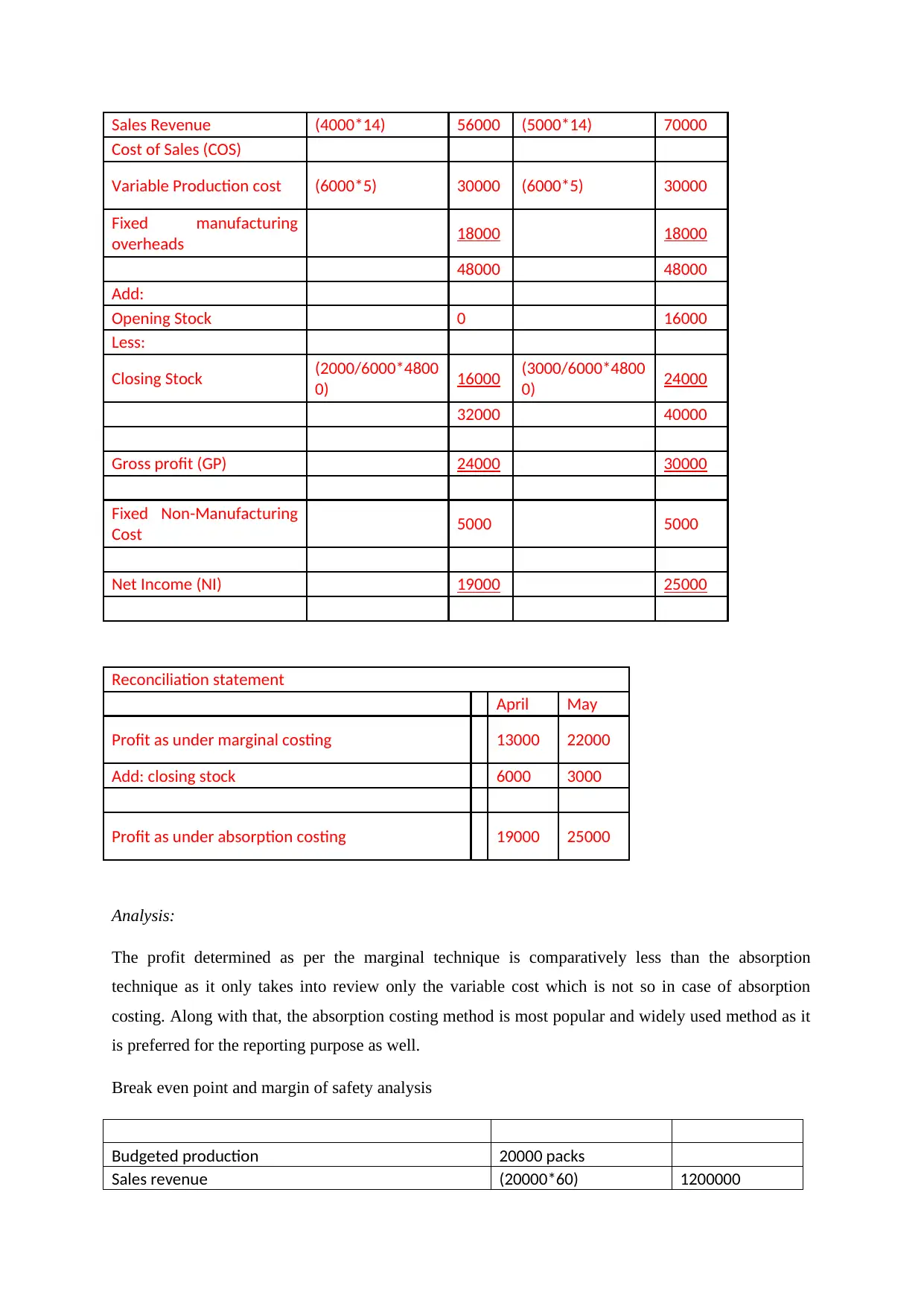

Income statement as per Marginal Costing

Particulars April May

Sales Revenue (4000*14) 5600

0 (5000*14) 7000

0

Marginal Cost of Sales

(MCOS)

Variable Production cost (6000*5) 3000

0 (6000*5) 3000

0

3000

0

3000

0

Add:

Opening Stock 0 (2000/6000*3000

0)

1000

0

Less:

Closing Stock (2000/6000*3000

0)

1000

0

(3000/6000*3000

0)

1500

0

2000

0

2500

0

Contribution 3600

0

4500

0

Fixed manufacturing

overheads

1800

0

1800

0

Fixed Non-Manufacturing

Cost 5000 5000

Net Income (NI) 1300

0

2200

0

Income statement as per Absorption Costing

Particulars Januar

y

Februar

y

beneficial in case of one product and overhead recovery rate is based upon the normal capacity.

Cost profit volume analysis

It is the extended part of the break even analysis. By breaking cost into fixed and variable,

this analysis provides a useful insight to the profitability associated with the product or service. It

helps in depicting how the variation in the cost and volume will have an impact over the operating and

net income of the organization.

Income statement as per Marginal Costing

Particulars April May

Sales Revenue (4000*14) 5600

0 (5000*14) 7000

0

Marginal Cost of Sales

(MCOS)

Variable Production cost (6000*5) 3000

0 (6000*5) 3000

0

3000

0

3000

0

Add:

Opening Stock 0 (2000/6000*3000

0)

1000

0

Less:

Closing Stock (2000/6000*3000

0)

1000

0

(3000/6000*3000

0)

1500

0

2000

0

2500

0

Contribution 3600

0

4500

0

Fixed manufacturing

overheads

1800

0

1800

0

Fixed Non-Manufacturing

Cost 5000 5000

Net Income (NI) 1300

0

2200

0

Income statement as per Absorption Costing

Particulars Januar

y

Februar

y

Sales Revenue (4000*14) 56000 (5000*14) 70000

Cost of Sales (COS)

Variable Production cost (6000*5) 30000 (6000*5) 30000

Fixed manufacturing

overheads 18000 18000

48000 48000

Add:

Opening Stock 0 16000

Less:

Closing Stock (2000/6000*4800

0) 16000 (3000/6000*4800

0) 24000

32000 40000

Gross profit (GP) 24000 30000

Fixed Non-Manufacturing

Cost 5000 5000

Net Income (NI) 19000 25000

Reconciliation statement

April May

Profit as under marginal costing 13000 22000

Add: closing stock 6000 3000

Profit as under absorption costing 19000 25000

Analysis:

The profit determined as per the marginal technique is comparatively less than the absorption

technique as it only takes into review only the variable cost which is not so in case of absorption

costing. Along with that, the absorption costing method is most popular and widely used method as it

is preferred for the reporting purpose as well.

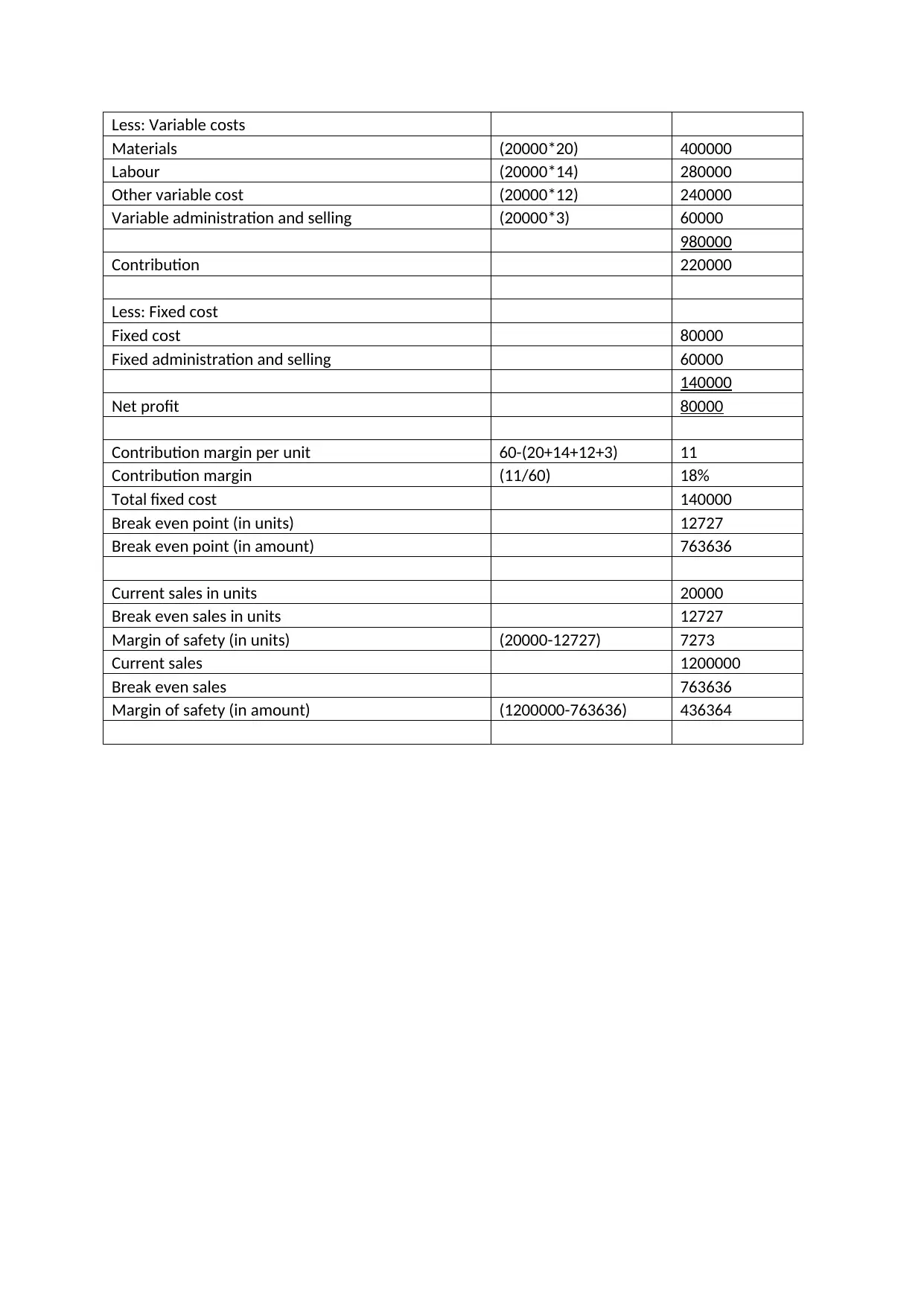

Break even point and margin of safety analysis

Budgeted production 20000 packs

Sales revenue (20000*60) 1200000

Cost of Sales (COS)

Variable Production cost (6000*5) 30000 (6000*5) 30000

Fixed manufacturing

overheads 18000 18000

48000 48000

Add:

Opening Stock 0 16000

Less:

Closing Stock (2000/6000*4800

0) 16000 (3000/6000*4800

0) 24000

32000 40000

Gross profit (GP) 24000 30000

Fixed Non-Manufacturing

Cost 5000 5000

Net Income (NI) 19000 25000

Reconciliation statement

April May

Profit as under marginal costing 13000 22000

Add: closing stock 6000 3000

Profit as under absorption costing 19000 25000

Analysis:

The profit determined as per the marginal technique is comparatively less than the absorption

technique as it only takes into review only the variable cost which is not so in case of absorption

costing. Along with that, the absorption costing method is most popular and widely used method as it

is preferred for the reporting purpose as well.

Break even point and margin of safety analysis

Budgeted production 20000 packs

Sales revenue (20000*60) 1200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Variable costs

Materials (20000*20) 400000

Labour (20000*14) 280000

Other variable cost (20000*12) 240000

Variable administration and selling (20000*3) 60000

980000

Contribution 220000

Less: Fixed cost

Fixed cost 80000

Fixed administration and selling 60000

140000

Net profit 80000

Contribution margin per unit 60-(20+14+12+3) 11

Contribution margin (11/60) 18%

Total fixed cost 140000

Break even point (in units) 12727

Break even point (in amount) 763636

Current sales in units 20000

Break even sales in units 12727

Margin of safety (in units) (20000-12727) 7273

Current sales 1200000

Break even sales 763636

Margin of safety (in amount) (1200000-763636) 436364

Materials (20000*20) 400000

Labour (20000*14) 280000

Other variable cost (20000*12) 240000

Variable administration and selling (20000*3) 60000

980000

Contribution 220000

Less: Fixed cost

Fixed cost 80000

Fixed administration and selling 60000

140000

Net profit 80000

Contribution margin per unit 60-(20+14+12+3) 11

Contribution margin (11/60) 18%

Total fixed cost 140000

Break even point (in units) 12727

Break even point (in amount) 763636

Current sales in units 20000

Break even sales in units 12727

Margin of safety (in units) (20000-12727) 7273

Current sales 1200000

Break even sales 763636

Margin of safety (in amount) (1200000-763636) 436364

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

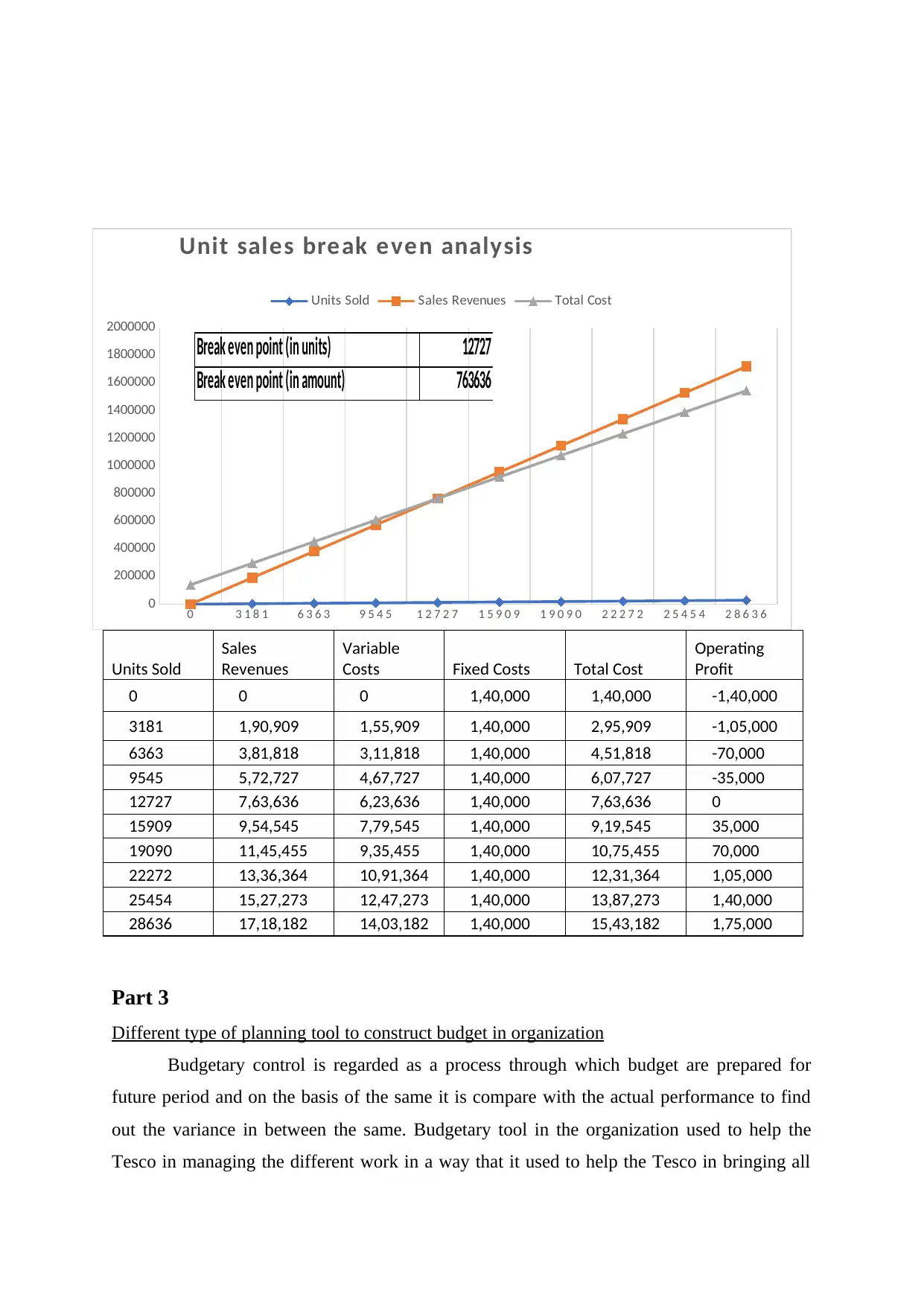

Units Sold

Sales

Revenues

Variable

Costs Fixed Costs Total Cost

Operating

Profit

0 0 0 1,40,000 1,40,000 -1,40,000

3181 1,90,909 1,55,909 1,40,000 2,95,909 -1,05,000

6363 3,81,818 3,11,818 1,40,000 4,51,818 -70,000

9545 5,72,727 4,67,727 1,40,000 6,07,727 -35,000

12727 7,63,636 6,23,636 1,40,000 7,63,636 0

15909 9,54,545 7,79,545 1,40,000 9,19,545 35,000

19090 11,45,455 9,35,455 1,40,000 10,75,455 70,000

22272 13,36,364 10,91,364 1,40,000 12,31,364 1,05,000

25454 15,27,273 12,47,273 1,40,000 13,87,273 1,40,000

28636 17,18,182 14,03,182 1,40,000 15,43,182 1,75,000

Part 3

Different type of planning tool to construct budget in organization

Budgetary control is regarded as a process through which budget are prepared for

future period and on the basis of the same it is compare with the actual performance to find

out the variance in between the same. Budgetary tool in the organization used to help the

Tesco in managing the different work in a way that it used to help the Tesco in bringing all

0 3 1 8 1 6 3 6 3 9 5 4 5 1 2 7 2 7 1 5 9 0 9 1 9 0 9 0 2 2 2 7 2 2 5 4 5 4 2 8 6 3 6

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

Unit sales break even analysis

Units Sold Sales Revenues Total Cost

Break even point (in units) 12727

Break even point (in amount) 763636

Sales

Revenues

Variable

Costs Fixed Costs Total Cost

Operating

Profit

0 0 0 1,40,000 1,40,000 -1,40,000

3181 1,90,909 1,55,909 1,40,000 2,95,909 -1,05,000

6363 3,81,818 3,11,818 1,40,000 4,51,818 -70,000

9545 5,72,727 4,67,727 1,40,000 6,07,727 -35,000

12727 7,63,636 6,23,636 1,40,000 7,63,636 0

15909 9,54,545 7,79,545 1,40,000 9,19,545 35,000

19090 11,45,455 9,35,455 1,40,000 10,75,455 70,000

22272 13,36,364 10,91,364 1,40,000 12,31,364 1,05,000

25454 15,27,273 12,47,273 1,40,000 13,87,273 1,40,000

28636 17,18,182 14,03,182 1,40,000 15,43,182 1,75,000

Part 3

Different type of planning tool to construct budget in organization

Budgetary control is regarded as a process through which budget are prepared for

future period and on the basis of the same it is compare with the actual performance to find

out the variance in between the same. Budgetary tool in the organization used to help the

Tesco in managing the different work in a way that it used to help the Tesco in bringing all

0 3 1 8 1 6 3 6 3 9 5 4 5 1 2 7 2 7 1 5 9 0 9 1 9 0 9 0 2 2 2 7 2 2 5 4 5 4 2 8 6 3 6

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

Unit sales break even analysis

Units Sold Sales Revenues Total Cost

Break even point (in units) 12727

Break even point (in amount) 763636

the work on correct path in the organization (Colares and et.al., 2019). Another relevance of

using different planning tool in the budgetary control is to optimize the usage of variety of

different resources in the market.

Flexible budget tool: Flexible budget is the type of the budget which generally flexes

with change in the volume of different activity. This sort of budgetary tool used to monitor

variety of different change and on the basis of same budget is constructed in the organization.

These sorts of tool ultimately assist in measuring the efficiency of manager performance.

Advantages

Flexible budget generally used to reflects current position or the financial status of

Tesco in market. Flexible budget in the organization also used to help the Tesco in

performance analysis at the workplace also. As flexibility to adapt the change help the

manager or owner to understand the performance of different individual in the market.

Disadvantage

This type of budget planning tool in the organization used to consume a good sort of

time for the organization to construct the budget. Any wrong understanding of change at the

time of planning a budget in the organization can create the issue of inaccuracy at the

workplace as well (Sponem and Lambert, 2016).

Incremental budgetary tool generally regarded as a budget which is generally

prepared on the basis of previous year budget of the organization. All the resources which are

generally allotted in the incremental budget are generally prepared on the basis of previous

period budget in the market. This type of budgetary tool is generally define as traditional

form of budgeting.

Advantage

It is one of the easiest budgeting approach as this type of budgeting tool used to

consume less amount of time to prepare the budget in the organization. As current budget is

prepared on the basis of previous year budget as no complex calculation are require in the

organization. Also it used to give the manager the option of having more secured information.

Disadvantage

Incremental budgetary in the organization can create the situation in which organization can

see unnecessary spending in the market. As all the spending are done on the previous year

using different planning tool in the budgetary control is to optimize the usage of variety of

different resources in the market.

Flexible budget tool: Flexible budget is the type of the budget which generally flexes

with change in the volume of different activity. This sort of budgetary tool used to monitor

variety of different change and on the basis of same budget is constructed in the organization.

These sorts of tool ultimately assist in measuring the efficiency of manager performance.

Advantages

Flexible budget generally used to reflects current position or the financial status of

Tesco in market. Flexible budget in the organization also used to help the Tesco in

performance analysis at the workplace also. As flexibility to adapt the change help the

manager or owner to understand the performance of different individual in the market.

Disadvantage

This type of budget planning tool in the organization used to consume a good sort of

time for the organization to construct the budget. Any wrong understanding of change at the

time of planning a budget in the organization can create the issue of inaccuracy at the

workplace as well (Sponem and Lambert, 2016).

Incremental budgetary tool generally regarded as a budget which is generally

prepared on the basis of previous year budget of the organization. All the resources which are

generally allotted in the incremental budget are generally prepared on the basis of previous

period budget in the market. This type of budgetary tool is generally define as traditional

form of budgeting.

Advantage

It is one of the easiest budgeting approach as this type of budgeting tool used to

consume less amount of time to prepare the budget in the organization. As current budget is

prepared on the basis of previous year budget as no complex calculation are require in the

organization. Also it used to give the manager the option of having more secured information.

Disadvantage

Incremental budgetary in the organization can create the situation in which organization can

see unnecessary spending in the market. As all the spending are done on the previous year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.